Dog Vaccines Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

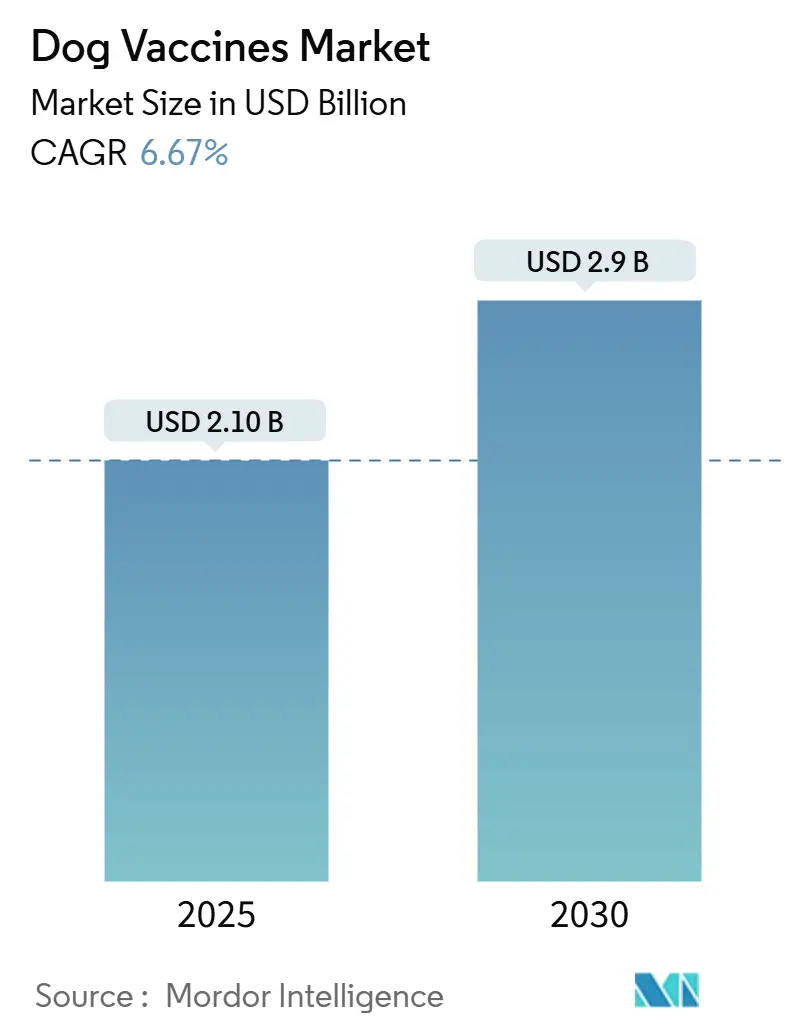

| Market Size (2025) | USD 2.10 Billion |

| Market Size (2030) | USD 2.9 Billion |

| Growth Rate (2025 - 2030) | 6.67% CAGR |

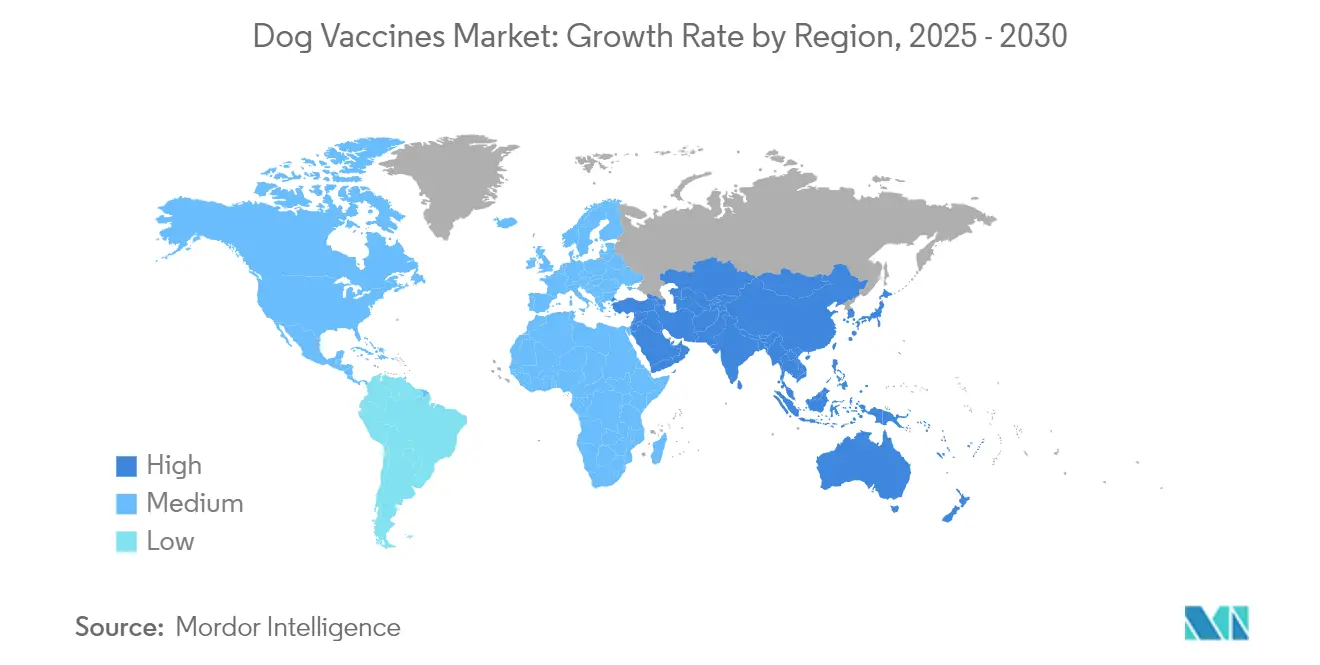

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dog Vaccines Market Analysis by Mordor Intelligence

The Dog Vaccines Market size is estimated at USD 2.10 billion in 2025, and is expected to reach USD 2.9 billion by 2030, at a CAGR of 6.67% during the forecast period (2025-2030).

Dog Vaccine Market Overview

The dog vaccine industry is experiencing significant transformation driven by evolving pet ownership patterns and increasing pet humanization trends. According to the 2024 American Pet Products Association (APPA) State of the Industry Report, 82 million United States households own a pet. This shift in pet ownership demographics is particularly pronounced among millennials, who account for 32% of pet owners and demonstrate unprecedented commitment to pet healthcare. A May 2023 study published by Women's Health United Kingdom revealed that nearly 63% of millennial pet owners are spending more on their dogs than on themselves, highlighting the growing prioritization of pet wellness and preventive care.

The global veterinary healthcare infrastructure has undergone substantial expansion to meet the rising demand for pet care services. In China alone, the number of veterinary clinics has reached approximately 28,000 as of 2023, reflecting the rapid development of pet healthcare facilities worldwide. This expansion has been accompanied by improvements in vaccine storage and distribution networks, enhanced clinical protocols, and standardization of vaccination schedules. Veterinary practices are increasingly adopting integrated healthcare management systems that enable better tracking of vaccination histories and more efficient reminder systems for booster shots.

Disease prevention and control initiatives have gained renewed focus, particularly in addressing zoonotic diseases. The economic burden of rabies alone is estimated at more than USD 583.5 million annually across Asia and Africa, driving increased emphasis on vaccination programs. International organizations and pharmaceutical companies are collaborating on mass vaccination campaigns, with particular attention to regions with high incidence rates of preventable diseases. These initiatives are complemented by educational programs aimed at raising awareness about the importance of regular vaccination schedules.

Technological advancements in vaccine development and delivery systems are reshaping the industry landscape. The emergence of novel vaccine formulations, including recombinant vaccines and improved delivery mechanisms, has enhanced vaccine efficacy and safety profiles. Manufacturers are investing in research and development to create multivalent vaccines that can protect against multiple diseases with a single administration. Additionally, the industry has witnessed significant progress in cold chain management and vaccine stability, enabling better preservation and distribution of vaccines across various geographical regions. These innovations have led to the development of more convenient administration methods, including oral vaccines, which are gaining popularity among pet owners and veterinarians alike.

Global Dog Vaccines Market Trends and Insights

Increasing Pet Adoption Rates

The rising trend of pet adoption, particularly dogs, has emerged as a significant driver for the vaccine market, supported by the growing phenomenon of pet humanization, where animals are increasingly treated as family members. According to the 2023 analysis by Shelter Animal Court 2023, approximately 2.2 million dogs were adopted in the United States in 2023, comprising 56% of the total intake, which indicates a strong demand for preventive healthcare measures, including vaccinations.

The pet humanization trend has fundamentally transformed the way pet owners approach veterinary care and preventive medicine. Pet owners are becoming increasingly educated about the importance of regular vaccinations and preventive healthcare, leading to higher compliance with recommended vaccination schedules. This shift in perspective has resulted in pet owners being more proactive about their pets' health, seeking comprehensive vaccination coverage beyond just the core vaccines. The trend is particularly notable among urban pet owners who have greater access to veterinary services and are more likely to invest in both core and non-core vaccines for their pets. This behavioral change has created a sustained demand for both traditional and advanced vaccine formulations, driving innovation in the vaccine development sector.

Advancements in Veterinary Medicine

Technological innovations in veterinary medicine have revolutionized vaccine development and delivery systems, significantly improving the efficacy and safety of dog vaccines. The development of bivalent viral vector-based vaccines targeting multiple diseases simultaneously, such as rabies and canine distemper, represents a major advancement in vaccination technology. These innovations have led to the creation of more sophisticated vaccine formulations, including recombinant vaccines that integrate pathogen genes with additional antigens for enhanced protection. For instance, the introduction of Nobivac Intra-Trac Oral BbPi in September 2022 marked a significant milestone as the first and only oral vaccine providing mucosal protection against both Bordetella bronchiseptica and canine parainfluenza virus, demonstrating the industry's capability to develop more convenient and effective vaccination solutions.

The advancement in vaccine delivery systems has also played a crucial role in improving vaccination compliance and effectiveness. The emergence of oral vaccines has addressed the challenges associated with traditional injectable formulations, making vaccination more convenient for both pet owners and veterinarians. This is exemplified by the August 2024 launch of Canigen Bb, an injectable Bordetella bronchiseptica vaccine for dogs, by Virbac to reduce clinical signs of upper respiratory tract disease and reduce bacterial shedding post-infection. Administered via subcutaneous injection, Canigen Bb is an inactivated subunit vaccine that offers vets a new option when intra-nasal vaccination with a live aerosolized vaccine is not possible or preferred.

Furthermore, the industry has witnessed significant progress in the development of small interfering RNA (siRNA) vaccines and bi-specific antibody (BsAb)-based therapies for rabies, opening new possibilities in therapeutic vaccination approaches. These technological advancements are complemented by stringent regulatory frameworks, with organizations like the European Medicines Agency (EMA) and the Veterinary Medicines Directorate (VMD) ensuring that new vaccine developments meet high standards of safety and efficacy.

Dog Vaccines Market Vaccine Type Segment Analysis

Modified/Attenuated Live Vaccines Segment in Dog Vaccines Market

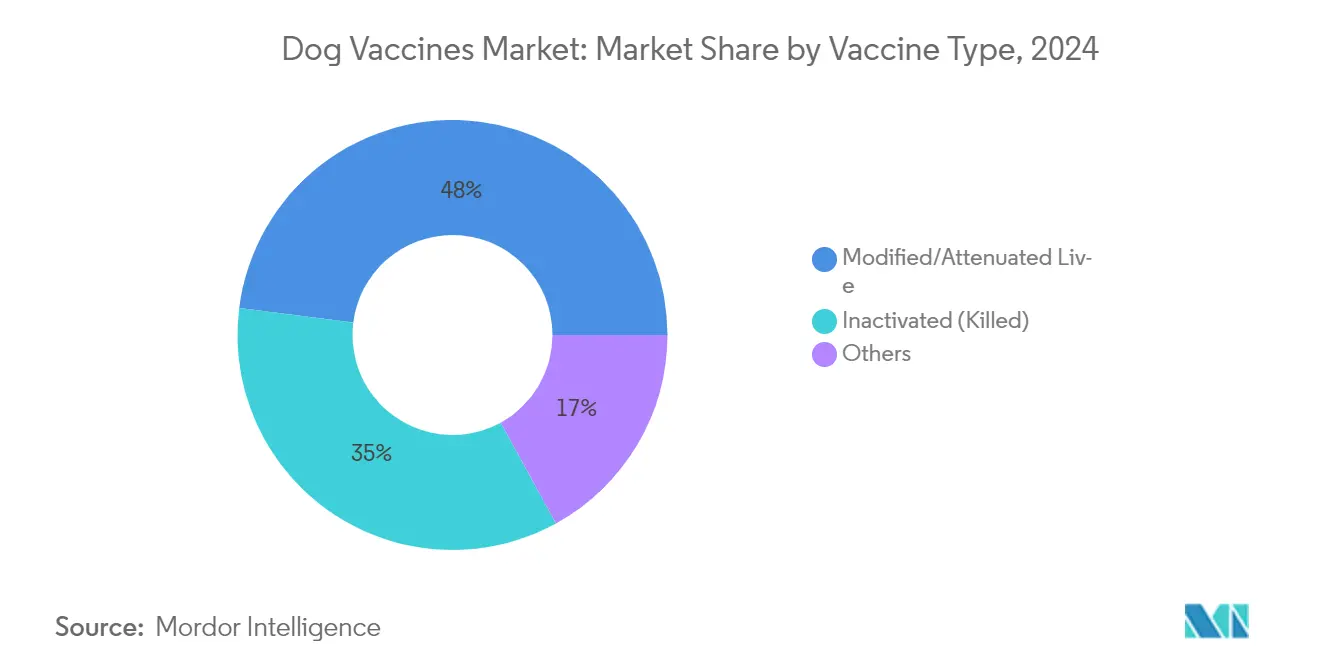

The modified/attenuated live vaccines segment has emerged as the dominant force in the global dog vaccines market, commanding an estimated 48% market share in 2024. This substantial market position is primarily attributed to these vaccines' superior ability to stimulate both humoral and cell-mediated immune responses, closely mimicking natural infection without causing disease. The segment's leadership is further strengthened by its cost-effectiveness in manufacturing and the longer-lasting immunity it provides compared to other vaccine types. Veterinarians worldwide show a strong preference for modified live vaccines, particularly for core vaccinations such as distemper and parvovirus, due to their proven track record of efficacy. The segment's dominance is also supported by extensive research backing their safety profile and the availability of combination vaccines that reduce the number of required shots.

Inactivated Vaccines Segment in Dog Vaccines Market

The inactivated vaccines segment is projected to exhibit a significant growth rate in the dog vaccines market during the forecast period 2025-2030. This accelerated growth is driven by increasing safety concerns among pet owners and veterinarians, particularly for immunocompromised dogs where modified live vaccines might pose risks. The segment's expansion is further fueled by technological advancements in vaccine production methods, improving the stability and efficacy of killed vaccines. Growing awareness about the benefits of inactivated vaccines, such as their inability to revert to virulence and longer shelf life, is contributing to their increasing adoption. The segment is also benefiting from substantial investments in research and development, leading to enhanced adjuvant technologies that improve immune response profiles.

Other Vaccine Type Segment in Dog Vaccines Market

The other vaccine type segment in the dog vaccines market, including recombinant vaccines, toxoid vaccines, and subunit vaccines, play a crucial role in providing diverse immunization options for specific canine health needs. These segments are witnessing increased attention from researchers and pharmaceutical companies due to their potential for enhanced safety profiles and targeted immune responses. The development of novel vaccine technologies, including DNA and RNA vaccines and vector-based vaccines, is expanding the possibilities within these segments. Market dynamics are being influenced by the growing demand for more specific and tailored vaccination approaches, particularly for dogs with special health conditions. These segments are also benefiting from increased investment in biotechnology and the emergence of personalized veterinary medicine approaches. The adoption of these alternative vaccine types is particularly notable in developed markets where pet owners are more willing to invest in advanced vaccination options.

Dog Vaccines Market Disease Type Segment Analysis

Canine Rabies Segment in Dog Vaccines Market

The canine rabies segment has emerged as a significant force in the dog vaccines market, commanding approximately 28% of the market share in 2024. This leadership position is primarily attributed to stringent vaccination regulations across multiple jurisdictions and the fatal nature of the disease. The segment's prominence is further reinforced by widespread public health campaigns and mandatory vaccination requirements for pet licensing and international travel. Municipal regulations requiring proof of rabies vaccination for dog registration have significantly contributed to the segment's market dominance. The segment's strength is also supported by established distribution networks and the availability of both single-dose and combination vaccines incorporating rabies protection. Healthcare providers' emphasis on rabies prevention as a core vaccination requirement has maintained consistent demand throughout various geographical regions. Additionally, increasing pet ownership rates and growing awareness about zoonotic diseases have further solidified the segment's market leadership.

Canine Lyme Disease Segment in Dog Vaccines Market

The canine lyme disease segment is projected to exhibit a significant growth rate in the dog vaccines market. This accelerated growth is primarily driven by the expanding geographical distribution of tick populations due to climate change and environmental factors. The segment's rapid expansion is further fueled by increasing awareness among pet owners about the serious complications associated with Lyme disease in dogs. Veterinary professionals are increasingly recommending Lyme disease vaccination in previously low-risk areas, contributing to market expansion. Advanced diagnostic capabilities and improved surveillance systems have led to better disease detection rates, subsequently driving vaccine demand. The development of more effective vaccine formulations and enhanced delivery systems has also contributed to the segment's growth trajectory. Moreover, the rising adoption of outdoor activities with pets and the expansion of suburban areas into tick-inhabited regions have created additional growth opportunities for this segment.

Other Disease Type Segment in Dog Vaccines Market

The other disease segments, including canine distemper, CIRDC, parvovirus, leptospirosis, and infectious canine hepatitis, continue to play vital roles in the overall market dynamics. The CIRDC segment has gained significant traction due to the increasing popularity of dog daycare facilities and boarding services. Parvovirus vaccines maintain steady demand as essential components of core vaccination protocols, particularly for puppies and young dogs. The leptospirosis segment shows notable regional variations, with higher adoption rates in areas with increased exposure risk. Canine distemper vaccines remain fundamental to core vaccination schedules, supported by veterinary guidelines worldwide. The infectious canine hepatitis segment, while smaller, maintains consistent demand due to its inclusion in combination vaccines. These segments collectively demonstrate varying growth patterns influenced by factors such as regional disease prevalence, veterinary recommendations, and evolving pet care practices. The development of new combination vaccines incorporating multiple disease protections has also influenced the market dynamics of these segments.

Dog Vaccines Market Route of Administration Segment Analysis

Injectable Segment in Dog Vaccines Market

The injectable segment maintains its dominant position in the dog vaccines market, commanding the highest market share in 2024. This substantial market presence is primarily attributed to the proven efficacy and reliability of injectable vaccines in providing immune protection against various canine diseases. Healthcare professionals consistently prefer injectable vaccines due to their precise dosage control and established safety protocols. The segment's strength is further reinforced by the extensive availability of injectable vaccines across veterinary clinics, hospitals, and specialized pet care facilities. Additionally, the robust distribution network and cold chain infrastructure specifically designed for injectable vaccines contribute to their market leadership. The segment's performance is also supported by comprehensive healthcare provider training and familiarity with injectable administration techniques, ensuring consistent and reliable vaccine delivery.

Oral Vaccines Segment in Dog Vaccines Market

The oral vaccines segment is emerging as the fastest-growing segment in the dog vaccines market and is projected to expand significantly from 2025 to 2030. This remarkable growth trajectory is driven by increasing pet owner preference for stress-free vaccination methods and technological advancements in oral delivery systems. The segment's expansion is further accelerated by the development of new formulations that enhance vaccine stability and effectiveness when administered orally. Pet owners' growing awareness of alternative vaccination methods and the reduced anxiety experienced by dogs during oral administration contribute to the segment's rapid growth. The convenience factor associated with oral vaccines, particularly for at-home administration, is attracting both veterinary professionals and pet owners. Additionally, ongoing research and development initiatives focusing on improving oral vaccine bioavailability and immune response are expected to further propel this segment's growth.

Dog Vaccines Market Distribution Channel Segment Analysis

Hospital/Clinic Pharmacies Segment in Dog Vaccines Market

The hospital/clinic pharmacies segment dominated the dog vaccines market in 2024, commanding approximately 47% of the total market share. This substantial market position is primarily attributed to the critical role veterinary professionals play in vaccine administration and the stringent storage requirements for vaccine products. The segment's dominance is further strengthened by the established trust between pet owners and veterinary professionals, who provide expert guidance on vaccination schedules and proper administration techniques. Hospital and clinic pharmacies also benefit from their ability to maintain proper cold chain management, ensuring vaccine efficacy and safety. The segment's strong performance is additionally supported by the immediate availability of vaccines during veterinary visits, integration with comprehensive pet healthcare services, and the ability to handle emergency vaccination needs effectively. Moreover, the presence of trained staff capable of addressing adverse reactions and providing proper documentation has reinforced this segment's market leadership position.

E-commerce Segment in Dog Vaccines Market

The e-commerce segment is emerging as the fastest-growing distribution channel in the dog vaccines market and is projected to expand at a CAGR of 8% from 2025 to 2030. This remarkable growth trajectory is driven by increasing digital adoption among pet owners and the convenience of online purchasing platforms. The segment's expansion is further accelerated by the development of sophisticated cold chain logistics solutions specifically designed for vaccine delivery. E-commerce platforms are increasingly partnering with licensed veterinary suppliers to ensure product authenticity and proper handling during transit. The growth is also supported by the rising number of tech-savvy pet owners who prefer the convenience of home delivery and the ability to compare prices across multiple vendors. Additionally, the integration of telemedicine services with online pharmacies has created a more comprehensive pet healthcare ecosystem, contributing to the segment's rapid growth. The expansion of e-commerce is particularly notable in urban areas where digital literacy and internet penetration are high.

Dog Vaccines Market Geography Segment Analysis

Dog Vaccines Market in North America

North America represents a dominant force in the global dog vaccines market, driven by high pet ownership rates and advanced veterinary healthcare infrastructure. The region benefits from widespread awareness about preventive pet healthcare and the strong presence of major market players. The United States and Canada form the key markets in North America, with both countries demonstrating robust demand for canine vaccines. The region's growth is supported by sophisticated distribution networks, well-established veterinary clinics, and increasing pet insurance penetration.

Dog Vaccines Market in the United States

The United States leads the North American market, holding approximately 38% share of the global market in 2024. The country's dominance is attributed to its large pet dog population. The presence of major vaccine manufacturers, an extensive veterinary network, and a strong regulatory framework further strengthen the market. Advanced research facilities and continuous product innovations by domestic players contribute to market growth. The country also benefits from high consumer spending on pet healthcare and the growing adoption of premium vaccine products.

Dog Vaccines Market in Canada

Canada emerges as the fastest-growing market in North America, projected to grow at approximately 6.5% CAGR from 2025-2030. The growth is driven by increasing pet adoption rates and rising awareness about preventive healthcare for pets. Canadian pet owners are increasingly investing in comprehensive vaccination programs for their dogs. The country's robust veterinary infrastructure and government support for animal health initiatives create favorable conditions for market expansion. Additionally, the growing trend of pet insurance coverage and rising disposable income contribute to increased spending on pet vaccines.

Dog Vaccines Market in Europe

Europe maintains a strong position in the global dog vaccines market, characterized by stringent regulations and high standards of pet healthcare. The region's market is well-developed across key countries, including Germany, the United Kingdom, France, Italy, and Spain. The European Medicines Agency's initiatives to enhance the accessibility of animal vaccines have significantly influenced market growth. The region benefits from advanced veterinary infrastructure and high awareness about pet vaccination schedules among pet owners.

Dog Vaccines Market in Germany

Germany stands as the largest market in Europe, commanding approximately 25% of the regional market share in 2024. The country's leadership position is supported by its well-established veterinary healthcare system and strict regulations mandating pet vaccinations. German pet owners demonstrate high compliance with vaccination schedules, particularly for core vaccines. The presence of major vaccine manufacturers and research facilities further strengthens the country's position in the market.

Dog Vaccines Market in the United Kingdom

The United Kingdom (UK) emerges as the fastest-growing market in Europe, with an expected growth rate of approximately 7% from 2025-2030. The growth is driven by increasing pet ownership and rising awareness about preventive healthcare for pets. The UK market benefits from advanced veterinary services and strong distribution networks. The country's pet insurance penetration rate and growing trend of pet humanization contribute significantly to market expansion. Additionally, innovative vaccine developments and strategic initiatives by market players fuel growth.

Dog Vaccines Market in Asia-Pacific

The Asia Pacific region represents a rapidly evolving market for dog vaccines, characterized by increasing pet ownership and rising disposable incomes. Key markets include China, India, Japan, South Korea, and Australia, each contributing uniquely to regional growth. The region demonstrates significant potential due to its large pet population and growing awareness about pet healthcare. Improving veterinary infrastructure and increasing investments in animal healthcare further drive market expansion.

Dog Vaccines Market in China

China leads the Asia Pacific market with its extensive network of veterinary clinics and growing pet ownership. The country's market benefits from rapid urbanization and increasing disposable income levels. The presence of numerous veterinary facilities and growing awareness about pet vaccination contribute to market growth. Government initiatives supporting animal health and increasing investments in veterinary infrastructure further strengthen China's position.

Dog Vaccines Market in India

India emerges as the fastest-growing market in the Asia-Pacific region. The growth is primarily driven by rapid urbanization and changing lifestyles. The country's market benefits from rising pet adoption rates and increasing consciousness about preventive pet healthcare. Growing disposable incomes and expanding veterinary infrastructure support market growth. The government's initiatives to control zoonotic diseases and increasing investments in animal healthcare contribute to market expansion.

Dog Vaccines Market in the Middle East and Africa

The Middle East and Africa region shows promising growth potential in the dog vaccines market, with South Africa and GCC countries, including UAE and Saudi Arabia, as key markets. The region's growth is driven by increasing urbanization, rising pet ownership, and growing awareness about animal healthcare. Saudi Arabia represents the largest market in the region, while the UAE demonstrates the fastest growth potential. The region benefits from improving veterinary infrastructure and increasing investments in animal healthcare. Government initiatives to control zoonotic diseases and rising pet healthcare awareness contribute to market expansion.

Dog Vaccines Market in South America

South America demonstrates significant potential in the dog vaccines market, with Brazil and Argentina as key contributing countries. The region's market is characterized by increasing pet ownership and growing awareness about pet healthcare. Brazil emerges as both the largest and fastest-growing market in the region, driven by its large pet population and increasing adoption of advanced vaccines. The region benefits from improving veterinary infrastructure and rising investments in animal healthcare facilities. The growing middle-class population and increasing pet healthcare expenditure further contribute to market growth.

Competitive Landscape

Top Companies in the Dog Vaccines Market

The leading companies in the global dog vaccines market include Zoetis Inc., Boehringer Ingelheim International GmbH, Merck & Co. Inc., Elanco, Virbac, Bioveta a.s, Hester Biosciences Limited, Brilliant Bio Pharma, Heska Corporation, and HIPRA S.A.. These market leaders demonstrate a consistent focus on product innovation through significant R&D investments in developing novel vaccine formulations and delivery systems. The industry witnesses regular strategic collaborations between pharmaceutical companies and research institutions to enhance vaccine efficacy and duration of immunity. Companies are expanding their geographical presence through distribution partnerships and regional manufacturing facilities while simultaneously working on operational improvements through automation and supply chain optimization. The competitive landscape is characterized by continuous efforts to develop combination vaccines that can protect against multiple diseases with fewer doses, alongside initiatives to make vaccine administration more convenient through innovations in delivery methods like oral and intranasal formulations.

Market Structure Shows Balanced Competition Dynamics

The dog vaccines market exhibits a balanced mix of global pharmaceutical conglomerates and specialized veterinary medicine companies. The major multinational players leverage their extensive research capabilities and global distribution networks to maintain market leadership, while regional specialists focus on addressing local disease patterns and regulatory requirements. The market demonstrates moderate consolidation, with the top players holding significant market share while leaving room for specialized players to serve niche segments. The industry structure supports both the large-scale production of core vaccines and the specialized development of region-specific formulations.

The market has witnessed strategic mergers and acquisitions aimed at expanding product portfolios and geographical reach. Companies are increasingly focusing on vertical integration to control quality and optimize costs throughout the value chain. Partnership agreements between manufacturers and veterinary clinic networks have become common, creating stable distribution channels. Regional players are strengthening their position through collaborations with global companies, combining local market knowledge with advanced technological capabilities.

Innovation and Accessibility Drive Future Success

For established players to maintain and expand their market position, the focus needs to be placed on developing next-generation vaccines with improved efficacy and longer duration of immunity. Companies must invest in novel delivery systems that simplify administration and improve compliance. Success will depend on building strong relationships with veterinary professionals and pet owners through educational initiatives and support programs. Market leaders need to balance premium positioning with accessibility to capture growth in emerging markets while maintaining profitability in mature markets.

New entrants and challenger companies can gain market share by focusing on underserved geographical regions or specific disease segments. Success factors include developing cost-effective manufacturing processes, establishing reliable distribution networks, and building trust with veterinary professionals. Companies must navigate complex regulatory requirements while maintaining flexibility to respond to emerging disease threats. The increasing focus on pet healthcare and preventive medicine creates opportunities for innovative players to introduce new vaccine technologies and delivery methods. Future success will depend on the ability to balance innovation with affordability while meeting stringent quality and safety standards.

Dog Vaccines Industry Leaders

Boehringer Ingelheim International GmbH

Merck & Co., Inc.

Virbac

Elanco

Zoetis Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Calviri, a biotechnology company that creates therapeutic and preventative cancer vaccines for dogs, announced the vaccination of its first participant dog with its investigational immunotherapy vaccine. The new vaccine trial for canines with early-stage hemangiosarcoma (HSA) was underway and aims to explore whether the company’s “pre-made” vaccine can lengthen the lifespan of dogs with stage 1 or stage 2 tumors when paired with standard care treatment like surgery and chemotherapy.

- October 2024: Chile launched a canine vaccine developed by the University of Chile's veterinary sciences division. The vaccine is described as one of the first of its kind, sterilizing dogs for a year. The injection prevents sexual behaviors and reproduction, offering an alternative to irreversible surgical castration. The vaccine can be used for both males and females and costs about CLP 50,000 (USD 54). It requires a veterinarian's prescription and evaluation to ensure the dog is a suitable candidate.

- June 2024: Merck & Co., Inc. introduced the NOBIVAC NXT Rabies portfolio in Canada, which includes NOBIVAC NXT Canine-3 Rabies, as part of the company's continued commitment to rabies prevention.

- March 2024: Zendal Group introduced Margarita Salas Biological Research Centre (CIB-CSIC)-developed vaccine against canine leishmaniasis, a recombinant vaccine to combat canine leishmaniasis, a parasite that causes skin ulcers to severe inflammation of the liver and spleen.

Global Dog Vaccines Market Report Scope

As per the scope of the report, dog vaccines are medical preparations that help protect dogs from infectious diseases by stimulating their immune system to recognize and fight specific pathogens.

The dog vaccines market is segmented into vaccine type, disease type, route of administration, distribution channel, and geography. By vaccine type, the market is segmented into modified/attenuated live, inactivated (killed), and others. By disease type, the market is segmented into canine distemper, canine infectious respiratory disease complex (cirdc), canine parvovirus, canine leptospirosis, canine lyme disease, infectious canine hepatitis, canine rabies, and others. By route of administration, the market is segmented into injectables, oral vaccines, and intranasal. By distribution channel, the market is segmented into hospital/clinic pharmacies, retail pharmacies, and e-commerce. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The report also offers the market size and forecasts for 17 countries across the region. For each segment, the market sizing and forecasts were made on the basis of value (USD).

| Modified/Attenuated Live |

| Inactivated (Killed) |

| Others |

| Canine Distemper |

| Canine Infectious Respiratory Disease Complex (CIRDC) |

| Canine Parvovirus |

| Canine Leptospirosis |

| Canine Lyme Disease |

| Infectious Canine Hepatitis |

| Canine Rabies |

| Others |

| Injectables |

| Oral Vaccines |

| Intranasal |

| Hospital/Clinic Pharmacies |

| Retail Pharmacies |

| E-commerce |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Vaccine Type | Modified/Attenuated Live | |

| Inactivated (Killed) | ||

| Others | ||

| By Disease Type | Canine Distemper | |

| Canine Infectious Respiratory Disease Complex (CIRDC) | ||

| Canine Parvovirus | ||

| Canine Leptospirosis | ||

| Canine Lyme Disease | ||

| Infectious Canine Hepatitis | ||

| Canine Rabies | ||

| Others | ||

| By Route of Administration | Injectables | |

| Oral Vaccines | ||

| Intranasal | ||

| By Distribution Channel | Hospital/Clinic Pharmacies | |

| Retail Pharmacies | ||

| E-commerce | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Dog Vaccines Market?

The Dog Vaccines Market size is expected to reach USD 2.10 billion in 2025 and grow at a CAGR of 6.67% to reach USD 2.9 billion by 2030.

What is the current Dog Vaccines Market size?

In 2025, the Dog Vaccines Market size is expected to reach USD 2.10 billion.

Which is the fastest growing region in Dog Vaccines Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Dog Vaccines Market?

In 2025, the North America accounts for the largest market share in Dog Vaccines Market.

What years does this Dog Vaccines Market cover, and what was the market size in 2024?

In 2024, the Dog Vaccines Market size was estimated at USD 1.96 billion. The report covers the Dog Vaccines Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Dog Vaccines Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: