Canine Vaccine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.27 Billion |

| Market Size (2031) | USD 3.06 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

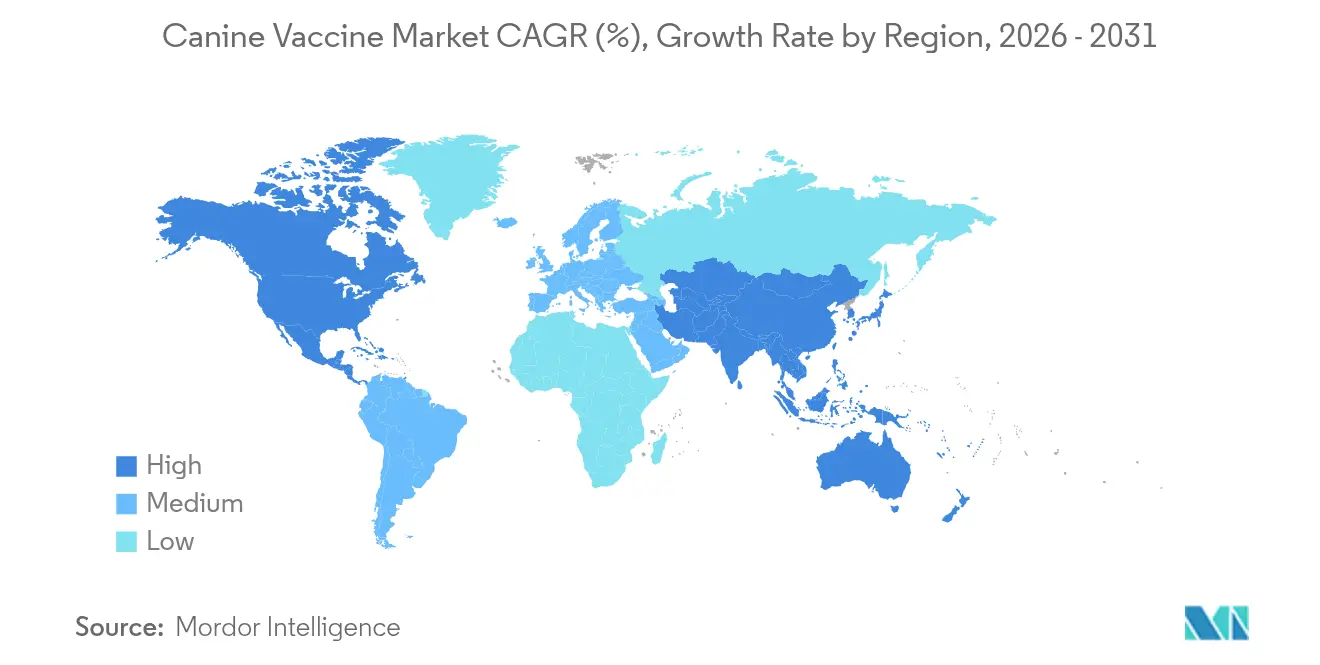

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canine Vaccine Market Analysis by Mordor Intelligence

The canine vaccine market size is expected to grow from USD 2.14 billion in 2025 to USD 2.27 billion in 2026 and is forecast to reach USD 3.06 billion by 2031 at 6.18% CAGR over 2026-2031. Robust growth persists even as 52% of United States pet owners delayed or declined veterinary visits for budget reasons, underscoring the sector’s resilience. DNA platforms are lifting overall momentum because their improved safety and broad immune activation drive the fastest 7.75% CAGR among vaccine technologies. Regional prospects diverge; Asia-Pacific leads with a projected 7.59% CAGR, while North America preserves leadership on the strength of its mature veterinary infrastructure and a 39.79% revenue share in 2024. Product innovation cycles are shortening as incumbents buy niche developers, illustrated by Boehringer Ingelheim acquiring Saiba Animal Health to expand into therapeutic vaccines. Heightened urban dog ownership in China, where the pet medical market is estimated at USD 30 billion and growing 17.7% annually, also lifts demand for premium multivalent shots.

Key Report Takeaways

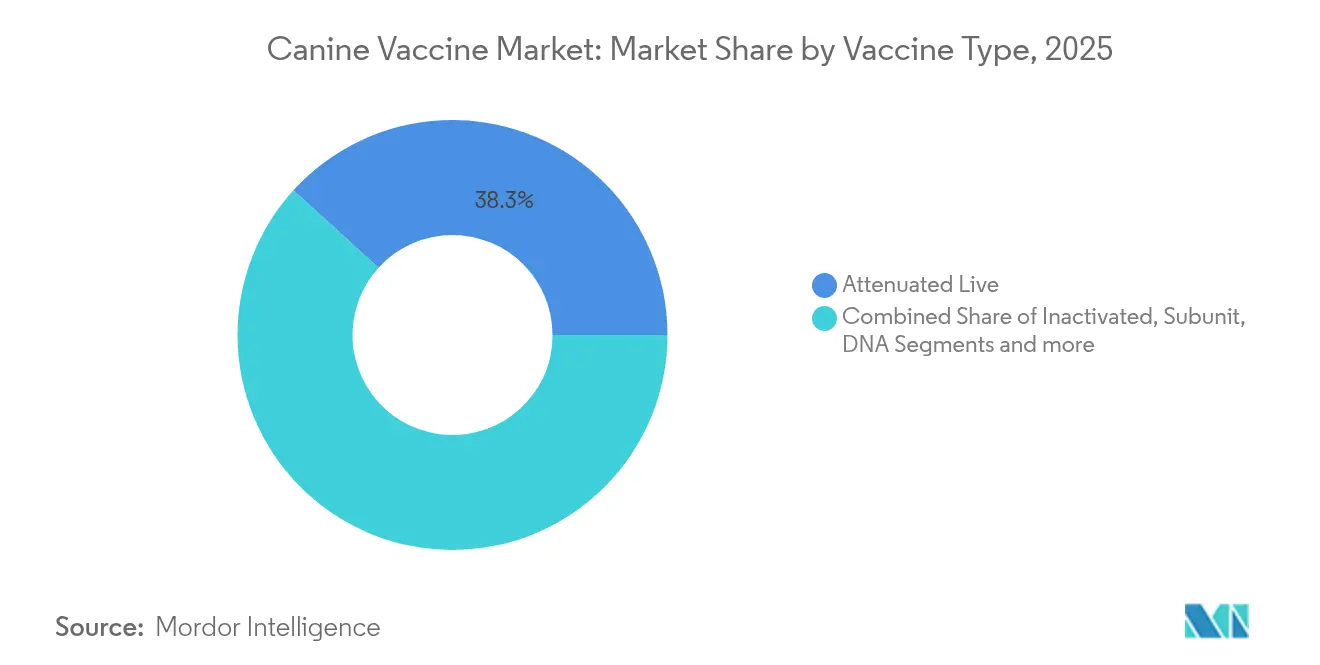

- By vaccine type, attenuated live formulations led with a 38.25% canine vaccine market share in 2025, while DNA vaccines are poised for the highest 7.35% CAGR to 2031.

- By valence, multivalent products captured 65.41% revenue share in 2025 and are projected to rise at a 7.10% CAGR through 2031.

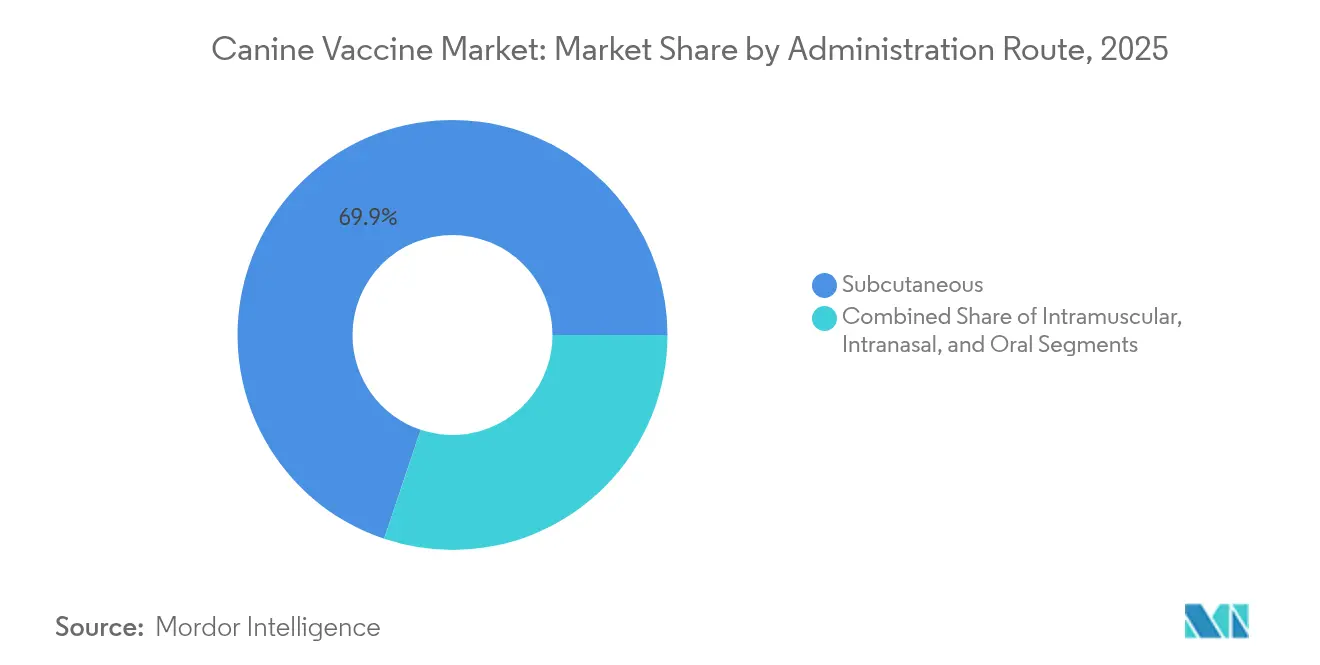

- By administration route, the subcutaneous segment held 69.85% of the canine vaccine market size in 2025; intranasal delivery is expanding at a 7.22% CAGR to 2031.

- By indication, rabies vaccines accounted for 28.60% of the canine vaccine market size in 2025, whereas Bordetella vaccines are set for the fastest 7.28% CAGR toward 2031.

- By geography, North America commanded 39.30% revenue in 2025, and Asia-Pacific is advancing at a 7.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Canine Vaccine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in adoption of dogs | +1.2% | Global, strongest in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Increased incidence of zoonotic diseases | +0.9% | Global, particularly emerging markets with limited veterinary infrastructure | Long term (≥ 4 years) |

| Advances in recombinant and vector vaccines | +1.1% | North America and EU leading, with technology transfer to APAC | Long term (≥ 4 years) |

| Rising preventive-care spend by pet owners | +0.8% | North America and EU core markets | Medium term (2-4 years) |

| Shift to 3-year DOI labeling and premium combos | +0.7% | North America and EU regulatory domains | Short term (≤ 2 years) |

| Tele-veterinary e-prescription platforms | +0.5% | North America leading, expanding to urban APAC centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise in Adoption of Dogs

Dog ownership keeps expanding as single-person households and older residents adopt pets for companionship. The American Veterinary Medical Association notes that canine patients account for 81% of clinic income, yet new puppy visits fell 9% year over year, signalling maturity in developed markets. Conversely, China’s high-growth pet sector and similar urbanization in Latin America sustain double-digit expansion. Older dogs need more frequent care, supporting premium combination vaccines that offer extended protection intervals. The human–animal bond, strengthened by pandemic lifestyle shifts, maintains compliance rates even when discretionary spending tightens. These dynamics collectively lift the canine vaccine market by widening both the client base and spend per visit.

Increased Incidence of Zoonotic Diseases

The World Health Organization’s Zero by 30 strategy requires a 70% vaccination threshold in dogs to eliminate human rabies deaths [1]World Health Organization, “Zero by 30: Global Strategic Plan for Rabies Elimination,” who.int . Climate change widens tick habitats, with studies finding 11.08% Ehrlichia prevalence in Chinese dogs, revealing gaps in current protection [2]Haiyue Zu, "Prevalence of Ehrlichia spp. in dogs and ticks in Hainan Province, China," BMC Veterinary Research, bmcvetres.biomedcentral.com. As a result, veterinary vaccines are now framed as public-health tools under the One Health banner. Emerging pathogens make rapid-response DNA and mRNA platforms attractive because they compress development timelines. Annual zoonotic outbreaks already impose treatment costs exceeding USD 100 billion, reinforcing public and private willingness to fund preventive programs.

Advances in Recombinant & Vector Vaccines

Regulators back next-generation technologies. The European Medicines Agency has published detailed guidance on plasmid DNA vaccines, trimming approval times [3]European Medicines Agency, "Guideline on plasmid DNA vaccines for veterinary use," ema.europa.eu. Merck’s NOBIVAC NXT Canine Flu H3N2, based on RNA-particle science, shows how leaders commercialize these advances. Recombinant products avoid reversion risks common to live viruses and support multivalent combinations without antigen interference. Production lines benefit from greater stability and reduced cold-chain dependence, giving manufacturers flexibility in emerging markets where logistics remain challenging. All these factors underpin the momentum behind DNA and vector solutions in the canine vaccine market.

Rising Preventive-Care Spend by Pet Owners

Pet healthcare outlays grew 9% annually between 2018 and 2024 despite macroeconomic volatility. Owners increasingly treat vaccination as a hedge against high treatment bills rather than a regulatory chore. Zoetis’ Simparica Trio surpassed USD 1 billion in global revenue by offering broad parasite and disease control in a single product. Virus-like particle research targeting chronic canine diseases broadens the revenue mix beyond traditional core vaccines. Premium pricing accepted by dedicated owners funds accelerated R&D pipelines and supports differentiated offerings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory complexity and high R&D cost | -0.8% | Global, highest impact in emerging markets | Long term (≥ 4 years) |

| Stringent cold-chain and GMP compliance | -0.6% | Global, particularly affecting smaller manufacturers | Medium term (2-4 years) |

| Anti-vaccination sentiment in pet owners | -1.1% | North America and EU primarily, spreading to urban APAC | Medium term (2-4 years) |

| Industry consolidation curbing innovation | -0.4% | Global, strongest impact in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Complexity & High R&D Cost

Approval times in ASEAN can stretch to four years, delaying commercial payback for small developers. Chinese filings also last up to four years and must meet Good Clinical Practice standards, adding cash strain. Since 2020, vaccine development costs climbed 40% due to stricter safety testing and advanced manufacturing needs. EU Good Distribution Practice rules demand continuous temperature logging that increases transport expenses for firms without global supply chains. These obstacles cement advantages for well-capitalized incumbents and limit fresh competition in the canine vaccine market.

Anti-Vaccination Sentiment in Pet Owners

A 2024 survey found 37% of dog owners questioned vaccine safety and 30% considered shots unnecessary, mirroring human debates. Puppy vaccination coverage in the United Kingdom fell from 88% in 2016 to 72% in 2019, eroding herd immunity for diseases such as parvovirus. Clinics report rising pushback on non-core boosters, with cost cited but safety fears underlying refusals. Social media misinformation sustains hesitancy and reduces confidence in veterinary advice. Lower uptake heightens outbreak risks that can depress revenue and trigger stricter regulation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vaccine Type: DNA Platforms Drive Innovation

Attenuated live vaccines held 38.25% of the canine vaccine market in 2025 on the strength of long-standing efficacy and low dosing schedules. DNA alternatives are advancing at a 7.35% CAGR and are expected to narrow the gap by 2031 as regulatory clarity improves and owners favor cutting-edge safety. Recombinant constructs avoid reversion risks, which reassures the 37% of hesitant owners. Inactivated products continue to serve immunocompromised animals, while subunit formats provide targeted antigen delivery for niche prophylaxis. Multivalent viral-vector solutions further enhance convenience. Collectively, these trends diversify the product mix and extend the canine vaccine market reach across varied risk profiles.

Manufacturers capitalize on streamlined plasmid guidelines from European authorities that shorten dossier review cycles. The recombinant category also benefits from simplified storage compared with live viruses, reducing wastage in developing economies. As capital flows shift toward next-generation science, R&D pipelines tilt to DNA and mRNA. This evolution underpins forecast premium pricing and enlarges the potential canine vaccine market size for innovative entrants.

By Valence Type: Multivalent Dominance Reflects Convenience

Multivalent products captured 65.41% revenue in 2025 because they protect against several pathogens with one injection, easing compliance in busy clinics and among cost-conscious owners. They also post the fastest 7.10% CAGR through 2031 as practitioners increasingly adopt three-year duration labels that align with owner preferences. Monovalent shots maintain relevance where focused immunity is needed, for example post-exposure rabies programs. Compatibility work shows rabies can be delivered alongside multivalent combos without antibody interference.

Premium blends command higher average selling prices and improve clinic margin per visit. Production, however, is technically demanding because each antigen must preserve integrity during formulation. This complexity strengthens the incumbents that already control GMP-certified multipurpose lines, reinforcing competitive barriers within the canine vaccine market.

By Administration Route: Intranasal Innovation Challenges Subcutaneous Standard

The subcutaneous route accounted for 69.85% of the canine vaccine market size in 2025. Intranasal alternatives advance at 7.22% CAGR due to rapid mucosal immunity and easier handling in anxious patients. Zoetis introduced a 0.5 mL single-nostril Bordetella vaccine, cutting procedure time and improving owner perception of comfort. Intramuscular shots fill occasions needing quick systemic coverage, while oral baits remain confined largely to wildlife rabies control.

Studies show intranasal formulations trigger protection within seven days, faster than injectables. Clinics adopting the method report higher acceptance rates among vaccine-hesitant clients. Manufacturers follow suit with pipelines that harness lyophilized powders mixed in clinic, minimizing cold-chain burdens and adding resilience to the canine vaccine market.

By Indication: Bordetella Growth Outpaces Rabies Leadership

Rabies vaccines led with 28.60% revenue in 2025 because regulatory mandates enforce coverage exceeding 70% to stop human cases. Bordetella shots, however, are projected to grow at 7.28% CAGR, aided by rising kennel cough awareness and novel intranasal formats. Parvovirus and distemper maintain core schedule positions, and new monoclonal adjuncts enhance protection for high-risk puppies.

Leptospirosis uptake lags in parts of Europe where only 50.1% of dogs meet vaccination guidelines, exposing opportunities for targeted education. Lyme disease sits within the Others category yet is drawing R&D interest as climate shifts expand tick ranges. The blend of stable core demand and fast-moving niche products supports a balanced revenue outlook for the canine vaccine market.

Geography Analysis

North America controlled 39.30% of canine vaccine market revenue in 2025, underpinned by expansive clinic networks, high dog ownership and insurance penetration that cushions economic shocks. Extended three-year label adoption aligns with owner convenience and encourages uptake despite cost concerns. Regulatory harmonization across the United States and Canada streamlines product rollouts, giving manufacturers the scale required to recover R&D spend.

Asia-Pacific is forecast to post the highest 7.24% CAGR to 2031. China drives this surge, posting a USD 30 billion pet medical segment that grows 17.7% annually, and where average clinics see heavier caseloads than peers in the United States. Rising middle-class wealth, single-person urban living and an aging population contribute to higher preventive spending. Governments also partner with industry on rabies eradication campaigns, expanding tender volumes.

Europe delivers steady mid-single-digit gains supported by the European Medicines Agency’s unified approval regime. Owners in Germany, France and the Nordic region gravitate toward premium products with extended duration of immunity, limiting injection frequency. Latin America shows variable growth tied to economic cycles but benefits from regional public-health initiatives targeting rabies elimination in dogs. The Middle East and Africa remain long-term propositions; however, multilateral donor funding for vaccine drives is expanding public awareness and infrastructure, laying groundwork for the next phase of canine vaccine market expansion.

Competitive Landscape

The canine vaccine market tilts toward moderate concentration. Zoetis heads the field with a diversified portfolio and generated USD 9.3 billion revenue in 2024, helped by 8% companion-animal growth anchored in vaccines. Merck Animal Health commands share through the NOBIVAC range and recently debuted RNA-particle technology that resets performance benchmarks. Boehringer Ingelheim deepened its platform breadth by purchasing Saiba Animal Health, signalling a strategic shift toward therapeutic vaccines for chronic conditions.

Strategic moves emphasize both platform acquisition and life-cycle management. Leaders align with tele-veterinary apps to time reminders, using data to drive compliance. R&D pipelines reveal a pivot to vector-based multivalent candidates that address emerging pathogens and reduce visit frequency. Although top players share global GMP networks, they also localize fill-finish lines to navigate tariff structures and assure cold-chain continuity.

Smaller firms focus on single-indication niches or regional needs, partnering with multinationals for marketing scale once proof of concept is secured. Venture funding favors DNA and mRNA innovation, mirroring human vaccine trends. Despite consolidation, competition remains vigorous across indication, route and valence, which ultimately benefits clinic choice and supports sustained growth across the canine vaccine market.

Canine Vaccine Industry Leaders

-

Boehringer Ingelheim International GmbH.

-

Zoetis Services LLC

-

Merck & Co., Inc

-

Vetoquinol

-

Ceva

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Calviri vaccinated its first canine patient in a trial assessing an immunotherapy vaccine for early hemangiosarcoma.

- October 2024: The University of Chile released a one-year sterilizing canine vaccine priced at CLP 50,000 (USD 54).

- June 2024: Merck & Co. introduced the NOBIVAC NXT Rabies portfolio in Canada.

- March 2024: Zendal Group launched a recombinant vaccine against canine leishmaniasis developed by CIB-CSIC.

Global Canine Vaccine Market Report Scope

As per the scope of the study, A canine vaccine is a biological preparation that provides active acquired immunity to specific diseases in dogs. These vaccines contain agents that resemble the disease-causing microorganisms, which are often made from weakened or killed forms of the microbe, its toxins, or one of its surface proteins. When administered, they stimulate the dog’s immune system to recognize the agent as a threat, destroy it, and remember it, so the immune system can more easily recognize and destroy any of these microorganisms it encounters in the future.

The canine vaccine market is segmented by vaccine type, including attenuated live vaccines, inactivated vaccines, subunit vaccines, DNA vaccines, and recombinant vaccines. The administration process includes subcutaneous, intramuscular, and intranasal, By geography includes North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD) for the above segments.

| Attenuated Live |

| Inactivated |

| Subunit |

| DNA |

| Recombinant |

| Viral-vectored |

| Monovalent |

| Multivalent |

| Subcutaneous |

| Intramuscular |

| Intranasal |

| Oral |

| Rabies |

| Parvovirus |

| Distemper |

| Leptospirosis |

| Bordetella |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Vaccine Type | Attenuated Live | |

| Inactivated | ||

| Subunit | ||

| DNA | ||

| Recombinant | ||

| Viral-vectored | ||

| By Valence Type | Monovalent | |

| Multivalent | ||

| By Administration Route | Subcutaneous | |

| Intramuscular | ||

| Intranasal | ||

| Oral | ||

| By Indication | Rabies | |

| Parvovirus | ||

| Distemper | ||

| Leptospirosis | ||

| Bordetella | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the canine vaccine market?

The canine vaccine market size stands at USD 2.27 billion in 2026 and is projected to reach USD 3.06 billion by 2031.

Which vaccine technology is growing the fastest?

DNA platforms are expanding at a 7.35% CAGR, the highest among all vaccine types.

Which region offers the strongest growth outlook?

Asia-Pacific is forecast to rise at a 7.24% CAGR through 2031, outpacing all other regions.

What segment dominates administration routes?

Subcutaneous injections retain 69.85% revenue share, although intranasal delivery is gaining traction.

How does anti-vaccination sentiment affect the market?

Owner hesitancy is estimated to trim market CAGR by 1.1% and has already lowered puppy vaccination coverage in several mature economies.

Who are the major industry players?

Zoetis, Merck Animal Health and Boehringer Ingelheim headline the competitive landscape, collectively controlling a significant share of global sales.

Page last updated on: