Canine Arthritis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

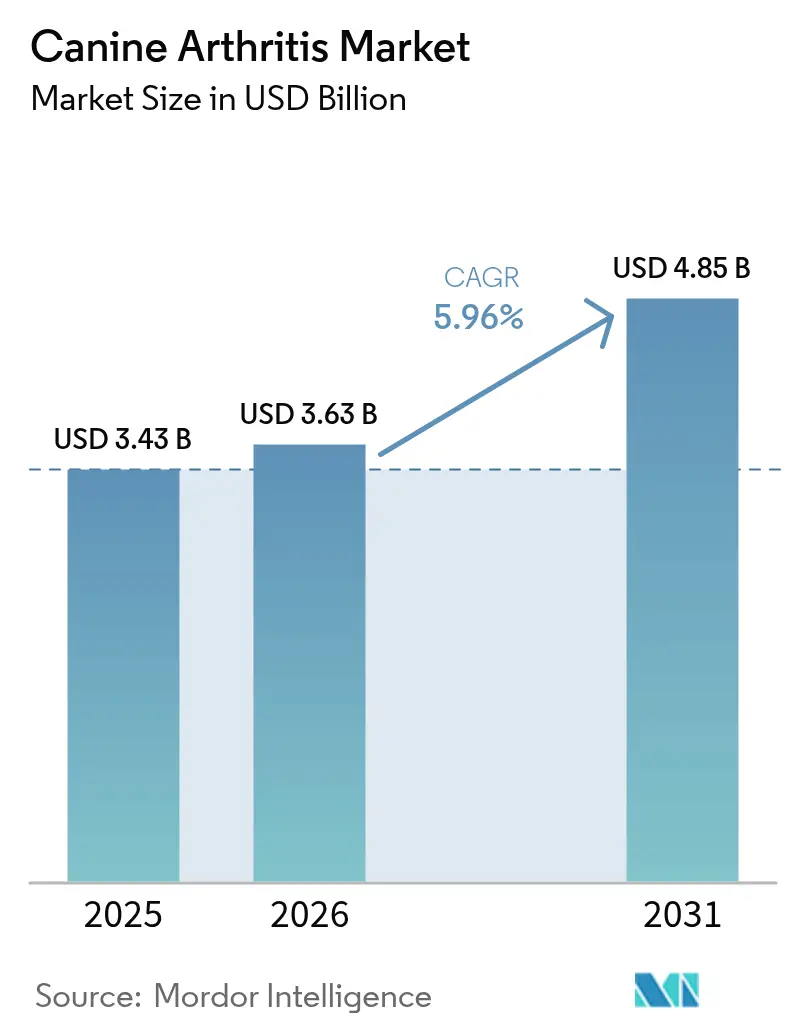

| Market Size (2026) | USD 3.63 Billion |

| Market Size (2031) | USD 4.85 Billion |

| Growth Rate (2026 - 2031) | 5.96% CAGR |

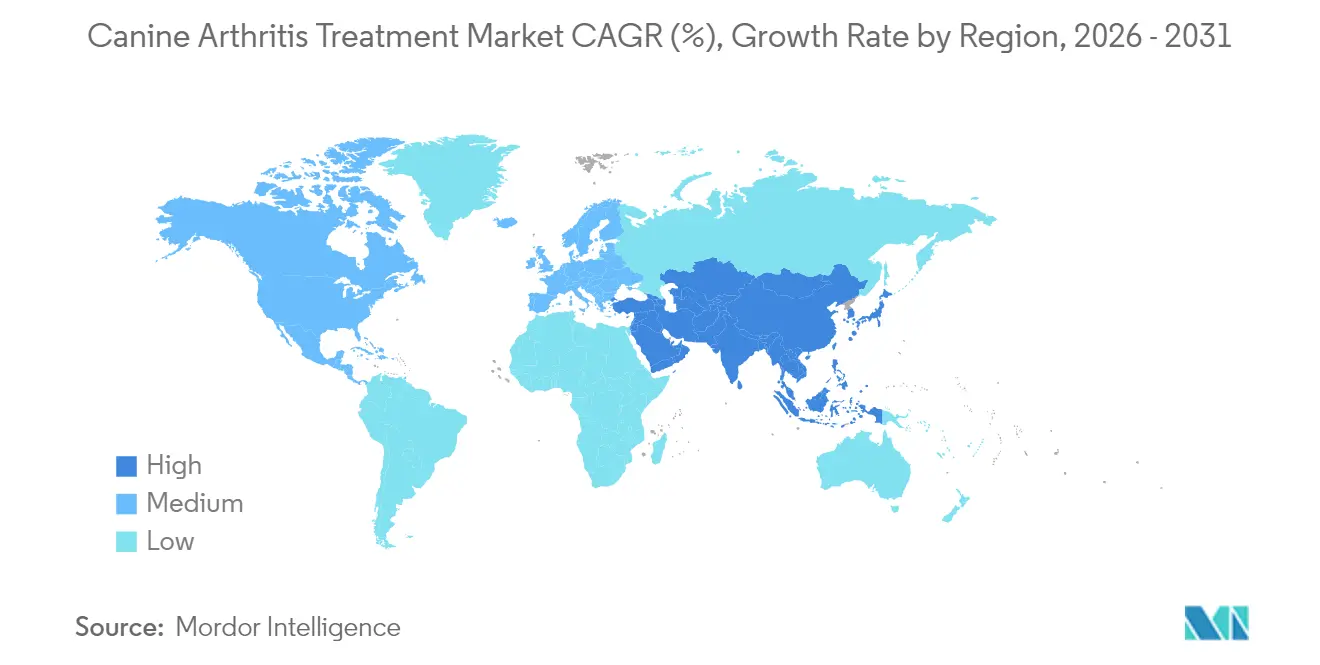

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canine Arthritis Market Analysis by Mordor Intelligence

The canine arthritis market size is expected to grow from USD 3.43 billion in 2025 to USD 3.63 billion in 2026 and is forecast to reach USD 4.85 billion by 2031 at 5.96% CAGR over 2026-2031. Growth is propelled by three structural forces: a swelling population of senior dogs, faster regulatory pathways for veterinary biologics, and artificial-intelligence-enabled imaging that detects pre-clinical osteoarthritis. The European Medicines Agency’s record 25 veterinary approvals in 2024, including monoclonal antibodies for nerve growth factor inhibition, illustrate how policy support is compressing product launch cycles.[1]European Medicines Agency, “Veterinary Medicines in 2024,” ema.europa.eu At the same time, AI radiomics platforms integrated with force-plate gait analytics allow veterinarians to begin disease-modifying therapy up to 18 months before overt lameness. These advances encourage a pivot from symptom control toward joint preservation and are enlarging the addressable canine arthritis treatment and diagnostics market.

Key Report Takeaways

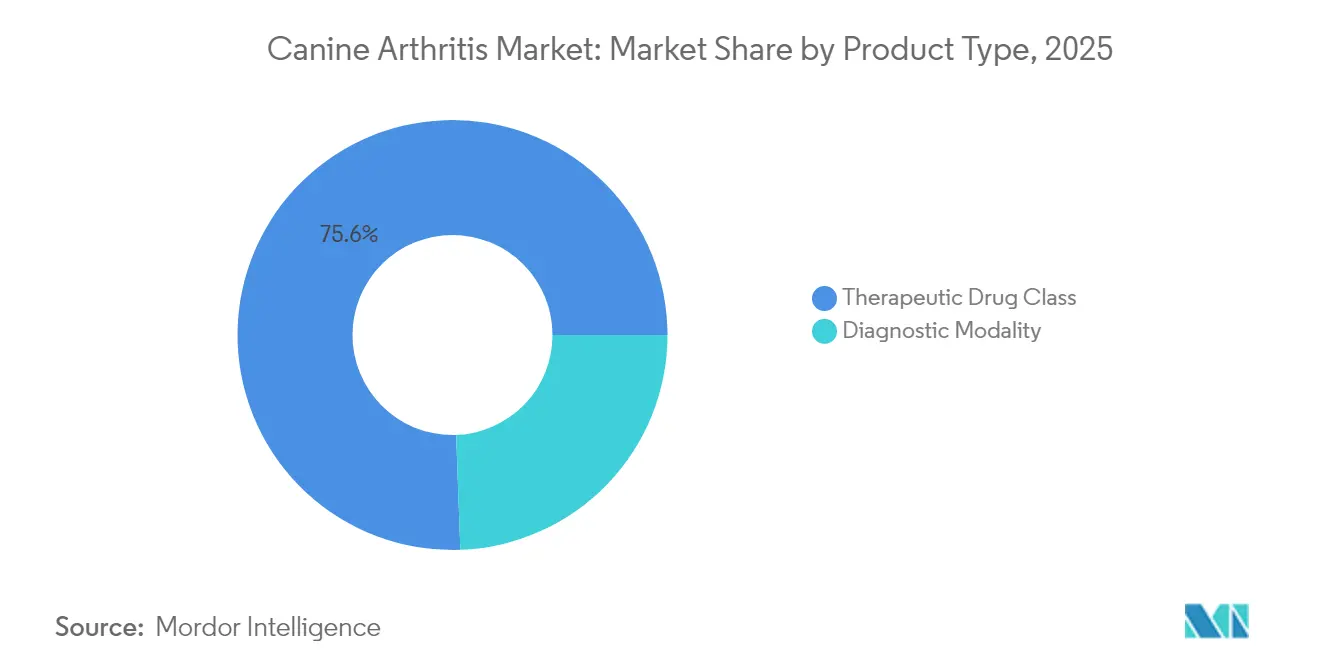

- By product type, therapeutic drug classes led with 75.58% revenue share in 2025; diagnostic modalities are forecast to expand at a 6.78% CAGR to 2031.

- By disease stage, moderate arthritis (Grade 3) captured 33.89% of cases in 2025, while pre-clinical and Grade 0-1 interventions are advancing at a 7.01% CAGR through 2031.

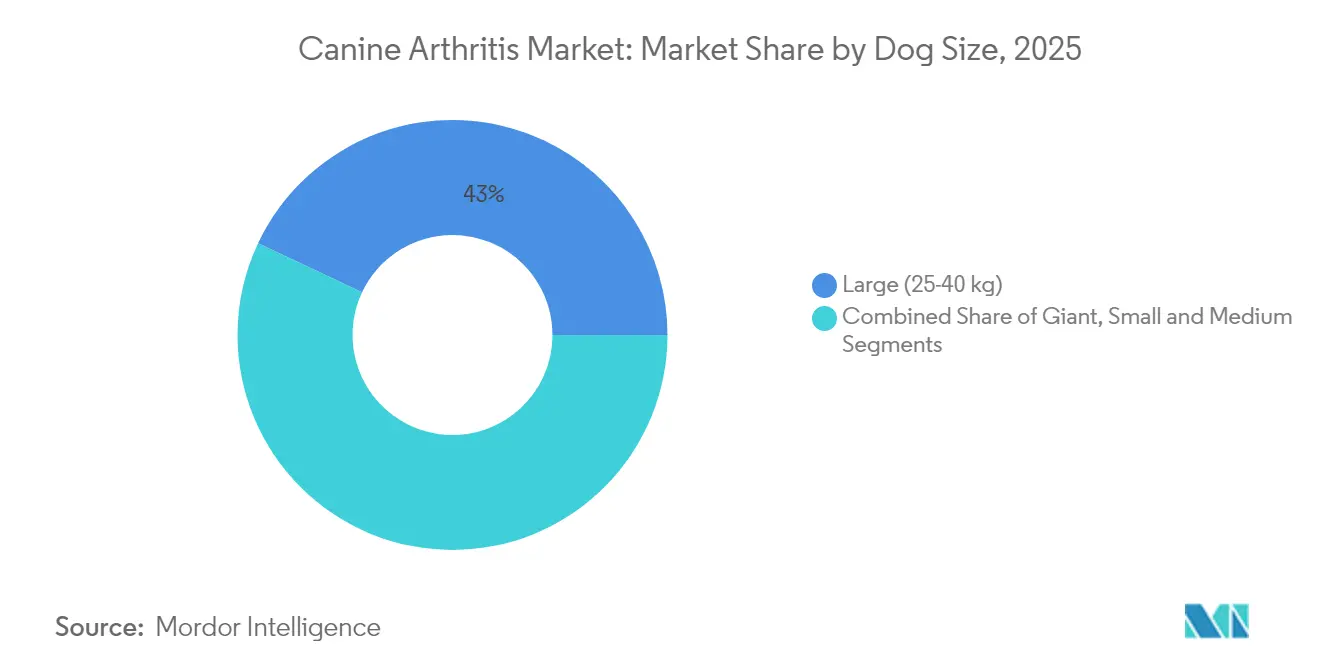

- By dog size, large breeds commanded 42.98% of the canine arthritis treatment and diagnostics market share in 2025; giant breeds are set to grow at an 8.45% CAGR to 2031.

- By age group, senior dogs made up 57.74% of patients in 2025; adult dogs are the fastest-growing cohort, registering a 9.07% CAGR to 2031.

- By end user, veterinary hospitals and specialty clinics held 45.62% of 2025 revenue, while home-care settings are rising at a 9.68% CAGR on the back of telemedicine uptake.

- By geography, north america held 34.88% of 2025 revenue, while asia-pacific is rising at a 9.88% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Canine Arthritis Market Trends and Insights

Drivers Impact Analysis*

| Driver | ~ (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Prevalence of Canine Obesity and Motion Injuries | +0.9% | North America, Western Europe | Medium term (2-4 years) |

| Ageing Pet Population and Pet-Humanization Trend | +1.2% | North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Rising Penetration of Pet Insurance and Veterinary Spend | +0.8% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Regulatory Fast-Track for Veterinary Monoclonal Antibodies | +1.0% | North America, EU, Australia, Japan | Short term (≤ 2 years) |

| AI-Driven Radiomics Enabling Sub-Clinical OA Detection | +0.7% | North America, Europe, Asia-Pacific follow-on | Medium term (2-4 years) |

| Preventive Joint-Health Functional Treats | +0.6% | Global premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Prevalence of Canine Obesity and Motion Injuries

Fifty-nine percent of U.S. dogs were overweight or obese in 2024, a biomechanical burden that accelerates cartilage wear in weight-bearing joints.[2]Banfield Pet Hospital, “State of Pet Health 2024 Report,” banfield.com Comparable surveys in the United Kingdom found a 50% obesity rate and a 2.8-fold rise in osteoarthritis diagnoses before age 8 among overweight dogs.[3]PDSA, “Animal Wellbeing Report 2024,” pdsa.org.uk Excess adiposity elevates systemic cytokines such as interleukin-6, eroding synovial viscosity. Agility sports and hard-surface urban exercise further compound joint trauma in working breeds. With 67% of U.S. households now owning pets, roughly 38 million dogs carry elevated arthritis risk. This demographic pressure sustains demand for early diagnostics and weight-management nutraceuticals that address inflammation before irreversible damage occurs.

Aging Pet Population and Pet-Humanization Trend

The median age of U.S. dogs climbed to 6.2 years in 2024, reflecting better nutrition and preventive medicine. Senior dogs already comprise 58.38% of arthritis patients, and owners increasingly treat them as family members, spending USD 1,543 per dog on veterinary care in 2024. Generation Z pet parents allocate discretionary income to platelet-rich plasma and hydrotherapy once reserved for performance animals. In Japan, 38% of households insure canine companions, reinforcing a culture of proactive longevity care. This willingness to invest underpins steady uptake of disease-modifying and regenerative therapies within the canine arthritis treatment and diagnostics market.

Rising Penetration of Pet Insurance and Veterinary Spend

More than 5 million U.S. dogs carried insurance in 2024, with orthopedic reimbursement ratios reaching 90% in premium tiers. Sweden’s 90% penetration and the United Kingdom’s 25% demonstrate insurance as a catalyst for advanced imaging adoption. Average orthopedic claims climbed 12% year-over-year, indicating owners pursue comprehensive diagnostics when financial risk is capped. This financial buffer expands the canine arthritis treatment and diagnostics market by opening the door to biologics and specialty care.

Regulatory Fast-Track for Veterinary Monoclonal Antibodies

The EMA cleared 25 veterinary drugs in 2024, including nerve-growth-factor inhibitors for osteoarthritis. In parallel, the U.S. ADUFA 2024 reauthorization trimmed biologic review cycles to 12 months. Zoetis’s bedinvetmab secured FDA approval in 2023 and generated USD 120 million in first-year sales, validating accelerated pathways. Harmonized VICH guidelines introduced in 2025 further streamline global launches, lowering capital hurdles for mid-sized innovators.

Restraints Impact Analysis*

| Restraint | ~ (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Lifetime Cost of Long-Term Analgesic and Biologic Therapy | -0.7% | Global, sharper in low-insurance markets | Medium term (2-4 years) |

| NSAID-Related Safety Concerns | -0.5% | North America, EU regulatory focus | Short term (≤ 2 years) |

| Limited Reimbursement for Advanced Imaging and Gait Analytics | -0.4% | North America, Europe | Medium term (2-4 years) |

| Divergent Global Rules for Autologous Cell and Gene Therapies | -0.3% | Worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Lifetime Cost of Long-Term Analgesic and Biologic Therapy

Monthly monoclonal antibody injections cost USD 80-120, pushing lifetime expense beyond USD 3,000 for dogs diagnosed at age 8. Autologous stem-cell cycles run USD 2,500-4,500, limiting uptake to affluent owners. Generic NSAIDs remain cheaper but require indefinite dosing and frequent monitoring. Where insurance penetration is low, cost becomes a primary barrier that tempers expansion of the canine arthritis treatment and diagnostics market.

NSAID-Related Safety Concerns

The FDA mandated stronger NSAID warning labels in 2024 after carprofen accounted for 47% of adverse-event reports. Voluntary withdrawal of deracoxib in Europe highlighted gastrointestinal risks. Owner hesitancy and the extra USD 150-300 in yearly bloodwork dampen first-line NSAID use, nudging clinicians toward higher-priced biologics while still constraining overall therapy volume.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Therapeutics Dominate, Diagnostics Accelerate

Therapeutic classes controlled 75.58% of 2025 revenue, underscoring pharmacologic reliance in the canine arthritis treatment and diagnostics market. NSAIDs still underpin daily pain control, yet nerve-growth-factor monoclonal antibodies such as bedinvetmab recorded USD 120 million in first-year U.S. sales, signifying rapid clinician adoption. Disease-modifying agents like polysulfated glycosaminoglycans enlarge the toolbox for early-stage disease.

Diagnostics accounted for a smaller base but are growing at 6.78% CAGR, buoyed by AI radiomics and biomarker assays that spot degradation before radiographic confirmation. Subscription analytics platforms expand usage beyond specialty hospitals, creating new touchpoints that enlarge the canine arthritis treatment and diagnostics market size.

By Disease Stage: Pre-Clinical Interventions Gain Momentum

Moderate arthritis remained the largest cohort at 33.89% of cases in 2025, aligning with the first point when owners notice mobility decline. Severe Grade 4 disease often forces euthanasia discussions despite multimodal analgesia.

In contrast, pre-clinical and Grade 0-1 cases are expanding at 7.01% CAGR as radiomics and force-plate screens become routine in wellness visits. Early intervention with disease-modifying drugs preserves cartilage and delays costly surgery. This shift shows how technology is pulling revenue into the front end of the canine arthritis treatment and diagnostics market.

By Dog Size: Giant Breeds Drive Premium Therapeutics

Large breeds held 42.98% of revenue in 2025, but giant breeds are topping the growth chart at 8.45% CAGR. A longitudinal review of 4.9 million dogs revealed giant breeds develop osteoarthritis 3.2 years earlier than small dogs. Dosage economics favor NSAIDs for giants but make biologics proportionally costlier, influencing product-mix decisions for veterinarians and owners. Targeted messaging around quality of life is converting giant-breed owners into high-value clients within the canine arthritis treatment and diagnostics market.

By Age Group: Adult Dogs Enter Preventive Paradigm

Senior dogs still dominate with 57.74% share, yet adult dogs aged 1-7 years are rising fastest at 9.07% CAGR. Breeders and performance-dog handlers popularized prophylactic supplements at 6 months of age, and mainstream owners are following suit. Force-plate gait screening at annual checkups is catching sub-clinical lameness that once went unnoticed. This preventive orientation strengthens lifetime value per patient and expands the overall canine arthritis treatment and diagnostics market size for wellness-based solutions.

By End User: Home-Care Settings Disrupt Traditional Delivery

Veterinary hospitals and specialty clinics generated 45.62% of 2025 revenue, steered by CT, MRI, and surgical interventions. Yet telemedicine is shifting revenue to the home, where remote consultations pair with mailed NSAIDs and nutraceuticals. Regulatory acceptance of remote prescribing in 2024 unlocked a 9.68% CAGR channel that augments reach, lowers client acquisition cost, and diversifies the canine arthritis treatment and diagnostics market.

Geography Analysis

North America retained 34.88% of 2025 revenue. U.S. veterinary spend averaged USD 1,500 per dog, and 22% of arthritic dogs received a monoclonal antibody injection within 12 months of Librela’s launch, illustrating biologic traction. Canada’s provincial insurance incentives for imaging further increase early diagnosis rates, whereas Mexico’s emerging middle class is price sensitive, dampening biologic uptake but stimulating generic NSAID sales.

Asia-Pacific is the fastest-growing region at 9.88% CAGR. China’s pet economy hit RMB 130 billion (USD 18.2 billion) in 2024, with millennial owners prioritizing preventive care. Japan’s high insurance penetration and hospice services showcase market maturity. India and South-East Asian nations are easing import rules for veterinary biologics, a policy change expected to accelerate growth of the canine arthritis treatment and diagnostics market.

Europe held 27.62% of 2025 revenue. Germany and France favor holistic adjuncts, while the United Kingdom’s 25% insurance penetration boosts rehabilitative therapy demand. EMA’s centralized procedure for biosimilar biologics promises price competition and broader access. Emerging regions in South America and the Middle East are smaller today yet show double-digit growth curves fueled by rising disposable income and greater availability of imported therapeutics.

Competitive Landscape

The top five players captured large share of 2024 revenue, indicating moderate concentration. Zoetis commands the monoclonal antibody niche with bedinvetmab, targeting USD 500 million annual sales by 2027. Elanco’s Credelio Plus combines NSAID and nutraceutical ingredients to appeal to early-stage cases, and Boehringer Ingelheim is co-developing autologous cell therapy with VetStem. Dechra focuses on ISO-certified generic NSAIDs, while Ceva aligns around practitioner education. Telemedicine entrants such as Vetster are building vertically integrated ecosystems that stitch diagnostics, e-pharmacy, and data analytics into remote care pathways, expanding the digital flank of the canine arthritis treatment and diagnostics market.

Strategic thrusts include diagnostic acquisitions that bundle imaging and therapeutics, joint ventures to cut manufacturing costs for regenerative products, and R&D into biosimilar monoclonal antibodies ahead of patent cliffs in 2027. The FDA’s draft guidance on AI-powered devices provides a clearer runway for software innovators, setting sensitivity and specificity thresholds that are commercially achievable.

Canine Arthritis Industry Leaders

Boehringer Ingelheim

Zoetis

Elanco

Boehringer Ingelheim

Dechra Pharmaceuticals

Merck Animal Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Zoetis released the first head-to-head trial showing Librela matched meloxicam efficacy with fewer adverse events, validating antibody use as first-line care.

- February 2025: Zoetis updated the U.S. Librela label after surpassing 25 million global doses, confirming adverse-event rates below 10 per 10,000.

- April 2024: A pilot study on amorphous calcium carbonate achieved 45.5% success versus 21.4% for placebo in osteoarthritis dogs, prompting larger trials.

- March 2024: Cornell University issued clinical guidance outlining nerve-growth-factor antibody integration into multimodal pain strategies.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the canine arthritis treatment market as the annual revenue generated worldwide from prescription and over-the-counter drugs, monoclonal antibodies, and nutraceutical supplements that manage clinically diagnosed osteoarthritis in dogs.

(Scope exclusion) Surgical joint replacements, orthopedic implants, diagnostic imaging fees, rehabilitation services, and therapies for cats, horses, or other companion animals are deliberately excluded to keep our modeling tight and comparable.

Segmentation Overview

- By Product Type

- Therapeutic Drug Class

- NSAIDs

- Monoclonal Antibodies

- Nutraceutical Supplements

- Disease-Modifying OA Drugs (DMOADs)

- Autologous Cell & Gene Therapies

- Others

- Diagnostic Modality

- Physical Examination / Palpation

- Radiography (X-ray)

- Advanced Imaging (CT / MRI / Ultrasound)

- Force-plate & Gait-analysis Wearables

- Biomarker Panels (Serum / Synovial Fluid)

- Therapeutic Drug Class

- By Disease Stage

- Pre-clinical / Grade 0–1

- Mild / Grade 2

- Moderate / Grade 3

- Severe / Grade 4

- By Dog Size

- Small (Less than 10 kg)

- Medium (10–25 kg)

- Large (25–40 kg)

- Giant (More Than 40 kg)

- By Age Group

- Juvenile (Less Than 1 yr)

- Adult (1–7 yrs)

- Senior (More Than 7 yrs)

- By End User

- Veterinary Hospitals & Specialty Clinics

- General Veterinary Practices

- Research & Academic Institutes

- Home-care Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with practicing veterinarians, pet insurance actuaries, contract manufacturers, and e-commerce pharmacy managers across North America, Europe, and Asia-Pacific. Their insights refined prevalence assumptions, typical course lengths, and regional price dispersion, letting us adjust early desk-based estimates before locking the model.

Desk Research

We collected foundational numbers from tier-one public sources such as the American Veterinary Medical Association, European Pet Food Industry Federation, United States FDA veterinary approvals, and customs shipment data covering major canine NSAID molecules. Company 10-Ks, investor decks, and veterinary trade journals provided average selling prices, prescription volumes, and launch timelines. Our team also tapped D&B Hoovers for firm-level revenue splits and Dow Jones Factiva for real-time product uptake stories, which helped us benchmark treatment adoption curves across regions.

Finally, canine demographic data from national statistics offices, pet insurance claim databases, and academic papers on osteoarthritis prevalence let us quantify the addressable dog population and age-linked risk. These references illustrate, rather than exhaust, the wider body of literature we reviewed.

Market-Sizing & Forecasting

Our analysts began with a top-down pool, converting dog population by age band into expected osteoarthritis cases using peer-reviewed prevalence ratios, which are then multiplied by average annual treatment spend to set the 2025 baseline. Select bottom-up checks, such as sampled NSAID shipments multiplied by blended ASP and channel inventory roll-ups, validated totals and highlighted any gaps. Key variables inside the forecast include aging-dog share, first-line NSAID prescription rate, uptake curve for monthly monoclonal antibodies, pet insurance penetration, regulatory approvals cadence, and inflation-adjusted drug pricing. A multivariate regression supported by ARIMA overlays projects each driver forward, and scenario analysis tests price-sensitive segments.

Data Validation & Update Cycle

Before sign-off, our reviewers compare model outputs with third-party shipment tallies, licensing fee disclosures, and abnormal variance alerts. Any deviation above preset thresholds triggers additional expert follow-ups. Reports refresh yearly, with interim updates when material events, such as product recalls, key approvals, or currency swings, shift the outlook.

Why Our Canine Arthritis Treatment Baseline Commands Veterinary Confidence

We realize published estimates often diverge, and we preview below the usual reasons.

Differing geographic reach, mixed inclusion of surgical revenues, currency translation methods, and refresh cadences commonly widen the gap from one publisher to another, whereas Mordor's disciplined scope and annual updates keep figures stable and transparent.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.62 B | Mordor Intelligence | |

| USD 2.47 B | Global Consultancy A | Adds feline and equine therapies, mixes 2024 FX rates with 2025 volumes |

| USD 2.53 B | Industry Research Firm B | Includes surgical procedures and rehab services alongside drugs |

| USD 2.50 B | Specialist Publisher C | Applies optimistic uptake scenario for biologics yet omits regional price differences |

Taken together, the comparison shows that once inconsistent scopes and assumptions are stripped away, Mordor Intelligence delivers a balanced, reproducible baseline rooted in clearly defined treatments and verifiable veterinary demand signals, giving decision-makers a figure they can trust.

Key Questions Answered in the Report

How large is the canine arthritis treatment and diagnostics market in 2026?

The market stands at USD 3.63 billion in 2026 and is forecast to reach USD 4.85 billion by 2031.

Which product class leads current spending?

Therapeutic drug classes, dominated by NSAIDs and monoclonal antibodies, captured 75.58% of 2025 revenue.

Which region is expanding fastest?

Asia-Pacific posts the highest growth at a 9.88% CAGR, supported by rising pet ownership and easier biologic approvals.

What drives the shift toward early diagnosis?

AI-powered radiomics and force-plate gait analytics detect sub-clinical joint changes, enabling intervention up to 18 months before lameness.

How costly are long-term biologic therapies?

Monthly monoclonal antibody injections cost USD 80-120, leading to lifetime expenses exceeding USD 3,000 for a senior dog.

Which companies dominate monoclonal antibodies?

Zoetis leads with bedinvetmab, while Elanco and Boehringer Ingelheim also invest aggressively in next-generation biologics.

Page last updated on: