Nursing Robots Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

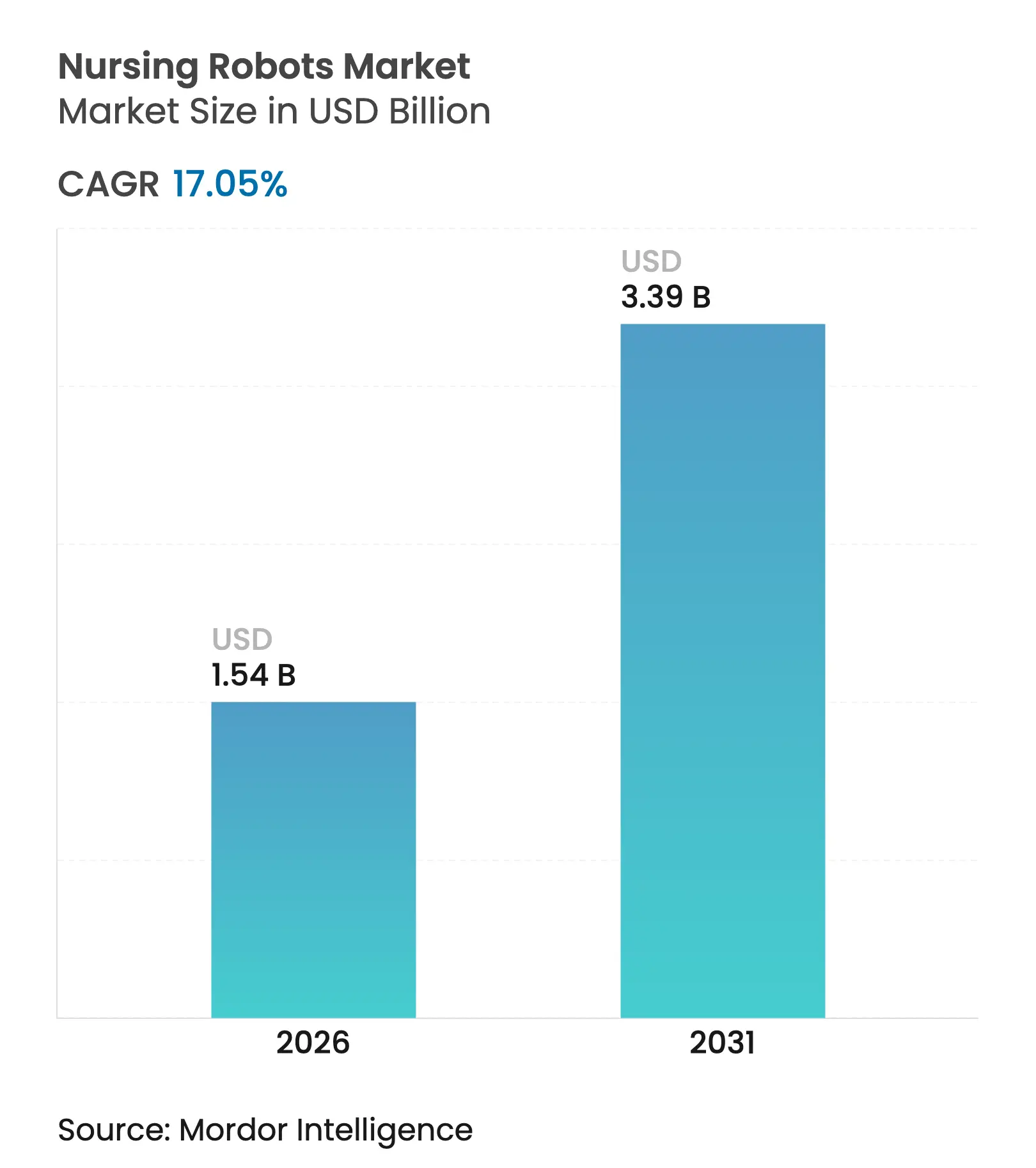

| Market Size (2026) | USD 1.54 Billion |

| Market Size (2031) | USD 3.39 Billion |

| Growth Rate (2026 - 2031) | 17.05 % CAGR |

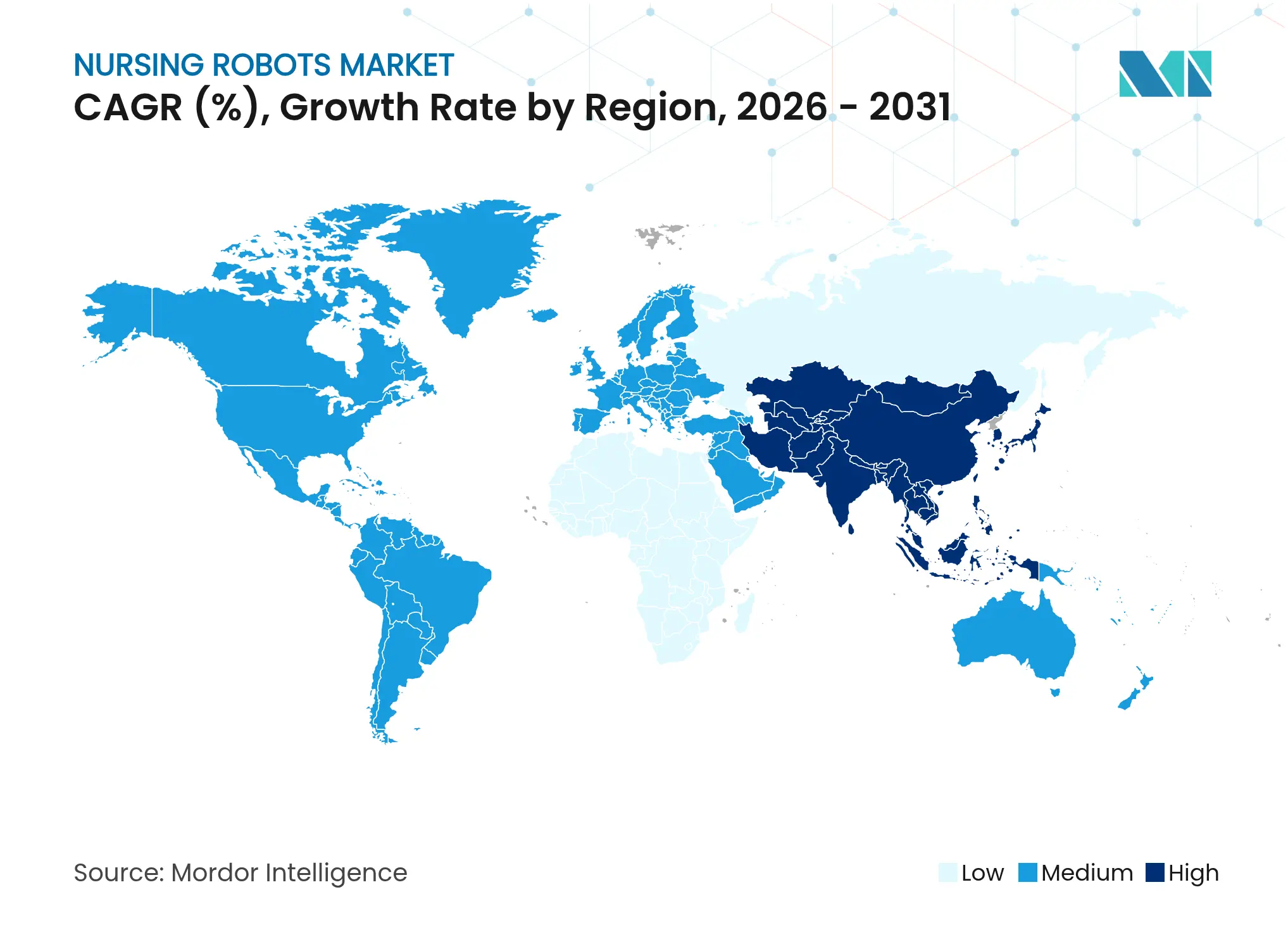

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

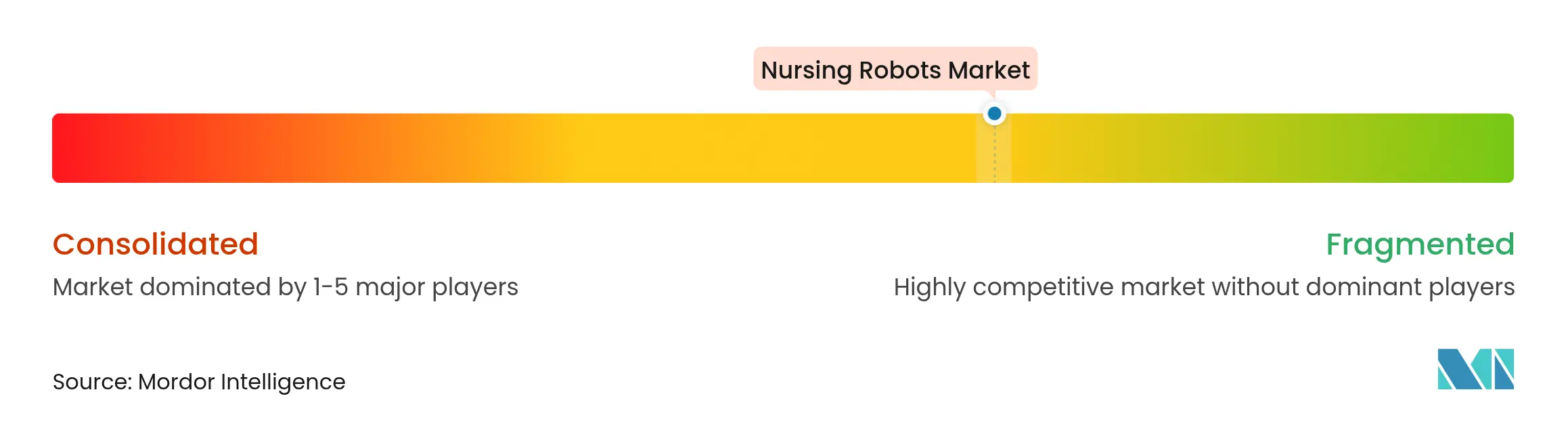

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Nursing Robots Market Analysis by Mordor Intelligence

The nursing robots market size was valued at USD 1.32 billion in 2025 and estimated to grow from USD 1.54 billion in 2026 to reach USD 3.39 billion by 2031, at a CAGR of 17.05% during the forecast period (2026-2031). Growth rests on converging demographic pressures, technological breakthroughs, and hospital‐at‐home reimbursement models that recast nursing robots as core healthcare infrastructure. A projected global shortage of 4.5 million nurses by 2030, coupled with Foxconn’s Nurabot deployment that trimmed nurse workloads by 30%, highlights the urgency of automation in direct care settings. Independent support robots hold the largest revenue share thanks to versatility in mobility aid and routine care, while robust venture funding accelerates software innovation that lifts AI performance benchmarks. Regional contrasts remain pronounced: North America benefits from Medicare’s Acute Hospital Care at Home program, whereas Asia-Pacific leads growth due to Japan’s aging-society policies and China’s new international standard for elderly-care robots. Competitive intensity is moderate; established firms such as Toyota and SoftBank Robotics face nimble entrants like Unlimited Robotics that secured USD 5 million for hospital-grade automation. Regulatory uncertainty and liability insurance gaps temper adoption, yet software-driven differentiation and fully autonomous capabilities sustain market optimism.

Key Report Takeaways

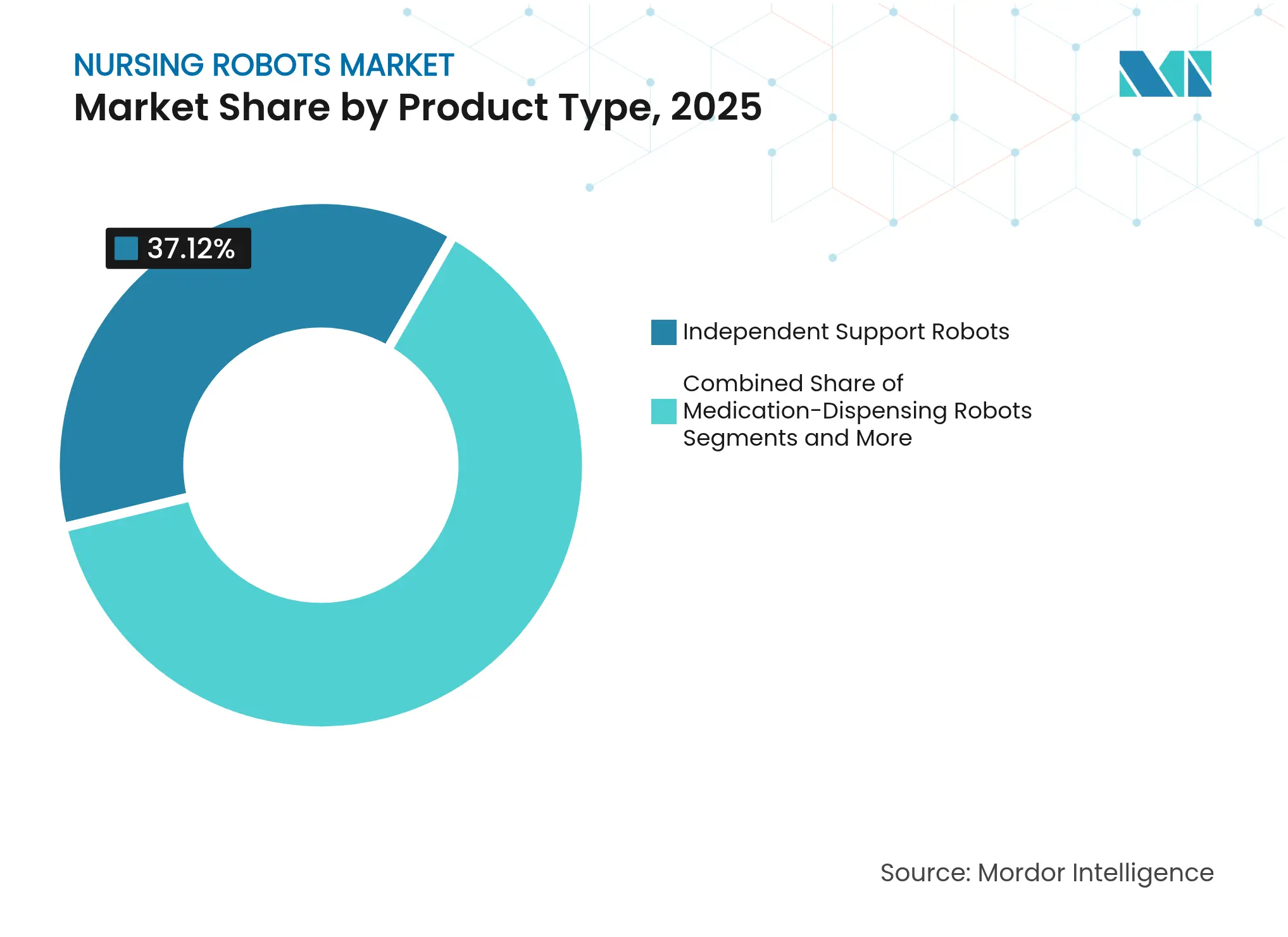

- By product type, Independent Support Robots held 37.12% of the nursing robots market share in 2025, while Telepresence & Telemedicine Robots are poised to expand at a 19.83% CAGR through 2031.

- By component, hardware led with 44.21% revenue share in 2025; software is forecast to grow at 20.74% CAGR to 2031.

- By autonomy level, semi-autonomous systems dominated with 38.56% of the nursing robots market size in 2025; fully autonomous platforms are projected to rise at a 18.55% CAGR.

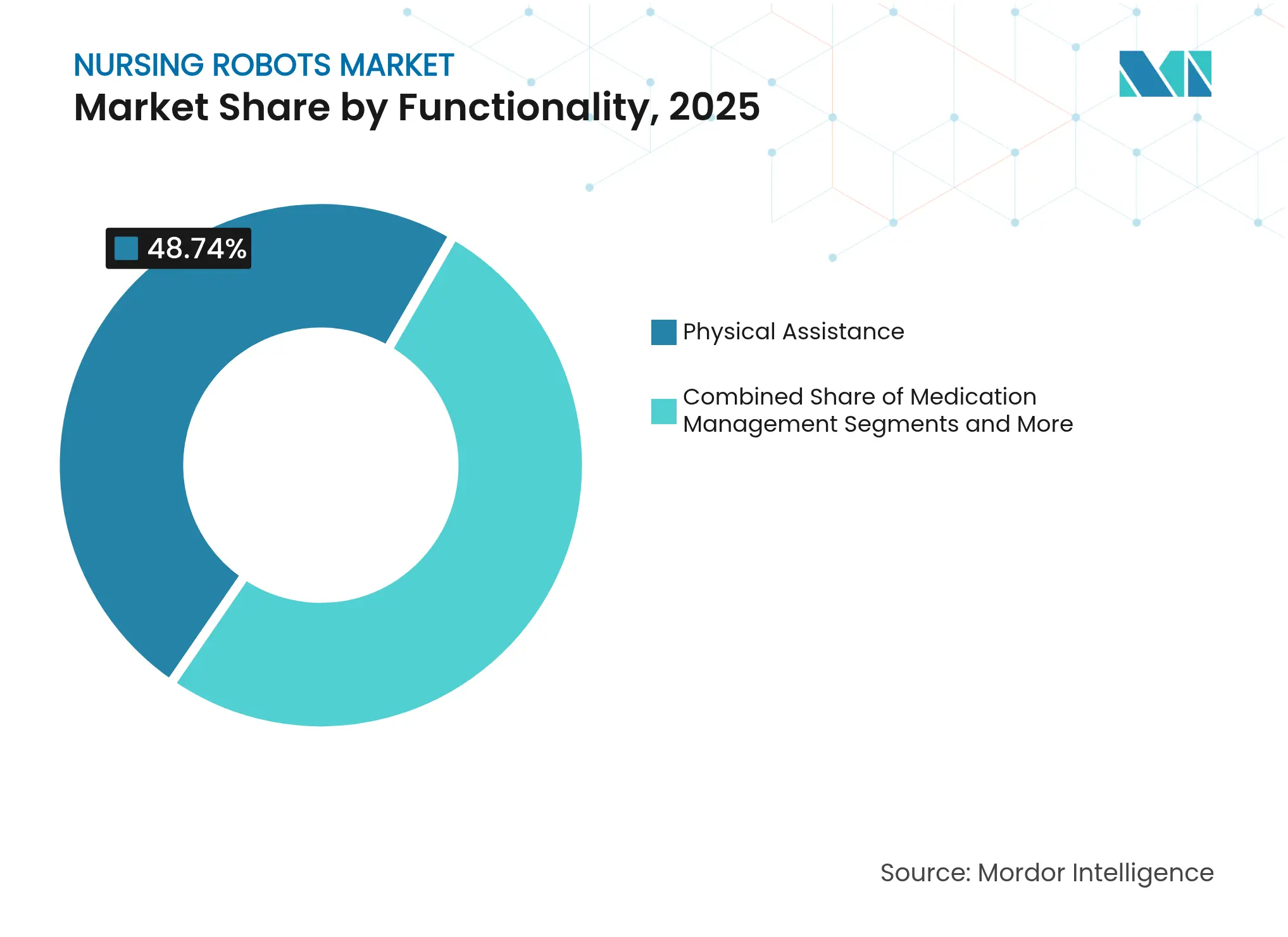

- By functionality, physical assistance commanded 48.74% share of the nursing robots market size in 2025; social/companion interaction is advancing at a 18.79% CAGR through 2031.

- By end user, hospitals & clinics accounted for 55.12% share of the nursing robots market size in 2025, while home-care settings are set to grow at an 18.2% CAGR.

- By geography, North America held 31.87% revenue share in 2025; Asia-Pacific is the fastest-growing region at a 18.47% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nursing Robots Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Shortage of nursing staff &

aging population

Shortage of nursing staff &

aging population

| +4.2% | Global, acute in Japan, Europe, North America | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+4.2%

|

Geographic Relevance

:

Global, acute in Japan, Europe,

North America

|

Impact Timeline

:

Long term (≥ 4 years)

|

Rising R&D investments &

funding

Rising R&D investments &

funding

| +2.8% | North America & EU, spill-over to APAC | Medium term (2-4 years) | |||

Advances in AI, tactile sensing

& HRI

Advances in AI, tactile sensing

& HRI

| +3.1% | Global, led by US, China, Japan | Medium term (2-4 years) | |||

Emergence of empathetic LLM-driven

care companions

Emergence of empathetic LLM-driven

care companions

| +2.5% | APAC core, expanding to North America & EU | Long term (≥ 4 years) | |||

Hospital-at-home reimbursement

models

Hospital-at-home reimbursement

models

| +1.9% | North America, early adoption in EU | Short term (≤ 2 years) | |||

Infection-prevention add-ons (UV-C,

etc.)

Infection-prevention add-ons (UV-C,

etc.)

| +1.7% | Global, healthcare-dense regions | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Shortage of Nursing Staff & Aging Population

America’s aging demographic is adding 2.1 million healthcare jobs by 2032, a figure representing 45% of all job growth. Robots such as Japan’s AIREC system now change diapers and reposition bedridden patients, easing caregiver burnout. University of Notre Dame research links robot use in nursing homes to lower staff turnover by shifting caregivers to empathy-driven tasks.[1]Allison Okamura, “Eldercare robot helps people sit and stand, and catches them if they fall,” ScienceDaily, sciencedaily.comChina’s need for over 6 million elderly-care workers while employing only 500,000 underlines scale mismatches that automation can bridge. Robots operate 24/7 without fatigue, addressing both quantity and quality gaps in patient care.

Rising R&D Investments & Funding

Unlimited Robotics raised USD 5 million to commercialize Gary, a multi-functional hospital robot ready for tasks from meal delivery to patient engagement. Richtech Robotics’ elevator-enabled Medbot posted a 100% delivery success rate in clinical pilots, boosting investor confidence. Panasonic’s acquisition of Danish AMR maker Robotize shows conglomerates buying specialized talent for healthcare entry. Funding now targets software stacks built on NVIDIA Jetson Orin, compressing iteration cycles and time-to-market. Capital availability thus widens the gap between well-funded suppliers and undercapitalized rivals.

Advances in AI, Tactile Sensing & HRI

Dual-arm nursing robots now run on large language models, coordinating each arm as an independent agent for higher precision.[2]Chuanhong Fang, “The Multi-Agentization of a Dual-Arm Nursing Robot Based on Large Language Models,” Bioengineering, bioengineering.com NVIDIA and Hippocratic AI report healthcare agents that beat human nurses on select safety metrics. AI-enhanced tactile sensors manage delicate wound-care tasks formerly reserved for clinicians bmcnurs.biomedcentral.com. Natural language processing bridges social isolation by enabling meaningful patient conversations, boosting acceptance rates. Collectively, these breakthroughs extend robots from logistics to comprehensive bedside support.

Emergence of Empathetic LLM-Driven Care Companions

Compassion-oriented humanoids rely on large language models to sense emotion and respond empathetically. Foxconn’s Nurabot converses naturally while handling logistics duties, proving practical merger of empathy and function. Clinical studies show generative AI can draft nursing care plans comparable to professional standards. ElliQ deployments in senior programs cut loneliness metrics through personalized dialogue. Robots are therefore repositioned as companions that address psychological as well as physical health.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High capex, unclear ROI &

data-security issues

High capex, unclear ROI &

data-security issues

| -2.1% | Global, cost-sensitive markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-2.1%

|

Geographic Relevance

:

Global, cost-sensitive markets

|

Impact Timeline

:

Medium term (2-4 years)

|

Fragmented & evolving regulatory

frameworks

Fragmented & evolving regulatory

frameworks

| -1.8% | Global, varied by region | Long term (≥ 4 years) | |||

Scarce liability insurance for

autonomous care robots

Scarce liability insurance for

autonomous care robots

| -1.3% | North America & EU | Medium term (2-4 years) | |||

Ethical pushback from unions &

patient advocates

Ethical pushback from unions &

patient advocates

| -0.9% | North America & EU | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Capex, Unclear ROI & Data-Security Issues

Hospitals contend with seven-figure robot invoices while traditional ROI models overlook intangible gains such as higher staff retention. Robots collect protected health data that intensifies cybersecurity spend, adding to total cost of ownership. Integration with legacy IT stretches budgets and timelines. Smart-home studies reveal seniors cite complexity and expense as primary adoption barriers, signaling parallel challenges for residential robots. Smaller facilities in emerging economies thus defer purchases, widening the digital divide.

Fragmented & Evolving Regulatory Frameworks

Manufacturers face divergent approval rules: EU Medical Device Regulation diverges from FDA pathways and Asia-Pacific standards.[3]European Parliament and Council, “EUR-Lex – 02017R0745-20250110 – EN,” eur-lex.europa.eu FDA analysis shows 86% of cleared surgical robots remain Level 1 autonomy amid unclear guidance for higher levels. China’s proactive elderly-care standard may tilt the competitive field to domestic suppliers. Scholars warn that autonomous AI blurs liability lines, requiring fresh legal constructs. Compliance cost inflation slows product launches and complicates global rollouts.

Segment Analysis

By Product Type: Independent Support Robots Redefine Core Care

Independent Support Robots held 37.12% of the nursing robots market share in 2025, proving indispensable for patient lifting, bed repositioning, and mobility tasks that mitigate caregiver injuries. Telepresence & Telemedicine Robots, the fastest-growing category at a 19.83% CAGR, match remote-care strategies that connect specialists to rural patients. Daily Care & Transportation Robots streamline meal and linen delivery, freeing staff for clinical duties. Medication-Dispensing Robots enhance pharmaceutical accuracy, as Wales’ REMEDY machine offers 24/7 access to urgent prescriptions. Mobility assist platforms intensify rehabilitation efforts, promoting faster patient independence.

Independent Support Robots thrive because hospitals prioritize robust payload capacity and safety-rated drives. The category’s dominance coincides with workforce policies aimed at reducing occupational injuries. Telepresence growth stems from stable broadband and payer support for virtual visits. Daily care robots leverage rising demand for logistics optimization within sprawling hospital campuses. Medication dispensing devices support antimicrobial stewardship by timestamping each unit dose, tightening inventory controls. Mobility aids find momentum in post-acute rehab centers that measure success by accelerated discharge timelines.

Note: Segment shares of all individual segments available upon report purchase

By Component: Software Emerges as the Differentiator

Hardware commanded 44.21% revenue share in 2025, reflecting the cost of actuators, sensors, and durable frames. Services revenue builds around installation, predictive maintenance, and staff training. Software remains the fastest-growing element at 20.74% CAGR because AI models now define task accuracy and conversational quality. Panasonic’s 2035 goal to derive 30% of group revenue from AI solutions illustrates this shift.

As machines commoditize, proprietary software dictates clinical acceptance by integrating with electronic health record systems. Cloud-delivered updates add fall-detection or triage routines, extending hardware life. API-driven ecosystems invite third-party developers, fostering network effects. Hospitals evaluate vendor roadmaps for AI transparency and model retraining cycles, making software governance a board-level agenda item.

By Level of Autonomy: Transition to Full Automation Gains Pace

Semi-Autonomous systems dominated the nursing robots market size with a 38.56% stake in 2025, aligning with regulatory comfort around human-in-the-loop controls. Fully Autonomous platforms post a 18.55% CAGR, lifted by sensor fusion and risk-aware path-planning. Diligent Robotics proved commercial reliability after completing 100,000 autonomous elevator rides without incident.

Hospitals evaluate autonomy against liability tolerance; mission-critical units such as ICUs often begin with semi-autonomous couriers before green-lighting wards for full autonomy. Payers reward full automation where continuous monitoring prevents sentinel events. Vendors counter liability fears with redundant perception modules and fail-safe brakes certified under IEC 61508, prompting regulators to reconsider autonomy ceilings.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Functionality: Physical Assistance Dominates while Social Interaction Accelerates

Physical Assistance accounted for 48.74% of revenue in 2025 due to tangible ROI from lift-related injury reduction. Monitoring & Telepresence extends clinician reach, and automated Medication Management cuts dispensing errors to near-zero variance. Disinfection & Sanitation robots remain staples after the pandemic, consistently lowering nosocomial infection rates.

Social/Companion Interaction, growing at 18.79% CAGR, draws funding as mental-health parity laws expand. Humanoid companions mitigate loneliness in eldercare and prompt medication adherence through conversational nudges. Large-language-model integration enables case-specific empathy that mirrors motivational interviewing, boosting patient engagement scores on Hospital Consumer Assessment metrics.

Note: Segment shares of all individual segments available upon report purchase

By End User: Hospitals Lead but Home Care Rises Quickly

Hospitals & Clinics controlled 55.12% of 2025 revenue through concentrated capital budgets and centralized procurement. Nursing Homes and Senior-Care Facilities adopt robots to address chronic staffing gaps. Rehabilitation Centers invest in gait-training exoskeletons anchored to robots that automate therapy repetitions.

Home-Care Settings post an 18.2% CAGR as reimbursement policies validate hospital-at-home models. In-home robots now integrate vitals monitoring, voice triage, and fall-prevention harnesses, cutting avoidable readmissions. Stanford research projects minority-majority elder households favor aging in place, reinforcing residential deployment potential.

Geography Analysis

North America retained 31.87% revenue share in 2025, supported by Medicare’s reimbursement expansions and venture capital depth. The United States records the highest installed base, while Canada pilots provincial subsidies that favor rural telepresence robots. Mexico’s private hospital chains adopt robots to differentiate premium services for cross-border medical tourists.

Europe’s single market accelerates regional compliance alignment, although each member state interprets MDR provisions differently. Germany funnels industrial automation know-how into medical robot production, and the United Kingdom’s NHS procures robots in response to staff strikes. Southern European nations face faster elder growth, prompting public funding for assisted-living automation.

Asia-Pacific is the fastest-growing region at 18.47% CAGR. Japan champions elder-centric robotics, embedding subsidies in its Long-Term Care Insurance Act. China leads global standardization, granting local vendors early-mover export opportunities. India’s urban hospitals deploy robots in crowded wards to streamline supply chains, while Australia invests in remote-area telehealth robots for indigenous communities. South Korea blends chaebol manufacturing strength with public-sector R&D, yielding export-ready platforms.

Competitive Landscape

Market Concentration

Market concentration remains moderate as industrial giants vie against agile entrants. Toyota leverages lean manufacturing to cut unit costs, ABB adapts industrial arms for lab automation, and SoftBank Robotics capitalizes on humanoid expertise. Diligent Robotics and Richtech Robotics differentiate through healthcare-specific analytics that optimize throughput. Unlimited Robotics positions Gary as a multi-domain platform, blurring lines between transport, telepresence, and social interaction.

Strategic collaborations dominate. Foxconn pairs with NVIDIA to embed edge AI modules in Nurabot, enhancing navigation accuracy and conversational latency. Panasonic acquires Robotize to accelerate vertical integration. Hospitals increasingly sign multi-year platform deals, locking in ecosystem loyalty. White-space niches such as infection control and medication security attract focused disruptors, protecting them from direct head-to-head clashes with conglomerates.

Pricing competition intensifies in mid-tier models, but total-solution contracts that bundle software and analytics preserve margins. Regulatory proficiency emerges as a moat; vendors that secure multi-regional approvals win enterprise contracts. Cybersecurity certifications now influence tenders, favoring firms with ISO 27001 and HIPAA compliance roadmaps.

Nursing Robots Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Foxconn unveiled Nurabot at Computex 2025, integrating NVIDIA Jetson Orin to cut nurse workloads by 30% in hospital pilots.

- March 2025: China gained IEC approval for the first international standard on elderly-care robots, setting global design and testing benchmarks.

- February 2025: Diligent Robotics’ Moxi crossed 1 million autonomous picks in live hospital environments, confirming industrial-scale reliability.

Table of Contents for Nursing Robots Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Shortage Of Nursing Staff & Ageing Population

- 4.2.2Rising R&D Investments & Funding

- 4.2.3Advances In AI, Tactile Sensing & HRI

- 4.2.4Emergence Of Empathetic LLM-Driven Care Companions

- 4.2.5Hospital-At-Home Reimbursement Models

- 4.2.6Infection-Prevention Add-Ons (UV-C, Etc.)

- 4.3Market Restraints

- 4.3.1High Capex, Unclear ROI & Data-Security Issues

- 4.3.2Fragmented & Evolving Regulatory Frameworks

- 4.3.3Scarce Liability Insurance For Autonomous Care Robots

- 4.3.4Ethical Pushback From Unions & Patient Advocates

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technology Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value-USD)

- 5.1By Product Type

- 5.1.1Independent Support Robots

- 5.1.2Daily Care & Transportation Robots

- 5.1.3Medication-Dispensing Robots

- 5.1.4Telepresence & Tele-medicine Robots

- 5.1.5Mobility/Locomotion Assist Robots

- 5.2By Component

- 5.2.1Hardware

- 5.2.2Software

- 5.2.3Services

- 5.3By Level of Autonomy

- 5.3.1Fully Autonomous

- 5.3.2Semi-Autonomous

- 5.4By Functionality

- 5.4.1Physical Assistance

- 5.4.2Social / Companion Interaction

- 5.4.3Monitoring & Telepresence

- 5.4.4Medication Management

- 5.4.5Disinfection & Sanitation

- 5.5By End User

- 5.5.1Hospitals & Clinics

- 5.5.2Home-Care Settings

- 5.5.3Nursing Homes

- 5.5.4Rehabilitation Centers

- 5.5.5Senior-Care Facilities

- 5.6By Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4Australia

- 5.6.3.5South Korea

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East and Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East and Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1Toyota Motor Corporation

- 6.3.2SoftBank Robotics

- 6.3.3Diligent Robotics

- 6.3.4Aethon Inc.

- 6.3.5Panasonic Holdings

- 6.3.6Relay Robotics Inc.

- 6.3.7Richtech Robotics Inc.

- 6.3.8Hstar Technologies

- 6.3.9Fraunhofer IPA

- 6.3.10RIKEN-SRK

- 6.3.11PAL Robotics

- 6.3.12UBTECH Robotics

- 6.3.13LG Electronics

- 6.3.14ABB Robotics

- 6.3.15Unlimited Robotics

- 6.3.16Intuition Robotics

- 6.3.17Paro Robots (AIST)

- 6.3.18Xenex Disinfection Services

- 6.3.19Savioke Inc.

- 6.3.20Ekso Bionics

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Nursing Robots Market Report Scope

As per the scope of the report, nursing robots are sophisticated robotic systems that aid healthcare professionals in delivering patient care. These robots undertake diverse tasks, including mobility assistance, bathing, dressing, and monitoring vital signs, aimed at boosting the efficiency and quality of healthcare services.

The nursing robots market is segmented into product type, end users, and geography. By product type, the market is segmented into independent support robots, daily care and transportation robots, medication dispensing robots, and other product types. By end user, the market is segmented into hospitals and clinics, home care settings, nursing homes, and other end users. By geography, the market is divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market sizes and forecasts were made based on value (USD).