Robotic Pet Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 438.36 Million |

| Market Size (2031) | USD 682.23 Million |

| Growth Rate (2026 - 2031) | 9.25% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

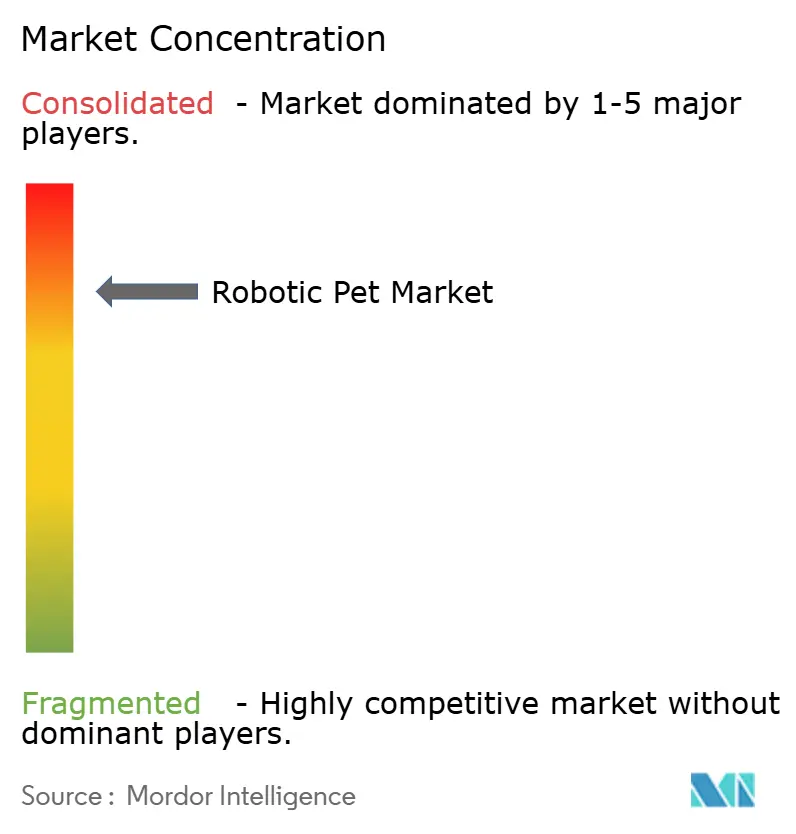

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Robotic Pet Market Analysis by Mordor Intelligence

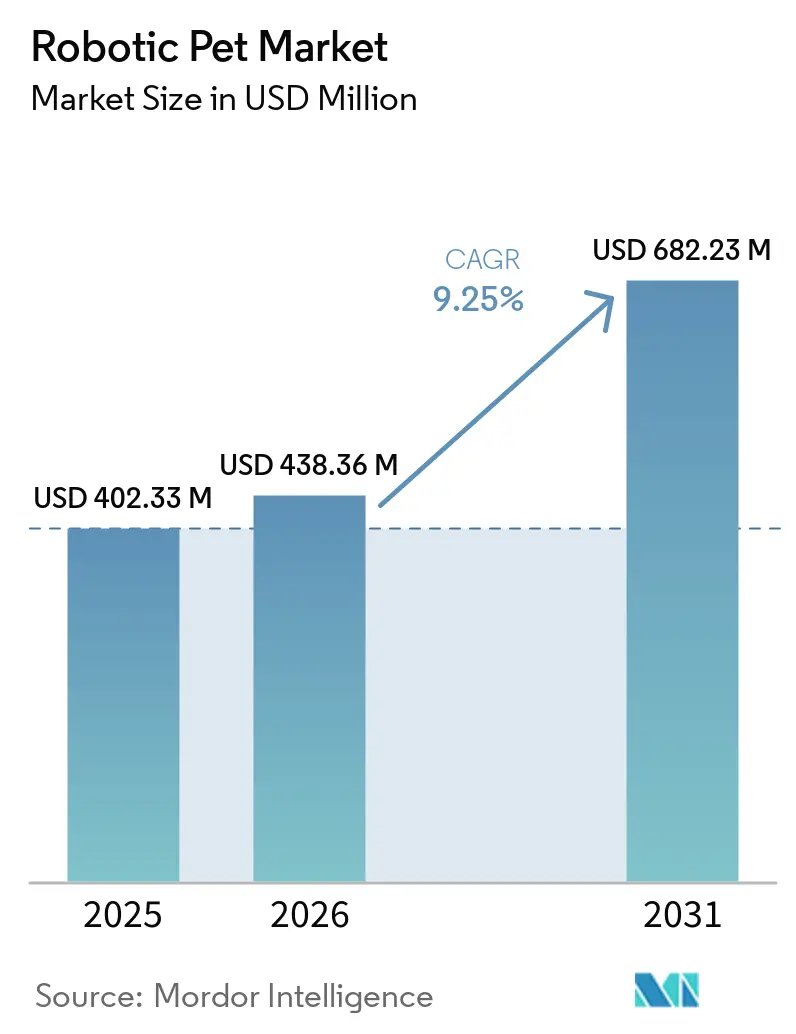

The Robotic Pet Market size is projected to be USD 402.33 million in 2025, USD 438.36 million in 2026, and reach USD 682.23 million by 2031, growing at a CAGR of 9.25% from 2026 to 2031.

Adoption drivers have shifted from novelty toward validated therapeutic use and eldercare workload relief, which changes purchase criteria and budget justification inside care ecosystems. Demographic aging, persistent loneliness among seniors, and caregiver shortages now direct institutional demand, while consumer awareness builds around evidence-based benefits in dementia care and stress reduction. Regulatory programs in Asia, including pilots for intelligent elderly-care robots, help lower adoption risk for providers and local authorities, which in turn accelerates procurement and informs design and data-handling standards. Companies with medical-device positioning and privacy-by-design workflows are better placed to win clinical and home-care channels, while direct-to-consumer storefronts support product education and long-term engagement. Hardware advances in sensors and on-device AI make mid-range units feel more responsive, yet total cost of ownership, privacy compliance, and runtime constraints still shape value-for-money perceptions in the robotic pet market.

Key Report Takeaways

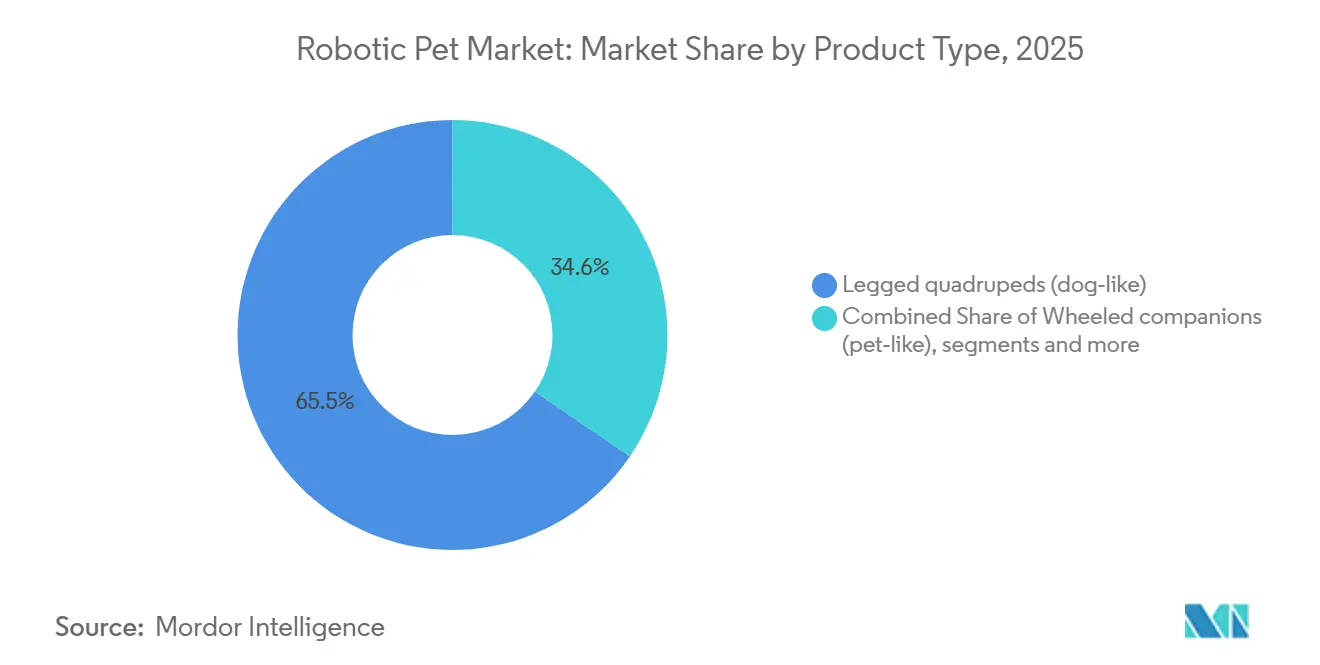

- By product type, legged quadrupeds led with 65.45% revenue share in 2025 and are projected to expand at an 11.23% CAGR through 2031.

- By application, households accounted for 45.90% share in 2025, while eldercare and nursing facilities are projected to grow at a 10.65% CAGR through 2031.

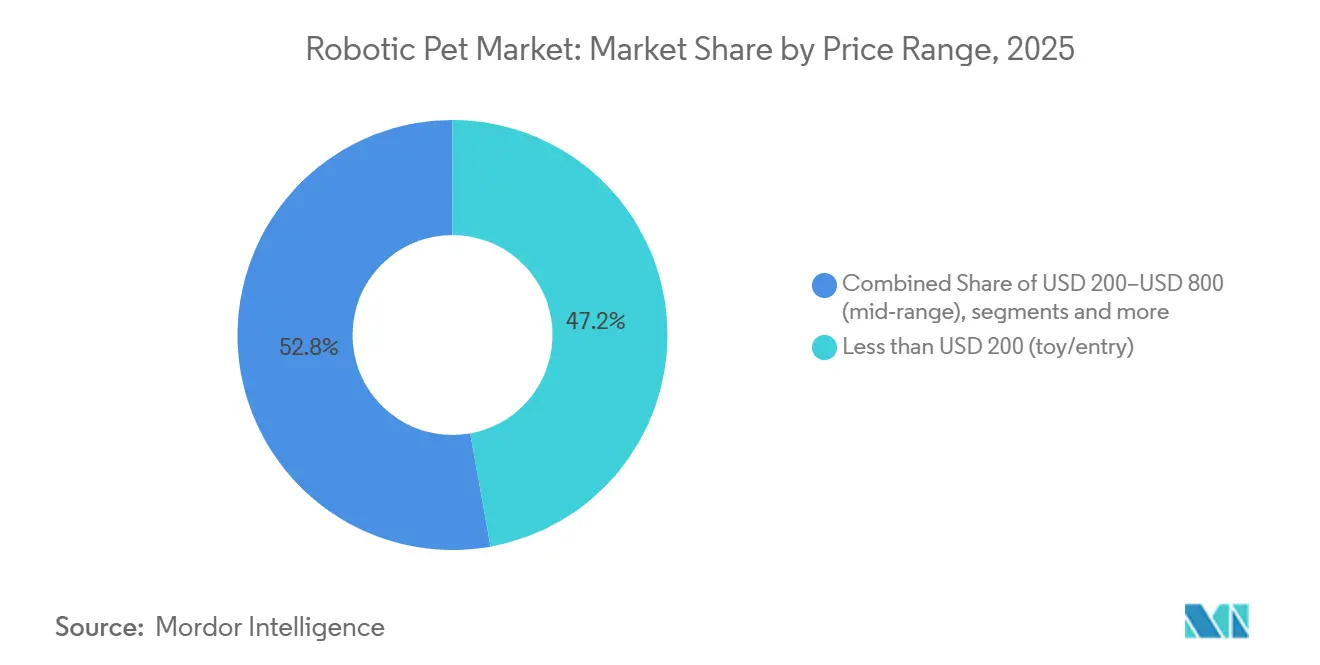

- By price range, the under-USD-200 tier captured 47.18% of unit volume in 2025, and the USD 800 to USD 2,000 segment is projected to register a 10.91% CAGR through 2031.

- By distribution channel, online marketplaces held a 70.13% share in 2025, while direct-to-consumer channels are projected to grow at an 11.23% CAGR through 2031.

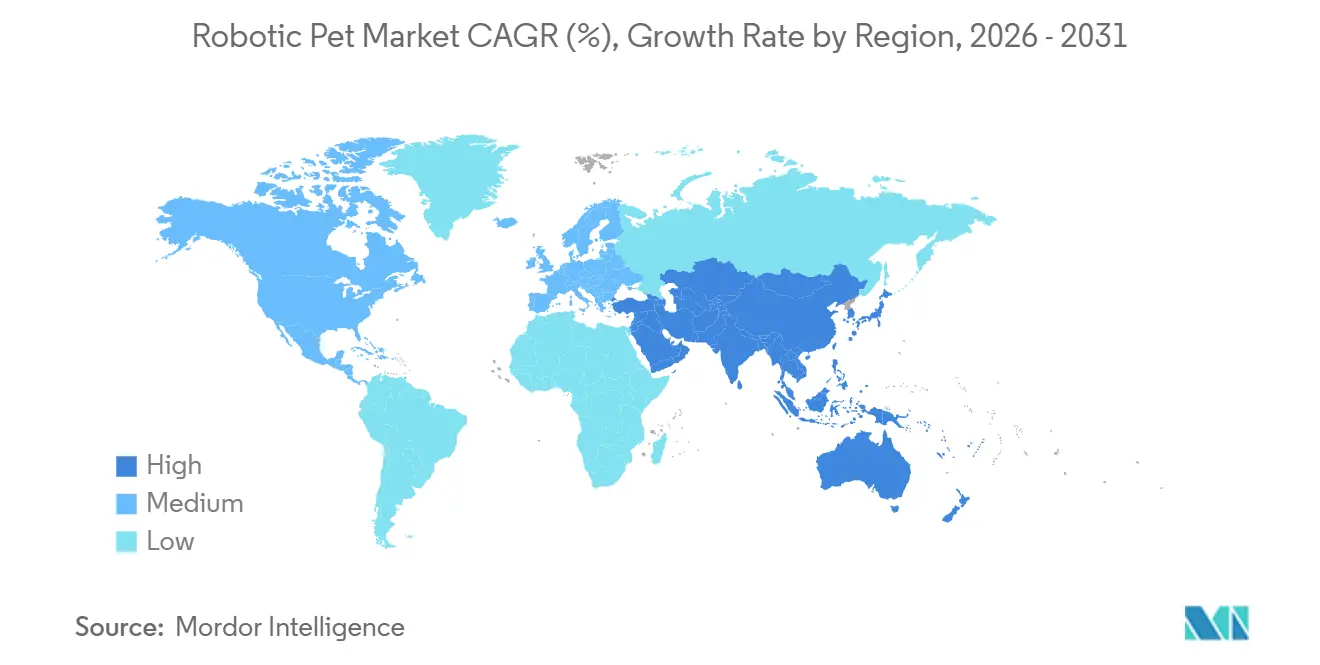

- By geography, North America held a 45.78% share in 2025, while Asia-Pacific is projected to grow at a 10.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Robotic Pet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population and Loneliness Driving Companion Adoption | +2.8% | Global, spikes in Japan, China, North America | Medium term (2-4 years) |

| Clinical Validation for Dementia/Autism Supports Therapeutic Use | +2.1% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| AI, Sensors, and Actuator Cost Curve Lowers the Bill of Materials | +1.9% | Global, led by China manufacturing | Short term (≤ 2 years) |

| E-commerce and Crowdfunding Accelerate Go-to-Market | +1.2% | Global, strongest in North America, APAC | Short term (≤ 2 years) |

| Government Subsidies and Pilots for Care and Communication Robots | +0.9% | China, Japan, select EU markets | Long term (≥ 4 years) |

| Quadruped Price Drops Unlock Prosumer “Pet” Use Cases | +0.4% | China core, spill-over to North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population and Loneliness Driving Companion Adoption

A sustained rise in the 65-plus population in large markets boosts institutional and at-home demand for companionship technologies that can mitigate social isolation and support routine engagement[1]Xinhua News Agency, “Across China: Futuristic robot ‘pets’, silent partners in the symphony of everyday life,” Xinhua, english.news.cn. Public discourse and national media coverage in China highlight the eldercare burden and the role of new robotic companions as part of a wider response to caregiver shortages and rising care needs. This demographic push elevates the robotic pet market beyond novelty and positions companions as a scalable, lower-cost supplement to human interaction in care settings. Policymakers and local health providers are piloting solutions that can reach residents at home and in facilities with consistent interaction patterns, which support longitudinal use. These initiatives help normalize procurement and accelerate learning curves for integration into daily routines, which sustains momentum in the robotic pet market.

Clinical Validation for Dementia and Autism Supports Therapeutic Use

Validated outcomes for non-pharmacological interventions guide hospitals and long-term care facilities to consider robotic companions for stress reduction, agitation management, and social engagement in dementia care. PARO, a therapeutic seal robot developed in Japan, has been positioned as a medical device in the United States, and program evaluations in national health systems in Europe signal growing confidence in the approach. The evidence context encourages consistent session design and staff training, which raises the standard for feature sets such as touch sensitivity, lifelike responses, and safe materials. As therapeutic claims enter procurement language, vendors differentiate with documentation, caregiver training materials, and integration support for multi-week engagement plans. The resulting clarity draws a line between toy-grade novelty and care-ready devices, and it positions the robotic pet market for deeper penetration in clinical and eldercare channels.

AI, Sensors, and Actuator Cost Curve Lowers the Bill of Materials

Rapid improvements in sensing, compute efficiency, and local AI inference allow more natural interaction at lower price points, which broadens the reachable user base for entry and mid-range categories. Manufacturers that integrate perception sensors and robust motion control can deliver more autonomy and reliability, which improves user satisfaction over longer ownership periods. As on-device models handle wake-words, simple dialog, and gesture recognition, latency improves and privacy risks may decrease, which supports use in homes and care facilities. Progress in commodity components reduces the threshold for new entrants in the robotic pet market, while established brands use these gains to add premium features or extend warranties. This hardware and software tailwind intersects with public-sector pilots and care-provider interest in scalable engagement tools, which creates a supportive demand environment.

Government Subsidies and Pilots for Care and Communication Robots

Policy pilots in Asia provide funding mechanisms, target cohorts, and verification periods that lower risk for providers and nurture supply ecosystems. The joint pilot program from China’s Ministry of Civil Affairs and the Ministry of Industry and Information Technology sets explicit scenarios for emotional companionship, monitoring, and early-warning systems, which guides vendors on product scope and compliance expectations. Required deployment sizes and verification timelines help produce comparable evidence across communities, which accelerates learning and iteration cycles for both vendors and care operators. Public networks that coordinate pilots share best practices on training and workflow integration, which shortens adoption curves and improves outcomes. Over time, these pilots may inform broader reimbursement or subsidy frameworks, which would further stabilize institutional demand in the robotic pet market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership (Device + Subscriptions) | -1.4% | Global, acute in premium segments | Medium term (2-4 years) |

| Limited Runtime and Maintenance or Repair Friction | -0.9% | Global, worse in industrial applications | Short term (≤ 2 years) |

| Vendor Longevity and Cloud-Dependency Risk | -0.7% | North America, Europe | Long term (≥ 4 years) |

| Child Data Privacy Constraints in Connected Companions | -0.5% | EU, North America, UK | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership (Device + Subscriptions)

Premium devices can require ongoing service plans to access full functionality, which raises multi-year ownership costs relative to the advertised base price. For example, Sony aibo owners can add a cloud plan that supports personality development and content features, which increases the effective spend over the lifetime of the product. Subscription renewals, accessories, and battery replacement cycles add to this burden, and this pushes buyers to favor transparent pricing and reliable warranty support. Device repair and logistics costs also impact international buyers, who may face shipping fees, customs charges, and delays during after-sales service. Companies in the robotic pet market that design for longevity, modular servicing, and clear subscription value see fewer objections in procurement and consumer channels. Pricing clarity, local repair networks, and predictable software roadmaps can mitigate hesitation in higher-value segments where return on engagement must be demonstrable.

Child Data Privacy Constraints in Connected Companions

Regulators require privacy-by-default and strong parental consent flows for connected toys that collect or process children’s data, which increases engineering overhead for device makers. The UK’s Age Appropriate Design Code prescribes data minimization, geolocation off by default, and avoidance of nudging designs that push children toward sharing personal information, which affects UX and data architecture choices. In the United States, the Federal Trade Commission enforces the Children’s Online Privacy Protection Act, including actions related to improper transmission of precise geolocation data without verifiable parental consent, which underscores vendor responsibility for embedded SDKs and supply-chain components. These requirements can slow release cycles for companion devices that rely on conversation logs or cloud processing for learning features. Makers in the robotic pet market address this with greater on-device processing, retention caps, and stricter vendor access controls, which improve compliance but add cost. Clear privacy notices, transparent data flows, and parental dashboards support trust and reduce regulatory exposure in family settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Legged Quadrupeds Dominate, Commanding Two-Thirds Share

Amid Industrial Crossover Legged quadrupeds captured 65.45% of the robotic pet market share in 2025 and are projected to expand at an 11.23% CAGR through 2031. This trajectory reflects how mobility and terrain handling attract prosumers and institutions that want inspection, patrol, or therapy-adjacent engagement, which raises visibility at the higher-performance end of the category.

The robotic pet market now benefits from stronger sensing stacks and motion control that reduce collisions and improve confidence in unattended operation. Institutions with mixed indoor and outdoor use favor platforms that navigate thresholds, ramps, and variable flooring, which keeps quadrupeds at the front of product discussions for more demanding settings. The robotic pet market also sees spillovers from service-robot ecosystems in Asia, where component suppliers and integrators accelerate iteration cycles and reduce time to market for legged designs.

As price-performance improves, quadrupeds that achieve quiet operation, safe torque limits, and recoverable falls see higher acceptance in homes and care facilities. Vendors who offer well-documented APIs and developer kits can extend use into education and research labs that treat quadrupeds as learning platforms. This creates a flywheel in the robotic pet market where education, hobbyist projects, and public pilots amplify awareness across the full product spectrum.

By Application: Households Lead Volume, Eldercare Sprints in Growth as Reimbursement Unlocks Institutional Spend

Households accounted for 45.90% share of the robotic pet market size in 2025, while eldercare and nursing facilities are projected to grow at a 10.65% CAGR through 2031. Families adopt companions for structured play, social presence, and allergy-safe alternatives to living pets, which provides a steady volume base for entry and mid-tier devices. The eldercare segment builds momentum as validated therapeutic companions help reduce agitation and support calming routines in dementia care. European health programs have evaluated robotic therapy with PARO in institutional settings, reinforcing confidence among clinicians and administrators who want non-pharmacological tools for behavior management[2]Portal InovarSaúde Editorial Team, “Impact of Robotherapy-PARO on Elderly People With Dementia in Portugal,” Portal InovarSaúde, inovarsaude.min-saude.pt. Government-backed pilots in Asia define scenarios around emotional companionship and early-warning systems, which align well with eldercare use cases and accelerate operational learning.

Household usage patterns emphasize intuitive setup and reliable autonomy within living spaces, which favors companions that combine simple navigation and responsive interaction. Care facilities look for easy-to-clean materials, repeatable session workflows, and consistent behavior, which pushes vendors to include staff training and documented protocols. The robotic pet market sees platform differentiation between devices that target playful daily companionship and those that prioritize measurable therapeutic goals. As adoption grows, cross-over use emerges where home-care agencies bring companions to client visits, which raises multi-setting familiarity and supports broader acceptance. These dynamics keep households as the largest segment while eldercare and nursing facilities set the pace for growth.

By Price Range: Entry Tier Holds Volume, Premium Segment Grows Fastest as Autonomy Demands Bill-of-Materials Depth

The under-USD-200 tier represented 47.18% of the robotic pet market size in unit terms in 2025, while the USD 800 to USD 2,000 segment is projected to register a 10.91% CAGR through 2031. Entry devices serve gift buyers and first-time users, and they reduce frictions for families who want to test robotic companionship before committing to higher-performance models. Premium tiers advance with on-device AI, better tactile sensing, and longer runtimes that sustain day-to-day routines in care or learning settings. Pricing transparency and cost-of-ownership clarity matter more at higher price points where buyers examine subscriptions, accessories, and service terms. Sony’s aibo illustrates how premium devices align hardware, content, and cloud plans to enrich long-term engagement for owners and caregivers.

The robotic pet industry also sees device exclusives and limited editions to refresh demand and maintain brand distinctiveness. Vendors that balance accessible hardware with thoughtful software roadmaps can upsell premium features without fragmenting user experience. Families and institutions often weigh premium choices against service life and ease of repair, which favors designs with modular components and predictable maintenance. Company-operated e-commerce channels and education bundles help explain premium value propositions that depend on feature depth and support. These patterns reinforce a two-speed market, with price-led volume at the base and feature-led growth in the premium band.

By Distribution Channel: Online Marketplaces Dominate, Direct-to-Consumer Surges on Crowdfunding and Vertical Brand Storytelling

Online marketplaces held a 70.13% share in 2025, while direct-to-consumer channels are projected to grow at an 11.23% CAGR through 2031. Marketplace visibility helps price-sensitive buyers compare features and reviews, which benefits volume leaders in the entry and mid-range. Direct storefronts strengthen brand education and long-term engagement with owners through firmware updates, care guides, and accessory ecosystems. Product pages that clarify privacy practices, repair options, and software lifecycles build trust, especially for families and care providers. Brands that own the customer relationship can better support personalization and after-sales service, which elevates the perceived value of premium devices in the robotic pet market.

Casio sells the Moflin companion through its dedicated brand site, which concentrates product storytelling and allows controlled feature rollouts and service updates for owners. Company-operated channels also support structured trials, bundles, and education discounts that help place devices into classrooms and therapy sessions. Marketplace-only strategies risk margin erosion and limited differentiation, while hybrid approaches can capture both reach and depth. The robotic pet industry benefits when first-time buyers find clear upgrade paths and when owners receive consistent support over multi-year periods. This is why direct-to-consumer momentum complements marketplace dominance in the current cycle.

Geography Analysis

North America accounted for a significant 45.78% share of the market in 2025. This dominance is attributed to the increasing demand for therapeutic companionship solutions, particularly for seniors managing conditions such as dementia and Alzheimer’s. The United States and Canada are the primary contributors to this trend, driven by high adoption rates of advanced technologies and elevated levels of disposable income. The robotic pets available in the market today are equipped with advanced features, including enhanced artificial intelligence (AI), machine learning capabilities, cloud-based learning systems, and multi-modal interaction functionalities such as voice recognition and tactile sensors. These technological advancements are enabling the development of more effective and interactive solutions, further driving market growth in the region.

Asia-Pacific is projected to grow at a 10.56% CAGR through 2031. Public pilots in China specify core scenarios for care robots and set minimum deployment thresholds, which build shared vocabulary across agencies, providers, and vendors[3]Ministry of Industry and Information Technology and Ministry of Civil Affairs, “Pilot work notice on intelligent elderly-care service robots,” China National Working Commission on Ageing (CRCA), crca.cn. The region’s manufacturing base and engineering talent pool shorten development cycles and increase the variety of form factors, which helps match devices to use cases across price points. Japan’s clinical orientation and Europe’s privacy-centered approach influence design blueprints that can be applied globally, especially in eldercare contexts.

Europe applies strict child-privacy principles and expects privacy by design in connected devices, which affects companion features that log or analyze children’s voices and behavior. Therapeutic use in hospitals and care facilities in Europe supports interest in validated devices that demonstrate calming and social benefits, which strengthens the case for institutional procurement. North America’s share reflects strong consumer electronics adoption and a growing awareness of therapy-ready companions for older adults. Over time, coverage policies and clinical protocols could shape household penetration, which keeps stakeholders attentive to outcomes data and device safety.

Competitive Landscape

Competition spans toy-grade companions, therapeutic devices, and prosumer quadrupeds, which diffuses share across many brands and feature sets. Premium vendors use device design, content ecosystems, and after-sales service to defend margins as component cost curves improve in lower tiers. Companies with clinical positioning provide care protocols and training materials that translate into predictable sessions and measurable outcomes for providers, which solidifies institutional trust. Manufacturers that disclose privacy controls and age-appropriate design decisions win favor among families and schools, which reduces friction during onboarding. The robotic pet market rewards vendors that pair reliable hardware with transparent service lifecycles and clear data-handling policies.

Strategic moves in 2025 and 2026 underscore the importance of product refreshes and channel control in higher-value tiers. Sony introduced the Kinako edition for aibo in the United States in 2025, which signaled continued investment in premium companionship and content-enabled engagement. Sony also supports long-term experiences through optional cloud plans and accessories, which deepens owner attachment and stabilizes recurring revenue in the premium band. Casio promotes the Moflin companion via its own site, which allows feature control, customer education, and community building without marketplace constraints. These examples reflect a broader pattern where premium brands emphasize direct channels to protect positioning and to deliver predictable firmware and service updates.

Public-sector pilots influence roadmaps and expected capabilities. China’s pilot program names emotional companionship and monitoring among priority scenarios for elderly-care robots and sets minimum deployment and verification requirements, which gives vendors clear targets for device design and field testing. Media coverage in China continues to amplify interest in robotic companions for daily life, which supports social acceptance and user curiosity. As component ecosystems mature, prosumer quadrupeds and therapy-focused companions each push fit-for-purpose features, which sustains variety across price bands. Over time, privacy assurances, service reliability, and clear clinical positioning will separate leaders in the robotic pet market.

Robotic Pet Industry Leaders

Ageless Innovation

Elephant Robotics

KEYi Technology

Sony

Unitree Robotics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: China’s Ministry of Civil Affairs and Ministry of Industry and Information Technology launched a three-year pilot program for intelligent elderly-care service robots, naming emotional companionship as a core application and requiring minimum deployments with multi-month verification.

- June 2025: Hengbot Innovation Ltd. introduced its first product, Sirius, within the Hengbot Universe. Sirius, an AI-powered robotic dog, gained significant attention at CES 2025 for its advanced multimodal interaction capabilities and superior dynamic motion performance. Utilizing cutting-edge AI models, Sirius is positioned as the first fully customizable and programmable robotic dog, enabling consumers to design and develop their personalized robotic solutions from the ground up.

Global Robotic Pet Market Report Scope

As per the scope of the report, robotic pets are engineered to replicate the appearance and behavior of real animals, serve as a solution for companionship and emotional support without the challenges of maintaining a live pet. These AI-driven, biomimetic machines leverage advanced sensors to interact with touch, sound, and light, effectively simulating pet-like behaviors such as barking, purring, or moving.

The robotic pet market is segmented by product type, application, price range, distribution channel, and geography. By product type, the market is segmented as legged quadrupeds (dog‑like), wheeled companions (pet‑like), and stationary plush robotic companions (e.g., seal, cushion). By application, the market is segmented as households, eldercare/nursing and long‑term care, hospitals/healthcare and therapy, education & research, and retail/experiential / visitor attractions. By price range, the market is segmented as less than USD 200 (toy/entry), USD 200–USD 800 (mid‑range), USD 800–USD 2,000 (premium), and greater than USD 2,000 (ultra‑premium/prosumer). By distribution channel, the market is segmented as retail/toy chains, online marketplaces, direct‑to‑consumer online, and business-to-business (B2B). By geography, the market is segmented as North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Legged quadrupeds (dog‑like) |

| Wheeled companions (pet‑like) |

| Stationary plush robotic companions (e.g., seal, cushion) |

| Households |

| Eldercare / nursing and long‑term care |

| Hospitals / healthcare and therapy |

| Education & research |

| Retail / experiential / visitor attractions |

| Less than USD 200 (toy/entry) |

| USD 200–USD 800 (mid‑range) |

| USD 800–USD 2,000 (premium) |

| Greater than USD 2,000 (ultra‑premium / prosumer) |

| Retail/Toy Chains |

| Online Marketplaces |

| Direct‑to‑Consumer Online |

| Business-to-Business (B2B) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Legged quadrupeds (dog‑like) | |

| Wheeled companions (pet‑like) | ||

| Stationary plush robotic companions (e.g., seal, cushion) | ||

| By Application | Households | |

| Eldercare / nursing and long‑term care | ||

| Hospitals / healthcare and therapy | ||

| Education & research | ||

| Retail / experiential / visitor attractions | ||

| By Price Range | Less than USD 200 (toy/entry) | |

| USD 200–USD 800 (mid‑range) | ||

| USD 800–USD 2,000 (premium) | ||

| Greater than USD 2,000 (ultra‑premium / prosumer) | ||

| By Distribution Channel | Retail/Toy Chains | |

| Online Marketplaces | ||

| Direct‑to‑Consumer Online | ||

| Business-to-Business (B2B) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the growth outlook for the robotic pet market through 2031?

The category is projected to grow from USD 438.36 million in 2026 to USD 682.23 million by 2031 at a 9.25% CAGR, supported by therapeutic adoption and eldercare pilots.

Which applications are set to scale fastest within the robotic pet market?

Eldercare and nursing facilities are projected to grow at a 10.65% CAGR through 2031 as validated therapeutic use and public pilots support institutional procurement.

Which product type currently leads the robotic pet market?

Legged quadrupeds led with 65.45% of 2025 revenue and are projected to grow at an 11.23% CAGR through 2031 on the strength of mobility and perception advances.

Which regions will drive growth in the robotic pet market over the forecast?

Asia-Pacific is projected to lead growth at a 10.56% CAGR through 2031 as public pilots scale deployments, while North America held a 45.78% share in 2025.

Page last updated on: