Stone Plastic Composite Flooring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

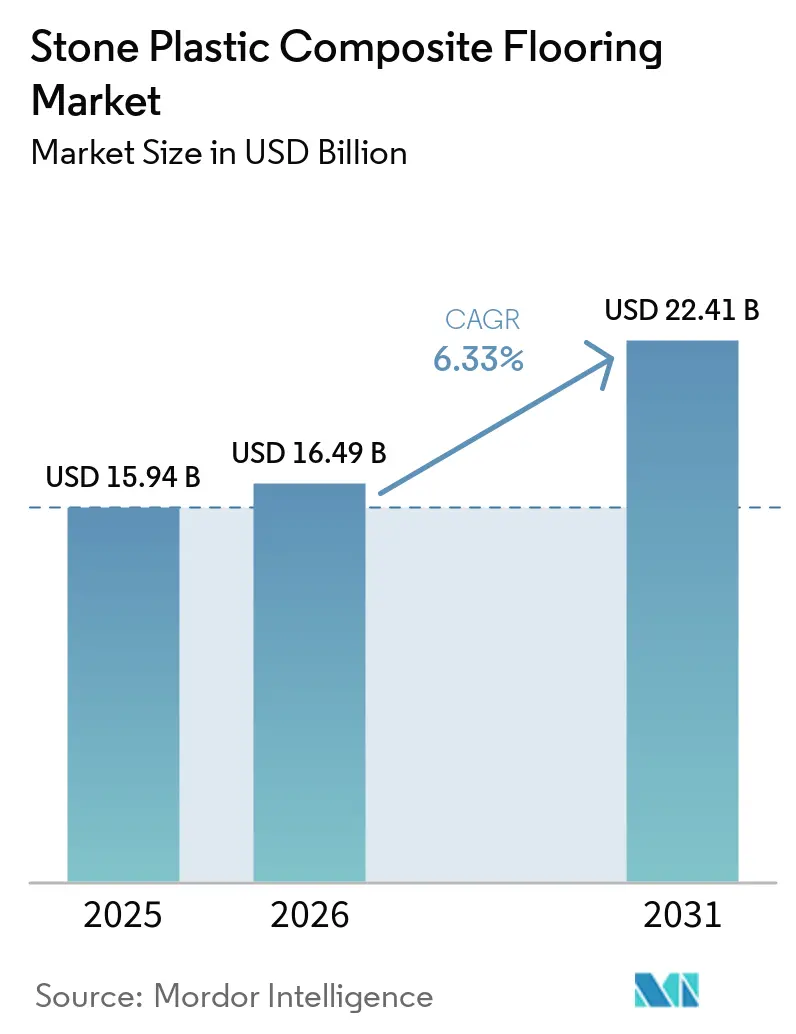

| Market Size (2026) | USD 16.49 Billion |

| Market Size (2031) | USD 22.41 Billion |

| Growth Rate (2026 - 2031) | 6.33% CAGR |

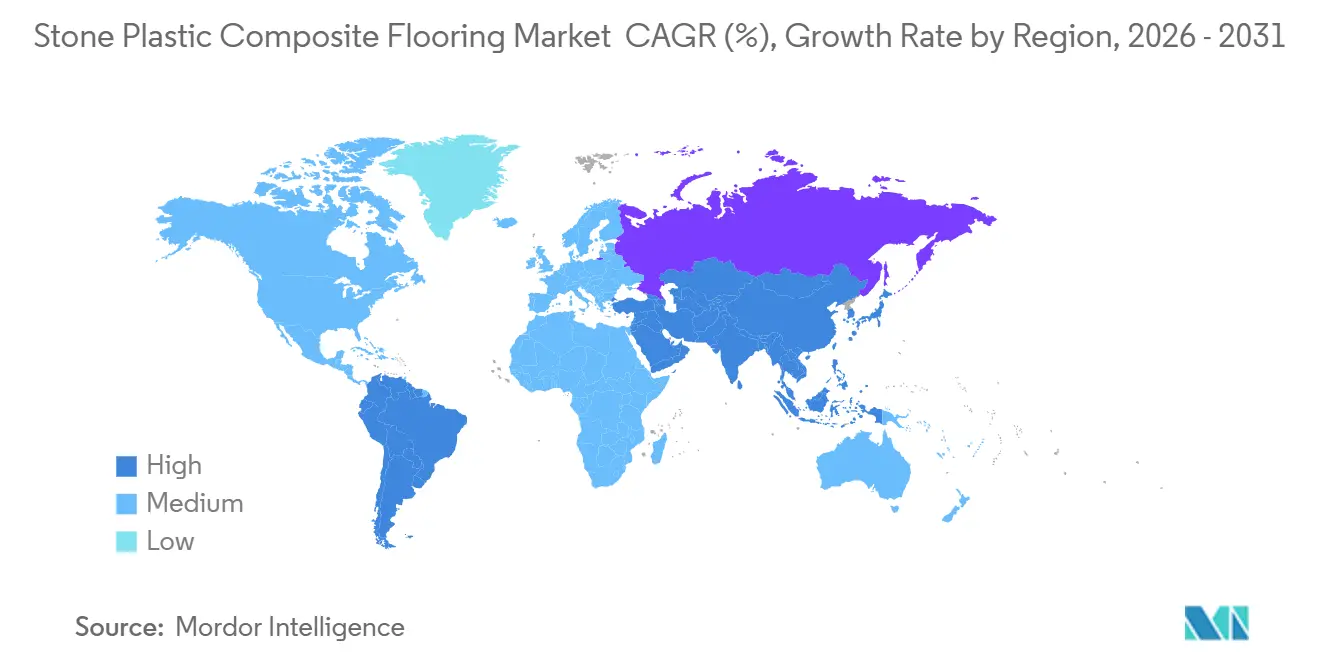

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

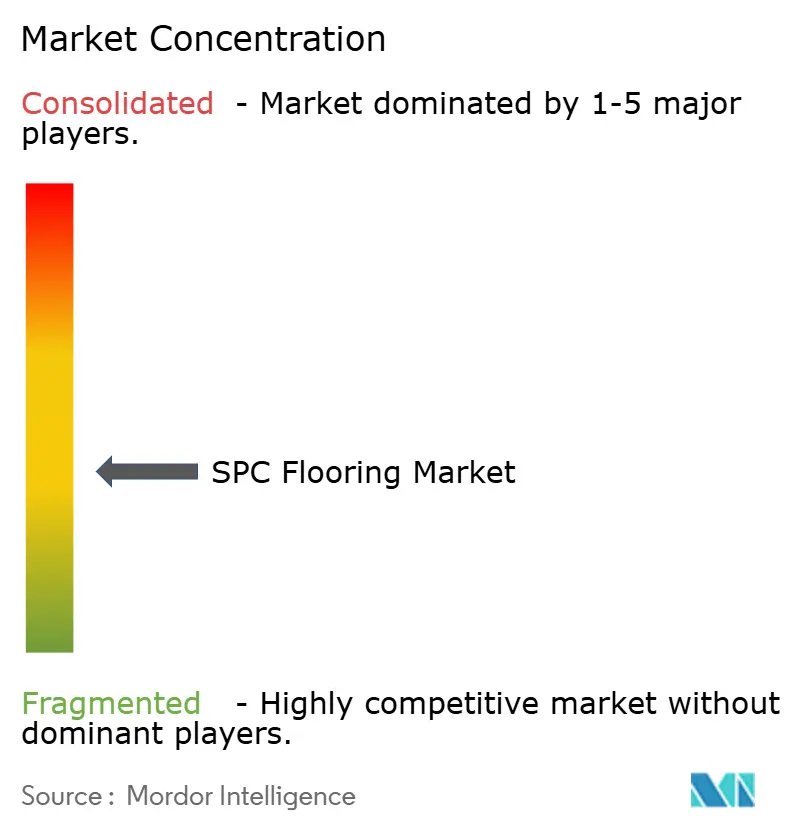

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stone Plastic Composite Flooring Market Analysis by Mordor Intelligence

The stone plastic composite flooring market size stood at USD 16.49 billion in 2026, up from USD 15.94 billion in 2025, and is projected to reach USD 22.41 billion by 2031 at a 6.33% CAGR. Rapid adoption in moisture-prone residential spaces and light-commercial areas continues as waterproof rigid-core formats displace flexible LVT and laminate, supported by click-lock systems that speed installation and reduce downtime. The stone plastic composite (SPC) flooring market is also benefiting from localized capacity expansions and diversified sourcing that improve delivery times and mitigate logistics risk in North America and Europe. Trade actions in Europe and the UK have reshaped resin and finished goods flows, encouraging nearshoring and the qualification of alternative suppliers by leading manufacturers. Facility managers and property owners favor SPC for faster turnover, acoustic compliance options, and lifecycle cost benefits in retail, healthcare, and multi-family settings. Building-code sound transmission requirements in the United States continue to reinforce the use of rigid-core assemblies with appropriate underlay to meet minimum Impact Insulation Class(IIC) and Sound Transmission Class (STC) thresholds in multi-unit dwellings.

Key Report Takeaways

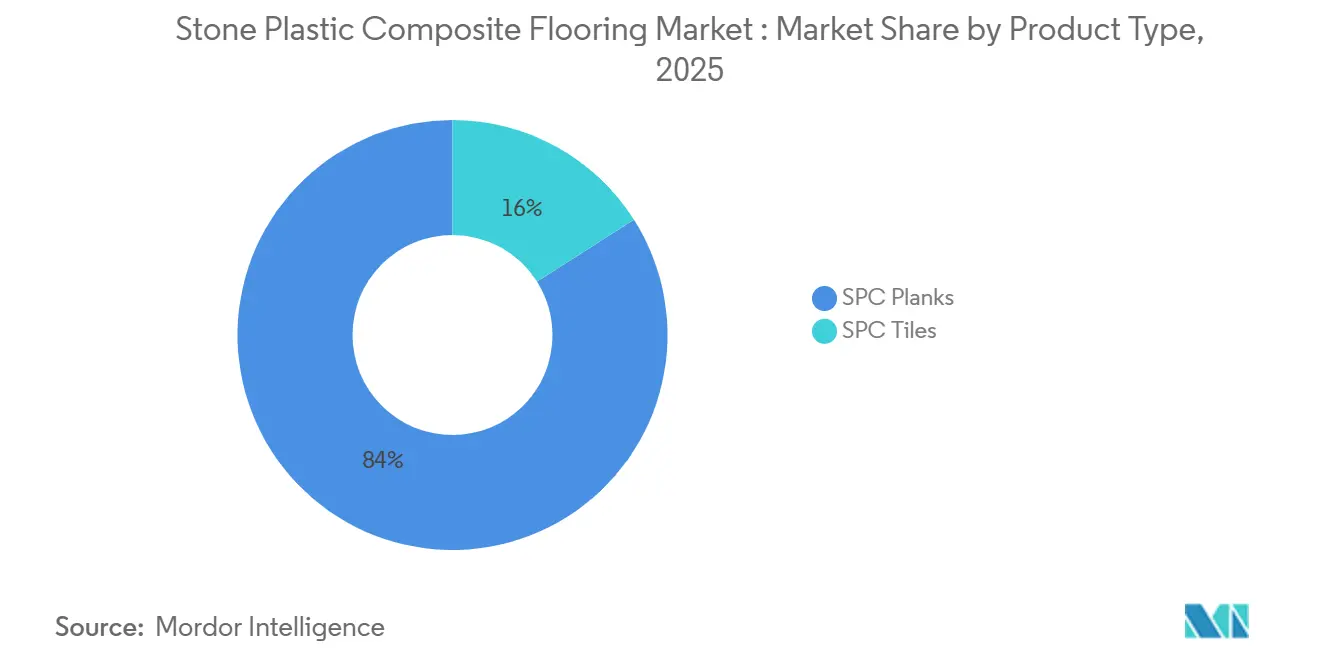

- By product type, SPC planks led with 84.0% share in 2025. By product type, planks are projected to grow at an 8.03% CAGR through 2031.

- By product thickness, 4.0-5.0 mm accounted for 43.7% of the market share in 2025. By product thickness, 5.1-6.0 mm is expected to record a 9.23% CAGR through 2031.

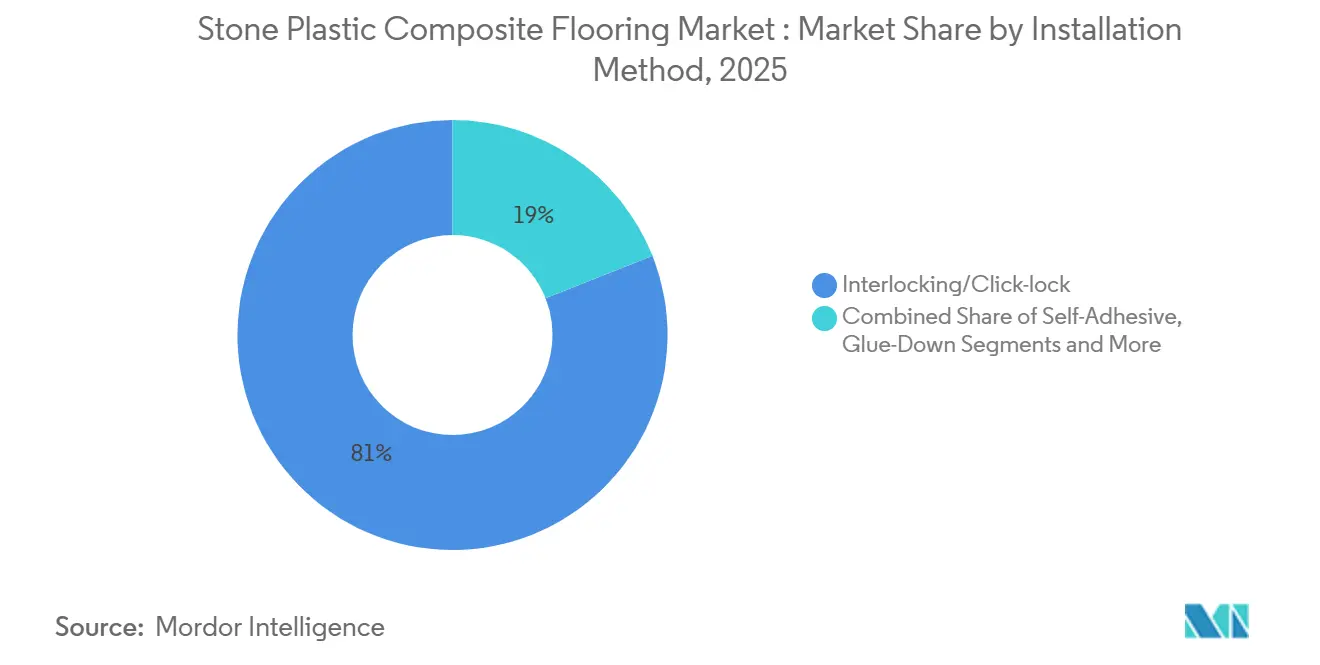

- By installation method, interlocking or click-lock captured 89.0% of the market share in 2025. By installation method, interlocking or click-lock is projected to expand at an 8.50% CAGR through 2031.

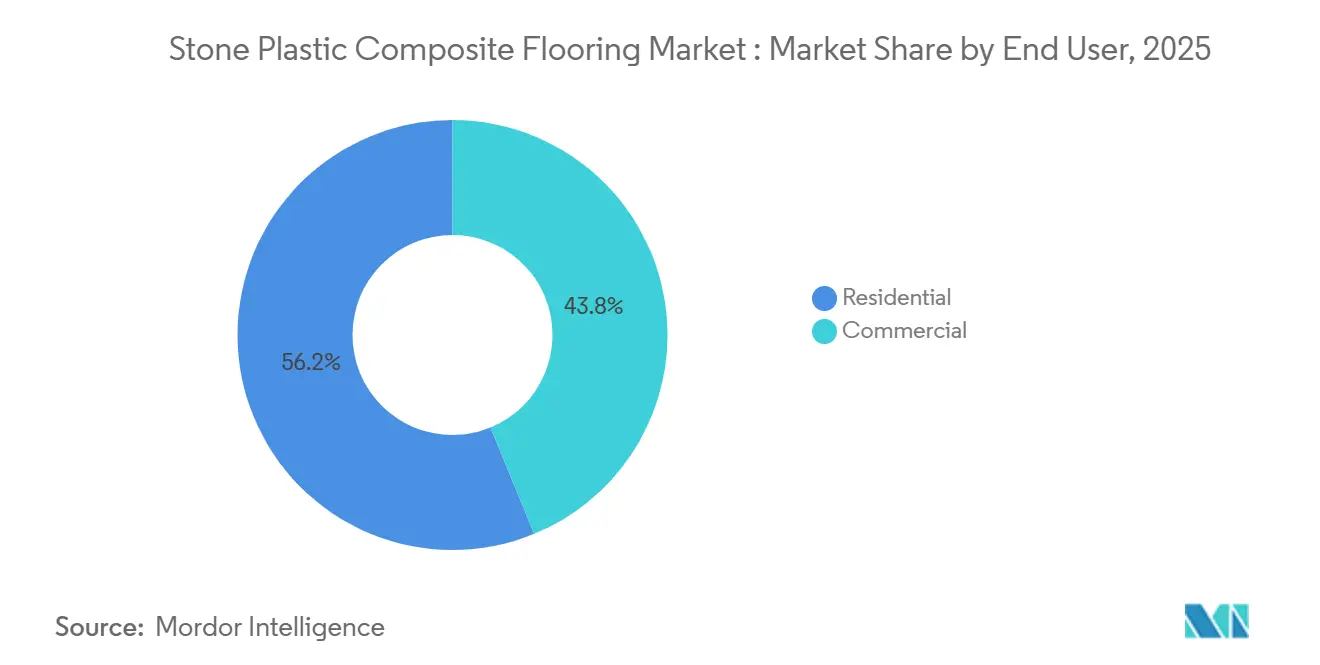

- By end user, residential accounted for 56.21% of the market share in 2025. By end user, commercial is forecast to grow at a 9.50% CAGR through 2031.

- By distribution channel, specialty flooring retailers within the B2C/retail segment accounted for 38.49% of market share in 2025. By distribution channel, online direct-to-consumer within B2C/retail is set to grow at a 10.16% CAGR through 2031.

- By geography, North America led with 35.88% share in 2025. By geography, Asia-Pacific is projected to post a 9.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Stone Plastic Composite Flooring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Waterproof rigid-core replaces laminate and flexible LVT in home and light commercial | +1.8% | North America, Western Europe, and urbanized Asia-Pacific | Medium term (2-4 years) |

| DIY-friendly click-lock and renovation-led demand | +1.5% | North America, Western Europe, and expanding to APAC | Short term (≤ 2 years) |

| Price-to-performance vs wood and tile | +1.2% | Asia-Pacific, India, Southeast Asia, Latin America | Medium term (2-4 years) |

| Multi-family and rental refresh cycles | +0.9% | North America metros, Western European cities | Medium term (2-4 years) |

| Tariff-driven supply shifts expand localized availability and specs | +0.6% | U.S. and EU import markets | Short term (≤ 2 years) |

| Fast-turn commercial fit-outs valuing minimal downtime | +0.7% | Global commercial hubs in retail, hospitality, and healthcare | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Waterproof Rigid-Core Replacing Laminate and Flexible LVT in Home and Light Commercial

The SPC flooring market continues to gain share in kitchens, bathrooms, basements, and light-commercial areas where 100% waterproof rigid cores and durable wear layers reduce failure risk associated with swelling or moisture ingress in other materials. Traditional laminate flooring, for example, can swell by 6–12% in thickness after prolonged water exposure, whereas SPC products typically show negligible dimensional change under similar conditions, as determined by standardized water-immersion and stability tests (e.g., American Society for Testing and Materials methods). Click-lock construction enables fast floating installations that require no adhesive cure, supporting phased occupancies and overnight retail refits that minimize lost trading hours. Installation productivity for click systems typically ranges from 20-40 m² per installer per day, compared with 10-20 m² for glued flooring systems due to adhesive application and curing requirements. This speed-to-service benefit makes SPC flooring compelling in healthcare and hospitality corridors where installations must proceed under tight schedules and enable immediate or same-day walk-on use, unlike adhesive-based resilient flooring, which may require 24-48 hours before full service. In commercial interiors, rigid-core options serve as resilient alternatives where wood or tile would extend timelines or increase maintenance demand. Ceramic tile installations, for instance, often require 2-3 days for setting and grout curing, while hardwood installations involve acclimation periods of 3-7 days depending on site conditions. By contrast, SPC flooring can be installed without acclimation in many cases due to its dimensional stability.

DIY-Friendly Click-Lock and Renovation-Led Demand Spike

Homeowners are drawn to the SPC flooring market because click-lock systems reduce tool requirements and eliminate the need for adhesives, bringing installation within reach for proficient DIY renovators. The ability to install over many existing hard surfaces without demolition also shortens project duration and reduces overall project disruption. Renovation cycles have therefore favored rigid-core products for single-weekend room refreshes and fast kitchen or bath upgrades that must be ready for immediate use. This pattern is reinforced by supplier content that emphasizes simplified installs, subfloor tolerances, and acclimation guidance that help non-professionals achieve reliable outcomes. The commercial side benefits from the same friction reduction, which compresses fit-out schedules for small offices, clinics, and boutique retail while keeping spaces open for business sooner after install.

Price-to-Performance vs Wood/Tile Expands Addressable Market

The SPC flooring market stands out for delivering the look of wood and stone with waterproof resilience and simplified care, which broadens its appeal in settings that do not tolerate extended downtime or intensive maintenance. SPC rigid cores typically show <0.1% dimensional change under water exposure (ASTM testing), compared with hardwood movement of 3-8% across grain with moisture variation, supporting use in wet-prone environments. Floating installations avoid adhesives in most applications and are compatible with phased construction, with installation rates of 20-40 m² per installer per day versus 10-20 m² for glue-down systems, lowering labor friction relative to traditional tile or site-finished wood surfaces. Commercial guides now frame rigid-core as a practical alternative for retail, office, and healthcare interiors when lifecycle costs and uptime are the decision anchors. Durability is supported by wear layers of 0.3-0.7 mm, with products meeting Class 32-34 commercial ratings (EN 13329) for heavy traffic use. The category’s maturation has also been supported by association-issued EPDs aligned with International Organization for Standardization frameworks and program operators such as UL Solutions, helping specifiers compare environmental metrics within and across resilient categories. As spec teams expand beyond single-material loyalty, the SPC flooring market captures projects where a durable, waterproof, and design-consistent surface can be installed on tight schedules.

Growth of Multi-Family and Rental Refresh Cycles

The SPC flooring market aligns well with multi-family turnover, where unit readiness and acoustic compliance are recurring priorities. Building codes in the United States commonly require minimum Impact Insulation Class (IIC) and Sound Transmission Class (STC) ratings of 50 for floor–ceiling assemblies (per ASTM E492 and E90 test methods), with field-tested thresholds often set at 45, and rigid-core assemblies paired with 1-2 mm acoustic underlayments can achieve IIC/STC improvements of 10–20 points, helping projects conform without heavier multi-component systems. These assemblies can be installed quickly in occupied buildings during short vacancy windows, with floating SPC installation rates of 20-40 m² per installer per day, helping keep rent loss and labor costs contained. For property managers, resilient surfaces that are waterproof and easy to clean reduce complaints and labor time after move-outs, as SPC demonstrates <0.1% dimensional change under moisture exposure (ASTM testing) and resistance to staining compared with porous materials. Turnover cleaning and repair cycles can be shortened by several hours per unit, and flooring replacement can be completed within 1-2 days per apartment, supporting predictable refresh schedules. As leasing teams market quiet and easy-care interiors, rigid-core options support those positioning goals for both new construction and refreshes, with typical wear layers of 0.3–0.5 mm supporting Class 32–33 residential and light-commercial ratings (EN 13329).

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PVC sustainability scrutiny and circularity barriers | -0.8% | Europe, North America, and the affluent APAC | Long term (≥ 4 years) |

| Feedstock price volatility for PVC resin and additives | -1.1% | Global, with pressure in import-dependent regions | Short term (≤ 2 years) |

| Acoustics and scratch resistance trade-offs vs WPC/laminate | -0.4% | Multi-family in North America and Western Europe | Medium term (2-4 years) |

| Tariffs and non-tariff barriers that raise landed costs | -0.9% | U.S. and EU import markets with global spillovers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Polyvinyl Chloride (PVC) Sustainability Scrutiny and Circularity/Recycling Barriers

Sustainability scrutiny remains a persistent headwind for the SPC flooring market, especially in Europe, where circular-economy targets and public procurement standards shape material selection. Plastics Recyclers Europe (PRE) has concluded that, despite decades of initiatives, certified post-consumer PVC recycling volumes in Europe remain well below overall waste generation, which underscores the gap between circular ambition and realized outcomes. As highlighted in the VinylPlus Progress Report (2024–2025), PVC recycling volumes have fluctuated year on year. Specifically, the total recycled volumes dipped from exceeding 737,000 tons in 2023 to approximately 724,000 tons in 2024, underscoring the challenges faced in the market and its structure. These realities have pushed manufacturers to document lifecycle impacts through EPDs and to offer reclamation initiatives for certain resilient lines. These steps improve transparency and ease participation in green building programs that value verifiable data. While such measures are expanding, current volumes of reclaimed or bio-attributed materials are small compared to total virgin throughput, which means specification decisions in the most sustainability-sensitive projects still weigh PVC content carefully[1]MDPI.COM https://www.mdpi.com/2071-1050/16/9/3854. European industry progress reports and new EPDs provide credible baselines for project teams that want to evaluate environmental performance more precisely and to plan end-of-life handling where infrastructure exists. Published category EPDs for rigid-core floors further help specifiers benchmark product-level impacts and documentation requirements. Company programs that offer resilient reclamation for qualifying projects demonstrate one practical route to reduce landfill disposal of installed products.

Feedstock Price Volatility (PVC Resin, Additives)

The SPC flooring market is exposed to swings in resin and additive costs that can compress converter margins and alter quotes within weeks, as PVC resin prices have historically moved by ±20-40% over 12 months in response to shifts in feedstock and energy costs. According to Tradeasia International Private Limited, in early 2026, global PVC conditions were characterized as a fragile recovery, with regional demand uneven and energy-linked feedstock dynamics limiting visibility into sustained price trends. Geopolitical developments that affect energy markets or key shipping routes can move ethylene-related feedstocks and freight costs in short order, with ocean freight rates on Asia-Europe lanes previously fluctuating by more than 3× between 2020 and 2024, raising procurement complexity for PVC-based categories. Such volatility often flows through to finished-goods pricing after a lag of 4-12 weeks, especially where spot resin sourcing dominates and where duties or freight surcharges shift landed costs for importers. Commercial buyers and distributors, therefore, balance indexed agreements with shorter fixed purchases, while also emphasizing formulation stability and production proximity where feasible[2]CHEMTRADEASIA.COM https://www.chemtradeasia.com/market-insights/why-pvc-resin-prices-remain-fragile-despite-short-term-recovery-signals. In parallel, episodic shipping disruptions have periodically tightened supply lines and lifted costs for materials moving from Asia to Europe and North America.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Planks Lead Residential, Tiles Gain in Commercial Mimicry

SPC planks held 84.00% of the 2025 market size and remain the default format for wood-look residential installations, and the segment is projected to expand at an 8.03% CAGR through 2031 as stone, terrazzo, and concrete visuals gain reach in commercial spaces within the SPC flooring market. The SPC flooring market share of plank formats reflects sustained homeowner preference for natural wood aesthetics paired with waterproof performance, and for floating installations that reduce disruption. Tiles are gaining popularity among designers who want large-format stone looks without the weight, cure time, or grout maintenance of ceramic or porcelain. In commercial settings, rigid-core tiles support overnight lobby and corridor upgrades with realistic visuals and immediate return to service.

Across residential and commercial projects, visuals and surface finishes continue to improve, reducing aesthetic trade-offs with natural materials. Wider and longer plank assortments deliver room-scale realism that was previously difficult to achieve with shorter lengths. For tiles, patterning options allow statement floors in hospitality and healthcare while maintaining the maintenance profile that resilient platforms are known for. The SPC flooring market benefits from a stable installation method that supports phased work, reduces adhesive use, and results in cleaner job sites. Commercial publications from manufacturers reinforce how rigid-core products can replace more labor-intensive surfaces where uptime is a scheduling constraint.

By Product Thickness: 4.0–5.0 mm Outpaces as Codes Tighten, Comfort Demands Rise

The 4.0-5.0 mm tier accounted for 43.67% of the SPC flooring market in 2025, yet 5.1-6.0 mm products are forecast to grow at a 9.23% CAGR through 2031, as project teams pursue higher acoustic ratings and a more cushioned feel underfoot in premium residential and multi-family settings. Thicker constructions with integrated underlayment help projects meet minimum code thresholds for IIC and STC without assembling multiple layers, reducing variables and simplifying documentation. For developers seeking stronger impact sound control, thicker single-SKU assemblies reduce the risk of mismatches between field conditions and lab-tested packages. These choices also reduce telegraphing from minor subfloor unevenness, which limits callbacks for hollow spots or lippage on harder substrates. EPDs now provide quantified lifecycle metrics, such as global warming potential (kg CO₂-eq/m²), energy use (MJ/m²), and end-of-life scenarios for different SPC constructions, enabling specifiers to compare how changes in thickness and underlayment affect environmental performance across project options.

There is a practical upper bound on thickness beyond which material cost and transitions to adjacent rooms become less forgiving. Within common ranges, however, the balance of acoustics, comfort, and ease of install continues to push premium formats into multi-family and higher-end residential specifications. The SPC flooring market size for premium assemblies is supported by projects where simplified code compliance and occupant comfort are procurement drivers. Underlayment knowledge has also improved as suppliers standardize acoustic definitions and field guidance. In the United States, minimum dwelling separation requirements for sound control anchor many of these choices in multi-family contexts. Education from underlayment providers continues to help teams select assemblies to reach target IIC, STC, and Delta IIC outcomes.

By Installation Method: Click-Lock Hegemony at 89% Reflects Labor-Cost Arbitrage and Multi-Family Velocity

Click-lock systems accounted for 89.00% of the SPC flooring market size in 2025 and are projected to grow at an 8.50% CAGR over 2026-2031, while glue-down held less than 8% of the SPC flooring market share. DIY adoption also supports click-lock because interlocking planks can be installed over many hard surfaces with basic tools when subfloor conditions are within tolerance, which reduces scheduling friction and helps projects start sooner.

Proprietary interlocking technologies are widely licensed and have matured to provide durable joints that meet the dimensional stability and performance expectations of rigid-core specifications, with standards like ASTM F3261 defining the category’s minimum requirements for residential and commercial use. Glue-down remains relevant where site conditions or service demands justify permanence, including healthcare corridors that undergo frequent wet cleaning, heavy rolling loads that generate lateral shear, or very large continuous spans beyond floating system recommendations. Self-adhesive formats serve thin-build retrofits over existing hard surfaces but remain a small niche due to narrower substrate windows and less favorable removability compared with floating installs.

By End User: Residential Anchors Volume, Commercial Accelerates on Lifecycle Economics

Residential applications accounted for 56.21% of 2025 SPC demand, while commercial is growing at a 9.50% CAGR through 2031 as operators value lifecycle cost advantages and streamlined installation. In retail, healthcare, and hospitality, rigid-core formats can be installed in tight windows and used immediately, which narrows the gap between demolition and reopening. Routine cleaning aligns with staff-friendly processes, and the waterproof surface is suited to back-of-house and public zones that see frequent spills or sanitizing. These factors strengthen SPC bids when uptime and predictable maintenance drive decisions. Published commercial guidance from manufacturers summarizes these benefits and shows how rigid-core fits code and operational requirements in typical interior projects.

On the residential side, the SPC flooring market captures kitchen, bath, and entry installations where moisture exposure is likely, while living areas may be mixed with other materials when comfort is prioritized. Multi-family turnover cycles place a premium on repeatable installs and basic care routines that maintain appearance between tenants. Where public and private projects require documentation of environmental performance and reclamation options, company programs offer defined pathways for qualifying resilient lines. These offerings help teams plan end-of-life handling for large projects more credibly than ad hoc disposal. They also reinforce the SPC flooring market’s position in institutional environments that track material flows and reporting requirements for certification systems.

By Distribution Channel: Online Surges at 10.16% as DIY and Direct-to-Consumer Models Disrupt Traditional Retail

Specialty flooring retailers within B2C/retail accounted for 38.49% of the 2025 SPC market share, and within that pool, online is projected at a 10.16% CAGR through 2031 as DIY adoption rises and digital merchandising improves. Web-based visualization, sample programs, and parcel-friendly carton sizes reduce friction for homeowners who plan and execute room-by-room upgrades. Omnichannel approaches from major retailers further blur lines, letting customers research and transact online with pickup or delivery options that accelerate starts.

For contractor and B2B buyers, credit terms, specification documentation, and job-site logistics remain decisive, which sustains growth in distribution channels serving commercial and multi-family projects. As domestic resilient capacity expands, retailers and distributors gain more options for lead time and logistics planning without extended ocean freight. Investments in North American resilient capacity make the SPC flooring market less exposed to shipping disruptions and policy shifts, which are shaping channel strategies around responsiveness and documentation[3]SHAWINC.COMhttps://shawinc.com/Newsroom/Press-Releases/Shaw-Industries-to-Invest-~$90-Million-to-Expand-D.

Geography Analysis

North America accounted for 35.88% of the global SPC market value in 2025. North American projects increasingly cite rapid renovation cycles and code-bound soundproofing thresholds as reasons to specify rigid-core assemblies that combine fast floating installation with underlayment-based acoustic control. Expanded domestic resilient capacity is expected to improve availability and reduce exposure to long shipping windows and variable surcharges. For spec-driven commercial projects, U.S. codes set floor-ceiling performance minimums for IIC and STC in dwelling separations. This baseline is often exceeded by thicker SPC assemblies with matched underlays. Those considerations keep the SPC flooring market relevant in rental refreshes and in new multi-family developments aiming for consistent resident experiences across stacked units. Company disclosures on resilient manufacturing expansion underline that lead times and product breadth will improve as new domestic lines reach full production.

Asia-Pacific is projected to record the fastest growth at a 9.77% CAGR from 2026 to 2031, reflecting both producer scale and urban housing stock adopting waterproof, resilient surfaces during renovation cycles in the SPC flooring market. European growth continues at a measured pace as mature markets weigh acoustic comfort, environmental disclosures, and public procurement criteria that prioritize detailed documentation. Trade actions in Europe have reshaped resin economics for downstream converters in 2025, which encouraged material diversification and investment in processes and lines closer to end demand. These conditions have expanded the SPC flooring market’s range of reliable sources in Europe and supported project teams focused on validated data and compliant assemblies[4]POLICY.TRADE. https://policy.trade.ec.europa.eu/news/commission-counters-dumped-polyvinyl-chloride-usa-and-egypt-2025-01-10_en.

In the United Kingdom and the EU, anti-dumping measures implemented in 2025 altered some resin price relationships and affected converters’ sourcing plans. These changes arrived alongside continued emphasis on transparent environmental product data and indoor-air quality documentation for resilient floors. Association-issued EPDs tailored to SPC provide a direct reference for teams comparing lifecycle reporting across product types, which supports consistent selection frameworks. As public and private green-building criteria spread, documentation and reclamation options become more relevant to procurement, and companies that can offer validated data and take-back programs are well-positioned. These factors sustain the SPC flooring market in Europe while steering it toward formats and suppliers that align with policy and documentation trends. The combined effect is steady demand with a tilt toward offerings that meet both performance and disclosure thresholds.

Competitive Landscape

The SPC flooring market remains moderately fragmented, with a top tier of internationally active manufacturers supported by strong brands, distribution, and increasingly local production footprints. Competitive intensity is rising as domestic resilient capacity expands, offering shorter lead times and certainty for projects that need consistent schedules. Technology and documentation are prominent differentiators, including locking systems, wear-layer durability, and third-party indoor-air quality verifications that simplify submittals. Sustainability programs and EPD-backed disclosures are also emerging as factors for public sector and certification-focused private projects. Companies that can pair reliable delivery with transparent environmental reporting and reclamation options are well-positioned to win specification-led bids.

Strategic moves mirror these themes. Investments in U.S. resilient capacity increase the share of domestic supply in North America and offer route-to-market advantages where ocean freight variability was a planning challenge. Company communications highlight capabilities tied to faster production cycles, expanded embossing and format options, and tighter lead-time windows that align with dealer and contractor expectations. On the commercial side, product guidance emphasizes how rigid-core supports quick turnarounds in offices, clinics, and retail environments and how it fits into maintenance routines that lower labor input over time. These developments help the SPC flooring market compete on total installed cost and uptime, not just material price.

Sustainability commitments and industry frameworks sit alongside capacity and performance as procurement criteria. Association programs and company disclosures are providing the data sets that owners, designers, and contractors use to evaluate environmental performance against documentation requirements. In practice, this means EPD references for SPC and adjacent resilient categories are commonly requested in bid packages, and buy-side teams consider reclamation programs where they apply. As a result, suppliers with well-documented offerings and accessible data have an edge in competition where transparency is mandatory. These dynamics, combined with expanded local production and fit-out advantages, define the SPC flooring market’s near-term competitive playbook.

Stone Plastic Composite Flooring Industry Leaders

Mohawk Industries

Shaw Industries

AHF Products

Tarkett

Mannington Mills

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: AHF Products unveiled a new sign at its recently acquired Cartersville, Georgia, rigid core manufacturing facility (328,000 square feet), signifying continued investment in American manufacturing and strengthening its supply chain to support Armstrong Flooring, Bruce, and U.S.-based private-label products. The plant produces millions of square feet of flooring annually, using advanced automation and AHF's proprietary HDPC (High Density Polymer Core) technology for waterproof, high-performance flooring.

- March 2026: Mohawk Industries announced organizational updates and product line refreshes for 2026, including new introductions across its resilient flooring segment (e.g., SPC, WPC, and LVT), aimed at improving product performance, design versatility, and dealer sell-through.

- March 2025: The Multilayer Modular Flooring Association (MMFA) published its second Environmental Product Declaration (EPD) for Vinyl-SPC floor coverings (4-5mm thickness range), verified by the German IBU Institute and valid for five years (2025-2030), providing independently verified environmental performance data to support sustainable building material selection and align with evolving LEED, BREEAM, and DGNB standards. Data was contributed by four MMFA member companies.

Global Stone Plastic Composite Flooring Market Report Scope

| SPC Tiles |

| SPC Planks |

| 4.0–5.0 mm |

| 5.1–6.0 mm |

| 6.1–6.5 mm |

| Above 6.5 mm |

| Self-Adhesive |

| Glue-Down |

| Interlocking/Click-lock |

| Others |

| Residential |

| Commercial |

| B2C/Retail | Home Centers |

| Specialty Flooring Stores | |

| Online | |

| Other Distribution Channels | |

| B2B/Contractors |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Product Type | SPC Tiles | |

| SPC Planks | ||

| By Product Thickness | 4.0–5.0 mm | |

| 5.1–6.0 mm | ||

| 6.1–6.5 mm | ||

| Above 6.5 mm | ||

| By Installation Method | Self-Adhesive | |

| Glue-Down | ||

| Interlocking/Click-lock | ||

| Others | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Home Centers |

| Specialty Flooring Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Contractors | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the SPC flooring market to 2031?

The SPC flooring market size was USD 15.94 billion in 2025 and is estimated at USD 16.49 billion in 2026, reaching USD 22.41billion by 2031 at a 6.33% CAGR.

Which segments are leading and which are growing fastest in SPC flooring?

Planks led with 84.00% share in 2025, and are projected to be the fastest growing at an 8.03% CAGR to 2031. By thickness, 4.0–5.0 mm led with 43.67% share in 2025, and 5.1–6.0 mm is set to grow at 9.23% CAGR.

Where is the demand for SPC flooring increasing fastest by region?

Asia-Pacific is projected to be the fastest-growing region at 9.77% CAGR through 2031, while North America held 35.88% of revenue in 2025.

Why are commercial buyers shifting toward SPC in fit-outs and renovations?

Fast floating installs, immediate walk-on readiness, and routine cleaning support quicker reopenings and lower lifecycle costs in offices, clinics, retail, and hospitality spaces.

How do building codes affect SPC specifications in multi-family projects?

U.S. codes require minimum IIC and STC thresholds for dwelling separations, and SPC assemblies with matched underlay help projects meet those benchmarks while preserving install speed.

What sustainability documentation is commonly requested for SPC specifications?

Project teams increasingly ask for EPDs and indoor-air quality verifications, and association-issued EPDs for SPC help standardize environmental disclosures across bids.

Page last updated on: