Hardwood Flooring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 55.46 Billion |

| Market Size (2031) | USD 73.79 Billion |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

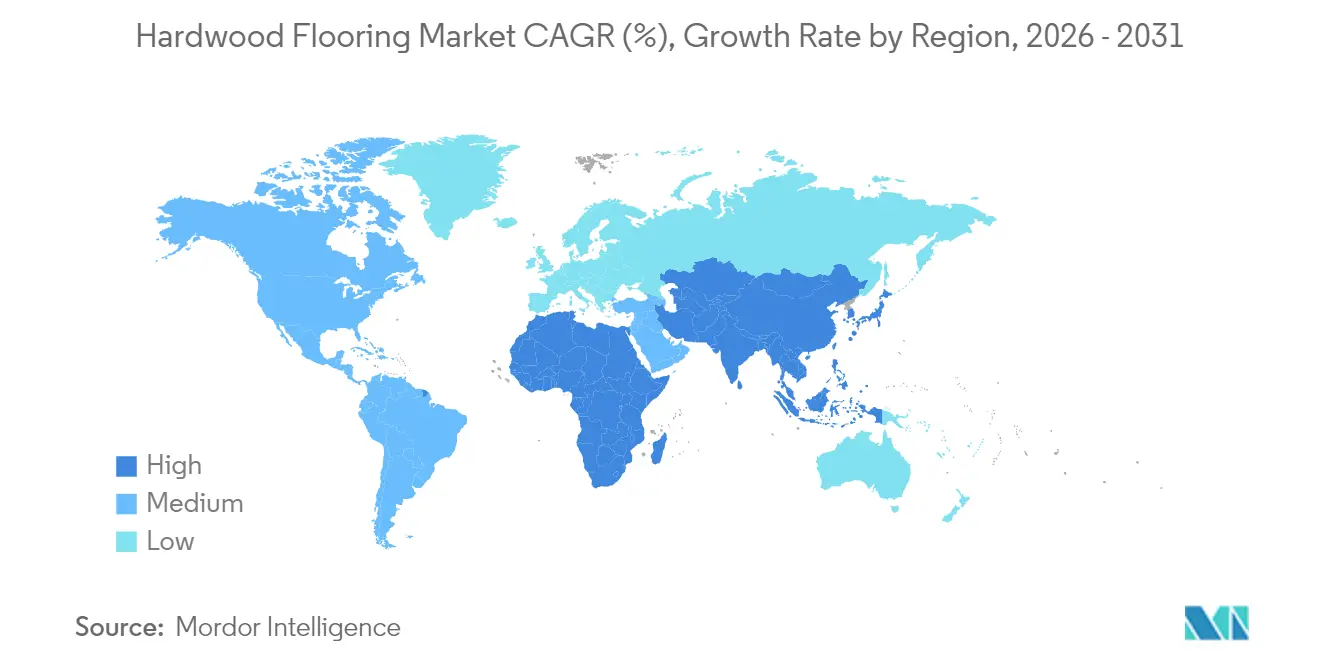

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

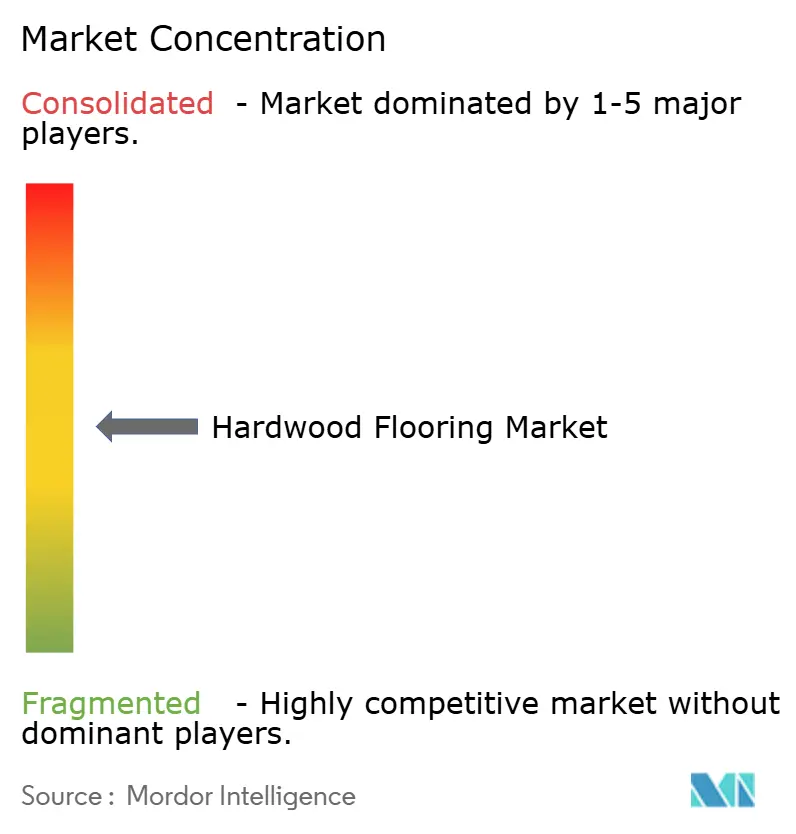

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hardwood Flooring Market Analysis by Mordor Intelligence

The hardwood flooring market size is expected to grow from USD 52.38 billion in 2025 to USD 55.46 billion in 2026 and is forecast to reach USD 73.79 billion by 2031 at 5.88% CAGR over 2026-2031. Renovation-focused spending in high-income economies, rapid engineered-wood innovations, and digital sales adoption collectively sustain a steady expansion trajectory even as interest-rate volatility challenges new-build activity. Rising demand for biophilic interiors, strict timber-traceability laws, and the growing popularity of thermally modified hardwood expand the hardwood flooring market into niches that command higher price realization. Leading companies broaden sourcing bases to manage phytosanitary risks and position certified products that satisfy emerging deforestation regulations. Technology-enabled click-lock systems shorten installation times, improving product competitiveness against resilient flooring while keeping labor shortages in check.

Key Report Takeaways

- By product type, engineered wood accounted for 71.98% of the hardwood flooring market share in 2025, while engineered wood is projected to expand fastest at a CAGR of 6.05% between 2026 and 2031.

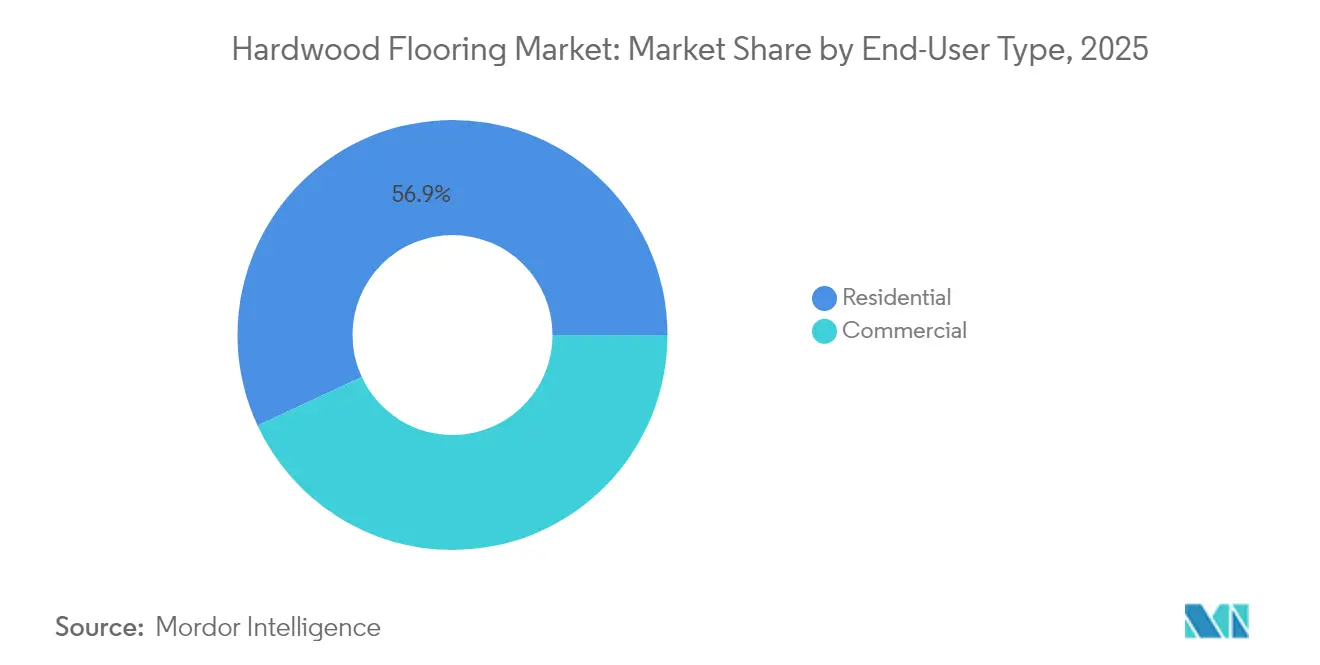

- By end user, residential applications captured 56.92% of the hardwood flooring market share in 2025, with commercial use forecast to grow at the highest CAGR of 7.42% during 2026–2031.

- By distribution channel, offline stores represented 66.55% of the hardwood flooring market share in 2025, while online stores are projected to rise fastest at a CAGR of 14.60% from 2026 to 2031.

- By geography, Europe held 33.05% of the hardwood flooring market share in 2025, while the Asia-Pacific is expected to grow at the highest CAGR of 7.48% during 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hardwood Flooring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging home-renovation spending in developed economies | +1.8% | North America & Europe | Medium term (2-4 years) |

| Expansion of engineered-wood click-lock technologies | +1.2% | Global | Long term (≥ 4 years) |

| Growing preference for biophilic interior aesthetics | +0.9% | North America & Europe, spill-over to APAC | Medium term (2-4 years) |

| Rising residential construction in emerging Asia | +1.5% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Commercial adoption of thermally modified hardwood floors | +0.7% | Global, early gains in North America & Europe | Medium term (2-4 years) |

| Uptake of reclaimed & recycled hardwood within circular-economy projects | +0.4% | Europe & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Home-Renovation Spending in Developed Economies

Elevated mortgage costs encourage households to remodel rather than relocate, fueling steady hardwood flooring upgrades in North America and Europe. Market research shows flooring projects deliver high resale value and tangible lifestyle benefits, making premium hardwood a favored investment even during macro uncertainty. The trend smooths revenue cyclicality by trying to increase demand for an aging housing stock rather than to volatile newly built pipelines. Manufacturers leverage the replacement cycle by bundling design services and extended-warranty packages that lift margins. Retailers benefit from predictable traffic and higher ticket values as consumers prioritize living-space enhancements over discretionary goods. Growth momentum is therefore embedded in renovation budgets that remain resilient despite shifting economic sentiment.

Expansion of Engineered-Wood Click-Lock Technologies

Proprietary locking mechanisms such as Uniclic and Välinge 5G fold-down profiles enable floating installations that cut labor time by up to 60%, expanding the hardwood flooring market among DIY enthusiasts and light-commercial specifiers. Moisture-resistant cores mitigate cupping concerns, allowing kitchens and basements to adopt engineered planks historically reserved for vinyl. Patent protection around locking systems creates pricing power and licensing revenue streams for technology owners, while driving industry-wide R&D is aimed at slimmer, more dimensionally stable constructions. This efficiency gains lower total project costs, making engineered hardwood a feasible upgrade path when budgets might otherwise tilt to resilient flooring. As a result, click-lock innovation acts as a structural demand driver with long-tail global relevance.

Growing Preference for Biophilic Interior Aesthetics

Architects and designers increasingly specify authentic wood surfaces to meet wellness goals in offices, schools, and healthcare environments. Studies link natural materials to improved productivity and occupant satisfaction, compelling corporate clients to allocate higher finish budgets to hardwood. Wide-plank, nature-grade visuals celebrate organic variation, a language design incompatible with digitally printed vinyl alternatives. Manufacturers highlight low-VOC finishes and traceable sourcing to align with green-building certification benchmarks, creating further pull for premium SKUs. This demand shift translates into higher average selling prices and stimulates product line extensions that pair contrasting species and textures for curated, nature-inspired spaces.

Rising Residential Construction in Emerging Asia

Rapid urbanization accelerates multi-family housing starts throughout China, India, Vietnam, and Indonesia, boosting hardwood penetration beyond luxury developments. Local sawmills scale rubberwood and acacia processing, shortening lead times and reducing landed costs for regional installers. Moreover, rising disposable incomes allow middle-class buyers to upgrade finish packages from laminate to engineered hardwood. Global suppliers co-locate finishing lines in Southeast Asia to capitalize on tariff advantages and proximity to growth markets. Consequently, emerging Asia constitutes the most durable volume opportunity for the hardwood flooring market over the next decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost versus vinyl & laminate alternatives | -1.1% | Global | Short term (≤ 2 years) |

| Stricter sustainability & deforestation regulations | -0.8% | Europe & North America, expanding to APAC | Medium term (2-4 years) |

| Supply-chain disruptions from phytosanitary import checks | -0.6% | Global | Short term (≤ 2 years) |

| Volatility in bio-based adhesive resin pricing | -0.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Versus Vinyl & Laminate Alternatives

Luxury vinyl tile replicates wood visuals at a fraction of the material and labor costs, siphoning entry-level demand away from hardwood. Inflation-driven lumber price spikes widen the gap, amplifying consumer price sensitivity. DIY-friendly resilient planks require no sanding or finishing, saving an additional 30-50% on installation labor. Commercial specifiers balancing budget and durability perceive limited ROI in hardwood for back-of-house or moisture-exposed zones. Manufacturers counter by amplifying value propositions around refinishing longevity and end-of-life recyclability yet cost parity remains elusive in price-driven bids.

Stricter Sustainability & Deforestation Regulations

The European Union Deforestation Regulation (EUDR), coming into effect in December 2025, obliges importers to provide full traceability to plot-level origin, adding 2-4% compliance costs across the supply chain[1]European Commission, “Regulation on Deforestation-Free Supply Chains,” europa.eu. . FSC and PEFC certifications transition from optional differentiation to baseline market access requirements, elevating audit fees and documentation burdens. Smaller mills face disproportionate overhead, accelerating consolidation toward vertically integrated groups. Retailers standardize EUDR-ready procurement frameworks globally, effectively extending European rules to third-country sales. Transition uncertainty dampens short-term export volumes and elongates shipping cycles as documentation is verified.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engineered Wood Drives Innovation

Engineered planks captured 71.98% of the hardwood flooring market share in 2025 and are forecast to maintain a 6.05% CAGR to 2031, underscoring their dominance in both scale and momentum. This leadership stems from multilayer cores that curb seasonal movement and accept factory-applied finishes, translating into lower call-backs and higher installer productivity. Engineered wood in the hardwood flooring market is anticipated to witness significant growth by 2031, highlighting its importance in both residential renovations and expansive commercial projects.

Solid wood maintains relevance among heritage restorations and premium custom homes, where the capability to sand multiple times supports century-long lifespans. Red and white oak species command pricing premiums due to grain uniformity and domestic availability, while maple earns niche demand in sports flooring for its hardness. Yet, scalable product innovation skews toward engineered formats: Välinge’s Woodura surface densification triples dent resistance and unlocks thinner wear layers that optimize raw-material yield. Producers also integrate recycled wood fibers into core layers, elevating sustainability credentials without compromising stability. These advances consolidate engineered wood’s status as the hardwood flooring market’s technology bellwether.

By End-User Type: Commercial Acceleration

Residential remodeling supplied 56.92% revenue in 2025, anchoring the hardwood flooring market with predictable upgrade cycles tied to aging housing stock. Pandemic-era nesting accelerated living-room and bedroom refits, a momentum that has normalized but remains structurally elevated relative to pre-2023 levels. Driven by a consistent trend of homeowners opting to stay put and renovate, the residential demand for hardwood flooring is anticipated to significantly boost the market size by 2031.

Conversely, the commercial segment is projected to expand to a 7.42% CAGR, the fastest across all end-user groups. Corporate workplace revamps center on wellness themes that prioritize tactile, low-VOC surfaces, positioning thermally modified ash and oak as attractive, durable options. Hospitality chains specify hardwood in lobby zones to reinforce brand identity via natural materials, while boutique retail adopts reclaimed planks for storytelling. Large-format office retrofits further lift demand, with square-foot volumes outpacing new office starts. Consequently, commercial growth adds balance to the hardwood flooring market by reducing reliance on consumer sentiment swings.

By Distribution Channel: Digital Transformation Accelerates

Brick-and-mortar outlets preserved a 66.55% share in 2025, leveraging in-store vignettes and pro-install networks that remain critical for big-ticket flooring purchases. Showroom walk-throughs enable sensory evaluation—color, texture, and acoustic absorption—that digital interfaces cannot fully replicate. However, omnichannel journeys increasingly begin online; Floor & Decor reports that web-initiated orders accounted for 19% of total sales in 2024.

Online pure-plays and click-and-collect hybrids are forecast to capture the bulk of incremental growth at 14.60% CAGR through 2031. Configurations using AR place planks into photos of customer rooms, reducing selection friction. Sample-by-mail programs cut decision cycles, while integrated installers close service gaps. E-commerce also accelerates rural penetration where showrooms are sparse, broadening the hardwood flooring market’s geographic reach. Yet digital fulfillment imposes new logistics challenges: bulky, heavy cartons require specialized carriers and white-glove delivery, favoring retailers with capital to build dedicated distribution centers.

Geography Analysis

Europe retained a 33.05% share of the hardwood flooring market in 2025, underpinned by stringent eco-labeling norms and a renovation-oriented building stock. Nordic design preferences favor light-tone engineered oak finished with natural oils, a look that permeates German and Dutch markets. The pending EUDR compliance deadline incentivizes domestic mills to secure chain-of-custody certifications, reinforcing regional supply security. France’s MaPrimeRénov’ subsidy boosts residential retrofits, while commercial upgrades linked to the Paris 2024 legacy program elevate demand in hospitality and mixed-use venues.

Asia-Pacific registers the fastest momentum with a 7.48% CAGR, adding millions of square feet of new apartments annually. China’s coastal provinces allocate higher finish budgets in response to up-market consumer shifts, while tier-two cities introduce local subsidies that reward low-formaldehyde flooring. India’s Pradhan Mantri Awas Yojana projects and Jakarta’s TOD schemes include green-building clauses that lift engineered-wood inclusion rates. Regional sawmills integrate kiln-drying and UV finishing lines to serve export markets facing anti-dumping duties, bolstering intra-Asia value addition.

North America sustains a mature, yet sizeable demand base anchored by renovation spending. Lumber tariffs and phytosanitary checks create periodic supply volatility, yet abundant FSC-certified Appalachian oak stabilizes input costs for domestic producers. U.S. builders increasingly specify thermally modified species for decking and three-season rooms, cross-selling indoor planks for design continuity. Canadian installers capitalize on favorable currency dynamics when sourcing from European mills, diversifying supply. While growth lags Asia, stable replacement demand ensures North America remains core to multinationals’ revenue mix.

Competitive Landscape

The hardwood flooring market exhibits moderate concentration; the five largest producers held 43% combined revenue in 2024. Mohawk Industries, AHF Products, and Kährs Group leverage vertically integrated sourcing and proprietary installation technologies to protect margins. Armstrong Flooring’s asset sale to AHF Products illustrates consolidation opportunities that emerge when leveraged players falter.

Strategic focus has pivoted to cost optimization and sustainable differentiation. Mohawk’s 2025 restructuring targets USD 100 million in annual savings through plant rationalizations and automation, buffering margin pressure from rising adhesive costs[3]Mohawk Industries, “Q1 2025 Results,” mohawkindustries.com. . Technology IP remains another battleground: Unilin enforces locking patents aggressively, collecting licensing royalties that fund next-generation R&D. Mid-sized regional specialists differentiate via locally popular species and fast-cycle custom color programs, a nimbleness that global giants struggle to match.

E-commerce upstarts employ direct-to-consumer models that bypass wholesale markups, leveraging algorithmic pricing and drop-shipping partnerships to undercut showroom quotes. Traditional retailers respond by integrating augmented-reality visualization and same-week installation services, replicating the digital convenience selling point. Sustainability further shapes rivalry: mills that achieve cradle-to-gate Environmental Product Declarations gain specification preference in institutional projects, nudging laggards toward greener chemistry and biomass energy adoption.

Hardwood Flooring Industry Leaders

Mohawk Industries

Shaw Industries Group

AHF Products (Bruce Hardwood)

Tarkett S.A.

Kährs Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: AHF Products has launched Armstrong Flooring TimberTones Densified Hardwood, designed for modern commercial spaces. Made from 100% real hardwood and manufactured in Somerset, Kentucky, this innovative flooring combines natural beauty, exceptional durability, and environmental responsibility.

- March 2025: Domestic resilient flooring producers expanded capacity after 45% tariffs on Chinese LVT imports, narrowing hardwood-vinyl price gaps.

- December 2024: Cyncly acquired Broadlume to integrate CRM and visualization solutions across flooring retail networks.

Global Hardwood Flooring Market Report Scope

Wood flooring involves any product manufactured from timber designed for structural or aesthetic flooring. This report covers a complete background analysis of the wood flooring market. It includes an assessment of the emerging trends by segments and regional markets, significant changes in market dynamics, and a market overview.

The Hardwood Flooring Market Is Segmented By Products Type (Solid Wood (Red Oak, White Oak, Maple, And Other Solid Wood) And Engineered Wood), End-User (Residential And Commercial), Distribution Channel (Offline Stores And Online Stores), And Geography (North America, South America, Europe, Asia-Pacific, And Middle East & Africa). The Market Size And Forecasts Are Provided In Terms Of Value (USD) For All The Above Segments.

| Solid Wood | Red Oak |

| White Oak | |

| Maple | |

| Other Solid Woods | |

| Engineered Wood |

| Residential |

| Commercial |

| Offline Stores |

| Online Stores |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East And Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product Type | Solid Wood | Red Oak |

| White Oak | ||

| Maple | ||

| Other Solid Woods | ||

| Engineered Wood | ||

| By End-User Type | Residential | |

| Commercial | ||

| By Distribution Channel (Value) | Offline Stores | |

| Online Stores | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East And Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

How large is the global hardwood flooring space in 2026, and what CAGR is expected through 2031?

It stands at USD 55.46 billion in 2026 and is forecast to climb to USD 73.79 billion by 2031, reflecting a 5.88% CAGR.

Which product type currently dominates hardwood flooring sales?

Engineered wood leads with 71.98% share in 2025 and also posts the fastest projected growth at a 6.05% CAGR.

What makes engineered wood increasingly popular with homeowners and contractors?

Multilayer cores provide moisture stability and click-lock systems trim installation time by up to 60%, lowering total project cost.

Which geographic region is projected to post the highest growth in hardwood flooring demand?

Asia-Pacific is expected to register a 7.48% CAGR through 2031, driven by rapid residential construction and rising disposable incomes.

How significant are online channels for purchasing hardwood flooring?

E-commerce remains a minority channel today but is forecast to grow at a 14.60% CAGR, fueled by AR visualization tools and sample-by-mail programs.

How concentrated is competition among top hardwood flooring suppliers?

The top five companies hold about 43% of global revenue, indicating moderate concentration with space for regional specialists and digital entrants.

Page last updated on: