Wood Plastic Composite Flooring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

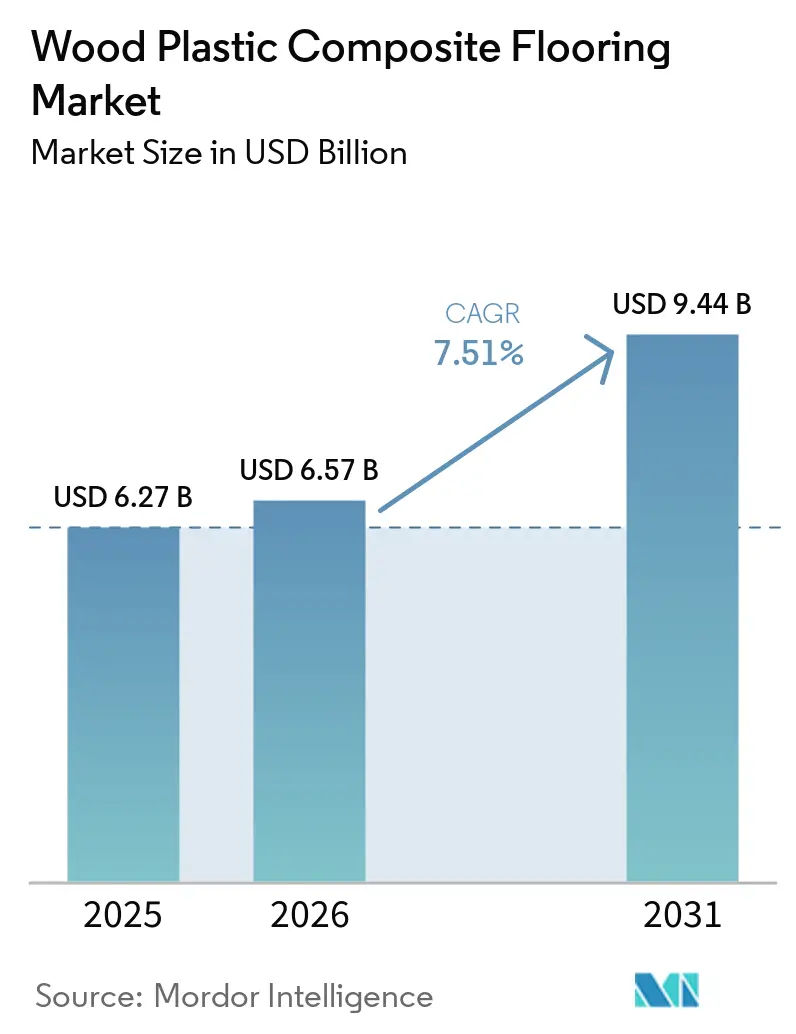

| Market Size (2026) | USD 6.57 Billion |

| Market Size (2031) | USD 9.44 Billion |

| Growth Rate (2026 - 2031) | 7.51% CAGR |

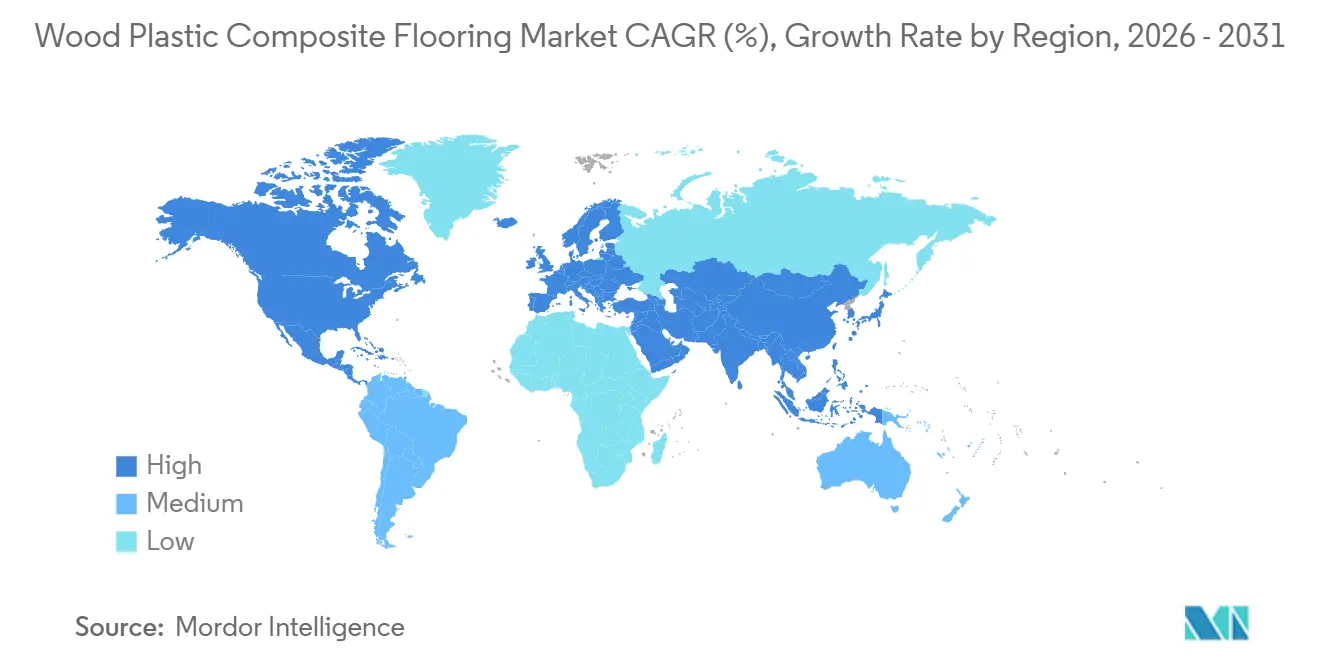

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wood Plastic Composite Flooring Market Analysis by Mordor Intelligence

The wood plastic composite flooring market size is expected to grow from USD 6.27 billion in 2025 to USD 6.57 billion in 2026 and is forecast to reach USD 9.44 billion by 2031 at 7.51% CAGR over 2026-2031. Growth reflects steady replacement cycles in North American remodeling and rising mid-market adoption in Asia-Pacific, where installers favor click-lock systems for predictable job timing and lower callbacks. Buyers who prioritize comfort and noise reduction continue to select WPC for upstairs rooms and multi-family projects as they weigh trade-offs against mineral-filled rigid alternatives. Manufacturers are also adjusting surface chemistries and documentation practices in response to evolving chemical oversight in major markets, which is shaping portfolio planning and supplier selection in the wood-plastic composite flooring market. Policy enforcement on forced-labor risk and related supply chain shifts has increased interest in nearshore and domestic options, which in turn supports lead-time reliability and compliance confidence for larger accounts. Product launches in glue-down and rigid LVT are also influencing specification choices at the margin, particularly in high-traffic zones where owners and facility managers prioritize hardness and long warranties.

Key Report Takeaways

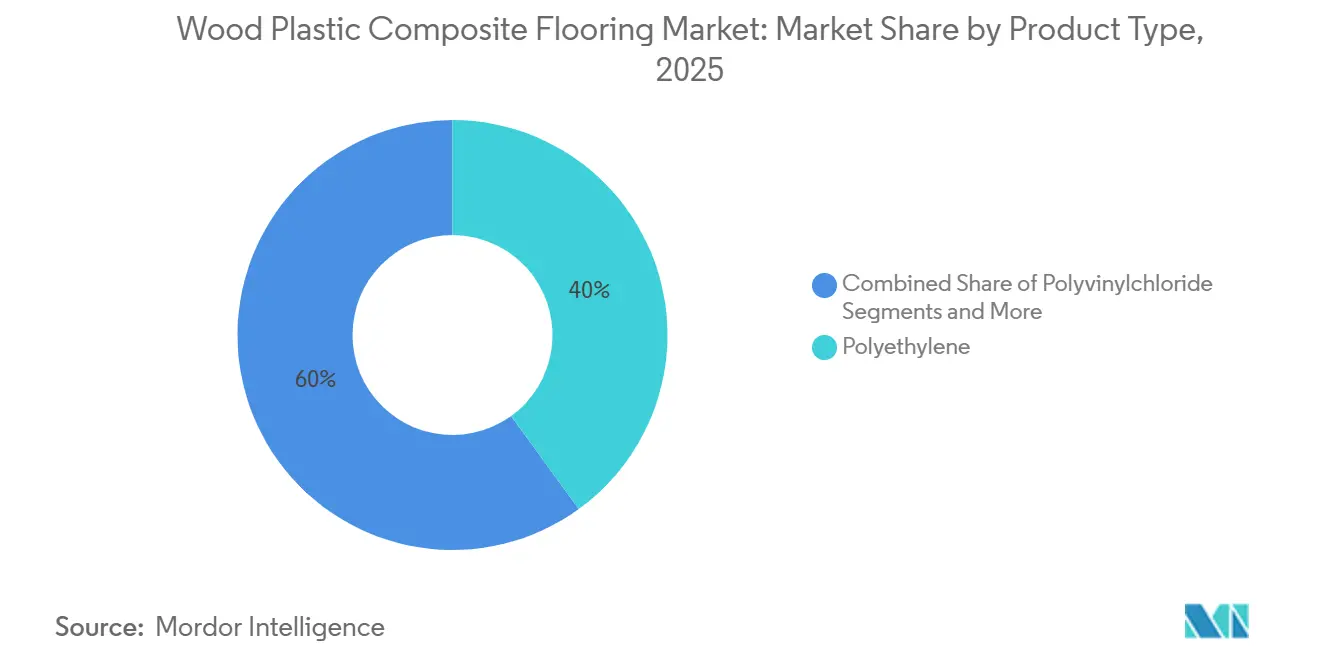

- By product type, polyethylene led with 40% of the wood-plastic composite flooring market share in 2025, while polypropylene is projected to grow at an 8.15% CAGR through 2031.

- By thickness, 5–6mm accounted for 56.72% of the wood plastic composite flooring market share in 2025, while 6.5–8mm is projected to expand at an 8.31% CAGR through 2031.

- By installation method, interlocking click-lock systems held 71% of the wood plastic composite flooring market share in 2025, while click-lock is projected to advance at an 8.48% CAGR through 2031.

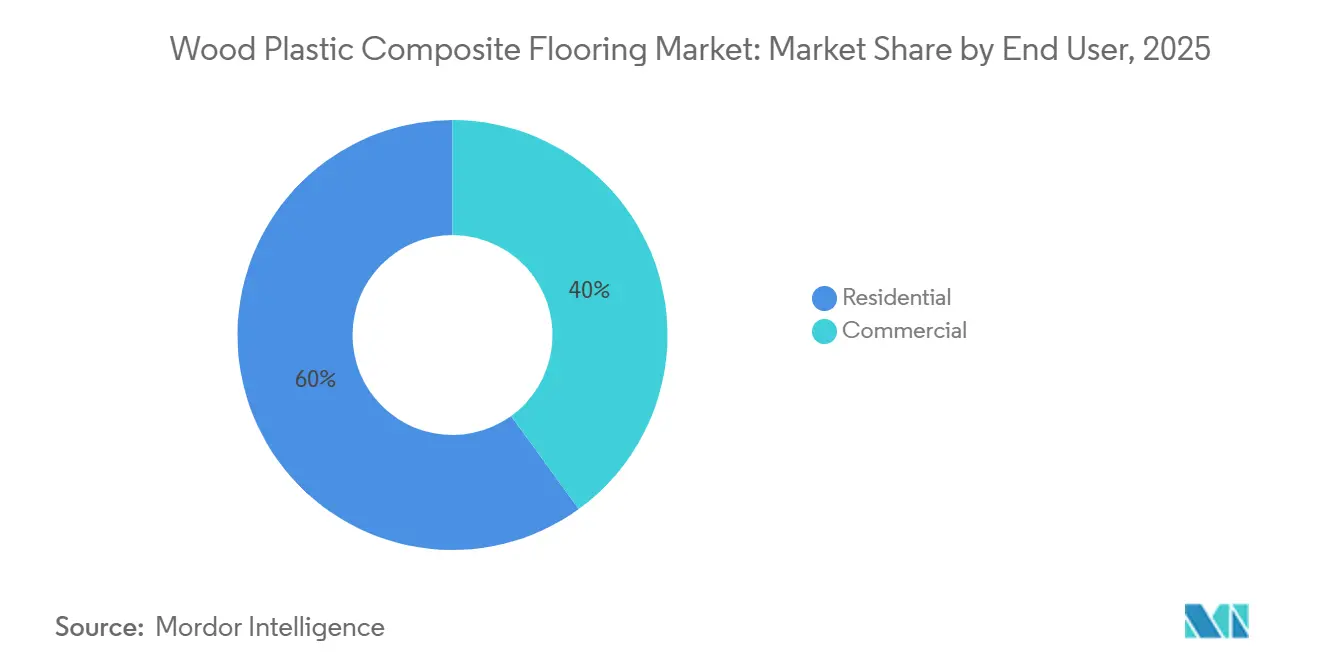

- By end user, residential led with 60% of the wood plastic composite flooring market share in 2025, while commercial is projected to grow at a 7.90% CAGR through 2031.

- By distribution channel, home centers held 40% of the wood plastic composite flooring market share in 2025, while online direct-to-consumer is projected to post a 9.10% CAGR through 2031.

- By geography, North America accounted for 33% of the wood plastic composite flooring market share in 2025, while Asia-Pacific is projected to record an 8.60% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wood Plastic Composite Flooring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| DIY-friendly click-lock rigid vinyl accelerates residential remodels | +1.8% | Global, peak in North America and Europe | Short term (≤ 2 years) |

| Waterproof and acoustic comfort advantages in multi-level housing | +1.5% | APAC core, spillover to MEA | Medium term (2–4 years) |

| Premium WPC rebound amid quality issues in entry-level SPC tiers | +1.2% | North America, Western Europe | Medium term (2–4 years) |

| Omnichannel discovery and visualization improve conversion | +0.9% | Global, led by North America's e-commerce | Short term (≤ 2 years) |

| Insurance-driven water-loss replacements favor waterproof, rigid floors | +0.7% | United States and Canada | Short term (≤ 2 years) |

| Extra-thick WPC, 10–12mm up to 19mm, as a hardwood substitute without trim changes | +1.4% | National, early gains in Santiago, Valparaíso, Concepción | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

DIY-Friendly Click-Lock Rigid Vinyl Accelerates Residential Remodels

Click-lock construction remains central to the value proposition in the wood plastic composite flooring market because it reduces job duration, simplifies training, and lowers rework risk in occupied homes. Large brands continue to refine profile geometry and edge stability to support faster installs with consistent finished-floor flatness, which eases scheduling in tight remodel windows. At retail, collections that package locking systems with matched trims and underlayment kits help homeowners and pros move from sample to completion with fewer decision points, which benefits conversion and satisfaction. Manufacturers that offer installation-ready systems with one-price simplicity have seen strong reception in recent product cycles, indicating that execution certainty is a critical purchase driver for remodels. Distribution programs that guarantee short lead times and regional stock also support DIY and pro remodels, as contractors can commit to dates with confidence and avoid delays tied to transoceanic shipments.

Waterproof and Acoustic Comfort Advantages in Multi-Level Housing

Multi-level housing projects favor products that control sound transmission and deliver a warmer underfoot experience, which sustains demand for WPC in bedrooms, lofts, and mezzanines. Collections that integrate thicker cores with engineered pads offer a balanced footprint that helps manage subfloor variation while improving step-sound characteristics, which matters in conversions and basements. Premium WPC lines also bundle high-wear surfaces with attached foam to deliver comfort and scratch resistance, which broadens their use into family rooms and media rooms where occupants prioritize quiet floors. Commercial and mixed-use properties apply similar criteria for select zones, especially where a softer feel and low-maintenance cleaning profile are preferred over maximum static load resistance, which keeps WPC in the specification mix. Product data sheets that highlight thermal and acoustic performance, alongside moisture tolerance, support clear positioning in the wood-plastic composite flooring market for projects where acoustic comfort is critical.

Premium WPC Rebound Amid Quality Issues in Entry-Level SPC Tiers

Buyers who experienced surface or joint performance concerns in entry-tier rigid vinyl are shifting toward thicker, premium WPC lines that emphasize stability and edge integrity. Suppliers have responded with SKUs that combine substantial total thickness and attached pads with high-performance wear layers, aiming at households that want comfort and longevity without complex subfloor work[1]TRUCORFLOORS.COM https://trucorfloors.com/products/trucor-prime-xl-12-in-moncton-oak. Offerings in the upper end often stress a “do it once” fit for busy homes, which aligns with remodelers seeking fewer callbacks and less time on repairs, and that alignment supports both brand equity and channel advocacy. Sustainability-linked improvements, such as increased recycled content or PVC-free approaches in adjacent portfolios, add another decision factor for customers seeking resilient options with lower embodied impacts. These dynamics combine to boost premium WPC visibility and reinforce product differentiation in the wood-plastic composite flooring market as brands move beyond a pure price play.

Omnichannel Discovery and Visualization Improve Conversion

Retailers and brands that meet shoppers online and in showrooms with consistent product data and clear installation pathways report stronger close rates for resilient floors. When customers can review wear-layer specs, edge details, and full-room photography, they reach confident decisions faster, and the effect is amplified when in-stock signals and delivery windows are transparent. Professional programs that link CRM, local inventory, and delivery routing also enable next-available job slots without cross-warehouse transfers, which improves both customer satisfaction and installer utilization. Channel strategies that blend brand-owned sites with partner dealer networks have continued to mature, evolving toward simplified sample kits that help households finalize color and texture choices. This approach supports the wood-plastic composite flooring market by aligning product education with logistics predictability, reducing friction from discovery to installation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SPC's lower cost and higher dent resistance cannibalize WPC | -1.3% | Global, concentrated in budget-tier residential | Short term (≤ 2 years) |

| Tightening PVC chemical policies and trade barriers raises compliance costs | -0.9% | North America and the EU, spillover to APAC export lanes | Medium term (2–4 years) |

| Import-reliant WPC faces UFLPA and logistics disruptions | -0.7% | United States, affecting China-sourced resin | Medium term (2–4 years) |

| Commercial specs de-prioritize WPC for rolling loads in healthcare and education | -0.5% | North America and Europe's commercial sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

SPC’s Lower Cost and Higher Dent Resistance Cannibalize WPC

Projects that prioritize dent resistance under rolling loads and stacked furniture often specify mineral-core rigid products or commercial-grade LVT, which creates competition for WPC in corridors and cafeterias. Facility managers in healthcare and education seek hard-surface warranties and surface-hardness solutions that maintain appearance over long service intervals, which typically narrow the field to rigid LVT families with proven track records. In entry-price residential projects where the total budget is fixed, buyers often trade underfoot comfort for lower material cost and higher static-load ratings to satisfy move-in schedules. That dynamic can slow WPC adoption in specific sub-segments, despite its strengths in comfort and impact sound control. As product lines evolve, WPC continues to retain share in rooms where dwellers prioritize warmth and noise control. At the same time, rigid LVT and mineral-core options remain common in heavy-traffic zones, which sustains a pragmatic split of use cases in the wood plastic composite flooring market.

Tightening PVC Chemical Policies and Trade Barriers Raise Compliance Costs

Evolving rules on plasticizer use and worker protections have increased the compliance burden for manufacturers that rely on flexible film layers and related chemistries in resilient flooring, and these shifts influence portfolio roadmaps and sourcing decisions. In Europe, restrictions on PFAS-containing treatments and rigorous low-emission designations are encouraging substitution toward non-fluorinated finishes and tighter disclosure practices, which raises documentation and testing costs for exporters to the region. Trade enforcement tied to forced labor policies has also changed procurement choices for North American buyers, with importers implementing origin audits and alternative materials planning to avoid detentions and delays[2]CBP.GOV https://www.cbp.gov/trade/forced-labor/UFLPA. These policy trends remain central to cost-to-serve and risk management, prompting some producers to diversify to nearshore sites and build out in-region capacity in adjacent categories. The net effect is a higher threshold for documentation readiness across the wood plastic composite flooring market, especially for portfolio items destined for public projects and large enterprises.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Polyethylene Leads Volume, Polypropylene Gains Momentum in Heat-Prone Climates

Polyethylene-based WPC led the product mix with 40% in 2025, while polypropylene is projected to grow at an 8.15% CAGR to 2031. Among commodity polymers through 2031, positioning both as anchors for pricing ladders that cover entry, mid, and premium tiers in the wood plastic composite flooring market. In practice, polyethylene variants are selected for their balanced density and resilience, which support comfortable step-sound performance and make them a fit for upstairs rooms and mixed-traffic residential zones. Product lines that emphasize dimensional stability across seasonal swings gain favor with installers who want to avoid callbacks related to gapping and edge telegraphing, which helps polyethylene families maintain mindshare. Polypropylene draws attention where higher heat-deflection tolerance is desired, particularly in sun-exposed rooms or warmer geographies, and that characteristic opens new placements, widening the overall addressable set. Brands that blend higher-spec cores with durable wear layers direct these collections toward homeowners who prefer a softer feel over maximum indentation resistance, keeping the portfolio logic consistent across both polymers.

The regulatory context reinforces material selection patterns as manufacturers evaluate plasticizer choices and certification targets for resilient surfaces above composite cores. Company disclosures suggest steady progress on recycled content and substitution strategies as brand owners seek routes to lower-carbon resilience across adjacent product families. In the wood-plastic composite flooring market, product managers are also shaping assortments so that clear use-case narratives guide selection by room and traffic level, limiting misapplications that can trigger warranty events. Where portfolios connect wear-layer durability to core stability and pad integration, the combination aligns user expectations with delivered performance, which supports repeat business and higher NPS scores for retailers. This pattern of polymer positioning, certification alignment, and room-by-room specification continues to define how brands defend share against mineral-core alternatives in overlapping price bands.

By Thickness: 5–6mm Balances Cost and Performance, 6.5–8mm Captures Premium Retrofit Spend.

The 5-6mm band accounted for 56.72% in 2025, as buyers in cost-sensitive projects selected options that meet indentation and comfort expectations without pushing total installed cost above budget, and the tier’s fit with quick-turn remodels keeps it prominent in the wood-plastic composite flooring market. Lines at this thickness typically integrate attached pads and consistent click profiles, which minimize prep and enable efficient room-by-room installs. The format also aligns with a large installed base of thresholds and trims in mid-market homes, limiting carpentry changes and helping installers finish more rooms per day. Portfolios that match colorways and textures across thicknesses give retailers flexibility to step customers up without changing the visual they fell in love with, which strengthens mix management. These features combine to keep the 5–6mm category central for builders and property managers who require predictable cost and reliable performance.

The 6.5-8mm tier is projected to grow at 8.31% through 2031, supported by homeowners who want more comfort and a quieter floor, and by pros who value pad integration that tolerates small subfloor variances without self-leveling. Premium lines in this range highlight thicker cores, higher-spec wear layers, and stronger visuals to justify a step-up ticket for rooms where families spend more time. Product pages that detail construction and wear performance help both installers and customers place these SKUs correctly in living rooms, home offices, and dens where thermal comfort and sound absorption are valued. The narrative also holds in light-commercial pockets, such as private offices and conference rooms, where a softer step and a premium look win out over maximum load capacity. This growth thesis is sustained by a portfolio logic that slots 6.5–8mm above entry tiers while staying under hardwood in cost and complexity.

By Installation Method: Click-Lock Systems Dominate DIY and Light-Commercial, Glue-Down Holds Niche in Heavy Traffic

Interlocking click-lock systems held 71% in 2025 and are projected to expand at 8.48% through 2031, because they shorten job timelines and support consistent quality without adhesive cure windows in the wood plastic composite flooring market. The format is attractive to DIYers who want speed and reversibility in case of a future remodel, and to pros who want to control labor risk when projects have many small rooms. Retailers and brands that package click-lock collections with clear subfloor prep guidance and matched accessories reduce error rates and simplify quoting, which lowers friction in both discovery and installation. In practice, click-lock remains the primary route for installing in bedrooms, lofts, and upstairs hallways, where noise control and comfort rank higher than maximum point-load resistance. The share gains also reflect channel strategies that ensure fast replenishment and store-available stock, so contractors avoid rescheduling jobs while waiting for glue-down adhesives or specialist installers.

Glue-down retains a durable niche for spaces that require high static-load tolerance and predictable performance under rolling carts, and brands continue to invest in this path with enhanced wear technologies and broad SKU assortments. These portfolios emphasize long commercial warranties, wide planks, and clear installation guidance, which aligns with corridors, cafeterias, and specific healthcare zones where facility teams prize consistency. Installers who want same-day transitions and rapid return-to-service windows value modern adhesive systems, which simplify phasing in occupied buildings and help contractors maintain schedules. The result is a pragmatic division of labor between click-lock and glue-down across property types, which supports portfolio breadth and helps retailers cover a wider range of use cases. This mix also reinforces specification clarity so project teams can weigh comfort and speed of install against indentation resistance when selecting among resilient families in the wood plastic composite flooring industry.

By End User: Residential Remodels Drive Volume, Commercial Hospitality Accelerates Post-Pandemic

Residential led with 60% of 2025 demand as households updated kitchens, bedrooms, and family rooms without the complexity of hardwood refinishing, which supports steady placements for the wood-plastic composite flooring market. DIY-ready formats make it easier for homeowners to schedule work and avoid prolonged downtime in high-traffic rooms, encouraging repeat projects across multiple floors of a home. Suppliers that align colors and textures with popular cabinet and paint palettes help remodelers coordinate design decisions more quickly, accelerating the installation process. Product lines that emphasize noise control and a warmer feel provide another rationale to upgrade from laminate or thinner resilient products in upstairs rooms. Portfolio features like attached pads and robust locking systems also reduce the need for specialized tooling, which helps general contractors and handyperson services deliver a good result for homeowners.

Commercial is projected to grow at 7.90% through 2031, led by hospitality and select healthcare spaces where comfort and easy maintenance in patient rooms and suites are valued, while heavier traffic corridors continue to favor more rigid alternatives. Commercial-grade resilient families with high wear ratings and strong surface technologies are expanding choice sets for specifiers, including glue-down collections that support phased renovations. Project teams that balance acoustic goals with long-term maintenance plans continue to allocate WPC to quieter zones while using mineral-core or sheet products in areas with heavy rolling loads. This approach helps owners maintain asset performance across varied spaces, reducing lifecycle cost surprises and aligning with warranty frameworks. The division of spaces by use case remains a stable planning practice that supports both residential and commercial adoption patterns across the wood plastic composite flooring industry.

By Distribution Channel: Home Centers, Anchor Retail, Online DTC Surges with AR Visualization

Home centers within B2C/Retail held 40% of 2025 volumes as shoppers combined in-person selection with bundled installation services, and assortments spanning entry to premium price points simplified step-up selling across the wood-plastic composite flooring market. In-store displays that showcase full planks and matched accessories shorten decision time and reduce returns, helping both retailers and installers keep schedules on track. As brands coordinate content across web and store, customers arrive better informed about wear layers, pad options, and locking details, which concentrates final visits on color decisions. Home centers also serve as dependable pickup points for pros, which matters for tight turnarounds and smaller projects with limited staging space. The net effect is high throughput for common styles with broad appeal and reliable replenishment.

Online direct-to-consumer within B2C/Retail is projected to grow at 9.10% through 2031 as brands and retailers refine sampling programs, logistics visibility, and post-purchase support, thereby lowering friction in digital journeys. Builder and multifamily programs that promise short lead times from regional warehouses continue to expand, enabling contractors to commit to project calendars with confidence[3]LIONSFLOOR.COM https://www.lionsfloor.com/builder-multifamily-solutions/. Many online journeys now integrate customer support that links product advice with installation resources and helps avoid avoidable claims. As direct channels scale, brands with strong after-sales service and clear technical documentation gain referral momentum. This complements physical retail in a hybrid path-to-purchase that aligns with modern buyer expectations and reinforces trust in the wood plastic composite flooring market.

Geography Analysis

North America accounted for 33% in 2025 as resilient demand from remodeling and replacement sustained steady placements for WPC in bedrooms and living spaces where warmth and sound control matter. Owners in healthcare and education continue to split specifications by zone, reserving softer-feel formats for select areas while using rigid LVT or mineral-core solutions under heavier loads. Trade enforcement related to forced-labor risk has also shaped procurement, prompting importers to adjust origin strategies and documentation practices to avoid detentions and delays. Domestic and nearshore investments in adjacent resilient families strengthen lead-time assurance across the broader category, which improves scheduling for high-utilization facilities. Portfolio variety and clear installation guidance remain points of differentiation in retail, as brands work to align product education with compliance readiness across the wood plastic composite flooring market.

Asia-Pacific is projected to post the fastest regional growth at 8.60% through 2031, reflecting urbanization, mid-market housing expansion, and ongoing improvements in channel infrastructure. Manufacturers continue to diversify capacity across the region to improve resilience and shorten transit times to key export destinations, which mitigates geopolitical and policy risk. Regional supply chains increasingly emphasize materials documentation and low-emission finishes to maintain access to regulated markets, and these efforts support smoother customs clearance and customer confidence. Growing adoption of thicker cores and attached pads aligns with buyer priorities for comfort and noise control in higher-density living. As online and offline channels mature in key cities, assortments that match popular interior styles and provide reliable delivery windows lift conversion for resilient floors across the region.

Europe maintains a substantial share driven by long-term modernization of housing stock and regulatory frameworks that prioritize low-emission products and safer surface chemistries, which influence specification criteria for resilient flooring[4]EUROFINS.COM https://sustainabilityservices.eurofins.com/news/pfas-regulations-overview-2026-for-consumer-products. WPC’s appeal in upstairs rooms and select commercial settings remains consistent, while stricter rules around certain chemical classes are steering reformulation in finishes and adhesives. Brands selling into the region are documenting materials choices with greater rigor and leaning on third-party testing to streamline compliance for institutional buyers. Portfolios that emphasize performance, certification, and aesthetic range are well placed to hold shelf space in specialty retail and builder channels. Consistency in regulatory interpretation and product labeling supports predictable planning in the wood plastic composite flooring market, which is valuable for cross-border programs.

Competitive Landscape

Competition is moderate with a broad field of domestic brands, regional specialists, and OEM producers supporting private labels, which sustains customer choice and price transparency across channels. Brands at scale lean on integrated supply chains, consistent customer service, and national dealer networks to maintain shelf space and installer loyalty. Sustainability and compliance capabilities are rising differentiators, as buyers elevate documentation in RFPs and channel partners consolidate around suppliers with reliable testing and labeling practices. Investments that strengthen production flexibility and shorten delivery windows are increasingly cited as reasons for award decisions in enterprise accounts. These factors, taken together, favor suppliers that pair balanced assortments with operational excellence in the wood plastic composite flooring market.

Company moves in adjacent categories also affect competitive positions because they influence distribution reach and project-share dynamics. MSI’s glue-down resilient launches expand choice sets for commercial projects and provide retailers with complementary options when end users require high-wear surfaces and phased installations. Lions Floor’s builder and multifamily solutions illustrate how predictable lead times and regional service models secure contractor loyalty in time-sensitive projects. These initiatives underscore how the breadth of offer and dependable fulfillment shape share outcomes even when products compete on similar aesthetics. The same logic supports end-user trust, which translates into referrals and repeat business in the remodel segment of the wood-plastic composite flooring market.

Supply chain diversification remains a strategic theme as companies expand manufacturing footprints to balance risk and support regional demand. New capacity investments in Southeast Asia are intended to improve resilience and reduce transit times to Western markets, helping brands and distributors protect delivery commitments. Corporate development in adjacent outdoor composites strengthens category adjacency for some players and can unlock cross-selling to contractors who handle both interior floors and exterior decking. M&A in rubber and other resilient families broadens specifications coverage in institutional spaces and positions suppliers for budget discussions beyond a single material class. These actions collectively reinforce that scale, documentation, and service depth are central to share defense and expansion in the wood plastic composite flooring market.

Wood Plastic Composite Flooring Industry Leaders

Shaw Industries

Mannington Mills

Mohawk Industries

The Dixie Group

MSI Surfaces

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: UFP Industries acquired Oldcastle APG's MoistureShield decking operating assets, including CoolDeck® composite technology, enabling Deckorators® to double wood-plastic composite capacity to USD 200 million by 2027. The deal positions UFP to meet surging outdoor-living demand while integrating heat-mitigating technology that reduces surface temperatures 20% below traditional WPC decking.

- February 2026: MSI launched its Nove, Nove Plus, and Nove Reserve glue-down luxury vinyl tile collections, featuring extra-wide 9×48-inch planks with CrystaLux™ wear layers ranging from 6-mil to 22-mil thickness. The Nove Reserve's 22-mil CrystaLux Ultra layer achieves Mohs 10 hardness, targeting high-traffic commercial applications where WPC's softer core historically ceded share to SPC.

Global Wood Plastic Composite Flooring Market Report Scope

| Polyethylene | High-Density Polyethylene (HDPE) |

| Low-Density Polyethylene (LDPE) | |

| Polyvinylchloride | Rigid PVC |

| Flexible PVC | |

| Polypropylene | Homopolymer Polypropylene |

| Copolymer Polypropylene | |

| Other Product Types |

| 3.5-4 mm |

| 5-6 mm |

| 6.5-8 mm |

| Above 8 mm |

| Joist-and-Clip System |

| Glue-Down |

| Interlocking/Click-lock |

| Others |

| Residential |

| Commercial |

| B2C / Retail Consumers | Home Centers |

| Specialty Flooring Stores | |

| Online | |

| Local Hardware Shops (unorganized market) | |

| Other Distribution Channels | |

| B2B / Contractors / Builders |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Product Type | Polyethylene | High-Density Polyethylene (HDPE) |

| Low-Density Polyethylene (LDPE) | ||

| Polyvinylchloride | Rigid PVC | |

| Flexible PVC | ||

| Polypropylene | Homopolymer Polypropylene | |

| Copolymer Polypropylene | ||

| Other Product Types | ||

| By Thickness | 3.5-4 mm | |

| 5-6 mm | ||

| 6.5-8 mm | ||

| Above 8 mm | ||

| By Installation Method | Joist-and-Clip System | |

| Glue-Down | ||

| Interlocking/Click-lock | ||

| Others | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C / Retail Consumers | Home Centers |

| Specialty Flooring Stores | ||

| Online | ||

| Local Hardware Shops (unorganized market) | ||

| Other Distribution Channels | ||

| B2B / Contractors / Builders | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the projected growth rate for the wood plastic composite flooring market through 2031?

The category is projected to grow at a 7.5% CAGR over 2026-2031 based on the current outlook and demand drivers.

How large is the wood plastic composite flooring market today, and where is it headed by 2031?

The wood plastic composite flooring market size was USD 6.27 billion in 2025 and is projected to reach USD 9.44 billion by 2031, supported by remodeling and multi-family adoption.

Which installation method is expected to remain the most common in residential applications?

Interlocking click-lock is expected to remain the preferred method due to speed, predictability, and simplified training for installers and DIYers.

Which region is expected to record the fastest growth in the next five years?

Asia-Pacific is projected to lead growth as urban housing and channel infrastructure mature in key markets.

What regulations are most likely to affect surface chemistries and supplier documentation?

EPA oversight of select phthalates and European restrictions around PFAS-containing treatments will continue to shape reformulation and testing practices.

When should specifiers favor WPC over mineral-core rigid alternatives?

WPC is most often preferred in bedrooms, upstairs rooms, and select commercial zones where acoustic comfort and a warmer underfoot feel are prioritized over maximum rolling-load resistance.

Page last updated on: