PVC-free Vinyl Flooring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

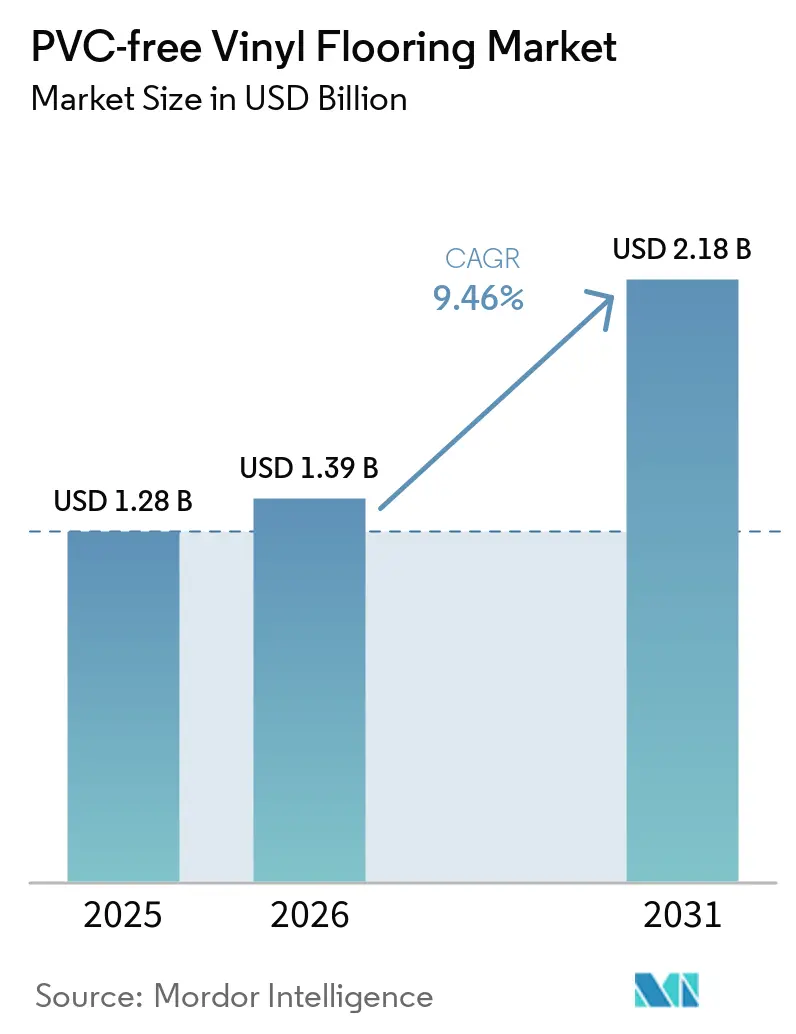

| Market Size (2026) | USD 1.39 Billion |

| Market Size (2031) | USD 2.18 Billion |

| Growth Rate (2026 - 2031) | 9.46% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

PVC-free Vinyl Flooring Market Analysis by Mordor Intelligence

The PVC-free vinyl flooring market size was valued at USD 1.28 billion in 2025 and is estimated to grow from USD 1.39 billion in 2026 to reach USD 2.18 billion by 2031, at a CAGR of 9.46% during the forecast period (2026-2031). This growth path reflects stronger green building criteria in public and private projects, rising adoption in hospitals and schools focused on indoor air quality, and broader access to chlorine-free, ortho-phthalate-free chemistries that support circular procurement. Procurement teams in the United States and Europe continue to reference third-party emission certifications and take-back requirements, which are tilting specifications toward PVC-free resilient alternatives. The shift is strongest in education and healthcare due to low-VOC performance thresholds and compliance frameworks that reference CDPH Section 01350 and equivalent test methods. Manufacturers that can back claims with verified EPDs, emissions certifications, and established reclamation programs are improving win rates in tenders with LEED-aligned or EU Green Public Procurement requirements.

Key Report Takeaways

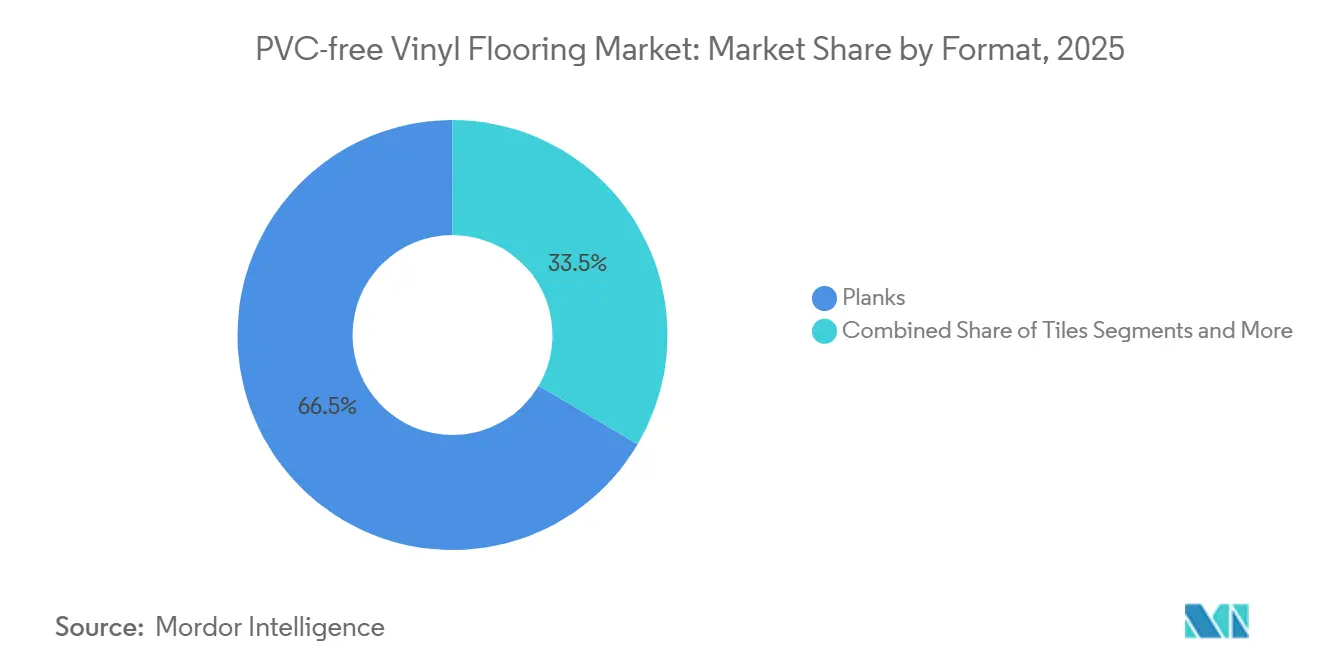

- By format, planks captured 66.52% of the PVC-free vinyl flooring market in 2025 and are projected to grow at 10.07% CAGR between 2026 and 2031, reflecting specification momentum in commercial retrofits and new construction.

- By installation method, click/interlocking captured 43.67% of the PVC-free vinyl flooring market in 2025, while loose-lay is projected to grow at 11.52% CAGR between 2026 and 2031 due to circular recovery benefits and simplified removal.

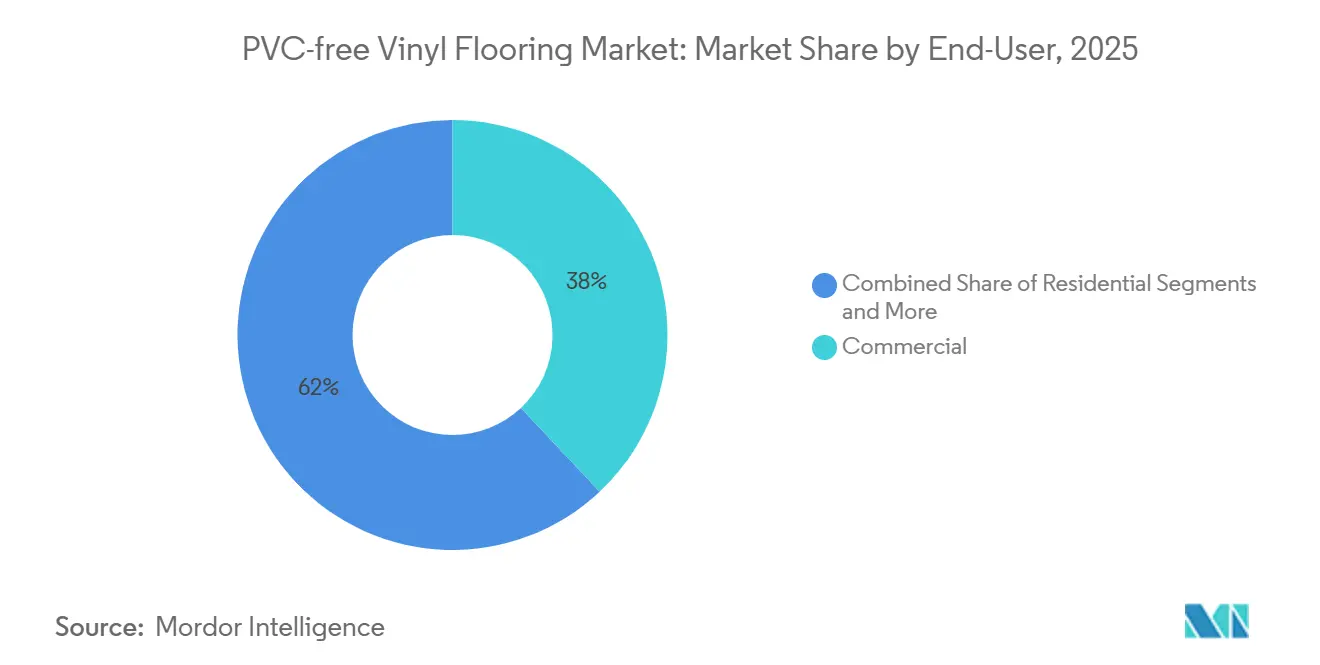

- By end user, commercial captured 38.00% of the PVC-free vinyl flooring market in 2025, while industrial and specialized vehicles are projected to grow at a 11.71% CAGR between 2026 and 2031 as transit operators tighten slip-resistance and durability criteria.

- By distribution channel, B2C/Retail captured 42.00% of the PVC-free vinyl flooring market in 2025, while B2B/Contractors/Builders are projected to grow at 9.84% CAGR between 2026-2031 as manufacturers expand domestic capacity and institutional programs.

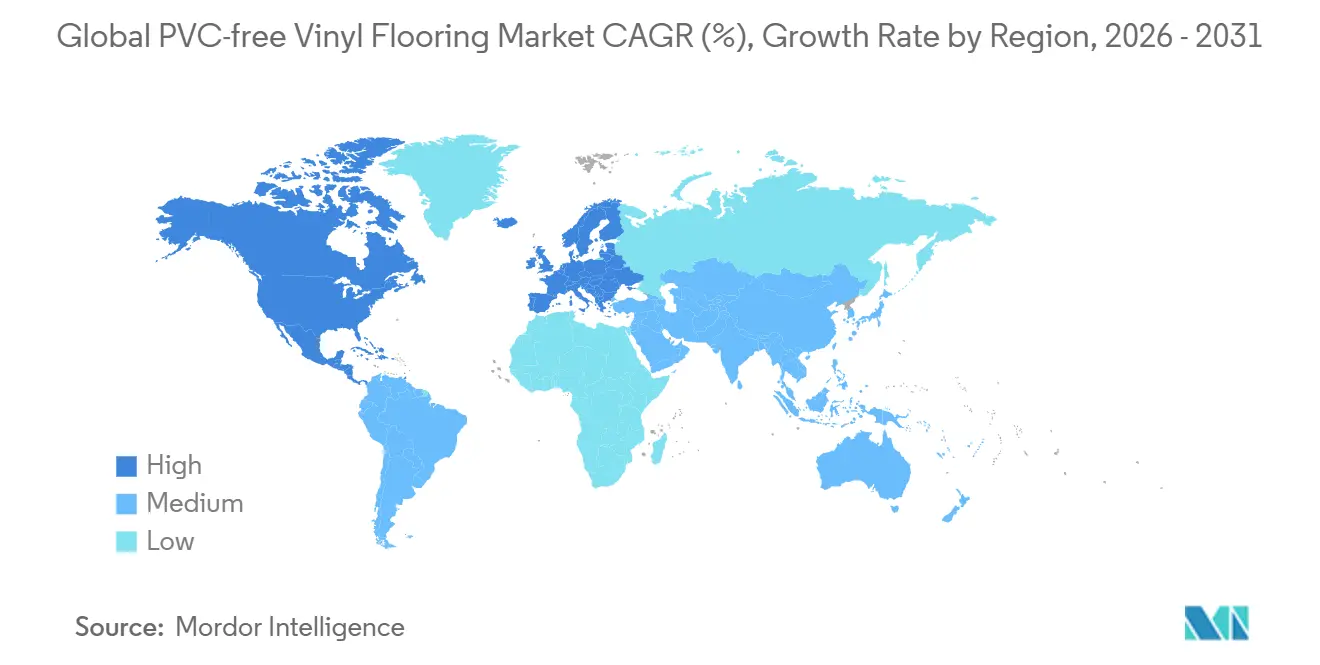

- By geography, North America captured 33.00% of the PVC-free vinyl flooring market in 2025 while Europe is projected to grow at 10.16% CAGR between 2026-2031 on the back of EU circular procurement mandates and ecolabel criteria.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global PVC-free Vinyl Flooring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in green-building certifications (LEED, BREEAM) | +2.1% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Tightening regulations on chlorine and ortho-phthalates | +1.9% | Europe and North America | Short term (≤ 2 years) |

| Healthcare and education demand for low-VOC interiors | +1.7% | North America, Europe, and developed Asia-Pacific | Medium term (2-4 years) |

| Bio-polyolefin breakthroughs enable 100% recyclability | +1.5% | Europe and Japan | Long term (≥ 4 years) |

| EU take-back mandates in public tenders | +1.2% | EU27 with Nordic pilots | Short term (≤ 2 years) |

| Niche OEM uptake in electric RVs and e-buses | +1.1% | North America, Europe, and Asia transit markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Green-Building Certifications

LEED v5 sharpened its material transparency and embodied carbon expectations, which are influencing product selection in institutional and large commercial projects. Procurement teams are prioritizing products with verified EPDs and robust low-emission certifications that map to CDPH Section 01350 or equivalent, reinforcing demand for PVC-free resilient options in health-sensitive spaces. BREEAM guidance updated in 2025-2026 clarifies accepted emissions schemes for indoor products, which further standardizes testing and compliance in the United Kingdom and other adopting markets[1]BREEAM Knowledge Base Editors, “Guidance Note 22 v3.1,” Building Research Establishment, kb.breeam.com. As these frameworks spread across owner requirements, suppliers with third-party verified declarations and proven emissions performance are gaining specification preference. This shift supports a structural mix change in the PVC-free vinyl flooring market toward emission-verified platforms for offices, schools, and healthcare facilities.

Tightening Regulations on Chlorine and Ortho-Phthalates

United States regulatory actions under TSCA and CPSC prohibitions on certain phthalates continue to shape material decisions across interior finishes in education and childcare environments[2]Editorial Team, “Phthalate Regulations in 2026,” The Chemical Company, thechemco.com. EU REACH restrictions and SVHC authorizations continue to exert strong pressure on the use of ortho-phthalates, steering public tenders toward PVC-free chemistries when alternatives are available. The result is an expansion of chlorine-free, ortho-phthalate-free resilient offerings that avoid labeling burdens and reduce regulatory risk for public-sector buyers. These policy dynamics reinforce the case for PVC-free materials in sensitive occupancies, where health-related criteria are strongly weighted in scoring. The PVC-free vinyl flooring market, therefore, benefits from both direct chemical restrictions and buyer risk-management preferences that favor phthalate- and halogen-free platforms.

Healthcare and Education Demand for Low-VOC Interiors

CDPH Section 01350 and related emissions criteria remain the most referenced thresholds for occupied spaces in schools and offices, which makes independent low-VOC certification a recurring prerequisite in public bids. U.S. federal and defense project specifications also reference emissions programs such as FloorScore or GREENGUARD Gold, extending low-VOC requirements to a broader portfolio of public projects. Adhesives must meet CDPH emissions or SCAQMD Rule 1168 VOC content limits, which reinforces a systems approach to indoor air quality for resilient flooring assemblies[3]CDPH.CA.GOV, https://www.cdph.ca.gov/. Hospitals and school districts continue to emphasize verified emission performance and manageable maintenance profiles that support healthy interiors over long lifecycles. These policies and procurement elements are concentrating demand for PVC-free resilient products that demonstrate compliance through accredited testing and recognized certification schemes.

Bio-Polyolefin Breakthroughs Enable 100% Recyclability

Innovation in bio-circular polymers is widening the material palette for PVC-free resilient flooring, with a focus on chemistries that can be reclaimed and reprocessed without performance loss. Mass balance approaches anchored in ISCC PLUS frameworks are enabling the demonstration of renewable content while maintaining product consistency at scale[4]CORPORATE.DOW.COM https://corporate.dow.com/en-us/news/press-releases/dow-introduces-first-bio-circular-flooring-product.html.. Suppliers are combining bio-based polyurethane with other chlorine-free binders and implementing reclamation programs to support closed-loop take-back in commercial settings. As these platforms undergo third-party life-cycle assessments and obtain verified EPDs, their alignment with procurement criteria improves for projects with embodied carbon targets. This trajectory aligns with the EU Circular Economy Action Plan and green public procurement schemes that increasingly reward products with credible take-back and recyclability pathways.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price premium versus conventional PVC flooring, installer hesitation, and supply-chain availability | -1.4% | Global, most acute in price-sensitive residential and light commercial | Short term (≤ 2 years) |

| Limited installer familiarity and tooling adaptation for new substrates | -0.8% | North America and emerging Asia-Pacific | Medium term (2-4 years) |

| Feed-stock volatility for bio-based polymers | -0.6% | Global, stronger in Europe and Asia supply chains | Medium term (2-4 years) |

| Dimensional stability considerations in humid climates | -0.4% | Southeast Asia, coastal India, Latin America, Middle East coastal zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adoption Barriers: Price Premium, Installer Acceptance, and Availability

PVC-free resilient products often cost more than commodity PVC-based alternatives, reflecting resin costs, certification investments, and smaller production runs that are still normalizing. Contractors trained on PVC-based LVT systems may need additional training on substrate preparation and adhesive compatibility when installing chlorine-free and ortho-phthalate-free platforms. Public specifications increasingly mandate emissions-compliant adhesives, which raises the importance of system-level guidance and documented compatibility to avoid warranty issues. Recognized installation and product testing standards are improving clarity for specifiers and installers by defining dimensional tolerances and performance verification. As capacity expands and training improves across regional networks, price and familiarity barriers are expected to ease in institutional and commercial channels that value verified low-VOC performance.

Feed-Stock Volatility for Bio-Based Polymers

Used cooking oil is a key input for several bio-circular polymers and mass balance programs, and its market shows variability driven by renewable diesel and SAF demand. Policy shifts affecting imports and tax credits can tighten or loosen regional availability, which then cascades into quarterly price adjustments for flooring feedstocks. Supply disruptions or price spreads between domestic and imported UCOs can complicate contracting for large public bids that prioritize stable long-term pricing. These factors encourage suppliers to design flexible procurement strategies and to broaden the portfolio of bio-based or circular inputs when technically viable. Near-term volatility is likely to persist until bio-circular markets deepen and indexing instruments for waste-based feedstocks become more standardized across the value chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Format: Planks Lead as Modular Aesthetics Scale

Planks accounted for 66.52% of revenue in 2025 and are expected to advance at 10.07% CAGR through 2031, supported by the preference for wood visuals and modularity in offices, retail, and education projects. This share confirms that architects and facility teams are adopting PVC-free alternatives that meet low-VOC requirements and deliver familiar installation rhythms. Where hygiene and seam minimization are critical, sheet formats continue to serve use cases in healthcare and cleanroom-adjacent spaces aligned with emissions criteria and cleaning protocols. Tile formats support phased renovations and visual zoning in high-traffic interiors, which suits commercial refresh cycles that prioritize minimal downtime. These options are increasingly accompanied by emissions certifications and documentation that meet CDPH Section 01350 thresholds and comparable schemes recognized by procurement teams.

The PVC-free vinyl flooring market is also seeing deeper integration of take-back considerations at the format level, with modular products positioned for selective replacement and improved material recovery. Verified low-emissions credentials and EPDs align these products with LEED v5 and BREEAM pathways, with emissions testing and accredited laboratory procedures enhancing confidence among education and healthcare clients. Tiles and planks support controlled disassembly, which aligns with EU Green Public Procurement language on take-back systems under the Circular Economy Action Plan. Sheet products remain essential in environments requiring seamless surfaces, but must demonstrate clear end-of-life handling to remain favored in public-sector bids. The PVC-free vinyl flooring market size signals that modular formats with robust documentation will continue to set the pace in specifications for institutional and commercial interiors with indoor air quality priorities.

By Installation Method: Click Dominates, Loose-Lay Gains for Circularity

Click-and-interlocking installations accounted for 43.67% of revenue in 2025, reflecting speed, predictability, and reduced site downtime, as adhesives are minimized or avoided. Loose-lay is the fastest-growing method, with a 11.52% CAGR, driven by end-of-life recovery considerations, simplified removal, and alignment with take-back requirements in Europe. Glue-down remains essential for heavy-traffic or specialty environments where peak bond strength and dimensional stability under dynamic loads are prioritized. Public specifications codify adhesive emissions and content rules for occupied spaces, ensuring that full systems are considered at design and procurement stages. These approaches are underpinned by performance standards that define dimensional stability, indentation resistance, and surface integrity for resilient products.

Circularity is a key theme influencing method selection, as tenders specify take-back and reuse plans, including for sports and community facilities that redeploy finished surfaces. Loose-lay systems make disassembly and reuse more practical and further reduce adhesive use, simplifying both installation and end-of-life processes. Click systems deliver consistent fit and shorter schedules that appeal to busy campuses and occupied healthcare environments, provided emissions and indoor air quality thresholds are met. Adhesive choices are documented in submittals with emissions program references that comply with CDPH Section 01350 or an equivalent, strengthening compliance narratives in public-sector bids. These conditions favor installation methods that integrate well with low-VOC adhesives, accredited emissions testing, and closed-loop collection frameworks consistent with EU public procurement guidance.

By End User: Commercial Leads While Vehicle Applications Accelerate

Commercial end users led with 38.00% share in 2025 as hospitals and schools prioritized low-VOC emissions, hygiene, and lifecycle maintenance in product selection. Education and healthcare projects frequently require compliance with recognized emissions programs and standardized testing methods, thereby strengthening the position of PVC-free, resilient formats in public construction. Hospitals specify chemical resistance and cleaning compatibility alongside slip resistance for wet areas, which directs demand to verified resilient solutions with documentation. School districts emphasize healthy interiors and durable surfaces that manage traffic and simplify upkeep over time, which aligns further with PVC-free, emissions-certified platforms. These customers also benefit from growing integration of take-back and reclamation programs to support circular procurement commitments where available.

Industrial and specialized vehicles represent a smaller slice but exhibit the fastest growth, with a 11.71% CAGR, as transit authorities tighten safety and durability standards. Specifications for buses and public fleets codify slip-resistance performance and validate floor conditions over time, which push materials toward documented performance and accredited testing. North American and European fleets align with emissions and material health requirements that favor halogen-free and ortho-phthalate-free systems where feasible. Transit authorities also publish installation and maintenance expectations that stress field durability across multi-year service intervals. This use case is a fit for PVC-free resilient solutions that can demonstrate safety metrics, hygiene, and lifecycle performance through clear, test-backed documentation.

By Distribution Channel: Specialty Retail Leads B2C, B2B Builds Scale

Specialty flooring retailers within B2C/Retail captured 42.00% in 2025, as showrooms and bundled installation services remained relevant for homeowners and small commercial buyers. B2B channels to contractors and builders are the fastest-growing, with a 9.84% CAGR, driven by domestic manufacturing expansions and direct programs that support institutional customers. Suppliers are aligning capacity investments with resilient platforms and take-back offerings to improve lead times and strengthen compliance narratives in public bids. Vertical programs and on-site reclamation services make it easier to meet take-back requirements, even when minimum volumes and collection logistics are challenging. This channel profile supports broader deployment of PVC-free resilient products in multi-site and programmatic builds across education, healthcare, and public administration.

Institutional procurement favors consistent specifications, emissions documentation, and EPDs that can be replicated across multiple projects, all of which align with B2B direct models. These models also ease submittal preparation for accredited testing and emissions programs, which reduces friction for owners and architects. As more suppliers integrate reclamation into service offerings, B2B partners can coordinate end-of-life collection and certification needs across portfolios. This allows public and private owners to build circularity elements into contracts with dimensions and timing that are clear from the project award. The PVC-free vinyl flooring market size outlook for 2026-2031 reflects the expansion of these builder and contractor channels in regions emphasizing circular procurement and domestic production.

Geography Analysis

North America held 33.00% share in 2025 as LEED-aligned projects and emissions-based specifications remained a backbone of public and private procurement. U.S. federal and defense construction documents reference low-VOC emissions programs, which reinforce systems-based compliance for resilient floors and adhesives. Domestic capacity additions in resilient platforms and reclamation services support institutional clients that prefer short supply lines and verified take-back. The education and healthcare segments continue to provide steady volume, with an emphasis on emissions performance and assured maintenance outcomes over time. These buyers prioritize third-party testing and recognized certifications that meet CDPH Section 01350 or equivalent standards widely used in the region.

Europe is expected to pace global growth at 10.16% CAGR through 2031, reflecting the EU’s Circular Economy Action Plan and the integration of take-back systems into green public procurement. Nordic ecolabel criteria and similar frameworks are tightening expectations for emissions and recycled content, which supports platforms with clear reclamation and reprocessing pathways. Public tenders in schools, hospitals, and government offices favor materials with documented emissions performance and established collection logistics. Suppliers with long-running take-back programs and verified EPDs are better positioned as minimum criteria become common within country-level procurement guidance. The PVC-free vinyl flooring market share in the region is supported by harmonized rules that promote circular design, end-of-life accountability, and consistent emissions testing.

Asia-Pacific accounts for a meaningful base with sustained growth through 2031, with activity strongest in mature markets that emphasize emissions and hygiene in healthcare and technology sectors. Standardized approaches to emissions testing and accredited laboratories continue to support adoption in pharmaceutical and medical technology facilities. Public projects in Southeast Asia are balancing cost with performance and durability, with humidity management and lifecycle maintenance shaping specifications. Regional policies on used cooking oil exports and renewable-blended fuels can tighten bio-circular feedstock markets, which the supply chain must navigate to deliver PVC-free, resilient platforms. Owner requirements in Japan and South Korea emphasize emissions and material-safety controls, which align with established low-VOC frameworks and recognized testing regimes.

Competitive Landscape

The market is moderately consolidated at the top, with the five largest suppliers reaching a combined share near the mid-40% range in 2025, while regional and niche players address specialized applications and local preferences. Strategic priorities emphasize emissions certifications, EPDs, and closed-loop collection capabilities that align with public procurement and corporate sustainability programs. Capacity expansions in North America are aimed at supporting resilient platforms with documented reclamation options and emissions assurance across adhesives and surfaces. European incumbents are reinforcing take-back and low-carbon production, providing verified documentation aligned to public tender requirements and ecolabel frameworks. These capabilities are expected to remain differentiators as owners demand proof of low-VOC performance, recyclability, and well-defined end-of-life handling.

Portfolio moves in 2024-2026 include targeted acquisitions to broaden sports and surfaces capabilities, capacity additions that shorten lead times, and new product launches tied to circular objectives. Partnerships in international sports underscore the performance credentials of resilient systems in high-visibility venues, with follow-on reuse supporting circular narratives. Corporate programs now more often include zero-cost pickup thresholds for reclamation, which helps institutional buyers structure multi-site agreements with documented recovery. Adhesives and system-level emissions compliance remain focus areas as owners seek streamlined submittals backed by accredited testing aligned with recognized emissions programs. These shifts strengthen the performance and compliance case for PVC-free resilient platforms in public and private tenders.

Technology developments include the introduction of bio-circular polymers, improved surface treatments, and enhanced testing protocols for resilient flooring. Mass balance approaches enable renewable content accounting while meeting performance criteria verified by third-party assessments. Energy management systems, lab accreditation, and emissions testing that align with CDPH Section 01350 or equivalent strengthen operational credibility in public procurement. Suppliers that integrate capacity, documentation, and reclamation at scale are best placed to expand share as owners enforce consistent verification across programs. The PVC-free vinyl flooring market will therefore reward suppliers that can combine performance, compliance, and circular services in an integrated offer.

PVC-free Vinyl Flooring Industry Leaders

Tarkett S.A.

Forbo Flooring Systems

Interface Inc.

Gerflor Group

Shaw Industries Group Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Gerflor renewed a global partnership with Volleyball World to supply Taraflex sports flooring for VNL and World Championships, expanding to Asian Volleyball Confederation events.

- April 2025: Shaw Industries’ EcoWorx Resilient, a PVC-free and fully recyclable product with a carbon footprint of 5.21 kg CO₂e/m², received a 2025 Edison Award for Innovation in circular design.

Global PVC-free Vinyl Flooring Market Report Scope

| Sheets |

| Tiles |

| Planks |

| Glue-down |

| Loose-lay |

| Click / Interlocking |

| Residential |

| Commercial |

| Industrial & Specialized Vehicles |

| B2C/Retail | Home Centers |

| Specialty Flooring Stores | |

| Online | |

| Local Hardware Shops (unorganized market) | |

| Other Distribution Channels | |

| B2B/Contractors/Builders |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East And Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Format | Sheets | |

| Tiles | ||

| Planks | ||

| By Installation Method | Glue-down | |

| Loose-lay | ||

| Click / Interlocking | ||

| By End User | Residential | |

| Commercial | ||

| Industrial & Specialized Vehicles | ||

| By Distribution Channel | B2C/Retail | Home Centers |

| Specialty Flooring Stores | ||

| Online | ||

| Local Hardware Shops (unorganized market) | ||

| Other Distribution Channels | ||

| B2B/Contractors/Builders | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East And Africa | United Arab of Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the current size and expected growth of the PVC-free vinyl flooring market?

The PVC-free vinyl flooring market size was USD 1.28 billion in 2025 and is projected to reach USD 2.18 billion by 2031 at a 9.5% CAGR during 2026-2031.

Which segments lead and grow fastest in this space?

Planks led by format with 66.52% in 2025 and are projected to grow at 10.07% CAGR, while loose-lay leads growth by installation method at 11.52% CAGR during 2026-2031.

Which regions show the strongest opportunity to 2031?

North America held 33.00% share in 2025, while Europe is projected to grow fastest at 10.16% CAGR through 2031 due to circular procurement and ecolabel criteria.

What procurement or certification trends are shaping specifications?

LEED and BREEAM frameworks, CDPH Section 01350-based emissions criteria, and EU Green Public Procurement language on take-back are shaping specifications and supplier selection.

Where are PVC-free resilient floors gaining traction by end user?

Commercial spaces such as hospitals and schools led with 38.00% in 2025, while industrial and specialized vehicles are the fastest-growing at 11.71% CAGR due to safety and durability requirements

How are distribution channels shifting for these products?

Specialty Flooring Retailers within B2C/Retail captured 42.00% in 2025, while B2B contractors and builders are the fastest-growing at 9.84% CAGR as manufacturers expand domestic capacity and reclamation programs.

Page last updated on: