Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

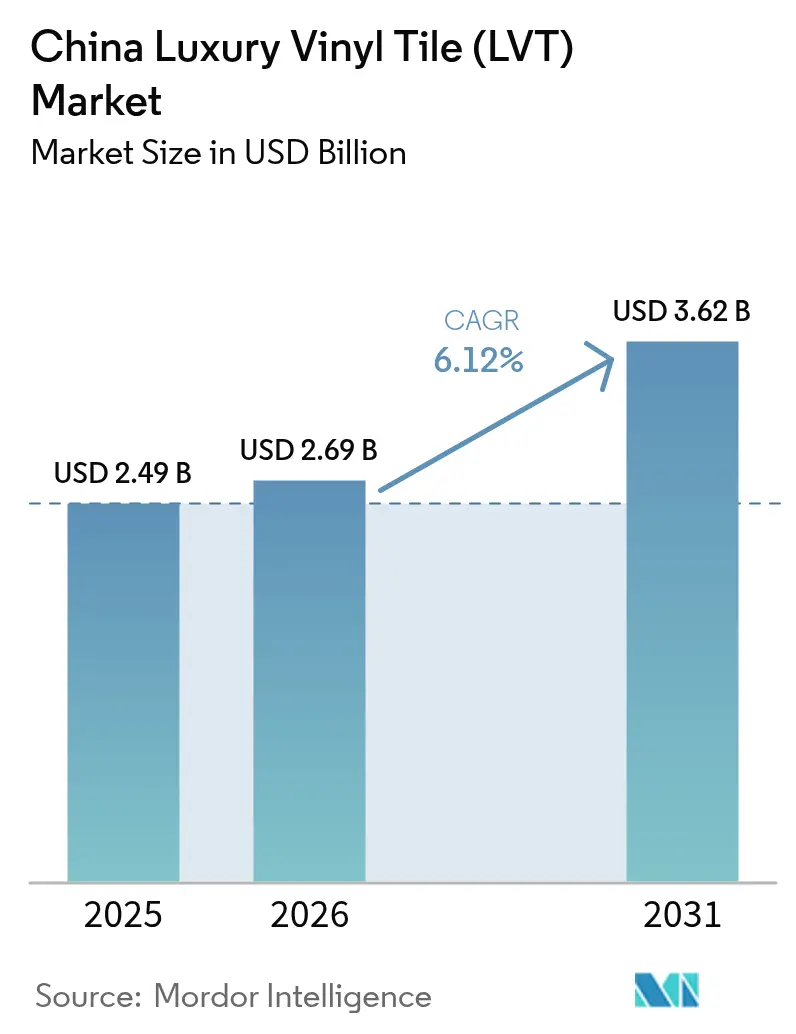

| Base Year Market Size (2025) | USD 2.49 Billion |

| Market Size (2026) | USD 2.69 Billion |

| Market Size (2031) | USD 3.62 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

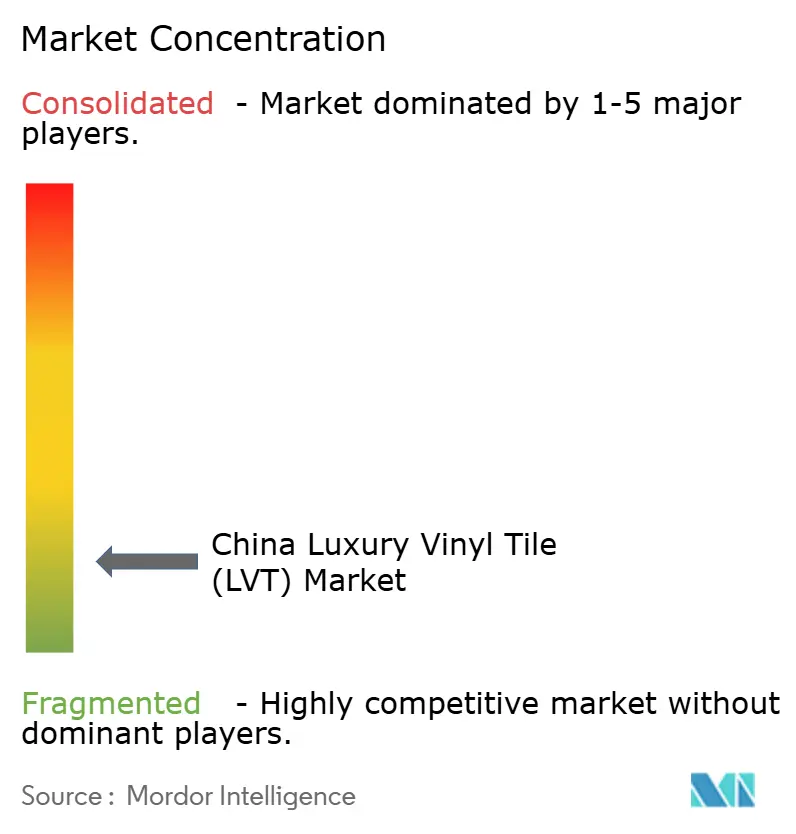

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Luxury Vinyl Tile (LVT) Market Analysis by Mordor Intelligence

The China luxury vinyl tile market size is expected to grow from USD 2.49 billion in 2025 to USD 2.69 billion in 2026 and is forecast to reach USD 3.62 billion by 2031, reflecting a CAGR of 6.12% from 2026 to 2031. Demand is accelerating as renovation programs in older residential towers and public facilities favor durable, quick-install flooring. New residential starts contracted to 392 million square meters in the first eleven months of 2025, while large-scale urban renewal lifted renovation activity and delivered 25,800 community upgrades over January to November 2025, signaling a durable pivot from new-build to retrofit placements[1]National Bureau of Statistics of China, “Housing Starts and Completions, 2025,” National Bureau of Statistics, stats.gov.cn. China's wide temperature swings favor the use of rigid-core formats, particularly stone-polymer-composite boards. Meanwhile, the rise of digital commerce is broadening product access to inland provinces. As a result, despite challenges like raw-material price fluctuations and waste management, the sector continues its robust upward trend, buoyed by renovation incentives, eco-compliance mandates, and the expansion of omnichannel retail.

Key Report Takeaways

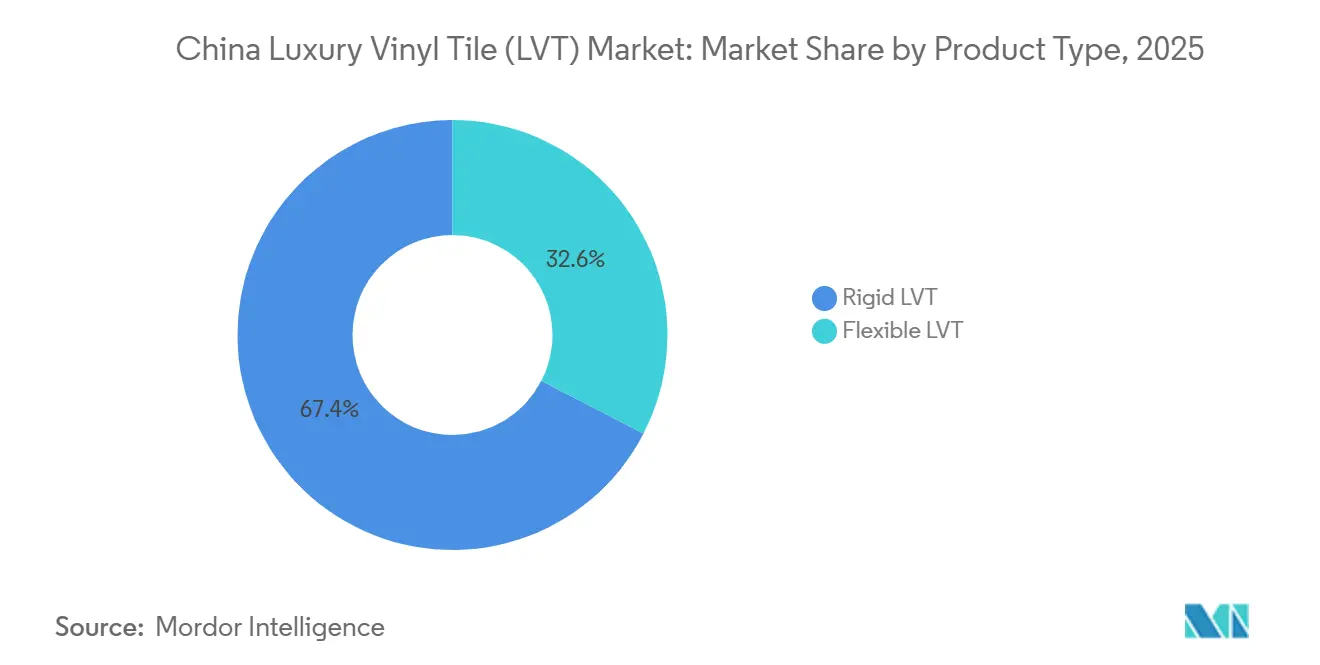

- By product type, rigid SPC led with 67.42% revenue share in 2025, while rigid SPC is projected to grow at a 7.95% CAGR through 2031.

- By installation type, click-lock systems accounted for 41.34% volume in 2025, and click-lock systems are expected to expand at a 6.55% CAGR to 2031.

- By end user, residential applications held a 67.20% share in 2025, while commercial end users are forecast to grow at a 6.84% CAGR through 2031.

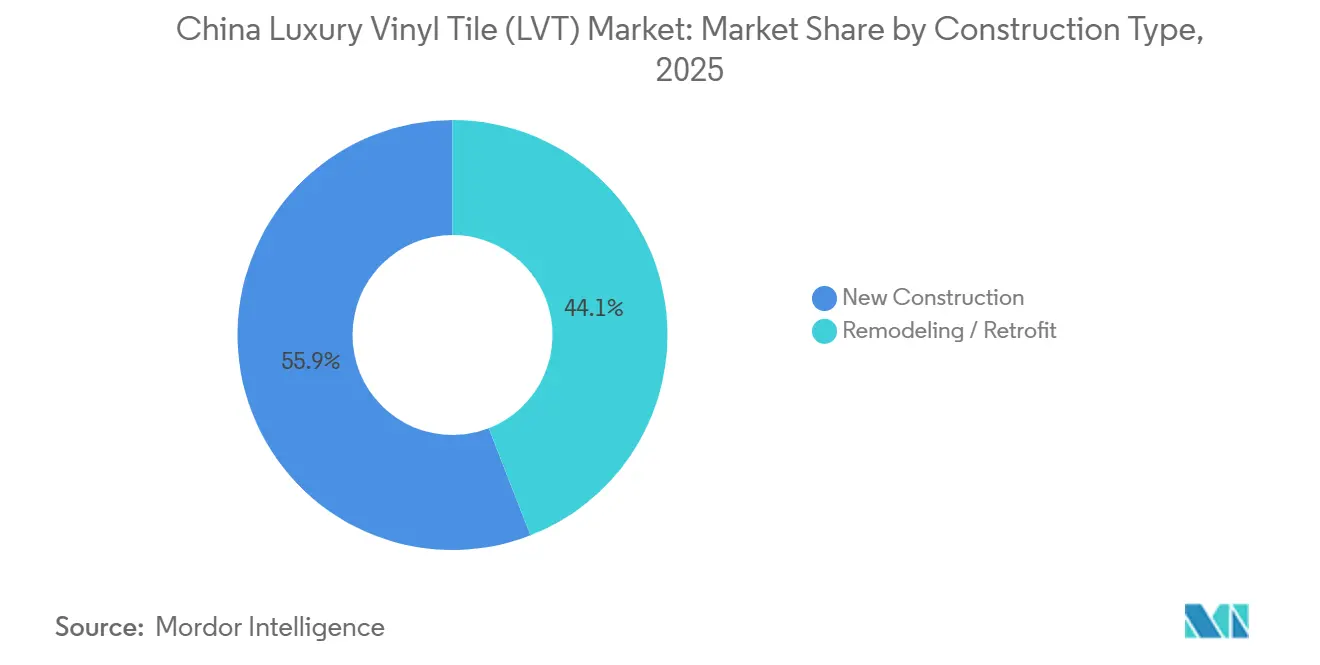

- By construction type, new-build commanded 55.91% share of placements in 2025, while retrofit is expected to advance at a 7.72% CAGR to 2031.

- By distribution channel, offline dealers and home centers held 82.31% share in 2025, while online sales are projected to grow at an 8.15% CAGR through 2031.

- By geography, East China held 27.74% revenue share in 2025, while Southwest China is projected to post the fastest growth at 7.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Luxury Vinyl Tile (LVT) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to rigid-core LVT for faster installation and durability | + 1.8% | National, strongest in East China manufacturing hubs and Southwest retrofit zones | Medium term (2-4 years) |

| Urban renewal and retrofit programs are boosting flooring replacements | + 2.1% | Tier-1 cities (Beijing, Shanghai), expanding to Tier-2/3 cities | Long term (≥ 4 years) |

| Domestic SPC capacity scale lowers unit costs and lead times | + 1.2% | East China (Jiangsu, Zhejiang) and Pearl River Delta | Short term (≤ 2 years) |

| E-commerce discovery and omnichannel sampling lift B2C conversion | + 0.9% | National, with a concentration in urban centers with robust logistics infrastructure | Medium term (2-4 years) |

| Low-VOC preferences in public procurement and premium residential | + 0.7% | National, particularly in Tier-1 cities and public-sector projects | Medium term (2-4 years) |

| Acoustic and hygiene upgrades in healthcare and education | + 0.5% | Urban centers with institutional construction activity, strongest in East and South-Central China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift to Rigid-Core LVT for Faster Installs and Durability

Rigid-core formats reduce labor hours and minimize downtime during renovations, making them the preferred choice for both residential and commercial upgrades nationwide. Installers favor click-lock SPC for retrofits because the floating method shortens job times and eliminates wet-adhesive cure windows, which helps projects stay within compressed schedules in occupied buildings. Production efficiencies are improving as medium- and high-output lines apply automation and process control to reduce scrap and improve yield, including AI-enabled monitoring that cuts rework and stabilizes quality at scale. China’s concentration of SPC capacity near major ports supports short lead times for coastal distributors and keeps freight and turnaround advantages in East China, which remains a core supply zone for national demand. Large-scale public investment programs that fund upgrades in older communities create a demand environment where quick, low-disruption installation is valued, and that steers specifications toward rigid-core click systems that deliver speed and surface stability[2]State Council Information Office, “Policy Briefings on Infrastructure and Urban Renewal,” SCIO, english.scio.gov.cn .

Urban Renewal and Retrofit Programs Boosting Flooring Replacements

Renovations covered 25,800 old residential communities from January through November 2025, exceeding the national target and confirming that retrofit is a durable engine of flooring replacements. Municipal programs elevate energy efficiency and interior performance, which pulls through hard-surface materials that meet green-building and acoustic requirements for multi-family dwellings and community facilities. Targeted funds and procurement templates align specifications toward low-VOC, easy-install solutions that reduce downtime in occupied dwellings and community spaces, helping retrofit teams complete their scope within narrow windows. Remodeling is projected to grow faster than new-build placements across the forecast period, which shifts the mix of the China luxury vinyl tile market toward click-lock and floating systems optimized for overlays and phased occupancy. City-level initiatives in growth corridors, supported by 2024 national infrastructure allocations of CNY 2.9 trillion (USD 402.8 billion), sustain backlogs for flooring vendors that pre-position inventory, technical support, and installation partners in high-priority districts.

Domestic SPC Capacity Scale Lowers Unit Costs and Lead Times

SPC capacity clustered in Jiangsu and Zhejiang complements nearby PVC and component supply, which lowers logistics overhead and stabilizes delivery timelines for high-volume buyers in the China luxury vinyl tile market. Automation and scale economics support competitive unit costs as medium-output lines achieve attractive payback periods at steady utilization, widening the gap with smaller operators on raw-material pricing and yield. Energy-recovery retrofits that capture extruder heat can trim utility bills meaningfully at the line level, further improving cost positions for producers that serve institutional tenders. Certification overhead for ISO systems and third-party indoor air quality schemes is better amortized across larger volumes, which enables scaled suppliers to meet procurement thresholds for public projects without diluting margins. Co-location with export gateways supports short-cycle replenishment for coastal distributors, and that responsiveness reinforces rigid-core share gains in time-sensitive retrofit jobs.

E-Commerce Discovery and Omnichannel Sampling Lift B2C Conversion

Online platforms with virtual-try tools and rapid last-mile logistics widen consumer reach, encouraging direct purchases of premium LVT planks. Direct-to-consumer stores from leading brands showcase SPC assortments, with large stores such as Power Dekor’s Tmall flagship generating about USD 41.7 million, as digital merchandising and sampling compress consideration cycles. Sample kits that ship next-day and white-glove installation scheduling within the same app experience allow buyers to evaluate finishes at home before committing, a hybrid model that blends the strengths of e-commerce discovery and in-home assurance. B2B procurement for builders and contractors is consolidating on digital marketplaces, where factory-direct ordering and centralized logistics shorten lead times for bulk projects and improve visibility into inventory. Logistics reliability in major cities reduces damage and delivery uncertainty for bulky goods, and that reliability helps online channels gain share against legacy dealers in urban markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged slowdown in new residential construction | - 1.4% | National, most severe in Tier-1 and Tier-2 cities | Short term (≤ 2 years) |

| PVC feedstock price volatility compresses margins | - 1.1% | National, concentrated impact in non-integrated producers across East and South China | Short term (≤ 2 years) |

| Indoor air quality scrutiny of adhesives and plasticizers | - 0.6% | National, particularly affecting flexible LVT and glue-down systems | Medium term (2-4 years) |

| Intensifying competition from laminate/tiles at entry price points | - 0.8% | Tier-2 and Tier-3 cities, rural and suburban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prolonged Slowdown in New Residential Construction

New residential starts fell to 392 million square meters in the first eleven months of 2025, which tightened demand from the new-build channel and further shifted placements toward remodeling and institutional upgrades. New-build still represented 55.91% of flooring placements by volume in 2025, leaving the China luxury vinyl tile market exposed to ongoing developer caution in the immediate term. Retrofit orders help smooth the impact, but procurement timing tied to public budgets and permitting can create uneven quarterly patterns for manufacturers and distributors. Larger suppliers that align inventory with municipal projects and affordable housing programs can absorb some volatility, while smaller players face sharper utilization swings when private residential pipelines thin. Over the medium term, the mix shift supports click-lock and floating systems optimized for quick overlays in occupied dwellings as construction cycles remain soft.

PVC Feedstock Price Volatility Compresses Margins

The Chinese luxury vinyl tile market continues to navigate volatility in PVC and related feedstocks, which complicates input-cost planning and pricing for both integrated and non-integrated producers. Inventory cycles in upstream materials can result in periodic overhangs, which pressure spot pricing and erode operating rates in parts of the value chain tied to construction, including floors. Non-integrated extruders face tighter working-capital windows and more frequent price resets, which can force volume sacrifices during adverse swings to maintain covenant headroom. Compliance investments add to fixed costs as tighter VOC and indoor-air standards require emissions testing infrastructure and reformulations to qualify for public tenders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rigid SPC Dominates on Installation Speed and Moisture Resistance

Rigid-core SPC captured 67.42% of the China luxury vinyl tile market share in 2025 and is forecast to expand at a 7.95% CAGR through 2031, widening its lead over flexible LVT in both residential and commercial use cases. The category’s dimensional stability under humidity and temperature variability favors installs in multifamily housing and high-traffic commercial areas where downtime and callbacks need to be minimized. WPC provides an acoustic edge in select institutional and multifamily contexts when paired with foam or cork underlays to lift impact insulation ratings to target thresholds under building guidance[3]Ministry of Housing and Urban-Rural Development, “Building Codes and Green-Building Evaluation,” MOHURD, mohurd.gov.cn . Flexible LVT remains relevant where installers must accommodate uneven subfloors or DIY contexts, but wet-adhesive systems face tighter indoor-air-compliance demands and more line-item testing for public tenders[4]State Administration for Market Regulation, “GB 50333-2013 and GB 50118-2010 References,” SAMR, samr.gov.cn. Production gains from automation and process controls have reduced scrap waste and stabilized SPC quality, which supports consistent field performance and keeps total installed cost competitive.

SPC’s quick, floating installs complement the growth of retrofit programs, where overlays avoid demolition and reduce disturbance in occupied buildings, contributing to a mix shift in the China luxury vinyl tile market. As procurement standards raise VOC expectations for interior materials, rigid-core and PVC-free variants extend the addressable market in schools and hospitals that require third-party indoor-air certifications. Click profiles licensed by major IP holders have become mainstream across Chinese factories, expanding the menu of rigid options for domestic and export buyers. SPC’s share gains in coastal hubs mirror nearby materials and component availability, which maintains short lead times and mitigates inbound freight exposures for distributors. These dynamics collectively reinforce SPC as the anchor product family in specification decisions for speed, moisture protection, and compliance outcomes in the China luxury vinyl tile market.

By Installation Type: Click-Lock Systems Gain on Labor Savings and Retrofit Suitability

Click-lock systems accounted for 41.34% of 2025 volume and are expected to expand at a 6.55% CAGR through 2031 as more projects favor floating installs to avoid adhesive cure times and subfloor moisture tests. Urban-renewal timelines and occupied-building constraints amplify the value of fast, clean installs where tenants remain in place during upgrades, reinforcing click-lock choices in tenders and residential remodels. Licensing ecosystems from Unilin and Välinge have broadened access to robust locking profiles across a large base of Chinese factories, standardizing performance while preserving brand differentiation on décors and wear layers. Glue-down remains relevant in heavy-traffic zones or where wheeled loads and thermal cycling require permanent adhesion, but installer availability and VOC scrutiny make floating systems more attractive in many scopes. Loose-lay serves specialty applications with limited removal windows or raised-access floors, though its overall penetration remains small because perimeter adhesion or tape is still needed in many layouts.

Digital tools and on-carton QR codes that link to installation videos help contractors’ de-skill parts of the workflow, allowing small crews to complete larger areas within tight scheduling windows in retrofit programs. As public buyers emphasize low-VOC compliance and accelerated completion, click-lock products clear certification hurdles without adhesive emissions and support faster room turnover. Material and labor budgets in many retrofit scopes continue to favor floating systems because they combine speed benefits with a lower risk of schedule overruns in occupied spaces. These drivers sustain the adoption curve for click-lock systems and reinforce their position as the default choice in many China luxury vinyl tile market installations. Increased familiarity among inspectors and procurement teams with floating standards also reduces approval friction across municipal projects.

By End User: Commercial Installations Accelerate on Hygiene and Acoustic Mandates

Residential applications held 67.20% of 2025 placements, while commercial end users are projected to grow at a 6.84% CAGR through 2031 as healthcare, education, and government buildings upgrade to low-VOC, easy-clean surfaces. Institutional specifications now emphasize disinfection resistance and acoustic damping under GB codes and hospital design guides, which support rigid-core formats with closed-cell structures and engineered underlays. Education-sector directives on indoor air quality and noise control push flooring toward certified, quiet systems that can be installed with minimal disruption during term breaks. Hospitality and retail also benefit from quick installs as click-lock systems bring lobbies and stores back online faster than traditional wet trades, a priority during compressed refresh cycles. Corporate offices and government buildings frequently specify acoustic underlays to manage open-plan environments, reinforcing the demand for rigid floors that combine stability with sound reduction.

Residential demand still sets the tone for overall volume, but demographic aging and indoor-air awareness guide more homeowners toward certified, low-emission floors that limit odors, reduce maintenance, and improve safety. Within residential retrofits, thin-profile SPC overlays avoid demolition and align with budgets that prioritize speed and cleanliness in occupied apartments, which strengthens rigid-core usage in higher-density cities. Commercial buyers rely on certification stacks that simplify tender compliance and reduce post-install IAQ risks, favoring suppliers with established testing and documentation processes. The balance of specifications shows a tilt to rigid formats across both sectors, with the China luxury vinyl tile market capturing incremental wins where time, hygiene, and acoustics converge. This positioning supports sustained growth in institutional segments that maintain capex programs even during private-residential soft patches.

By Construction Type: Retrofit Projects Outpace New Builds Amid Housing Slowdown

Remodeling is projected to grow at a 7.72% CAGR through 2031, while new construction had a larger 55.91% share in 2025 but faces softer near-term pipelines, especially in Tier-1 and Tier-2 cities. National statistics confirm a pullback in new residential starts, which repositions retrofit as a priority channel for growth in the China luxury vinyl tile market. Retrofit budgets often devote larger shares to flooring within the total interior scope because overlays, leveling, and noise-control measures are bundled to minimize resident disruptions. Click-lock SPC has gained traction in overlays because it avoids demolition, reduces dust and noise, and allows spaces to be reoccupied quickly. Certification and IAQ requirements are simpler with floating installs, which improves approval velocity in public retrofit programs.

Public spending and community-scale programs continue to support a regional spread of retrofit work, including building envelopes and interior finishes that contribute to green-building points where applicable. Municipal subsidies help de-risk flooring demand for suppliers that align technical support and inventory with scheduled upgrades, strengthening order visibility. In new builds, specifications in premium towers may still lean to ceramics or engineered wood, but cost pressures in mass-market developments keep SPC competitive at installed-cost targets. The mix horizon therefore favors retrofit-led growth, with floating rigid cores central to schedules and compliance outcomes in the China luxury vinyl tile market. Over the forecast window, this mix is likely to hold even as private residential activity stabilizes.

By Distribution Channel: Online Sales Surge Despite Offline Dominance

Offline dealers and home centers accounted for 82.31% of 2025 revenue, while online channels, at 17.69% share, are growing at 8.15% CAGR through 2031, on the strength of visualization, sampling, and logistics improvements. Home centers provide tactile sampling and trusted installer networks but face pressure as brands expand direct-to-consumer storefronts and bundle installation with digital scheduling. Power Dekor’s Tmall flagship has surpassed USD 41.7 million by leveraging assortment breadth and rapid sampling that lowers return rates and boosts conversion. Hybrid journeys that start online with AR tools and end with in-home sample viewing and scheduled installs are becoming standard in Tier-1 and Tier-2 cities. B2B procurement for builders is shifting to digital marketplaces where bulk orders, factory-direct pricing, and integrated freight compress cycle times and ease working-capital needs.

Specialty retailers continue to serve complex projects requiring bespoke coordination, but they compete with online assortments that display more SKUs and deliver samples the next day in major cities. Logistics providers now offer scheduled delivery and install windows for bulky goods, which narrows the former service moat of offline stores and strengthens the online value proposition for urban buyers. Social commerce expands the discovery funnel, and brand-owned streams tied to platform events improve education on scratch resistance, moisture performance, and acoustic benefits. As a result, online share is poised to climb steadily even as offline remains significant for tactile evaluation and complex project scoping in the China luxury vinyl tile market. Over time, omnichannel approaches will likely define category leaders that capture both showroom and digital traffic with consistent service levels.

Geography Analysis

East China held 27.74% of China's luxury vinyl tile market share in 2025, supported by concentrated SPC capacity in Jiangsu and Zhejiang and by proximity to major ports that compress replenishment cycles. Shanghai’s urban-renewal pipeline and coastal logistics keep distributors stocked for time-sensitive retrofit orders, including community-scale upgrades executed under national infrastructure allocations in 2024. The region’s supplier base includes export-oriented and domestic-focused producers, which intensifies local competition but also lifts quality service for institutional buyers that require certified products and short lead times. Local procurement and developer familiarity with click-lock rigid cores for fast overlays reinforces the share for SPC in retrofit-heavy urban districts. These dynamics collectively underpin East China’s role as both a production and demand center for the China luxury vinyl tile market.

Southwest China is projected to be the fastest-growing region at 7.18% CAGR through 2031, as infrastructure linkages and logistics upgrades reduce transit times and delivery risk for flooring shipments into interior provinces. As distributors improve service coverage and project support, local contractors can execute more overlays and phased retrofits within municipal templates that favor short downtime and low-VOC materials. South Central hubs anchored by Guangdong also post healthy growth with commercial installations, where hospitality and retail refreshes value speed and moisture performance. In North China, government retrofits that require green-building compliance partly offset declines in private residential activity by prioritizing certified, click-lock systems that avoid adhesive VOCs. Northeast and Northwest demand remains smaller, with colder climates favoring tile in many applications, though overlays with rigid-core floors are gaining in apartments where demolition would disrupt heating systems.

Regional competitive structures vary, with East China remaining the most fragmented due to the density of factories that hold mainstream click licenses, while Southwest markets see more local contract manufacturing that competes aggressively on price but often lacks the certifications needed for large public tenders. As institutional demand rises in fast-growing regions, suppliers with audit-ready quality systems, documented IAQ credentials, and reliable last-mile service stand to gain share. Procurement practices increasingly emphasize supplier readiness and response speed, and that supports scaled producers that can adjust to quarter-by-quarter public funding flows. Across regions, the acceleration in retrofit work ensures that rigid-core overlays and floating installs remain central to growth for the China luxury vinyl tile market. Over the forecast horizon, regional differences in specification preferences are likely to narrow as national standards harmonize IAQ and acoustic expectations.

Competitive Landscape

The Chinese luxury vinyl tile market is highly fragmented, with hundreds of domestic producers and no single player holding a double-digit national share. Licensing ecosystems from Unilin and Välinge have enabled broad adoption of click technologies among Chinese factories, which evens the playing field on core mechanics and shifts differentiation toward design, certifications, and service. Scaled producers that integrate digital print, in-house lab testing, and automation improve their cost positions while meeting public procurement requirements for quality and IAQ documentation. Digital-native and hybrid brands use AR visualization, live consultations, and rapid sampling to capture direct-to-consumer sales online and then convert to scheduled installations with certified crews.

Strategically, vertical integration into décor printing, wear layers, and testing capabilities is becoming a differentiator in tenders and large retail accounts that value shorter lead times and clear compliance documentation. Companies that have introduced PVC-free or bio-attributed rigid-core lines are expanding access to projects governed by stricter procurement rules and sustainability metrics.

On the channel side, brand-owned online storefronts reduce dependency on dealer margins and surface long-tail designs that are hard to stock in physical stores, widening the appeal to younger homeowners. Over the medium term, suppliers that balance omnichannel reach, certification intensity, and installation ecosystems will be best placed to consolidate share as compliance costs and service expectations rise. Fragmentation will persist, but scale advantages in testing, automation, and logistics will continue to shape winners in the Chinese luxury vinyl tile market.

China Luxury Vinyl Tile (LVT) Industry Leaders

CFL Flooring

Novalis Innovative Flooring

Taizhou Huali New Materials (Huali Floors)

Zhangjiagang Yihua Rundong New Material (Yihua)

Power Dekor Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: China’s State Council reported 25,800 old residential communities were renovated in the first eleven months of 2025, surpassing the annual target and supporting retrofit-led demand for fast-install floors.

- October 2025: The Environmental Protection Tax Law amendment expanded taxable VOC categories, reinforcing incentives for lower-emission flooring materials and adhesives in public procurement.

China Luxury Vinyl Tile (LVT) Market Report Scope

Luxury Vinyl is designed to replicate hard surface flooring materials such as stone or wood and is available in planks or tiles. It uses a realistic photographic print film and a clear vinyl layer that opens up a wide variety of design concepts.

The China Luxury Vinyl Tile Market is segmented by Product Type, Installation Type, End User, Construction Type, Distribution Channel, and Geography. By product type, the market is divided into Rigid LVT and Flexible LVT. By installation type, the market is segmented into Click-Lock, Glue-Down, and Loose-Lay. By end user, the market is categorized into Residential and Commercial segments. By construction type, the market is segmented into New and Retrofit. By distribution channel, the market is divided into B2C and B2B channels. Geographically, the market analysis covers East, Southwest, North, South Central, Northeast, and Northwest China. The report provides market size and forecasts for the China luxury vinyl tile market in value (USD) across all the above segments.

By Product Type

| Rigid LVT | Stone Plastic Composite |

| Wood Plastic Composite | |

| Flexible LVT |

By Installation Type

| Click-Lock / Floating |

| Glue-Down |

| Loose-Lay |

By End User

| Residential | |

| Commercial | Hospitality & Leisure |

| Retail & Shopping Centers | |

| Healthcare Facilities | |

| Education | |

| Corporate Offices | |

| Public & Government Buildings | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Remodeling / Retrofit |

By Distribution Channel

| B2C/Retail Consumers | Home Centers |

| Specialty Flooring Stores | |

| Online | |

| Other Distribution Channels | |

| B2B/Contractors/Builders |

By Geography

| East China |

| Southwestern China |

| North China |

| South Central China |

| Northeast China |

| Northwestern China |

| By Product Type | Rigid LVT | Stone Plastic Composite |

| Wood Plastic Composite | ||

| Flexible LVT | ||

| By Installation Type | Click-Lock / Floating | |

| Glue-Down | ||

| Loose-Lay | ||

| By End User | Residential | |

| Commercial | Hospitality & Leisure | |

| Retail & Shopping Centers | ||

| Healthcare Facilities | ||

| Education | ||

| Corporate Offices | ||

| Public & Government Buildings | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Remodeling / Retrofit | ||

| By Distribution Channel | B2C/Retail Consumers | Home Centers |

| Specialty Flooring Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Contractors/Builders | ||

| By Geography | East China | |

| Southwestern China | ||

| North China | ||

| South Central China | ||

| Northeast China | ||

| Northwestern China | ||

Key Questions Answered in the Report

What is the size and growth outlook for the China luxury vinyl tile market?

The China luxury vinyl tile market size was USD 2.49 billion in 2025 and is projected to reach USD 3.62 billion by 2031 at a 6.12% CAGR over 2026 to 2031.

Which product type leads demand in China for luxury vinyl tile?

Rigid-core SPC led with 67.42% share in 2025 and is forecast to grow at 7.95% CAGR through 2031, supported by fast installs and dimensional stability.

Which regions are most important for growth in China luxury vinyl tile?

East China held 27.74% of revenue in 2025, while Southwest China is projected to grow the fastest at 7.18% CAGR through 2031 due to improved logistics and retrofit activity.

How is channel mix evolving for China luxury vinyl tile?

Offline dealers and home centers had an 82.31% share in 2025, while online channels at 17.69% are growing at an 8.15% CAGR with AR visualization, sampling, and better last-mile services.

What are the key regulatory factors shaping China luxury vinyl tile specifications?

GB 18584-2024 and related standards raise VOC and hazardous-substance thresholds, and certifications like FloorScore and GREENGUARD are increasingly required in tenders.

Which end-user segment is growing the fastest in China luxury vinyl tile?

Commercial end users are projected to grow at a 6.84% CAGR on hygiene and acoustic mandates across healthcare, education, and public buildings.

Page last updated on: