Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

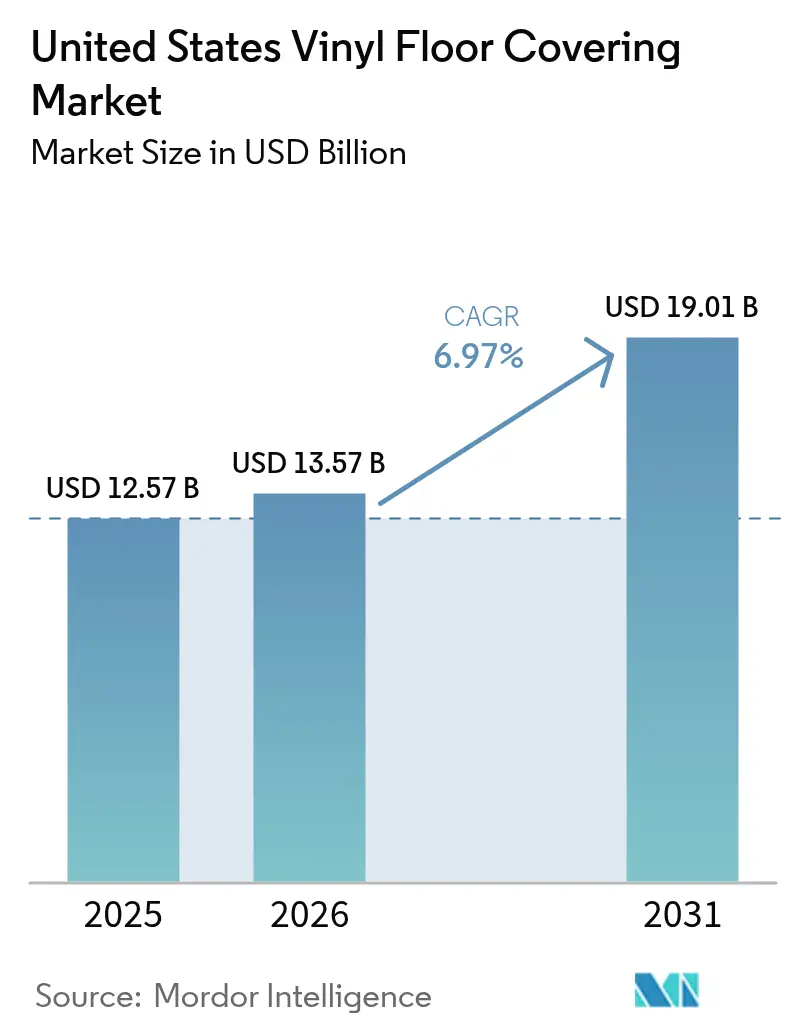

| Base Year Market Size (2025) | USD 12.57 Billion |

| Market Size (2026) | USD 13.57 Billion |

| Market Size (2031) | USD 19.01 Billion |

| Growth Rate (2026 - 2031) | 6.97% CAGR |

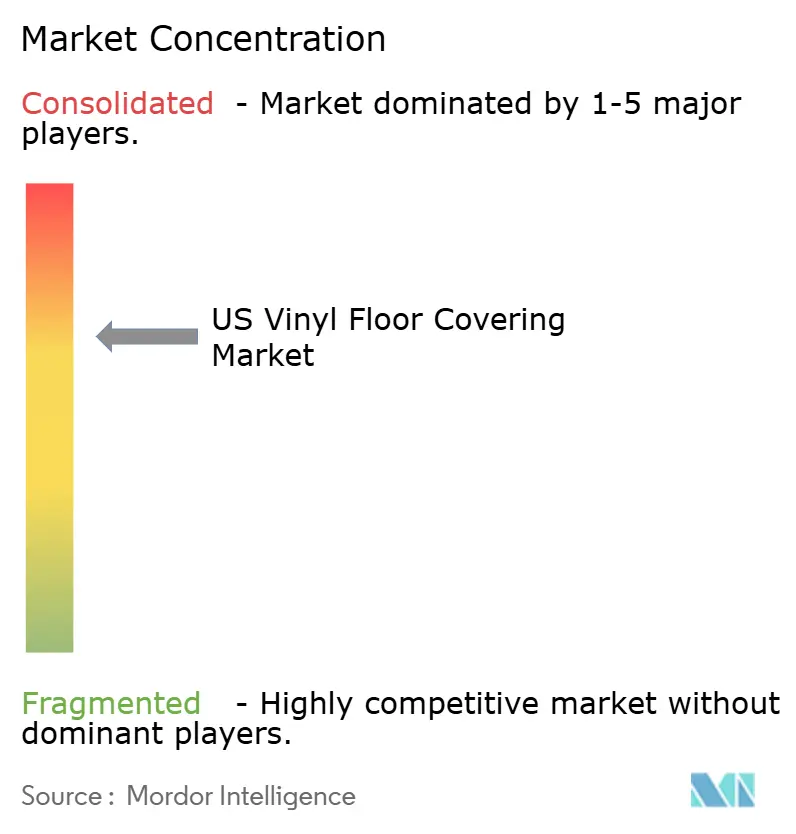

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Vinyl Floor Covering Market Analysis by Mordor Intelligence

The United States vinyl floor covering market size is projected to be USD 12.57 billion in 2025, USD 13.57 billion in 2026, and reach USD 19.01 billion by 2031, growing at a CAGR of 6.97% from 2026 to 2031. Demand continues to shift toward premium rigid core formats because they combine waterproof performance, strong dimensional stability, and click-lock installation, which reduces labor time. Domestic manufacturing expansions from leading producers support faster replenishment cycles and reduce tariff exposure on rigid core sourced from China. Institutional buyers in healthcare and education favor vinyl for hygiene, acoustics, and lifecycle cost control, which reinforces nonresidential momentum. Regional growth patterns favor the Southeast on the back of multifamily activity, while the West benefits from sustainability policies and retrofit needs.

Key Report Takeaways

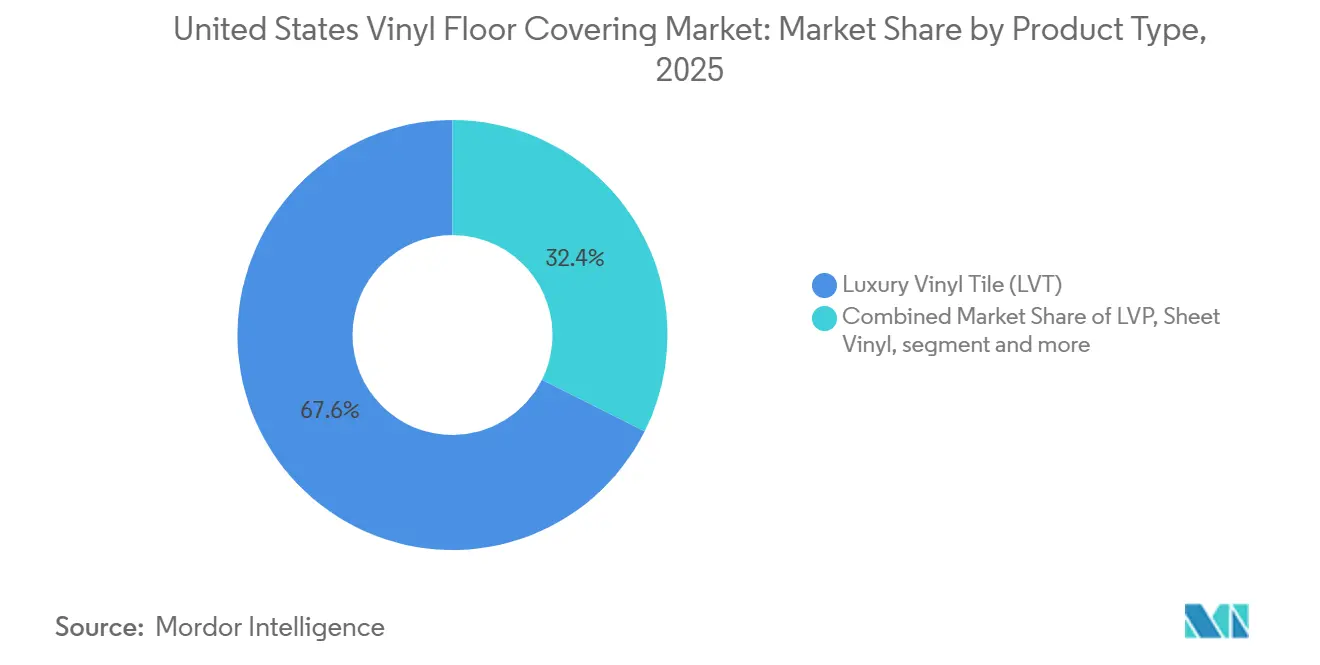

- By product type, Luxury Vinyl Tile led with a 67.62% revenue share in 2025, while LVT is forecast to expand at a 8.64% CAGR through 2031.

- By installation method, interlocking planks accounted for 53.65% of shipments in 2025, and glue-down formats are projected to record a 7.62% CAGR through 2031.

- By end-user, residential accounted for 70.92% of the United States vinyl floor covering market in 2025, while commercial applications are projected to grow at a 9.28% CAGR through 2031.

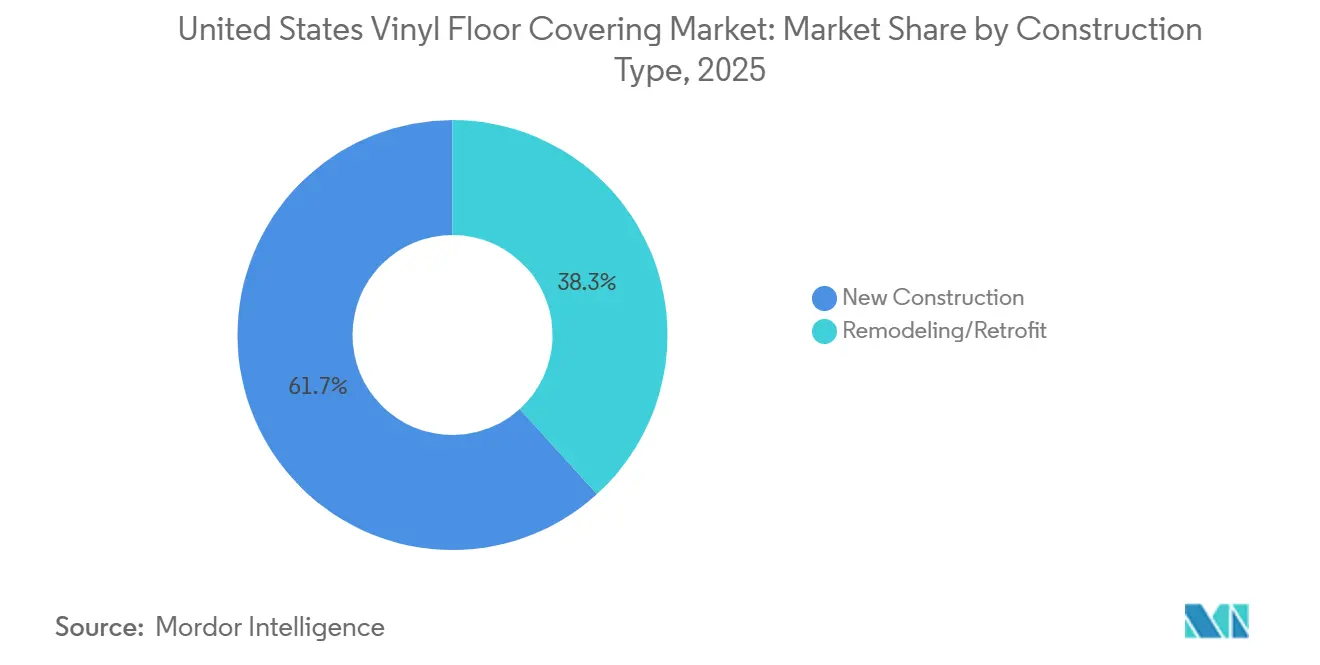

- By construction type, new construction accounted for 61.74% of volume in 2025, while remodeling and retrofit are projected to expand at a 7.76% CAGR through 2031.

- By geography, the Southeast held the largest share at 23.85% in 2025, while the West region is projected to grow at a 7.94% CAGR to 2031.

- By distribution channel, B2C retail accounted for 69.40% in 2025, while B2B contractor and builder pipelines are projected to post the highest CAGR of 8.53% through 2031.

- By company concentration, Mohawk, Shaw, AHF Products, Tarkett, and Mannington accounted for 73% of revenue in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Vinyl Floor Covering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Remodeling rebound 2025–2027, lifting LVP/LVT replacement cycles | +1.8% | National, with early gains in aging housing corridors, the Midwest, and the Northeast | Medium term (2-4 years) |

| Rigid core SPC performance and waterproofing displacing laminate and wood | +2.1% | National, strongest in Southeast multifamily and West sustainability zones | Short term (≤ 2 years) |

| Healthcare and education hygiene and lifecycle cost preferences boost vinyl | +1.3% | National, concentrated in the Midwest healthcare and Southeast education expansion. | Medium term (2-4 years) |

| Omnichannel distribution scale via home centers, specialty retail, and e-commerce | +0.9% | National, accelerated in metro markets with D2C adoption | Short term (≤ 2 years) |

| Domestic SPC/LVT capacity expansions shorten lead times and improve service | +1.5% | National, anchored in Georgia and Tennessee manufacturing clusters | Medium term (2-4 years) |

| Digital printing/EIR aesthetics accelerate premium mix and reduce cannibalization | +1.2% | National premium adoption in coastal metros with spillover to Sunbelt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Remodeling Rebound 2025–2027 Lifting LVP/LVT Replacement Cycles

Remodeling activity remains a durable tailwind for floor replacement cycles, and it benefits vinyl due to waterproof performance, simpler installations, and strong design optionality. The lock-in effect from earlier mortgage vintages increases the likelihood that homeowners upgrade floors where they live rather than move, and that dynamic keeps kitchen and bathroom refresh projects in focus. In this environment, click-lock systems support faster project turnover relative to adhesive formats, and that efficiency reinforces vinyl’s role in do-it-for-me installations. Industry outlooks continue to indicate steady remodeling growth through 2027, which aligns with premium-mix migration toward rigid core LVT in owner-occupied homes and rental units. In institutional buildings that renovate in phases, vinyl’s hygiene and maintenance advantages help it capture a larger slice of planned lifecycle upgrades. This pattern supports the United States vinyl floor covering market as producers scale domestic capacity to align with recurring replacement demand.

Rigid Core SPC Performance and Waterproofing Displacing Laminate and Wood

Rigid core SPC has reset performance expectations, combining dimensional stability, dent resistance, and complete waterproofing, which allows it to capture share from laminate and engineered wood across residential and commercial projects. The limestone-polymer core limits expansion and contraction, which reduces joint separation under seasonal temperature swings and helps deliver a cleaner installed appearance under heavy rolling loads. Specifiers value that SPC allows large-format installations with fewer transitions and click-lock designs, cutting labor hours in occupied spaces where downtime must be minimized. Within LVT, rigid formats reached deep penetration and continue to gain because they satisfy performance and convenience needs at competitive price points. Product innovation from leading brands pairs high-definition printing with embossed-in-register textures that narrow the gap to hardwood and stone aesthetics, enabling premium substitution without trade-offs on moisture. This broad adoption supports higher throughput in the United States vinyl floor covering market as retail, healthcare, education, and hospitality projects converge on waterproof cores.

Healthcare and Education, Hygiene and Lifecycle Cost Preferences Boost Vinyl

Hospitals, outpatient clinics, and long-term care facilities prioritize infection control, acoustics, and cleanability, conditions where resilient vinyl offers practical advantages. Vinyl’s non-porous surfaces and heat-welded seams in sheet formats simplify sanitation workflows, and newer rigid core options deliver wear resistance that stands up to wheelchairs, beds, and heavy traffic. Education facilities face similar constraints, and many opt for LVT in corridors, cafeterias, and classrooms to lower maintenance and reduce disruptions linked to frequent replacements. Manufacturers now offer healthcare-focused resilient lines with antimicrobial surface treatments and robust wood and stone visuals to support healing environments. In procurement, lifecycle modeling shows that lower maintenance and longer wear life reduce the total cost of ownership compared to carpet in high-traffic areas. These attributes reinforce recurring specification in public and private institutions, which sustains nonresidential momentum in the United States vinyl floor covering market[1]Mohawk Industries, “Investor Update and 2026 Outlook,” Mohawk Industries Investor Relations, mohawkind.com.

Domestic SPC/LVT Capacity Expansions Shorten Lead Times and Improve Service

New and expanded United States facilities are compressing lead times to less than four weeks for common assortments, improving service levels for distributors and national accounts. Shaw expanded SPC and LVT production in Ringgold, Georgia, with a USD 90 million investment that more than doubles domestic capacity and supports advanced emboss textures and stability for loose-lay applications by 2026. AHF Products purchased a 328,000 square foot facility in Cartersville, Georgia, in November 2025, lifting its United States manufacturing network to 12 plants and adding automation to support a range of wear layers and locking systems [2]AHF Products, “AHF Products Acquires Cartersville, Georgia Facility,” AHF Products News, ahfproducts.com. Mohawk reports ongoing United States investments and restructuring actions to optimize cost and throughput, which position the company to meet quick-ship needs as demand recovers. These expansions align with preferences among retailers, contractors, and institutional buyers to source tariff-free, domestically made rigid core where possible. Local production also mitigates port delays and freight variability, which reduces the inventory risk in seasonal or fast-changing design assortments. As a result, domestic capacity acts as a structural driver for the United States vinyl floor covering market through the medium term.

Restraints Impact Analysis*

| Driver / Restraint (as applicable in title case) | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Section 301 tariffs and compliance risks raise landed costs for China-sourced SPC/LVT | -1.4% | National, acute for importers reliant on Asian supply chains | Short term (≤ 2 years) |

| Retailer chemicals policies tighten formulations and compliance | -0.6% | West Coast and Northeast OTC states, especially CA, NY, WA | Long term (≥ 4 years) |

| PVC resin/plasticizer price volatility compresses margins | -0.9% | National, feedstock-dependent regions face acute pressure | Short term (≤ 2 years) |

| New construction softness and rate-sensitive housing demand caps near-term growth | -1.1% | National, most severe in high-cost metros with affordability challenges | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Section 301 Tariffs and Compliance Risks Raise Landed Costs for China-Sourced SPC/LVT

A 25% Section 301 tariff remains in force on many Chinese vinyl tile and plank products, increasing landed costs and compliance complexity for import-reliant firms. The measure covers a broad set of vinyl floor coverings, and policy reviews have kept the duty in place, which alters sourcing economics when compared with tariff-free domestic output. United States trade authorities and industry submissions have documented the sharp rise in rigid core imports before the duty and a subsequent investment response in United States capacity [3]U.S. Trade Representative, “Section 301 Tariff Actions: Status and Reviews,” Office of the United States Trade Representative, ustr.gov. Enforcement of the Uyghur Forced Labor Prevention Act adds documentation burdens and detention risks for shipments tied to restricted regions, and many importers continue to adapt compliance protocols. In practice, the tariff advantage supports “Made in USA” positioning and diversifies the supply base, although some entry-level SKUs remain cost-competitive from Asia after freight swings. These forces collectively temper near-term import volumes while accelerating domestic scale in the United States vinyl floor covering market [4]U.S. Customs and Border Protection, “Uyghur Forced Labor Prevention Act Operational Guidance,” U.S. Customs and Border Protection, cbp.gov.

Retailer Chemicals Policies (Phthalates/PFAS) Tighten Formulations and Compliance

Large home centers adopted chemical policies that phase out ortho-phthalates in vinyl flooring, which accelerated an industry shift to alternative plasticizers and new surface treatments. Home Depot communicated a commitment to eliminate added ortho-phthalates in vinyl flooring and related categories, and that decision set a benchmark for other retailers and suppliers. Lowe’s adopted similar restrictions in flooring assortments, which signals consistent expectations for consumer-facing products. In parallel, Washington State regulations enforce ortho-phthalate caps of 1,000 ppm effective January 1, 2025, with structured reporting for covered products. These policies encourage wider adoption of non-phthalate alternatives and PVC-free options in projects driven by green building standards. Compliance investments raise costs in the near term, yet they support product differentiation for low-VOC, third-party certified lines in healthcare, education, and public projects. The result is a clearer standard for acceptable formulations that shapes assortments across the United States vinyl floor covering market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rigid Core Dominance and Premium LVT Migration

Luxury Vinyl Tile accounted for the largest position in 2025, with a 67.62% share and a projected 8.64% CAGR to 2031 as premium-mix migration continues in both residential and institutional uses. Within LVT, rigid core formats, including SPC and WPC, achieved deep penetration by 2025, enabled by dimensional stability and waterproof cores that address performance pain points in kitchens, baths, corridors, and tenant turnover refreshes. Click-lock systems reduce labor time, boosting adoption in do-it-for-me and professional contractor channels that manage tight schedules. Enhanced digital printing and embossed-in-register textures improve visual realism that narrows the gap to hardwood and ceramic, supporting trade-up behavior within vinyl rather than switching to other finishes. The combination of performance and aesthetic gains helps LVT displace flexible LVT and sheet in many retrofit situations. These patterns reinforce the leadership of LVT as buyers emphasize lifecycle cost and ease of maintenance across the United States vinyl floor covering market.

LVT’s breadth of constructions supports distinct use cases, and SPC leads to rigid core in moisture-prone spaces because it balances thin profiles, dent resistance, and thermally stable cores. WPC platforms remain relevant where comfort underfoot and sound attenuation are priorities, which adds depth in single-family areas and targeted hospitality or senior living applications. Digital printing pipelines enable faster visual refreshes that can cycle with seasonal assortments and retailer resets without long offshore lead times. This responsiveness helps national accounts and specialty retailers maintain tight SKU sets with high turns. Builders and remodelers gravitate toward lines with performance guarantees around wear layers and stain resistance, and that new assurance lowers perceived risk for rapid installations. The overall result is a durable product roadmap for the United States vinyl floor covering market as category leaders invest in domestic LVT lines, premium rigid cores, and flexible offerings for clinical or multifamily needs.

By Installation Method: Interlocking Planks Lead, Glue-Down Accelerates in Commercial

Interlocking tiles and planks led with 53.65% of the United States vinyl floor covering market share in 2025, as the floating method suited both DIY and do-it-for-me projects with minimal disruption in occupied spaces. This format allows faster installation, easier plank replacement after localized damage, and avoids in-place adhesive fumes or cure times. Mechanical locking designs have improved over successive product generations, and they now offer stable seams, better tolerance of subfloor variation, and stronger edge retention. Retailers and installers position floating rigid core as a reliable solution for quick-turn renovations, which reduces overall labor hours and gets spaces back into use sooner. In multifamily, click systems are widely deployed in living areas and bedrooms due to the repairability between tenants. These dynamics align with broad consumer and contractor preferences in the United States vinyl floor covering market.

Glue-down formats are growing at a projected 7.62% CAGR through 2031, gaining share in corridors, retail aisles, and other heavy rolling-load zones where full-spread adhesives offer better stability. Commercial contractors favor dryback LVT in retrofit programs because it balances price and long-term performance when maintained under routine schedules. For institutional work, a glue-down sheet remains essential in sterile clinical spaces that require welded seams and cove base transitions. Loose-lay and hybrid systems also carve out niches where rapid lift-and-replace programs are prioritized, although they are most effective in specific subfloor conditions. Installation method choice reflects a trade-off between speed, permanence, and performance criteria, and the resulting mix supports growth across project types. These installation trends help distribute demand across floating and adhesive-backed lines in the United States vinyl floor covering market.

By End-User: Residential Dominates, Commercial Installations Surge

Residential applications accounted for 70.92% of volume in 2025, driven by replacement cycles and the need for waterproof, easy-care surfaces that handle kitchens, bathrooms, and active family areas. Homeowners and property managers value click-lock rigid core for simple repairs and upgrades without major demolition, and that supports sales in home center and specialty retail channels. Design quality has improved with embossed-in-register textures, which increases consumer willingness to upgrade within vinyl ranges for a more natural look. For households with pets and kids, scratch resistance, stain protection, and low-VOC certifications are now routine buying criteria that align with leading residential LVT lines. These features underpin frequent specification of vinyl in multifamily turnovers where durability and scheduling certainly are paramount. Together, these drivers sustain residential leadership in the United States vinyl floor covering market.

Commercial installations are the fastest-growing end-user segment with a 9.28% projected CAGR through 2031 as healthcare, education, retail, and hospitality emphasize hygiene, durability, and overall value. Healthcare facilities set tight performance requirements for cleanability and wear under rolling loads, and resilient vinyl meets those needs while delivering wood and stone visuals for warmer spaces. Schools prioritize low maintenance and long life in corridors, cafeterias, and classrooms, which favors thicker wear layers and repeatable installation methods. Retail environments place a premium on uptime and uniform appearance across locations, which aligns with SPC’s waterproof core and scratch resistance. Hospitality brands adopt vinyl in bathrooms and back-of-house areas for moisture control, and newer premium visuals are migrating into guestroom areas to support consistent looks and fast refreshes. These specifications strengthen the nonresidential mix within the United States vinyl floor covering market.

By Construction Type: New Construction Leads, Remodeling/Retrofit Outpace

New construction accounted for 61.74% of volume in 2025 as builders value the balance of cost, speed, and performance across tract housing, multifamily, and selected commercial projects. Builder-grade assortments often include dryback LVT and sheet options where straightforward maintenance and standardized visuals help manage cost. In offices, healthcare, and education, rigid core formats have carved out roles in areas not requiring fully seamless installations, and they contribute to specification diversity. Public projects frequently require low-emitting products with independent certifications, and resilient vinyl lines are available to satisfy these requirements. New builds also benefit from the simplicity of scheduling around adhesive cure windows or from choosing floating options for speed. This mix underpins the largest share for new construction in the United States vinyl floor covering market.

Remodeling and retrofit are projected to grow at a 7.76% CAGR through 2031, exceeding the new construction growth rate as households and institutions invest in existing spaces. In homes, lock-in mortgage dynamics increase renovation intensity, and LVT’s waterproof performance makes it a default choice for kitchens and baths. Multifamily renovations rely on click-lock and selected glue-down options to reduce downtime between tenants while preserving design consistency across units. Public sector and resilience programs in flood-prone areas also favor resilient flooring where waterproof performance and rapid return-to-service are critical. Institutional retrofits in healthcare and education balance aesthetics with hygienic performance and easier maintenance programs. Together, these needs accelerate retrofit share within the United States vinyl floor covering market.

By Distribution Channel: B2C Retail Dominant, B2B Contractor Pipelines Accelerate

B2C retail dominated with 69.40% in 2025 as home centers and specialty flooring retailers combine nationwide access with curated assortments and in-store displays. Big-box retailers reinforce safety and sustainability standards through chemical policies that exclude added ortho-phthalates, which shape vendor formulations and strengthen consumer trust. Specialty stores differentiate with deeper sample libraries, design consultation, and bundled installation, which support higher-end WPC and digitally enhanced LVT lines. Online discovery and visualization tools help consumers preview wood and stone looks, and sample programs reduce friction for style selection. Together, these efforts maintain B2C strength within the United States vinyl floor covering market across DIY and do-it-for-me segments.

B2B contractor and builder pipelines are projected to grow at an 8.53% CAGR through 2031 as institutions, developers, and national retail accounts plan rolling renovations and new schedules. Manufacturers support this channel with specification documents, low-emission certifications, and local inventory programs that support quick turns. Domestic capacity expansions at Shaw, AHF Products, and others shorten delivery times, which reduces working capital tied up in inventory for distributors. E-commerce also expands in commercial procurement with a projected 9.64% CAGR through 2031 as buyers adopt digital tools to streamline sampling and ordering. These channel dynamics broaden access to assortments and help align supply to regional project cycles across the United States vinyl floor covering market.

Geography Analysis

The Southeast held 23.85% of the United States vinyl floor covering market share in 2025, supported by multifamily completions, in-migration, and favorable cost structures that keep new builds and renovations moving. The region is also home to a resilient flooring manufacturing cluster, including Shaw’s Ringgold expansion and AHF Products’ Cartersville facility, which anchors supply chains and reduces lead times for distributors and builders. Tourism-oriented markets lean on waterproof LVT for hospitality back-of-house and guest-facing wet areas, and education and healthcare spending in states like North Carolina and Tennessee sustains commercial installation pipelines. Proximity to production also supports quick-ship programs for home centers and specialty retailers serving fast-growing metros. These features reinforce the Southeast’s leadership in the United States vinyl floor covering market.

The West is forecast to expand at a 7.94% CAGR through 2031, supported by stronger sustainability mandates and commercial retrofit activity in technology hubs. Washington State’s phthalate limits of 1,000 ppm in vinyl flooring, effective January 1, 2025, create clear compliance thresholds that help push formulations to lower emissions. California’s public sector projects and private office retrofits require certified, low-VOC options, and newer PVC-free resilient platforms from large suppliers aligning with these priorities. Western commercial markets also lean on fast replacement cycles in retail and hospitality to keep space current and in service. This policy and retrofit environment favor premium LVT and high-spec resilient products in the United States vinyl floor covering market.

The Midwest and Northeast combine significant institutional footprints with elevated median housing ages that support steady replacement cycles. In the Midwest, large healthcare systems and education networks sustain baseline nonresidential demand, and contractors favor glue-down LVT for corridors and heavy-traffic areas. The Northeast benefits from ongoing remodeling in older housing stock, where vinyl’s waterproof performance is valuable in kitchens and bathrooms. Office and mixed-use retrofits continue to shape urban markets, and return-to-office adjustments add periodic project waves. Specialty retailers and distributors in these regions rely on domestic inventory programs to respond to seasonal demand spikes. These regional fundamentals support the diversity of project types across the United States vinyl floor covering market.

Competitive Landscape

The United States vinyl floor covering market is moderately concentrated, with the top five producers accounting for more than half of revenue in 2025, while numerous mid-sized and specialist brands compete in targeted niches. Leading companies have prioritized domestic manufacturing to reduce lead times, manage costs, and buffer against tariff and compliance risks on imports. Shaw’s USD 90 million expansion in Ringgold, Georgia, more than doubles its United States resilient capacity by 2026 and supports new emboss textures and improved stability, broadening application formats. AHF Products’ acquisition of a Cartersville, Georgia, plant in November 2025 adds rigid-core automation and expands its United States footprint to 12 plants. Mohawk’s restructuring actions and capital investments point to improved throughput and cost positions as housing-related categories recover.

Product strategies center on premium visuals and improved performance. Brands are using high-definition digital printing paired with embossed-in-register textures to deliver wood and stone looks that compete in mid- to upscale spaces without moisture risks. Leading portfolios also emphasize low-emission certifications to serve public sector, healthcare, and education projects. In residential assortments, scratch resistance, stain protection, and pet-focused performance features form a consistent story across premium rigid core lines. These moves serve to protect the share against ceramics and wood in areas where vinyl’s waterproof and maintenance profile is compelling. As a result, LVT remains the anchor for innovation cycles in the United States vinyl floor covering market.

Go-to-market strategies blend home center reach, specialty retail service, and B2B contractor programs. Retailers provide curated assortments with visualizers and sample programs that lower consumer decision friction, while specialty stores deliver design guidance for higher-end projects. B2B contractor pipelines grow with institutional and multifamily schedules, and manufacturers support these channels with spec documentation, training, and local inventory. Companies also emphasize circular initiatives and take-back programs where feasible, aligning with customer sustainability goals in commercial segments. These channel strategies help brands balance volume with a premium mix in the United States vinyl floor covering market.

United States Vinyl Floor Covering Industry Leaders

Mohawk Industries Inc.

Armstrong Flooring

Shaw Industries Group Inc.

Mannington Mills Inc.

Tarkett N.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: AHF Products completed the purchase of the former Well-made manufacturing facility in Cartersville, Georgia, expanding its domestic network to 12 manufacturing plants and enhancing rigid core production capabilities with advanced automation for various product formats and wear layers.

- July 2025: Mohawk Industries published its 16th annual impact report, highlighting PVC-free resilient developments, reductions in emissions intensity, and increased renewable energy consumption.

- April 2025: Shaw Industries released its 2024 Corporate Sustainability Report, describing its EcoWorx Resilient platform and expanded product takeback programs.

United States Vinyl Floor Covering Market Report Scope

Vinyl floor covering is a type of resilient floor covering made by combining natural and synthetic polymer materials placed in repeating structural units. It is a synthetic flooring material that is water- and stain-resistant. The report covers a complete background analysis of the vinyl floor covering market. It includes emerging trends by segments and regional markets, significant changes in market dynamics, and a market overview. The report also features a qualitative and quantitative assessment by analyzing data gathered from industry analysts and market participants across key points in the industry's value chain. The US Vinyl Floor Covering Market is segmented by product (vinyl sheet, vinyl composite tile, and luxury vinyl tile), end user (contractors, specialty stores, home centers, and others), and distribution channel (residential replacement, commercial, and builder). The report offers Market size and forecasts for US Vinyl Floor Covering Market in terms of transaction volume and/or revenue (USD) for all the above segments.

By Product Type

| Luxury Vinyl Tile (LVT) | Stone Plastic Composite (SPC) |

| Wood Plastic Composite (WPC) | |

| Luxury Vinyl Plank (LVP) | |

| Sheet Vinyl | |

| Others (VCT, Resilient Vinyl-Backed Rubber Hybrid) |

By Installation Method

| Self-Adhesive Vinyl Tiles |

| Glue-Down |

| Interlocking Vinyl Tiles |

| Others |

By End-User

| Residential | |

| Commercial | Hospitality & Leisure |

| Retail & Shopping Centers | |

| Healthcare Facilities | |

| Education | |

| Corporate Offices | |

| Public & Government Buildings | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Remodeling / Retrofit |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Flooring Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Contractors / Builders |

By Geography

| Northeast |

| Midwest |

| Southeast |

| Southwest |

| West |

| By Product Type | Luxury Vinyl Tile (LVT) | Stone Plastic Composite (SPC) |

| Wood Plastic Composite (WPC) | ||

| Luxury Vinyl Plank (LVP) | ||

| Sheet Vinyl | ||

| Others (VCT, Resilient Vinyl-Backed Rubber Hybrid) | ||

| By Installation Method | Self-Adhesive Vinyl Tiles | |

| Glue-Down | ||

| Interlocking Vinyl Tiles | ||

| Others | ||

| By End-User | Residential | |

| Commercial | Hospitality & Leisure | |

| Retail & Shopping Centers | ||

| Healthcare Facilities | ||

| Education | ||

| Corporate Offices | ||

| Public & Government Buildings | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Remodeling / Retrofit | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Flooring Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Contractors / Builders | ||

| By Geography | Northeast | |

| Midwest | ||

| Southeast | ||

| Southwest | ||

| West | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the United States vinyl floor covering market?

The United States vinyl floor covering market size is USD 13.57 billion in 2026 and is projected to reach USD 19.01 billion by 2031 at a 6.97% CAGR.

Which product category leads demand in the United States vinyl floor covering market?

Luxury Vinyl Tile led with 67.62% share in 2025, and it is also the fastest-growing product with an 8.64% projected CAGR through 2031.

Which installation method is most common in the United States vinyl floor covering market?

Interlocking planks were the largest method with 53.65% of shipments in 2025, while glue-down formats are set to grow at a 7.62% CAGR.

Which end-user segment is expanding fastest within the United States vinyl floor covering market?

Commercial applications are projected to grow at a 9.28% CAGR through 2031, driven by healthcare, education, retail, and hospitality specifications.

Which region is poised for the highest growth in the United States vinyl floor covering market?

The West region is forecast to grow at a 7.94% CAGR to 2031, supported by sustainability mandates and retrofit activity.

How are tariffs influencing sourcing in the United States vinyl floor covering market?

A 25% Section 301 tariff on many Chinese vinyl floor products and UFLPA enforcement increase landed costs and documentation needs, encouraging greater domestic sourcing and investment.

Page last updated on: