Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

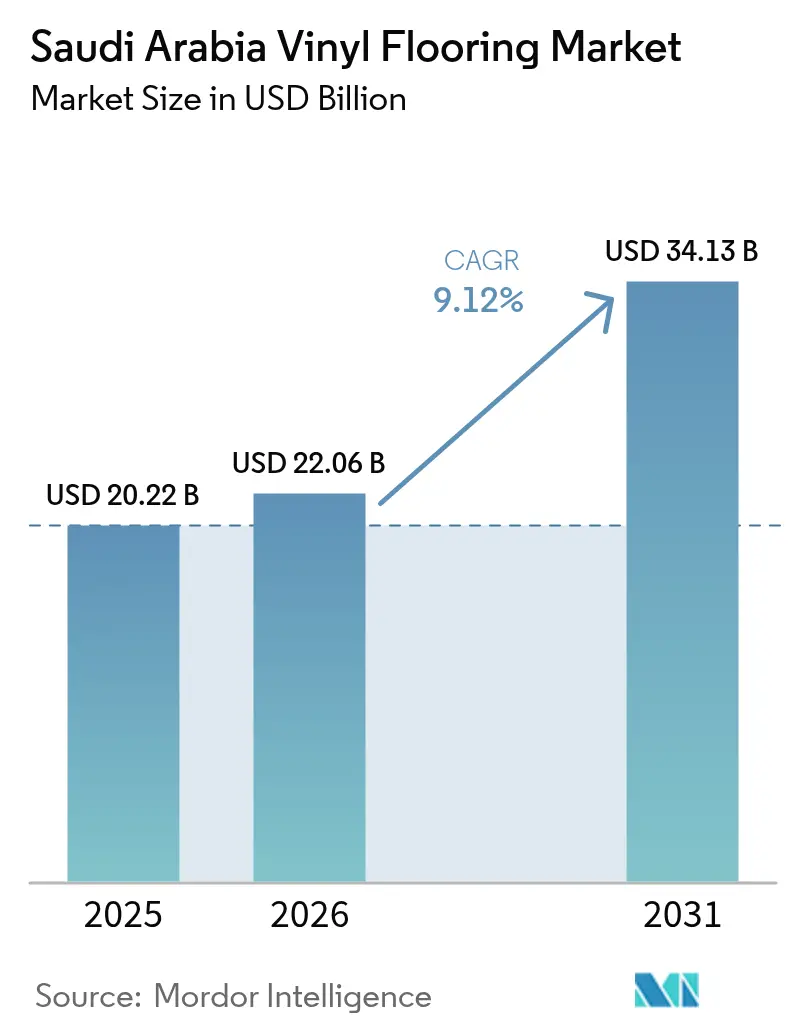

| Base Year Market Size (2025) | USD 20.22 Billion |

| Market Size (2026) | USD 22.06 Billion |

| Market Size (2031) | USD 34.13 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

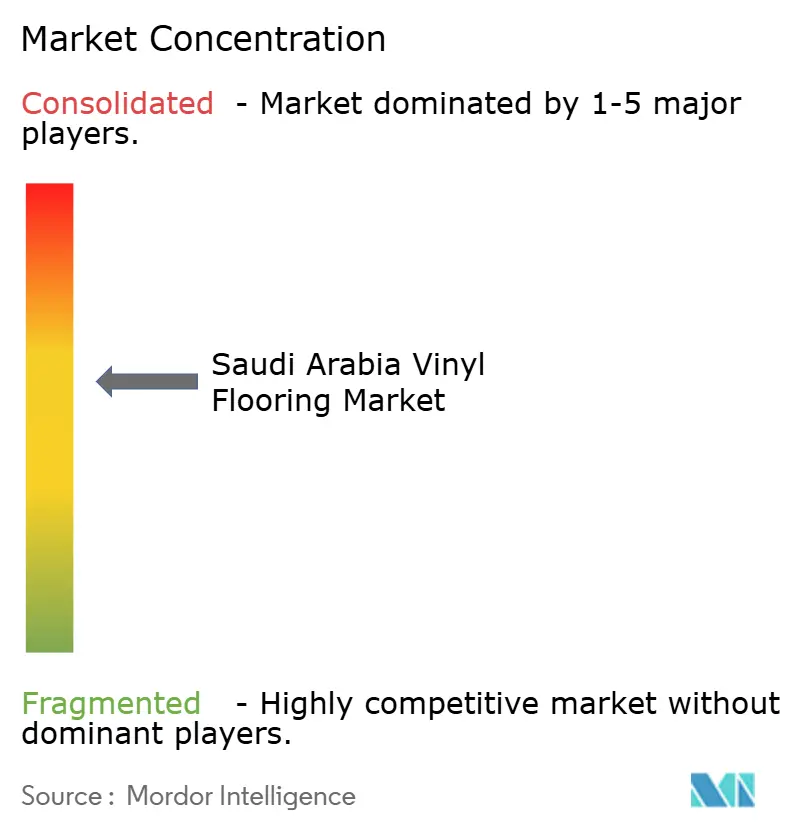

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Vinyl Flooring Market Analysis by Mordor Intelligence

The Saudi Arabia vinyl flooring market size was valued at USD 20.22 billion in 2025 and estimated to grow from USD 22.06 billion in 2026 to reach USD 34.13 billion by 2031, at a CAGR of 9.12% during the forecast period (2026-2031). Sustained government investment under Vision 2030, a record pipeline of giga-projects, and strong residential lending momentum underpin the upward trajectory of the Saudi Arabia vinyl flooring market. Luxury Vinyl Tile (LVT) remains the preferred solution thanks to high moisture resistance and authentic design options that align with local aesthetic preferences. Concurrently, domestic production capacity is expanding most notably through Tarkett’s 2024 Jeddah joint venture, which lowers lead times, satisfies localization quotas, and reduces exposure to currency fluctuations. Nonetheless, PVC resin cost swings and evolving VOC regulations pose near-term margin pressures, while cash-flow risks linked to delayed payments on public projects remain an operational restraint.

Key Report Takeaways

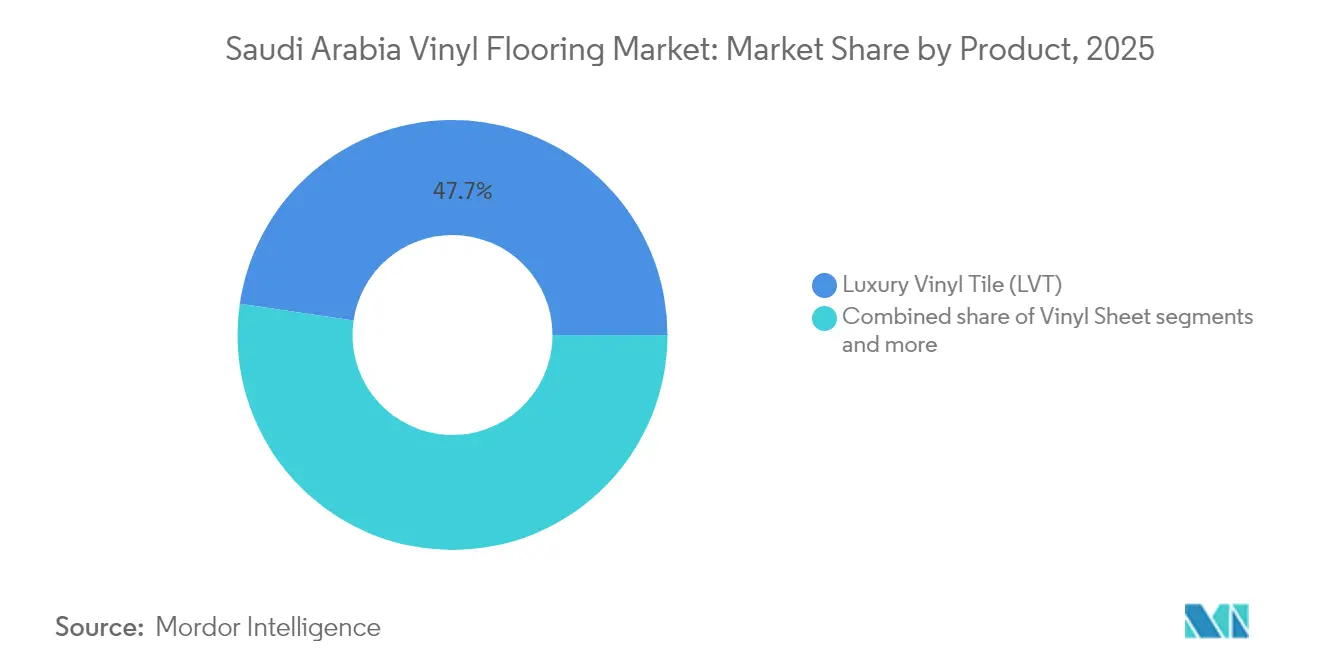

- By product category, luxury vinyl tile captured 47.68% of the Saudi Arabia vinyl flooring market share in 2025, whereas Vinyl Sheet is projected to expand at a 10.84% CAGR through 2031.

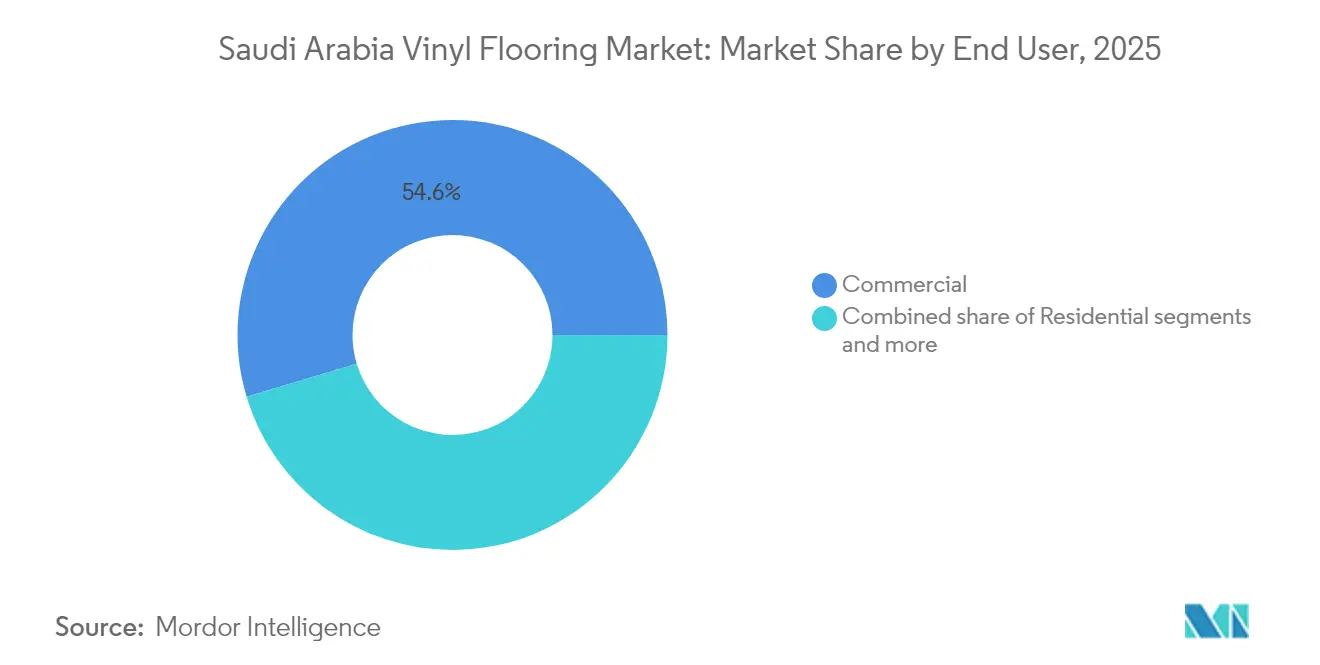

- By end user, commercial construction held 54.63% of the Saudi Arabia vinyl flooring market share in 2025; the builder channel records the fastest growth at 10.62% CAGR between 2026 and 2031.

- By distribution channel, contractors accounted for 43.78% of the Saudi Arabia vinyl flooring market share in 2025, while online platforms are forecast to rise at t 14.96% CAGR to 2031.

- By geography, the Western Region controlled 36.21% of the Saudi Arabia vinyl flooring market share in 2025; the Central Region is on track for an 8.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Vinyl Flooring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Home-ownership and mortgage expansion | +2.1% | Riyadh, Western Region | Medium term (2-4 years) |

| Mega-projects ramp-up (NEOM, Red Sea, Qiddiya) | +1.8% | Western & Central Regions | Long term (≥ 4 years) |

| Retail modernization & fit-out boom | +1.2% | Urban centers nationwide | Short term (≤ 2 years) |

| Rising LVT penetration for design & moisture needs | +1.5% | Nationwide, coastal zones | Medium term (2-4 years) |

| Local-content drive & new Saudi vinyl tile production | +1.3% | Western Region manufacturing hub | Medium term (2-4 years) |

| Healthcare PPP pipeline with hygiene flooring specs | +1.0% | Major metro areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Residential Real-Estate and Mortgage Initiatives

Mortgage volumes climbed 28.3% year-over-year through February 2025 as government programs target 70% national homeownership by 2030[2]CBRE Research, “Saudi Arabia Real Estate Market Review Q1 2025,” cbre.sa. . The construction wave fuels demand for cost-effective, low-maintenance surfaces, positioning the Saudi Arabia vinyl flooring market as an attractive alternative to ceramic or stone. In humid coastal cities, vinyl’s moisture barrier outperforms wood-based flooring, while its click-lock systems allow rapid installation in large multi-family developments. Developers have begun specifying rigid-core LVT across whole apartment towers to ensure consistent thermal performance, and bulk procurement models are reducing unit costs. The shift dovetails with consumer preference for natural-look décors, further cementing LVT’s foothold in new housing schemes.

Mega-Projects Ramp-Up Creates Bulk Procurement Opportunities

Flagship ventures such as NEOM, the Red Sea Project, and Qiddiya collectively account for well over USD 500 billion in committed capital and demand resilient flooring that meets stringent sustainability benchmarks. These projects specify advanced flooring systems capable of supporting high-traffic volumes while meeting stringent sustainability and performance criteria. However, recent fiscal pressures have prompted project reassessments, with some developments facing potential scaling adjustments due to Public Investment Fund funding constraints and lower oil revenues. The modular construction approach adopted by several giga-projects, including NEOM's volumetric assembly plants, creates opportunities for prefabricated flooring systems and standardized vinyl installations that can accelerate project timelines while ensuring consistent quality across massive development scales.

Retail Modernization Drives Commercial Flooring Upgrades

Saudi Arabia's retail transformation extends beyond traditional shopping centers to encompass the modernization of neighborhood convenience stores (baqala) and the development of integrated retail-entertainment complexes. The Kingdom's retail sector demonstrated resilience with approximately 8% year-over-year POS sales growth in early 2025, supported by expanding mall development and tourism-driven retail expansion. This retail evolution demands flooring solutions that balance aesthetic appeal with operational durability, particularly in high-traffic areas where vinyl's slip resistance and easy maintenance provide operational advantages. The integration of digital payment systems and interactive retail technologies requires flooring installations that accommodate cable management and equipment mounting while maintaining seamless appearance standards across diverse retail formats.

LVT Technology Advancement Captures Market Share

Luxury Vinyl Tile's technological evolution has positioned it as the dominant product category, capturing 48.27% market share through superior moisture performance and design authenticity. Recent innovations include rigid-core SPC formulations that eliminate expansion concerns in Saudi Arabia's temperature extremes, while digital printing technologies enable wood and stone aesthetics that satisfy cultural preferences for natural material appearances[3]Floor Focus, “LVT Report 2024,” floordaily.net. . The shift toward click-lock installation systems reduces labor requirements and installation time, addressing skilled installer shortages in remote provinces while ensuring consistent quality across projects. Advanced wear layer technologies now provide commercial-grade durability in residential-thickness products, expanding LVT applications across mixed-use developments where unified flooring systems offer design continuity and maintenance efficiency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PVC resin price volatility | -1.4% | Nationwide | Short term (≤ 2 years) |

| Tightening VOC and sustainability rules on PVC | -0.8% | Nationwide | Long term (≥ 4 years) |

| Shortage of trained vinyl-floor installers | -0.6% | Rural areas | Medium term (2-4 years) |

| Government payment delays on public projects | -1.2% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

PVC Resin Price Volatility Pressures Margins

Global PVC resin markets experienced significant price increases in February 2024, driven by construction sector demand recovery and feedstock cost pressures. Saudi Arabia's petrochemical advantage through SABIC's local production provides some insulation, with the company reporting stable Q3 2024 performance and ongoing capacity expansion projects. However, specialized vinyl flooring grades often require imported additives and processing chemicals that remain subject to global price fluctuations. The volatility particularly affects smaller distributors and contractors operating on thin margins, while larger players with hedging capabilities and direct supplier relationships maintain better cost stability. Local manufacturing initiatives, including Tarkett's Jeddah facility, may provide some price stability through reduced logistics costs and currency exposure mitigation.

Government Payment Delays Strain Cash Flow

Despite the implementation of the Etimad platform and regulatory reforms, payment delays in public construction projects continue to challenge contractor cash flow, with studies identifying slow decision-making on claims (mean score 3.96) and complex bureaucratic procedures (3.64) as primary delay causes. The Saudi Civil Transactions Law's prohibition on conventional interest compounds the challenge by limiting contractors' ability to recover financing costs from delayed payments. While the Ministry of Finance reported 99% of private-sector dues paid by December 2022, the 60-70 day payment timeline established by Executive Regulation still creates working capital pressures for flooring suppliers and installers. The situation particularly affects smaller companies lacking credit facilities to bridge payment gaps, potentially consolidating market share toward financially stronger players with better access to trade financing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Rigid-Core Innovation Anchors LVT Dominance

Luxury Vinyl Tile commands 47.68% market share in 2025 and leads growth projections with 11.52% CAGR through 2031, driven by technological advances in rigid-core SPC formulations and enhanced wear layer performance. The segment's dominance reflects Saudi Arabia's demanding climate conditions, where LVT's dimensional stability and moisture resistance outperform traditional materials in coastal humidity and desert temperature extremes. Tarkett's new Jeddah manufacturing facility specifically targets LVT production, indicating strategic confidence in continued segment expansion. Vinyl Sheet maintains 33.21% market share, primarily serving commercial applications where seamless installations provide hygiene advantages in healthcare and food service environments. The format's cost-effectiveness supports large-scale institutional projects, though growth remains constrained by installation complexity and skilled labor requirements. Vinyl Composite Tile represents 19.11% share, appealing to budget-conscious residential applications and retrofit projects where individual tile replacement offers maintenance advantages. The segment benefits from simplified installation requirements but faces competitive pressure from advancing LVT technologies that offer superior aesthetics at narrowing price premiums.

By End User: Commercial Demand Reflects Infrastructure Priorities

Commercial applications lead with 54.63% market share in 2025, reflecting the Kingdom's massive infrastructure development and institutional construction programs. Healthcare facility expansion under PPP models drives the specification of specialized vinyl formulations meeting infection control standards, while educational construction supports the Kingdom's human capital development objectives. Retail modernization initiatives, from traditional souks to contemporary shopping centers, require flooring solutions that balance aesthetic appeal with operational durability under high-traffic conditions.

Residential applications account for 37.52% market share, supported by government mortgage initiatives and the Vision 2030 homeownership target of 70%. The segment benefits from vinyl's cost-effectiveness and design versatility, particularly in multi-family housing developments where maintenance efficiency influences long-term operational costs. However, the Builder segment emerges as the fastest-growing category at 10.62% CAGR, reflecting accelerated construction timelines and bulk procurement strategies that favor vinyl's installation efficiency and consistent quality standards. This segment's growth indicates market maturation toward more sophisticated procurement approaches that recognize vinyl's total cost of ownership advantages over initial price considerations.

By Distribution Channel: Digital Procurement Gains Momentum

Contractors remained the chief purchasing route, representing 43.78% of 2025 turnover and acting as gatekeepers for large public tenders. Specialty stores held 25.12% by offering curated displays and technical advice. Home centers captured 18.21% through rising DIY interest, particularly among younger homeowners. The Saudi Arabia vinyl flooring market size ordered through online portals, however, is growing fastest at 14.96% CAGR as institutional buyers adopt e-tender platforms aligned with Vision 2030’s digital economy targets. The COVID-19 pandemic accelerated digital adoption, while government initiatives promoting digital transformation support continued online channel expansion. Major players increasingly invest in digital capabilities, with comprehensive product catalogs, specification tools, and virtual design services becoming competitive differentiators in the evolving distribution landscape.

Geography Analysis

The Western Region commanded 36.21% of Saudi Arabia's vinyl flooring market revenues in 2025 on the back of Jeddah’s logistics edge and the concentration of mega-projects such as NEOM and the Red Sea destination. Port proximity slashes inbound freight costs for imported additives, while a cluster of flooring installers and distributors ensures rapid projectmobilizationn Large pilgrimage volumes into Mecca and Medina also support continual hotel refurbishments, helping stabilize regional demand. The Central Region, anchored by Riyadh, delivered a 29.15% share and is forecast to grow at an 8.12% CAGR. Office vacancies remain tight, and premium rent levels encourage landlords to refurbish legacy towers with high-end LV Headquarters mandates require foreign multinationals to shift operations to Riyadh, driving incremental interior fitout. Government ministries seeking LEED-certified buildings further favor vinyl products that carry a low-VOC declaration. The Eastern Region captured an 17.86% share thanks to petrochemical expansion corridors linking Dammam, Jubail, and Ras Tanur. Industrial operators prefer resilient sheet vinyl in lab blocks where chemical resistance is paramount. Northern and Southern Regions jointly contributed about 16.78. Both are benefiting from regional development programs, border-trade hubs, and new tourism circuits that demand robust yet cost-efficient flooring solutions.

Competitive Landscape

The Saudi Arabia vinyl flooring market is moderately concentrated, with the top five players holding a significant share, reflecting healthy competition and room for further market share expansion through strategic positioning and strengthened local presence. Tarkett stands out as the market leader, supported by its 2024 joint venture manufacturing facility in Jeddah. This local setup helps the company reduce lead times, enhance cost efficiency, and align with the growing emphasis on local content in government procurement. The facility also reinforces Tarkett’s long-term commitment to the Saudi market. Overall, local manufacturing is becoming a key differentiator in securing both public and private sector projects. The company's global sustainability credentials, including SBTi-validated climate targets and ReStart® recycling programs, position it favorably for projects requiring environmental certifications.

Competitive strategies increasingly emphasize technology differentiation and service capabilities rather than price competition alone. Major international players like Gerflor and Armstrong Flooring maintain strong positions through specialized product offerings and established distributor relationships, while emerging local players like Mattex demonstrate the potential for domestic manufacturers to capture market share through vertical integration and project-specific customization. The market structure supports both global brands seeking scale advantages and specialized suppliers targeting niche applications, with success increasingly determined bythe ability to navigate regulatory requirements, provide technical support, and maintain consistent supply chain performance in a rapidly growing market environment.

Regulatory compliance capabilities represent an emerging competitive differentiator as SASO 2025 import regulations eliminate previous flexibilities and mandate dual certification for all imported vinyl flooring products in Saudi Arabia. These new requirements mark a significant tightening of standards, raising the entry barrier for less-prepared players. Companies with strong quality control systems and accredited testing relationships are well-positioned to gain faster market access and maintain cost efficiency. Conversely, firms lacking adequate compliance infrastructure may face delayed product approvals, increased operational complexity, and potential erosion of market share. As the regulatory landscape evolves, preparedness and adaptability will become critical for sustained competitiveness in the Saudi vinyl flooring market.

Saudi Arabia Vinyl Flooring Industry Leaders

Tarkett (incl. Tarkett Arabia JV)

Gerflor

Armstrong Flooring

Shaw Industries

Mohawk Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: SASO implemented mandatory PCoC and SCoC certification requirements for all imported products, eliminating the previous "Letter of Undertaking" option and requiring exporters to obtain dual certifications before shipment to ensure compliance with Saudi technical standards.

- January 2025: Saudi Arabia announced a SAR 10 billion (USD 2.67 billion) Standard Incentives Programme providing up to 35% funding for qualifying industrial projects, with building materials identified as a priority sector under the National Industrial Strategy, creating significant opportunities for vinyl flooring manufacturing investments.

- November 2024: Tarkett opened its joint venture vinyl LVT manufacturing facility in Jeddah, Saudi Arabia, representing the first major international vinyl flooring production investment in the Kingdom and establishing local manufacturing capability to serve regional demand while meeting local content requirements.

- September 2024: Tarkett opened its joint venture vinyl LVT manufacturing facility in Jeddah, Saudi Arabia, representing the first major international vinyl flooring production investment in the Kingdom and establishing local manufacturing capability to serve regional demand while meeting local content requirements.

Saudi Arabia Vinyl Flooring Market Report Scope

Sheet vinyl flooring is vinyl flooring that comes in large, continuous, flexible sheets. A vinyl sheet floor is completely impermeable to water, unlike vinyl floor tile, which comes in stiff tiles, and vinyl planks, which come in interlocking strips. This report aims to provide a detailed analysis of the Saudi Arabia vinyl flooring market. It focuses on the market dynamics, emerging trends in the segments and regional markets, and insights into various product and application types. It also analyzes the key players and the competitive landscape in the Saudi Arabian vinyl flooring market. The Saudi Arabia Vinyl Flooring Market is segmented by Product (Vinyl Sheet, Vinyl Composite Tile, and Luxury Vinyl Tile), End User (Residential, Commercial, and Builder), and Distribution Channel (Contractors, Specialty Stores, Home Centers, Online, and Other Distribution Channels). The report offers Market size and forecasts for the Saudi Arabia Vinyl Flooring Market in terms of revenue (USD million) for all the above segments.

By Product

| Vinyl Sheet |

| Vinyl Composite Tile |

| Luxury Vinyl Tile |

By End User

| Residential |

| Commercial |

| Builder |

By Distribution Channel

| Contractors |

| Specialty Stores |

| Home Centers |

| Online |

| Other Distribution Channels |

By Geography

| Central Region |

| Western Region |

| Eastern Region |

| Northern Region |

| Southern Region |

| By Product | Vinyl Sheet |

| Vinyl Composite Tile | |

| Luxury Vinyl Tile | |

| By End User | Residential |

| Commercial | |

| Builder | |

| By Distribution Channel | Contractors |

| Specialty Stores | |

| Home Centers | |

| Online | |

| Other Distribution Channels | |

| By Geography | Central Region |

| Western Region | |

| Eastern Region | |

| Northern Region | |

| Southern Region |

Key Questions Answered in the Report

How large is the Saudi Arabia vinyl flooring market in 2026?

The market is valued at USD 22.06 billion in 2026, with expectations of reaching USD 34.13 billion by 2031.

Which product dominates Saudi demand?

Luxury Vinyl Tile leads with 47.68% share, helped by rigid-core technology suited to the Kingdom’s climate and design preferences.

What growth rate is forecast for the sector?

The market is projected to grow at a 9.12% CAGR from 2026 to 2031.

Which distribution channel is expanding fastest?

Online procurement is rising at a 14.96% CAGR as institutional buyers embrace digital tender platforms.

How will local manufacturing affect the competitive scene?

Domestic plants such as Tarkett’s Jeddah facility cut delivery times, satisfy localization rules, and may shift market share toward in-Kingdom producers.

Page last updated on: