Potato Harvesting Machinery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

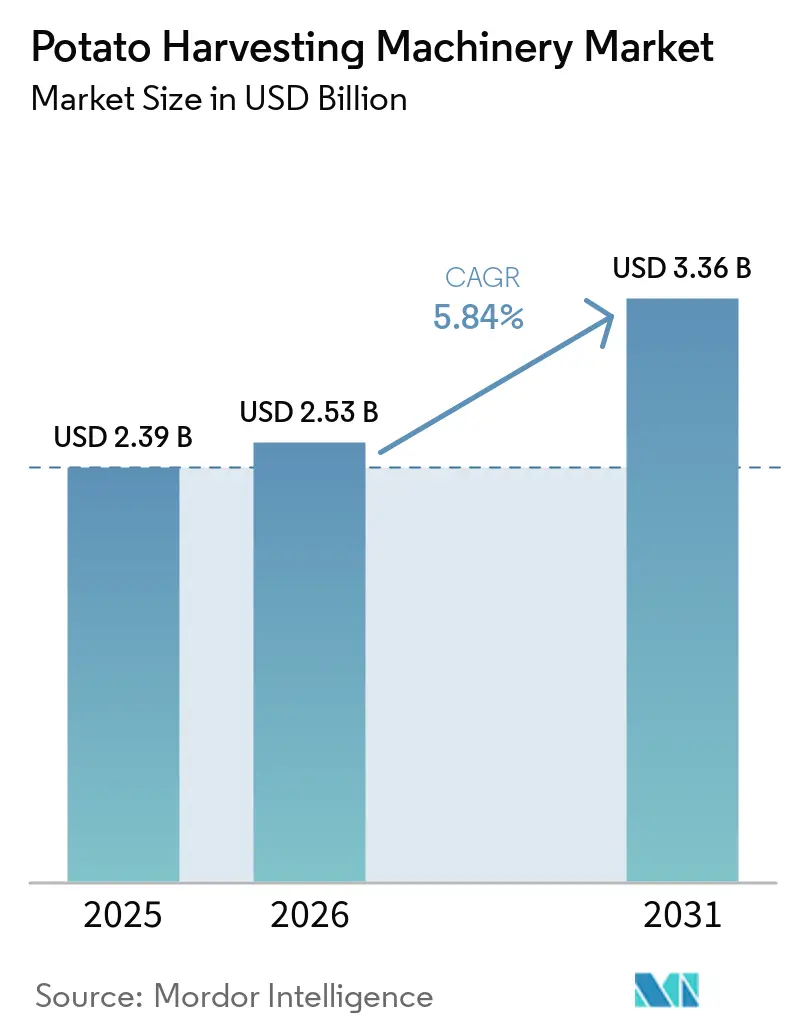

| Market Size (2026) | USD 2.53 Billion |

| Market Size (2031) | USD 3.36 Billion |

| Growth Rate (2026 - 2031) | 5.84% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Potato Harvesting Machinery Market Analysis by Mordor Intelligence

The potato harvesting machinery market is valued at USD 2.39 billion in 2025 and is anticipated to grow from USD 2.53 billion in 2026 to USD 3.36 billion by 2031, registering a CAGR of 5.84% through 2026-2031. This growth is driven by farm labor shortages, the expansion of processed-potato supply chains, and the adoption of GPS-enabled and connected machinery, which enhance field precision and reduce reliance on operator judgment. With global potato production reaching 390 million metric tons across 17.1 million harvested hectares in 2024, the market benefits from a substantial crop base reliant on efficient, low-damage mechanical harvesting systems. Europe, holding the largest regional market share, underscores the demand for advanced machinery. However, challenges such as the high cost of premium machines exceeding EUR 400,000 (USD 432,000), limited-service capacity outside core markets, and weather-related disruptions in major production regions underscore the need for cost-effective, resilient solutions to sustain growth and ensure consistent harvest quality.

Key Report Takeaways

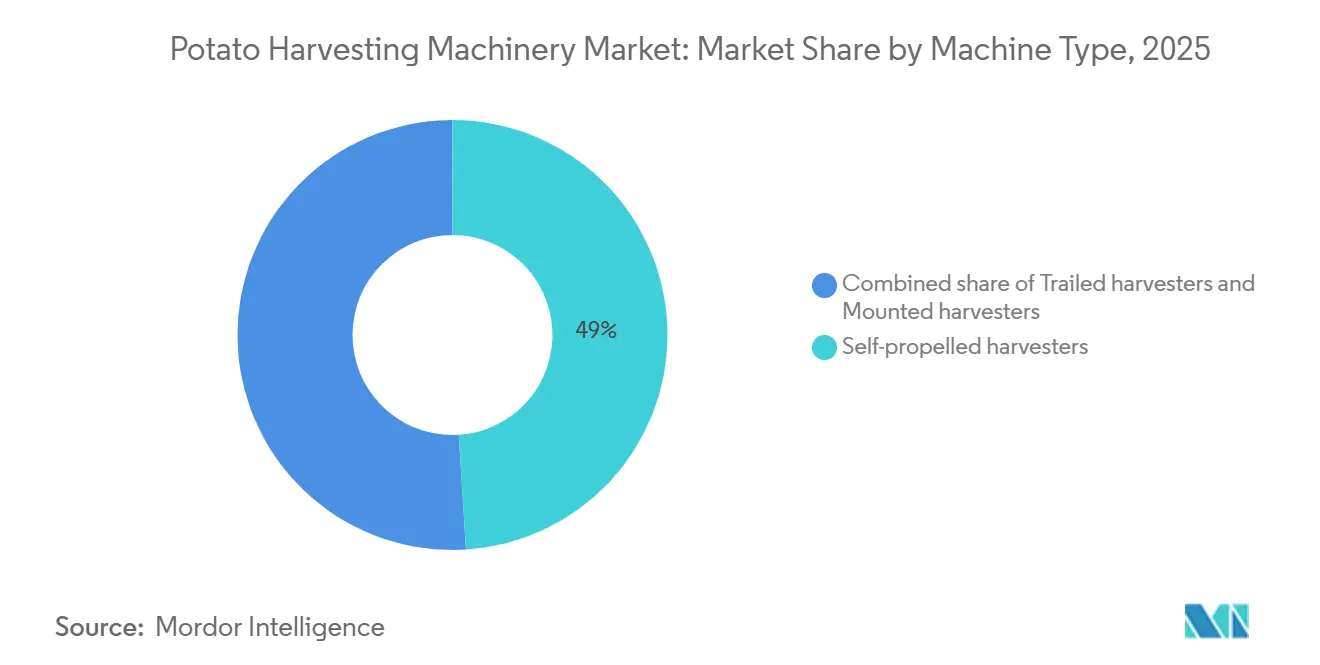

- By machine type, self-propelled harvesters held the largest 49.0% of the potato harvesting machinery market share in 2025, while trailed harvesters are the fastest-growing segment at a 6.5% CAGR during 2026-2031.

- By automation level, conventional harvesters remained the largest segment, with a 65% market share of the potato harvesting machinery market in 2025, while GPS-enabled and connected harvesters are the fastest-growing segment at a 7.8% CAGR during 2026-2031.

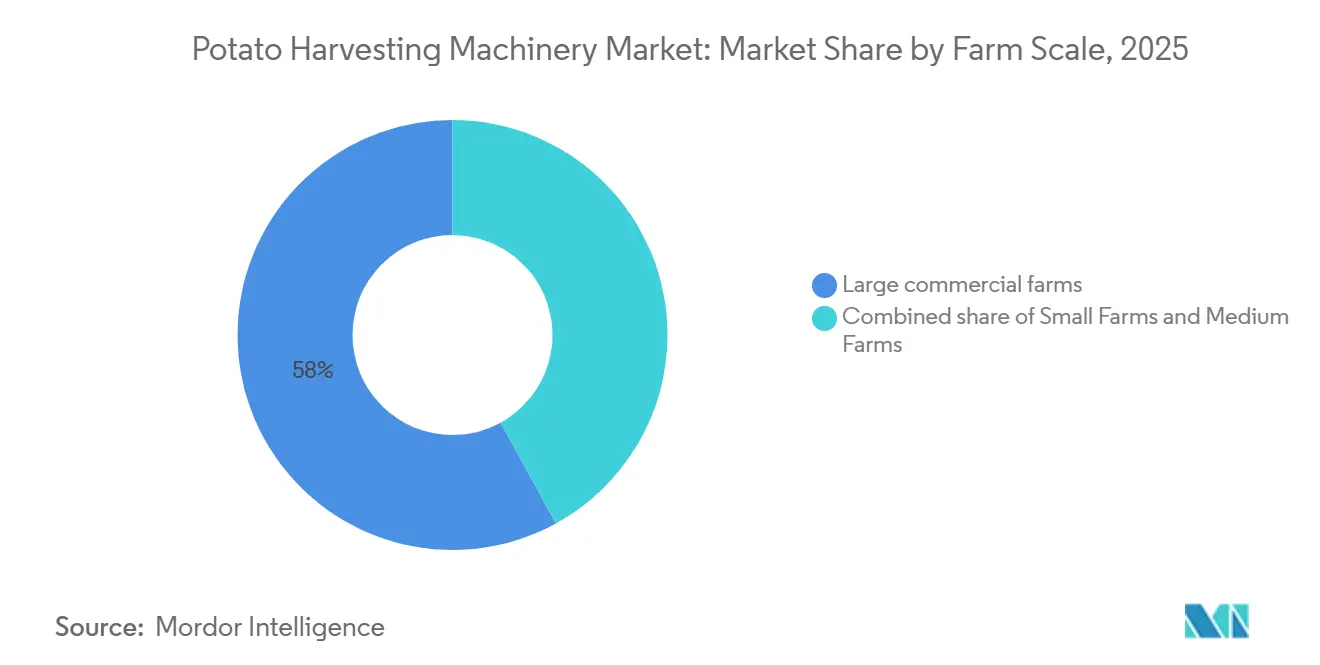

- By farm scale, Large commercial farms accounted for 58% of the potato harvesting machinery market share in 2025 and are gaining momentum with the fastest 6.2% CAGR through 2026-2031.

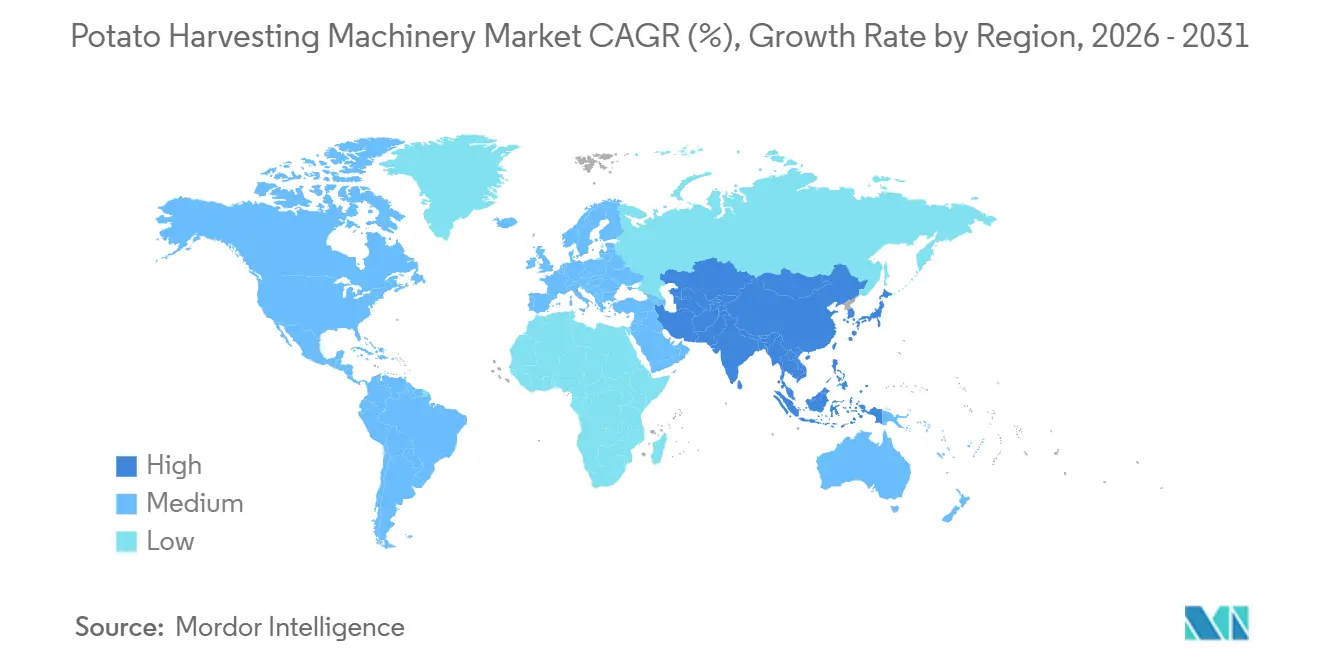

- By geography, Europe held the largest share, accounting for 35.0% of the potato harvesting machinery market in 2025, while Asia-Pacific is the fastest-growing region, with a 6.8% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Potato Harvesting Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Farm labor scarcity and rising seasonal wages | +1.4% | Global, with the strongest pressure in North America and Europe, where labor dependence and wage levels are high | Short term (≤ 2 years) |

| Precision harvesting and smart-machine upgrades | +1.2% | North America and Europe first, with adoption widening across the Asia-Pacific and South America | Medium term (2-4 years) |

| Processed-potato demand raises harvest quality requirements | +1.1% | Global, with the highest pull from North America, Europe, and emerging Asia-Pacific processing hubs | Medium term (2-4 years) |

| Mechanization subsidies and modernization programs | +0.9% | Asia-Pacific core, with wider influence across South America and Africa, where affordability remains a barrier | Short term (≤ 2 years) to Medium term (2-4 years) |

| Processor contract penalties for bruising and foreign material | +0.8% | North America and Europe first, with growing relevance in the Asia-Pacific processor corridors | Medium term (2-4 years) |

| Weather-compressed harvest windows favoring high-capacity machines | +0.8% | Europe and North America first, with rising relevance in South America | Medium term (2-4 years) to Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Farm Labor Scarcity and Rising Seasonal Wages

Rising farm labor costs are driving the growth of the potato harvesting machinery market by shortening the payback period for mechanized systems. The United States Department of Agriculture National Agricultural Statistics Service reported that average field worker wages from July to October 2024 were USD 18.42 per hour. With labor expenses projected to rise further in 2025, as per the United States Department of Agriculture Economic Research Service, the pressure on growers continues to intensify[1]Source: United States Department of Agriculture National Agricultural Statistics Service Agricultural Statistics Board, “Farm Labor (November 2024),” United States Department of Agriculture, esmis.nal.usda.gov.. Despite H-2A temporary agricultural visa certifications reaching 385,000 in fiscal 2024, the seasonal labor supply gap persists. In labor-intensive and time-sensitive potato operations, these trends are compelling growers to transition to mechanized harvesting systems, particularly as manual methods become impractical at larger scales.

Precision Harvesting and Smart-Machine Upgrades

Precision features are now central to the potato harvesting machinery market as growers focus on data-driven efficiency and control. A January 2024 review by the United States Government Accountability Office reported that GPS-supported autosteer and yield monitoring were widely adopted, with automated steering accounting for 53% of guidance system use on soybean crop acreage in 2024[2]Source: U.S. Government Accountability Office, “Precision Agriculture: Benefits and Challenges for Technology Adoption and Use,” U.S. GAO, gao.gov. Reflecting this shift, GRIMME Group enhanced its two-row VARITRON series in April 2025 with the CCI 1200 terminal, SmartView video support for up to 13 cameras, and optional yield mapping. These innovations underscore the growing importance of integrated agronomic and machine data, extending the market's value beyond the harvest season. By enabling informed decisions for processors, lenders, and input suppliers, the potato harvesting machinery market is driving efficiency and long-term operational benefits across the supply chain.

Processed-Potato Demand Raising Harvest Quality Requirements

The increasing demand for processed potatoes is driving the need for low-damage harvesting, pushing the adoption of advanced equipment in the potato harvesting machinery market. A January 2025 review published in the journal Agriculture (MDPI) in Agriculture identified mechanical damage, particularly during potato-to-soil separation, as the primary source of bruising in the production process. Potatoes intended for processing must be free from bruises, loose sprouts, and foreign materials, making harvester settings crucial for ensuring commercial compliance. This is highlighted by India's 48.6% year-over-year growth in frozen potato product exports in 2024, reaching 172,444 metric tons. The rising demand for processing emphasizes the need for mechanized harvesting solutions, especially in regions shifting from manual methods to meet evolving quality standards.

Mechanization Subsidies and Modernization Programs

Subsidy programs significantly support the potato harvesting machinery market by reducing the financial strain of purchases on farm balance sheets. India’s Sub-Mission on Agricultural Mechanization offers 40% to 50% financial assistance for eligible machinery, including potato harvesters, with the portal active for the 2025-26 cycle. Similarly, China expanded its machinery replacement subsidy program in February 2025, adding equipment categories and increasing per-unit support through special treasury bond funding. In Europe, the European Commission’s Common Agricultural Policy (CAP) 2028-2034 framework, with a budget exceeding EUR 300 billion (USD 340 billion), continues co-financing for modernization under national strategic plans[3]Source: Directorate-General for Agriculture and Rural Development, “The CAP 2028-2034 Proposal Explained, Fairer, Better Targeted Income Support for Farmers,” European Commission, europa.eu. Collectively, these programs not only ease machinery acquisition but also drive standardization, enhance service density, and encourage the adoption of advanced, scalable machine generations, strengthening the overall market framework.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront machine cost and long payback | -1.2% | Global, with the greatest pressure in Asia-Pacific, the Middle East, Africa, and South America | Short term (≤ 2 years) to Medium term (2-4 years) |

| Skilled operator and service-network shortages | -0.9% | Strongest in Asia-Pacific, the Middle East, Africa, and South America, with lower intensity in Europe and North America | Medium term (2-4 years) to Long term (≥ 4 years) |

| Soil variability and tuber bruise sensitivity | -0.6% | Global, with the highest operational complexity across mixed-soil regions in Europe, Asia-Pacific, and South America | Medium term (2-4 years) |

| Seasonal utilization limiting fleet economics | -0.5% | Global, especially in temperate zones, where harvest windows are narrow | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Machine Cost and Long Payback

The high capital cost of potato harvesting machinery significantly limits market growth, as premium equipment often exceeds many growers' financial capacity. For example, new four-row self-propelled machines from leading European manufacturers are priced above EUR 400,000 (USD 432,000), making them inaccessible for farms with limited acreage or shorter planning horizons. A January 2024 review by the United States Government Accountability Office emphasized that high acquisition costs hinder the adoption of precision agriculture on small and medium farms, a challenge equally applicable to premium potato harvesters. For farms harvesting less than 100 to 150 hectares per season, payback periods of 10 to 15 years often exceed growers' financial capabilities. While contractors, cooperatives, and custom hiring services offer partial solutions, their uneven availability continues to restrict market growth, particularly in emerging regions, underscoring the persistent challenge of high upfront costs.

Skilled Operator and Service-Network Shortages

The increasing complexity of modern potato-harvesting machinery, featuring ISOBUS electronics, camera systems, connected diagnostics, and AI-based adjustment tools from manufacturers such as GRIMME Group, AVR BV, and the Dewulf Group, demands advanced training and robust after-sales support. In regions where mechanization advances faster than technical training, inadequate setup and delayed repairs lead to tuber damage, lower productivity, and shorter machine lifespans. This issue is exacerbated by an aging agricultural workforce in the United States, where the pace of operator replacement falls short of meeting the technical requirements of modern machinery. The shortage of skilled operators not only reduces operational efficiency but also increases the risk of equipment misuse, resulting in higher maintenance costs and operational downtime. This highlights the urgent need for skilled operators and effective service networks to maintain productivity, extend machine durability, and ensure the optimal use of advanced agricultural machinery.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Self-Propelled Platforms Command Commercial Scale

Self-propelled harvesters led, holding the largest 49.0% share of the potato harvesting machinery market size in 2025. Their dominance stems from their ability to deliver high-throughput, single-pass harvesting, meeting the needs of commercial farms and contractors that require speed, separation quality, and bunker management in a single platform. By eliminating tractor dependency, these machines provide operators with precise control over digging speed, haulm separation, and loading flow, especially critical during narrow harvest windows.

Trailed harvesters are projected to be the fastest-growing machine type, with a 6.5% CAGR over 2026-2031. Innovations such as AVR BV’s Spirit 9200i VW, showcased at Potato Europe 2025, demonstrate how advanced technologies, such as the Varioweb module and ISOBUS compatibility, are being integrated into cost-effective platforms. At the same time, mounted harvesters remain significant for smaller farms in Asia-Pacific, South America, and Africa, serving as a transitional option from manual or semi-mechanized systems.

By Automation Level: GPS-Enabled Platforms Outpace the Market

Conventional harvesters accounted for 65% of the potato harvesting machinery market share in 2025 within the automation segment, driven by their lower ownership costs, familiar repair needs, and suitability for short-season use. Automated harvesters, offering features like haulm removal and bunker management without full GPS integration, serve as a transitional step for buyers upgrading from basic systems. However, the market is steadily shifting toward connected platforms, as GPS-supported autoguidance has been linked to a 3% increase in operating profits across the United States crop farming, according to the United States Department of Agriculture (USDA) Economic Research Service.

GPS-enabled and connected harvesters are the fastest-growing segment, projected to grow at a 7.8% CAGR during 2026-2031. Their adoption is driven by benefits such as machine visibility, field traceability, and consistent operational adjustments. The Dewulf Group’s Level X platform, launched in October 2025, highlights this trend, with its Gold tier using AI-driven analysis to optimize harvesting in real time. Additionally, Europe’s digital reporting requirements are reinforcing this shift, as connected systems simplify data handling and enhance compliance workflows. Together, these factors underline the growing preference for GPS-enabled platforms, signaling a clear trajectory toward fully connected harvesting systems.

By Farm Scale: Large Operations Drive Revenue

By farm scale, large commercial farms accounted for 58% of the potato harvesting machinery market share in 2025 and are gaining momentum with the fastest 6.2% CAGR through 2026-2031. Their investment is focused on full-specification equipment, as owning machinery becomes more cost-effective when the harvested area is extensive, harvest windows are narrow, and quality penalties are significant. In both regions, larger commercial and contract-farmed operations contribute disproportionately to machinery investments. Processor supply contracts further encourage equipment ownership in this segment, as bruising, foreign material, and size deviations directly affect grower returns. This combination ensures that large farms remain the primary revenue contributors to the potato harvesting machinery market, even as growth extends to other buyer groups.

Medium farms are becoming more prominent, supported by India's mechanization assistance program, which provides eligible buyers with 40% to 50% financial aid for machinery, including potato harvesters. This initiative improves affordability for growers shifting from smaller-scale systems. Additionally, contractor-service models are making advanced trailed platforms more accessible to mid-scale growers seeking improved harvest quality without bearing the full cost of ownership. While small farms remain the largest group by unit count in several developing regions, they primarily rely on single-row mounted diggers and semi-mechanized options. Their integration into the potato harvesting machinery market will continue to depend on sustained subsidies, local dealer availability, and operator training programs.

Geography Analysis

Europe held the largest share, accounting for 35.0% of the potato harvesting machinery market in 2025. Countries such as Germany, France, the Netherlands, and the United Kingdom drive this demand through extensive commercial potato farming, robust processing, and established dealer networks. Food and Agriculture Organization (FAO) data indicates Europe produced 101 million metric tons of potatoes from 4.0 million hectares in 2024, with a 2.03% yield increase from 2023 despite reduced harvested areas, highlighting a focus on productivity and precision. The region's growth is linked to replacement cycles and the adoption of advanced systems, such as connected and adaptable cleaning technologies.

Asia-Pacific is the fastest regional segment in the potato harvesting machinery market and is projected to expand at 6.8% CAGR during 2026-2031. In 2024, China and India significantly contributed to global potato production, creating a large base for mechanized harvesting. China, the largest producer, drives demand for multi-row self-propelled systems in regions such as Inner Mongolia and Yunnan. In comparison, developed countries such as the United States, Canada, and key European nations, including Germany, the Netherlands, France, and Belgium, achieve much higher processing levels due to advanced technologies, automation, and efficient quality control systems. Japan and Australia represent the premium segment due to high labor costs and established dealer networks, complementing the region's overall growth.

North America, with significant farming regions in Idaho, Washington, and Prince Edward Island, is anticipated to witness moderate growth due to strict processor-quality standards. In South America, countries such as Brazil and Argentina are experiencing growth driven by increased processing investments and larger field scales. In the Middle East, Turkey and Saudi Arabia promote mechanization through modernization programs, while Africa faces challenges such as limited financing and uneven dealer networks. However, South Africa and Egypt show stronger commercial farming activity. A notable development in September 2025 saw GRIMME Group opening a branch in Cape Town, enhancing support for southern African growers. Across regions, the market's growth is interconnected by a shared focus on productivity, mechanization, and advanced harvesting technologies to meet evolving agricultural demands.

Competitive Landscape

The potato harvesting machinery market is moderately concentrated, with the top five players capturing a significant share of 2025 revenue, while the remaining players are fragmented among regional and specialized manufacturers. This fragmentation is prominent in regions such as Poland, the Netherlands, Spain, and North America, where smaller suppliers compete on price, local dealer support, and adaptability to specific field conditions. GRIMME Group leads globally, operating in over 120 countries with a portfolio of more than 150 machine types, while AVR bv and Dewulf Group have shown notable sales growth. This structure highlights a market led by strong global players but with opportunities for local brands to compete through proximity, service, and tailored solutions.

Competition is increasingly driven by connected systems, cleaning performance, and operator support rather than traditional factors such as engine power or row width. In 2025, GRIMME Group launched the updated two-row VARITRON line with advanced digital features, including the CCI 1200 terminal and SmartView support for up to 13 cameras. In October 2025, Dewulf Group introduced Level X with IoT monitoring and autonomous adjustment capabilities, while AVR BV unveiled the fifth-generation Puma with enhanced telematics and performance upgrades. These advancements underline a shift toward software-enabled field control and data-driven adaptability, emphasizing the growing importance of technology in maintaining competitive advantage.

Despite the dominance of established European brands, opportunities remain in emerging markets and underserved segments. Medium-scale farms in India and Southeast Asia require affordable one-row and two-row solutions, while aging fleets in Eastern Europe and South America drive demand for cost-effective digital upgrades. Additionally, integrating harvester data with storage and processing systems presents untapped potential as field data becomes increasingly valuable. While Asia-Pacific manufacturers such as Shandong Transce Agricultural Machinery Technology Co., Ltd. compete on price, established players retain an edge through compliance, dealer support, and reliability. Ultimately, the market remains open to new entrants, as buyers prioritize local agronomic fit and support quality, reinforcing the balance between global leadership and localized competition.

Potato Harvesting Machinery Industry Leaders

GRIMME Group

AVR BV

Dewulf Group

Lockwood Manufacturing

Oxbo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: AVR BV has launched the fifth-generation Puma four-row self-propelled potato harvester, known as "The Final Roar." Powered by a 551 hp Volvo engine, an 81 hp improvement over its predecessor, it offers a 10-metric-ton bunker with 25% more capacity, a 20% larger cleaning area, and an enhanced AVR BV Connect telematics system for remote diagnostics. With over 600 units produced since its 2006 debut, this release represents the most significant redesign in the model's history, combining increased power, capacity, and advanced technology to set a new benchmark for performance.

- October 2025: Dewulf Group launched Level X, a tiered IoT and AI-powered platform for the Enduro and R3060 harvesters, designed to enhance efficiency. Operating across Bronze (IoT monitoring), Silver (advanced camera integration), and Gold (autonomous adjustment) tiers, the Gold tier uses real-time sensor data and AI-driven analysis to optimize harvesting parameters, achieving an average increase of up to 2 km/h in harvesting speed during field tests.

- September 2025: GRIMME Group introduced the fourth-generation VARITRON 470 XL, a four-row self-propelled potato harvester featuring a patented 13 m³ NonstopBunker XL (11 metric tons capacity), enhanced MultiSep cleaning with 25% more hydraulic drive power, and a 340 kW/460 hp Mercedes-Benz MTU engine. This launch, combined with the opening of a new branch in Fisantekraal, Cape Town, South Africa, highlights GRIMME's strategic focus on delivering advanced harvesting solutions while expanding into the African premium market.

Global Potato Harvesting Machinery Market Report Scope

Potato harvesting machinery refers to specialized agricultural equipment designed to automate the lifting, cleaning, and collection of potato tubers from the soil. These machines minimize manual labor by separating potatoes from dirt, vines, and debris while protecting the crop from mechanical bruising.

The potato harvesting machinery market report is segmented by machine type (self-propelled harvesters, trailed harvesters, and mounted harvesters), by automation level (conventional harvesters, automated harvesters, and GPS-enabled and connected harvesters), by farm scale (small farms, medium farms, and large commercial farms), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Self-propelled harvesters |

| Trailed harvesters |

| Mounted harvesters |

| Conventional harvesters |

| Automated harvesters |

| GPS-enabled and connected harvesters |

| Small farms |

| Medium farms |

| Large commercial farms |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Machine Type | Self-propelled harvesters | |

| Trailed harvesters | ||

| Mounted harvesters | ||

| By Automation Level | Conventional harvesters | |

| Automated harvesters | ||

| GPS-enabled and connected harvesters | ||

| By Farm Scale | Small farms | |

| Medium farms | ||

| Large commercial farms | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current outlook for potato harvesting machinery through 2031?

The potato harvesting machinery market is valued at USD 2.53 billion in 2026 and is anticipated to reach USD 3.36 billion by 2031, growing at 5.84% CAGR during 2026-2031.

Which machine type leads global revenue?

Self-Propelled Harvesters accounted for the largest share of revenue in 2025, at 49.0%, as they meet the needs of commercial farms and contractors during narrow harvest windows.

Which automation category is expanding the fastest?

GPS-Enabled and Connected Harvesters are the fastest-growing segment, with a 7.8% CAGR during 2026-2031, as buyers place greater value on machine data, field traceability, and real-time adjustment.

Why are processors influencing equipment purchases more strongly now?

Processor contracts are placing greater emphasis on bruising, foreign material, and quality consistency, so growers are choosing machines that protect tuber condition while maintaining throughput.

Which region offers the strongest growth potential?

Asia-Pacific is the fastest-growing region, with a 6.8% CAGR during 2026-2031, as China and India together account for 39% of global potato production and still have room for mechanization gains.

Page last updated on: