Grape Harvesting Machinery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

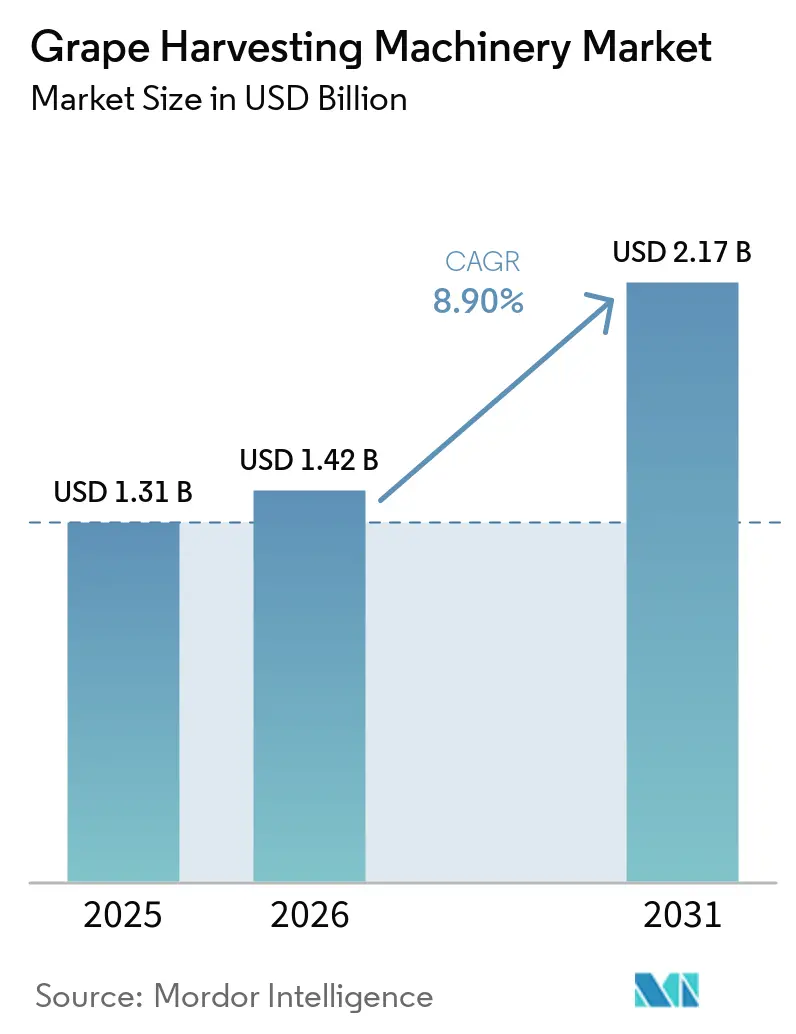

| Market Size (2026) | USD 1.42 Billion |

| Market Size (2031) | USD 2.17 Billion |

| Growth Rate (2026 - 2031) | 8.90% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Grape Harvesting Machinery Market Analysis by Mordor Intelligence

The grape harvesting machinery market size is anticipated to increase from USD 1.31 billion in 2025 to USD 1.42 billion in 2026 and reach USD 2.17 billion by 2031, growing at a CAGR of 8.9% during 2026-2031. Labor scarcity in vineyards, wage inflation, and subsidies for mechanization are prompting even mid-sized estates to adopt automated pickers. Self-propelled units remain the largest product class in terms of value, yet tractor-mounted platforms are the fastest-growing, as estates under 200 hectares pivot toward lower-capital solutions. Battery-powered models are advancing as regulations in premium wine regions are tightening each year. Precision agriculture mandates are transforming harvesters into data platforms that feed yield maps, canopy vigor indices, and carbon-footprint calculators. As vineyard consolidation accelerates, large commercial growers and wine producers are increasingly influencing purchasing trends through multi-unit procurement agreements, driving manufacturers to tailor machinery design, financing models, and after-sales service offerings.

Key Report Takeaways

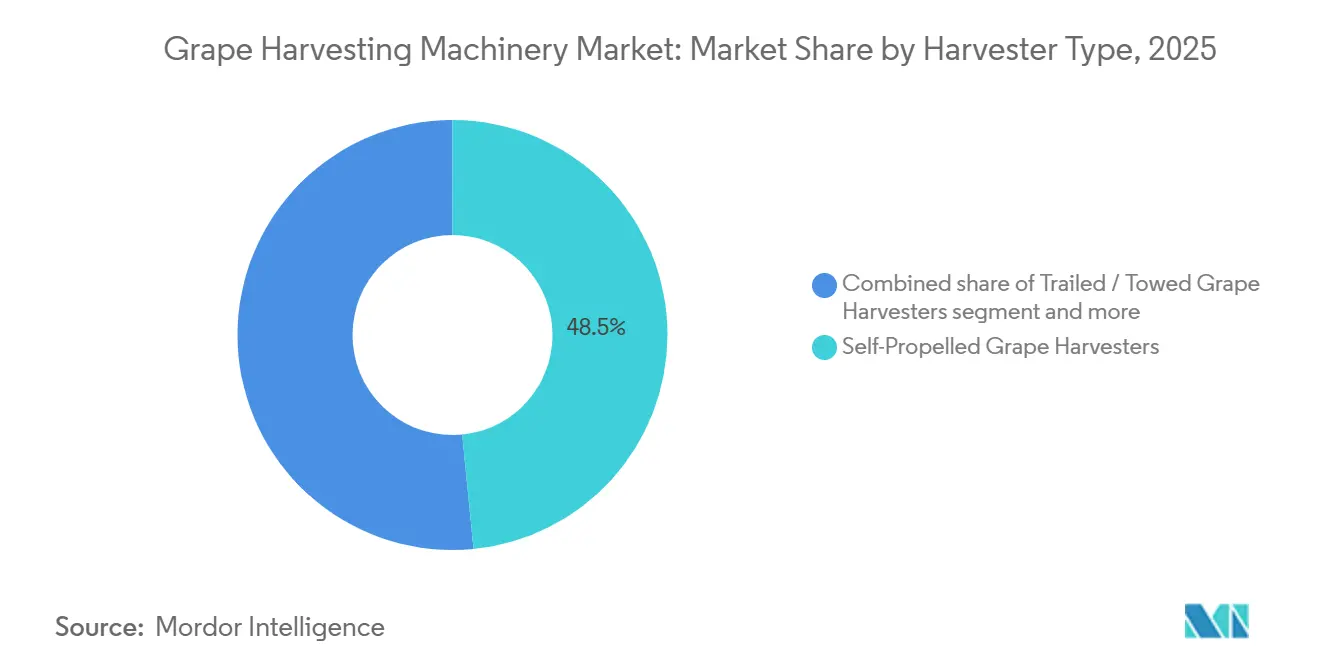

- By harvester type, self-propelled units led with 48.5% of the grape harvesting machinery market share in 2025, while tractor-mounted platforms recorded the fastest 11.8% CAGR during 2026-2031.

- By mode of operation, assisted and precision-guided operations held 54.2% share of the grape harvesting machinery market size in 2025, whereas autonomous/semi-autonomous operations are projected to expand at the fastest 13.2% CAGR through 2026-2031.

- By power source, diesel remained the largest at 66.8% share in 2025, but electric harvesters are forecast to deliver the fastest 14.0% CAGR between 2026 and 2031.

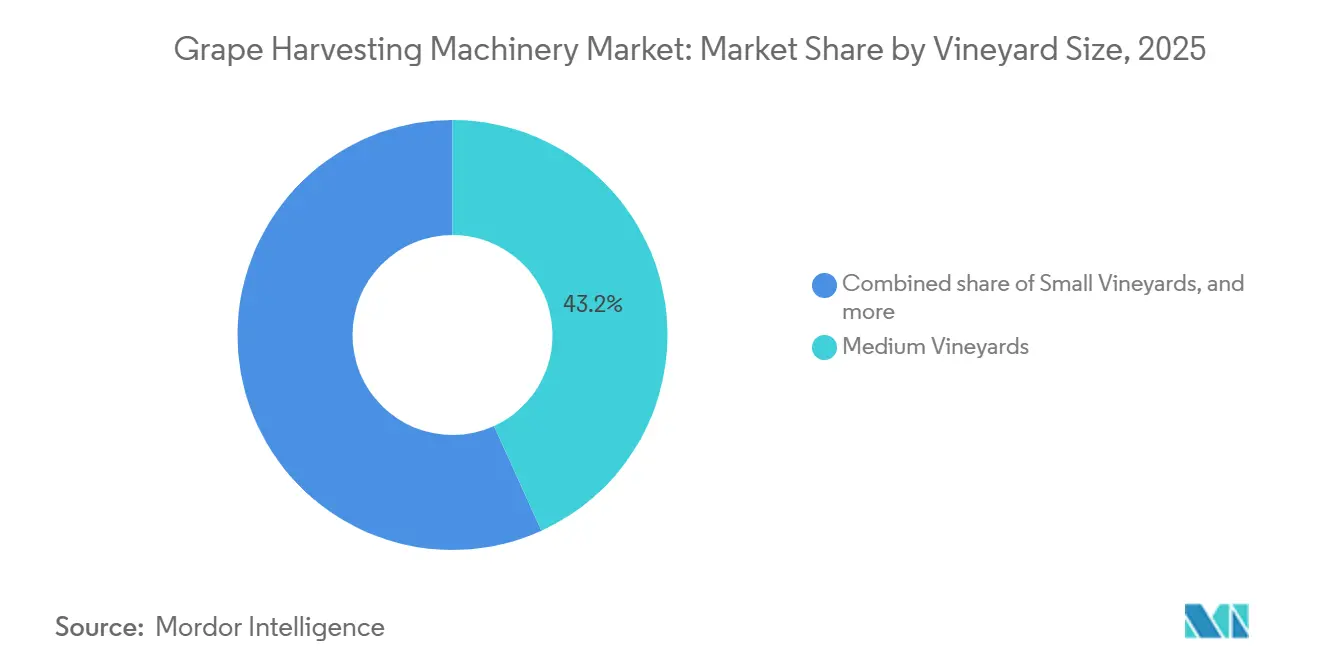

- By vineyard size, medium vineyards (51-200 hectares) captured the largest 43.2% share in 2025, whereas small vineyards (below 50 hectares) will post the fastest 12.4% CAGR from 2026-2031.

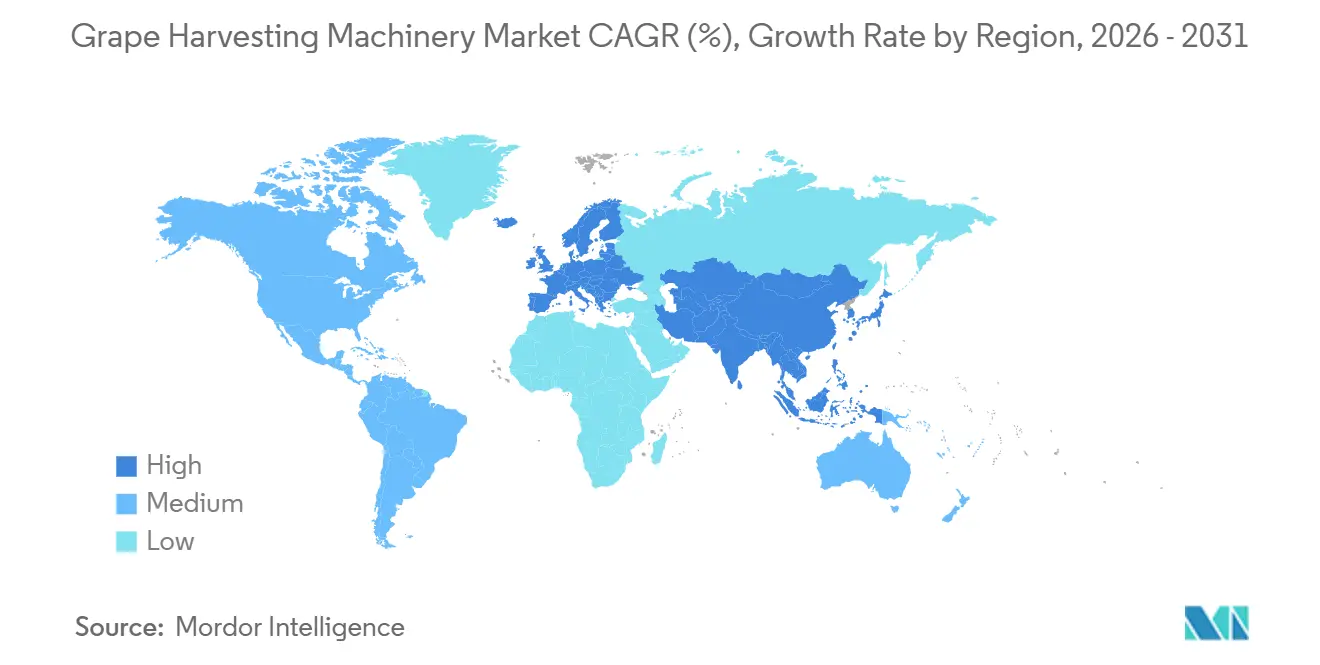

- By geography, Europe accounted for 37.1% of revenue in 2024, and the Asia Pacific region is projected to register a 9.4% CAGR until 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Grape Harvesting Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor-shortage driven mechanization surge | +2.10% | Global, with highest intensity in North America, Europe, and Australia | Medium term (2-4 years) |

| Vineyard consolidation among large wine producers | +1.80% | North America and Europe core, emerging in South America and Asia-Pacific | Long term (≥ 4 years) |

| Government mechanization subsidies and tax credits | +1.50% | Europe, North America, China, Australia | Short term (≤ 2 years) |

| Precision-viticulture adoption requiring data-ready machinery | +1.30% | Global, led by North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Emerging rental and subscription ownership models | +0.90% | Global, with early traction in Australia, North America, and fragmented European regions | Medium term (2-4 years) |

| Development of lightweight self-propelled micro-harvesters | +0.70% | Europe and Asia-Pacific, targeting steep-slope and narrow-row vineyards | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor-Shortage Driven Mechanization Surge

Labor shortages in vineyard operations are becoming a persistent challenge across major wine-producing regions, driving the adoption of mechanized grape harvesting solutions. The United States Department of Agriculture (USDA) reported rising H-2A certifications in 2025 and wage inflation that outpaced other farm sectors[1]Source: United States Department of Agriculture Economic Research Service, “Farm Labor Trends,” ers.usda.gov. Australia experienced contract-harvesting fees of USD 345 (AUD 525) per hour in 2025, dwarfing hand-picking costs and accelerating the purchase of automated pickers. Germany’s 2025 harvest fell 16% below the ten-year average due to crew shortages, prompting traditional estates to turn to machinery. Premium properties in Napa Valley, California, United States, adopted night mechanical picking in 2025 to address labor shortages and maintain fruit acidity. With labor costs rising faster than grape prices, automated solutions have become critical to ensuring profitability.

Vineyard Consolidation Among Large Producers

Consolidation shifts demand from thousands of small owners to a few capital-intensive buyers. In the United States, the Wine Group acquired 6,600 acres from Constellation Brands in June 2025, expanding its mechanized fleet requirement [2]Source: Wine Business, “The Wine Group and Atlas Vineyard Management Deals,” winebusiness.com. Atlas Vineyard Management, headquartered in California, United States, acquired Results Partners, based in Oregon, United States, during the same month. This acquisition expanded its managed acreage in Oregon to 9,000, facilitating multi-unit harvester contracts. Larger estates are focusing on standardizing brands, requiring uniform data interfaces, and advocating for autonomous features to mitigate seasonal labor demands. As mergers progress, order volumes are increasingly concentrated on high-capacity platforms equipped with advanced sensors.

Government Mechanization Subsidies and Tax Credits

Government fiscal support is lowering the net price of machinery in grape-producing regions. The European Union allocated USD 1.12 billion (EUR 1.06 billion) annually to the wine sector in 2025, with up to 80% co-financing on climate-related mechanization. Italy allocated USD 152 million (EUR 144.1 million) for vineyard restructuring, which includes the purchase of mechanical harvesters. Ireland's 2025 Horticulture Capital Investment Scheme provides 60% aid for automation equipment. Similarly, the United Kingdom offers grants for automation under its 2025 Farming Equipment and Technology Fund. In 2024, China expanded provincial machinery subsidies, increasing adoption in regions such as Ningxia and Xinjiang. These incentives reduce payback periods and promote faster fleet renewal.

Precision-Viticulture Adoption Requiring Data-Ready Machinery

Growers now insist harvesters capture yield maps, berry quality, and geo-tagged weight data. Gregoire added ISOBUS connectivity to its 2025 models, enabling two-way data flow into farm-management platforms. Pellenc launched EASY ADJUST in 2025, a smartphone interface that remotely tunes shaker settings and logs performance. Duxton Vineyard's 900-hectare autonomous tractor pilot, completed in 2024 in Australia, integrates canopy sensors with data streams from harvesters. Data-rich machinery allows variable-rate harvest, selective picking, and carbon tracking, elements now demanded by sustainability audits.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital expenditure | −1.2% | Global with acute effect in fragmented European and emerging Asia-Pacific vineyards | Short term (≤ 2 years) |

| Operator-skill and maintenance complexity | −0.9% | Global, prominent where service networks lag | Medium term (2-4 years) |

| Quality concerns for premium hand-picked varietals | −0.6% | Europe and North America premium zones | Long term (≥ 4 years) |

| Limited suitability on extreme-slope vineyards | −0.5% | Mountainous Europe plus scattered South American and Asia-Pacific sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure

High capital requirements hinder the adoption of grape harvesting machinery, especially for small, fragmented vineyard operators. Entry-level self-propelled harvesters cost around USD 80,000, while advanced models exceed USD 400,000, limiting affordability for small-scale growers. In Europe, where over half of vineyards span less than 1 hectare, low machinery utilization and return on investment persist despite subsidy programs. Underdeveloped rental and contractor-based services in many regions outside mechanized markets, such as California, the United States, and Australia, further slow adoption. High costs and limited financing continue to restrict the use of mechanized harvesters, particularly in smaller vineyards and traditional wine regions.

Operator-Skill and Maintenance Complexity

Modern harvesters combine global navigation satellite steering, optical sorters, and electro-hydraulic shakers, all of which require proficiency in mechatronics. The United States National Grape Research Alliance's 2024 survey indicated a shortage of technicians capable of servicing embedded controllers. Cellular black spots hinder remote diagnostics in rural valleys. OEM-certified parts depots may sit hundreds of kilometers away in South America, extending downtime during peak harvest. This skills gap prompts buyers to retain older, simpler machinery that sacrifices data for reliability, slowing fleet upgrade cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Harvester Type: Self-Propelled Dominance Faces Tractor-Mounted Disruption

Self-propelled machines captured 48.5% of the grape harvesting machinery market share in 2025, reflecting productivity advantages for estates above 200 hectares. Tractor-mounted units posted the fastest 11.8% CAGR over 2026-2031 in the grape harvesting machinery market size as growers leverage existing horsepower. Harvesters designed for trailing are now serving a diverse range of farms, enabling equipment rotation across various crops and broadening their utility beyond grapes. High-capacity self-propelled models, such as the Pellenc OPTIMUM XXL80, come equipped with telemetry features that record and upload yield data with every pass. Meanwhile, premium wineries continue to favor self-propelled machines, valuing their ability to reduce tractor compaction and enhance cleaning modules.

Driving the surge in tractor-mounted units is a focus on capital efficiency. Manufacturers, including GREGOIRE and other vineyard equipment providers, are broadening their offerings with ISOBUS-compatible tractor-mounted platforms. These platforms not only align with precision agriculture and digital monitoring needs but also offer lower ownership costs[3]Source: Gregoire, “ISOBUS Enabled Harvesters,” gregoire.com. Manufacturers are focusing on modular platforms and interchangeable shaker technologies compatible with various configurations.

By Mode of Operation: Assisted Systems Today, Autonomous Tomorrow

Assisted and precision-guided harvesters held the largest share, 54.2%, in 2025, driven by GPS steering and camera sorters that augment human oversight. Manual machines linger in aging European fleets, yet account for less than one-third of the grape harvesting machinery market. Autonomous/Semi-Autonomous operations are projected to register the fastest CAGR of 13.2% during 2026–2031, driven by increasing adoption of sensor-integrated systems that reduce dependence on manual labor. In February 2024, trials at Duxton Vineyards in Australia demonstrated that autonomous tractors can efficiently transmit canopy data to harvester controls, guiding pickers along optimal paths. Meanwhile, regulatory frameworks are adapting to authorize driverless operations on geofenced private lands.

Despite the promise, transition costs pose a significant barrier to adoption. Autonomous systems come with a higher price tag than their assisted counterparts. Yet, California's overtime premiums render round-the-clock driverless operations financially appealing. In the European Union, stringent data privacy regulations mandate the use of secure cloud services. This has prompted Original Equipment Manufacturers (OEMs) to set up regional data centers. Furthermore, potential buyers are weighing liability insurance premiums as a crucial factor before finalizing their purchases.

By Power Source: Diesel Reigns While Electric Surges

Diesel-powered harvesters accounted for 66.8% share of the grape harvesting machinery market size in 2025. Their torque suits steep grades and dusty canopies. Electric harvesters, however, are projected to record the fastest CAGR of 14.0% during 2026–2031, supported by the expanding adoption of carbon labeling and sustainability compliance programs across wine-producing regions. In 2024, Fendt unveiled its e100 Vario tractor, equipped with a robust 100-kilowatt-hour (kWh) battery, showcasing its prowess for specialty crops. Meanwhile, Monarch Tractor's MK-V, which underwent field trials in 2025, introduced autonomous electric towing tailored for smaller harvesters. While hybrid genset models alleviate range anxiety, they introduce a layer of maintenance intricacies.

California's Advanced Clean Fleets regulation aims to phase out new off-road diesel vehicles by 2035. This mandate is steering Original Equipment Manufacturers (OEMs) towards a unified battery standard. With pack costs projected to dip below USD 100 per kilowatt-hour (kWh) by 2028, the pricing divide is shrinking. Yet, diesel is set to retain its stronghold on expansive hill farms, prioritizing refueling flexibility over potential emission penalties, even past 2031.

By Vineyard Size: Medium Vineyards, Small Vineyards Accelerate

Medium vineyards (51–200 Hectares) held the largest 43.2% share in 2025 because their acreage justifies ownership while remaining nimble with capital allocation. Large vineyards (above 200 hectares) show saturation, with fleets being upgraded rather than adding units. Small vineyards (below 50 hectares) will experience the fastest 12.4% CAGR through 2026-2031, driven by rental, cooperative, and subscription access. In 2025, cooperative purchases surged in Spain's Rioja and Italy's Chianti. Rioja, in particular, saw a 5% uptick in wine tourism visitors, underscoring the viability of shared assets. Meanwhile, financing programs with 100% loan-to-value are enticing first-time buyers, even amid tight profit margins.

Machinery design is increasingly leaning towards modularity to cater to diverse sizes. With adjustable head widths, a single model can adeptly navigate both the narrow terraces of German Riesling and the expansive rows of Californian Cabernet. Data subscription tiers are now aligned with vineyard sizes, ensuring enterprise software costs don't burden smallholders. Service contractors are strategically positioning satellite depots near scattered wine clusters, alleviating downtime concerns and boosting service penetration in villages that have traditionally relied on hand crews.

Geography Analysis

In 2025, Europe commanded a dominant 37.1% share of the grape harvesting machinery market, bolstered by advanced mechanization in France, Italy, and Spain. The region benefited from robust funding of USD 1.12 billion (EUR 1.061 billion) from the Annual Common Agricultural Policy, underscoring its commitment to fleet renewal and precision agriculture in key wine-producing areas. Highlighting the impact of climate volatility, Germany's 2025 crop shortfall nudged its traditionally conservative vineyard estates towards embracing mechanized harvesting. In a bid to modernize, Italy earmarked USD 152 million (EUR 144.1 million) for vineyard restructuring in 2026, with a focus on harvester upgrades. The European market, dominated by established manufacturers, is witnessing a pronounced shift in demand towards lightweight, digitally advanced, and fuel-efficient harvesting units, particularly for premium vineyards and Alpine terrace cultivation.

Asia-Pacific is set to witness a robust 9.4% CAGR in the grapes harvesting machinery market between 2026 and 2031. In China, Ningxia estates are modernizing their operations to counteract a dip in national wine output, bolstered by regional subsidies that ease machinery costs. In Australia, wage pressures have driven machinery hire rates to nearly USD 345 per hour in 2025, spurring large vineyard estates to accelerate trials of autonomous harvesting. Meanwhile, in India, the Maharashtra government is expanding mechanization grants to include grape pickers, signaling growing acceptance of mechanization in emerging commercial vineyards.

North America is witnessing a surge in demand for high-capacity grape harvesting machinery, fueled by increasing vineyard consolidation in major wine-producing states. Notable acquisitions, such as The Wine Group's 2025 buyout of a sprawling 6,600-acre vineyard, are paving the way for efficient harvesting fleets that promise reduced labor reliance. Concurrently, manufacturers are bolstering regional supply chains and enhancing aftermarket services. A case in point is Oxbo's New York facility, which is amplifying parts accessibility and service responsiveness for the often-overlooked East Coast vineyards. In South America, both Chilean and Argentine wine producers are ramping up investments in mechanization. Their goal: to curtail production costs, ensure consistent harvests, and bolster their competitive edge in exports, especially in light of rising labor costs. Meanwhile, the Middle East and Africa, still in the nascent stages of adoption, are witnessing selective mechanization growth. Regions like South Africa's Westerreliance on labormore amidn Cape and Turkey's Thrace are seeing commercial vineyards invest in modern harvesting tools, aiming to boost operational efficiency and maintain export quality.

Competitive Landscape

The grape harvesting machinery market remains moderately concentrated in 2025, with competition driven by established manufacturers offering integrated harvesting, automation, and vineyard-management capabilities. Pellenc S.A.S. holds a strong market position with advanced grape harvesters such as the OPTIMUM XXL, featuring EASY TOUCH and EASY DRIVE control systems to enhance operator efficiency. In 2025, New Holland Agriculture, a division of CNH Industrial N.V., strengthened its market presence with Braud grape harvesters, featuring upgraded cleaning systems, the SDC shaking system, and extensive dealer service networks. In April 2026, Oxbo International expanded its North American operations by opening a new manufacturing facility in Bergen, New York, to support the production of specialty-crop harvesting equipment and improve regional service capabilities. Grégoire S.A.S. and ERO GmbH continue to differentiate themselves with steep-slope harvesting systems, vineyard-specific machinery, and ISOBUS-enabled connectivity for mixed-brand equipment fleets.

Industry strategies are increasingly centered on electrification, automation, and robotic harvesting technologies. In 2024, Fendt introduced the e100 Vario electric tractor, designed for zero-emission vineyard and specialty-crop applications. Additionally, the European Union-backed BACCHUS robotics project continued its development of robotic vineyard systems, emphasizing autonomous inspection and selective harvesting technologies.

Innovation remains a critical factor for differentiation in the market. Pellenc S.A.S. continues to integrate optical sorting and machine-vision technologies, which help minimize unwanted material during harvesting and support premium wine production standards. Across the market, manufacturers are increasingly incorporating telematics, automation, and analytics platforms into harvesting equipment to enhance labor efficiency, improve harvest quality, and provide long-term service support.

Grape Harvesting Machinery Industry Leaders

Pellenc S.A.S.

Grégoire S.A.S. (SDF S.p.A.)

ERO GmbH

Oxbo International Corporation (Ploeger Oxbo Group B.V.)

New Holland Agriculture – Braud (CNH Industrial N.V.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Oxbo International Corporation opened a new manufacturing and service facility in Bergen, New York, expanding its presence to support high-value crop harvester sales, including grapes, and aftermarket service in premium wine regions such as the Finger Lakes, Hudson Valley, and Long Island appellations.

- November 2025: New Holland introduced upgraded Braud 9.50L, 9.70L, and 9.70M self-propelled grape harvesters at SITEVI 2025 in Montpellier, France, featuring the new Vari-Control System for proportional automatic leveling and faster hopper unloading. The launch strengthened New Holland’s position in high-capacity vineyard harvesting and reflected growing industry focus on productivity enhancement, operator safety, and precision machinery stabilization technologies.

- November 2025: New Holland unveiled its autonomous R4 robot series for vineyards and orchards at Agritechnica 2025. The company introduced both fully electric and hybrid-electric versions designed to automate mowing, tillage, and spraying operations while addressing labor shortages and sustainability requirements in specialty crop farming.

Global Grape Harvesting Machinery Market Report Scope

A grape harvesting machine is a mechanized device used in vineyards to detach grapes from vines and collect them efficiently during harvest, reducing manual labor and increasing harvesting speed. The grape harvesting machinery market report is segmented by harvester type (self-propelled, trailed or towed, and more), by mode of operation (manual, assisted or precision-guided, and more), by power source (diesel, hybrid, and electric), by vineyard size ( small vineyards (below 50 hectares), and more), and by geography (North America, South America, Europe, and More). The market forecasts are provided in USD.

| Self-Propelled Grape Harvesters |

| Trailed / Towed Grape Harvesters |

| Tractor-Mounted Grape Harvesters |

| Manual Steering & Operation |

| Assisted / Precision-Guided Operation |

| Autonomous / Semi-Autonomous Operation |

| Diesel-Powered Harvesters |

| Hybrid Harvesters |

| Electric Harvesters |

| Small Vineyards (Below 50 Hectares) |

| Medium Vineyards (51–200 Hectares) |

| Large Vineyards (Above 200 Hectares) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | France |

| Italy | |

| Spain | |

| Germany | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Australia | |

| Japan | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Morocco | |

| Rest of Africa |

| By Harvester Type | Self-Propelled Grape Harvesters | |

| Trailed / Towed Grape Harvesters | ||

| Tractor-Mounted Grape Harvesters | ||

| By Mode of Operation | Manual Steering & Operation | |

| Assisted / Precision-Guided Operation | ||

| Autonomous / Semi-Autonomous Operation | ||

| By Power Source | Diesel-Powered Harvesters | |

| Hybrid Harvesters | ||

| Electric Harvesters | ||

| By Vineyard Size | Small Vineyards (Below 50 Hectares) | |

| Medium Vineyards (51–200 Hectares) | ||

| Large Vineyards (Above 200 Hectares) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | France | |

| Italy | ||

| Spain | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Australia | ||

| Japan | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Morocco | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected size of the grapes harvesting machinery market by 2031?

The grapes harvesting machinery market size is forecast to reach USD 2.17 billion by 2031, reflecting steady demand growth across both established and emerging wine regions.

Which harvester type leads revenue?

Self-propelled units remain the largest class, capturing 48.5% of global revenue in 2025 because their high-capacity suits large commercial vineyards.

Which segment grows the fastest during 2026-2031?

Tractor-mounted harvesters post the fastest 11.8% CAGR during 2026-2031 as mid-sized estates leverage existing tractors to mechanize at lower cost.

What region records the highest growth?

Asia-Pacific is projected to deliver the highest 9.4% CAGR through 2026-2031 driven by Chinese modernization programs and Australian labor shortages.

How do subsidies influence adoption?

Government schemes, especially in the European Union, can cover up to 80% of purchase price, sharply reducing payback periods and accelerating fleet renewal.

Page last updated on: