Dehydrated Potato Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

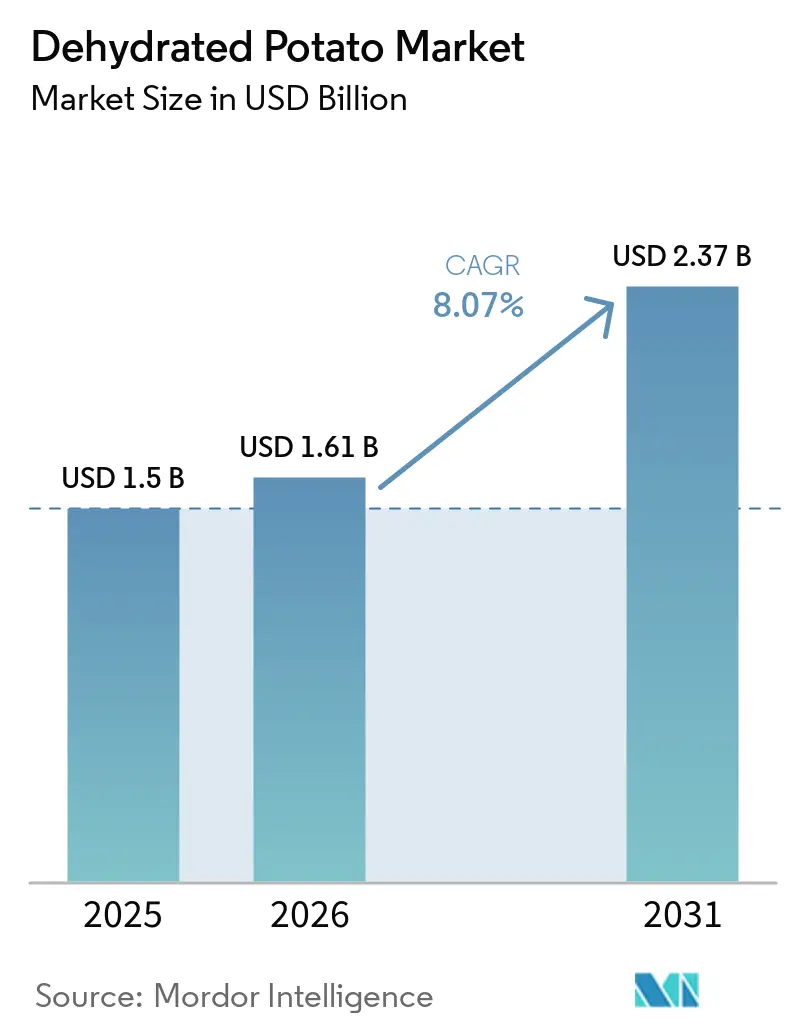

| Market Size (2026) | USD 1.61 Billion |

| Market Size (2031) | USD 2.37 Billion |

| Growth Rate (2026 - 2031) | 8.07% CAGR |

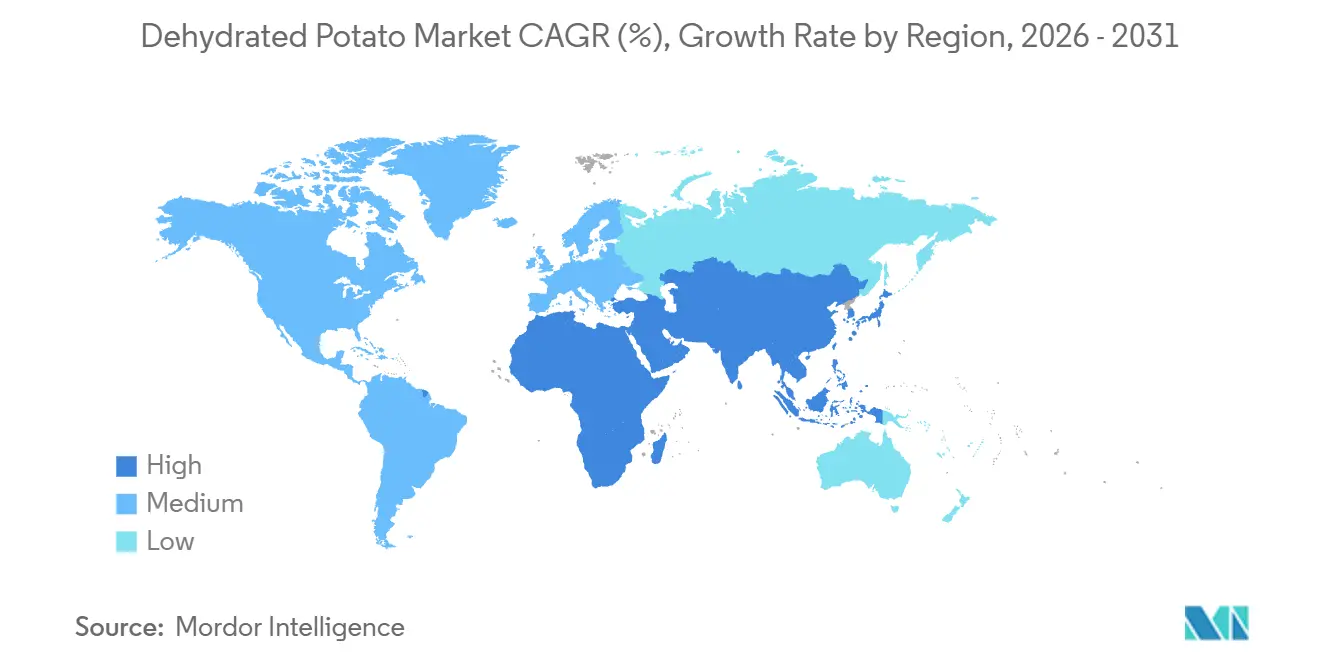

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dehydrated Potato Market Analysis by Mordor Intelligence

The dehydrated potato market size is projected to be USD 1.5 billion in 2025, USD 1.6 billion in 2026, and reach USD 2.4 billion by 2031, growing at a CAGR of 8.1% from 2026 to 2031. This growth is driven by food manufacturers, commercial kitchens, and snack producers shifting from fresh and frozen potatoes to shelf-stable formats, which simplify storage and standardize production. These formats enable faster meal preparation, reduce reliance on refrigerated logistics, and improve yield management during supply shortages, strengthening their role in convenience food production. In the Asia-Pacific, the expansion of QSR chains and institutional catering boosts demand, as ambient products align better with growth strategies than cold-chain alternatives. Market players are focusing on scaling operations, increasing capacity, and diversifying products, while raw potato supply pressures in North America emphasize processor efficiency and disciplined sourcing. This combination of strong demand, product innovation, and strategic moves ensures steady growth for the dehydrated potato market throughout the forecast period.

Key Report Takeaways

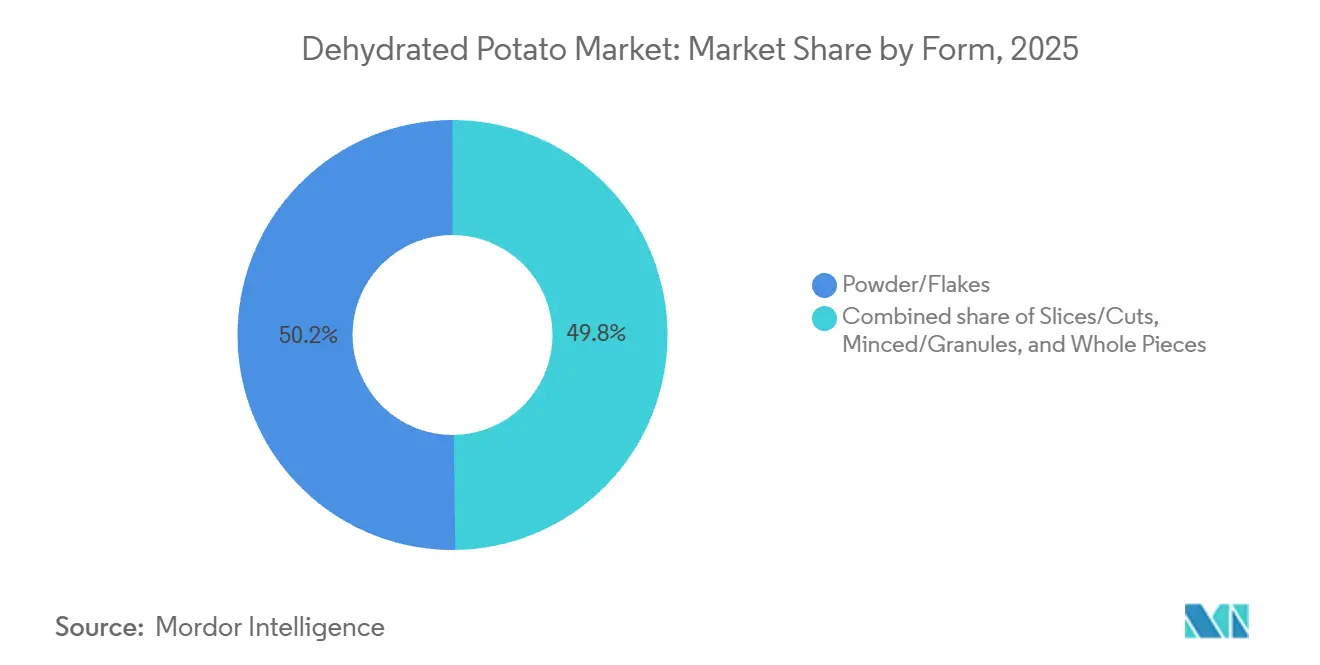

- By form, Powder and Flakes led with 50.21% revenue share in 2025, while Whole Pieces is forecast to expand at a 9.26% CAGR through 2031 in the dehydrated potato market.

- By nature, Conventional products held 75.23% share in 2025, while Organic products recorded the highest projected CAGR at 8.86% through 2031.

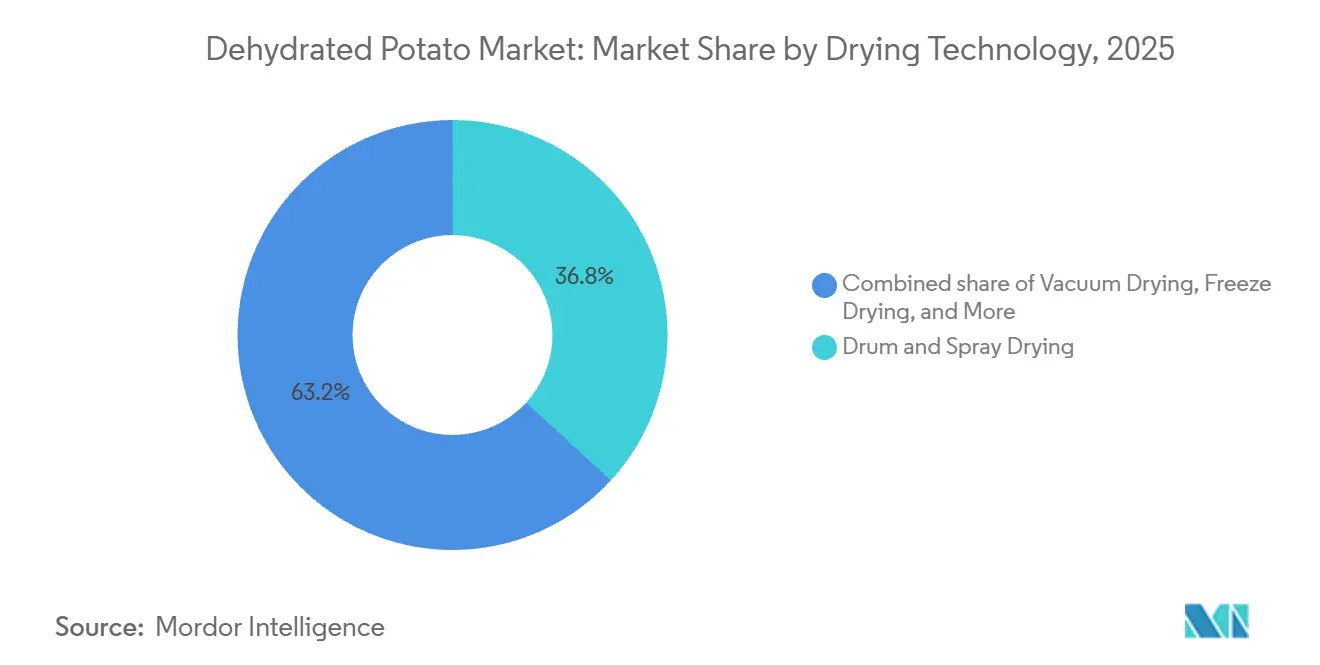

- By drying technology, Drum and Spray Drying accounted for 36.82% of revenue in 2025, while Vacuum Drying is advancing at a 9.5% CAGR through 2031.

- By distribution channel, Foodservice captured 56.78% of revenue in 2025, while Retail is forecast to grow at a 10.03% CAGR through 2031 in the dehydrated potato market.

- By geography, North America held 28.98% share in 2025, while Asia-Pacific remained the fastest-growing regional segment, forecast to grow at a 9.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dehydrated Potato Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand For Convenience Foods And Ready-To-Eat Products | +2.0% | Global, particularly North America, Europe, and urban APAC | Short term (≤ 2 years) |

| Extended Shelf Life And Ease Of Storage | +1.2% | Global, with elevated impact in Middle East, Africa, and South America | Medium term (2-4 years) |

| Technological Advancements In Dehydration Process | +1.4% | North America, Europe, and APAC manufacturing hubs | Long term (≥ 4 years) |

| Product Innovation And New Flavor Developments | +1.0% | North America, Europe, and East Asia | Medium term (2-4 years) |

| Growing Adoption Of Sustainable Practices | +0.7% | Europe and North America | Long term (≥ 4 years) |

| Health-Conscious Consumer Trends And Nutritional Benefits | +0.9% | North America, Europe, and urban APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Convenience Foods and Ready-to-Eat Products

Dehydrated potatoes are increasingly popular among foodservice buyers due to operational needs and changing consumer preferences. Quick-service restaurants and institutional caterers prefer them for reducing prep time, simplifying portion control, and fitting kitchens with limited labor and storage. This is especially beneficial in emerging markets, where restaurant chains expand faster with ambient products, avoiding costly investments in chilled storage and fresh produce handling. For instance, Lamb Weston’s 2026 launch in Singapore of the shelf-stable Original Mash Cup, requiring only water and 30 seconds of prep, suits labor-light kitchens and airline catering. A 2025 study in Frontiers in Nutrition also highlighted white potatoes' nutritional value, with one serving providing 372.42 mg of potassium (11% of daily intake) and 6% of daily dietary fiber. These factors are strengthening the role of dehydrated potatoes in convenience foods, side dishes, soups, and ready-to-eat meals that demand speed and consistency[1]Source: Frontiers in Nutrition, “Assessment of the Unique Nutrient Contribution of White Potatoes in the Diet and the Nutrient Implications of Replacing Refined and Whole Grains with Starchy Vegetables”, frontiersin.org.

Extended Shelf Life and Ease of Storage

Dehydrated potatoes offer a key advantage over frozen options: long storage life without full cold-chain reliance. Vacuum-sealed flakes and granules store well for extended periods, reducing spoilage and enabling better inventory management during volatile supply cycles. This benefit is especially significant in regions like the Middle East, Africa, and South America, where refrigerated distribution is limited, making frozen products costly to transport. In 2025, Idahoan Foods noted that its Fresh-Dried potato products eliminate 30-40% of waste linked to fresh potato handling in foodservice. This highlights the value of dehydrated products, even when convenience isn't the main buying factor. Additionally, USDA product specifications provide institutional buyers with clear standards for moisture, color, and reconstitution, ensuring confidence in storage performance and product consistency across large procurement programs. Consequently, the dehydrated potato market remains relevant in areas where shelf life and freight costs are as important as food quality.

Technological Advancements in Dehydration Process

Innovative processing methods are enhancing the quality of dehydrated potatoes while easing production burdens. EnWave revealed that its technique, which melds freeze drying with vacuum microwave dehydration, slashes drying time by over 75% compared to traditional freeze drying, all while maintaining the color, flavor, and nutritional integrity of the potatoes. These abbreviated drying cycles not only boost throughput but also enable quicker responses to seasonal raw material availability, resulting in reduced energy consumption per kilogram – a boon for processors keen on managing their margins. A 2024 study in Potato Research highlighted that an optimized pulsed electric field pretreatment trimmed drying time by 31.5% and cut specific energy consumption by 16.6%. Beyond the cost savings, these advancements empower processors to produce whole-piece products with superior rehydration texture, a feat that older drum-based systems struggled to achieve. This evolution is expanding the premium segment of the dehydrated potato market, solidifying quality differentiation at a time when potato flakes were predominantly viewed as a commodity.

Product Innovation and New Flavor Developments

The dehydrated potato market is shifting from basic commodity supply to customized ingredient systems and ready-to-consume formats. In 2025, Idahoan Foods launched +PROTEIN Mashed Potatoes, adding a protein boost to a familiar convenience product, appealing to health-conscious retailers. In 2026, Emsland Group introduced a flexible ingredient toolkit combining potato flakes, granules, fiber, pea protein, and texturizing starches. This innovation simplifies production for mid-sized food manufacturers and expands dehydrated potato applications beyond traditional uses like mashed potatoes and soup thickening. PubMed research shows freeze-dried potatoes retain high resistant starch levels after microwave heating, supporting their premium positioning for digestive health and nutrition. As a result, the market is focusing more on functionality, nutrition, and easier product customization for foodservice and retail sectors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Shelf Life Compared To Other Dehydrated Ingredients | -0.8% | Global, with elevated impact in high-humidity retail markets | Medium term (2-4 years) |

| Supply Chain Disruptions Due To Logistical Challenges | -0.9% | North America and APAC export routes | Short term (≤ 2 years) |

| Fluctuating Prices Of Raw Potato Materials | -0.8% | EU, North America, and APAC | Short term (≤ 2 years) |

| Regulatory Compliance Challenges For Food Safety | -0.6% | Global, with elevated impact on organic cross-border trade | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Shelf Life Compared to Other Dehydrated Ingredients

Dehydrated potatoes face shelf-life challenges compared to refined dry ingredients like starches and flours. Once opened, moisture exposure quickly reduces reconstitution quality, creating issues for buyers managing partial-use inventories in humid conditions. Drum-dried flakes, with higher residual fat content, are more prone to quality degradation and off-flavors from oxidation during long storage. This risk is greater in tropical retail markets, where secondary packaging and strict storage controls are often necessary to maintain product performance. USDA commodity specifications stress that shelf life depends on proper processing and storage, not just long-life claims. These challenges limit the market's growth in environments with high exposure and slow pack turnover.

Supply Chain Disruptions Due to Logistical Challenges

The dehydrated potato market faces supply chain risks due to the concentration of raw material production and processing in limited locations. Key hubs like Idaho, Washington, and the Netherlands mean that weather disruptions, port delays, or trade shifts can impact multiple markets simultaneously. USDA ERS reported a 20% drop in U.S. dehydrated potato exports during the 2024/25 marketing year, with declines in Japan, Mexico, Canada, and the UK, indicating widespread adjustments rather than isolated issues[2]Source: USDA Economic Research Service, “Vegetables and Pulses Outlook: VGS-377”, ers.usda.gov. Additionally, USDA NASS noted a 2% decrease in U.S. and Canadian potato production in 2025, totaling approximately 538 million cwt, tightening raw material supply for processors. Buyers without diversified sourcing strategies face greater uncertainty, especially when procurement contracts require consistent volume, quality, and delivery timing across regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Flakes Lead Volume, Whole Pieces Gain Ground

In 2025, Powder and Flakes led the dehydrated potato market, holding 50.2% of the form segment's market share. Their dominance is due to extensive use in instant mashed potatoes, batter systems, soup thickening, and extruded snacks, where quick rehydration and consistent texture outweigh the need for visible potato structure. USDA ERS data revealed that potato flakes accounted for nearly 75% of U.S. dehydrated potato export value, highlighting their central role in trade. USDA quality standards for flakes, focusing on moisture, color, and water absorption, ensure reliable performance for major buyers like military, government, and institutional meal programs. While slices, cuts, minced forms, and granules remain in demand for soups and snacks, they lack the volume dominance of flakes and powders in the market.

Whole Pieces is expected to grow at a strong 9.3% CAGR through 2031, making it the fastest-growing category in the dehydrated potato market. Rising demand comes from foodservice and retail buyers seeking a less processed look and a rehydrated texture similar to freshly cooked potatoes. Advances in vacuum drying and pulsed electric field pretreatment are preserving cellular structure during processing, improving texture after rehydration. These quality improvements are driving adoption in premium soups, meal kits, and airline catering, where visual appeal and texture are critical. As a result, whole-piece formats are shifting from niche to mainstream, combining convenience with a premium eating experience.

By Nature: Conventional Products Retain Dominance as Organic Segment Accelerates

In 2025, conventional products held a 75.2% share of the dehydrated potato market, reflecting large buyers' preference for reliability and cost-effectiveness. Foodservice operators and industrial processors favor stable pricing, contract farming, and consistent year-round availability, making conventional raw materials the preferred choice. A January 2025 partnership between Emsland Group and UniBourne in India showcased suppliers using conventional lines to access growing processed food markets, where price remains a key factor. USDA data reported a 2% drop in U.S. and Canadian potato production in 2025, increasing raw material costs and pressuring the conventional segment. Despite this, conventional supplies dominate the market due to their scalability, affordability, and established sourcing practices.

Organic products are projected to grow at an 8.9% CAGR through 2031, outpacing the overall dehydrated potato market. This growth is driven by premium retail buyers and health-focused foodservice operators seeking traceable, additive-free ingredients and cleaner product positioning. The rising demand for organic products aligns with a broader trend toward transparent sourcing in packaged foods and prepared meals. Agrana's 2024 launch of an organic dehydrated potato line, as noted in the user draft, shows suppliers with conventional roots treating organic as a distinct commercial tier rather than a niche. This shift indicates the industry is creating a clearer premium hierarchy, positioning organic products alongside conventional ones without replacing the mass market base.

By Drying Technology: Drum Drying Leads, Vacuum Drying Gains

In 2025, Drum and Spray Drying accounted for 36.8% of segment revenue, maintaining its dominance in the dehydrated potato market. This is due to its cost efficiency, widespread processor use, and the industry's focus on low unit costs for high-volume flake and granule production over premium texture. Major North American and European plants, equipped for large-scale operations, ensure a long replacement cycle and durability for this technology. Conventional systems remain relevant through gradual energy and waste improvements, even as newer methods emerge. Freeze drying continues to play a key role in premium sectors like outdoor foods, military rations, and emergency storage, where nutrient preservation and extended storage justify higher costs.

Vacuum Drying, projected to grow at a 9.5% CAGR through 2031, is the fastest-growing technology in the dehydrated potato market. This growth stems from rising demand for better flavor, color retention, nutrient preservation, and improved texture after rehydration. EnWave data shows hybrid vacuum microwave dehydration reduces drying time by over 75% compared to freeze drying, enhancing throughput and commercial viability. Additionally, a 2024 Potato Research study reported a 16.6% drop in specific energy consumption with pulsed electric field pretreatment, strengthening the efficiency and quality case. These advancements make vacuum-based systems an attractive investment for processors targeting premium applications without sacrificing operational efficiency.

By Distribution Channel: Foodservice Dominates While Retail Captures the Fastest Growth

In 2025, foodservice led the dehydrated potato market, contributing 56.8% of the revenue. This dominance highlights the importance of dehydrated potato products in commercial kitchens, where quick preparation, consistent yields, ambient storage, and reduced waste improve cost control. Quick Service Restaurant (QSR) chains use these products for mashed potato sides, hash browns, soup bases, and coating systems, showing demand driven by necessity rather than promotion. Bulk purchasing gives foodservice buyers pricing and contract advantages, surpassing those of retail pack formats. While other channels diversify, the dehydrated potato market remains anchored in institutional and commercial kitchen demand.

Retail is expected to grow at a 10.0% CAGR through 2031, becoming the fastest-growing distribution channel in the dehydrated potato market. This growth stems from steady home cooking demand and the suitability of shelf-stable potato products for online sales over frozen ones. Online retail is expanding rapidly due to lower delivery complexities and return risks of ambient products, improving the economics of broader assortments. Supermarkets and hypermarkets dominate retail volumes with branded flakes and instant mashed products, while convenience stores increasingly offer single-serve and flavored options. Retail is becoming a key channel for challenger brands, especially in organic and flavored segments, which often grow online before scaling in larger store networks.

Geography Analysis

In 2025, North America held a 29.0% share of the dehydrated potato market, maintaining its position as the leading demand region. The region benefits from integrated processing infrastructure in Idaho, Washington, Oregon, and parts of Canada, strategically located near major potato production zones. This setup reduces transportation costs for high-moisture raw materials and improves economic efficiency for large processors. However, challenges persist: USDA ERS reported a 20% decline in U.S. dehydrated potato export volumes for the marketing year 2024/25 across key destinations. Additionally, USDA NASS noted a 2% drop in U.S. potato production in 2025, totaling 413 million cwt, due to a 3% reduction in planted area. These factors are pushing processors to prioritize yield efficiency and throughput discipline.

Asia-Pacific emerged as the fastest-growing region in the dehydrated potato market during the forecast period. Growth is driven by rising instant food manufacturing, QSR expansion, and increased use of packaged convenience products in daily meals. China's instant noodle production ensures steady demand for flakes and granules used in texture management and shelf-stable meal systems. In India, dehydrated potatoes are increasingly used in instant mash, cup soups, and baby food, aligning with the growth of processed foods and convenience retail. Aviko expanded its Gansu facility in December 2025, increasing potato flake capacity by 70%, while McCain invested USD 480 million in Madhya Pradesh in July 2025, reflecting major suppliers' confidence in the region's long-term potential.

Europe remains the largest production base for dehydrated potatoes, shifting focus from commodity throughput to value-added supply. Emsland Group's plan to double potato flake capacity at Emlichheim highlights confidence in European and export demand, despite rising costs for processors. In South America, led by Brazil, Argentina, and Colombia, demand is growing due to QSR expansion and rising urban incomes, though local processing remains limited, and import reliance is high. The Middle East and Africa show steady institutional demand, with Gujarat-based exports to GCC markets indicating a shift in sourcing routes within the dehydrated potato market.

Competitive Landscape

McCain Foods, Lamb Weston, J.R. Simplot, and Aviko lead the dehydrated potato market, leveraging their scale, sourcing reach, and customer access. These companies benefit from vertical integration, extensive raw material networks, and strong ties with foodservice, retail, and industrial buyers. Competing closely are Emsland Group, Idahoan Foods, Basic American Foods, and Idaho Pacific Corporation, which focus on formulation expertise, regional advantages, and specialized ingredient offerings. Royal Avebe's acquisition of Solan in August 2025 expanded its portfolio from starches to flakes and granules, adding new products and processing assets in Poland and Sweden. This highlights the importance of portfolio expansion to meet growing demand and diverse product needs.

Emsland Group plans to double its flake capacity in Germany and partnered with UniBourne Food Ingredients in India in January 2025. Aviko increased potato flake output by 70% at its Gansu plant in December 2025, supporting food manufacturers and snack producers in the Asia-Pacific region. McCain's USD 480 million investment in a Madhya Pradesh food processing plant in July 2025 reflects confidence in the region's contract farming and long-term demand. These strategies show that success in the dehydrated potato market depends on capacity expansion, supply security, and quick establishment of local or regional market routes.

Technology is a key differentiator in the dehydrated potato market, especially between commodity supplies and premium ingredients. Advanced techniques like vacuum microwave hybrid drying and pulsed electric field support enable processors to produce whole-piece and premium flake products with better texture and nutrient retention than traditional drum-dried outputs. Lamb Weston’s launch of the Original Mash Cup in Singapore in 2026 illustrates a shift from bulk ingredients to operator-ready, shelf-stable solutions with quick preparation. This combination of scale, technology, and targeted channel development ensures competition in the dehydrated potato market remains strong, neither overly fragmented nor dominated by a few players.

Dehydrated Potato Industry Leaders

McCain Foods Limited

Lamb Weston Holdings, Inc.

The J. R. Simplot Company

Aviko B.V.

Emsland Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Lamb Weston introduced Snap Fries, Frenzy Fries, and Original Mash Cup at Food & Hospitality Asia 2026 in Singapore. The Original Mash Cup is a shelf-stable, ambient-temperature dehydrated potato format with a 12-month shelf life requiring only water and 30 seconds of preparation time, designed for labour-constrained foodservice and airline catering operators across Southeast Asia. The product range signals a strategic move by Lamb Weston into direct foodservice operator channels beyond bulk ingredient supply.

- December 2025: Aviko officially commenced Phase III expansion works at its Gansu, China potato dehydration facility in Zhangye, targeting a 70% increase in potato flake production capacity. The expansion is part of parent company Cosun's Unlock 30 strategy and positions Aviko to serve growing demand across Asia-Pacific food manufacturers and snack producers.

- August 2025: Royal Avebe acquired Solan, a Poland-based producer of potato flakes and granules, in an agreement signed August 18, 2025. The acquisition diversifies Avebe's portfolio beyond potato starch for the first time, adding production sites in Poland and Sweden and providing access to established flake and granule customer relationships.

Global Dehydrated Potato Market Report Scope

| Slices/Cuts |

| Minced/Granules |

| Whole Pieces |

| Powder/Flakes |

| Organic |

| Conventional |

| Freeze Drying |

| Vacuum Drying |

| Drum and Spray Drying |

| Others |

| Foodservice | |

| Retail | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Form | Slices/Cuts | |

| Minced/Granules | ||

| Whole Pieces | ||

| Powder/Flakes | ||

| By Nature | Organic | |

| Conventional | ||

| By Drying Technology | Freeze Drying | |

| Vacuum Drying | ||

| Drum and Spray Drying | ||

| Others | ||

| By Distribution Channel | Foodservice | |

| Retail | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the dehydrated potato space by 2031?

The dehydrated potato market is projected to reach USD 2.37 billion by 2031, rising from USD 1.61 billion in 2026 at an 8.07% CAGR.

Which product form leads current revenue?

Powder and Flakes led with 50.21% share in 2025 because they are deeply used in instant mash, soups, coatings, and snack production.

Which distribution route is growing the fastest?

Retail is forecast to grow at a 10.03% CAGR through 2031, helped by at-home cooking demand and easier online fulfillment for shelf-stable products.

How is technology changing product quality?

Vacuum microwave and pulsed electric field supported drying are improving texture, color, nutrient retention, and energy efficiency, which is helping premium formats such as whole pieces grow faster.

Page last updated on: