Agricultural Machinery Components Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

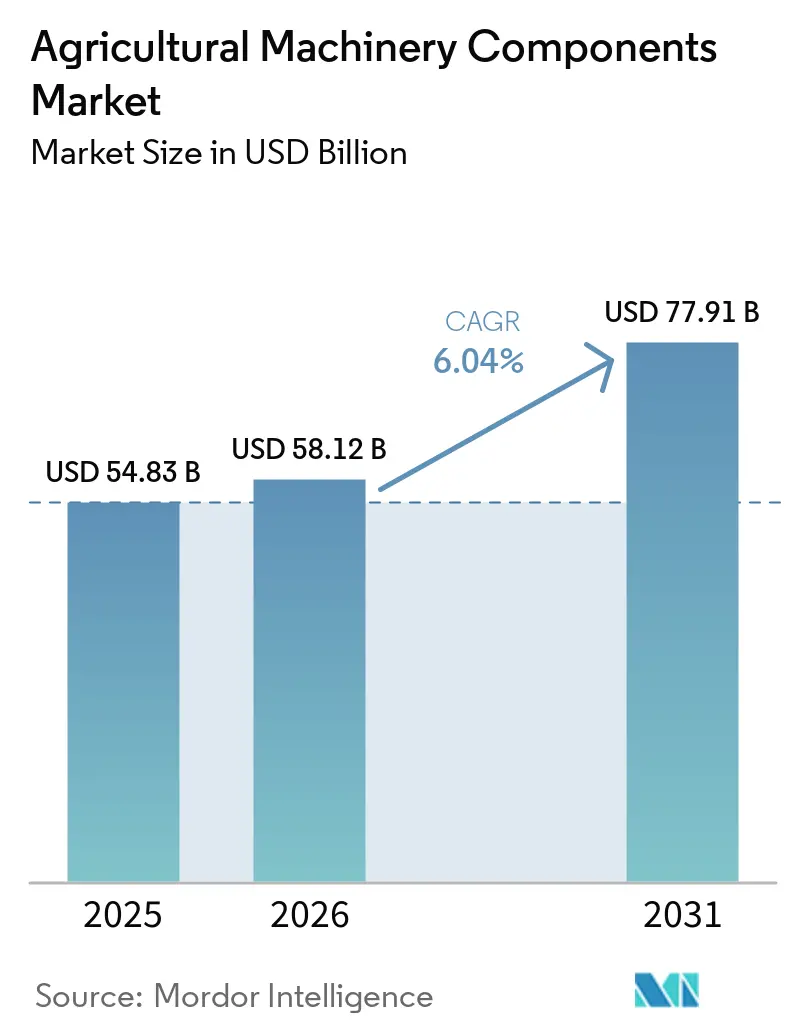

| Market Size (2026) | USD 58.12 Billion |

| Market Size (2031) | USD 77.91 Billion |

| Growth Rate (2026 - 2031) | 6.04% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Agricultural Machinery Components Market Analysis by Mordor Intelligence

The agricultural machinery components market size is projected to grow from USD 54.83 billion in 2025 and USD 58.12 billion in 2026 to USD 77.91 billion by 2031, registering a CAGR of 6.04% between 2026 and 2031. Demand in the market remained steady in 2025, because lower new-equipment purchases are keeping tractors, harvesters, and application equipment in service for longer periods, which raises replacement demand for engines, hydraulics, driveline systems, filters, and control modules. In Europe, tractor registrations fell to a 10-year low in 2024[1]Source: European Agricultural Machinery Association (CEMA), “European Tractor Registrations at 10-Year Low in 2024,” cema-agri.org. In China, a renovation program backed across multiple provinces overhauled tractors, showing that policy-led refurbishment can directly support the market. Competitive activity in the market is also shifting toward mixed-fleet retrofits, digital ordering, and wider repair access, which gives independent distributors and technology suppliers more room to serve installed fleets. At the same time, software restrictions, compliance needs, and cost pressure in metal-intensive components are raising execution complexity, which favors suppliers with stronger catalog depth, documentation capability, and regional service reach in the agricultural machinery components market.

Key Report Takeaways

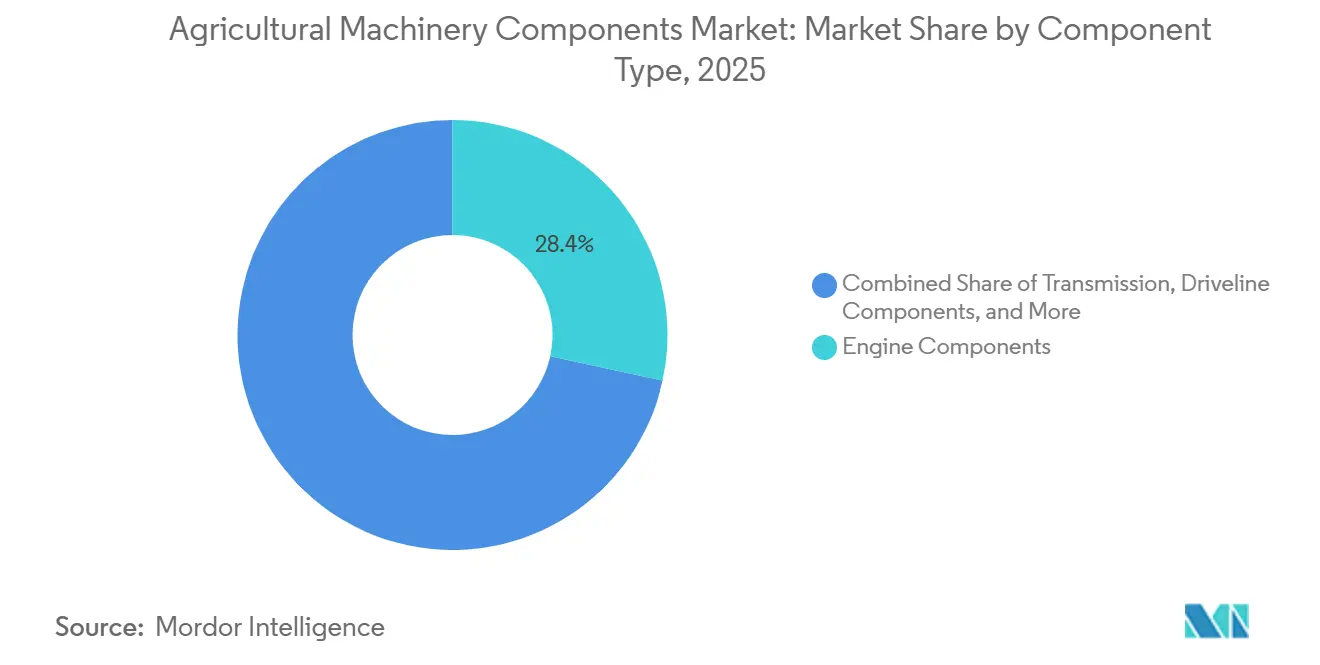

- By component type, engine components held 28.4% of the agricultural machinery components market share in 2025, while electrical and electronic components are projected to expand at an 8.1% CAGR through 2031.

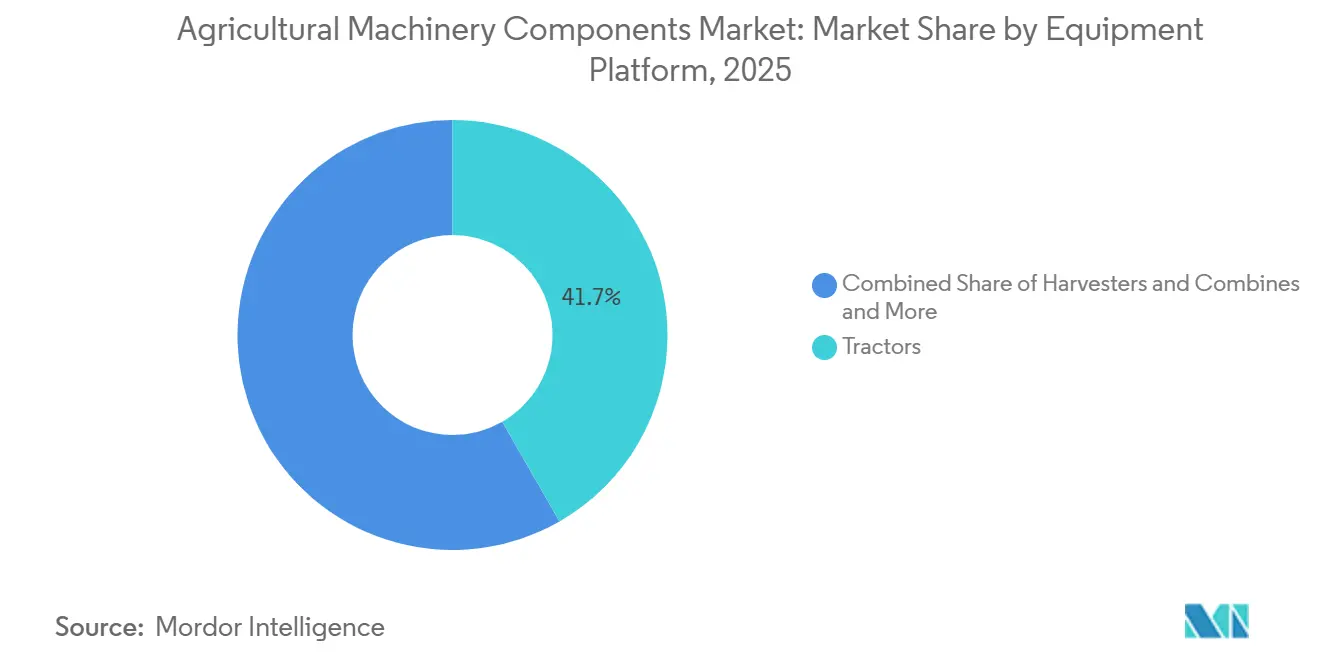

- By equipment platform, tractors accounted for 41.7% share of the market in 2025, while sprayers and fertilizer applicators are projected to grow at a 6.6% CAGR through 2031.

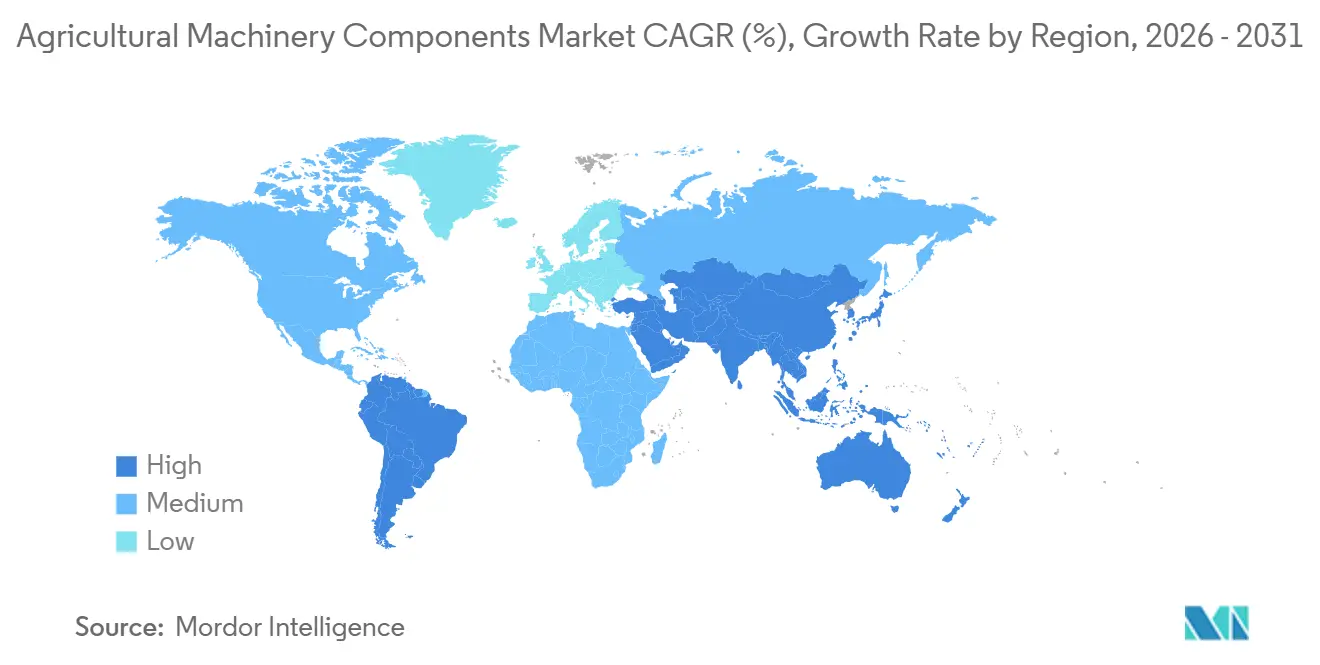

- By geography, North America held 32.7% share of the agricultural machinery components market size in 2025, while Asia-Pacific is forecast to expand at a 6.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agricultural Machinery Components Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging global fleet and replacement cycles | +1.4% | Worldwide, strongest in North America, Europe, and South America | Short term (≤ 2 years) |

| Precision farming electronics and telematics retrofits | +1.1% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Mechanization expansion in India, China, Brazil, and Southeast Asia | +1.0% | Asia-Pacific core, with spillover to South America, Middle East, and Africa | Medium term (2-4 years) |

| High new-equipment prices favor life-extension spending | +0.9% | Worldwide, concentrated in North America and Europe | Short term (≤ 2 years) |

| Right-to-repair regulation expands accessible parts demand | +0.5% | North America and Europe | Medium term (2-4 years) |

| Carbon-accounting-ready retrofit modules and verified emissions data | +0.4% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Global Fleet and Replacement Cycles

Fleet aging remains the strongest structural support for the agricultural machinery components market because component demand rises when producers keep tractors, harvesters, and applicators in service for longer periods. Italy’s used tractor activity reached 57,000 units and the average machine age was 22 years[2]Source: European Agricultural Machinery Association (CEMA), "European Tractor Registrations," cema-agri.org, which supports steady demand for filters, bearings, gaskets, injectors, hoses, and cooling system components in the market. Deere and Company and AGCO Corporation both reported weaker equipment demand through 2025, which reinforces the pattern of farmers holding on to existing machines and allocating more money to maintenance rather than new purchases. Older machines also remain easier for independent workshops to service because many predate the tighter software controls found on newer platforms, which broadens the serviceable base for the market. This combination of slower fleet renewal, wider repair access, and heavier wear on mature equipment keeps replacement cycles active even when new-equipment shipments remain under pressure in the agricultural machinery components market.

Precision Farming Electronics and Telematics Retrofits

Electrical and control-system retrofits are becoming a major growth layer inside the agricultural machinery components market because legacy fleets are being updated with guidance, monitoring, and connected service capabilitie. AGRA-GPS updated its JD-Bridge retrofit in July 2025, and that product integrates John Deere AutoTrac guidance onto non-John Deere machines, which shows active demand for cross-brand retrofit hardware[3]Source: AGRA-GPS, “JD-Bridge,” agragps.eu. AGCO Corporation completed its PTx Trimble transaction in April 2024, and the company is building a brand-agnostic precision agriculture portfolio aimed at USD 2 billion in sales by 2029. As more mixed fleets add sensors, displays, controllers, telematics units, and harnesses, replacement demand shifts from purely mechanical wear toward software-linked electronic hardware in the agricultural machinery components market. AxisTech’s FarmScore platform is already active across the United States, Australia, and Brazil, which confirms that data-rich machinery hardware is moving into day-to-day farm operations rather than staying limited to pilot use. These products also tend to refresh faster than core mechanical assemblies because compatibility, connectivity, and sensor performance change more often than castings or shafts. That shorter replacement interval is why electronics are becoming a larger revenue pool inside the market, especially where mixed-fleet operation and retrofit economics matter more than brand loyalty.

Mechanization Expansion in India, China, Brazil, and Southeast Asia

Mechanization growth across developing farm systems strengthens the agricultural machinery components market because every new machine sale becomes future service demand after the first operating cycle. Deere and Company reported that small agriculture and turf sales volumes in India increased significantly in fiscal year 2025, which signals a wider installed base that will need recurring engine, filter, hydraulic, tire, and electronic replacement demand. China’s 2025 tractor renovation program shows that installed bases in Asia are not only expanding but also being supported through organized refurbishment, which directly supports component turnover. AxisTech’s carbon-intelligence platform is active in Brazil, which suggests that large commercial operations there are already adopting telemetry-linked systems that increase future service content per machine. Kubota Corporation’s investment in Kilter in February 2026 shows that manufacturers are positioning for the next phase of precision-enabled machinery demand across regions where mechanization depth is still rising. As fleets deepen in India, China, Brazil, and Southeast Asia, component demand tends to become more stable because maintenance cycles expand across a larger active machine population in the market. This driver matters over several years because the agricultural machinery components market usually captures the economic benefit after machines enter field use and begin to accumulate utilization hours.

High New-Equipment Prices Favor Life-Extension Spending

Higher replacement costs for whole machines are helping the agricultural machinery components market because farmers are more willing to rebuild equipment they already own when capital budgets tighten. Lower equipment demand reported by Deere & Company, CNH Industrial N.V., and AGCO Corporation through 2024 and 2025 shows that many operators delayed major purchases and stayed focused on upkeep. In Europe, sector conditions remained difficult, and European Agricultural Machinery Industry Association (CEMA) indicated continuing pressure from farm incomes, energy costs, and input costs, which supports repair-first decisions in the market. When budgets are constrained, operators often postpone full machine replacement but still need hydraulic pumps, injectors, bearings, shafts, seals, and cooling system repairs to keep field operations running. That behavior benefits distributors and component specialists because rebuild work usually involves multiple line items rather than a single emergency purchase. It also supports remanufacturing and bundled service kits, since owners prefer predictable maintenance spending over large capital outlays when equipment affordability weakens. As long as new-equipment replacement remains financially difficult, life-extension spending should continue to underpin the agricultural machinery components market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High equipment financing pressure slows discretionary rebuilds | -0.9% | Worldwide, strongest in North America, Europe, and South America | Short term (≤ 2 years) |

| Proprietary software locks and paired diagnostics limit independent replacement | -0.7% | North America and Europe | Medium term (2-4 years) |

| Rental and custom-hiring models defer some replacement purchases | -0.6% | Asia-Pacific core, Middle East and Africa, and South America | Medium term (2-4 years) |

| Tariff-origin compliance and metal-input traceability raise component complexity | -0.5% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Equipment Financing Pressure Slows Discretionary Rebuilds

Financing pressure limits the agricultural machinery components market when farmers postpone non-essential upgrades and buy only what is needed to keep machines operating. CEMA noted that sector conditions remained difficult in Europe, with real income pressure continuing in 2024 while energy costs stayed 23% above four-year averages and fertilizer prices remained elevated[4]Source: CEMA – European Agricultural Machinery, “European Tractor Registrations at 10-Year Low in 2024,” cema-agri.org. Deere and Company reported increasing allowance for credit losses and rising non-performing financing receivables, which shows measurable financial strain in farm equipment funding. Under those conditions, buyers still replace safety-critical and uptime-critical components, but they often delay premium rebuild packages, higher-specification upgrades, and broad preventive overhauls. This creates a mixed pattern where baseline demand remains intact, yet basket size can weaken for discretionary orders in the market. Credit pressure also hurts dealers and distributors that rely on larger service packages because customers focus on near-term cash preservation. Until farm incomes and financing conditions improve, this restraint will continue to cap some of the upside for the agricultural machinery components market.

Proprietary Software Locks and Paired Diagnostics Limit Independent Replacement

Software pairing remains a real brake on the agricultural machinery components market because modern electronic modules often cannot be installed or calibrated without controlled access to brand-specific tools. Deere and Company disclosed that the United States Federal Trade Commission filed a lawsuit in January 2025 alleging monopolization through restrictions on access to repair software, which confirms that the issue is material at the company level. Even when a third-party component is technically compatible, installation can still be delayed if pairing, coding, or emissions-system validation is locked behind original equipment manufacturer channels. This affects high-value electronics most directly, including control units, displays, telematics modules, and software-linked hydraulic controls. Retrofit providers have shown that mixed-fleet integration is possible, but those solutions still highlight how difficult direct replacement can be when proprietary architecture is involved. The United States Environmental Protection Agency’s 2026 repair guidance helps on emissions-related work, yet it does not fully remove the wider software-access challenge across every system. As a result, the market still faces uneven access conditions that can slow independent competition in advanced electronics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component Type: Engine Components Led Revenue While Electronics Grew Fastest

Engine components held 28.4% of the agricultural machinery components market share in 2025, supported by the universal service and replacement needs of tractors, harvesters, sprayers, tillage machinery, and other field equipment operating across intensive agricultural production systems globally. Transmission and driveline components, hydraulic and PTO components, wear components, and electrical and electronic components collectively generated significant aftermarket revenues. This growth was primarily driven by increasing machinery utilization rates, aging agricultural equipment fleets, and a growing emphasis on preventive maintenance and enhancing operational efficiency in commercial farming operations.

Electrical and electronic components are projected to expand at an 8.1% CAGR through 2031, making this category the fastest-growing in the market, as mixed-fleet retrofits and the adoption of precision farming drive demand for sensors, displays, electronic control units, GPS guidance systems, and telematics hardware. AGCO Corporation continues to scale its PTx Trimble precision platform across global farming operations. Tires, wheels, and structural parts remain important. Still, their growth is comparatively more exposed to raw material cost fluctuations, machinery cyclicality, and regulatory compliance burdens than electronics-oriented component categories.

By Equipment Platform: Tractors Anchored Revenue While Sprayers Advanced Most Quickly

Tractors accounted for 41.7% of revenue in 2025 and represented the largest platform in the agricultural machinery components market, reflecting their broad installed base across mature and developing farm systems. Rising tractor mechanization across row crop, horticulture, and mixed farming operations continues supporting strong replacement demand for engines, transmission and driveline components, hydraulic and PTO components, and structural components used in high-utilization agricultural equipment globally.

Sprayers and fertilizer applicators are projected to grow at a 6.6% CAGR through 2031, the fastest rate among platforms, as precision application upgrades increase the replacement need for boom sensors, flow-control units, section-control actuators, and guidance-linked electronics. CNH Industrial N.V. has continued to prioritize precision technology in its strategic plan, supporting sustained component demand across electronically enabled spraying and nutrient application systems. Furthermore, increasing adoption of variable-rate technologies, automated section control, and connected farm equipment is accelerating demand for advanced electronic and sensor-integrated machinery components across commercial agricultural operations worldwide.

Geography Analysis

North America held 32.7% of the agricultural machinery components market share in 2025 and remained the largest regional revenue base because it has a large installed fleet of high-horsepower equipment and demanding operating cycles. Deere and Company’s 2025 filing also showed rising credit stress, which reinforces the shift from new-equipment replacement toward service and maintenance work. The United States Environmental Protection Agency’s February 2026 repair guidance should widen access to emissions-related repairs for independent channels. The Freedom for Agricultural Repair and Maintenance Act, introduced in November 2025, adds further policy support for access to tools, software, and documentation. Together, those conditions keep North America central to the market.

Asia-Pacific is projected to grow at a 6.9% CAGR through 2031 and represents the fastest-expanding regional block in the market. Deere and Company reported a significant rise in India sales volumes for its small agriculture and turf business in fiscal year 2025, which points to a larger installed base entering recurring service cycles. Kubota Corporation’s February 2026 investment in Kilter also shows that suppliers are building more precision capability for fleets in this region. These factors give Asia-Pacific the strongest expansion profile in the agricultural machinery components market.

Europe is being shaped by aging agricultural machinery fleets and increasingly stringent regulatory compliance requirements, which are steadily strengthening replacement demand for aftermarket machinery components, emission-compatible systems, precision electronics, and equipment modernization solutions across regional farming operations. That mix supports steady demand for wear items, hydraulics, driveline systems, and retrofit-capable electronics in the market. South America remains important because commercial-scale operations are already using data-linked machinery tools, as shown by AxisTech’s FarmScore activity in Brazil. Middle East and Africa remain smaller today, but the market should broaden there as mechanization deepens and active machine populations expand.

Competitive Landscape

The agricultural machinery components market remains highly fragmented. The broad mix of machinery brands, model generations, and equipment categories continues to create opportunities for regional distributors, remanufacturers, and specialized component suppliers. Deere & Company maintains a strong structural advantage through its extensive global distribution and warehousing infrastructure, while CNH Industrial N.V. continues expanding precision technology integration and aftermarket service capabilities across its agricultural equipment portfolio.

AGCO Corporation has continued strengthening its replacement component and precision farming business through the expansion of mixed-fleet precision platforms and aftermarket service operations. Meanwhile, CLAAS KGaA mbH is increasing investments in research, development, and advanced agricultural technologies to support next-generation machinery systems. Furthermore, Kubota Corporation is expanding its precision agriculture ecosystem through strategic technology investments, reinforcing long-term demand for retrofit-compatible and digitally integrated machinery components across global farming operations.

Dana Incorporated, HYDAC International GmbH, Gruppo Carraro S.p.A, and Comer Industries S.p.A remain strategically important as hydraulic systems, drivetrains, axles, sensors, filtration technologies, and motion-control components continue generating recurring replacement demand across mixed agricultural equipment fleets. Additionally, increasing digitalization of aftermarket channels and online genuine-parts platforms is intensifying competition around catalog accuracy, compatibility support, predictive maintenance integration, and rapid component availability for multi-brand repair operations.

Agricultural Machinery Components Industry Leaders

-

Deere & Company

-

CNH Industrial N.V.

-

AGCO Corporation

-

Kubota Corporation

-

CLAAS KGaA mbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Kubota Corporation made a strategic investment in Kilter as part of a USD 7.0 million financing round, reinforcing its precision agriculture retrofit strategy in European and wider markets.

- November 2025: Danfoss A/S launched the Aeroquip GH888 hydraulic hose for tractor main pump applications, designed to reduce hose weight, improve routing flexibility, and support higher-pressure hydraulic systems in modern agricultural equipment. The development strengthens Danfoss’ position in hydraulic component solutions for high-performance tractors and precision-enabled farming machinery.

- June 2024: Karasawa Agricultural Machinery Service Co., Ltd in Japan introduced the Noukinavi online platform for ordering genuine parts, providing international shipping for Kubota Corporation and Yanmar Holdings Co., Ltd.

Global Agricultural Machinery Components Market Report Scope

The Agricultural Machinery Components Market encompasses the systems and technologies that enhance the functionality, performance, maintenance, and operational efficiency of agricultural machinery utilized in land preparation, planting, irrigation, crop protection, harvesting, and post-harvest farming activities. The Agricultural Machinery Components Market is segmented by Component Type (Engine Components, Transmission and Driveline Components, Hydraulic and PTO Components, Electrical and Electronic Components, Tires and Wheels, Filters and Fluid Management Components, Wear Components and Ground-Engaging Tools, Chassis and Structural Components, and Other Components), by Equipment Platform (Tractors, Harvesters and Combines, Planters and Seeders, Tillage and Cultivation Equipment, Sprayers and Fertilizer Applicators, Irrigation Equipment, and Hay and Forage Equipment), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Engine Components |

| Transmission and Driveline Components |

| Hydraulic and PTO Components |

| Electrical and Electronic Components |

| Tires and Wheels |

| Filters and Fluid Management Components |

| Wear Components and Ground-Engaging Tools |

| Chassis and Structural Components |

| Other Components |

| Tractors |

| Harvesters and Combines |

| Planters and Seeders |

| Tillage and Cultivation Equipment |

| Sprayers and Fertilizer Applicators |

| Irrigation Equipment |

| Hay and Forage Equipment |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Italy | |

| United Kingdom | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Component Type | Engine Components | |

| Transmission and Driveline Components | ||

| Hydraulic and PTO Components | ||

| Electrical and Electronic Components | ||

| Tires and Wheels | ||

| Filters and Fluid Management Components | ||

| Wear Components and Ground-Engaging Tools | ||

| Chassis and Structural Components | ||

| Other Components | ||

| By Equipment Platform | Tractors | |

| Harvesters and Combines | ||

| Planters and Seeders | ||

| Tillage and Cultivation Equipment | ||

| Sprayers and Fertilizer Applicators | ||

| Irrigation Equipment | ||

| Hay and Forage Equipment | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| United Kingdom | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is driving growth in agricultural machinery components demand through 2031

Growth is being supported by older equipment fleets, wider precision retrofits, better repair access, and expanding installed bases in Asia-Pacific, with the sector rising from USD 58.12 billion in 2026 to USD 77.91 billion by 2031 at a 6.04% CAGR.

Which component category leads revenue in 2025?

Engine components led with 28.4% share in 2025 because nearly every active machine needs recurring engine-related maintenance, filters, cooling parts, and fuel-system servicing.

Which category is growing the fastest?

Electrical and electronic components are growing the fastest at an 8.1% CAGR through 2031 as sensors, telematics units, displays, and control modules become more common on retrofit-ready fleets.

Which equipment platform contributes the most revenue?

Tractors contributed 41.7% of 2025 revenue because they remain the most widely used platform across mature farm systems and developing mechanization bases.

Page last updated on: