Cotton Harvesting Machinery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

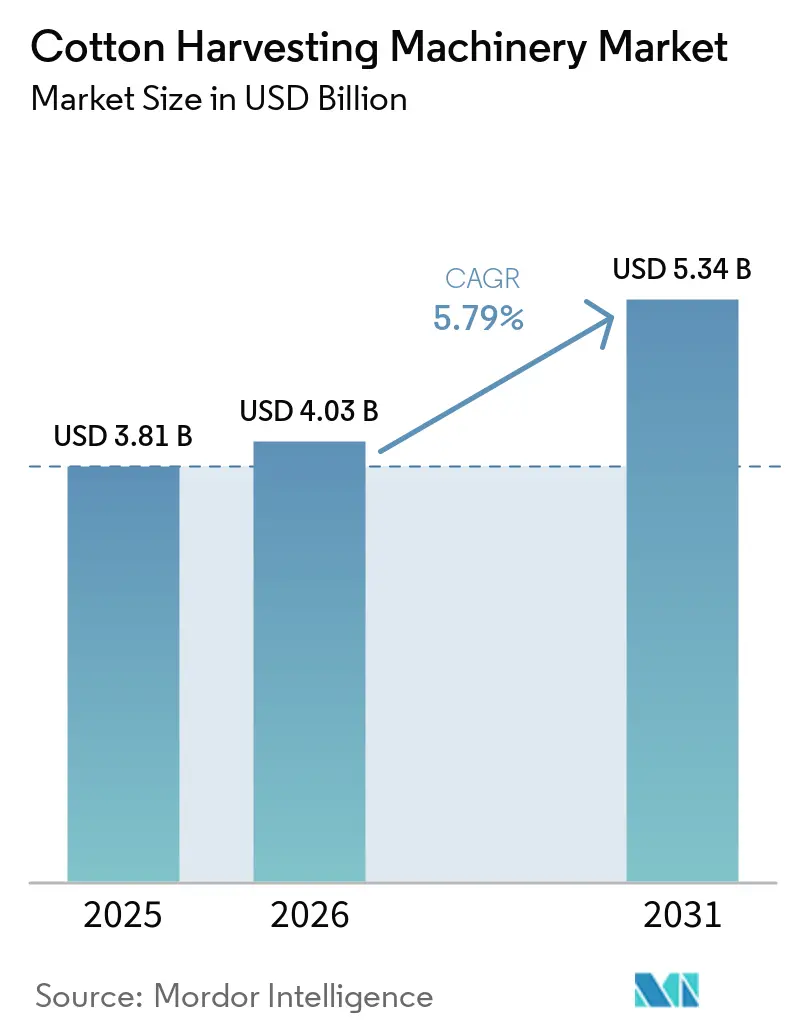

| Market Size (2026) | USD 4.03 Billion |

| Market Size (2031) | USD 5.34 Billion |

| Growth Rate (2026 - 2031) | 5.79% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cotton Harvesting Machinery Market Analysis by Mordor Intelligence

The cotton harvester market size is projected to grow from USD 3.81 billion in 2025 and USD 4.03 billion in 2026 to USD 5.34 billion by 2031, registering a CAGR of 5.79% between 2026 and 2031. Rising labor shortages, expanding subsidy programs in China and India, and embedded precision-agriculture features are pushing growers to mechanize faster, especially in dryland zones, where once-over harvests reduce field passes. Integrated round-bale module builders that eliminate separate baling steps are lowering logistics costs by about USD 22 per acre and shortening the payback window for premium machines. Meanwhile, series-hybrid powertrains that cut fuel use by 45% are positioning electric-leaning platforms for markets in China, the European Union, and California that are constrained by emissions. Competitive intensity remains moderate because the top five players hold a significant share, yet service-network gaps in Africa and Asia-Pacific leave white space for asset-light harvesting-as-a-service models, supporting greater adoption of flexible mechanization solutions across emerging cotton-producing regions.

Key Report Takeaways

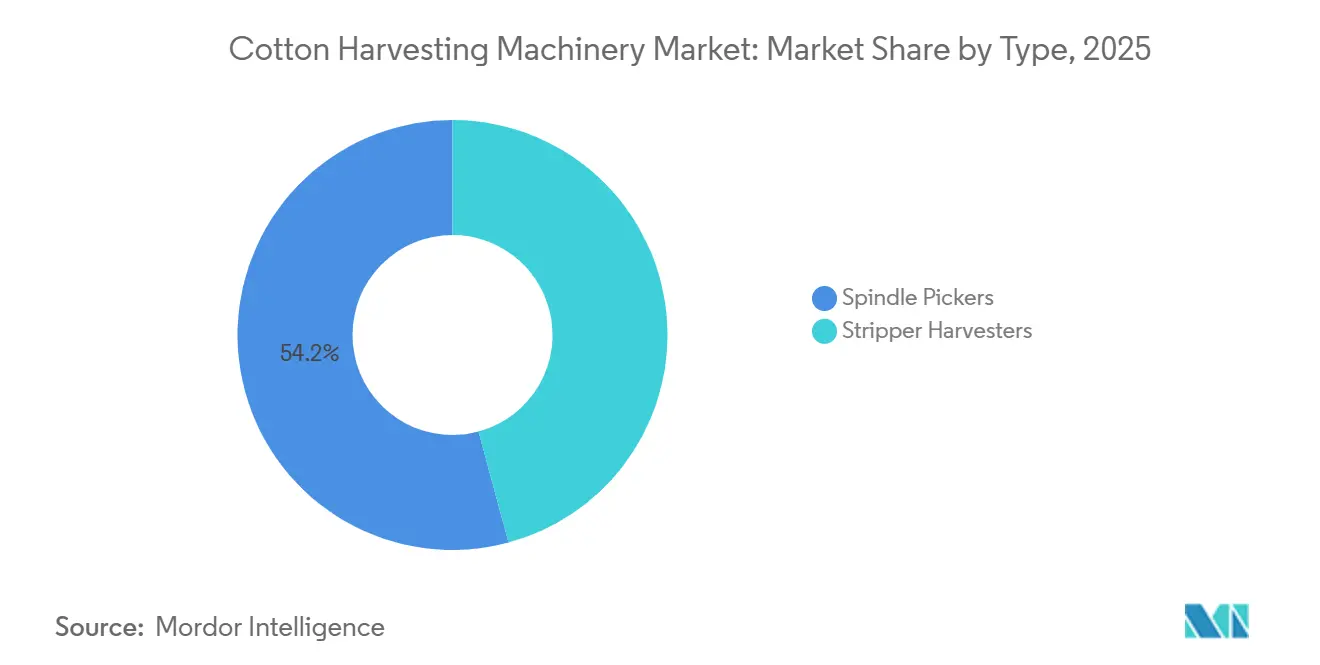

- By type, spindle pickers led with 54.2% of the cotton harvester market share in 2025. Stripper harvesters are forecast to expand at a 6.4% CAGR through 2031, the fastest among types.

- By mechanism, self-propelled machines held 62.5% share of the cotton harvester market size in 2025. Tractor-mounted units are projected to post the fastest growth, with a 7.2% CAGR through 2031.

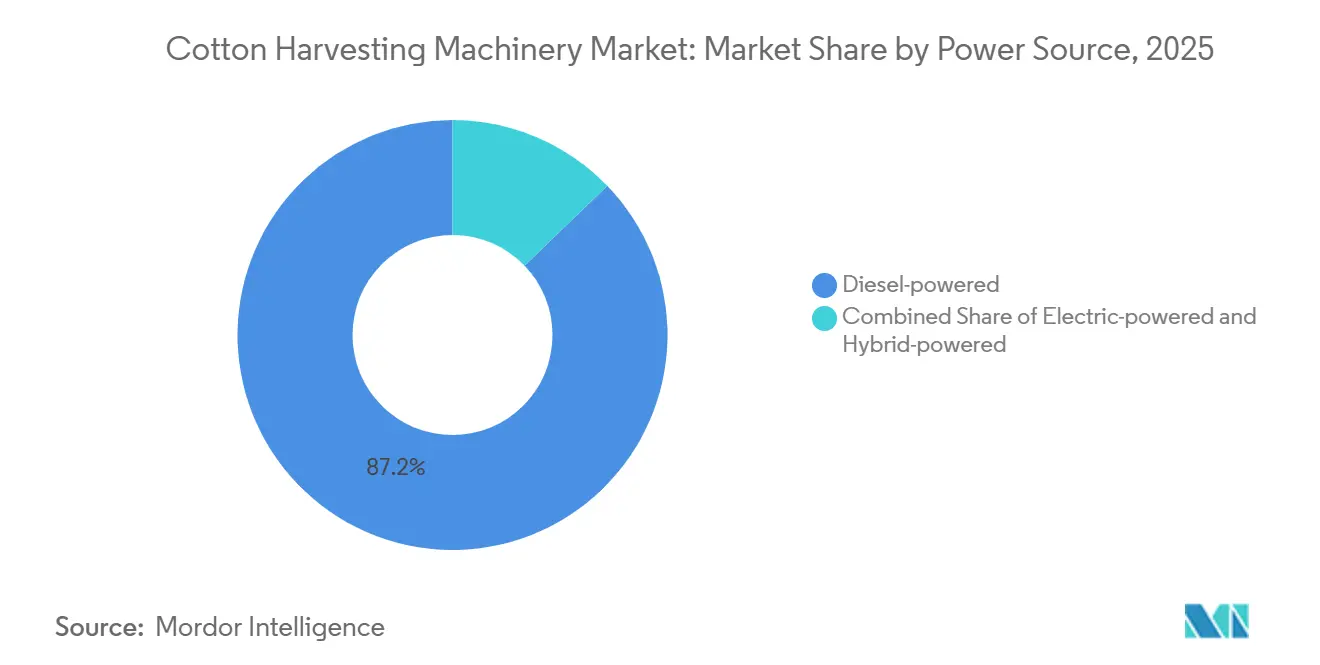

- By power source, diesel-powered models accounted for 87.2% of the cotton harvester market in 2025. Electric-powered variants are set to register the highest 11.3% CAGR through 2031.

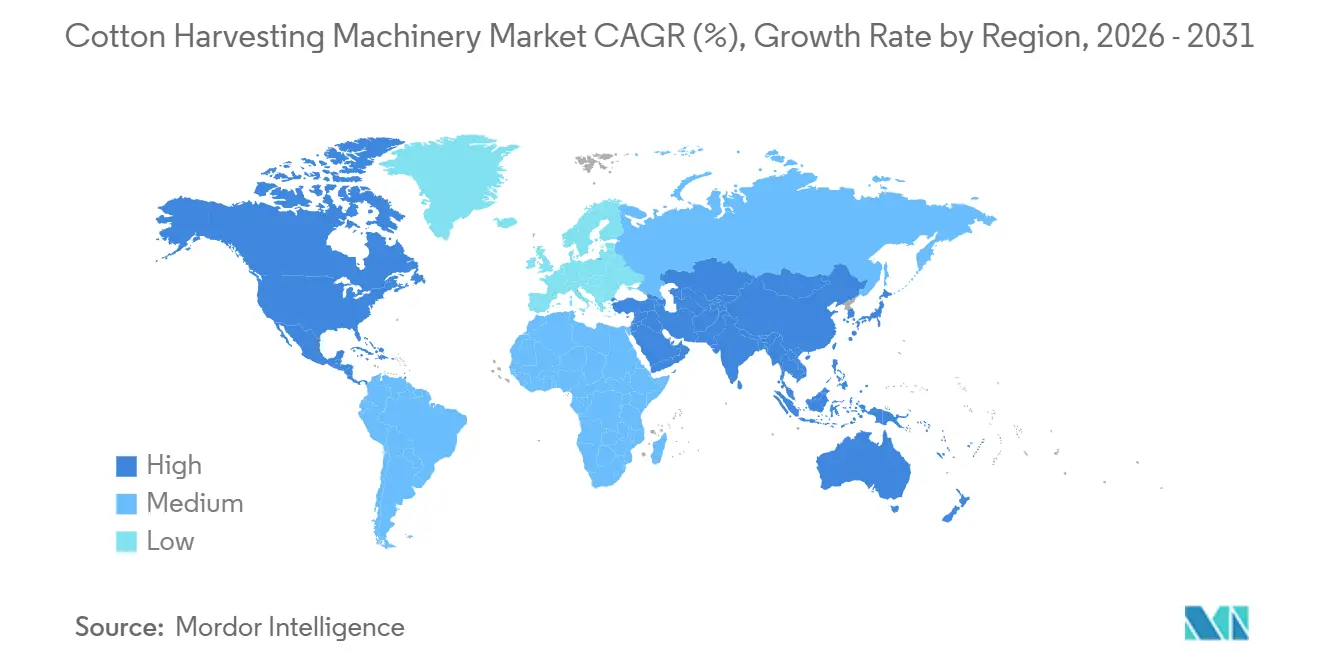

- By geography, North America accounted for 36.8% of the cotton harvester market's 2025 revenue. Asia-Pacific is anticipated to record the strongest regional growth, with a 8.3% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cotton Harvesting Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating farm-labor shortages and wage inflation | +1.20% | North America, Europe, Asia-Pacific core regions | Medium term (2-4 years) |

| Rapid adoption of automation, artificial intelligence, and GPS-guided precision harvesting | +1.00% | Global, with early concentration in North America and China | Short term (≤ 2 years) |

| Government subsidy programs accelerating mechanization in China, India, and the United States | +0.90% | Asia-Pacific (China, India), North America (United States) | Short term (≤ 2 years) |

| Rising global cotton consumption and acreage expansion | +0.80% | Global, led by South America (Brazil), Asia-Pacific (India, Australia) | Long term (≥ 4 years) |

| Proliferation of on-board round-bale module builders that cut logistics costs | +0.70% | North America, South America, and Australia | Medium term (2-4 years) |

| Emergence of pay-per-use harvesting-as-a-service platforms in developing markets | +0.60% | Africa, and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Farm-Labor Shortages and Wage Inflation

Cotton-picking labor pools shrank significantly across leading producing regions between 2021 and 2025, pushing growers toward mechanized solutions. The United States H-2A program certified more than 398,258 positions in fiscal 2025[1]Source: American Farm Bureau Federation, “H-2A Program Use Continues to Soar,” fb.org, yet seasonal labor shortages persisted in major agricultural states. Rising Adverse Effect Wage Rates, including increases in California, are strengthening the economic case for large-scale mechanized cotton harvesting. China’s Xinjiang region experienced rural-to-urban migration, reducing the availability of cotton pickers and accelerating the adoption of mechanization across the region. In India, government support programs have increased subsidies for agricultural machinery in labor-deficit states where manual harvesting costs remain high. Australia also faced shortages of seasonal agricultural labor, prompting growers in key cotton-producing valleys to lease additional harvesters rather than expand manual crews. Together, these labor and wage pressures are shortening the payback period for mechanized harvesting and sustaining demand for cotton-harvesting equipment.

Rapid Adoption of Automation, Artificial Intelligence, and GPS-Guided Precision Harvesting

Cotton harvesters are evolving into connected, precision-agriculture platforms designed to enhance traceability, operational efficiency, and fiber-quality management. At the Consumer Electronics Show 2024, John Deere showcased automated cotton harvesting technologies integrated with the CP770 cotton picker, enabling real-time monitoring of module production, moisture, weight, GPS location, and harvest data. The system supports digital data sharing across cotton harvesting and gin-management workflows. These advanced harvesting capabilities enable growers to optimize harvesting decisions, minimize manual processes, and improve cotton traceability from the field to end use[2]Source: Hello Tractor, "Powering Africa’s Transformation", 2025, hellotractor.com. Meanwhile, manufacturers are integrating advanced satellite-guided auto-steering technologies into cotton harvesters to enhance field precision and operational efficiency at lower implementation costs compared to imported navigation systems. These technological advancements are delivering immediate operational benefits, encouraging growers in major cotton-producing countries such as the United States, China, and Australia to accelerate equipment upgrades despite fluctuations in cotton prices.

Government Subsidy Programs Accelerating Mechanization in China, India, and the United States

Public incentives are compressing payback periods for new equipment across major cotton-producing countries. In China, government support programs continue to prioritize mechanization in Xinjiang, which accounts for the majority of the country’s cotton production. China continues to prioritize mechanization in Xinjiang, the country’s main cotton-producing region. Cotton-related subsidy programs for the 2024/25 season are estimated at roughly USD 2.4 billion, indirectly supporting continued investment in large-scale mechanized harvesting. India’s Cotton Productivity Mission is supporting the adoption of cotton-harvesting machinery through capital subsidy programs to increase mechanization across states with low equipment penetration. Collectively, these policy initiatives are advancing mechanization adoption, accelerating near-term equipment purchases, and strengthening revenue visibility for agricultural machinery manufacturers.

Rising Global Cotton Consumption and Acreage Expansion

World cotton production reached 25.9 million metric tons in 2025, slightly exceeding consumption at 25.2 million metric tons[3]Source: International Cotton Advisory Committee (ICAC), "ICAC", icac.org. Planted area expanded across major cotton-producing countries, led by gains in Brazil, where double-cropping with soybeans improved land returns. Australia’s sown area increased following improved water availability and irrigation conditions. India continues to rely heavily on manual harvesting across smallholder farms, signaling latent demand for compact cotton pickers. China’s highly mechanized cotton sector is generating replacement demand as earlier-generation harvesting machines age out. The growing global cotton trade and rising fiber demand continue to support the long-term need for faster, cleaner, and more fuel-efficient cotton-harvesting equipment worldwide.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront purchase and life-cycle maintenance costs | -0.80% | Global, acute in Asia-Pacific, Africa, and South America | Medium term (2-4 years) |

| Cotton-price volatility delaying capital-equipment spending | -0.60% | Global, with heightened sensitivity in export-dependent regions | Short term (≤ 2 years) |

| Sparse dealer telematics infrastructure hindering predictive-maintenance adoption in emerging regions | -0.50% | Africa, Asia-Pacific, parts of South America | Long term (≥ 4 years) |

| Stricter soil-compaction and emission regulations raising redesign and compliance expenses | -0.50% | Europe, California, and Australia | Medium term (2-4 years |

| Source: Mordor Intelligence | |||

High Upfront Purchase and Life-Cycle Maintenance Costs

A six-row spindle picker is typically priced at premium levels, reflecting its advanced automation, large-scale harvesting efficiency, and high operational capacity, equal to 15–20 years of net income for a 10-hectare farm in Gujarat or Kaduna. Annual upkeep includes spindle replacement, hydraulic rebuilds, and telematics fees. Even with subsidies, growers still face significant financing requirements that exceed typical rural credit ceilings. In Africa, limited access to affordable financing and high interest rates constrain adoption despite rising labor costs. Brazilian mid-sized farms face high equipment costs that absorb a large share of annual revenue. Specialty financiers carry residual-value risk, limiting lease offerings where acreage fluctuates significantly year to year. Until capital costs fall or flexible financing models expand, high entry prices will continue to restrict penetration in smallholder regions.

Cotton-Price Volatility Delaying Capital-Equipment Spending

The Cotlook A Index declined significantly, reducing gross margins per hectare and prompting growers in key regions such as Texas and Mato Grosso to postpone equipment orders. China’s quota system provides insulation for domestic production but imposes high out-of-quota tariffs, creating pricing volatility and delaying equipment purchases in 2025. India’s minimum support price revisions have not fully offset rising fertilizer, labor, and irrigation costs, putting pressure on grower profitability and reducing demand for capital-intensive harvesting machinery. Australian growers, heavily reliant on export markets, have experienced softer cotton prices due to elevated global inventories, leading to more cautious investment decisions[4]Source: United States Department of Agriculture Foreign Agricultural Service, "Cotton and Products Annual: Australia, Report No. AS2024-0006", 2024, apps.fas.usda.gov. In Turkey, currency volatility and slower demand in the textile sector have curbed mechanization spending in several cotton-producing regions. Commodity price fluctuations are extending payback periods and increasing lender caution, delaying equipment purchase cycles until market conditions stabilize. As volatility continues, growers are increasingly expected to transition from ownership models to renting or leasing agricultural machinery.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Stripper Gains Share in Dryland Zones

Spindle pickers accounted for 54.2% of the cotton harvester market share in 2025, reflecting their dominance in premium-grade upland and long-staple production. Stripper harvesters ranked second-largest, favored in once-over dryland operations across Texas, Oklahoma, and Australia. Their widespread adoption is driven by lower contamination rates, higher fiber retention efficiency, and compatibility with large-scale mechanized harvesting operations.

Stripper harvesters are projected to register the quickest 6.4% CAGR between 2026 and 2031 as dryland acreage expands in the United States and Brazil, while spindle units are set to advance more modestly over the same span. Fuel savings of 18% on once-over passes, a 20% speed gain on Deere’s CS770, and rising cultivar tolerance for aggressive stripping methods all support the lead growth rate. Replacement demand in China and Turkey will still sustain spindle sales, as stringent fiber-quality penalties remain. The combined effect leaves the cotton harvester market size more balanced by 2031, without dislodging spindle leadership. Rising investments in mechanization and continuous advancements in harvesting technology are anticipated to further drive demand in both developed and emerging cotton markets.

By Mechanism: Tractor-Mounted Units Unlock Smallholder Access

Self-propelled machines accounted for 62.5% of the cotton harvester market share in 2025, driven by their productivity of 1.2–1.8 hectares per hour and by factory-installed module builders, which large farms in North America and Australia highly value. Their ability to reduce field losses, optimize harvesting speed, and support precision-guided operations further strengthens adoption across technologically advanced cotton-producing regions. Advanced telematics integration and automated bale-handling systems are enhancing operational efficiency and minimizing labor dependency during peak harvest periods.

Tractor-mounted pickers are forecast to log a 7.2% CAGR through 2031, the highest within this segmentation, driven by capital-light cooperative models in India, Asia-Pacific, and Africa. Self-propelled platforms are estimated to grow more slowly but steadily as integrated precision packages drive replacement cycles in mature markets. Export programs from Changzhou Dongfeng and subsidies in Turkey further boost tractor-mounted momentum. The increasing availability of affordable financing solutions and localized manufacturing partnerships is further encouraging adoption among medium-scale cotton producers globally.

By Power Source: Electric Hybrids Gain Traction in Emission-Constrained Zones

Diesel-powered models dominated the cotton harvester market with 87.2% market share in 2025, owing to established fuel infrastructure and proven reliability. Their reliable field performance, extended operating hours, and extensive service network availability continue to drive adoption in large-scale commercial cotton farming operations worldwide, particularly in emerging agricultural economies focused on mechanization.

Electric-powered and series-hybrid variants are estimated to post the fastest 11.3% CAGR between 2026 and 2031 as Yuchai’s IE-Power system cuts fuel use 45% and meets China Stage IV particulate rules. Diesel units will still expand, though at a reduced pace, through 2031, driven by Tier 4 Final optimizations that deliver up to 15% efficiency gains. Hybrid price premiums of 18-22% are being offset by tax credits in Germany and France, while module-equipped diesel pickers remain the default choice in Brazil and India, where emission enforcement is lighter. The cotton harvester market will therefore evolve toward a dual-fuel landscape, with hybrids occupying compliance-driven niches. Increased investments in sustainable farm mechanization, emission-reduction goals, and improvements in battery efficiency are expected to further accelerate the commercialization of hybrid harvesters in developed agricultural markets.

Geography Analysis

North America generated 36.8% of 2025 revenue, and the region is projected to grow at a steady pace driven by rising farm-labor costs and increasing adoption of mechanized and precision agriculture practices. Leading equipment manufacturers continue to strengthen their presence through advanced technology integration and automation capabilities, supporting ongoing replacement and upgrade demand even during periods of cotton price softness.

Asia-Pacific is forecast to record the fastest 8.3% CAGR through 2031, supported by government subsidies and productivity improvement programs that reduce payback periods for mechanized harvesting equipment. High mechanization levels in China are generating steady replacement demand, while Australia continues to demonstrate strong adoption of advanced harvesting systems. In India, compact and affordable picker development is estimated to unlock adoption in smallholder farms that currently rely on manual harvesting, significantly expanding the addressable market across fragmented landholding structures.

South America is projected to advance steadily, led by Brazil where expanding cotton acreage and mechanization are supporting equipment demand, while credit programs are steering adoption toward more affordable machinery options. Argentina’s import-related constraints and currency volatility continue to influence purchasing behavior. Europe holds a smaller share of revenue, with regulatory compliance requirements and higher operational costs limiting new equipment adoption despite underlying acreage expansion in select regions. The Middle East and Africa together account for a modest share, where policy support is improving mechanization in some markets, but limited financing access and weak service infrastructure continue to restrict large-scale adoption in several sub-Saharan regions.

Competitive Landscape

The competitive landscape is moderately concentrated, with leading suppliers accounting for a majority of global revenue. Deere maintains market leadership through advanced module-building systems and AI-enabled harvesting technologies that improve operational efficiency and crop quality, while CNH Industrial follows with strong positioning in modular harvesting solutions and autonomous guidance technologies deployed across pilot-scale operations.

Chinese manufacturers, including Shandong Swan Cotton Industrial Machinery Stock Co., Ltd., Changzhou Dongfeng Agricultural Machinery Group Co., Ltd., and Xinjiang Boshiran Intelligent Agricultural Machinery Co., Ltd., collectively hold a significant share, supported by domestic subsidies and cost-competitive GNSS-enabled equipment. These players are expanding their presence in emerging cotton-producing regions where mechanization is increasing but service infrastructure remains limited. Emerging opportunities are also visible in service-based and rental models, where equipment utilization-as-a-service is gaining traction in capital-constrained regions.

Technology development is diverging between premium and cost-focused segments, with high-end manufacturers prioritizing automation, AI-driven quality control, and emissions-compliant drivetrains, while value-focused players emphasize affordability and simplified tractor-mounted solutions. Overall, sustained investment in innovation by leading companies, combined with supportive policy environments for domestic manufacturers, is estimated to drive gradual shifts in competitive positioning rather than abrupt market disruption.

Cotton Harvesting Machinery Industry Leaders

-

Deere & Company

-

CNH Industrial N.V.

-

Shandong Swan Cotton Industrial Machinery Stock Co., Ltd.

-

Changzhou Dongfeng Agricultural Machinery Group Co., Ltd.

-

Xinjiang Boshiran Intelligent Agricultural Machinery Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Deere & Company announced the expansion of its United States facilities in Kernersville, North Carolina, and Hebron, Indiana, strengthening manufacturing capacity, supply chain efficiency, and support for advanced agricultural and cotton-harvesting equipment.

- January 2026: CNH Industrial N.V. introduced advanced AI-enabled precision agriculture and automation technologies through its Case IH FieldOps platform, enhancing operational efficiency, machine intelligence, and smart harvesting capabilities across agricultural and cotton harvesting equipment applications.

- June 2025: CNH Industrial N.V. subsidiary New Holland Agriculture introduced upgraded harvester and header technologies for its 2026 equipment lineup, enhancing harvesting productivity, reducing fuel consumption, and strengthening operational efficiency across advanced agricultural and cotton harvesting machinery applications.

Global Cotton Harvesting Machinery Market Report Scope

Cotton harvesting machinery comprises specialized agricultural equipment designed to harvest cotton crops from fields. These machines efficiently pick or strip mature cotton bolls, facilitating faster harvesting, enhancing cotton collection efficiency, and reducing dependence on manual labor in cotton farming. The Cotton Harvesting Machinery Market Report is Segmented by Type (Spindle Pickers and Stripper Harvesters), by Mechanism (Self-Propelled and Tractor-Mounted), by Power Source (Diesel-Powered, Electric-Powered, and Hybrid-Powered), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Spindle Pickers |

| Stripper Harvesters |

| Self-propelled |

| Tractor-mounted |

| Diesel-powered |

| Electric-powered |

| Hybrid-powered |

| North America | United States |

| Canada | |

| Rest of the North America | |

| South America | Brazil |

| Argentina | |

| Rest of the South America | |

| Europe | Germany |

| Spain | |

| Greece | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Israel | |

| Rest of the Middle East | |

| Africa | Egypt |

| South Africa | |

| Rest of the Africa |

| By Type | Spindle Pickers | |

| Stripper Harvesters | ||

| By Mechanism | Self-propelled | |

| Tractor-mounted | ||

| By Power Source | Diesel-powered | |

| Electric-powered | ||

| Hybrid-powered | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of the North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of the South America | ||

| Europe | Germany | |

| Spain | ||

| Greece | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Israel | ||

| Rest of the Middle East | ||

| Africa | Egypt | |

| South Africa | ||

| Rest of the Africa | ||

Key Questions Answered in the Report

What is the current value of the global cotton harvester market?

The cotton harvester market size stands at USD 4.03 billion in 2026 and is set to reach USD 5.34 billion by 2031.

Which machine type leads global sales?

Spindle pickers command 54.2% of the cotton harvester market share in 2025, driven by their suitability for premium upland and long-staple fiber.

Which segment is growing the fastest?

Stripper harvesters are projected to rise at a 6.4% CAGR from 2026 to 2031 as dryland acreage expands in the United States, Brazil, and Australia.

Which region will add the most revenue through 2031?

Asia-Pacific is estimated to post the highest 8.3% CAGR, led by subsidy-backed mechanization in China and India.

Page last updated on: