Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

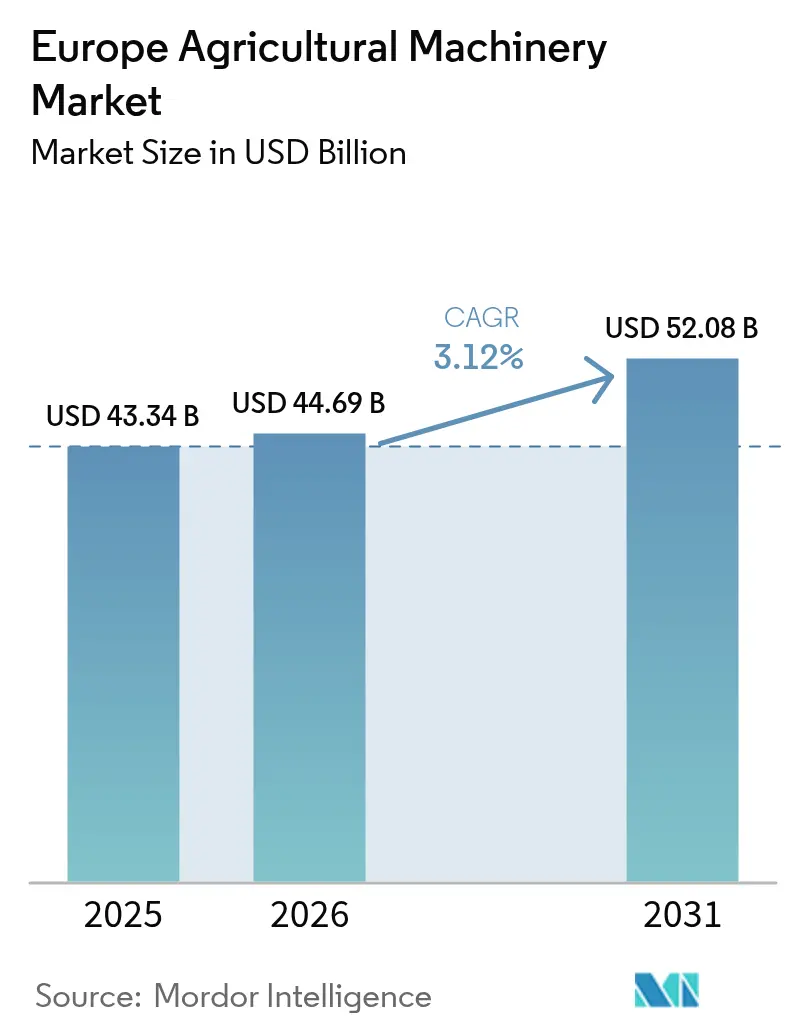

| Base Year Market Size (2025) | USD 43.34 Billion |

| Market Size (2026) | USD 44.69 Billion |

| Market Size (2031) | USD 52.08 Billion |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Agricultural Machinery Market Analysis by Mordor Intelligence

The Europe agricultural machinery market size in 2026 is estimated at USD 44.69 billion, growing from 2025 value of USD 43.34 billion with 2031 projections showing USD 52.08 billion, growing at 3.12% CAGR over 2026-2031. Tight farm-labor supply, stringent European Union environmental mandates, and widespread digitalization are reshaping capital‐spending priorities toward low-emission, sensor-rich equipment. Farmers are shifting from horsepower upgrades to intelligent systems that automate repetitive tasks, document sustainability performance, and integrate with enterprise software. Original Equipment Manufacturers (OEMs) are responding with modular platforms that accept continuous software and sensor retrofits, shortening model life cycles and expanding recurring-revenue streams. Rising semiconductor availability and falling battery costs from 2027 onward are anticipated to stabilize delivery schedules and accelerate electrification, closing the gap between early-adopter and late-adopter regions of the Europe agricultural machinery market.

Key Report Takeaways

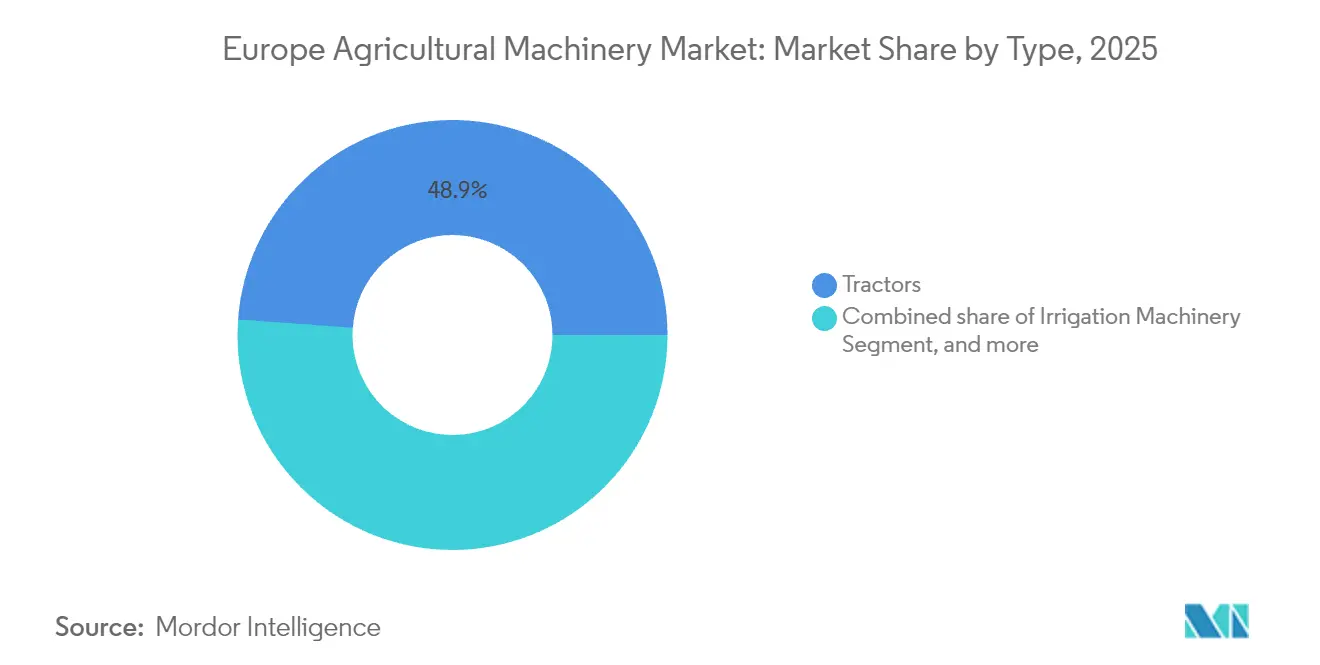

- By type, tractors captured 48.85% of the Europe agricultural machinery market share in 2025, while irrigation machinery is advancing at a 3.74% CAGR through 2031.

- By geography, Germany held 24.12% of the Europe agricultural machinery market size in 2025, and the United Kingdom is expanding at the fastest 5.12% CAGR to 2031.

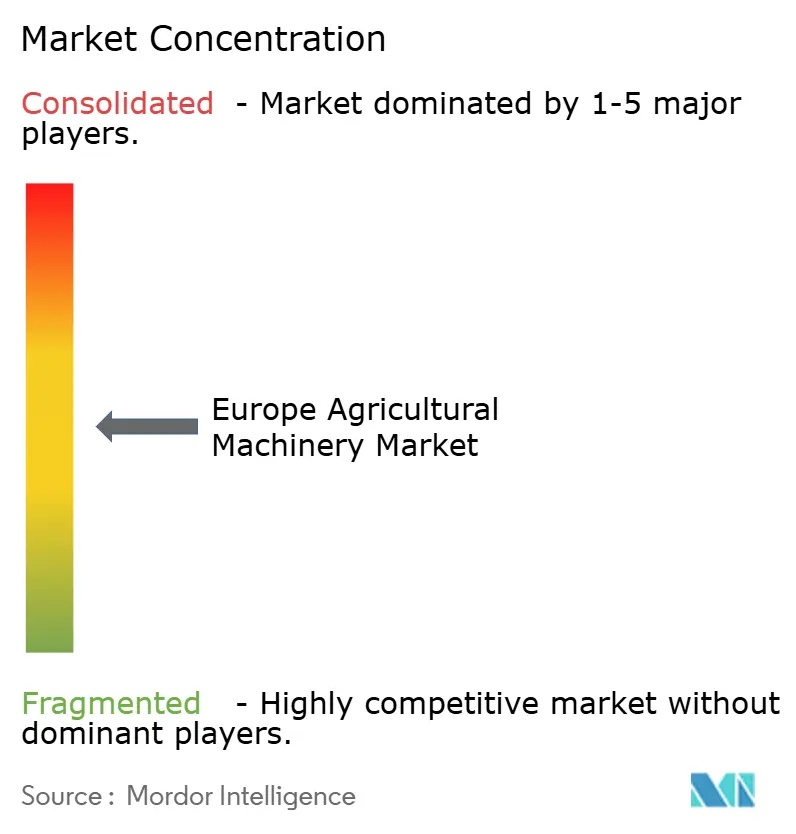

- The Europe agricultural machinery market is moderately concentrated. Deere & Company, CNH Industrial N.V., AGCO Corporation, CLAAS KGaA mbH, and Kubota Corporation anchor the top tier, leveraging scale to fund multimillion-dollar software roadmaps.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Agricultural Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic farm-labor shortage | +0.8% | Germany, France, Netherlands, and Eastern Europe spillovers | Medium term (2-4 years) |

| European Union and national subsidies are accelerating mechanization | +0.6% | European Union-27 core with emphasis in Germany, France, and Italy | Short term (≤ 2 years) |

| Rapid model upgrades in agricultural machinery | +0.5% | Germany, United Kingdom, and Scandinavia | Medium term (2-4 years) |

| High adoption of telematics and predictive maintenance | +0.4% | Western Europe core, Central and Eastern Europe expansion | Long term (≥ 4 years) |

| Eco-scheme incentives for low-emission machinery | +0.3% | Germany, France, the Netherlands, within the European Union-27 | Long term (≥ 4 years) |

| OEM ag-software hardware-bundle financing | +0.2% | United Kingdom, Germany, and France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

European Union and National Subsidies are Accelerating Mechanization

The European Investment Bank’s EUR 1 billion (USD 1.05 billion) sustainability-linked agtech loan window covers up to 70% of equipment list prices for emissions-verified purchases. When stacked with Germany’s federal 20% machinery grant, net acquisition costs for Stage V tractors drop to parity with legacy Tier III units, flattening payback curves for conservative buyers. France and Italy deploy similar top-up schemes, ensuring that subsidy budgets are front-loaded into the 2025-2027 window, which drives a spike in advance orders. OEMs are synchronizing product-launch calendars with grant-application deadlines to maximize uptake. Leasing companies are extending contracts to seven years to align with subsidy claw-back periods, lowering annual cash footprints and fostering premature retirement of sub-40-horsepower fleets.

Rapid Model Upgrades in Agricultural Machinery

Average release cycles for mainstream tractor lines have compressed from six years to fewer than two, propelled by emission revisions and the influx of digital subsystems. Deere & Company’s 2025 autonomous tractors debuted new LiDAR arrays and over-the-air firmware that optimize path planning without hardware swaps. Farmers now view machinery as an evolving platform, with 47% of German survey respondents plan to upgrade software quarterly to capture agronomic gains. The speed of iteration pushes dealers to invest in advanced service tools. Manufacturers in the Europe agricultural machinery market are pivoting to subscription pricing for feature unlocks, diversifying revenue beyond unit sales.

High Adoption of Telematics and Predictive Maintenance

Telematics penetration is forecast to rise in the coming years as asset utilization data proves its value in audited sustainability reporting. Kubota Connect can forecast hydraulic-pump failures three weeks in advance, eliminating unplanned downtime during peak periods. Cooperatives in Normandy logged 9% diesel savings by coaching operators on optimal PTO load ranges, capturing both cost and carbon reductions that qualify for eco-scheme bonuses. Proemion’s cloud dashboards also auto-populate EU logbooks, easing regulatory paperwork. As insurers increasingly require telematics evidence to underwrite multi-million-dollar harvesters, connectivity is becoming mandatory on new purchases across the European agricultural machinery market.

Eco-Scheme Incentives for Low-Emission Machinery

The Common Agricultural Policy earmarks EUR 8 billion (USD 8.4 billion) each year for eco-schemes, and 42% of approved farm plans in 2024 included machinery upgrades that cut particulate matter by at least 30%. Electric tractors gained traction when subsidy calculators began awarding higher points for zero-tailpipe equipment. Monarch’s battery-electric tractor shipped its first European units in 2024, pairing autonomous operation with carbon-credit verification that generates monetizable offsets. OEM pipelines indicate nine battery-electric or hybrid series launches by 2027, supported by field-swappable packs sized for eight-hour shifts. Farmers adopting electric powertrains also circumvent Stage V diesel filter maintenance, a pain point cited by 68% of survey respondents in Spain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront and maintenance costs | –0.7% | Europe-wide, most acute in Eastern Europe and small farms | Short term (≤ 2 years) |

| Cybersecurity risks in connected equipment | –0.4% | Western Europe leadership, expanding with telematics rise | Medium term (2-4 years) |

| Semiconductor supply constraints | –0.3% | Global shortage hitting high-tech machinery | Short term (≤ 2 years) |

| Diesel-emission compliance cost escalation | –0.2% | European Union-27 with staggered national rollouts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront and Maintenance Costs

List prices for sensor-rich combines and autonomous sprayers jumped 18% between 2024 and 2025, pushing some configurations beyond USD 1 million per unit. Mid-sized growers operating 200-400 hectares face difficult trade-offs between machinery and land-improvement projects, especially in Eastern Europe where average net margins hover near 7%. Maintenance expenses have also climbed as proprietary electronics require dealer intervention. Hourly service rates in France now average EUR 105 (USD 110) compared with EUR 68 (USD 71) in 2020. Smaller farms mitigate costs by forming machinery rings, but coordination overhead can erode efficiency gains.

Cybersecurity Risks in Connected Equipment

As machines integrate guidance, telemetry, and cloud analytics, cyberattack vectors multiply. A 2024 ransomware incident in Northern Italy locked an entire fleet of seed drills until the grower paid EUR 42,000 (USD 44,100), resulting in missed planting windows. Insurers are tightening underwriting standards, adding 2-3% to equipment operating expenses for cyber coverage. While OEMs have begun over-the-air patching, 37% of surveyed farms still rely on factory default passwords, amplifying vulnerability across the Europe agricultural machinery market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Tractors Dominate Despite Precision Shift

Tractors maintain commanding market leadership with a 48.85% share in 2025, reflecting their fundamental role as the primary power source for most European farming operations. Within the tractor category, the 100-150 HP segment captures the largest share among European farms that average 65 hectares, while the greater than 150 HP segment experiences the fastest growth as large-scale operations pursue efficiency through higher-capacity equipment. Plowing and cultivating equipment represents the second-largest category, with cultivators and tillers showing particular strength as conservation tillage practices gain adoption across the continent. The financial grant of Euro 430 million (USD 455 million) by the European Commission for the farmers opting for high-cost inputs in 2023, including agricultural equipment such as plows, is also one of the major factors increasing the adoption rates.

Irrigation machinery emerges as the fastest-growing segment at 3.74% CAGR, driven by increasingly erratic precipitation patterns and water usage regulations that mandate efficiency improvements. Drip irrigation systems lead this expansion as they deliver 40-60% water savings compared to traditional sprinkler systems while enabling precise nutrient delivery that enhances crop yields. Harvesting machinery maintains steady demand with combine harvesters dominating the category, though smart and autonomous harvesters represent the highest-growth subsegment as labor shortages intensify during critical harvest windows. Haying and forage machinery serves the substantial European dairy sector, with balers experiencing particular demand as farmers optimize feed production efficiency. The "Other Types" category, including drones and precision seeders, shows explosive growth from a small base as farmers experiment with emerging technologies that promise operational advantages over conventional approaches.

Geography Analysis

Germany contributed 24.12% to the European agricultural machinery market size in 2025, stemming from the confluence of industrial capability, structured subsidy pipelines, and a technologically receptive producer base. The nation’s average 60-hectare farm scale is large enough to leverage advanced equipment yet small enough to require versatility, nudging OEMs toward modular architecture. Beyond equipment sales, Germany houses 40% of Europe’s agricultural robotics start-ups, feeding a local innovation ecosystem that accelerates proof-of-concept trials. Telematics utilization exceeded 45% in 2024, compared with a continental average of 35%, illustrating rapid digital convergence. Still, macroeconomic uncertainty in early 2025 curbed new-tractor registrations, spotlighting sensitivity to commodity swings even in a technology-forward setting.

France and Italy illustrate mature yet divergent demand structures. Cereal plains in northern France favor 14-meter header combines capable of 100-hectare daily throughput, while specialty vineyards in the south deploy tracked harvesters that protect root zones. Financial incentives under FranceAgriMer prioritize emission reductions, leading to a surge in Stage V engine retrofits. Italy’s fragmented holdings require narrow-chassis tractors, with 62% of 2025 tractor sales fall below 110 horsepower. Lombardy dairy operators pilot autonomous feeding robots that free labor for higher value tasks, portraying country-specific innovation pathways within the Europe agricultural machinery market.

The United Kingdom posts the fastest 5.12% CAGR through 2031. After Brexit severed CAP inflows, London introduced productivity grants covering up to 50% of precision seeding and robotic weeding equipment costs. Wales channels innovation grants into pasture-mapping drones to enhance grassland efficiency. Alongside policy carrots, a shortage of seasonal labor from Eastern Europe pushes horticulture growers toward autonomous harvest assistants. Currency fluctuation initially inflated imported equipment prices, but domestic manufacturers of small electric tractors emerged, insulating buyers from exchange shocks.

Competitive Landscape

The Europe agricultural machinery market is moderately concentrated. Deere & Company, CNH Industrial N.V., AGCO Corporation, CLAAS KGaA mbH, and Kubota Corporation anchor the top tier, leveraging scale to fund multimillion-dollar software roadmaps. CLAAS KGaA mbH integrates machine data into 365FarmNet, providing end-to-end crop planning tools that differentiate beyond pure hardware. AGCO Corporation and SDF Group’s 2025 supply agreement for low-mid horsepower tractors pools component sourcing, aiding competitive pricing for growth regions in Central and Eastern Europe.[3]AGCO Corporation, “AGCO and SDF Strategic Agreement,” agcocorp.com

Regional challengers such as Kverneland AS and Lemken GmbH & Co. KG carve niches in seeding and tillage, often partnering with precision-software vendors to bundle agronomic algorithms. Start-ups focusing on specialty-crop robotics introduce disruptive pricing but lack service networks, prompting alliances with established dealers keen to diversify portfolios. Competitive intensity is shifting from mechanical prowess to data ownership. OEMs are lobbying Brussels for data-sharing frameworks that favor proprietary cloud platforms. In response, farmer cooperatives advocate open standards to prevent vendor lock-in, injecting policy risk into strategic planning across the European agricultural machinery market.

Capital commitments underscore the pivot to service differentiation. AGCO Corporation’s EUR 87 million (USD 91.35 million) French parts hub reduces 24-hour delivery radius to 95% of Western European dealerships, ensuring uptime guarantees that justify premium service contracts. Kubota Corporation positions itself through zero-interest financing to capture loyalty among cost-sensitive segments. Deere & Company showcases its CES-launched autonomous fleet annually, signaling first-mover advantage in driverless field operations. As margins tighten on metal, recurring revenue from software, telematics, and extended warranties will separate winners from laggards.

Europe Agricultural Machinery Industry Leaders

Deere & Company

AGCO Corporation

CNH Industrial N.V.

SDF S.p.A

CLAAS KGaA mbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: AGCO Corporation and SDF Group entered a strategic supply agreement to produce low-mid horsepower tractors for Massey Ferguson starting mid-2025, providing streamlined portfolios and economies of scale.

- January 2025: Deere & Company introduced autonomous agricultural machines at CES 2025 that incorporate computer vision and machine learning capabilities for continuous operation. The company launched these machines in Europe alongside other regions.

- October 2024: Case IH unveiled its AF10 combine harvester and enhanced Farmall C tractors at EIMA International 2024 in Bologna, Italy. The new models feature improved hydraulic systems, updated designs, and advanced precision farming capabilities to increase operational efficiency for farms of different sizes.

Europe Agricultural Machinery Market Report Scope

Agricultural machinery is used to perform farming operations such as harvesting, plowing, irrigation, and planting. For the purpose of this report, machinery used in agricultural operations has been considered. The report does not cover machinery used for industrial and construction purposes or multi-purpose tractors, machinery, and equipment used for farming and non-agricultural operations.

The European agricultural machinery market is segmented by type (Less than 50 HP, 50-100 HP, 100-150 HP, and >150 HP), plowing and cultivating machinery (plows, harrows, cultivators and tillers, and other equipment), harvesting machinery (combine harvesters, forage harvesters, and other harvesting equipment), irrigation machinery (sprinkler irrigation, drip Irrigation, and other irrigation machinery) haying and forage machinery (mowers, balers, and other haying and forage machinery) and other types and geography (Germany, Italy, United Kingdom, France, Spain, Russia, and the Rest of Europe). The report offers market size and forecast in terms of value in USD for the above segments.

By Type

| Tractor | Less than 50 HP |

| 50 to 100 HP | |

| 100 to 150 HP | |

| More than 150 HP | |

| Plowing and Cultivating Equipment | Plows |

| Harrows | |

| Cultivators and Tillers | |

| Other Equipment (Ridger, Rotary tillers, etc.) | |

| Irrigation Machinery | Sprinkler |

| Drip | |

| Other Irrigation Machinery (Micro-irrigation, Pivot irrigation, etc.) | |

| Harvesting Machinery | Combine Harvesters |

| Forage Harvesters | |

| Smart/Autonomous Harvesters | |

| Haying and Forage Machinery | Mowers |

| Balers | |

| Other Haying Equipment (Rakes, Tedders, etc.) | |

| Other Types (Drones, Precision Seeders) |

By Geography

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Type | Tractor | Less than 50 HP |

| 50 to 100 HP | ||

| 100 to 150 HP | ||

| More than 150 HP | ||

| Plowing and Cultivating Equipment | Plows | |

| Harrows | ||

| Cultivators and Tillers | ||

| Other Equipment (Ridger, Rotary tillers, etc.) | ||

| Irrigation Machinery | Sprinkler | |

| Drip | ||

| Other Irrigation Machinery (Micro-irrigation, Pivot irrigation, etc.) | ||

| Harvesting Machinery | Combine Harvesters | |

| Forage Harvesters | ||

| Smart/Autonomous Harvesters | ||

| Haying and Forage Machinery | Mowers | |

| Balers | ||

| Other Haying Equipment (Rakes, Tedders, etc.) | ||

| Other Types (Drones, Precision Seeders) | ||

| By Geography | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the Europe agricultural machinery market in 2026?

The market is valued at USD 44.69 billion in 2026.

What is the CAGR for European farm machinery through 2031?

It is forecast to grow at a 3.12% CAGR from 2026 to 2031.

Which equipment type commands the highest revenue share?

Tractors lead with 48.85% share of 2025 value.

Which country is expanding fastest?

The United Kingdom is advancing at a 5.12% CAGR through 2031.

Page last updated on: