Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

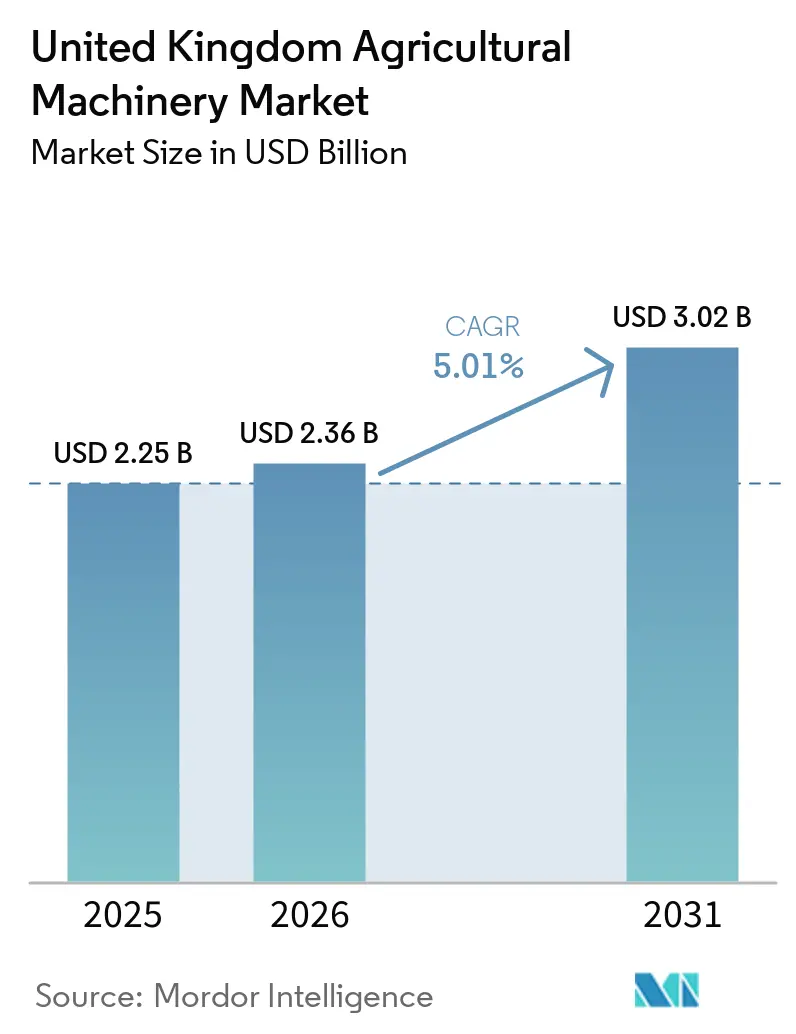

| Base Year Market Size (2025) | USD 2.25 Billion |

| Market Size (2026) | USD 2.36 Billion |

| Market Size (2031) | USD 3.02 Billion |

| Growth Rate (2026 - 2031) | 5.01% CAGR |

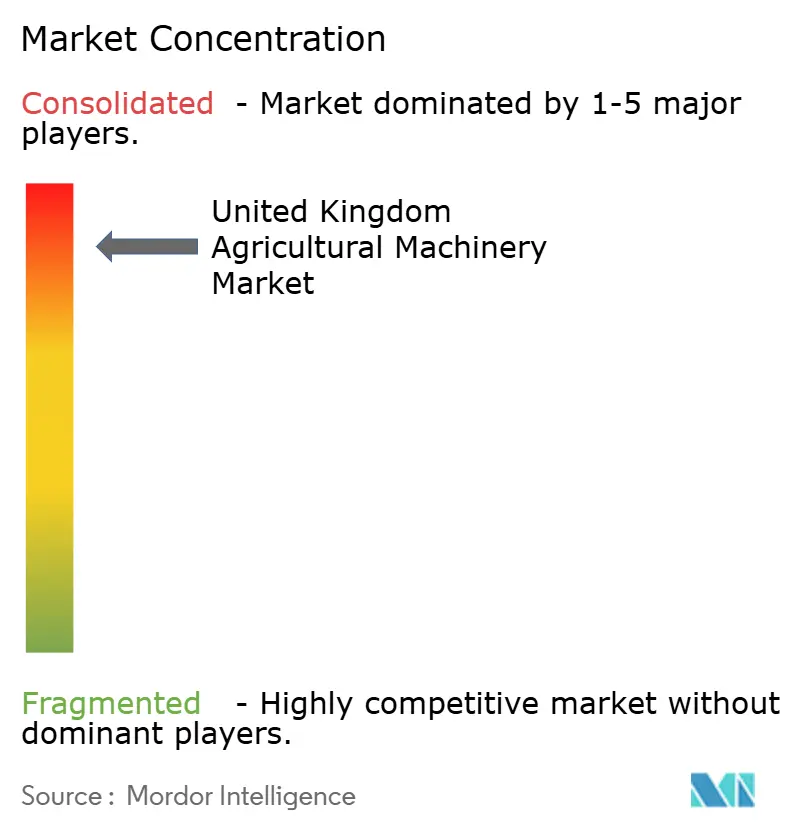

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Agricultural Machinery Market Analysis by Mordor Intelligence

The United Kingdom agricultural machinery market size was valued at USD 2.25 billion in 2025 and estimated to grow from USD 2.36 billion in 2026 to reach USD 3.02 billion by 2031, at a CAGR of 5.01% during the forecast period (2026-2031). This upward trajectory underscores the sector’s resilience amid post-Brexit regulation, persistent labor shortages, and accelerating on-farm automation. Over the next five years, equipment purchases will be buoyed by the Farming Equipment and Technology Fund, a GBP 50 million (USD 63 million) grant program that directly offsets capital costs for productivity-enhancing machinery.[1]Source: Department for Environment and Rural Affairs, “50 million Equipment and Technology Grants,” gov.uk Demand is also influenced by the Clean Power 2030 Action Plan, which channels investment toward low-emission electric and hydrogen tractors that help farms meet the national net-zero target for 2030. Meanwhile, the Expansion of agri-robotics testbeds, supported by the Smart Machines Strategy 2035, is fostering rapid prototype adoption and attracting technology partnerships across research clusters.

Key Report Takeaways

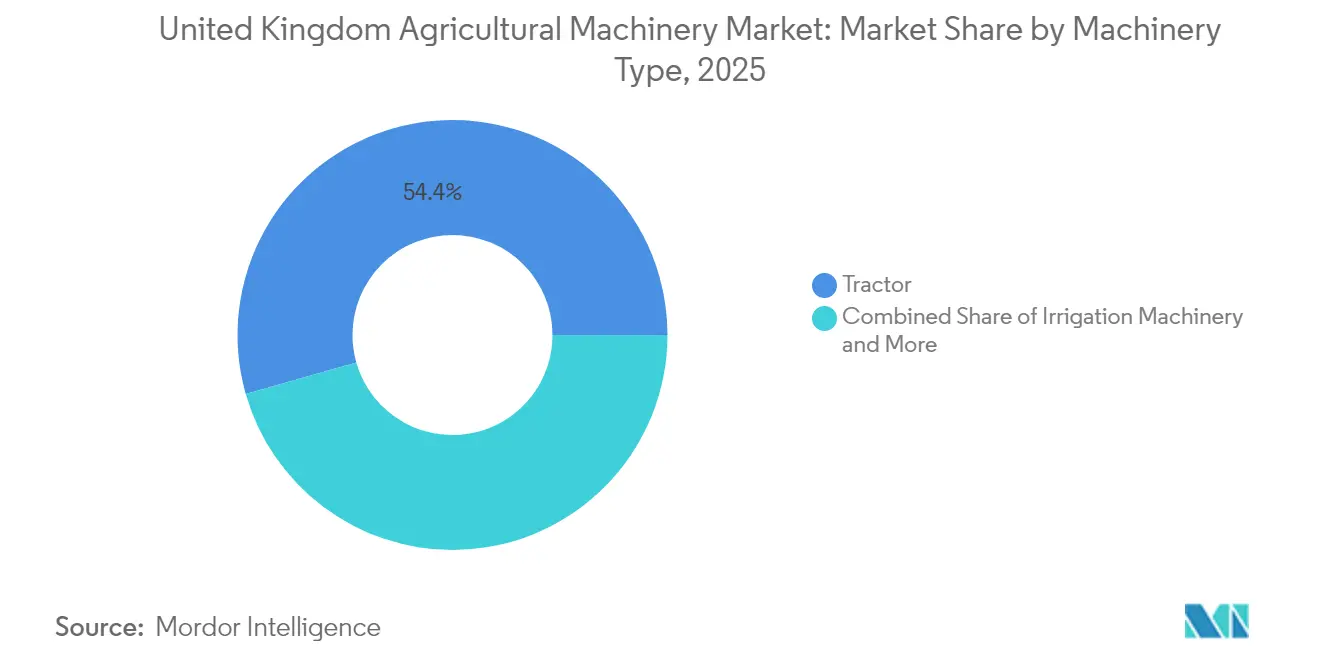

- By machinery type, tractors held 54.42% of the United Kingdom agricultural machinery market share in 2025, while irrigation equipment is forecast to expand at a 7.74% CAGR to 2031, the fastest pace among all categories.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Agricultural Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of labor accelerating mechanization | +1.8% | National, concentrated in East Anglia, Kent, and Lincolnshire | Short term (≤ 2 years) |

| Government grant schemes and tax relief on farm machinery | +1.2% | England-focused with spillover to devolved administrations | Medium term (2-4 years) |

| Demand for precision agriculture and digitalization | +1.0% | National, higher adoption in arable regions | Medium term (2-4 years) |

| Regenerative-farming incentives driving low-compaction equipment demand | +0.8% | National, notably upland and marginal areas | Long term (≥ 4 years) |

| Expansion of agri-robotics testbeds boosting prototype uptake | +0.6% | Regional clusters near universities and innovation hubs | Long term (≥ 4 years) |

| Net-Zero electrification mandates catalyzing electric tractor purchases | +0.3% | National, subject to rural grid capacity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of labor accelerating mechanization

More than 40% of British farms report an insufficient workforce, a figure that has intensified capital outlays toward autonomous and semi-autonomous machinery capable of substituting manual labor.[2]Source: National Farmers Union, “Poor Rural Connectivity,” nfuonline.com Seasonal-worker visas have been extended to 45,000 positions through 2029, yet government policy is simultaneously investing GBP 50 million (USD 63 million) in automation to reduce long-term reliance on migrant labor. Fieldwork Robotics’ raspberry-picking system exemplifies how continuous operation and human-comparable throughput shift return-on-investment calculations in favor of robotics. As labor costs rise, specification requirements move toward equipment that can work longer hours with limited oversight, reinforcing demand across the United Kingdom agricultural machinery market.

Government grant schemes and tax relief on farm machinery

The Farming Equipment and Technology Fund awards between GBP 1,000 and GBP 25,000 (USD 1,250 to USD 31,250) per applicant, while the Improving Farm Productivity program finances up to GBP 500,000 (USD 625,000) for robotics and precision systems. Each funded item must remain in use for five years, providing equipment suppliers with predictable demand cycles. Grant scoring frameworks prioritize carbon reduction and animal welfare metrics, steering purchases toward sensor-rich implements, autonomous guidance, and low-compaction solutions. These incentives directly lift overall equipment turnover within the United Kingdom agricultural machinery market, especially for small and mid-sized farms that historically delayed high-ticket investments.

Regenerative-farming incentives driving low-compaction equipment demand

The Sustainable Farming Incentive’s WBD4 action pays GBP 489 (USD 611) per hectare each year for arable reversion to grassland with restrained fertilizer use. Producers practicing nine or more regenerative techniques record lower input costs but also yield trade-offs, spurring demand for machinery that protects soil while maintaining throughput. Equipment makers have responded with wider tires, reduced axle loads, and controlled-traffic architecture that limits compaction hotspots. Low-impact designs align with the nation’s 2035 Nationally Determined Contribution, which targets an 81% greenhouse-gas cut and makes soil health a pivotal compliance focus. These dynamics are adding specialized-equipment line items to procurement plans throughout the United Kingdom agricultural machinery market.

Net-Zero electrification mandates catalyzing electric tractor purchases

Legislation enacted in 2024 allows hydrogen-powered non-road mobile machinery on public roads, catalyzing pre-orders of hydrogen tractors for 2026 delivery. Clean Power 2030 further pushes carbon intensity below 50 g CO2e/kWh by 2030, compelling farms to adopt hybrid, electric, or hydrogen powertrains.[3]Source: United Kingdom Government, “Clean Power 2030 Action Plan,” gov.uk Grid constraints and charger-access issues temper near-term volumes, yet pilot fleets in Norfolk and Yorkshire already integrate battery-electric tractors for horticulture. As infrastructure gradually improves, electrification adds 0.3-percentage-point growth to the United Kingdom agricultural machinery market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront and maintenance costs | −1.5% | National, especially small operations | Short term (≤ 2 years) |

| Cybersecurity and data privacy risks in connected machinery | −0.8% | Digitally advanced farms | Medium term (2-4 years) |

| Rural grid-capacity limits slowing electric-equipment adoption | −0.6% | Rural areas with limited infrastructure | Long term (≥ 4 years) |

| Post-Brexit certification divergence escalating compliance costs | −0.4% | Import-dependent operations nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High upfront and maintenance costs

The Institute of Chartered Accountants in England and Wales notes that large producers are delaying equipment purchases despite healthy cash flows, reflecting rising unit prices and tighter financing. AGCO Corporation’s Q1 2025 revenue fell 30%, a signal that cost-sensitive buyers are pruning capital budgets. Maintenance burdens compound the hurdle modern combines and tractors require proprietary diagnostic software, cloud subscriptions, and specialized technicians. Even with grant offsets, many small operations find lifecycle costs prohibitive, trimming projected expansion of the United Kingdom agricultural machinery market.

Cybersecurity and data privacy risks in connected machinery

Connected tractors gather field-level yield maps, variable-rate inputs, and telematics that can reveal competitive strategies. Absent clear sector standards, farms fear data misuse or cyberattacks that might shut down guidance or application systems. The United Kingdom Telecoms Innovation Network identifies equipment hacking as an emergent threat, citing proof-of-concept GPS spoofing that could misapply fertilizers. Until robust protocols emerge, risk-averse operators will moderate the adoption of advanced connectivity, dampening full-feature sales within the United Kingdom agricultural machinery market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Tractors Secure the Largest Wallet Share While Irrigation Leads Growth

Tractors accounted for a 54.42% share of the United Kingdom agricultural machinery market in 2025. Segment expansion remains tethered to replacement cycles and horsepower upgrades, with autonomous and telematics integration becoming default specifications. Within tractors, models under 100 horsepower dominate volume, yet high-horsepower units above 150 horsepower capture disproportionate revenue due to their premium pricing and full-stack technology. Deere & Company’s majority share highlights the importance of integrated guidance, connectivity, and after-sales networks that lower the total cost of ownership across the United Kingdom agricultural machinery market.

Irrigation equipment posted an 7.74% CAGR outlook through 2031, the strongest among all categories, and a direct response to unpredictable rainfall and tightening abstraction permits. Pivot systems coupled with soil-moisture sensors help farms align with the Environment Agency’s water-management directives, while drip technology gains traction in high-value horticulture. Precision irrigation supports regenerative objectives by reducing runoff and input waste, underscoring how climate volatility drives product diversification within the United Kingdom agricultural machinery market size framework. Harvesters, forage machinery, and tillage implements also report steady demand, but their growth trails irrigation as water stewardship rises on farm agendas.

Geography Analysis

England generates a significant portion of total equipment turnover, reflecting large contiguous arable tracts in East Anglia and the Midlands that require high-capacity tractors, sprayers, and combines. Scotland prioritizes forage harvesters and livestock equipment for its extensive grazing systems, while Wales and Northern Ireland focus on hill-farm tools and mixed-use machinery suited to fragmented field patterns. The Farming Equipment and Technology Fund’s England-centric allocation accentuates regional asymmetry, informing supplier stock strategies across the United Kingdom agricultural machinery market.

Connectivity gaps create further divergence: in the Scottish Highlands, broadband absence limits precision-tool uptake, whereas East Anglia’s 5G corridors support variable-rate seeding and autonomous irrigation. Regions with grid reinforcement, such as parts of Yorkshire, are early adopters of battery-electric tractors, aided by local renewable-energy clusters. In border counties, post-Brexit import charges complicate parts supply, nudging dealers toward larger safety stocks and longer lead-time planning. Consequently, manufacturers segment product offerings and financing packages by geography to capture unique demand niches across the United Kingdom agricultural machinery market landscape.

Rising temperature variability pushes southern vegetable producers to adopt sensor-based irrigation, while northern arable farms focus on low-compaction tractors to safeguard soil during wetter winters. Government pilots that mandate electric powertrains on public-road travel concentrate initially in grid-ready counties, reinforcing geographic gradients in technology diffusion within the United Kingdom agricultural machinery market.

Competitive Landscape

Five global manufacturers, Deere & Company, CNH Industrial N.V., AGCO Corporation, J.C. Bamford Excavators Ltd., and Kubota Corporation, command the majority of revenue. This high market concentration secures scale efficiencies in Research and Development and distribution, but exposes suppliers to synchronized demand shocks.

Strategic pivots emphasize autonomy and alternative fuels. CNH Industrial N.V.’s New Holland brand partnered with Bluewhite to retrofit autonomous kits that can slash specialty crop operating costs by up to 85%. J.C. Bamford Excavators Ltd. invests in hydrogen combustion engines, aligning with the nation’s road-use regulations for non-road machinery. AGCO Corporation’s divestiture of its Grain and Protein business refocuses capital toward precision agriculture, telematics, and dealer-integrated digital platforms.

Dealer networks play a decisive role in buyer choice, given the importance of uptime and localized service. Leading brands leverage multi-tier finance, remote diagnostics, and subscription-based agronomic support to embed switching costs. Start-ups that pioneer robotics often license technology to incumbents rather than attempt full-line competition, reinforcing incumbent dominance yet adding innovation momentum to the United Kingdom agricultural machinery market.

United Kingdom Agricultural Machinery Industry Leaders

Deere & Company

CNH Industrial N.V.

AGCO Corporation

J.C. Bamford Excavators Ltd.

Kubota Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Deere & Company's acquisition of Sentera, a remote imagery solutions provider, strengthens its precision agriculture capabilities in the UK. The integration of drone-based scouting tools allows farmers to create weed maps, monitor crop health, and optimize agricultural inputs, improving farming efficiency and sustainability across British farmlands.

- February 2025: AGCO Corporation and SDF Group S.p.A. established a supply agreement to manufacture Massey Ferguson tractors with low to mid-range horsepower (up to 85 hp). The production will commence globally, including in the UK, from mid-2025. The collaboration aims to improve Massey Ferguson's market position in utility tractors by utilizing SDF's manufacturing capabilities and providing farmers with reliable, economical equipment.

United Kingdom Agricultural Machinery Market Report Scope

Agricultural machinery encompasses the mechanical devices and structures employed in farming and related activities. The United Kingdom Agricultural Machinery Market is Segmented by Type Into Tractors, Equipment, Irrigation Machinery, Harvesting Machinery, Haying and Forage Machinery, and Other Machinery Types. The Report Offers Market Size and Forecast in Terms of Value in (USD) for the Abovementioned Segments.

By Machinery Type

| Tractor | Less than 50 HP |

| 50 to 100 HP | |

| 100 to 150 HP | |

| Above 150 HP | |

| Equipment | Plows |

| Harrows | |

| Cultivators and Tillers | |

| Other Equipment (Seed Drills, Rollers, etc.) | |

| Irrigation Machinery | Sprinkler Irrigation |

| Drip Irrigation | |

| Other Irrigation Machinery (Center Pivot Systems, Micro Sprinklers, etc.) | |

| Harvesting Machinery | Combine Harvesters |

| Forage Harvesters | |

| Other Harvesting Machinery (Potato Harvesters, Beet Harvesters, etc.) | |

| Haying and Forage Machinery | Mowers and Conditioners |

| Balers | |

| Other Haying and Forage Machinery (Rakes, Tedders) | |

| Other Machinery Types |

| By Machinery Type | Tractor | Less than 50 HP |

| 50 to 100 HP | ||

| 100 to 150 HP | ||

| Above 150 HP | ||

| Equipment | Plows | |

| Harrows | ||

| Cultivators and Tillers | ||

| Other Equipment (Seed Drills, Rollers, etc.) | ||

| Irrigation Machinery | Sprinkler Irrigation | |

| Drip Irrigation | ||

| Other Irrigation Machinery (Center Pivot Systems, Micro Sprinklers, etc.) | ||

| Harvesting Machinery | Combine Harvesters | |

| Forage Harvesters | ||

| Other Harvesting Machinery (Potato Harvesters, Beet Harvesters, etc.) | ||

| Haying and Forage Machinery | Mowers and Conditioners | |

| Balers | ||

| Other Haying and Forage Machinery (Rakes, Tedders) | ||

| Other Machinery Types | ||

Key Questions Answered in the Report

What is the value of the United Kingdom agricultural machinery market in 2026?

The market is worth USD 2.36 billion in 2026 and is projected to reach USD 3.02 billion by 2031.

Which machinery category leads sales nationwide?

Tractors lead, holding 54.42% of total revenue in 2025.

Which segment is growing fastest through 2031?

Irrigation equipment is forecast to post an 7.74% CAGR as farms prioritize water efficiency.

What public funding is available to offset equipment costs?

The Farming Equipment and Technology Fund offers grants up to GBP 25,000 (USD 31,250) per applicant for productivity and sustainability machinery.

Page last updated on: