Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

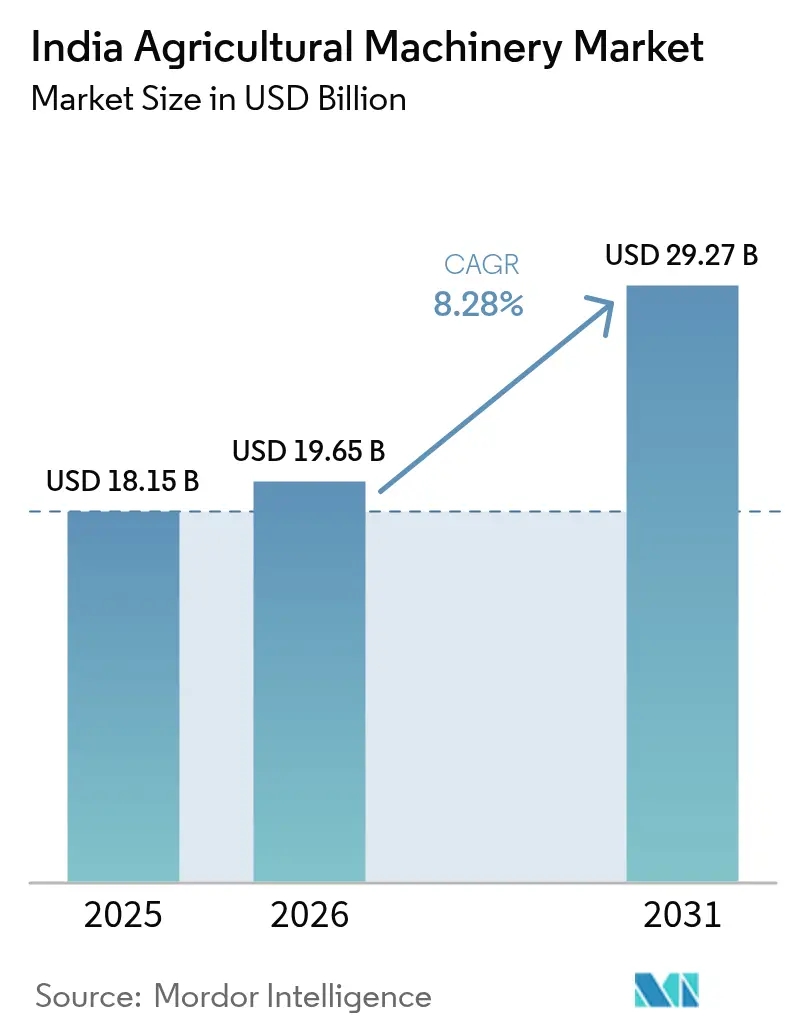

| Base Year Market Size (2025) | USD 18.15 Billion |

| Market Size (2026) | USD 19.65 Billion |

| Market Size (2031) | USD 29.27 Billion |

| Growth Rate (2026 - 2031) | 8.28% CAGR |

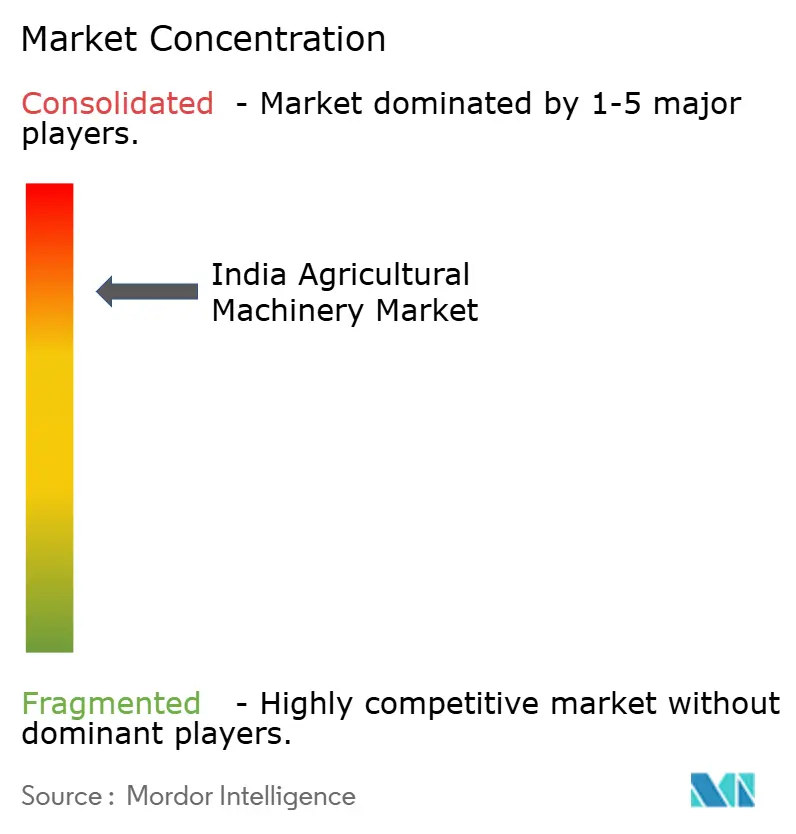

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Agricultural Machinery Market Analysis by Mordor Intelligence

India Agricultural Machinery Market size market size in 2026 is estimated at USD 19.65 billion, growing from 2025 value of USD 18.15 billion with 2031 projections showing USD 29.27 billion, growing at 8.28% CAGR over 2026-2031. Robust public-sector incentives, persistent rural labor shortages, and rapid digitalization are converging to accelerate equipment adoption nationwide. Subsidies under the Sub-Mission on Agricultural Mechanization (SMAM) lower the upfront cost of tractors, irrigation systems, and precision implements, while custom-hiring centers extend access to smallholder farmers. Rising urban migration reduces available farm labor, pushing growers toward mechanized solutions that can sustain timely planting and harvesting operations. In parallel, the Digital Agriculture Mission is creating a farmer registry and geotagged crop database that will underpin precision equipment deployment and data-driven financing. Emission regulations plus emerging incentives for low-emission tractors spur investment in cleaner powertrains, positioning electric and hybrid models as a nascent but strategic growth pocket. Competitive rivalry intensifies as the top five vendors command an 81.5% share, prompting new product launches and capacity expansions geared toward mid-power tractors and smart implements.

Key Report Takeaways

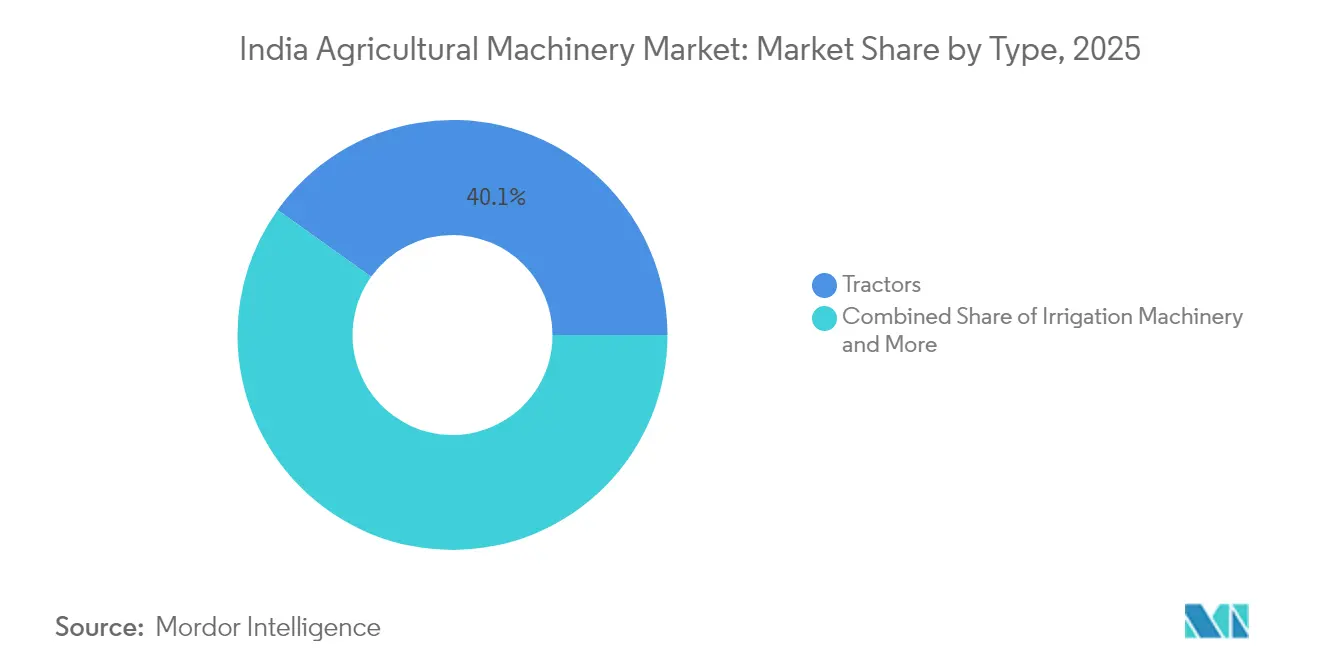

- By type, tractors captured 40.12% of the India agricultural machinery market share in 2025, while irrigation machinery is forecast to expand at a 10.18% CAGR through 2031.

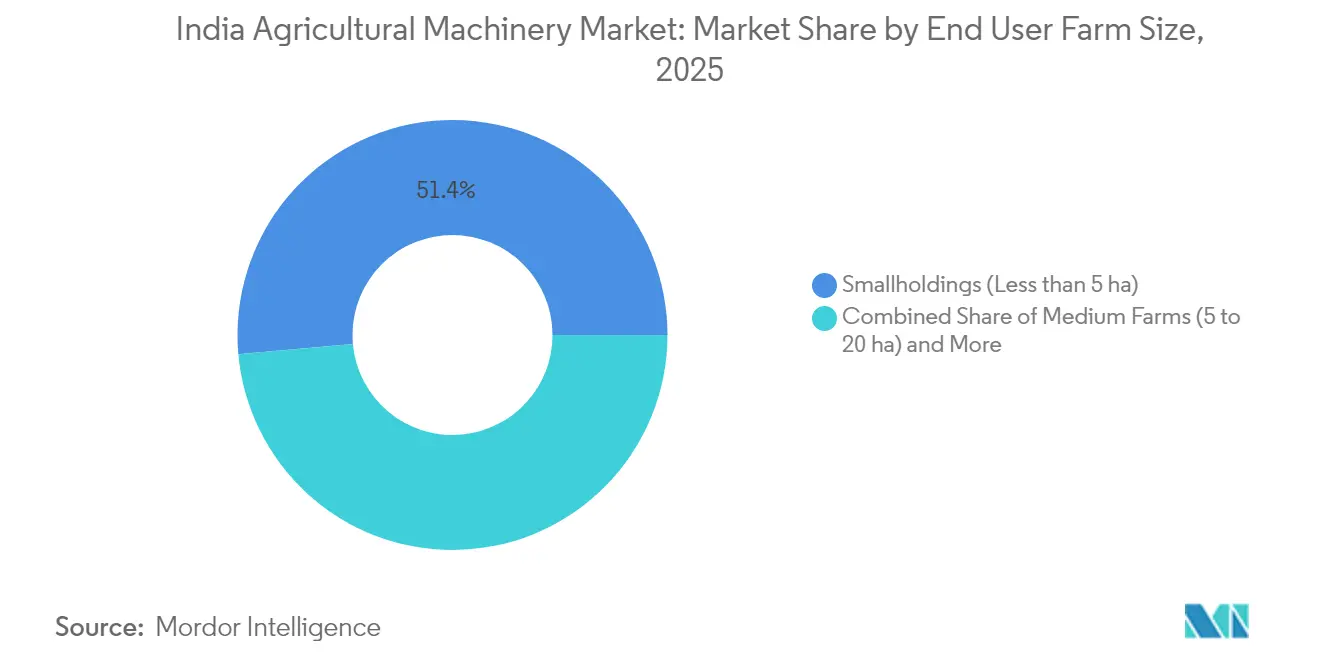

- By end-user farm size, smallholdings under 5 hectares represented 51.42% of the India agricultural machinery market size in 2025, and the large farms above 20 hectares are advancing at an 11.31% CAGR through 2031.

- The Indian agricultural machinery market is concentrated, with five companies - Mahindra & Mahindra Ltd, TAFE Motors and Tractors Limited, Deere & Company, CNH Industrial N.V., and International Tractors Limited (Sonalika) - holding 81.12% market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Agricultural Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government schemes boosting mechanization adoption | +1.2% | Uttar Pradesh, Punjab, and Haryana | Medium term (2-4 years) |

| Rural labor shortage caused by sustained migration to urban centers | +0.9% | Bihar, West Bengal, and Uttar Pradesh | Long term (≥ 4 years) |

| FPOs and contract farming aggregation | +0.7% | Maharashtra, Karnataka, and West Bengal | Medium term (2-4 years) |

| Digital credit platforms enabling financing | +0.8% | Gujarat, Maharashtra, and Tamil Nadu | Short term (≤ 2 years) |

| Electric equipment incentives accelerating adoption | +0.6% | Punjab, Haryana, and Maharashtra | Long term (≥ 4 years) |

| Climate insurance favoring mechanized cultivation | +0.5% | Rajasthan and Maharashtra | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government schemes boosting mechanization adoption

Policy interventions under SMAM provide 40%-50% subsidies on individual machinery purchases and up to 80% on custom-hiring centers. In Uttar Pradesh alone, SMAM disbursed INR 65.66 billion (USD 790 million) between 2014 and 2024, distributing 176,000 machines and establishing 10,769 custom-hiring centers, which collectively expand access to high-capacity equipment across smallholder communities.[1]Source: Press Information Bureau, “Digital Agriculture Mission: Tech for Transforming Farmers’ Lives,” PIB.gov.in Complementary initiatives such as the Kisan Drone subsidy and crop-specific support under the National Food Security Mission channel further demand high-precision implements. These programs not only minimize upfront costs but also strengthen after-sales networks, thereby fostering sustained mechanization across diverse agro-climatic zones.

Rural labor shortage caused by sustained migration to urban centers

Household survey data indicate that only 9% of main income earners remain in farming, down from historic norms above 50%. Seasonal out-migration peaks during planting and harvesting, intensifying labor deficits that mechanization can bridge through timely tillage, sowing, and harvesting.[2]Source: International Crops Research Institute for the Semi-Arid Tropics, “Farm mechanization trends and policy in India,” ICAR.org.in Combine harvesters cut labor requirements by up to 30% and reduce post-harvest losses by 2-4 percentage points, making them indispensable in rice-wheat rotations. Equipment sharing through custom-hiring centers further leverages scarce machinery to maintain cropping intensities in labor-scarce districts.

FPOs and contract farming aggregation

More than 26,000 Farmer-Producer Organizations (FPOs) have been registered, with government grants of up to INR 1.8 million (USD 21,700) per entity to finance collective infrastructure. Aggregation bolsters bargaining power, enabling bulk procurement of tractors, planters, and threshers on favorable terms. Contract farming within Farmer-Producer Organizations (FPOs) clusters also creates predictable cash flows, aligning loan repayment with harvest cycles and incentivizing higher-capacity machinery acquisitions that individual smallholders could not manage alone.

Digital credit platforms enabling financing

Over 7.7 million Kisan Credit Cards have been digitized, providing working-capital limits up to INR 500,000 (USD 6,000) and seamless integration with equipment dealerships. Advanced risk scoring that uses satellite imagery and yield analytics has trimmed loan-approval times to less than 72 hours and reduced default rates by 120 basis points, prompting lenders to roll out pay-per-use tractor loans and embedded insurance bundles. Accessible financing accelerates the India agricultural machinery market by unlocking latent demand among credit-constrained farmers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High equipment cost and limited credit access | -1.1% | Bihar, Odisha, and eastern states | Medium term (2-4 years) |

| Fragmented landholdings limit scale efficiency | -0.8% | Punjab, Haryana, and Uttar Pradesh | Long term (≥ 4 years) |

| Emission norms vary across states | -0.4% | Industrialized regions | Short term (≤ 2 years) |

| Lack of skilled telematics technicians | -0.3% | Rural districts nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High equipment cost and limited credit access

Despite generous subsidies, a mid-horsepower tractor still requires an outlay exceeding INR 600,000 (USD 7,200), a sum beyond the reach of many marginal growers. Formal lenders often demand collateral, and interest spreads remain 200-300 basis points above prime lending, deterring big-ticket investments. Custom-hiring centers cushion the cost hurdle but are unevenly distributed, eastern India hosts fewer than 12 centers per district versus 45-plus in parts of the north, perpetuating regional disparities.

Fragmented landholdings limit scale efficiency

The average operational holding has shrunk to 0.2 hectares, making self-owned machinery economically unviable. Narrow field geometry complicates maneuverability for combine harvesters and boom sprayers, raising per-acre operating costs. While FPO aggregation and land-leasing reforms are evolving, the structural constraint of fragmentation continues to throttle large-equipment penetration in the India agricultural machinery market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Tractors anchor adoption while irrigation accelerates

Tractors retained a 40.12% revenue share in 2025, underscoring their foundational role in tillage and haulage across diverse cropping systems. Irrigation Machinery is the fastest growing segment with micro-irrigation pumps and drip systems advancing at a 10.18% CAGR, propelled by drought-mitigation programs and rising electricity tariffs that favor precision watering. Equipment segments, including plows, harrows, and rotovators, benefit from the mechanization push in smallholder farming, where these implements provide entry-level mechanization solutions that require lower capital investment than tractors. Harvesting machinery experiences steady growth as labor shortages intensify during peak seasons, with combine harvesters and forage harvesters becoming essential for timely crop collection in commercial farming operations.

Adapters that merge global navigation satellite systems with traditional implements are converting conventional tractors into smart machines that execute straight-line plowing and seed placement within ±2.5 cm precision, reducing input waste by 6%-8%. Electric-assist rotovators and battery-powered orchard sprayers are gaining traction among fruit growers, where low noise and zero emissions are prized. The India agricultural machinery market continues to diversify as balers, mowers, and mulchers gain relevance in residue-management schemes aimed at curbing open-field burning. Market leaders respond with modular attachment ecosystems, allowing a single tractor chassis to support over 20 task-oriented implements, thereby spreading ownership cost over multiple revenue streams.

By End-User Farm Size: Smallholders dominate, yet large farms surge

Smallholdings under 5 hectares captured 51.42% of the India agricultural machinery market in 2025, reflecting the structural dominance of marginal holdings. These growers gravitate toward low-horsepower tractors (20-35 HP) and entry-level implements priced below INR 175,000 (USD 2,100). Medium farms spanning 5-20 hectares account for 35.02% of revenue and display a growing appetite for precision seeders and multi-crop threshers that shorten turnaround times between successive crops.

Large farms above 20 hectares post the highest growth at 11.31% CAGR through 2031 as consolidation accelerates in peri-urban belts and export-oriented commodity zones. This cohort invests in 45-70 HP tractors, combine harvesters, and variable-rate fertilizer applicators that enhance scale economies. Government policies specifically target small and marginal farmers through enhanced subsidies and Custom Hiring Centres, creating pathways for mechanization access regardless of farm size while supporting the transition toward more efficient agricultural structures. Integrated telematics dashboards help estate managers oversee fleet utilization and predictive maintenance, unlocking uptime improvements exceeding 5 percentage points.

Geography Analysis

Punjab and Haryana jointly account for a significant share of aggregate tractor sales despite holding only 7% of the national cultivable area, mirroring high farm power availability above 3 kW per hectare. Subsidized residue-management kits and favorable minimum support prices sustain demand for straw balers and reversible plows that reduce open-field burning episodes. These two states illustrate a mature mechanization plateau where replacement and technology upgrade cycles, rather than first-time purchases, now drive growth.

Maharashtra and Gujarat showcase diversified cropping patterns that necessitate equipment ranging from cotton pickers to drip-line installation rigs. Vidarbha’s dramatic 850-fold surge in rotovator adoption within a decade underscores latent demand once price and credit barriers are eased. Gujarat’s horticulture clusters adopt fertigation pumps and greenhouse sprayers, helping the state achieve India’s highest micro-irrigation coverage at 65% of irrigated area. The state's progressive policies and farmer education programs create an environment conducive to technology adoption, with digital agriculture initiatives gaining traction through public-private partnerships and demonstration projects.

Eastern and central regions represent the next frontier, with Uttar Pradesh alone requiring farm power to double from 2.0 kW per hectare to 4.0 kW to meet projected food demand. Farmer-Producer Organization (FPO)-led aggregation and state-backed custom-hiring hubs are key to scaling machinery density, particularly in rice-dominated districts where puddling and transplanting are labor-intensive. Meanwhile, Karnataka and Tamil Nadu lead southern India in integrating digital advisory with equipment services, exemplified by e-crop booking systems that synchronize machinery availability with phenology forecasts. Together, these initiatives position the India agricultural machinery market for geographically balanced growth over the coming decade.

Competitive Landscape

The India agricultural machinery market remains concentrated, with Mahindra & Mahindra Ltd, TAFE Motors and Tractors Limited, Deere & Company, CNH Industrial N.V., and International Tractors Limited (Sonalika) collectively holding an 81.5% share in 2024. Mahindra & Mahindra Ltd extended its lead to 43.3% in FY 2025 by leveraging a 1,200-dealer network and rolling out the OJA smart-tractor platform that embeds automation and remote diagnostics. Deere & Company’s USD 100 million greenfield plant in Maharashtra targets mid-power tractor exports and positions the company to challenge the incumbent leadership in premium utility segments.

Technology differentiation is paramount. Mahindra & Mahindra Ltd’s MYOJA intelligence pack offers in-cabin displays and geofence alerts, while Escorts Kubota Limited integrates Kubota’s engine technology for improved fuel efficiency. CNH Industrial N.V. pilots 4G-enabled combine harvesters that transmit real-time yield maps to cloud dashboards, aiding input optimization. Domestic innovators such as VST Tillers Tractors Ltd. progressively shift from two-wheel to compact four-wheel tractors, targeting niche orchard and horticulture applications where maneuverability is crucial.

Strategic alliances accelerate Research and Development and market penetration. Mahindra & Mahindra Ltd collaborates with Mitsubishi Mahindra Agricultural Machinery on compact diesel engines, while Deere & Company partners with Indian startups for AI-based weed detection. Policy-driven electrification opens a greenfield segment where new entrants develop battery-swap systems tailored to remote villages lacking continuous grid power. As emission rules stiffen, larger firms exploit scale economies in compliance engineering, potentially widening the moat against smaller assemblers in the India agricultural machinery market.

India Agricultural Machinery Industry Leaders

TAFE Motors and Tractors Limited

Deere & Company

CNH Industrial N.V.

International Tractors Limited (Sonalika)

Mahindra & Mahindra Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Deere & Company introduced the 5130M tractor in India, featuring 130 HP capacity, making it the highest-powered tractor in the country. The tractor incorporates GearPro and PermaClutch technologies, along with smart connectivity features and precision farming capabilities to enhance operational efficiency and reduce fuel consumption.

- December 2024: Mahindra Tractors formed a partnership with Punjab National Bank (PNB) to provide dealer financing solutions, which aim to improve inventory funding and increase tractor availability in rural markets. The partnership supports agricultural mechanization by providing dealers with better access to funds and improving tractor distribution.

- June 2024: New Holland, a brand of CNH Industrial N.V., launched the WORKMASTER 105 tractor in India. This 100+ horsepower (HP) model features a TREM-IV emission standard-compliant engine, bringing advanced technology, quality, and performance to Indian customers. The tractor is equipped with an FPT Engine delivering 106 HP and includes features such as a 3,500 kg lift capacity, electro-hydraulic 4WD engagement, and an air-suspended seat with adjustable backrest.

- February 2024: International Tractors Limited (Sonalika) introduced 10 new Tiger tractors in the 40-75 HP range. The tractors feature five new engines, multi-speed transmissions, and 5G hydraulics to improve power, fuel efficiency, and versatility. The European-designed range serves various farming and commercial applications, supporting Sonalika's export market presence.

India Agricultural Machinery Market Report Scope

Agricultural machinery is the mechanical structures and devices used in farming or other agricultural purposes. The India Agricultural Machinery Market is segmented by type (tractors (less than 50 HP, 50 to 75 HP, 76 to 100 HP, 101 to 150 HP, greater than 150 HP), equipment (plows, harrows, rotovators and cultivators, seed and fertilizer drills, and other equipment), irrigation machinery (sprinkler machinery, drip irrigation, and other irrigation machinery), harvesting machinery (combine harvesters, forage harvesters, and other harvesting machinery), and haying and forage machinery (mowers and conditioners, balers, and other haying and forage machinery). The report offers market size and forecast in terms of value (USD) for all the abovementioned segments.

By Type

| Tractors | Less than 50 HP |

| 50 to 75 HP | |

| 76 to 100 HP | |

| 101 to 150 HP | |

| Greater than 150 HP | |

| Equipment | Plows |

| Harrows | |

| Rotovators and Cultivators | |

| Seed and Fertilizer Drills | |

| Other Equipment (Post-Hole Diggers, Power Weeders, etc.) | |

| Irrigation Machinery | Sprinkler Irrigation |

| Drip Irrigation | |

| Other Irrigation Machinery (Center-Pivot Systems, Micro-Sprinklers, etc.) | |

| Harvesting Machinery | Combine Harvesters |

| Forage Harvesters | |

| Other Harvesting Machinery (Sugarcane Harvesters, Potato Harvesters, etc.) | |

| Haying and Forage Machinery | Mowers and Conditioners |

| Balers | |

| Other Haying and Forage Machinery (Tedders, Rakes, etc.) |

By End-User Farm Size

| Smallholdings (Less than 5 ha) |

| Medium Farms (5 to 20 ha) |

| Large Farms (Greater than 20 ha) |

| By Type | Tractors | Less than 50 HP |

| 50 to 75 HP | ||

| 76 to 100 HP | ||

| 101 to 150 HP | ||

| Greater than 150 HP | ||

| Equipment | Plows | |

| Harrows | ||

| Rotovators and Cultivators | ||

| Seed and Fertilizer Drills | ||

| Other Equipment (Post-Hole Diggers, Power Weeders, etc.) | ||

| Irrigation Machinery | Sprinkler Irrigation | |

| Drip Irrigation | ||

| Other Irrigation Machinery (Center-Pivot Systems, Micro-Sprinklers, etc.) | ||

| Harvesting Machinery | Combine Harvesters | |

| Forage Harvesters | ||

| Other Harvesting Machinery (Sugarcane Harvesters, Potato Harvesters, etc.) | ||

| Haying and Forage Machinery | Mowers and Conditioners | |

| Balers | ||

| Other Haying and Forage Machinery (Tedders, Rakes, etc.) | ||

| By End-User Farm Size | Smallholdings (Less than 5 ha) | |

| Medium Farms (5 to 20 ha) | ||

| Large Farms (Greater than 20 ha) | ||

Key Questions Answered in the Report

What is the value of the India Agricultural Machinery Market in 2026?

The market stands at USD 19.65 billion in 2026 and is forecast to reach USD 29.27 billion by 2031.

How fast is tractor electrification progressing in India?

Pilot programs show electric tractors can cut operating costs by 18%, and dedicated subsidies under PM E-DRIVE are accelerating commercialization.

Which segment is expanding the fastest?

Irrigation machinery leads with a 10.18% CAGR through 2031 as water-efficient technologies gain traction.

Why are custom-hiring centers important?

They pool capital-intensive machinery so smallholders can rent equipment during peak periods, boosting productivity without heavy upfront investment.

Page last updated on: