Market Overview

| Study Period | 2021 - 2031 |

|---|---|

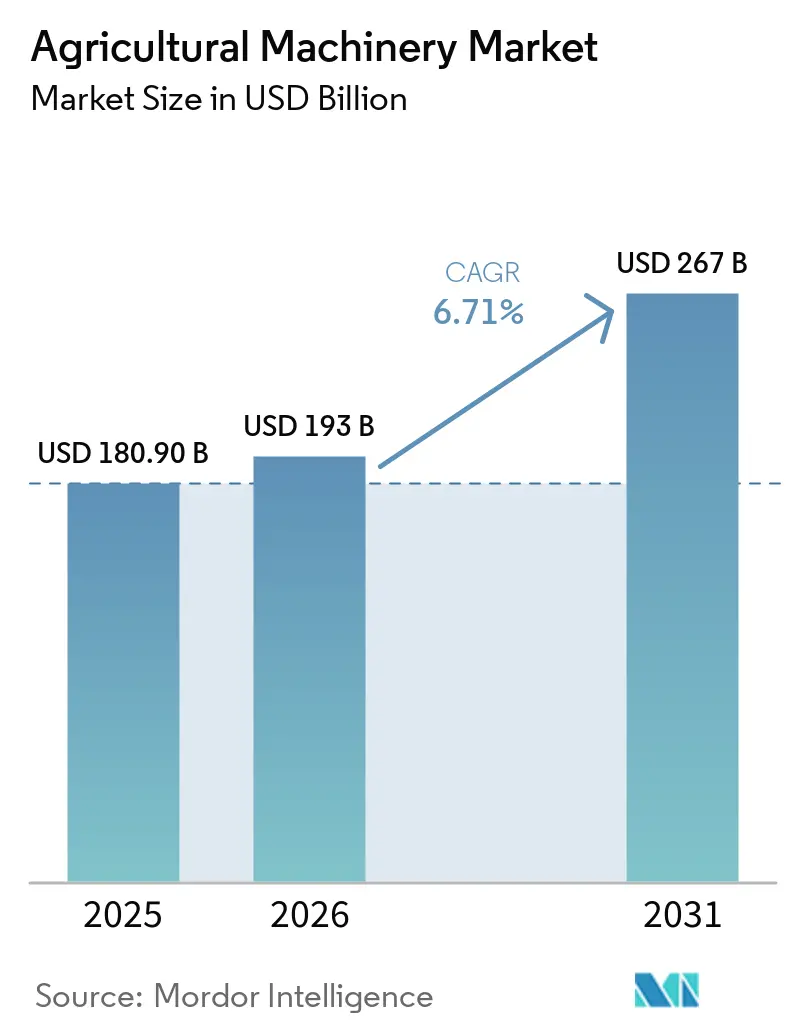

| Market Size (2026) | USD 193 Billion |

| Market Size (2031) | USD 267 Billion |

| Growth Rate (2026 - 2031) | 6.71% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Machinery Market Analysis by Mordor Intelligence

The agricultural machinery market size is projected to grow from USD 180.9 billion in 2025 to USD 193.0 billion in 2026 and USD 267.0 billion by 2031, registering a CAGR of 6.71% during 2026-2031. The market maintains a strong demand base due to challenges in securing farm labor, rising wage costs, and the need for higher output from fewer farms. According to the National Agricultural Statistics Service (NASS), Agricultural Statistics Board, United States Department of Agriculture (USDA), in the United States, the average gross wage for all hired farm workers reached USD 19.10 per hour in October 2024, a 3% increase from the previous year, further strengthening the economic rationale for mechanized field operations. Policy support for fleet renewal and digital adoption in major farming economies is also influencing the market. However, in early 2026, demand softened in North America and Europe, leading to delayed purchases rather than eliminating long-term replacement needs. Deere & Company reported a net income of USD 656 million for the first quarter of fiscal year 2026, down from USD 869 million in the previous year, reflecting cyclical pressures currently affecting the agricultural machinery market.

Key Report Takeaways

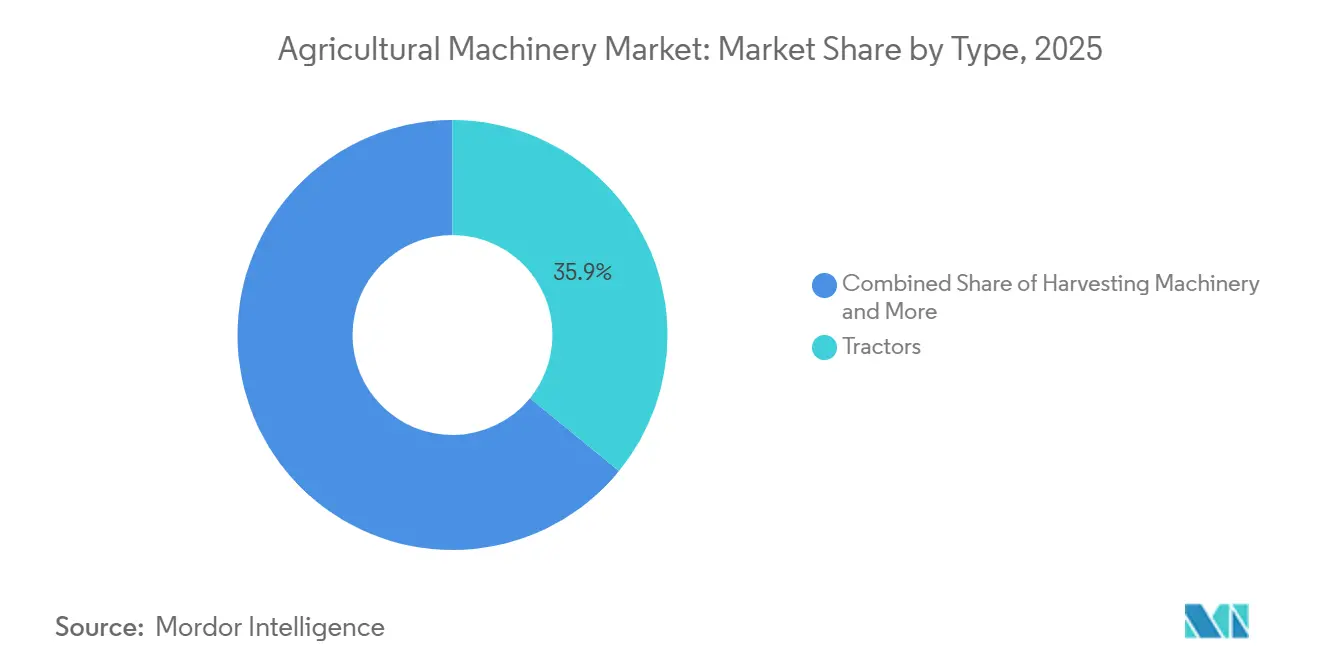

- By type, tractors led with the largest 35.90% of the agricultural machinery market share in 2025, whereas the harvesting machinery segment is projected to expand at a 6.00% CAGR from 2026 to 2031.

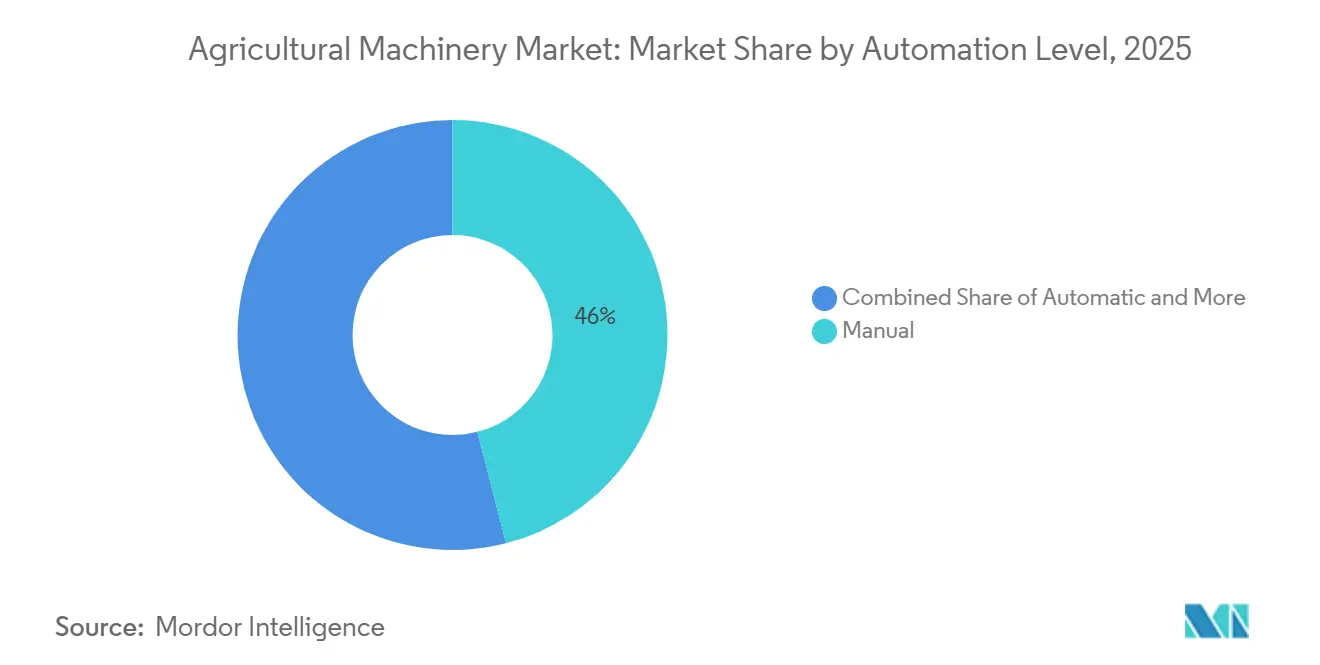

- By automation level, manual equipment held the largest share of the agricultural machinery market size at 46.0% in 2025, while automatic systems recorded the fastest CAGR at 6.17% from 2026 to 2031.

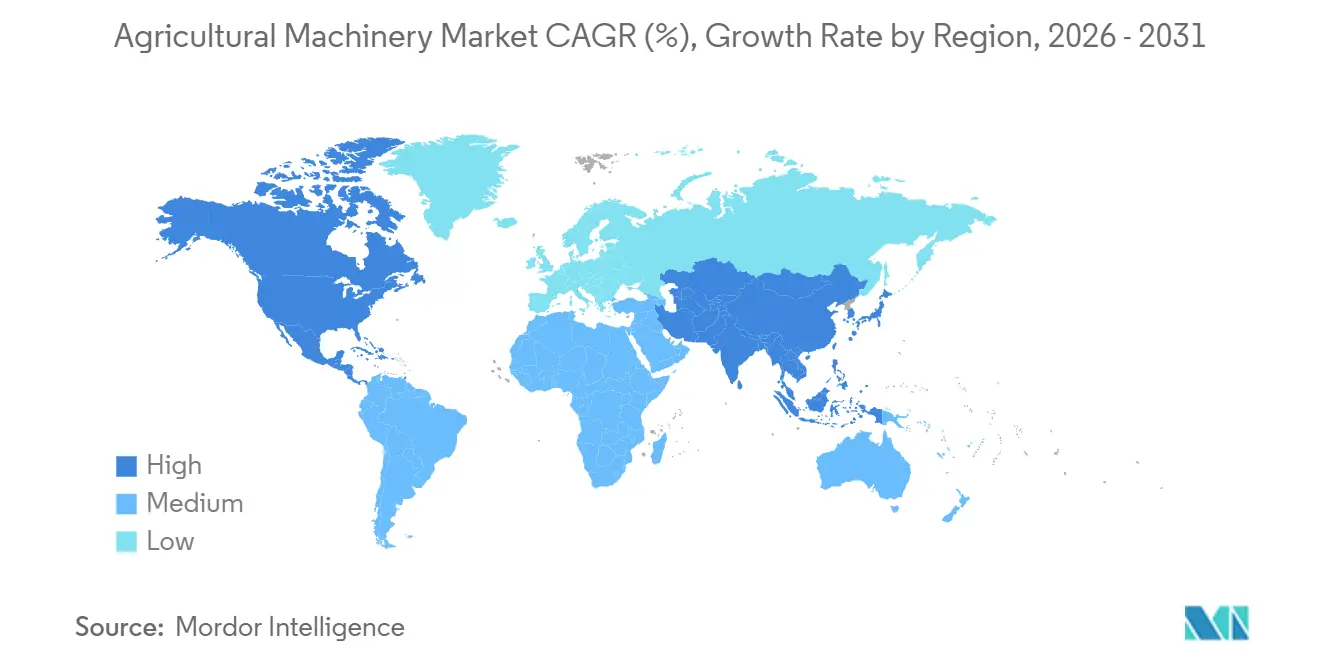

- By geography, Asia-Pacific held the largest share of 36.8% in the agricultural machinery market in 2025, while North America recorded the fastest CAGR of 7.20% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Agricultural Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Farm labor scarcity and wage inflation | +1.6% | Global, highest intensity in North America, Europe, and East Asia | Short term (≤ 2 years) |

| Precision agriculture and telematics integration | +1.8% | Global, early adoption concentrated in North America and Europe, scaling in Asia-Pacific | Medium term (2-4 years) |

| Subsidies and mechanization credit support | +1.3% | Asia-Pacific, South America, and North America | Short term (≤ 2 years) |

| Farm consolidation and output-per-acre pressure | +1.0% | North America, Europe, and emerging areas of South America | Medium term (2-4 years) |

| Custom hiring and equipment-as-a-service expansion | +0.7% | Global, with fastest uptake in South Asia and Sub-Saharan Africa | Medium term (2-4 years) |

| Regenerative and low-emission equipment funding | +0.6% | North America, Europe, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Farm Labor Scarcity and Wage Inflation

The agricultural machinery market is currently influenced by tighter farm labor conditions. According to America Farm Bureau Federation, nearly 384,900 H-2A temporary agricultural worker visas were issued in fiscal year 2024 [1]Source: American Farm Bureau Federation, “Critical Farm Labor Visa Use Ticks Up,” FB.org. Despite this, labor shortages persist in many seasonal operations. This has impacted purchasing decisions within the agricultural machinery market, as growers increasingly compare labor costs with the expenses and operational stability associated with machine ownership. Equipment that reduces peak labor demand in activities such as harvesting, transplanting, and spraying is gaining popularity, even as overall demand for machinery remains subdued.

Precision Agriculture and Telematics Integration

The agricultural machinery market is increasingly transitioning to a stage where telematics and digital agronomy tools are becoming standard features on mid-range and premium equipment. In February 2025, Deere & Company launched its Precision Essentials package, which includes a StarFire 7500 receiver, G5 display, and JDLink modem. This package enables both newer and older machines to be upgraded more efficiently. This development is significant for the agricultural machinery market, as retrofit options allow farmers to extend the lifespan of existing equipment while adopting features such as guided operations, connectivity, and field data functionalities. Consequently, market competition is evolving from a focus solely on hardware to integrated ecosystems comprising hardware, software, and services.

Subsidies and Mechanization Credit Support

The agricultural machinery market is benefiting significantly from public support programs and credit structures that reduce barriers to mechanization. In key growth economies, policies are evolving from basic volume-based incentives to initiatives promoting higher-performing, connected, and more efficient machinery. This transition is important as it sustains average selling prices in the agricultural machinery market, even when overall unit demand fluctuates. Additionally, it enables smaller operators to access machinery through mechanisms such as custom hiring centers, farm machinery banks, shared-use fleets, and targeted credit channels, rather than requiring full ownership from the outset. These measures are driving continued mechanization in regions like the Asia-Pacific and South America, even under constrained private financing conditions.

Farm Consolidation and Output-Per-Acre Pressure

The agricultural machinery market is undergoing changes driven by farm consolidation and the need to enhance field productivity per pass. According to the United States Department of Agriculture National Agricultural Statistics Service, the number of farms in the United States decreased to 1.86 million in 2025, a reduction of 15,000 farms compared to 2024. Meanwhile, the average farm size increased to 469 acres in 2025, up from 466 acres in the previous year [2]Source: United States Department of Agriculture National Agricultural Statistics Service, “Farms and Land in Farms 2025 Summary,” USDA.gov. These trends in the agricultural machinery market favor the adoption of wider implements, higher horsepower tractors, and combines capable of covering more acres per working day. Additionally, the focus on uptime, fuel efficiency, and guidance accuracy has grown, as larger farms increasingly depend on fewer machines to manage greater areas of land.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost and financing pressure | -1.8% | Global, most acute in North America, Europe, and Brazil | Short term (≤ 2 years) |

| Fragmented farm structures and uneven payback | -1.2% | South Asia, Southeast Asia, Africa, and smallholder regions of South America | Medium term (2-4 years) |

| Autonomous field-operation regulatory uncertainty | -0.6% | North America and Europe | Medium term (2-4 years) |

| Data ownership, repair access, and interoperability frictions | -0.5% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost and Financing Pressure

The agricultural machinery market faces challenges due to the high cost of new equipment and the financial strain associated with large purchases. This issue is particularly pronounced in high-horsepower tractors and combines, where farmers are postponing replacement cycles due to constrained cash flow and increased borrowing costs. AGCO Corporation reported net sales of USD 10.1 billion in 2025, a 13.5% decrease compared to 2024 [3]Source: AGCO Corporation, “AGCO Reports Fourth Quarter and 2025 Full Year Results,” AGCOCorp.com. According to the Association of Equipment Manufacturers (AEM) 2026 report, the sales of agricultural tractors in the United States were down 9.1%, and combine sales dropped 25.3% compared to March 2025, driven by weaker farm economics and financial pressures. Dealer inventory normalization and improved credit conditions are critical for a stronger recovery in equipment demand.

Fragmented Farm Structures and Uneven Payback

The agricultural machinery market encounters structural limitations in regions dominated by smallholder farming. According to the Food and Agriculture Organization of the United Nations (FAO), as of 2026, Africa accounts for nearly half of the world’s uncultivated arable land. However, crop yields on the continent remain at only 56% of the global average, and mechanization penetration is particularly low, especially in hilly and semi-arid areas. In such regions, individual machine ownership often yields limited returns due to small field sizes, fragmented land tenure, and restricted annual utilization. These factors hinder demand growth in the agricultural machinery market, even when the need for mechanization is evident. While rental models and shared service centers provide some relief, they do not fully address the utilization challenges influencing purchase decisions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Tractors Drive Value, Harvesting Technology Accelerates Growth

Tractors led the agricultural machinery market with 35.9% of the market share in 2025, keeping them the largest type category by value. This dominance reflects their role as the primary power source for field preparation, planting, haulage, crop care, and various attachments across most farming systems. However, demand within the tractor category varies. Compact models are performing well in horticulture and specialty applications, while machines with 100 horsepower and above remain essential for large row-crop operations in North America and Europe. Additionally, there is growing interest in purpose-built orchard and vineyard tractors, driven by advancements in autonomy and precision spraying for specialty crops.

The harvesting machinery segment of the agricultural machinery market is projected to grow at a CAGR of 6.0% from 2026 to 2031, making it the fastest-growing segment. This growth is attributed to increased adoption of automated settings, crop sensing, header control, and grain-quality management technologies, which enhance field efficiency during limited harvest periods. The market is also expanding beyond traditional combines and threshers, with forage harvesters gaining traction in dairy and livestock systems and specialty crop harvesters transitioning from pilot use to broader commercialization. Other key categories, such as soil preparation and cultivation machinery, planting and seeding machinery, and spraying and crop protection machinery, continue to benefit from advancements in conservation tillage, precision application, and improved input control.

By Automation Level: Manual Segment Leads by Share, Automatic Systems Gain the Fastest Momentum

Manual agricultural machinery accounted for the largest market share at 46.0% in 2025, highlighting the significant role of developing farm economies in the agricultural machinery market. This segment remains dominant in regions where small landholdings, limited farm income, and operator-driven equipment are prevalent. As a result, the market continues to witness substantial sales of equipment with minimal automation, even as higher-end buyers shift towards advanced technologies. This divide is particularly evident in regions such as South Asia, Africa, and parts of South America, where affordability and basic functionality drive purchasing decisions.

Automatic systems are projected to grow at the fastest CAGR of 6.2% from 2026 to 2031, making them the most rapidly advancing segment in the agricultural machinery market. Semi-automatic machines serve as a critical intermediary between manual and fully automated systems, offering features such as steering assistance, section control, and telematics at a lower cost compared to fully autonomous solutions. The agricultural machinery industry is projected to experience the most significant automation advancements in high-value specialty crops and larger consolidated farms, where the benefits of labor savings and precision are most pronounced.

Geography Analysis

Asia-Pacific accounted for the largest 36.8% of the agricultural machinery market size in 2025, which made it the largest regional market. The market in this region is driven by China's fleet modernization initiatives and India's significant tractor demand by volume. China is focusing on intelligent machinery, autonomous driving support systems, and new-energy equipment, with agricultural drone usage already operating at a substantial scale. In India, demand is bolstered by robust farm activity and ongoing mechanization needs. For instance, Mahindra and Mahindra Limited reported tractor sales of 46,404 units in April 2026, reflecting a 20% year-on-year increase. Meanwhile, the agricultural machinery markets in Japan and Australia are more mature and technology-driven, whereas Southeast Asian markets are expanding through smallholder mechanization programs.

North America is projected to grow at the fastest 7.2% CAGR from 2026 to 2031, which makes it the fastest-growing geography in the agricultural machinery market. Although the market is currently experiencing a cyclical trough, replacement demand from fleets purchased in the last decade is projected to drive a later-cycle recovery. South America remains a high-potential region for the agricultural machinery market. Brazil and Argentina are supported by large-scale crop production, although tighter credit conditions have slowed near-term purchases.

Europe continues to be a significant agricultural machinery market due to its robust manufacturing base, high levels of mechanization, and ongoing investments in precision farming technologies. Demand in the region is shaped by factors such as replacement cycles, financing conditions, and agricultural policies focused on sustainability, which promote efficiency improvements on farms. In the Middle East, irrigation expansion projects and controlled-environment agriculture are driving demand for specialized machinery and water-management equipment. Africa, while at an earlier stage of mechanization, is witnessing gradual growth in long-term machinery demand, supported by government-led agricultural modernization programs and food security initiatives in several developing farming economies.

Competitive Landscape

The agricultural machinery market is moderately fragmented. The leading group comprises the top five companies: Deere and Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, and CLAAS KGaA mbH. These companies maintain their position through broad product portfolios, extensive dealer networks, financing capabilities, and increasing digital integration. Other established manufacturers, such as SDF S.p.A., Yanmar Holdings Co., Ltd., and Argo Tractors S.p.A., compete by leveraging regional expertise, product specialization, and a strong presence in specific agricultural equipment categories. Additionally, niche players, including irrigation specialists, India-focused tractor manufacturers, and implement companies, hold strong positions in particular segments. This multi-tiered structure promotes active competition while preventing the market from becoming highly concentrated.

Competition is intensifying in areas where precision software, automation, and recurring service revenue intersect with traditional equipment sales. AGCO Corporation’s PTx Trimble structure exemplifies this trend, providing a robust digital platform that complements its hardware offerings and extends into retrofit, guidance, and autonomy functions. Similarly, CLAAS KGaA mbH demonstrated its commitment to innovation by maintaining research and development spending at EUR 319.9 million (USD 346 million) in fiscal year 2025, despite a slight decline in overall revenue. These developments highlight that product leadership in the agricultural machinery market increasingly depends on automation and connectivity capabilities, alongside traditional factors like engine power and machine size.

The agricultural machinery market is also creating opportunities for companies that can deliver advanced capabilities to farms unable to afford premium autonomous platforms. For instance, Mahindra and Mahindra Limited is defending its market share in India through rapid product updates. In March 2026, the company launched the Mahavator and Mahavator HD heavy-duty rotavator range and continued promoting orchard spraying solutions via its M.I.T.R.A platform. These initiatives suggest that the most sustainable competitive advantage lies in integrating machinery, software, agronomic data, and post-sale services to enhance farm outcomes throughout the entire operating cycle.

Agricultural Machinery Industry Leaders

Deere & Company

AGCO Corporation

Kubota Corporation

CNH Industrial N.V.

CLAAS KGaA mbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mahindra and Mahindra Limited introduced the Mahavator and Mahavator HD heavy-duty rotavator series, offering working widths ranging from 4 to 9 feet. These models feature an improved, wider mast design and are designed for heavy tillage applications across various agronomic zones in India.

- August 2025: CLAAS KGaA mbH introduced the JAGUAR 1000 series forage harvesters, offering throughput capacities of up to 500 tons per hour and engine outputs between 850 and 1,110 hp. This launch addresses the growing demand in the agricultural machinery market for high-capacity, precision-enabled harvesting equipment designed to enhance operational efficiency and forage quality.

- February 2025: Deere & Company introduced its next-generation autonomous tillage system, equipped with 16 cameras and advanced processing capabilities. This system enables fully autonomous field operations without requiring human supervision. It marks an advancement in agricultural automation, reinforcing Deere & Company's position in the development of autonomous farming technology.

Global Agricultural Machinery Market Report Scope

Agricultural machinery encompasses mechanical equipment and tools utilized in farming activities, including land preparation, planting, irrigation, crop protection, harvesting, and post-harvest processing. These machines enhance operational efficiency, minimize labor dependency, boost productivity, and facilitate large-scale modern agricultural practices across various crop systems. The Agricultural Machinery Market Report is segmented by type (tractors, soil preparation and cultivation machinery, planting and seeding machinery, harvesting machinery, spraying and crop protection machinery, hay and forage machinery, and irrigation machinery), by automation level (manual, semi-automatic, and automatic), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

By Type

| Tractors | By Horsepower | Less than 40 HP |

| 40 HP to 99 HP | ||

| 100 HP and Above | ||

| By Tractor Type | Compact Utility Tractors | |

| Utility Tractors | ||

| Row Crop Tractors | ||

| Orchard and Vineyard Tractors | ||

| Soil Preparation and Cultivation Machinery | Plows | |

| Harrows | ||

| Cultivators and Tillers | ||

| Planting and Seeding Machinery | Seed Drills | |

| Planters | ||

| Broadcast Spreaders | ||

| Transplanters | ||

| Harvesting Machinery | Combine Harvesters and Threshers | |

| Forage Harvesters | ||

| Specialty Crop Harvesters | ||

| Spraying and Crop Protection Machinery | Self-Propelled Sprayers | |

| Trailed and Mounted Sprayers | ||

| Aerial and Drone-Enabled Spraying Systems | ||

| Hay and Forage Machinery | Mower-Conditioners | |

| Balers | ||

| Rakes and Tedders | ||

| Irrigation Machinery | Sprinkler Irrigation | |

| Drip Irrigation | ||

| Mechanized Pivot Systems | ||

By Automation Level

| Manual |

| Semi-Automatic |

| Automatic |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Type | Tractors | By Horsepower | Less than 40 HP |

| 40 HP to 99 HP | |||

| 100 HP and Above | |||

| By Tractor Type | Compact Utility Tractors | ||

| Utility Tractors | |||

| Row Crop Tractors | |||

| Orchard and Vineyard Tractors | |||

| Soil Preparation and Cultivation Machinery | Plows | ||

| Harrows | |||

| Cultivators and Tillers | |||

| Planting and Seeding Machinery | Seed Drills | ||

| Planters | |||

| Broadcast Spreaders | |||

| Transplanters | |||

| Harvesting Machinery | Combine Harvesters and Threshers | ||

| Forage Harvesters | |||

| Specialty Crop Harvesters | |||

| Spraying and Crop Protection Machinery | Self-Propelled Sprayers | ||

| Trailed and Mounted Sprayers | |||

| Aerial and Drone-Enabled Spraying Systems | |||

| Hay and Forage Machinery | Mower-Conditioners | ||

| Balers | |||

| Rakes and Tedders | |||

| Irrigation Machinery | Sprinkler Irrigation | ||

| Drip Irrigation | |||

| Mechanized Pivot Systems | |||

| By Automation Level | Manual | ||

| Semi-Automatic | |||

| Automatic | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East | Saudi Arabia | ||

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of agricultural machinery demand worldwide in 2026?

The agricultural machinery market stands at USD 193.0 billion in 2026.

Which product category leads global equipment demand?

Tractors are the largest type segment, accounting for 35.9% of total market value in 2025.

Which automation tier is growing the fastest?

Automatic systems are projected to grow at a 6.2% CAGR from 2026 to 2031.

Why are farmers investing in more advanced equipment even during a weak cycle?

Labor is tighter, wages are higher, and larger farms need more acres covered per pass, so the payback from efficient and connected machines is improving even when purchase timing is delayed.

Page last updated on: