Agricultural Planting And Fertilizing Machinery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

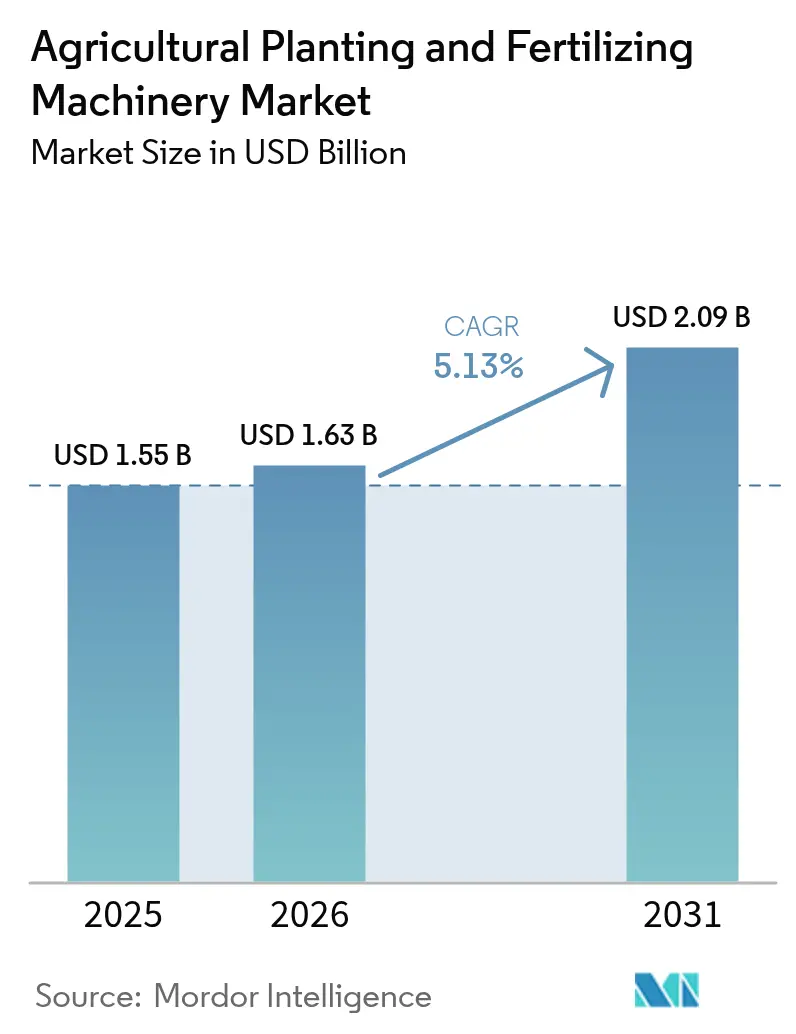

| Market Size (2026) | USD 1.63 Billion |

| Market Size (2031) | USD 2.09 Billion |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

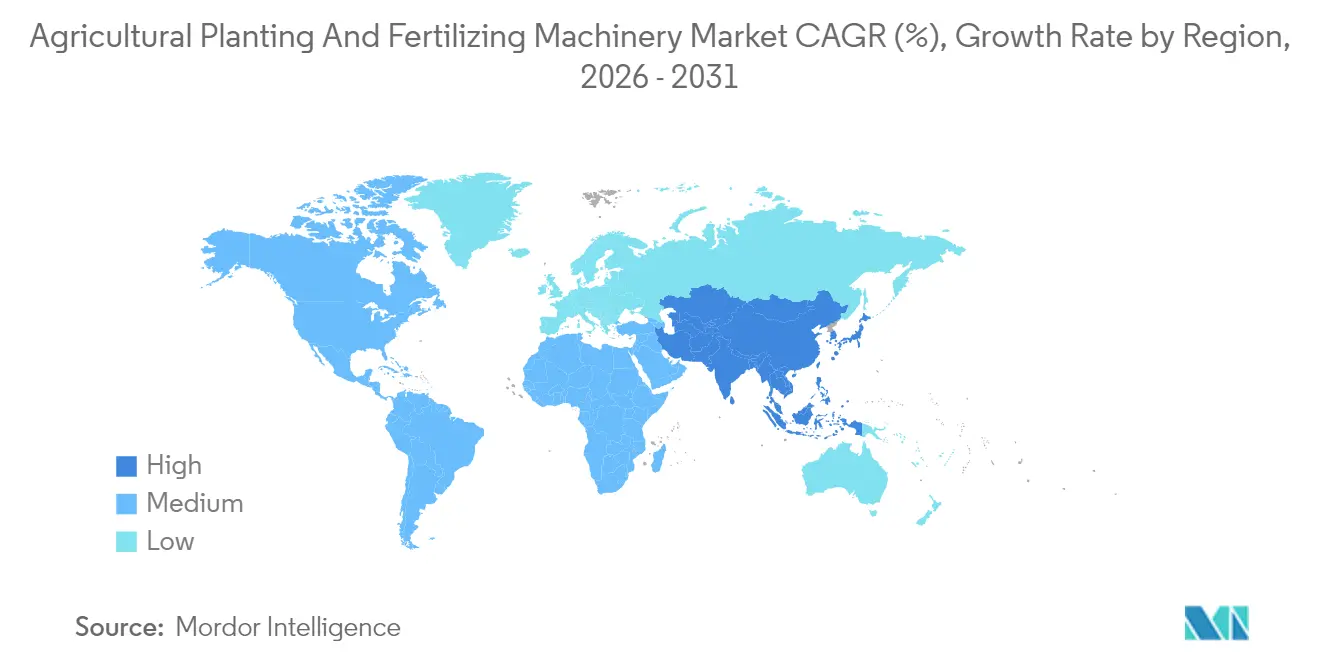

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

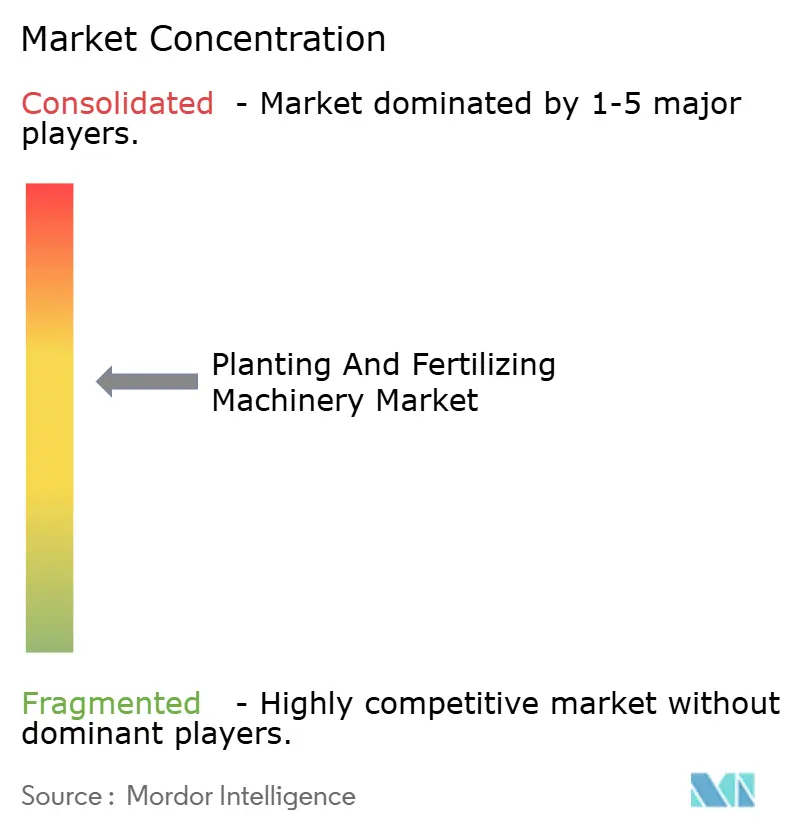

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Planting And Fertilizing Machinery Market Analysis by Mordor Intelligence

The agricultural planting and fertilizing machinery market size was valued at USD 1.55 billion in 2025 and estimated to grow from USD 1.63 billion in 2026 to reach USD 2.09 billion by 2031, at a CAGR of 5.13% during the forecast period (2026-2031). Capital intensity and lengthy replacement cycles place a natural ceiling on expansion, yet persistent labor scarcity, stricter environmental rules, and widening carbon-credit opportunities are prompting growers to replace legacy implements with precision-ready models. Mid-sized farms increasingly view variable-rate technology as a dual-purpose tool that boosts per-hectare output and unlocks verified emissions reductions. Semiconductor supply constraints continue to stretch lead times for GPS (Global Positioning System) modules, but the industry is redesigning control units around alternative chips to keep production flowing. Meanwhile, business models that package agronomic analytics with hardware and financing are sustaining revenue growth even where unit sales flatten.

Key Report Takeaways

- By Type, planting led with 60.40% of the agricultural planting and fertilizing machinery market share in 2025, while Fertilizer machinery is projected to expand at a 6.67% CAGR through 2031.

- By Geography, North America commanded 35.02% revenue in 2025, while Asia-Pacific is forecast to post the fastest regional growth at a 7.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Agricultural Planting And Fertilizing Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Decline in farm labor availability | +1.2% | Global, acute in North America, Europe, and Australia | Medium term (2-4 years) |

| Increased farm mechanization rates | +0.9% | Asia-Pacific core, spillover to Sub-Saharan Africa | Long term (≥ 4 years) |

| Growing adoption of precision agriculture | +1.4% | North America and Europe lead, expanding to Brazil and Argentina | Short term (≤ 2 years) |

| Government subsidies and low-interest credit lines | +0.8% | India, China, select EU member states | Medium term (2-4 years) |

| Emergence of Agriculture-Technology-as-a-Service (ATaaS) models | +0.5% | North America, pilot programs in Brazil and India | Long term (≥ 4 years) |

| Regenerative-farming carbon-credit incentives for precision input placement | +0.4% | North America, European Union, and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Decline in Farm Labor Availability

Tight labor markets are trimming the seasonal workforce by double digits, especially in the United States and Western Europe, prompting operators to turn to automated seeders and spreaders that reduce the number of field passes. USDA data show farm employment dropped below its pre-2020 level even while planted area held steady, a gap that magnifies the penalty for delayed operations[1]Source: United States Department of Agriculture, “Farm Labor Survey,” USDA.gov. Equipment that pairs telematics with task automation lets one operator supervise several machines, raising labor productivity without matching wage inflation. Despite the efficiency gains, regions with structural underemployment experience muted demand, which limits their global reach in the near term.

Increased Farm Mechanization Rates

Policy-backed mechanisation runs in India and China are converting subsistence plots into semi-commercial units that can collectively finance new equipment. India’s Sub-Mission on Agricultural Mechanisation reimbursed up to 50% of the machine cost for women and scheduled caste farmers in 2024. China’s cooperative land-use model enables villages to share precision planters that individual households cannot afford. The momentum, while strong, hinges on sustained fiscal support; past subsidy cuts triggered order slumps, making this driver sensitive to budget cycles.

Growing Adoption of Precision Agriculture

Variable-rate seeding and fertilization are becoming mainstream after peer-reviewed trials confirmed double-digit input savings without yield sacrifice. Compliance pressure compounds the economic case, the EU Farm to Fork Strategy targets a 20% fertilizer reduction by 2030[2]Source: European Commission, “Farm to Fork Strategy,” ec.europa.eu. OEMs (Original Equipment Manufacturers) now ship prescription-map compatibility as a standard feature, trimming the incremental premium and widening appeal among cost-conscious growers.

Government Subsidies and Low-Interest Credit Lines

Capital access remains the swing factor for first-time buyers. Canada’s Agricultural Clean Technology Program issued CAD 50 million (USD 37 million) in 2024 for precision implements. India’s NABARD (National Bank for Agriculture and Rural Development) refinancing lowered tractor loan rates to 4%, pulling equipment finance below inflation[3]Source: National Bank for Agriculture and Rural Development, “Rural Infrastructure Development Fund,” nabard.org. Such programs compress payback periods, yet their withdrawal can promptly chill demand as Brazil’s 2023 rural-credit rollback proved.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial equipment investment | -0.7% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Complex operation and maintenance requirements | -0.5% | Regions with limited technical extension services | Medium term (2-4 years) |

| Semiconductor tariff and sensor supply-chain volatility | -0.4% | Global, concentrated in precision-equipment segments | Short term (≤ 2 years) |

| Data-privacy and cyber-security concerns around connected machinery | -0.2% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Equipment Investment

Precision planters with variable-rate capability cost USD 80,000 to USD 120,000, outstripping annual income for many farms under 200 hectares. Limited collateral and elevated lending rates in Sub-Saharan Africa and South Asia keep ownership concentrated among capital-rich operators. Cooperative models and leasing mitigate outlay, yet scant rural logistics hamper large-scale sharing.

Complex Operation and Maintenance Requirements

GPS calibration, prescription-map handling, and sensor diagnostics require skill sets often absent in regions where extension programs have eroded. A 2024 Midwest survey found 38% of operators failed to activate variable-rate modes despite owning the feature. OEM efforts to simplify user interfaces assume reliable cellular networks, a weak link across many rural zones.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Precision Drives Fertilizer Machinery Growth

Planting machinery captured 60.40% of the agricultural planting and fertilizing machinery market share in 2025, underscoring its status as the workload anchor on row-crop farms. Seed drills dominate cereal acreage thanks to mechanical simplicity, lower purchase price, and compatibility with small-tract plots. Planters and transplanters cater to high-value vegetables and tobacco; their premium pricing limits diffusion to regions with intensive horticulture and ready credit. Fertilizer machinery is set for a 6.67% CAGR through 2031, making it the fastest-growing component of the agricultural planting and fertilizing machinery market. Prescription maps and nutrient-runoff penalties are pushing operators to swap broadcast units for variable-rate spreaders that trim input waste and satisfy compliance. Seed-cum-fertilizer drills combine both tasks in one pass, saving fuel and preserving soil moisture in dryland zones.

Environmental mandates amplify demand for rate control. The EU Nitrates Directive enforces nitrogen-leaching limits, accelerating the replacement of legacy spreaders with sensor-guided variants. In North America, carbon programs link abatement payments to verified nutrient cuts, turning precision fertilization into an income stream rather than an optional feature. Manufacturers now ship controllers as default, shrinking the price gap and expanding the agricultural planting and fertilizing machinery market size of precision-ready spreaders.

Geography Analysis

North America held 35.02% of 2025 revenue in the agricultural planting and fertilizing machinery market due to large-scale maize and soybean farms that view machinery as a productivity lever. Replacement demand dominates, operators upgrade to maintain precision capability rather than expand unit counts. Canada’s prairie growers favor high-capacity air seeders suited to no-till residues. Mexico is beginning to mechanize communal ejido plots, but credit barriers slow the transition.

Asia-Pacific is projected to grow at a 7.72% CAGR through 2031, the fastest regional pace in the agricultural planting and fertilizing machinery market. China’s village cooperatives pool resources to buy GPS-guided planters that optimize dense planting windows. India’s subsidy programs target women-led self-help groups, widening the addressable customer base. Japan and Australia represent mature niches where replacements and precision retrofits keep value rising even as unit volumes plateau. Australian adoption of controlled-traffic systems requires highly accurate guidance, further boosting advanced planter demand.

Europe’s market revolves around policy-linked sustainability conditions. Subsidy payments now hinge on demonstrable nutrient-use cuts, making rate-controlled spreaders essential. Germany and France top adoption thanks to robust dealer networks. Post-Brexit United Kingdom shifts support from acreage to environmental outcomes, stimulating equipment purchases that capture and validate field data. Southern Europe lags due to fragmented farms and aging operators, but cooperative ownership is gaining traction. South America centers on Brazil and Argentina, both driven by export-oriented soybean and maize operations. Brazil’s MODERFROTA loan program historically underpinned purchases, yet its 2023 scale-back exposed demand sensitivity to fiscal shifts. Argentina’s currency volatility steers buyers toward domestically built planters that offer reliability at lower precision. The Middle East and Africa remain emergent; Saudi Arabia’s controlled-environment projects are bright spots for high-spec spreaders in desert farming.

Competitive Landscape

The sector shows moderate concentration, with Deere & Company, CNH Industrial, AGCO Corporation, Kubota Corporation, and Mahindra & Mahindra Limited capturing a modest percentage of sales. Vertical integration lets incumbents bundle equipment, financing, and agronomic software, binding customers through multi-year service contracts. Right-to-repair debates in the United States threaten that moat by compelling OEMs to share diagnostics and parts catalogs. Regulatory loosening could open service revenue to independents, trimming OEM margin.

Emerging rivals exploit precision niches. Horsch and Väderstad push high-speed planters with individual row control, courting growers who prize stand uniformity. Great Plains Manufacturing and Monosem focus on conservation and row-crop seeders for mixed fleets. Sensor specialists license hardware to established builders while monetizing algorithms, shifting value away from metal toward data layers.

Strategic shifts underline the digital tilt. CNH Industrial paired with Microsoft to feed Azure analytics into field terminals, cutting prescription latency. AGCO’s Fendt Momentum planter uses row shut-off to curb overlap, capturing premium pricing among technology-forward operators. Kubota’s stake in Bloomfield Robotics brings AI-based scouting to its planter line. Mahindra expanded Indian capacity to supply subsidy-driven rural demand. CLAAS integrates spreader control into tractor displays, simplifying adoption in Europe’s tight regulatory backdrop.

Agricultural Planting And Fertilizing Machinery Industry Leaders

CNH Industrial NV

AGCO Corporation

Kubota Corporation

Deere & Company

Mahindra & Mahindra Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: SKY Agriculture has introduced the FALCON T range of trailed fertilizer spreaders, featuring advanced precision technologies such as dynamic weighing, ISOBUS control, and the FertiEye system, which has received industry recognition. The equipment is notable for its versatility, enabling farmers to transition between spreading granulated fertilizers and wet bulk within 7 minutes. This ensures efficiency, precision, and adaptability to varying field conditions.

- September 2025: Amazone is preparing to introduce the world's first fully autonomous fertilizer spreader, capable of operating without a driver while ensuring precise application. This development, revealed before Agritechnica, incorporates advanced GPS guidance and automation systems to enhance efficiency and minimize labor requirements in contemporary farming practices.

- September 2025: Väderstad introduced its new Spirit and Inspire seed drills at Agritechnica 2025, equipped with the TriForce II seed coulter suspension for enhanced depth control precision. These seed drills offer increased coulter pressure, hydraulic depth adjustment, and improved crop establishment across diverse soil conditions.

Global Agricultural Planting And Fertilizing Machinery Market Report Scope

Agricultural planting and fertilizing machinery market encompasses agricultural equipment such as seed drills, planters, spreaders, and sprayers that enable efficient seed sowing and precise fertilizer application. These machines increase agricultural productivity, minimize resource waste, and promote sustainable farming practices. The agricultural planting and fertilizing machinery market is segmented by type into planting machinery and fertilizing machinery. The planting machinery market is segmented by Type (seed drills and planters & transplanted), and the fertilizing machinery segment (seed cum fertilizer drills and fertilizer spreaders). The market is also segmented by Geography (North America, Europe, Asia-Pacific, South America, and Africa). The report offers the market sizes and forecasts in value (USD) for all the above segments.

| Planting Machinery | Seed Drills |

| Planters and Transplanters | |

| Fertilizing Machinery | Seed-cum-Fertilizer Drills |

| Fertilizer Spreaders |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Russia | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Type | Planting Machinery | Seed Drills |

| Planters and Transplanters | ||

| Fertilizing Machinery | Seed-cum-Fertilizer Drills | |

| Fertilizer Spreaders | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Russia | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the agricultural planting and fertilizing machinery market in 2031?

The market is forecast to reach USD 2.09 billion by 2031, rising from USD 1.63 billion in 2026.

Which equipment segment is growing the fastest?

Fertilizer spreaders are anticipated to post the highest growth, advancing at a 6.67% CAGR through 2031.

Why is Asia-Pacific the fastest-growing region?

Government subsidies, land consolidation, and rising precision adoption lift mechanization rates, supporting a 7.72% regional CAGR.

How does labor scarcity influence equipment demand?

Shortage of seasonal workers pushes farms toward automated planters and spreaders that complete fieldwork on tighter schedules.

Page last updated on: