Organic Whey Protein Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

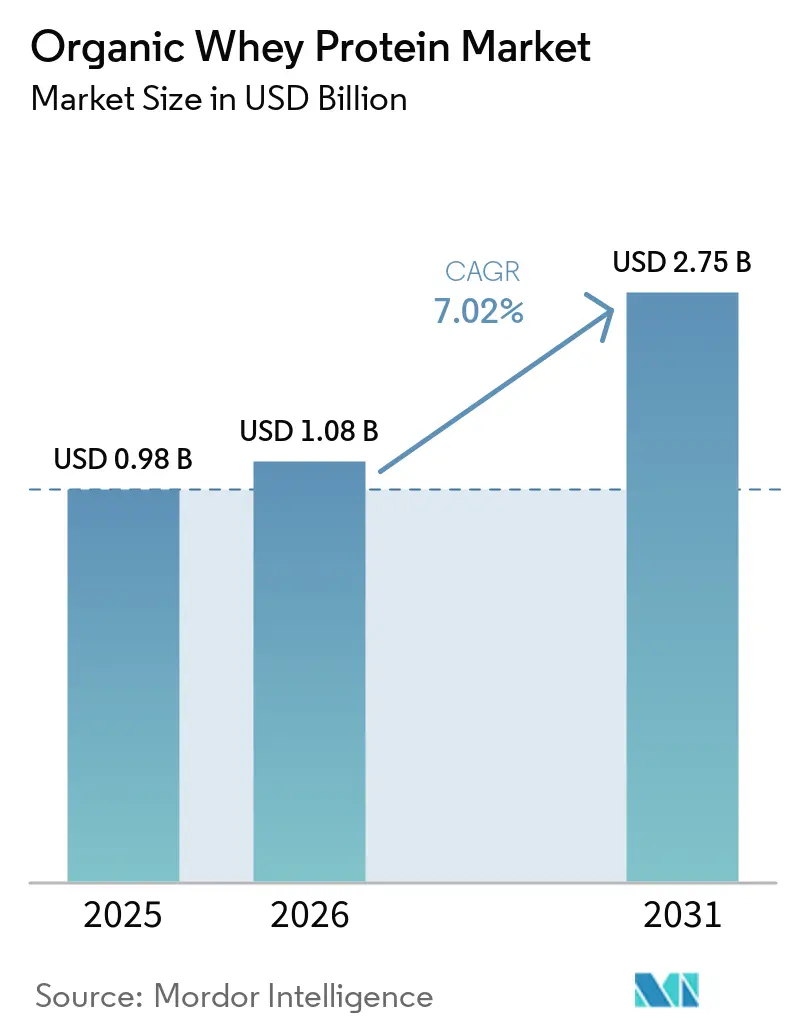

| Market Size (2026) | USD 1.08 Billion |

| Market Size (2031) | USD 2.75 Billion |

| Growth Rate (2026 - 2031) | 7.02% CAGR |

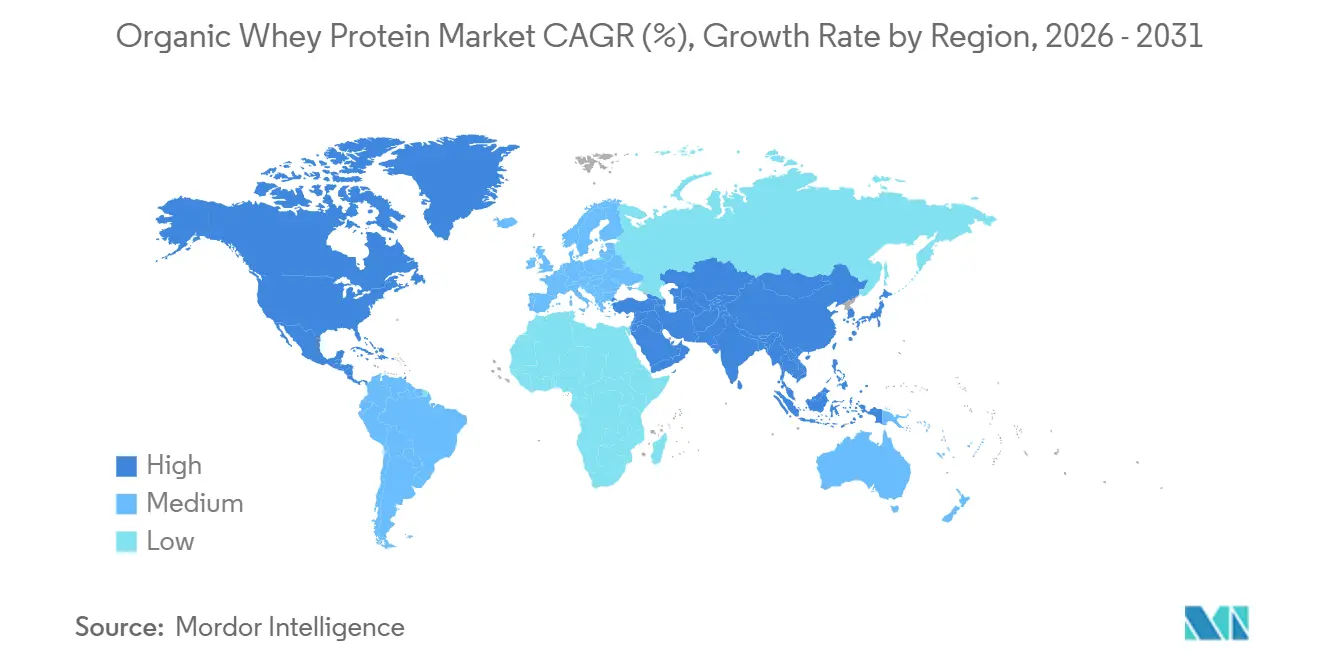

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organic Whey Protein Market Analysis by Mordor Intelligence

The organic whey protein market size was valued at USD 0.98 billion in 2025 and estimated to grow from USD 1.08 billion in 2026 to reach USD 2.75 billion by 2031, at a CAGR of 7.02% during the forecast period (2026-2031). The organic whey protein market is being supported by stronger demand for clean-label protein, a broader active nutrition consumer base, and rising use of premium protein in reformulated food and beverage products. Certified supply remains a clear pricing advantage because producers that can meet both USDA organic expectations and EU Organic Regulation 2018/848 requirements are better placed to defend premium positioning than conventional whey suppliers. Tight whey processing capacity, especially in higher-protein formats, has also increased the value of established certified supply chains and raised the strategic importance of filtration capacity. Competitive strategy in the organic whey protein market is centered on certification depth, traceability, and product format expansion, while new entry remains limited by the cost of organic dairy sourcing and long certification lead times. High production costs, tighter compliance oversight, and slow growth in organic milk supply keep the organic whey protein market exposed to supply pressure even as demand expands

Key Report Takeaways

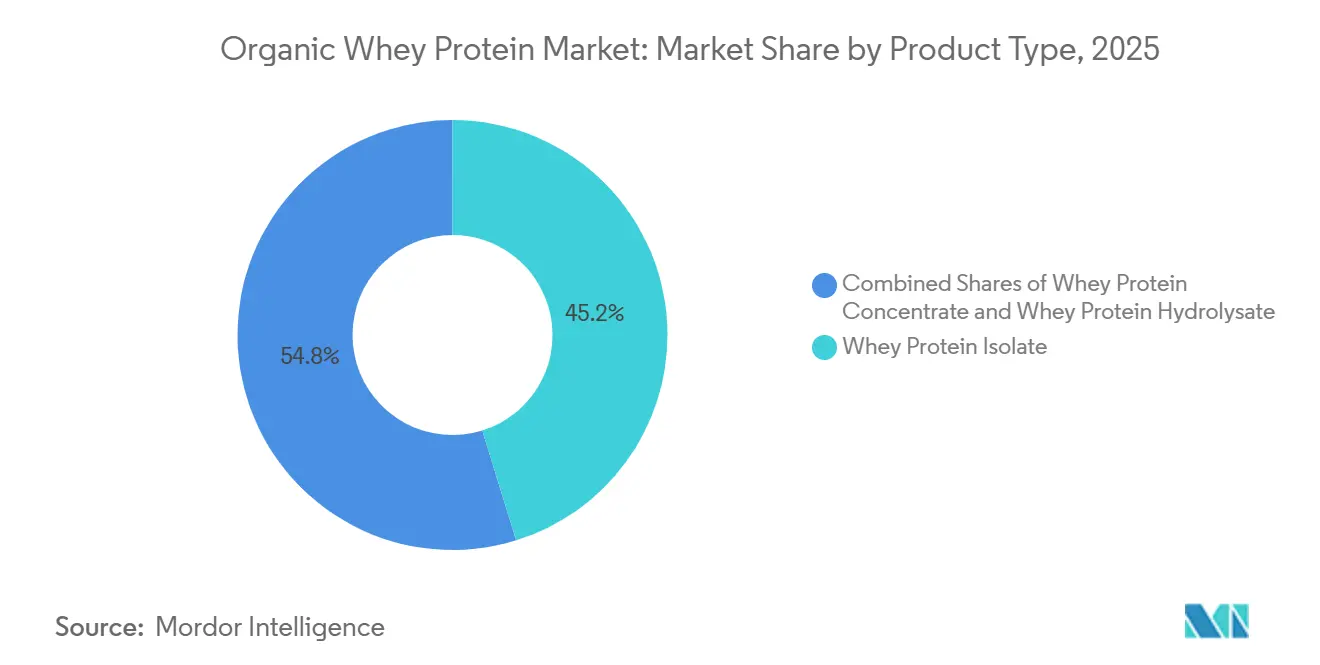

- By product type, Whey Protein Isolate held 45.21% share in 2025, while Whey Protein Hydrolysate is forecast to expand at an 8.55% CAGR through 2031.

- By form, Powder accounted for 75.48% share in 2025, while Liquid is projected to grow at an 8.11% CAGR through 2031.

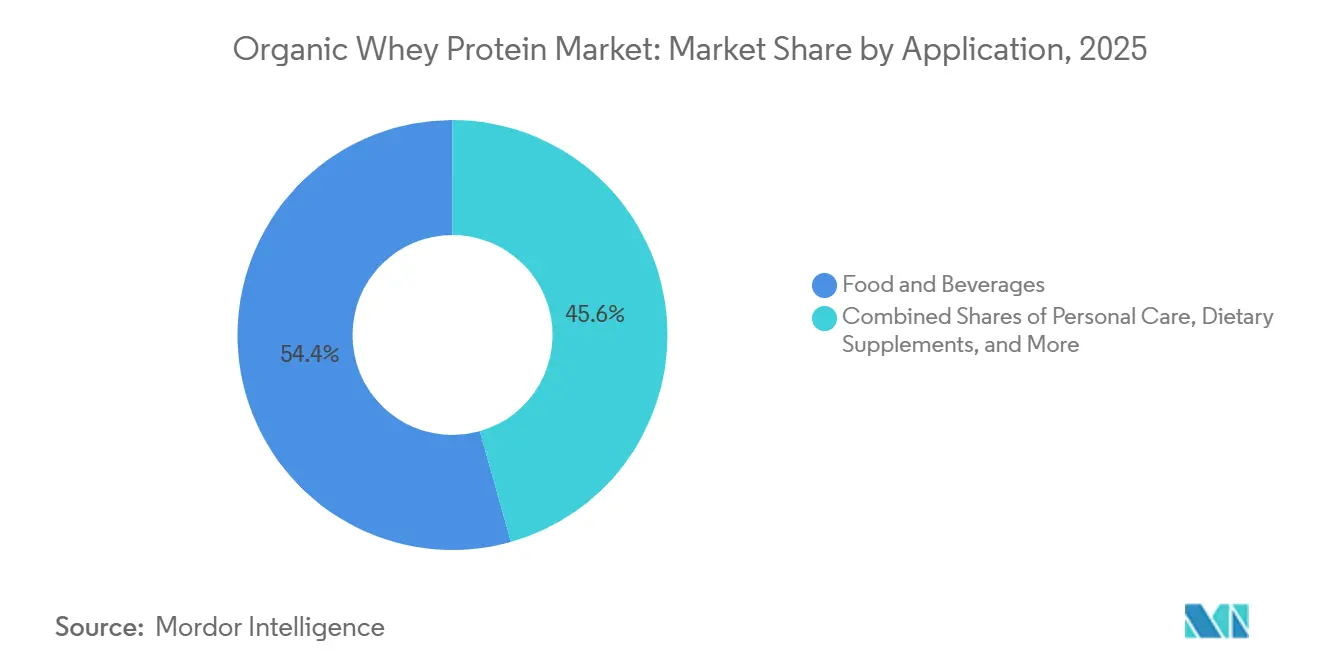

- By application, Food and Beverages accounted for 54.38% share of the organic whey protein market in 2025, while Sports Nutrition and Dietary Supplements is advancing at an 8.24% CAGR through 2031.

- By geography, North America held 42.38% share of the organic whey protein market in 2025, while Asia-Pacific recorded the highest projected CAGR at 8.02% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Organic Whey Protein Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumer Preference for Clean-Label Nutrition Products | +1.8% | Global, concentrated in North America and Western Europe | Short term (≤ 2 years) |

| Increasing Sports Nutrition and Active Lifestyle Trends | +1.5% | North America, Europe, APAC (China, India, Australia) | Short term (≤ 2 years) |

| Expansion of Functional Food and Beverage Applications | +1.2% | Global, with FMCG-led growth in North America and Europe | Medium term (2-4 years) |

| Rising Health and Wellness Awareness | +0.9% | Global, increasingly APAC and South America | Medium term (2-4 years) |

| Growing Demand for Grass-Fed and Sustainably Sourced Dairy Ingredients | +0.8% | North America, Europe (Germany, Netherlands, Ireland, NZ) | Medium term (2-4 years) |

| Increasing Adoption in Infant and Clinical Nutrition Products | +0.6% | APAC core (China, India), spill-over to MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Preference for Clean-Label Nutrition Products

Consumer demand for ingredient transparency is changing procurement decisions from the shelf level back to ingredient sourcing. A 2025 Clean Label Project study found that 47% of tested protein powders exceeded safe lead thresholds, which is pushing more buyers toward USDA-certified organic and third-party-tested products with clearer provenance[1]Source: Clean Label Project, “Protein Powder Study Whitepaper,” Clean Label Project, cleanlabelproject.org. State-level disclosure pressure is also increasing scrutiny around supplement safety and is raising the value attached to documented ingredient chains. This dynamic strengthens the organic whey protein market because suppliers with organic status, traceability systems, and recognized quality certifications are becoming easier for premium retailers to approve. The result is a stronger premium tier where buyers are paying more attention to restricted inputs, origin claims, and testing discipline than they did in earlier protein cycles.

Increasing Sports Nutrition and Active Lifestyle Trends

Sports nutrition demand is moving beyond competitive athletes and is bringing the organic whey protein market into more routine daily-use occasions. In China, the sports nutrition protein market reached USD 9.3 billion, in 2025, and whey held 70.4% of sports protein sales volume. The fastest shift in protein powder consumption came from adults aged 50 and above, whose share rose from 10.9% to 31.5%, which supports demand for cleaner and easier-to-digest formats. In the United States, whey represented 55.2% of protein powder sales in 2024 and generated USD 2.71 billion, showing the category kept its lead over plant-based alternatives. Producers are responding with new protein capacity, and Fonterra's first WPC production runs at Studholme in 2026 show that large dairy groups expect sustained demand for premium protein ingredients

Expansion of Functional Food and Beverage Applications

Food manufacturers are increasingly incorporating whey protein into bakery products, dairy items, snack bars, and ready-to-drink (RTD) beverages. This approach not only enhances the protein content of these products but also aligns with the growing consumer demand for clean-label offerings. In 2025, Arla Foods Ingredients reported a significant 29% increase in sales of protein ingredients, primarily driven by their application in RTD coffee and protein drinks. Additionally, premium RTD yogurts containing 20g or more of protein experienced an impressive 65% year-on-year growth. By 2026, RTD protein drinks in the United States recorded a 10% growth, highlighting the broadening appeal of protein-enriched products across everyday food and beverage categories. As consumer expectations for purity in food applications continue to rise, suppliers capable of delivering consistently certified materials are better positioned to secure opportunities within premium formulation pipelines.

Growing Demand for Grass-Fed and Sustainably Sourced Dairy Ingredients

Grass-fed and sustainably sourced dairy inputs have become a stronger differentiator inside the organic whey protein market because buyers increasingly connect pasture access and traceability with product quality. Germany's organic food market reached EUR 18.23 billion in 2025, and dairy was among the stronger categories in that expansion BÖLW. EU Organic Regulation 2018/848 has tightened operating discipline around pasture access, feed traceability, and inspection procedures, which raises the value of well-established certified milk pools[2]Source: European Commission, “Regulation (EU) 2018/848 on Organic Production and Labelling of Organic Products,” EUR-Lex, eur-lex.europa.eu. Fonterra's move to expand South Island organic milk processing, with a target of 4 to 5 million kg MS from the 2028/29 season and a 2025/26 organic milk price midpoint of NZD 14.00 per kg MS, shows long-term confidence in organic price premiums. These pricing signals keep raw material supply tight and help preserve premium positioning for processors that have already secured certified milk agreements.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production and Procurement Costs | -1.2% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Stringent Organic Certification Requirements | -0.8% | Global, most acute for new entrants in APAC and South America | Medium term (2-4 years) |

| Supply Chain Constraints in Organic Dairy Production | -0.6% | Europe (Germany, Netherlands), North America | Medium term (2-4 years) |

| Competition from Plant-Based Protein Alternatives | -0.4% | North America, Europe, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Production and Procurement Costs

High production and procurement costs remain the most immediate restraint on the organic whey protein market. The broader whey protein supply crisis kept price pressure elevated through 2025 and 2026, and contract conditions showed that the squeeze had not eased in the near term. Organic variants face an additional cost layer because certified feed, mandatory pasture access, and restricted processing inputs keep organic WPI cost structures 40% to 60% above conventional equivalents before sustainability premiums are applied. This creates margin pressure for smaller brands when consumers resist shelf-price increases, and it can delay organic reformulation decisions for B2B food manufacturers facing commodity cost pressure. Even with new investments in global whey capacity, meaningful relief is not expected before Q3 2027, so near-term volatility is likely to remain part of the operating environment.

Competition from Plant-Based Protein Alternatives

Plant-based proteins remain a live competitive pressure, even though they are not the main reason the organic whey protein market is constrained in 2026. Plant-based protein dollar sales fell 7.3% year-on-year in 2024 and unit sales fell 5.7%, which shows that first-generation products lost momentum at retail. The longer-term issue is precision fermentation, which targets buyers who want whey functionality without animal-based sourcing. That alternative proposition overlaps with some premium protein demand and can become more relevant if taste, texture, and scaling continue to improve. For now, the threat is more medium to long term than immediate, but it still shapes how suppliers in the organic whey protein market think about future differentiation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Isolate Dominates, Hydrolysate Signals the Premium Shift

Whey Protein Isolate held 45.21% of the organic whey protein market share in 2025, which kept it in the lead across product types. Its position came from high purity, lower lactose content, and a strong fit with premium sports nutrition, infant formula, and RTD beverage uses. The membrane filtration route also aligns well with organic processing rules because it relies on separation methods that fit more naturally within certified handling systems. Whey Protein Concentrate stayed relevant as the more accessible option for baked goods, dairy products, and formulations that balance function with cost.

Whey Protein Hydrolysate is the fastest-growing product type, and its organic whey protein market size is projected to advance at 8.55% CAGR through 2031. That pace reflects the extra digestibility and rapid absorption valued in clinical nutrition, premium sports nutrition, and sensitive-use applications. Hydrolysates also face a tighter supply base because enzymatic processing must remain within certified organic conditions, which raises the technical barrier for newer suppliers. As a result, established processors with verified capability are in a better position to defend premium pricing than suppliers focused mainly on concentrate volumes.

By Form: Powder's Scale Advantage Intact as Liquid Formats Accelerate

Powder accounted for 75.48% of the organic whey protein market in 2025 and remained the clear scale format. That lead came from lower freight risk, longer shelf life, and consumer familiarity across tubs, sachets, and bulk ingredient formats. Mature logistics also make powder easier to move through retail, e-commerce, and B2B food manufacturing channels. These strengths keep powder as the format with the widest commercial reach even as other forms continue to gain traction.

Liquid formats are projected to expand at 8.11% CAGR through 2031, which puts them ahead of powder on growth. That momentum is tied to RTD protein beverages and ultra-filtered dairy products that turn protein consumption into a more frequent and convenient purchase. Organic Valley's March 2026 national launch of Protein Plus, with 50% more protein and 50% less sugar than regular milk, showed how mainstream organic dairy brands are pushing liquid protein into national retail channels. Better aseptic processing and broader chilled distribution are also making liquid formats easier to scale across the organic whey protein market.

By Application: Food and Beverages Anchors Demand as Sports Nutrition Accelerates

Food and Beverages accounted for 54.38% of the organic whey protein market size in 2025, giving this application the widest revenue base. Its lead reflects the ingredient's versatility across bakery, beverages, dairy, snacks, and other reformulated food products. That breadth lowers dependence on standalone supplement demand and gives suppliers exposure to several premium food categories at once. Personal Care and Cosmetics remained smaller, but traceable whey peptides are drawing attention where brands want ingredient stories tied to provenance and function.

Sports Nutrition and Dietary Supplements is projected to grow at 8.24% CAGR through 2031, which is the fastest pace among applications. Demand is being reinforced by broader protein use beyond athletes and by consumers who need high-quality protein support during weight management. Clinical and medical nutrition also carries strategic importance because high-digestibility protein is becoming more relevant in aging-related care settings. Quality and compliance frameworks in more sensitive applications raise the bar for suppliers and favor companies that can document consistency across the full processing chain.

Geography Analysis

North America held 42.38% of the organic whey protein market share in 2025, with the United States as the main contributor. The region benefits from mature supplement retail, strong natural grocery distribution, and a large base of premium dairy processing. Organic compliance rules keep documentation burdens high, yet they also reward processors that already control traceable feed and milk networks. Canada and Mexico add incremental demand, but the United States remains the central procurement and product development hub for the regional business. Competitive pressure is also highest in North America because branded specialists and large ingredient groups are both competing for premium shelf space and B2B contracts.

Europe remained the second-largest regional block in the organic whey protein market, supported by Germany, the Netherlands, Ireland, and the United Kingdom. Germany's organic food market reached EUR 18.23 billion in 2025, and dairy was among the stronger organic categories[3]Source: Bund Ökologische Lebensmittelwirtschaft, “Umsatzentwicklung, Absatz und Importe Beim Deutschen Bio-Markt,” BÖLW, boelw.de. German organic milk pricing reflected the same tight supply conditions that support whey premiums across the region. The June 2026 Arla Foods and DMK merger, together with Arla's acquisition of Volac's whey nutrition business in Wales, increased processing scale and certification reach for European supply Organic Regulation 2018/848 continues to tighten compliance expectations, which tends to shift volume toward larger cooperatives that can absorb inspection and traceability costs.

Asia-Pacific is the fastest-growing geography in the organic whey protein market, with an 8.02% CAGR projected through 2031. China and India are driving much of that momentum through premium nutrition demand, tighter labeling expectations, and broader use of whey in sports nutrition and infant-related categories. In China, dairy imports including whey grew 3.5% in volume and 14.8% in value in January to September 2025, and high-end products led that increase. South America and the Middle East and Africa still account for smaller shares, but Brazil's rising middle class and GCC health-focused investment give the organic whey protein market a longer runway beyond the current forecast window.

Competitive Landscape

The organic whey protein market is moderately consolidated at the ingredient processing tier, where Glanbia plc, Arla Foods amba, Fonterra Co-operative Group, Lactalis Ingredients, and Carbery Group hold the strongest positions. The branded consumer layer is more fragmented, with Organic Valley, The Organic Protein Co., Natural Force Benefit Co., and Puori ApS competing on certification depth, traceability, flavor, and direct-to-consumer execution. This split means scale matters most in milk sourcing and filtration, while brand equity matters more in retail conversion and repeat purchase. Entry remains difficult because certified milk pools take time to build and organic handling systems require process discipline across the full chain. That keeps the organic whey protein market open to niche brands, but it limits the number of companies that can scale ingredient supply quickly.

Arla's June 2026 merger with DMK and its related acquisition of Volac's whey nutrition business in Wales were major scale moves that lifted European whey capacity and widened contract fulfillment ability. Glanbia confirmed a 10-million-pound WPI capacity expansion through the Southwest Cheese joint venture in New Mexico, with commissioning targeted for 2027. Fonterra started WPC production runs at its expanded Studholme facility in 2026, which showed continued investment in protein ingredients for global demand. Organic Valley launched Protein Plus nationally in March 2026, using a mainstream retail push to extend organic protein into more frequent-use liquid dairy occasions. These moves show that competition in the organic whey protein market now centers on certified supply access, processing scale, and formats that widen consumption frequency.

A smaller white space sits where organic certification and hydrolysate capability overlap, because few suppliers can manage both at commercial scale. That technical barrier is especially relevant for clinical nutrition and infant formula customers, where digestibility, documentation, and consistency all matter. Smaller brands can still compete when they focus on narrow channels and high-certification propositions rather than broad distribution. Overall rivalry is active, but advantage stays with companies that can pair trusted sourcing stories with repeatable processing and enough scale to stay in stock.

Organic Whey Protein Industry Leaders

Glanbia plc

Arla Foods amba

Fonterra Co-operative Group Ltd

Agropur Ingredients

Groupe Lactalis

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: FrieslandCampina announced an investment program exceeding €90 million to expand its high-value whey protein business and optimize its ingredients production network across the Netherlands. The investment includes technological upgrades at its Bedum, Veghel, and Workum facilities.

- November 2025: Tirlán announced a €126 million investment in a state-of-the-art whey processing facility at its Ballyragget site in Kilkenny, Ireland. The new facility will expand the company's whey processing and product innovation capabilities, focusing on advanced nutritional whey protein products, including clear whey protein isolate for sports nutrition, lifestyle beverages, infant formula, and medical nutrition applications.

- November 2024: Arla Foods Ingredients launched Lacprodan DI-3092, a new whey protein hydrolysate designed for peptide-based medical nutrition applications. The ingredient enables manufacturers to formulate medical nutrition beverages with up to 10g of high-quality protein per 100ml, significantly higher than conventional formulations, while delivering improved taste and reduced bitterness.

Global Organic Whey Protein Market Report Scope

| Whey Protein Isolate |

| Whey Protein Concentrate |

| Whey Protein Hydrolysate |

| Powder |

| Liquid |

| Food and Beverages | Bakery |

| Beverages | |

| Dairy and Dairy Alternatives | |

| Meat and Meat Alternatives | |

| Snacks | |

| Others | |

| Sports Nutrition and Dietary Supplements | |

| Personal Care and Cosmetics | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| Product Type | Whey Protein Isolate | |

| Whey Protein Concentrate | ||

| Whey Protein Hydrolysate | ||

| Form | Powder | |

| Liquid | ||

| Application | Food and Beverages | Bakery |

| Beverages | ||

| Dairy and Dairy Alternatives | ||

| Meat and Meat Alternatives | ||

| Snacks | ||

| Others | ||

| Sports Nutrition and Dietary Supplements | ||

| Personal Care and Cosmetics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is driving growth in organic whey protein through 2031?

Growth is being supported by clean-label demand, wider sports nutrition use, and stronger food and beverage reformulation activity. The category is projected to rise from USD 1.08 billion in 2026 to USD 2.75 billion by 2031 at a 7.02% CAGR.

Which product type leads current demand?

Whey Protein Isolate leads with 45.21% share in 2025 because it fits premium needs around purity, lower lactose, and broader use in sports nutrition and RTD products.

Why does Food and Beverages hold the largest application share?

Food and Beverages accounts for 54.38% in 2025 because organic whey is now used across bakery, dairy, snacks, and beverages, which gives suppliers a broader base than supplements alone.

How concentrated is competition among suppliers?

The ingredient side is moderately consolidated around a few large dairy processors, while the branded consumer side remains fragmented, so scale matters in sourcing and filtration more than it does in brand positioning alone.

Page last updated on: