Hydrolyzed Whey Protein Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 150.58 Million |

| Market Size (2031) | USD 203.86 Million |

| Growth Rate (2026 - 2031) | 6.25% CAGR |

| Fastest Growing Market | North America |

| Largest Market | North America |

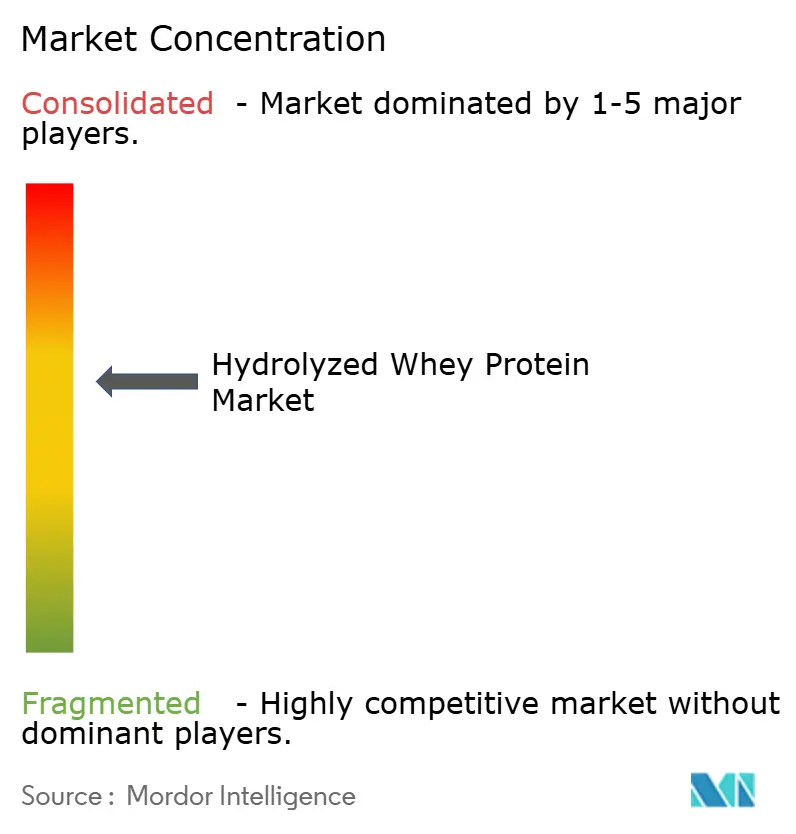

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hydrolyzed Whey Protein Market Analysis by Mordor Intelligence

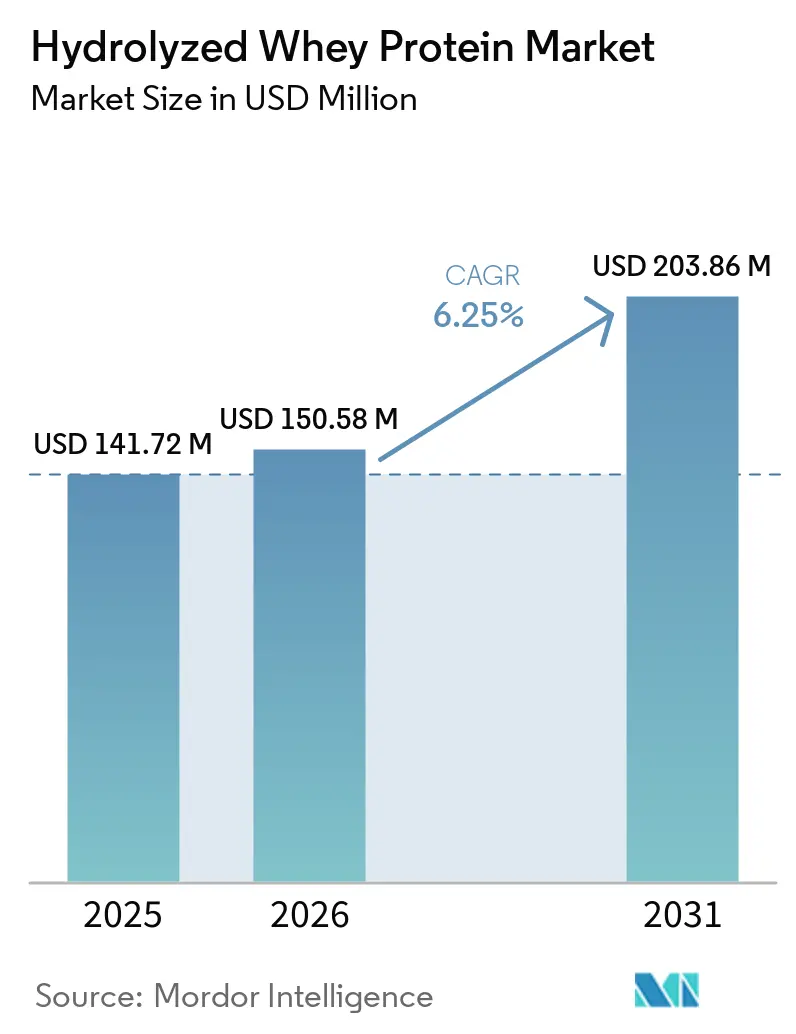

The hydrolyzed whey protein market size was valued at USD 141.72 million in 2025 and estimated to grow from USD 150.58 million in 2026 to reach USD 203.86 million by 2031, at a CAGR of 6.25% during the forecast period (2026-2031). The market's growth is driven by increasing consumer awareness regarding health and fitness, coupled with the rising demand for high-protein dietary supplements. Additionally, the expanding application of hydrolyzed whey protein in sports nutrition, infant formula, and clinical nutrition further fuels its adoption. The growing prevalence of lifestyle-related diseases, such as obesity and diabetes, has also led to a surge in demand for functional foods and beverages, where hydrolyzed whey protein plays a significant role. Furthermore, the market benefits from advancements in production technologies, which have improved the efficiency and quality of hydrolyzed whey protein products. The increasing preference for clean-label, organic, and sustainable food products is another factor propelling market growth. Key players in the industry are focusing on product innovation and strategic partnerships to cater to the evolving consumer demands.

Key Report Takeaways

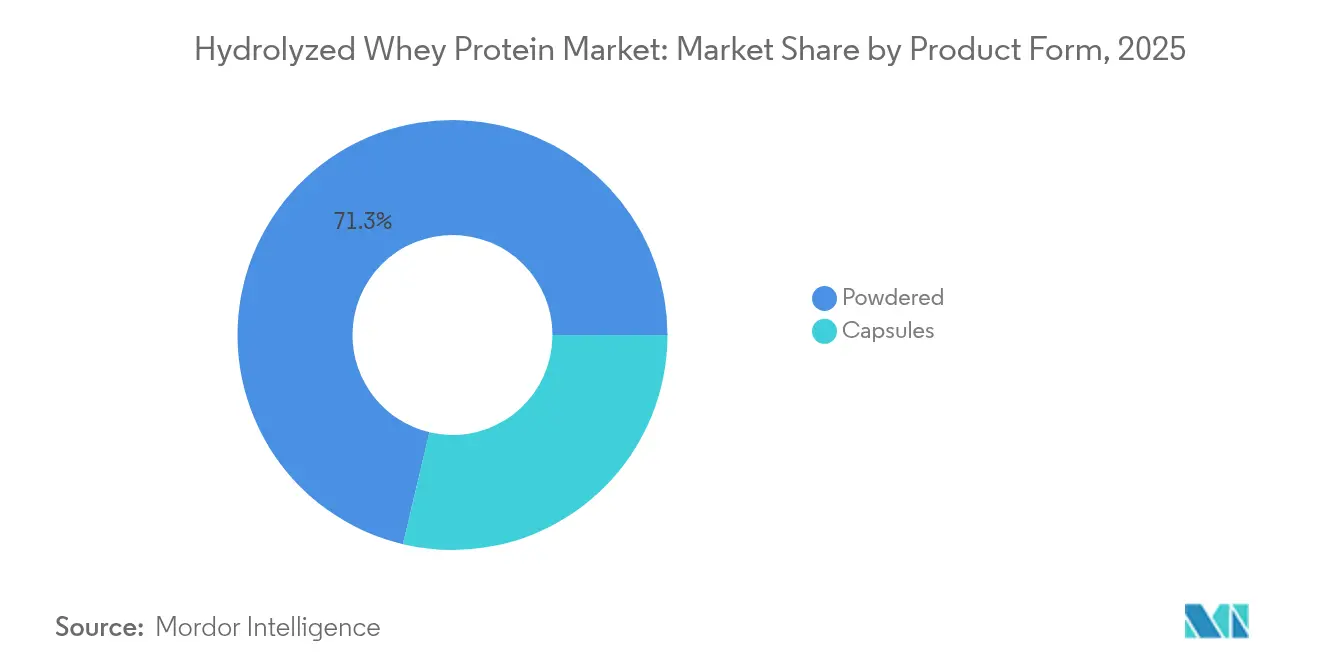

- By product form, powdered variants led with 71.30% revenue share in 2025; capsulated formats are projected to record the highest CAGR at 8.00% through 2031.

- By degree of hydrolysis, low-DH products accounted for 51.20% of the hydrolyzed whey protein market share in 2025, while high-DH products are expected to expand the fastest at an 7.7% CAGR to 2031.

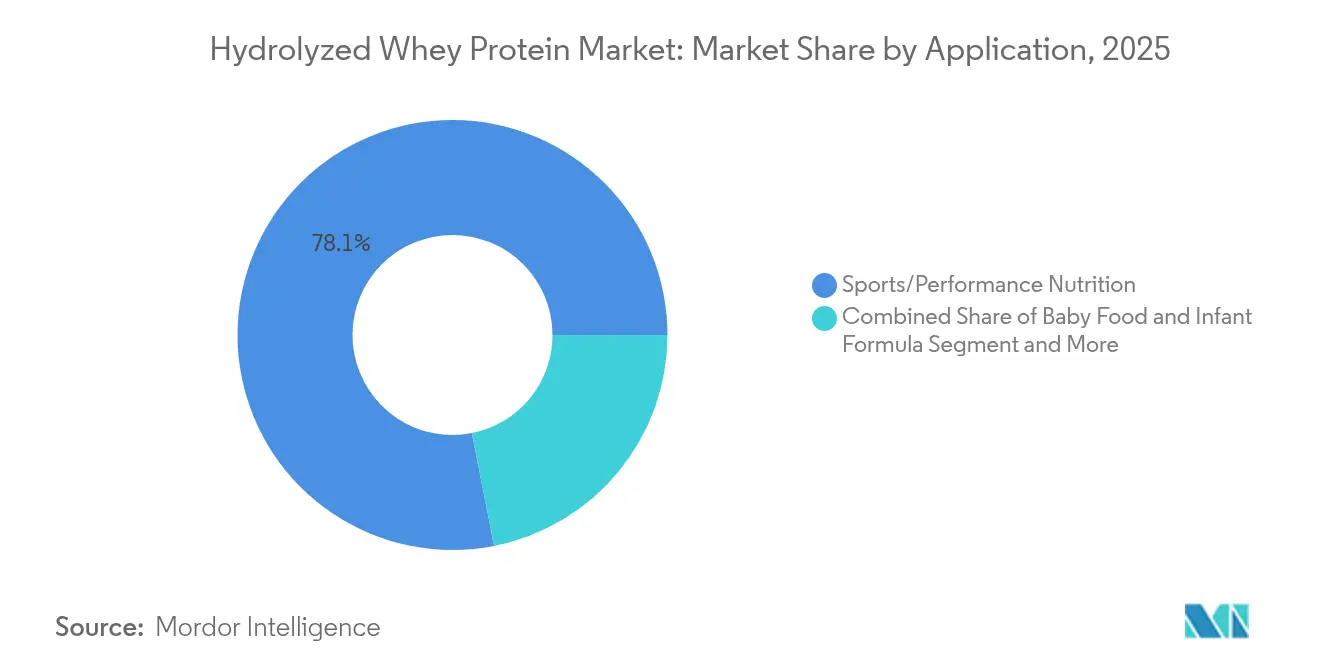

- By application, sports/performance nutrition commanded 78.10% of the hydrolyzed whey protein market size in 2025 and is set to progress at a 7.05% CAGR through 2031.

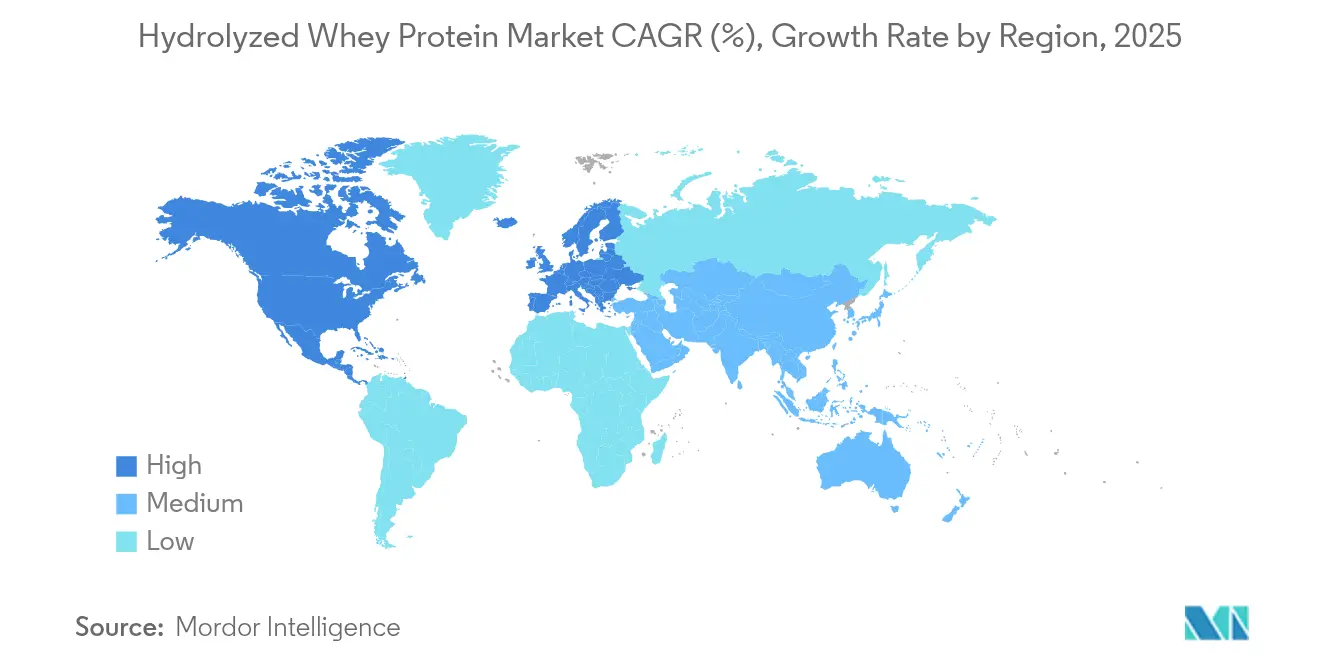

- By geography, North America held 56.30% of global revenue in 2025 and is forecast to grow at 7.02% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hydrolyzed Whey Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hypo-Allergenic Infant-Formula Boom | +1.2% | Global, with early gains in North America, Europe | Medium term (2-4 years) |

| Growing Demand in Sports Nutrition | +1.8% | North America and Europe core, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Growing Demand from Clinical Nutrition and Elderly Population for Muscle Health | +1.5% | Global, concentrated in aging populations | Long term (≥ 4 years) |

| Growing Application Functional Food and Beverage | +0.9% | Asia-Pacific core, expansion to global markets | Medium term (2-4 years) |

| Trend Toward Clean-Label Products | +0.7% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Rising Health and Fitness Consciousness | +0.8% | Global, with strongest growth in urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hypo-Allergenic Infant-Formula Boom

The increasing demand for hypoallergenic infant formulas is a significant driver in the hydrolyzed whey protein market. These formulas, designed to reduce the risk of allergic reactions in infants, are gaining traction among parents seeking safer and more suitable nutritional options for their children. Hydrolyzed whey protein, a key ingredient in these formulas, is processed to break down proteins into smaller peptides, making it easier for infants to digest and less likely to trigger allergies. The rising awareness of infant allergies and the growing prevalence of conditions such as cow's milk protein allergy (CMPA) are further fueling the adoption of hypoallergenic formulas. Additionally, healthcare professionals increasingly recommend these products, reinforcing their credibility and boosting market growth. Regulatory approval momentum is also accelerating the adoption of protein hydrolysates in infant nutrition. For instance, in July 2024, Arla Foods Ingredients received FDA clearance for four whey protein hydrolysates, marking the first such authorization for allergy management applications [1]Source: U.S.Food and Drug Administration, "FDA confirms Arla Foods Ingredients’ whey protein hydrolysates can be used in infant formula", www.fda.gov. This regulatory milestone is expected to further drive innovation and expansion in the hydrolyzed whey protein market as parents prioritize the health and well-being of their infants.

Growing Demand in Sports Nutrition

The growing demand for sports nutrition is a significant driver in the hydrolyzed whey protein market. Consumers are increasingly focusing on fitness and health, leading to a rise in the consumption of sports nutrition products. Hydrolyzed whey protein, known for its rapid absorption and high bioavailability, has become a preferred choice among athletes and fitness enthusiasts. This trend is further fueled by the increasing awareness of the benefits of protein supplements in muscle recovery, performance enhancement, and overall health. Additionally, the expansion of the fitness industry, coupled with the rising popularity of gym culture and sports activities, has amplified the demand for hydrolyzed whey protein. The product's ability to cater to the specific nutritional needs of active individuals positions it as a key component in the sports nutrition segment. Furthermore, the growing prevalence of lifestyle-related health issues, such as obesity and diabetes, has encouraged consumers to adopt healthier dietary habits, including the incorporation of protein-rich products like hydrolyzed whey protein.

Growing Demand from Clinical Nutrition and Elderly Population for Muscle Health

The hydrolyzed whey protein market is experiencing significant growth, driven by increasing demand from clinical nutrition applications and the aging population seeking improved muscle health. Hydrolyzed whey protein, known for its rapid absorption and high bioavailability, is widely utilized in clinical nutrition to support recovery, manage malnutrition, and enhance overall health outcomes. It is particularly beneficial for patients recovering from surgeries, illnesses, or injuries, as it aids in faster tissue repair and muscle regeneration. Furthermore, the elderly population, which is more prone to muscle loss and sarcopenia, is increasingly adopting hydrolyzed whey protein as a dietary supplement to maintain muscle mass, improve physical performance, and reduce the risk of falls and fractures. The rising prevalence of age-related conditions, coupled with growing awareness of the importance of muscle health in overall well-being, is further fueling the adoption of hydrolyzed whey protein. Additionally, healthcare professionals and nutritionists are increasingly recommending hydrolyzed whey protein for its superior digestibility and ability to meet the protein requirements of individuals with compromised digestive systems, such as the elderly or critically ill patients.

Trend Toward Clean-Label Products

The growing consumer preference for clean-label products is a significant driver in the hydrolyzed whey protein market. Consumers are increasingly seeking products with transparent ingredient lists, minimal processing, and no artificial additives. This trend is fueled by rising health awareness, the increasing prevalence of lifestyle-related diseases, and the demand for natural and organic products. Hydrolyzed whey protein, known for its high nutritional value, digestibility, and suitability for various dietary needs, aligns well with these preferences. Additionally, the clean-label movement is gaining traction across multiple demographics, including fitness enthusiasts, health-conscious individuals, and those with dietary restrictions, further boosting the demand for hydrolyzed whey protein. Research from CBI, the Ministry of Foreign Affairs, indicates that clean-label products are set to rise from 52% of portfolios in 2021 to over 70% by 2025 and 2026 [2]Source: CBI Ministry of Foreign Affairs, "Which trends offer opportunities," www.cbi.eu. This data highlights the growing importance of clean-label offerings in shaping consumer purchasing decisions. Manufacturers are responding by reformulating products to meet clean-label standards, incorporating innovative processing techniques, and ensuring compliance with regulatory requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of Alternative Protein Sources | -1.1% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Bitterness of High-DH Hydrolysates Limiting its Use | -0.8% | Global, affecting premium applications | Short term (≤ 2 years) |

| High Production Costs | -1.3% | Global, with acute pressure in emerging markets | Long term (≥ 4 years) |

| Milk Allergies and Sensitivities | -0.4% | Developed markets primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availability of Alternative Protein Sources

The availability of alternative protein sources poses a significant restraint to the hydrolyzed whey protein market. Consumers now have access to a wide range of protein options, including plant-based proteins such as pea, soy, and rice protein, as well as other animal-based proteins like egg and collagen. These alternatives often appeal to specific consumer preferences, such as vegan, vegetarian, or allergen-free diets, which can divert demand away from hydrolyzed whey protein. Additionally, advancements in food technology have improved the taste, texture, and nutritional profiles of these alternative proteins, making them more competitive in the market. The growing focus on sustainability and environmental concerns further drives the adoption of plant-based proteins, as they are perceived to have a lower environmental impact compared to animal-derived proteins. This increasing competition from alternative protein sources challenges the growth potential of the hydrolyzed whey protein market, as consumers continue to explore and adopt these substitutes based on their dietary needs and ethical considerations.

Bitterness of High-DH Hydrolysates Limiting its Use

The bitterness associated with high-degree hydrolysis (High-DH) hydrolysates is a significant restraint in the hydrolyzed whey protein market. High-DH hydrolysates are widely recognized for their enhanced digestibility and rapid absorption, making them a preferred choice in various applications, including sports nutrition and clinical nutrition. However, their inherent bitterness poses a challenge to their broader adoption. This bitterness often affects the sensory profile of end products, limiting their appeal to consumers. Manufacturers face difficulties in masking or reducing this bitterness without compromising the nutritional benefits or functional properties of the hydrolysates. Consequently, the bitterness of High-DH hydrolysates restricts their use in applications where taste is a critical factor, such as in ready-to-drink beverages, protein bars, and other consumer-centric products. Addressing this issue remains a key focus area for industry players, as overcoming this restraint could unlock new opportunities in the hydrolyzed whey protein market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Powdered Dominance Drives Market Efficiency

In 2025, powdered hydrolyzed whey protein captures a commanding 71.30% of the market share, thanks to its superior shelf stability, cost-effective transportation, and versatile applications spanning infant formula, sports nutrition, and clinical uses. The segment's dominance is bolstered by manufacturing efficiencies in spray-drying technology, which allow for large-scale production without compromising protein integrity. These efficiencies not only reduce production costs but also ensure consistent quality, making powdered hydrolyzed whey protein a preferred choice for manufacturers and end-users alike. While capsulated forms hold a smaller market share, they are witnessing the fastest growth, projected at an 8.00% CAGR from 2026 to 2031. This surge is fueled by a growing consumer preference for convenient, portion-controlled delivery formats, especially in sports nutrition and dietary supplements. The portability and ease of use of capsulated forms further enhance their appeal, particularly among active individuals and those with busy lifestyles.

Historical growth comparisons highlight a trend towards premiumization, with capsulated formats becoming increasingly popular among health-conscious consumers. These consumers prioritize precise dosing and enhanced bioavailability. Meanwhile, liquid concentrate formats find their niche in medical nutrition, where the need for immediate consumption justifies their higher production costs. Addressing previous challenges, Arla has developed UHT-stable formulations, paving the way for broader adoption of liquid formats. These advancements in UHT technology ensure that liquid concentrates maintain their nutritional integrity and safety during heat treatment, overcoming a significant barrier to their wider acceptance in the market.

By Degree of Hydrolysis: Low-DH Products Balance Function and Taste

In 2025, low-degree hydrolysis products command a 51.20% market share, striking an ideal balance between functionality and taste. These products, commonly used in infant formulas and functional beverages, preserve enough protein structure to minimize bitterness while enhancing digestibility over intact proteins. Their widespread adoption is attributed to their ability to meet the dual demands of nutritional efficacy and consumer preference for palatable options. Meanwhile, high-DH variants, primarily used in clinical nutrition for their superior bioavailability, are witnessing the fastest growth at an 7.7% CAGR through 2031, even if taste is secondary. The increasing prevalence of chronic illnesses and aging populations globally has driven the demand for clinical nutrition products, further boosting the growth of high-DH variants.

Medium-DH products cater to niche markets, especially in sports nutrition, where there's a push for quick absorption without sacrificing flavor. This segment reaps the rewards of advancements in enzymatic processing, allowing for meticulous control over the degree of hydrolysis. For instance, Arla's Lacprodan DI-3092 showcases how refined enzymatic techniques can yield high protein concentrations (10g per 100ml) while ensuring taste remains palatable through careful hydrolysis management. The growing interest in fitness and active lifestyles has also contributed to the demand for medium-DH products, as they align with consumer preferences for effective and enjoyable sports nutrition solutions.

By Application: Sports Nutrition Leads with Clinical Segments Emerging

In 2025, Sports/Performance Nutrition commands a dominant 78.10% market share and is projected to maintain a robust 7.05% CAGR through 2031. This growth underscores its widespread acceptance, not just among elite athletes but also among recreational sports enthusiasts and fitness aficionados. Research reveals that the type of exercise plays a pivotal role in shaping consumption trends, with a notable surge in demand for quickly absorbed protein sources, particularly among those engaged in endurance and strength training. Endurance athletes often prefer protein sources that aid in muscle recovery and energy replenishment, while strength trainers prioritize proteins that support muscle repair and growth, driving innovation in product formulations tailored to these specific needs.

Regulatory nods, like the FDA's recent clearance of Arla's hydrolysates, are bolstering applications in Baby Food and Infant Formula, paving the way for more hypoallergenic product formulations. This regulatory support has encouraged manufacturers to explore advanced protein hydrolysates and other specialized ingredients, enabling the creation of products that address specific dietary needs, such as lactose intolerance and allergies, in infants. Meanwhile, segments like Elderly Nutrition and Medical Nutrition are witnessing a surge, fueled by an aging population and mounting clinical evidence underscoring the importance of protein supplementation in preserving muscle health. The growing focus on healthy aging and the increasing prevalence of age-related muscle loss (sarcopenia) are further propelling demand in these segments, encouraging manufacturers to develop targeted nutritional solutions.

Geography Analysis

In 2025, North America dominates the hydrolyzed whey protein market with a 56.30% market share and is expected to maintain its leadership with a 7.02% CAGR through 2031. This growth is driven by robust regulatory frameworks that ensure product quality and safety, alongside a mature sports nutrition market that continues to expand. Significant capacity investments by key players in the region further strengthen its position, enabling the development of innovative products to meet evolving consumer demands. The increasing adoption of hydrolyzed whey protein in fitness and wellness applications also contributes to the region's sustained growth.

Europe benefits significantly from EFSA regulatory approvals, which enhance consumer trust and facilitate market expansion. The region's well-established infant formula market plays a crucial role, with companies like FrieslandCampina gaining approval for specific protein hydrolysates tailored for infant applications. This regulatory support, combined with a growing focus on health and nutrition, drives the adoption of hydrolyzed whey protein across various end-user industries. Additionally, the rising trend of clean-label and high-protein products further propels market growth in Europe. In the Asia-Pacific region, demand for hydrolyzed whey protein is surging, driven by heightened consumer awareness of protein-rich diets and the effects of globalization. Younger consumers, influenced significantly by social media, are increasingly gravitating towards flavored variants. Additionally, the market is buoyed by smaller packaging formats that cater to regional preferences for convenience and affordability. China and Indonesia have emerged as top global importers of whey powders in 2024, with import values reaching USD 811.09 million and USD 209.53 million, respectively, as reported by ITC Trade Map . Meanwhile, South America and the Middle East and Africa represent emerging markets with significant potential. These regions are witnessing a rise in health consciousness and an expanding middle-class population, creating opportunities for hydrolyzed whey protein manufacturers to tap into new consumer segments.

Competitive Landscape

The hydrolyzed whey protein market, rated at a moderate concentration level of 6 out of 10, demonstrates a balanced competitive environment. This market is shaped by the presence of large dairy processors with integrated supply chains and specialized ingredient manufacturers focusing on high-value applications. The technical complexity of hydrolysis processes creates significant barriers to entry, limiting new participants. However, these complexities also provide opportunities for differentiation, particularly through the development of proprietary enzyme systems and expertise in specific applications, which allow companies to stand out in this competitive landscape.

Market dynamics reveal a bifurcation between two distinct strategies. On one side, volume-focused players prioritize cost efficiency to compete in broader markets. On the other side, specialty producers target high-margin niches by offering customized peptide profiles designed for specific functional benefits. Companies such as Arla Foods and Glanbia are leveraging vertical integration strategies to secure raw material supplies and maintain stringent quality control. This approach ensures consistency and reliability in their production processes, giving them a competitive edge. Meanwhile, smaller players like Carbery Group are concentrating on proprietary hydrolysis technologies that enable the production of unique bioactive peptides, catering to specialized market demands.

Innovation is a key driver in this market, with increased patent activity centered around enzyme systems that address critical challenges. For instance, advancements in enzyme technologies are focused on reducing bitterness, a common limitation of hydrolyzed whey protein, while preserving its functional properties. These innovations aim to expand the applicability of hydrolyzed whey protein across a wider range of products and consumer segments. As a result, the market is witnessing a shift toward solutions that balance functionality and sensory appeal, enabling broader adoption and growth opportunities in the forecast period.

Hydrolyzed Whey Protein Industry Leaders

-

Arla Foods amba

-

Agropur Co-Operative

-

Glanbia PLC

-

Fonterra Co-operative Group Limited

-

Kerry Group PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hilmar Cheese Company inaugurated its USD 600 million production facility in Dodge City, Kansas, featuring advanced cheese and whey processing capabilities with emphasis on sustainability and carbon-neutral operations by 2050.

- November 2024: Arla Foods Ingredients launched Lacprodan DI-3092, a new whey protein hydrolysate for peptide-based medical nutrition offering 10g protein per 100ml while addressing taste challenges through optimized enzymatic processing

- November 2024: Arla Foods Ingredients completed the acquisition of Volac's Whey Nutrition business following UK Competition and Markets Authority approval, significantly enhancing WPI production capabilities and market position.

Global Hydrolyzed Whey Protein Market Report Scope

Hydrolyzed whey protein is whey protein that has been partially pre-digested, making it easier and faster for the body to absorb. This is achieved through a process called hydrolysis, where enzymes break down the protein into smaller peptides. The hydrolyzed whey protein market is segmented into product type, degree of hydrolysis, application and geograohy. Based on product type, the market is segmented into capsulated, and powdered. Based on degree of hydrolysis, the market is segmented into low, medium and high. Based on application, the market is segmented into RTE/RTC food products, sport performance nutrition, baby food and infant formula, elderly nutrition and medical nutrition and personal care and cosmetics. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, market sizing and forecast have been done based on value (USD million).

| Capsulated |

| Powdered |

| Low |

| Medium |

| High |

| RTE/RTC Food Products |

| Sport/Performance Nutrition |

| Baby Food and Infant Formula |

| Elderly Nutrition and Medical Nutrition |

| Personal Care and Cosmetics |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Form | Capsulated | |

| Powdered | ||

| By Degree of Hydrolysis | Low | |

| Medium | ||

| High | ||

| By Application | RTE/RTC Food Products | |

| Sport/Performance Nutrition | ||

| Baby Food and Infant Formula | ||

| Elderly Nutrition and Medical Nutrition | ||

| Personal Care and Cosmetics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the hydrolyzed whey protein market?

The hydrolyzed whey protein market stood at USD 150.58 million in 2026 and is projected to reach USD 203.86 million by 2031.

Which application segment holds the highest share?

Sports/performance nutrition leads with 78.10% revenue share, reflecting widespread consumer adoption and premium pricing.

Why are high-degree hydrolysates growing faster despite taste issues?

Clinical and medical-nutrition buyers prioritize rapid amino-acid absorption over flavor, pushing high-DH products at an 7.7% CAGR even as processors refine bitterness-masking techniques.

What regulatory changes have propelled infant-formula demand?

The FDA and EFSA both authorized specific whey protein hydrolysates for hypo-allergenic formulas in 2024, opening significant new formulation territory.

Page last updated on: