Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.03 Billion |

| Market Size (2026) | USD 1.09 Billion |

| Market Size (2031) | USD 1.44 Billion |

| Growth Rate (2026 - 2031) | 5.80% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Whey Protein Market Analysis by Mordor Intelligence

The China whey protein market size is expected to grow from USD 1.03 billion in 2025 to USD 1.09 billion in 2026 and is forecast to reach USD 1.44 billion by 2031 at 5.8% CAGR over 2026-2031. This growth is driven by rising demand for sports nutrition, fortified infant formulas, and medical nutrition products. Increasing gym memberships, stricter infant nutrition standards, and a higher prevalence of chronic diseases are boosting demand. However, reliance on imports, feed price fluctuations, and counterfeiting pose challenges. Government efforts to modernize the dairy sector and investments in processing facilities by local and global players are supporting the adoption of whey concentrates, isolates, and hydrolysates. Urbanization, premium product demand, and preference for grass-fed or organic options are driving revenue growth, despite high raw material costs. Capacity expansions by companies like Yili, Mengniu, and global suppliers are reducing import dependency and offering more ingredient options for manufacturers.

Key Report Takeaways

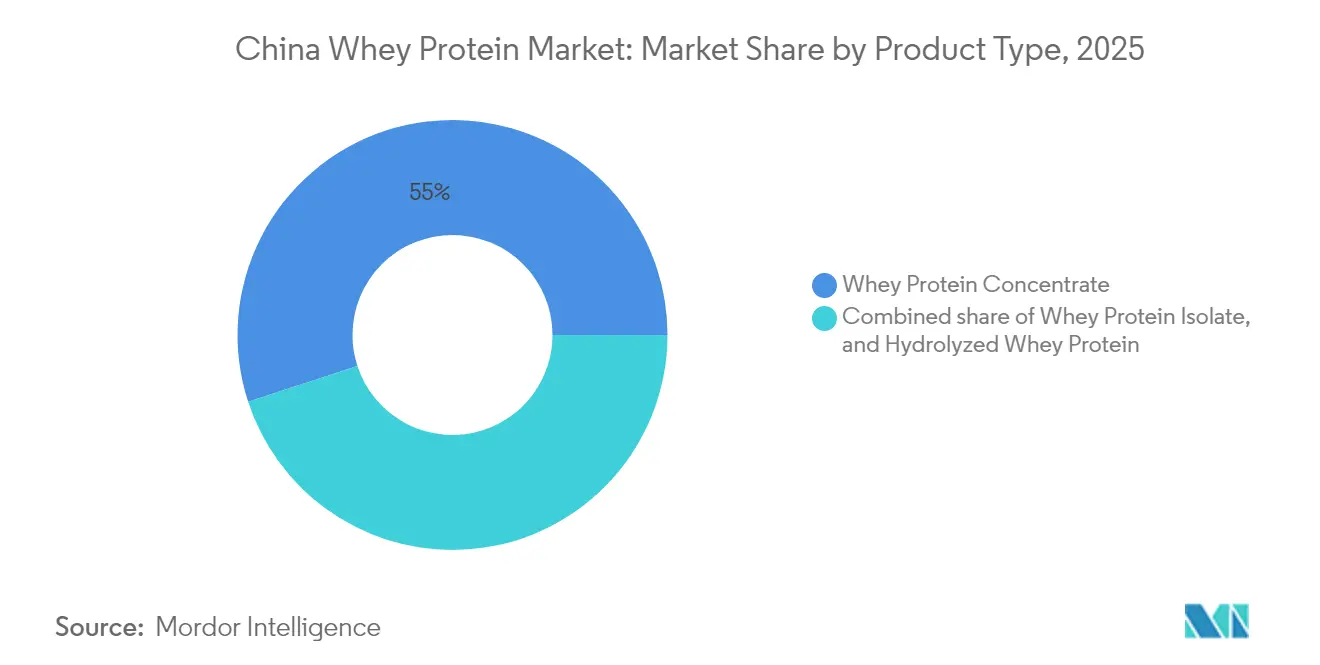

- By product type, whey protein concentrate accounted for 55.02% of China whey protein market share in 2025. and hydrolyzed whey protein is advancing at a 6.93% CAGR through 2031.

- By category, the mass segment held 60.55% of China whey protein market share in 2025, and the premium segment is expanding at a 6.54% CAGR up to 2031.

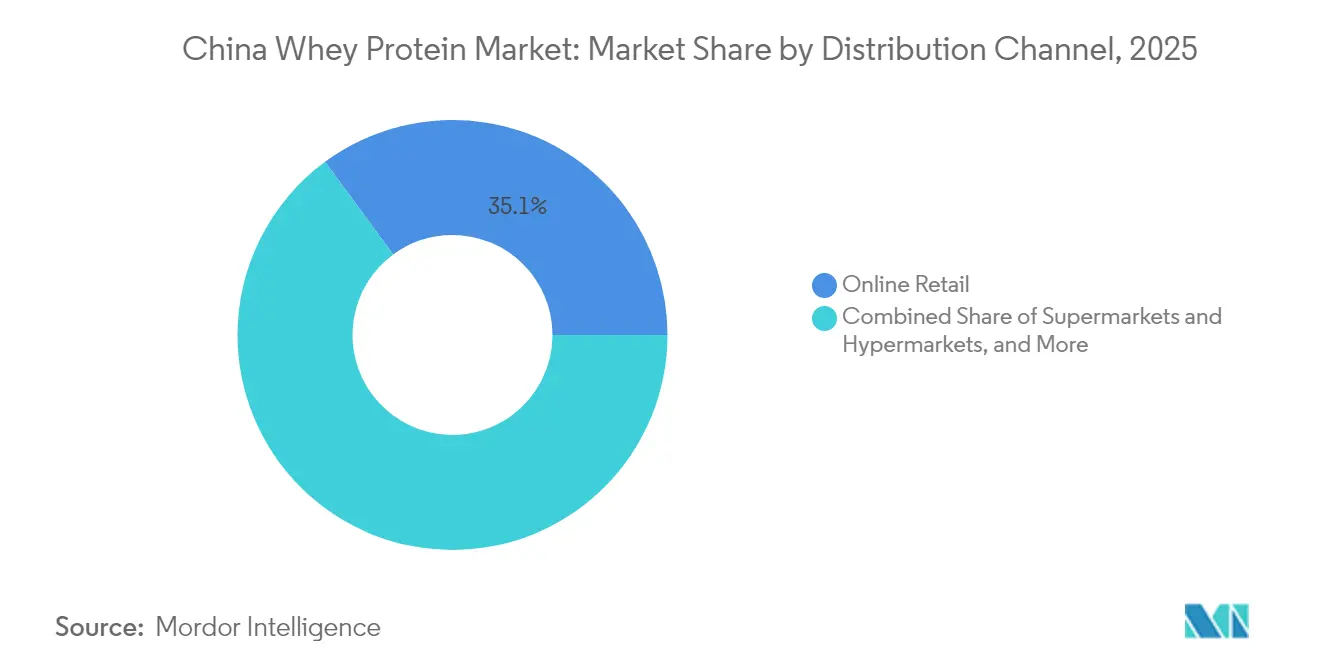

- By distribution channel, nline retail drove 35.10% of China whey protein market size in 2025, and health and wellness stores are projected to grow at a 7.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Whey Protein Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of fitness and gym culture | +1.2% | National, with concentration in tier-one and tier-two cities (Beijing, Shanghai, Guangzhou, Shenzhen) | Medium term (2-4 years) |

| Increasing prevalence of lifestyle diseases | +0.9% | National, higher burden in urban centers and aging provinces (Jiangsu, Zhejiang, Guangdong) | Long term (≥ 4 years) |

| Increasing adoption of whey in infant-nutrition formulas | +1.4% | National, with early gains in premium infant-formula markets (Shanghai, Beijing, Hangzhou) | Short term (≤ 2 years) |

| Government initiatives supporting dairy industry | +1.0% | National, targeted support in Inner Mongolia, Heilongjiang, Ningxia dairy belts | Medium term (2-4 years) |

| Shift toward high-protein, low-carb diets | +0.8% | Urban centers, tier-one and tier-two cities with higher disposable incomes | Medium term (2-4 years) |

| Technological advancements in processing | +0.7% | National, with R&D hubs in Jiangnan University, Northeast Agricultural University regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Fitness and Gym Culture

China's fitness industry is experiencing rapid growth in memberships. By 2024, the country had over 140,000 gyms, including 28,683 fitness clubs and 43,232 fitness studios. In 2023, fitness club memberships reached 69.75 million[1]Shanghai University of Sport, "Number of members in fitness clubs in China from 2017 to 2023", eng.sus.edu.cn. The National Fitness Plan (2021-2025) targets 38.5% regular physical activity participation, boosting demand for sports nutrition products like whey protein powders and ready-to-drink protein beverages. Boutique fitness studios and cross-training centers in tier-one cities are driving this trend by offering nutritional counseling with memberships, increasing demand for premium whey isolates and hydrolysates. At Food Ingredients China 2024, Glanbia Nutritionals introduced high-protein products, including High Protein Acidified Milk (12 grams whey protein) and High Protein Electrolyte Water, catering to post-workout recovery and hydration. Government fitness initiatives and gym expansions are solidifying whey protein's role in the active lifestyle market, with younger consumers (18-35 years) driving e-commerce subscriptions for repeat purchases.

Increasing Prevalence of Lifestyle Diseases

By 2030, China is expected to have around 164 million diabetics aged 20 to 79, according to the International Diabetes Federation[2].International Diabetes Federation, "Estimated number of people with diabetes mellitus in China from 2000 to 2021 with forecasts until 2045", diabetesatlas.org The Global Burden of Disease study ranks China among the top three countries globally for metabolic diseases, with type 2 diabetes closely tied to high body mass index. To tackle this, healthcare providers and policymakers are emphasizing dietary protein for better blood sugar control and weight management. Whey protein, valued for its ability to boost insulin and reduce appetite, is a key focus. The China National Nutrition Plan promotes combining plant and animal proteins to fight malnutrition and chronic diseases, driving regulatory support for whey-based functional foods. Hospitals and clinics are increasingly recommending whey protein isolates for diabetic and pre-diabetic patients, while pharmaceutical-grade whey hydrolysates are being used in Food for Special Medical Purposes (FSMP). With 14% of the population aged 65 and older in 2024, the demand for easily digestible protein sources is growing, positioning hydrolyzed whey as an essential part of clinical nutrition.

Increasing Adoption of Whey in Infant-Nutrition Formulas

The State Administration for Market Regulation has introduced stricter standards, GB 19644-2024 for milk powder and GB 25596-2025 for special medical infant formulas, emphasizing quality and traceability. Manufacturers must now use premium whey protein isolates and hydrolysates with verified origins. Hydrolyzed whey protein, processed to reduce allergens and improve digestion, is mandatory in hypoallergenic infant formulas, supported by clinical evidence of reduced gastric distress and better nitrogen retention. Yili Group's 2024 acquisition of Ausnutria Dairy highlights the growing importance of whey sourcing, as Ausnutria specializes in formulas for premature and lactose-intolerant infants. Fonterra, in partnership with Marathontime, launched a grass-fed whey protein series at the 2024 China International Import and Export Fair, reflecting the demand for certified, premium ingredients in pediatric nutrition. With stricter regulations and rising parental demand for transparency, formulas are shifting to higher whey-to-casein ratios, closely resembling human breast milk.

Government Initiatives Supporting Dairy Industry

In 2024, Beijing's Central Document No. 1 and a notice issued by seven ministries in September focused on stabilizing dairy production. The government set a target to achieve 45 million tonnes of raw milk output by 2025 and introduced subsidies to support the development of cheese and whey processing facilities. Provincial governments in Inner Mongolia, Heilongjiang, and Ningxia extended feed subsidies and insurance programs for dairy farmers. These initiatives aim to reduce fluctuations in raw milk supply and ensure a consistent whey supply for downstream processors. Additionally, the student milk program, which provides dairy products to primary and secondary schools, indirectly supports whey demand. By utilizing surplus milk powder, the program creates a stable market for fortified dairy products. In 2023, China's raw milk production reached 41.97 million tonnes, reflecting a 6.7% year-on-year growth. Fresh milk achieved a 100% quality pass rate, with an average protein content of 3.28 grams per 100 grams. These improvements in milk quality contribute to higher whey protein yields during cheese and casein production.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Quality control and counterfeit issues | -0.6% | National, with higher incidence in tier-three and tier-four cities and e-commerce platforms | Short term (≤ 2 years) |

| Heavy reliance on imports | -0.8% | National, with supply-chain exposure in coastal ports (Shanghai, Ningbo, Shenzhen) | Medium term (2-4 years) |

| Competition from plant-based alternatives | -0.5% | Urban centers, tier-one cities with vegan and flexitarian populations | Medium term (2-4 years) |

| Supply chain vulnerabilities | -0.7% | National, with acute risk in cold-chain logistics and port congestion | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Quality Control and Counterfeit Issues

Counterfeit whey protein products are flooding e-commerce platforms and tier-three cities, shaking consumer trust and diminishing the pricing power of legitimate brands. These counterfeiters are taking advantage of the State Administration for Market Regulation's (SAMR) limited enforcement reach, especially in rural areas where testing facilities are few and far between. While SAMR has ramped up its post-market surveillance—randomly inspecting imported whey protein powders and penalizing mislabeling and adulteration—the vastness of cross-border e-commerce transactions makes traceability a daunting challenge. In response, genuine brands are turning to blockchain-based provenance systems and QR-code verifications to set their products apart. However, these protective measures come with added costs and complexities. The shadow of past scandals looms large: incidents like the 2008 melamine adulteration in dairy products have tainted the domestic perception of whey protein. As a result, many affluent consumers are gravitating towards imported brands that boast third-party certifications like NSF and Informed-Sport. This trend has effectively split the market: a premium segment that prioritizes and pays for verified quality, and a mass segment that remains susceptible to counterfeit threats.

Heavy Reliance on Imports

In 2025, China imported 652,295 tonnes of whey protein, an increase from 626,150 tonnes in 2020[3]UN Comtrade, "Product: 0404 Whey, whether or not concentrated or containing added sugar or other sweetening matter", trademap.org. The United States supplied 42.1% of these imports, while the European Union contributed 30.3%, making the market vulnerable to geopolitical and logistical challenges. The average import price in early 2025 was USD 1,203 per tonne, reflecting the volatility of global dairy commodity prices. Factors such as droughts in New Zealand and rising energy costs in Europe significantly impacted prices for Chinese buyers. Additionally, the Ministry of Commerce launched an anti-subsidy investigation into EU dairy products in August 2024, creating tariff uncertainties that could raise landed costs and disrupt long-term supply agreements. Domestic whey production in China remains limited due to low cheese output, as cheese production is minimal compared to liquid milk and yogurt. This restricts the availability of whey as a by-product. To address this issue, processors are exploring partnerships with cheese manufacturers in regions like Inner Mongolia and Heilongjiang to establish whey extraction facilities near cheese production sites. However, progress is slow due to high capital requirements and a lack of technical expertise. This trade imbalance leaves Chinese buyers exposed to supply disruptions. For instance, in December 2024, port congestion delayed whey shipments, forcing manufacturers to rely on their inventory reserves to meet demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hydrolyzed Whey Gains Clinical Traction

In 2025, Whey Protein Concentrate (WPC) commanded a 55.02% market share, primarily due to its cost-effectiveness. WPC is favored in mass-market protein powders, bakery fortification, and beverages, where a moderate protein purity of 35-80% is adequate. Its processing, typically through ultrafiltration and not ion exchange, is less intensive, leading to competitive pricing. This makes WPC the go-to for domestic brands, especially those catering to price-sensitive consumers in tier-two and tier-three cities. Food manufacturers incorporate WPC into high-protein biscuits, noodles, and dairy drinks.

From 2026 to 2031, Hydrolyzed Whey Protein is projected to grow at a 6.93% CAGR, outpacing both WPC and WPI. Its enzymatic pre-digestion shortens peptide chains, hastening amino acid absorption. This rapid absorption is vital for infant formulas, especially for premature or lactose-intolerant infants. Hydrolyzed whey not only minimizes gastric distress and allergic reactions but also meets the GB 25596-2025 standards for special medical formulas. Sports nutrition brands are increasingly turning to hydrolyzed whey for post-workout recovery products, leveraging its swift leucine delivery to boost muscle protein synthesis.

By Category: Premium Segment Captures Urban Affluence

In 2025, the Mass category captured 60.55% of the market share, buoyed by its affordability and widespread presence in supermarkets, hypermarkets, and online platforms. Priced typically below CNY 200 per kilogram, mass-market whey protein powders cater to gym enthusiasts, students, and middle-income buyers. These consumers seek basic protein supplementation, often forgoing premium certifications or imported origins. Domestic brands lead this segment, capitalizing on localized flavors like red bean, taro, and matcha. They also run aggressive promotional campaigns during events like Singles' Day and the 618 shopping festival. Yet, this segment grapples with margin pressures from counterfeit products and intense price wars. Some manufacturers, in a bid to cut costs, compromise on raw material quality. This not only erodes consumer trust but also fuels a trend of premiumization among more affluent buyers.

The Premium segment is set to expand at a 6.54% CAGR from 2026 to 2031. This growth is driven by urban consumers who are increasingly willing to invest in grass-fed certifications, organic labels, and imported brands that boast third-party testing, such as NSF and Informed-Sport. A testament to this premium positioning strategy is Marathontime's collaboration with Fonterra. They unveiled a grass-fed whey protein series at the 7th China International Import and Export Fair in 2024, aiming at health-conscious consumers who equate New Zealand dairy with top-notch quality and traceability. Similarly, MuscleTech introduced a China-exclusive Longjing Milk Tea flavor whey protein in January 2024. Packaged for the Year of the Dragon, it underscores how premium brands can localize taste preferences while upholding the integrity of imported ingredients. In a strategic move, SAVAS, a renowned Japanese sports nutrition brand, rebranded itself as "Jin Bei Shi" in China in December 2024. They enhanced their whey protein isolate and hydrolyzed whey formulas, boosting protein content and fine-tuning nutritional profiles to cater to the needs of Chinese athletes.

By Distribution Channel: Health Stores Outpace E-Commerce Growth

Online Retail accounted for 35.10% of 2025 distribution share, leveraging Tmall, JD.com, and Pinduoduo's logistics networks and consumer-review ecosystems. E-commerce platforms enable direct-to-consumer models, subscription services, and flash sales that compress distribution costs and accelerate inventory turnover. Cross-border e-commerce facilitates imports of premium whey protein from the United States, New Zealand, and Europe, bypassing traditional importers and offering consumers access to international brands at competitive prices. However, the channel's growth is moderating as market penetration in tier-one cities approaches saturation, and logistics costs rise due to last-mile delivery challenges in rural areas. Counterfeit infiltration on third-party marketplaces remains a persistent issue, prompting platforms to implement stricter seller verification and product authentication protocols.

Health and Wellness Stores are forecast to expand at 7.42% CAGR from 2026 to 2031, the fastest among all distribution channels, driven by specialty chains' expansion into tier-two cities and their ability to offer personalized consultations, product sampling, and loyalty programs. These stores cater to affluent consumers seeking expert guidance on protein supplementation, with staff trained to recommend whey isolates for lactose intolerance, hydrolysates for clinical nutrition, and WPC for general fitness. The channel's growth is amplified by the proliferation of boutique fitness studios, which co-locate with or partner with health stores to create integrated wellness ecosystems. Glanbia Nutritionals' FIC 2024 showcase included concepts for health-store distribution, such as High Protein Immunity Melon Drink and FerriUp lactoferrin-enriched whey for women's iron balance, targeting the specialty retail segment.

Geography Analysis

In China, tier-one cities like Beijing, Shanghai, Guangzhou, and Shenzhen lead whey protein consumption due to higher incomes, advanced fitness infrastructure, and early adoption of Western nutrition trends. These cities act as testing grounds for premium imported brands, with Alibaba Health reporting that international brands dominated China's health supplement market in 2023. Coastal consumers prefer certified origins and third-party testing. Tier-two cities such as Chengdu, Hangzhou, Wuhan, and Nanjing are rapidly growing markets, driven by rising incomes and expanding boutique fitness chains. Fonterra's new Application Center in Wuhan highlights central China's increasing purchasing power and demand for localized products. These cities, with younger, educated populations, are receptive to sports nutrition and benefit from collaborations with institutions like Jiangnan University and Northeast Agricultural University on whey protein applications in functional foods.

China's northern dairy belt, including Inner Mongolia, Heilongjiang, and Ningxia, dominates raw milk production, supported by government subsidies for feed, insurance, and cheese processing (per the September 2024 seven-ministry notice). Inner Mongolia contributed significantly to the 2023 national total of 41.97 million tonnes of raw milk, with a 100% pass rate and 3.28 grams of protein per 100 grams, ensuring high-quality whey yields. Mengniu's Ningxia factory, recognized as a World Economic Forum "Lighthouse Factory" in October 2024, showcases advanced systems that optimize whey extraction and quality control, marking the region's shift to high-value ingredient manufacturing.

Coastal ports like Shanghai, Ningbo, and Shenzhen handle most whey imports, which rose 31.8% year-on-year from January to April 2025, mainly from the U.S. and EU. Cross-border e-commerce enables direct shipments to inland provinces, bypassing distributors and reducing costs. However, tier-three and tier-four cities remain underserved due to high delivery costs and low awareness of whey protein benefits. The Ministry of Commerce's August 2024 anti-subsidy investigation into EU dairy imports may lead to tariff changes, shifting sourcing to Oceania and North America. This could favor southern ports with strong trans-Pacific links. Yili Group's investments in New Zealand, Indonesia, and Thailand strengthen its supply chain, allowing it to source cost-effective whey while maintaining "imported" claims that appeal to Chinese consumers.

Competitive Landscape

The China whey protein market is moderately consolidated, with a mix of global nutrition companies and strong domestic manufacturers shaping competitive dynamics across sports nutrition, functional foods, and clinical nutrition segments. Global players benefit from advanced processing technologies and consistent product quality, while local firms leverage cost-efficient production and proximity to fast-growing consumer clusters. Import regulations and quality standards also influence market structure, giving established suppliers an edge in navigating compliance and building long-term distributor partnerships. Key players in the market include Arla Foods Ingredients Group P/S, Lactalis Group, Royal FrieslandCampina N.V., Glanbia plc, and Fonterra Co-operative Group Limited.

Rising demand for high-protein beverages and healthy snacking is attracting smaller entrants, though most operate at niche levels due to limited scale. Digital retail channels, including cross-border e-commerce, further amplify the visibility of leading brands. As competition intensifies, differentiation is driven by product purity, flavor innovation, and targeted formulations for fitness, weight management, and healthy aging.

Smaller contenders are exploiting niche applications, such as Angel Yeast's July 2024 partnership with ffit8 to launch protein nougat bars, signaling ingredient suppliers' downstream integration into finished snack products. Mengniu's ownership of Bellamy's Organic and its partnership with Danone for high-end dairy products exemplify the use of international brand portfolios to capture premium segments, while its Ningxia factory's October 2024 certification as a World Economic Forum "Lighthouse Factory", the first in China's dairy industry, underscores the role of intelligent manufacturing and sustainability credentials in competitive differentiation.

China Whey Protein Industry Leaders

-

Glanbia plc

-

Fonterra Co-operative Group Limited

-

Arla Foods Ingredients Group P/S

-

Royal FrieslandCampina N.V.

-

Lactalis Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: FrieslandCampina strengthened its global protein position with the acquisition of Wisconsin Whey Protein. The acquisition will enable the company to scale and extend its market-leading position in Europe and Asia (including China) into the North American market.

- June 2023: The State Administration for Market Regulation (SAMR) in China, in collaboration with the National Health Commission (NHC) and the National Administration of Traditional Chinese Medicine, issued an update regarding healthy food raw materials. This update introduced two new raw materials, namely Soybean Protein Isolate and Whey Protein, for use in health food products.

- August 2022: Arla Foods Ingredients intensified its focus on the Chinese market by unveiling a range of innovative whey protein-based ingredient concepts. The company presented these ingredients at the Food Ingredients China (FIC 2022) event held in Guangzhou. These concepts encompassed various categories, including organic dairy, early life nutrition, sports nutrition, and medical nutrition. Among the products launched, Nutrilac Organic milk proteins stood out for their ability to not only enable manufacturers to create organic products but also to reduce whey wastage and generate cost savings in capital expenditure.

China Whey Protein Market Report Scope

Whey protein is a powdered form of protein sourced from whey.

The Chinese whey protein market is segmented by product type and application. By product type, the market is segmented into whey protein concentrate, whey protein isolate, and hydrolyzed whey protein. Based on application, the market is segmented into sports and performance nutrition, infant formula, and functional or fortified food.

For each segment, the market sizing and forecasts have been done based on the value in USD million.

By Product Type

| Whey Protein Concentrate |

| Whey Protein Isolate |

| Hydrolyzed Whey Protein |

By Category

| Mass |

| Premium |

By Distribution Channel

| Online Retail |

| Supermarkets and Hypermarkets |

| Health and Wellness Stores |

| Other Distribution Channels |

| By Product Type | Whey Protein Concentrate |

| Whey Protein Isolate | |

| Hydrolyzed Whey Protein | |

| By Category | Mass |

| Premium | |

| By Distribution Channel | Online Retail |

| Supermarkets and Hypermarkets | |

| Health and Wellness Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

How big is the China whey protein market in 2026?

The market reached USD 1.09 billion in 2026 and is on course to hit USD 1.44 billion by 2031 at a 5.8% CAGR.

Which product type is growing fastest?

Hydrolyzed whey protein leads with a 6.93% forecast CAGR thanks to its rapid absorption and regulatory acceptance in infant and medical nutrition.

What share does online retail hold in whey protein sales?

Online platforms accounted for 35.10% of 2025 sales, leveraging cross-border e-commerce and direct-to-consumer subscriptions.

What drives premiumization in urban areas?

Rising disposable income, demand for grass-fed or organic certification, and concerns over counterfeit goods steer consumers toward higher-priced imported or certified products.

Page last updated on: