North America Luxury Apparel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

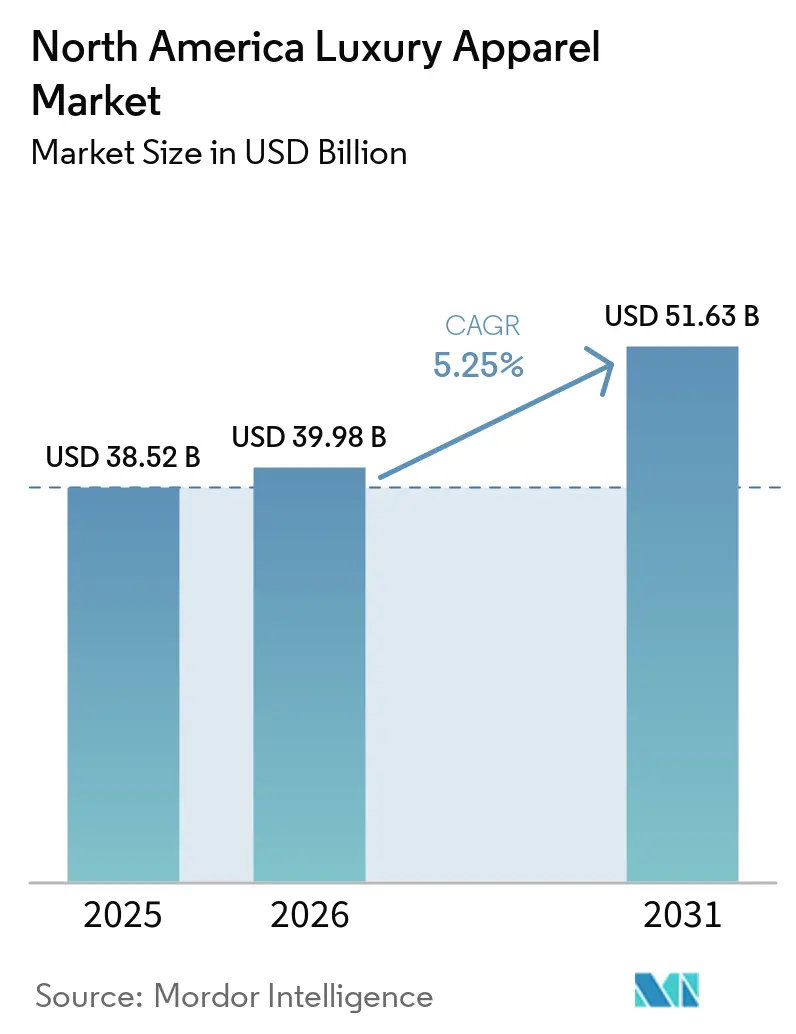

| Base Year Market Size (2025) | USD 38.52 Billion |

| Market Size (2026) | USD 39.98 Billion |

| Market Size (2031) | USD 51.63 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Luxury Apparel Market Analysis by Mordor Intelligence

The North America luxury apparel market size is projected to expand from USD 38.52 billion in 2025 and USD 39.98 billion in 2026 to USD 51.63 billion by 2031, registering a CAGR of 5.3% between 2026 and 2031. The North America luxury apparel market is moving through a steady recovery phase, supported by resilient spending from high-income consumers and sustained demand for premium wardrobe staples. The category mix shows that daily wear has become more important, with elevated basics and premium outerwear shaping assortment priorities across the region. The North America luxury apparel market is also benefiting from stronger omnichannel execution, because specialty stores still lead the channel mix while online retail is expanding faster as brands improve digital storefronts and service tools. The United States remained the anchor geography in 2025, while Canada is set to post the fastest regional growth through 2031. Competition in the North America luxury apparel market remains active across global luxury groups and domestic labels, while counterfeit pressure and rising compliance requirements continue to raise the operating threshold for smaller players.

Key Report Takeaways

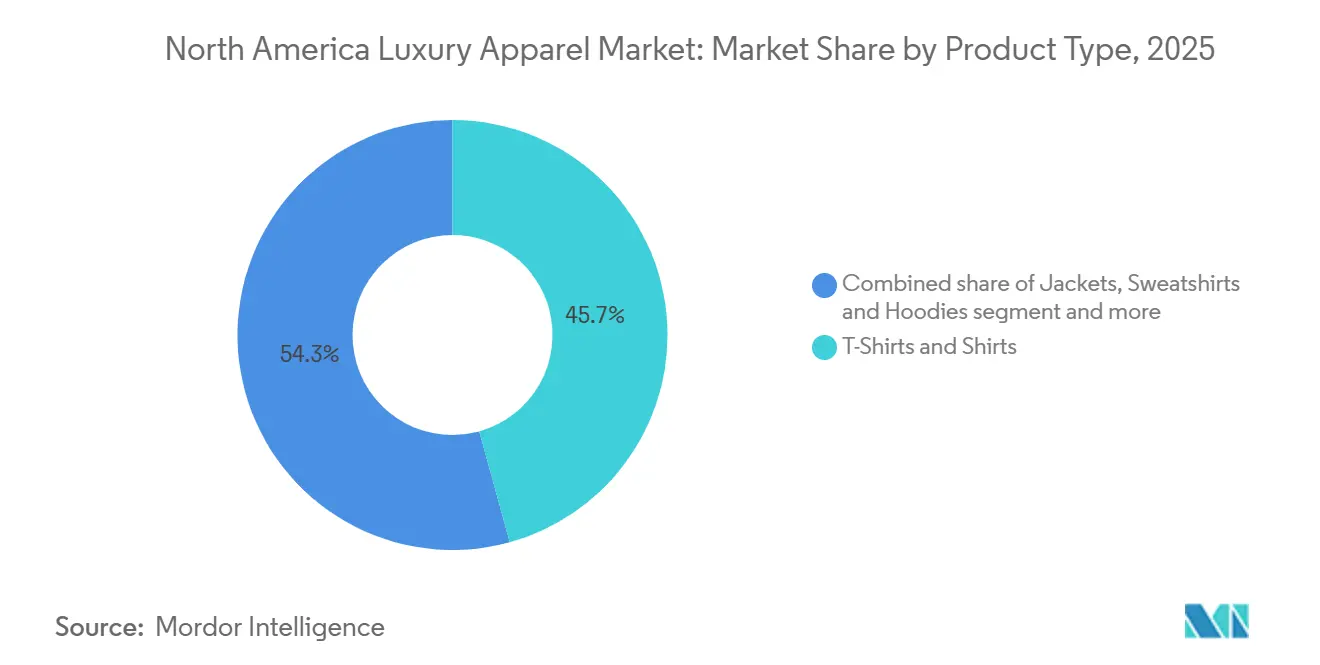

- By product type, T-Shirts and Shirts accounted for the largest share of the apparel market, at 45.71% in 2025, while Jackets, Sweatshirts, and Hoodies are projected to grow at the fastest CAGR of 6.96% during 2026-2031.

- By end purpose, Fashion and Casual accounted for the largest share of the apparel market, at 66.62% in 2025, while Athleisure is projected to grow at the fastest CAGR of 7.01% during 2026-2031.

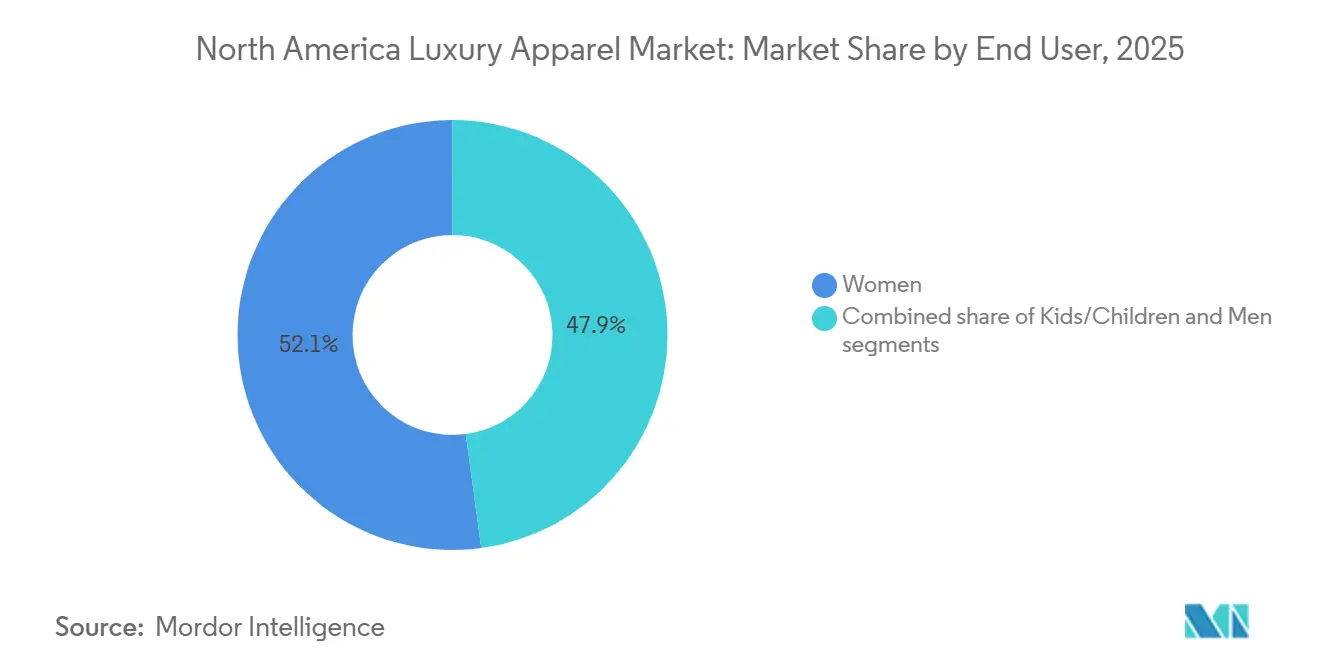

- By end user, Women accounted for the largest share of the apparel market, at 52.13% in 2025, while Kids and Children are projected to grow at the fastest CAGR of 7.51% during 2026-2031.

- By distribution channel, Specialty Stores accounted for the largest share of the apparel market, at 38.13% in 2025, while Online Retail Stores are projected to grow at the fastest CAGR of 7.29% during 2026-2031.

- By geography, the United States accounted for the largest share of the apparel market, at 36.40% in 2025, while Canada is projected to grow at the fastest CAGR of 6.98% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Luxury Apparel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-High-Net-Worth Consumers Driving Premium Demand | +1.4% | United States, Canada (Toronto, Vancouver) | Short term (≤ 2 years) |

| Luxury E-Commerce and Omnichannel Expansion | +1.2% | United States, Canada; urban corridors | Medium term (2–4 years) |

| Growing Preference for Casualization of Luxury | +0.9% | Global, with the United States leading adoption | Short term (≤ 2 years) |

| Rise of Customization and Personalization in Premium Clothing | +0.5% | United States, Canada | Medium term (2–4 years) |

| Shift Toward Sustainable and Ethical Luxury Fashion | +0.6% | United States, Canada (federal and state/provincial mandates) | Medium term (2–4 years) |

| Increased Focus on Inclusivity and Extended Sizing | +0.3% | The United States primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ultra-high-net-worth consumers anchoring market resilience

In 2024-2025, while global luxury faced spending pullbacks, the North American luxury apparel market found stability, thanks to the ultra-high-net-worth (UHNW) consumer segment. In Q1 2026, Hermès' Americas division boasted a +17.2% growth in constant currencies. Demand was "balanced across all métiers" in the U.S., Canada, and South America, highlighting a resilience not seen in the broader market, thanks to the unwavering engagement of top-tier consumers. Brunello Cucinelli reported a 20.3% revenue surge in constant currencies for Q1 2026, with the strongest demand for its premium-priced items[1]Source: Brunello Cucinelli, “Q1 2026 Investor Presentation,” Brunello Cucinelli, brunellocucinelli.com. This trend suggests that for this elite group, higher prices are seen as a feature, not a deterrent. Notably, a surge in wealth from the tech sector, especially the AI boom in U.S. coastal cities, is birthing a new wave of UHNW buyers. These individuals view luxury apparel not just as a display of wealth, but as a distinct cultural marker. J.P. Morgan highlighted in September 2025 that the robust performance of equity markets and resultant wealth creation were pivotal in bolstering North American luxury spending. As brands adjust their Very Important Client (VIC) programs to tap into this influx of tech-driven wealth, the trend of luxury spending becoming increasingly concentrated among the highest income brackets is poised to amplify through 2031.

Luxury e-commerce and omnichannel expansion reshaping distribution

In 2024, online luxury sales in North America experienced a significant surge, with a notable majority of Americans turning to the internet for their premium goods purchases. This shift has redefined the approach for premium clothing brands, elevating digital platforms from a mere supplementary channel to a primary avenue for customer acquisition. However, there's a growing nuance: as luxury brands seek tighter control over their brand experience, traditional pure-digital strategies are beginning to wane in effectiveness. LuxExperience, the parent company of Mytheresa, NET-A-PORTER, and MR PORTER, reported a commendable 9% net sales growth for the entirety of FY2025[2]Source: LuxExperience, “Q4 FY2025 Press Release,” LuxExperience, luxexperience.com. Their Adjusted EBITDA saw an impressive 73% uptick, a testament to their strategy of focusing marketing efforts on high-value clientele instead of broadening their aspirational customer base. Ralph Lauren witnessed a 21% surge in its North American digital commerce for Q4 FY2026. Additionally, in 2025, a striking 77% of REVOLVE's customer orders were made via mobile devices. The crux of the emerging strategy lies in striking a balance: while brands aim for digital expansion, they must also uphold the exclusivity that luxury embodies. A misstep, such as diluting curated digital experiences with discounting tactics, could jeopardize their in-store pricing integrity. According to BCG's insights, the future competitive edge may well lie in AI-driven client advisors, adept at mirroring the premium in-store service, but in a digital realm.

Growing preference for casualization blurring the luxury-sportswear boundary

The growing preference for casualization is increasingly blurring the boundary between luxury fashion and sportswear, becoming a key driver of the North American luxury apparel market. Consumers are prioritizing comfort, versatility, and everyday wearability, prompting luxury brands to expand offerings in premium outerwear, hoodies, sweatshirts, knitwear, and elevated athleisure. This trend is particularly evident among younger consumers, who seek luxury products that seamlessly transition between work, leisure, and social settings. According to the National Retail Federation (NRF), casual and comfort-oriented apparel continues to gain traction as lifestyle preferences evolve toward more relaxed dress codes. Reflecting this shift, Burberry reported double-digit growth in its Outerwear and Scarves categories during the second half of FY2026 and highlighted plans to extend this momentum across additional product categories in its FY2025/2026 preliminary results. Furthermore, the Jackets, Sweatshirts, and Hoodies segment is projected to grow at a 6.96% CAGR through 2031, underscoring the increasing convergence of luxury and casualwear. In 2025 and 2026, leading luxury houses, including Burberry, Louis Vuitton, Dior, and Gucci, continued introducing elevated sportswear-inspired collections, premium hoodies, and luxury outerwear lines, further strengthening demand for casual luxury apparel across North America.

Rise of customization and personalization as a conversion lever

In North America's luxury apparel market, personalization has shifted from being a mere value-added service to an essential requirement. Many luxury consumers now actively seek out personalized shopping experiences. This trend suggests that personalization is not just a luxury but a vital strategy: brands offering tailored services can deter price-sensitive younger consumers from switching to competitors. A testament to this shift is Gabriela Hearst's introduction of the Tailored Bespoke program, a made-to-order suiting service now available at flagship stores in New York, Los Angeles, and London. This move underscores how even mid-sized luxury brands are prioritizing customization. Given the generational divide, brands face the challenge of balancing two personalization approaches: offering artisanal customization for elite clients while leveraging AI-driven personalization for younger buyers. This strategy ensures they don't lose ground to niche specialists. Furthermore, premium clothing brands that embrace widespread customization are reaping financial rewards, with made-to-order items fetching a 30–60% price premium over their standard counterparts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Counterfeit Products Threatening Brand Equity | -1.2% | United States, Canada; border entry points | Short term (≤ 2 years) |

| Inventory Risk from Short-Cycle Fashion Trend Volatility | -0.8% | United States, Canada (all channels) | Short term (≤ 2 years) |

| Compliance Cost from Sustainability and Chemical Regulations | -0.4% | United States (California, New York), Canada | Medium term (2–4 years) |

| Strict Scrutiny Over Sustainability Claims and Greenwashing Risk | -0.3% | United States, Canada | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Counterfeit proliferation eroding brand equity and consumer trust

Counterfeit apparel and accessories pose a significant threat to the North American luxury apparel market, undermining brand equity and diverting consumer spending away from legitimate channels. In FY2025, U.S. Customs and Border Protection seized nearly 79 million counterfeit items, with a potential street value exceeding USD 7.3 billion, and clothing ranked among the top categories, as reported by UPI. A 2025 OECD report highlighted that the global counterfeit trade is valued at approximately USD 467 billion annually, accounting for over 2% of worldwide imports. A notable shift occurred in August 2025, when the U.S. closed its de minimis loophole, a move that previously let shipments valued under USD 800 slip past customs scrutiny. This change is expected to boost interdiction rates but may also drive counterfeiters to adopt more sophisticated distribution methods. According to BCG's 2025 consumer survey, 70% of luxury buyers prioritize Digital Product Passport authentication, indicating that brands embracing blockchain traceability and QR-code authentication could leverage this concern, setting themselves apart from unverified rivals. Consequently, this trend creates a cycle of compliance and technology investments, favoring larger, well-capitalized brands over their emerging or mid-market counterparts.

Inventory risk from short fashion-trend cycles straining operational models

Luxury apparel brands, traditionally structured for season-long planning, now grapple with the rapid pace of fashion trend cycles. These cycles, accelerated by social media, influencer-driven micro-trends, and AI's demand sensing, present a unique challenge. Typically, luxury brands operate on an 18–24 month lead time for bespoke and made-to-order lines. This creates a stark mismatch with the swift shifts in consumer preferences. The repercussions are evident: Kering, during its April 2026 Capital Markets Day, set a target of reducing inventory by EUR 1 billion within a year, highlighting the pressure on margins. Furthermore, excess inventory, especially at the aspirational luxury tier, is increasingly being offloaded through discount channels. Such moves jeopardize the brand's desirability, a key driver of its premium pricing. While the Bank of America Luxury Spending report highlighted a 10-quarter decline in U.S. luxury spending, signs of recovery emerged in 2025. Notably, aspirational consumers began prioritizing luxury services over goods. This trend emphasizes the dual risks of inventory mismanagement: immediate financial write-downs and potential long-term brand dilution from off-price sales visibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Casualization and Outerwear Innovation Redefine the Core

In 2025, T-Shirts and Shirts captured 45.71% of North America's luxury apparel market, solidifying their role as the leading symbols of luxury's casualization. This dominance isn't merely about volume or pricing; it's indicative of a broader shift in values. Affluent consumers, spanning various age groups, are increasingly channeling their luxury apparel budgets towards elevated basics. They're opting for premium cottons, exclusive prints, and capsule-collection tees from renowned houses like Loro Piana and Brunello Cucinelli, moving away from traditional, occasion-driven formal attire. Jackets, Sweatshirts, and Hoodies are set to be the fastest-growing product type through 2031, with a projected 6.96% CAGR. Brands like Moncler are at the forefront, leveraging the performance-luxury nexus. Their technically advanced outerwear is being marketed as long-term wardrobe investments, not just seasonal buys, evident from Moncler's 7% growth in the Americas segment in Q1 2026.

Mid-tier in the product hierarchy are Trousers, Jeans, Shorts, Skirts, Innerwear, and Dresses and Gowns, each appealing to distinct consumer segments. While Jeans are often viewed as a mass-market commodity, in the luxury realm, limited-edition denim from heritage houses commands premium prices between USD 500 and 2,000+, primarily sold through exclusive boutique channels. Dresses and Gowns, though challenged by the trend towards casualization, still hold significance for occasion-wear and among older affluent buyers. Burberry's move to assert dominance in Outerwear and Scarves, both witnessing double-digit growth in H2 FY2026, underscores the potential of a targeted product strategy within the expansive apparel category, even in a stabilizing market. Additionally, compliance mandates, like the PFAS bans in New York and California set for January 2025, are reshaping product designs, necessitating changes in technical fabric treatments for Jackets and Innerwear.

By End Purpose: Athleisure's Structural Rise Challenges Fashion's Primacy

The Fashion and Casual segment accounted for the largest share of the North America luxury apparel market in 2025, driven by consumers’ preference for versatile, everyday luxury clothing that balances style, comfort, and brand prestige. The continued relaxation of workplace dress codes and growing demand for premium casualwear have strengthened sales of luxury shirts, knitwear, outerwear, and denim. Reflecting this trend, Burberry reported double-digit growth in its Outerwear and Scarves categories in FY2026, while luxury brands such as Gucci and Louis Vuitton expanded casual ready-to-wear collections during 2025–2026. According to the National Retail Federation (NRF), consumers increasingly prioritize apparel suitable for multiple occasions, supporting sustained demand for fashion-oriented luxury casualwear.

Athleisure is projected to be the fastest-growing segment, registering a 7.01% CAGR between 2026 and 2031, fueled by the convergence of luxury fashion, wellness, and active lifestyles. Consumers increasingly seek premium apparel that offers both performance functionality and luxury aesthetics, encouraging brands to introduce elevated sportswear collections. Industry organizations such as the Sports & Fitness Industry Association (SFIA) continue to report strong participation in fitness and recreational activities across North America, supporting demand for premium activewear. During 2025 and 2026, luxury houses including Dior, Louis Vuitton, and Prada expanded luxury sneakers, performance-inspired apparel, and athleisure-focused collections, reflecting the growing appeal of high-end activewear among affluent consumers.

By End User: Women Lead, but Kids/Children Emerge as the Fastest-Growing Cohort

In 2025, women dominated North America's luxury apparel market, accounting for 52.13% of revenues. Their sustained engagement spanned the entire apparel spectrum, from ready-to-wear items to formal gowns, and they showed an increasing appetite for luxury basics, regardless of the occasion. Digital engagement also favored women's luxury apparel: Ralph Lauren's Women's Apparel category saw a constant currency growth of over 20% in Q4 FY2026, with North American digital commerce mirroring a 21% rise[3]Source: Ralph Lauren, “Q4 FY2026 Earnings Release,” Ralph Lauren, ralphlaurencorporation.com. Meanwhile, men emerged as the second-largest segment, with notable success in suit alternatives and elevated casual wear, a shift reflecting the evolving professional wardrobe shaped by hybrid work trends.

Children's luxury apparel is on a rapid ascent, projected to grow at a 7.51% CAGR through 2031. This growth isn't merely a fleeting demographic trend but stems from a fundamental shift in affluent parents' purchasing behavior. A key factor driving this trend is the resale value of premium children's clothing. Garments retain 40%–60% of their original value on resale platforms like Vinted and TheRealReal. This makes the luxury price tag more justifiable for affluent parents, who might otherwise balk at spending on items their children will quickly outgrow. Yet, this resale-value insight remains underutilized in brand messaging, presenting an untapped opportunity for many.

By Distribution Channel: Specialty Stores Hold, Online Retail Accelerates

In 2025, Specialty Stores commanded a 38.13% share of North America's luxury apparel market, highlighting the pivotal role of curated physical retail in offering the immersive experience that premium clothing buyers seek. According to the Q1 2026 report on Canada's luxury retail scene, brands are ramping up investments in mono-brand boutiques and flagship stores. This move grants them tighter control over customer relationships, pricing, inventory, and brand presentation, effectively diminishing their reliance on wholesale channels. Meanwhile, Online Retail Stores are witnessing the swiftest growth, boasting a 7.29% CAGR through 2031. This surge is fueled by enhanced digital experiences, AI-driven personal shopping assistants, and a push towards mobile-first luxury platforms.

Other Distribution Channels, which include department store concessions, wholesale, and off-price outlets, are facing structural challenges. Saks Global's Chapter 11 filing in 2026 underscored the risks tied to department store reliance. This event spurred many luxury brands to hasten their shift from wholesale concessions to directly operated boutiques. Tapestry, the parent company of Coach and Kate Spade New York, reported a 20% revenue surge in Q3 FY2026, raking in USD 1.1 billion in North America. Tapestry's leadership credited this success to a disciplined approach to full-price sell-throughs and a conscious cutback on promotions. This underscores a pivotal strategic insight: the mix of distribution channels, particularly the balance between direct-to-consumer and wholesale, has emerged as a key factor influencing gross margins and brand appeal in North America's luxury apparel landscape.

Geography Analysis

In 2025, the United States commanded a dominant 36.40% share of North America's luxury apparel market, solidifying its status as the region's largest player. The U.S. stands as the pivotal reference for brand positioning, flagship investments, and customer acquisition strategies. Even amidst global challenges for its Fashion and Leather Goods division, LVMH spotlighted the U.S. as a beacon of growth in 2025. Spending trends indicate a pronounced concentration at the upper echelons of the customer base, bolstering the resilience of premium pricing. Furthermore, heightened state-level scrutiny on product claims and supply-chain accountability is elevating operational standards for brands eyeing expansion in major U.S. luxury hubs.

Canada is set to outpace its North American counterparts, boasting a projected growth rate of 6.98% CAGR in the luxury apparel market through 2031. The draft attributes this surge to an influx of high-income migrants, a boost in inbound tourism, and a surge in mono-brand boutique investments, particularly in urban centers like Toronto and Vancouver. This positions Canada as a prime market for brands aiming to enhance visibility in select high-value cities, offering global houses a chance to tap into regional growth beyond the U.S. The allure of Canada in the North American luxury apparel landscape lies in its blend of concentrated demand and potential for further premium expansion.

While Mexico and other parts of North America hold the smallest share in the regional luxury apparel segment, Mexico's strategic significance remains undiminished for luxury brands. The draft pegged the Mexican luxury goods market at USD 6.94 billion in 2025, with projections soaring to USD 9.25 billion by 2031, marking a steady 4.92% CAGR. Hermès, in a testament to its confidence in Mexico City's affluent clientele, reintroduced its Molière store in October 2025. Although trade policy uncertainties loom over the pricing of imported luxury goods, the dual engines of domestic wealth generation and tourism continue to fuel selective brand investments.

Competitive Landscape

In North America, the luxury apparel market showcases a dual nature: while it's moderately concentrated at the conglomerate level, individual labels operate in a fragmented landscape. Giants like LVMH, Hermès, Kering, and Richemont set the tone for pricing, visibility, and premium standards. Yet, domestic brands and niche labels fiercely compete, carving out their own spaces in terms of products, customers, and sales channels. This dynamic ensures a competitive edge for North America's luxury apparel scene, even under the sway of a few global titans.

Kering's ambitious April 2026 strategy to shutter 250 stores and revamp two-thirds of its retail outlets by 2030 underscores a shift towards heightened productivity, stringent network oversight, and streamlined inventory. Meanwhile, Hermès's commitment to selective distribution and exclusivity translated to a commendable 12.4% growth in the Americas for 2025, with an even more impressive 17.2% surge in Q1 2026. Ralph Lauren's North American revenue hit USD 3.3 billion in FY2026, buoyed by a 16% uptick in comparable store sales in Q4. Such maneuvers highlight the market's preference for brands that uphold full-price sales, fine-tune their offerings, and ensure direct customer engagement. Additionally, companies investing in store enhancements, advanced customer service, and robust data systems stand to gain.

Technology has cemented its role in shaping competitive strategies within North America's luxury apparel sector. In FY2026, Ralph Lauren harnessed AI and analytics for customer outreach and product selection, while Tapestry attributed its North American success to data-driven product introductions and a focus on full-price sales. This trend indicates that top players are blending brand legacy with enhanced inventory oversight, tighter channel management, and targeted client interactions. With distribution voids left by less robust wholesale channels, there's ample opportunity for dedicated direct-to-consumer brands, ensuring the competition remains fierce in North America's luxury apparel arena.

North America Luxury Apparel Industry Leaders

LVMH Moët Hennessy Louis Vuitton SE

Kering SA

Hermès International S.A.

Chanel S.A.

Compagnie Financière Richemont SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Chanel opened its second boutique in Vancouver at Oakridge Park Mall, designed by architect Peter Marino and spanning 750 square metres. The space features Ready-to-Wear, Fine Jewelry, and a CHANEL Privé personalized consultation suite, signaling deepening investment in Western Canada's luxury corridor.

- May 2026: Prada opened a 7,000 sq ft Milan-inspired flagship at Vancouver's Oakridge Park, bringing men's and women's ready-to-wear, leather goods, footwear, and fine jewellery under one roof. The opening is part of Prada's declared strategy to "heavily expand" North American presence between 2026 and 2028, with 80–85% of growth expected from like-for-like flagship productivity.

- November 2025: Chanel opened its largest Canadian boutique at Holt Renfrew Yorkdale, ahead of a planned second Vancouver boutique at Oakridge Park in 2026, reinforcing the brand's long-term commitment to the Canadian luxury market.

North America Luxury Apparel Market Report Scope

Luxury apparel refers to premium, high-end clothing and fashion accessories that are defined by exceptional craftsmanship, exclusivity, high price points, and strong brand prestige. The North America luxury apparel market is segmented by product type, end purpose, end user, distribution channel, and geography. By product type, the market is segmented into trousers, jeans, t-shirts and shirts, shorts and skirts, jackets, sweatshirts and hoodies, innerwear, dresses and gowns, and other product types. By end purpose, the market is segmented into athleisure, fashion, and casual. By end user, the market is segmented into men, women, and kids/children. By distribution channel, the market is segmented into specialty stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Trousers |

| Jeans |

| T-Shirts and Shirts |

| Shorts and Skirts |

| Jackets, Sweatshirts and Hoodies |

| Innerwear |

| Dresses and Gowns |

| Other Product Types |

| Athleisure |

| Fashion and Casual |

| Men |

| Women |

| Kids/Children |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| Product Type | Trousers |

| Jeans | |

| T-Shirts and Shirts | |

| Shorts and Skirts | |

| Jackets, Sweatshirts and Hoodies | |

| Innerwear | |

| Dresses and Gowns | |

| Other Product Types | |

| End Purpose | Athleisure |

| Fashion and Casual | |

| End User | Men |

| Women | |

| Kids/Children | |

| Distribution Channel | Specialty Stores |

| Online Retail Stores | |

| Other Distribution Channels | |

| Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

What is the current and forecast value of North America's luxury apparel?

The North America luxury apparel market stood at USD 39.98 billion in 2026 and is projected to reach USD 51.63 billion by 2031, growing at a 5.3% CAGR.

Which product category leads revenue in this space?

T-Shirts and Shirts led in 2025 with a 45.71% share, which shows the strength of elevated everyday wear in premium wardrobes.

Which segment is growing fastest by product type?

Jackets, Sweatshirts, and Hoodies are the fastest-growing product category, with a 6.96% CAGR projected through 2031.

Why is athleisure gaining more traction in premium clothing?

Athleisure is growing at 7.01% through 2031 because buyers are blending performance, comfort, and lifestyle use into one wardrobe spend pattern.

Page last updated on: