North America Athletic Wear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

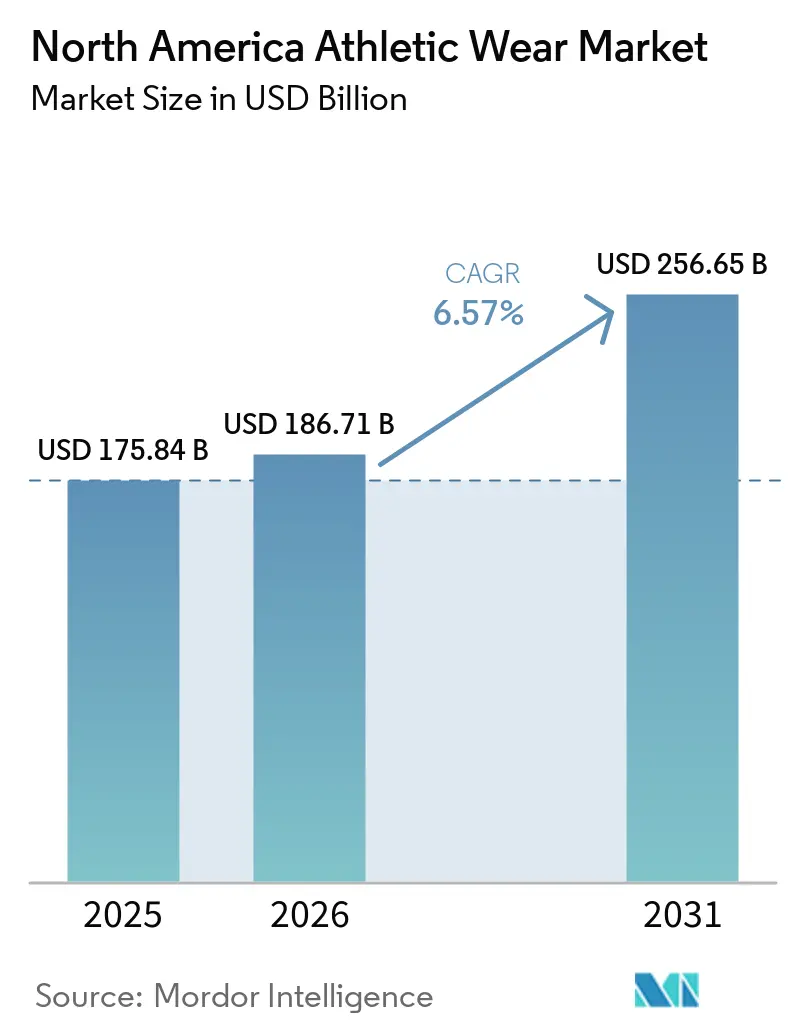

| Base Year Market Size (2025) | USD 175.84 Billion |

| Market Size (2026) | USD 186.71 Billion |

| Market Size (2031) | USD 256.65 Billion |

| Growth Rate (2026 - 2031) | 6.57% CAGR |

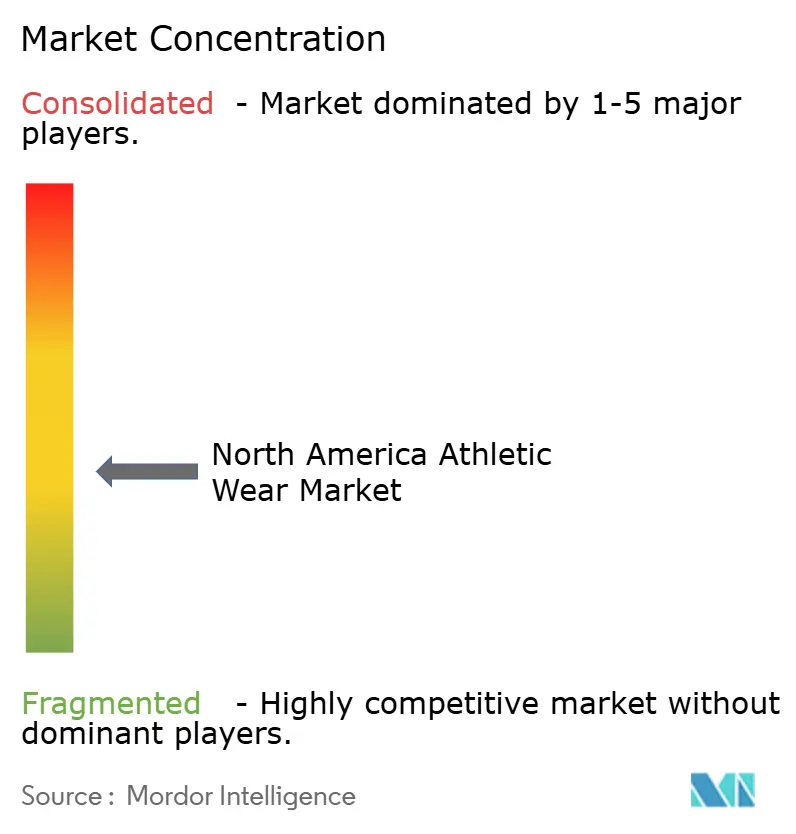

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Athletic Wear Market Analysis by Mordor Intelligence

The North America athletic wear market size is projected to expand from USD 175.8 billion in 2025 and USD 186.7 billion in 2026 to USD 256.7 billion by 2031, registering a CAGR of 6.6% between 2026 and 2031. This market is growing because athletic wear now serves both performance use and daily wear, which keeps purchase frequency high across age groups and price tiers. Demand in the North America athletic wear market is also being supported by record youth participation in school sports and by strong sporting goods sales in the United States, which keeps the replacement cycle active for footwear and apparel [1]Source: SFIA (Sports & Fitness Industry Association), "Sporting Goods Industry Reaches Nearly $130B Amid Trade and Tariff Pressures", sfia.org. Product development is becoming more important in the North America athletic wear market because brands are using new fabric technologies and women-focused design platforms to defend pricing and widen their consumer base[2]Source: NCAA (National Collegiate Athletic Association), "Women’s sports reach record NCAA participation as leadership roles keep rising", ncaa.org. Competition in the North America athletic wear market is being shaped by brand strength, direct-to-consumer execution, and faster innovation cycles, while companies with weaker channel discipline are losing momentum in the region.

Key Report Takeaways

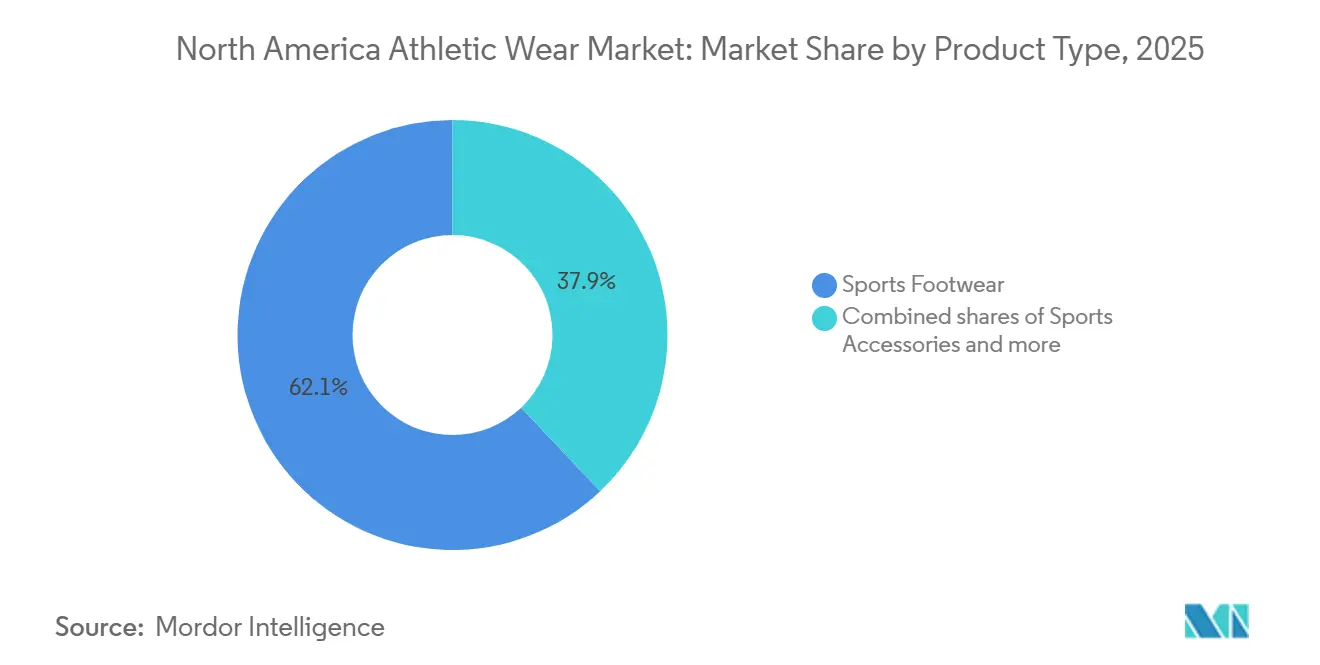

- By product type, Sports Footwear led with 62.04% of the North America athletic wear market share in 2025, while Sports Accessories is forecast to expand at an 8.03% CAGR through 2031.

- By category, Mass held 68.11% share in 2025, while Premium recorded the highest projected CAGR at 7.33% through 2031.

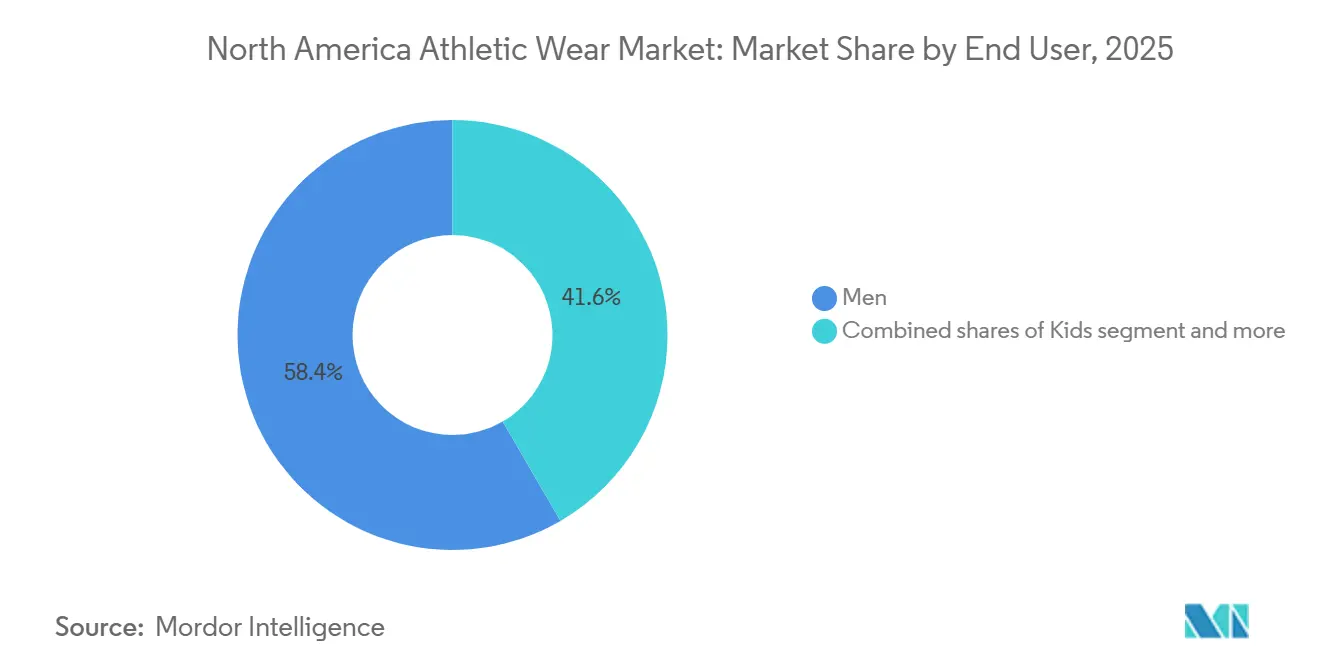

- By end user, Men held 58.37% share in 2025, while Kids recorded the highest projected CAGR at 7.39% through 2031.

- By distribution channel, Specialty Stores held 45.09% share in 2025, while Online Retail Stores recorded the highest projected CAGR at 8.04% through 2031.

- By geography, the United States accounted for 78.34% of the North America athletic wear market size in 2025, while Mexico recorded the highest projected CAGR at 8.15% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Athletic Wear Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising fitness awareness increases demand for athletic wear | +1.8% | Global, highest intensity in United States and Canada | Medium term (2-4 years) |

| Technological advancements in fabric development | +1.2% | United States and Canada, with spillover to Mexico | Long term (≥ 4 years) |

| Product innovations enhance comfort, performance, and durability | +1.1% | Global, concentrated in United States | Medium term (2-4 years) |

| Celebrity endorsements influence athletic wear purchasing decisions | +0.9% | United States, with growing impact in Mexico and Canada | Short term (≤ 2 years) |

| Women's sports participation expands the consumer base | +0.8% | Across North America, fastest in United States and Canada | Medium term (2-4 years) |

| Demand for sustainable apparel encourages product innovation | +0.6% | Led by United States, with compliance influence in Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Fitness Awareness Increases Demand for Athletic Wear

Sports participation in North America has moved beyond a short wellness cycle and is now supporting repeat demand for sport-specific clothing and footwear across multiple age groups. The National Federation of State High School Associations reported 8,266,244 high school sports participants in the 2024-25 school year, which was a record high and more than 200,000 above the prior year [3]Source: NFHS (National Federation of State High School Associations), "Participation in High School Sports Hits Record High with Sizable Increase in 2024-25", nfhs.org. That rise matters for the North America athletic wear market because youth participation creates fresh demand for uniforms, training shoes, recovery items, and replacement purchases as athletes move through school programs. The Sports & Fitness Industry Association reported that U.S. sporting goods wholesale sales reached USD 130 billion in 2025, with athletic footwear contributing USD 24.1 billion, which shows that active participation is already translating into large commercial volumes. Brands that align product design with specific age, sport, and training needs are better positioned than broad lifestyle labels to capture this demand in the North America athletic wear market.

Technological Advancements in Fabric Development

Fabric development is becoming a stronger driver of product differentiation in the North America athletic wear market because consumers are now responding to materials that enhance comfort, cooling, and visible performance. Nike introduced Aero-FIT in 2026 and said the platform delivers more than double the airflow of older athletic apparel while using 100% textile waste through chemical recycling. Lululemon also launched ShowZero in March 2026 and positioned it as a yarn-level solution that makes sweat less visible during high-intensity activity. These launches show that fabric research in the North America athletic wear market is not just a background capability, because it now supports brand image, premium pricing, and stronger consumer retention. Brands that own core material platforms are likely to hold a clearer advantage than those that depend mainly on licensed or easily copied inputs.

Women's Sports Participation Expands the Consumer Base

Women's participation is widening the demand base for the North America athletic wear market because more athletes are entering structured sports environments and staying active longer. The NCAA reported 242,341 women student-athletes in 2024-25, up 14% from a decade earlier, while participation in emerging sports rose 24% year over year. That pattern supports more spending on performance bras, studio apparel, training footwear, and sport-specific gear rather than only general activewear. Nike SKIMS launched its Studio Stretch collection in May 2026 and used a women-centered product platform to target studio workouts with lightweight softness, adaptive stretch, and support. Brands that build women's ranges from the start, instead of adapting men's designs, are in a stronger position to capture this longer cycle of participation growth.

Celebrity Endorsements Influence Athletic Wear Purchasing Decisions

Celebrity and athlete partnerships now have a direct effect on how brands enter new categories and reach consumers in this market. Li-Ning announced a 10-year, USD 400 million partnership with Stephen Curry and Curry Brand in June 2026, and the company tied the agreement to basketball, golf, lifestyle categories, and an explicit U.S. expansion plan. The WNBA and Skechers also announced a multiyear official partnership in May 2026, which strengthens Skechers' visibility in women's sports and helps it reach younger fans whose brand preferences are still forming. These deals show that endorsements in this market do more than support advertising because they can open retail paths, shape relevance, and improve credibility in performance categories. Rising endorsement costs also make it harder for mid-tier brands to secure talent at the same scale as larger incumbents.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit products negatively impact brand sales and trust | -0.7% | United States wide, heightened around major sporting events | Short term (≤ 2 years) |

| Fluctuating raw material costs affect manufacturing profitability | -0.5% | Global supply chain, with pass-through risk concentrated in United States and Canada | Medium term (2-4 years) |

| Seasonal demand fluctuations create sales volatility challenges | -0.3% | Across North America, highest in Canada and northern United States | Short term (≤ 2 years) |

| Environmental regulations increase compliance and production costs | -0.4% | Led by United States, especially California, New York, and Washington, with spillover to Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit Products Negatively Impact Brand Sales and Trust

Counterfeit products remain a real restraint on the North America athletic wear market because they affect both revenue and consumer confidence. The American Apparel & Footwear Association said in 2026 that 41% of 39 tested counterfeit apparel, footwear, and accessory products failed U.S. and international product safety standards. U.S. Customs and Border Protection also states that nearly 90% of intellectual property rights seizures originate from China and Hong Kong, which shows how concentrated the supply source remains. In February 2025, U.S. Homeland Security Investigations and Customs and Border Protection seized USD 39.5 million in counterfeit sports merchandise through Operation Team Player ahead of the Super Bowl, which underlines the scale of the issue during major events. For the North America athletic wear market, this means brand owners must spend more on monitoring, enforcement, and marketplace control even when results remain uneven.

Fluctuating Raw Material Costs Affect Manufacturing Profitability

Raw material cost swings continue to pressure margins in the North America athletic wear market because many product lines still depend on petroleum-linked and imported inputs. The Sports & Fitness Industry Association identified trade and tariff pressures as key variables shaping the 2026 sporting goods outlook in the United States. Columbia Sportswear said in its first quarter 2026 results that its outlook assumed current U.S. tariff rates through July 2026, which shows how policy conditions are already affecting planning and pricing decisions. Larger brands can spread procurement risk across more suppliers and negotiate better terms, but smaller manufacturers and suppliers have less room to absorb sudden cost increases. That imbalance can widen the gap between strong incumbents and mid-market players in the North America athletic wear market during periods of supply chain stress.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sports Accessories Quietly Outpacing Core Segments

Sports footwear held 62.04% share in 2025, which kept it as the largest product block within the North America athletic wear market. Sports Accessories is projected to grow at an 8.03% CAGR through 2031, which makes it the fastest-moving product type over the forecast period. Footwear remains large because innovation cycles are frequent in running shoes, training shoes, and sport-specific products, and these cycles support both replacement demand and higher average selling prices. The Sports & Fitness Industry Association reported that athletic footwear reached billions in U.S. wholesale sales in 2025, which confirms the commercial weight of the category in the region. Walking shoes also retain relevance because an older active consumer base continues to value comfort-oriented designs alongside performance features.

Sports apparel remains broad in the North America athletic wear industry because it covers tops, T-shirts, bottom wear, jackets, hoodies, innerwear, compression wear, and swimwear across both performance and casual use occasions. This range helps brands serve competitive athletes, gym users, school sports participants, and everyday active consumers without relying on one narrow demand pool. Jackets, hoodies, and compression products benefit from dual use because they work in training, recovery, and streetwear settings, which gives the segment steadier purchase support across seasons. Accessories are gaining speed because committed consumers increasingly buy full activity kits that include bags, caps, socks, gloves, and other add-on items instead of limiting purchases to core athletic wear. Nike's Aero-FIT launch also points to where apparel development is headed, because it combines advanced cooling with recycled feedstock and shows that performance and circularity are being engineered together rather than treated as separate goals.

By Category: Mass Holds Ground as Premium Accelerates

Mass accounted for 68.11% of 2025 demand, while Premium is projected to grow at a 7.33% CAGR through 2031, which shows a split structure inside the North America athletic wear market. The large Mass base reflects the strength of accessible price points across specialty retail, broadline retail, and other high-volume channels. Premium is moving faster because a growing set of consumers is paying more for technical fabrics, brand credibility, and purpose-built performance claims. Lululemon's 2026 launches of Unrestricted Power and ShowZero show the type of product engineering that supports higher pricing and stronger brand distinction in premium apparel. In practical terms, the North America athletic wear market size is being lifted at the premium end by product stories that consumers can see and feel rather than by branding alone.

This split is sharpening execution demands across the North America athletic wear industry because brands now need a clear reason to play either at scale or at a premium. Nike SKIMS extended into Studio Stretch in May 2026 and used a targeted women-focused design approach to defend premium positioning in a busy category. At the mass end, tariff uncertainty matters more because lower price products have less margin room to absorb higher input or import costs without hurting demand. Columbia Sportswear's first quarter 2026 outlook showed that current tariff assumptions were still affecting planning, which reflects the pressure on brands that compete mainly through price and volume. Brands caught between value and premium positioning face the most risk because they can lose price-sensitive shoppers without gaining enough product authority to sustain higher margins.

By End User: Kids Emerge as the Fastest-Growing Consumption Cohort

Men held 58.37% share in 2025, but Kids is projected to rise at a 7.39% CAGR through 2031, making it the fastest-growing end-user group in the North America athletic wear market. This growth is closely tied to high participation in youth sports, which creates a regular need for uniforms, footwear replacements, and training accessories as children advance through sports calendars. The National Federation of State High School Associations recorded 8,266,244 total high school participants in 2024-25 and more than 3.5 million girls, both at record levels. Parents are also directing more spending toward sport-specific items instead of generic athletic wear, especially where competition intensity and school participation remain high. This means the Kids segment is not just a volume story, because it is also linked to earlier brand formation and repeat demand over many years.

Men still provide the largest revenue base because the North America athletic wear market has long been shaped by strong brand investment in running, training, basketball, and football categories. Women's demand is also rising steadily, supported by broader participation and by brands that are now designing more specific performance ranges for female athletes. The NCAA reported continued gains in women's student-athlete participation in 2024-25, which suggests that the pipeline from school sport to adult active lifestyles remains strong. Skechers' multiyear WNBA partnership adds another signal because it helps the brand connect with younger followers while women's sports visibility continues to rise. Brands that gain trust early in the Kids segment can carry those relationships into Men's and Women's demand later, which makes youth-focused execution important well beyond immediate sales.

By Distribution Channel: Online Gains Ground While Specialty Stores Defend Share

Specialty stores held 45.09% share in 2025, while online retail stores are projected to grow at an 8.04% CAGR through 2031, which shows that channel change is active but not one-sided in the North America athletic wear market. Online growth is being supported by direct-to-consumer strategies, mobile purchasing habits, and stronger use of data for fit guidance and repeat purchasing. Under Armour said in fiscal 2026 that improvements in its e-Commerce platform are part of its North America reset, with a focus on better full-price sell-through and higher average unit retail values. Digital channels give brands tighter control over pricing and consumer data, which is why online sales should remain the faster-growth path in the North America athletic wear market. Even so, footwear conversion still depends heavily on trust and fit, which keeps store-based trial relevant.

Specialty stores remain important because they provide curated assortments, staff guidance, and a brand environment that many digital channels cannot fully replace. That matters most in athletic wear, where consumers still want to compare feel, fit, and function before they commit to a higher-priced purchase. Supermarkets and hypermarkets continue to serve convenience-led and price-led buying, especially inside the mass category. Other channels, including brand-owned stores and off-price outlets, remain useful for inventory control, segmentation, and selective premium presentation. The result is a hybrid channel structure where the North America athletic wear market continues to rely on physical retail for conversion while digital platforms handle discovery, replenishment, and brand-owned consumer relationships.

Geography Analysis

The United States held 78.3% of the North America athletic wear market share in 2025, which made it the clear demand anchor for the region. The Sports & Fitness Industry Association reported that U.S. sporting goods wholesale sales reached billions in 2025. That scale reflects a large active population, mature retail infrastructure, and strong product turnover across footwear and apparel. The United States also shapes compliance expectations for the wider region because California regulations and the AAFA restricted substances framework are influencing how brands manage textiles, chemicals, and reporting. Companies that already invested in stronger compliance systems should face less disruption as regulation becomes more demanding.

Canada offers a steady consumer base for the North America athletic wear market, with room to grow further in women's and youth segments. Canadian Women & Sport reported in late 2024 that 63% of Canadian girls participate in organized sports weekly, while more than 1 million girls remain outside organized sport. That gap shows both a participation challenge and a commercial opening for brands that can improve accessibility, sizing, and relevance. Canada also benefits from strong premium brand trust, especially where local or regionally familiar players already hold a strong image with active consumers.

Mexico is the fastest-growing geography in the North America athletic wear market, with an expected 8.2% CAGR through 2031. The 2026 FIFA World Cup is adding visibility and purchase intent around fanwear, footwear, and related apparel in the market. Mexico also benefits from younger demographics and a rising sports culture, which gives brands a wider base for future expansion beyond event-led demand. Rest of North America remains smaller in value terms, but it still matters for companies that are building regional distribution and looking for wider shelf presence over time.

Competitive Landscape

The North America athletic wear market shows moderate concentration at the top because large global brands still hold strong positions, but the field remains open enough for share shifts when product cycles or channel choices change. Adidas reported 10% currency-neutral revenue growth in North America in 2025 and expects continued low-double-digit currency-neutral growth in the region in 2026, which points to regained momentum in one of the market's largest branded positions. Under Armour moved the other way, with North America revenue down 8% to USD 2.9 billion in fiscal 2026 as it continued channel rationalization and brand repositioning. Amer Sports generated USD 6.6 billion in 2025 revenue and is scaling Arc'teryx through a direct-to-consumer epicenter strategy while also pushing Salomon footwear growth in North America. VF Corporation also returned to full-year revenue growth in fiscal 2026, with The North Face up 12%, which shows that recovery is possible when brand investment and operating discipline improve.

Three broad positions are visible in the North America sports apparel and footwear market: premium innovation leaders, performance-led heritage players, and brands still restructuring for relevance. NikeSKIMS Studio Stretch is one example of how leading brands are trying to protect premium ground through more focused design and material stories rather than relying only on scale. Li-Ning's 10-year Stephen Curry partnership is another example because it links athlete credibility to a stated U.S. expansion strategy and gives the brand a faster route into basketball and lifestyle conversations. Under Armour's launch of The Bouncy Tee in May 2026 shows how product renewal is being used alongside channel reset to support its comeback effort.

In this setting, the North America athletic wear market is rewarding brands that can match strong product stories with disciplined distribution and consistent brand signals. Speed still matters, but not every fast launch turns into durable gains if the brand lacks trust or fit with consumer needs. Circular product claims and supply chain visibility are also becoming more useful in retailer conversations, especially as compliance and sourcing scrutiny rise. Smaller brands can still win targeted pockets of demand, but sustained gains usually depend on clear category focus rather than broad expansion without product authority.

North America Athletic Wear Industry Leaders

-

Nike, Inc.

-

adidas AG

-

PUMA SE

-

Lululemon Athletica Inc.

-

Anta Sports Products Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Li-Ning announced a 10-year, USD 400 million endorsement partnership with Stephen Curry and Curry Brand, covering basketball, golf, and lifestyle categories with an explicit U.S. retail expansion mandate. The deal represents the most strategically significant North America market-entry move by a Chinese sports brand to date, leveraging Curry's NBA superstar status as a brand-building platform.

- May 2026: NikeSKIMS launched the Studio Stretch material-innovation collection targeting women's studio workouts, combining lightweight softness, adaptive stretch, and understated support. The launch extends the NikeSKIMS platform into functional performance, reinforcing Nike's effort to recapture premium women's apparel ground.

North America Athletic Wear Market Report Scope

The North America athletic wear market refers to the industry encompassing apparel, footwear, and accessories designed for sports, fitness, and active lifestyles, including products used for both athletic performance and everyday athleisure wear across the United States and Canada. The North America Athletic Wear Market Report is Segmented by Product Type (Sports Apparel, Sports Footwear, and More), Category (Mass and Premium), End User (Men, Women, Kids), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, and More), and Geography (United States, Canada, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Sports Apparel | Tops and T-Shirts |

| Bottom Wear | |

| Jackets and Hoodies | |

| Innerwear and Compression Wear | |

| Swimwear | |

| Other Sports Apparel | |

| Sports Footwear | Running Shoes |

| Training and Gym Shoes | |

| Walking Shoes | |

| Sports-Specific Footwear | |

| Other Sports Footwear | |

| Sports Accessories | Bags |

| Caps and Hats | |

| Socks | |

| Gloves | |

| Other Sports Accessories |

| Mass |

| Premium |

| Men |

| Women |

| Kids |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America |

| Product Type | Sports Apparel | Tops and T-Shirts |

| Bottom Wear | ||

| Jackets and Hoodies | ||

| Innerwear and Compression Wear | ||

| Swimwear | ||

| Other Sports Apparel | ||

| Sports Footwear | Running Shoes | |

| Training and Gym Shoes | ||

| Walking Shoes | ||

| Sports-Specific Footwear | ||

| Other Sports Footwear | ||

| Sports Accessories | Bags | |

| Caps and Hats | ||

| Socks | ||

| Gloves | ||

| Other Sports Accessories | ||

| Category | Mass | |

| Premium | ||

| End User | Men | |

| Women | ||

| Kids | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

What is the outlook for North America athletic wear through 2031?

The sector is projected to rise from USD 186.7 billion in 2026 to USD 256.7 billion by 2031 at a 6.6% CAGR, supported by active lifestyle demand, product innovation, and broader participation in sports.

Which product type leads sales in North America athletic wear?

Sports Footwear leads with a 62% share in 2025, helped by strong replacement cycles and higher pricing tied to running, training, and sport-specific innovation.

Which segment is growing fastest by end user?

Kids is the fastest-growing end-user segment with a 7.4% CAGR through 2031, supported by record school sports participation and rising spending on sport-specific gear.

Why are specialty stores still important if online sales are rising?

Specialty Stores still held 45.1% share in 2025 because consumers often want in-person fit, feel, and product guidance, especially for footwear and higher-value performance products.

Page last updated on: