Running Apparel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

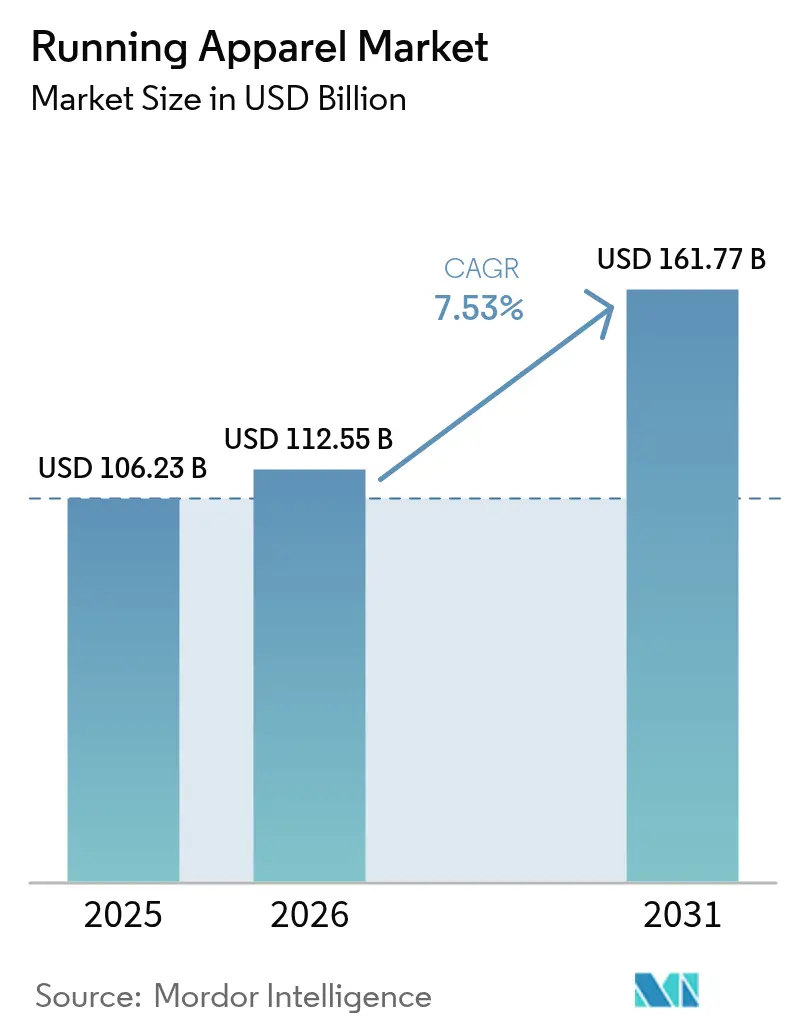

| Market Size (2026) | USD 112.55 Billion |

| Market Size (2031) | USD 161.77 Billion |

| Growth Rate (2026 - 2031) | 7.53% CAGR |

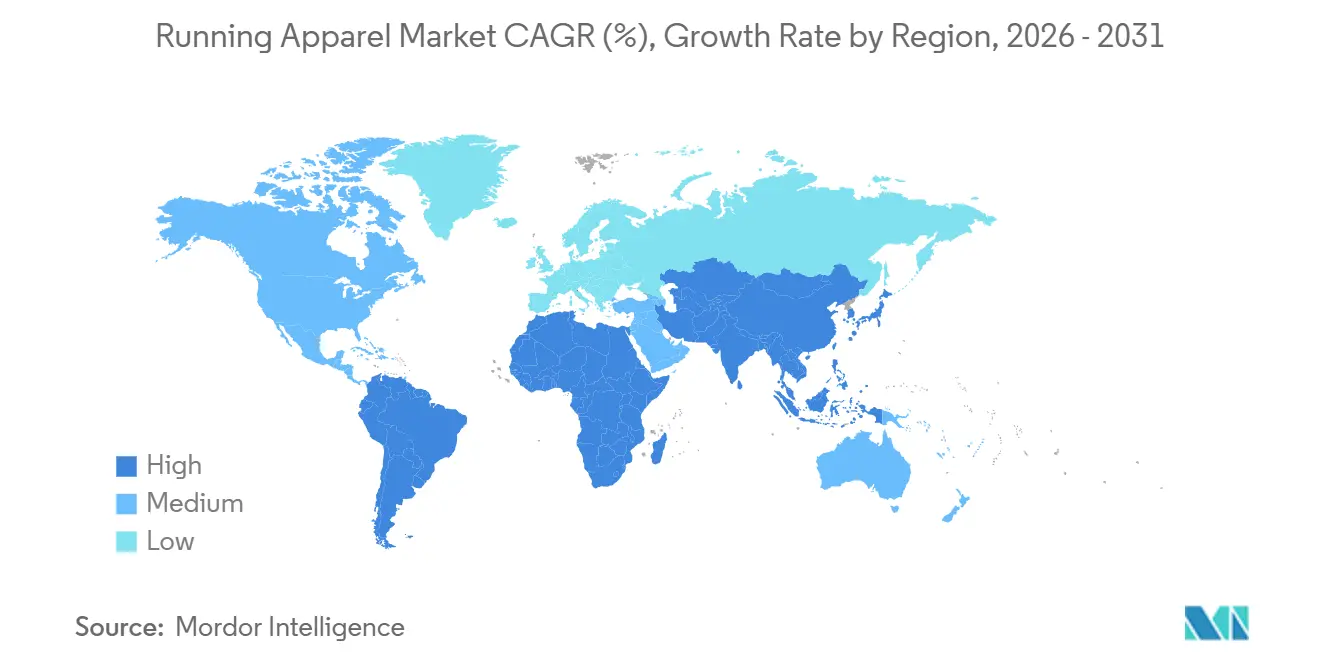

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

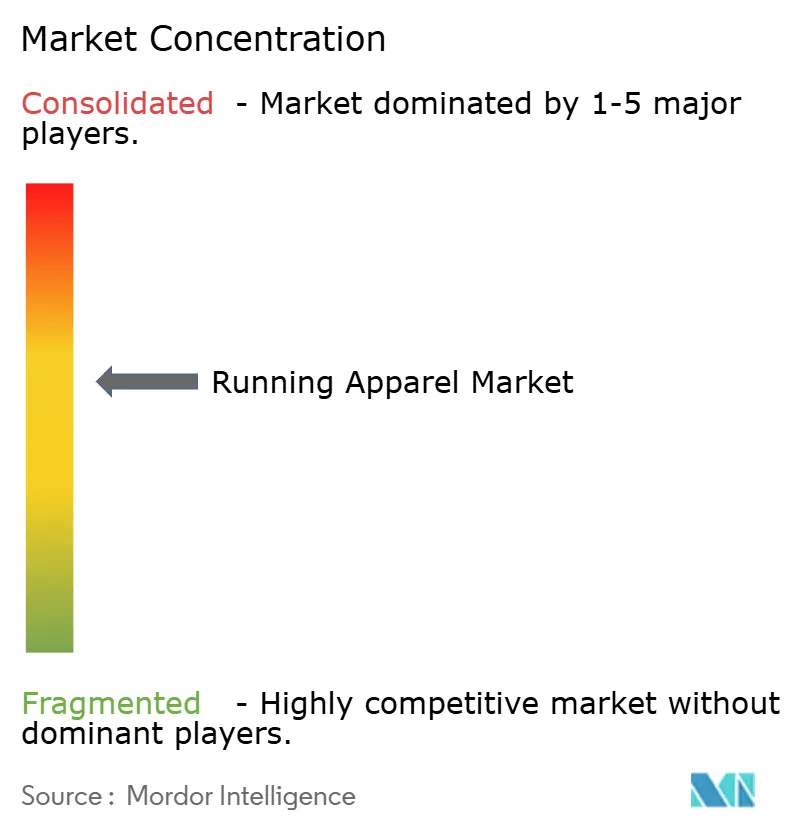

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Running Apparel Market Analysis by Mordor Intelligence

The running apparel market size is projected to grow from USD 106.23 billion in 2025 and USD 112.55 billion in 2026 to USD 161.77 billion by 2031, registering a CAGR of 7.53% between 2026 and 2031. The increasing participation of women in fitness and running activities has driven demand for gender-specific designs and collections. While premiumization is a key trend in mature markets, urbanization and rising disposable incomes are fueling growth in emerging economies. The integration of athletic wear with everyday fashion enhances the versatility and appeal of running apparel, attracting a wider audience beyond dedicated runners. Factors such as the social acceptance of athleisure, growing female participation in organized sports, and the visibility of running communities on social media are expanding the consumer base. Synthetic performance fabrics continue to dominate the market; however, recycled variants are gaining traction, supported by European and Californian regulations that incentivize products with reduced microplastic shedding. Competitive intensity remains moderate, with Nike, Adidas, and Lululemon holding significant market positions. However, premium disruptors and direct-to-consumer brands are increasingly challenging the market share of established players in the running apparel segment.

Key Report Takeaways

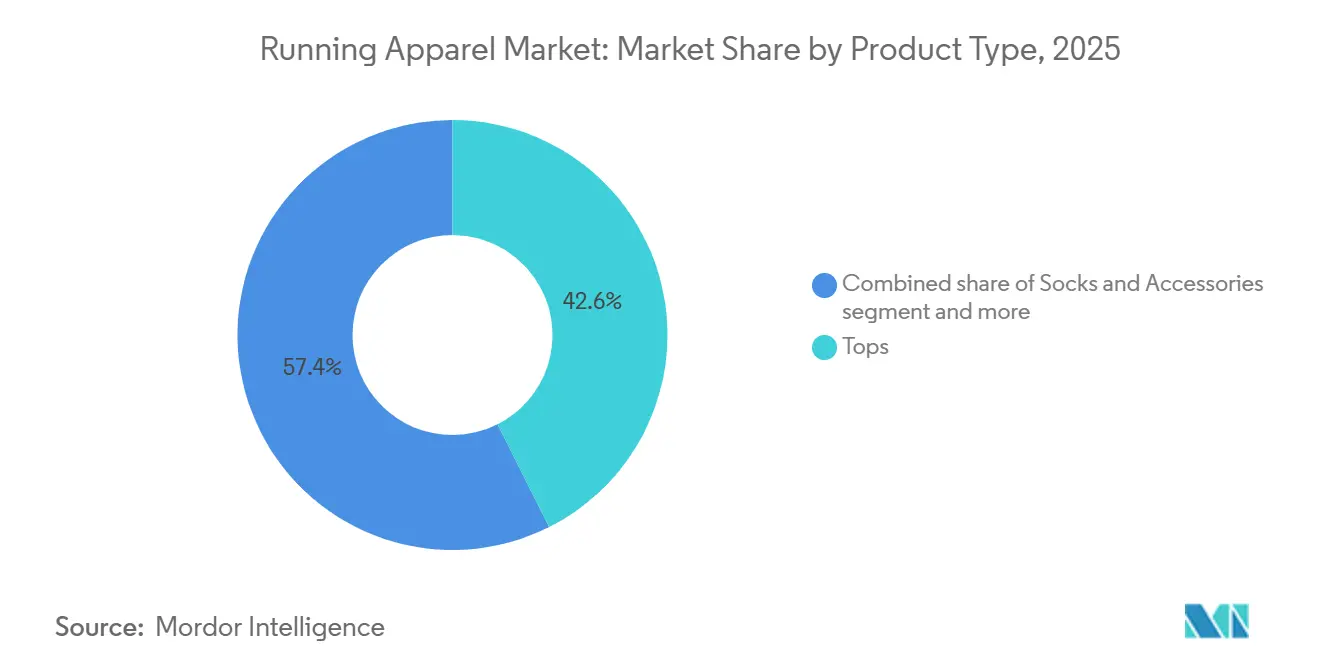

- By product type, tops held 42.58% of the running apparel market share in 2025, while socks and accessories are advancing at a 7.89% CAGR through 2031.

- By fabric and material, synthetics held a 66.75% share of the running apparel market size in 2025; recycled and bio-based synthetics are forecast to grow 9.86% annually through 2031.

- By end user, men contributed 49.78% revenue in 2025, whereas the women’s segment is forecast to grow at a 7.98% CAGR to 2031.

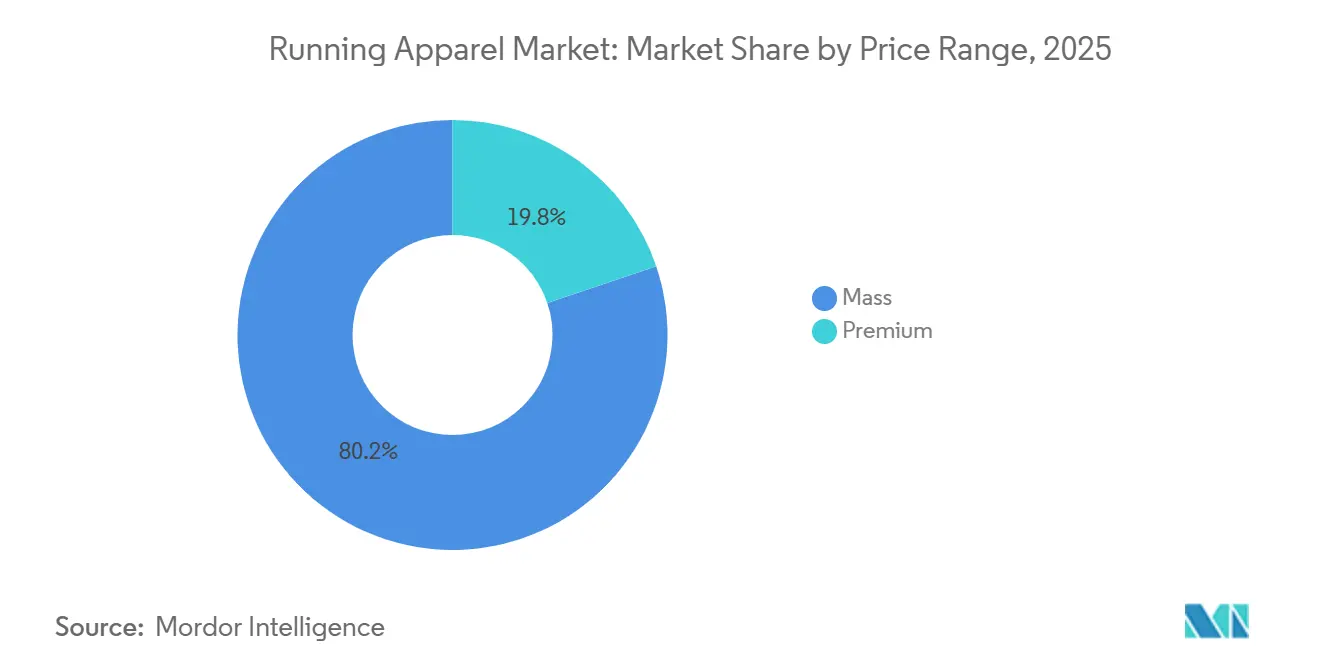

- By price range, the mass tier controlled 80.18% revenue in 2025; premium products are projected to climb at a 9.61% CAGR.

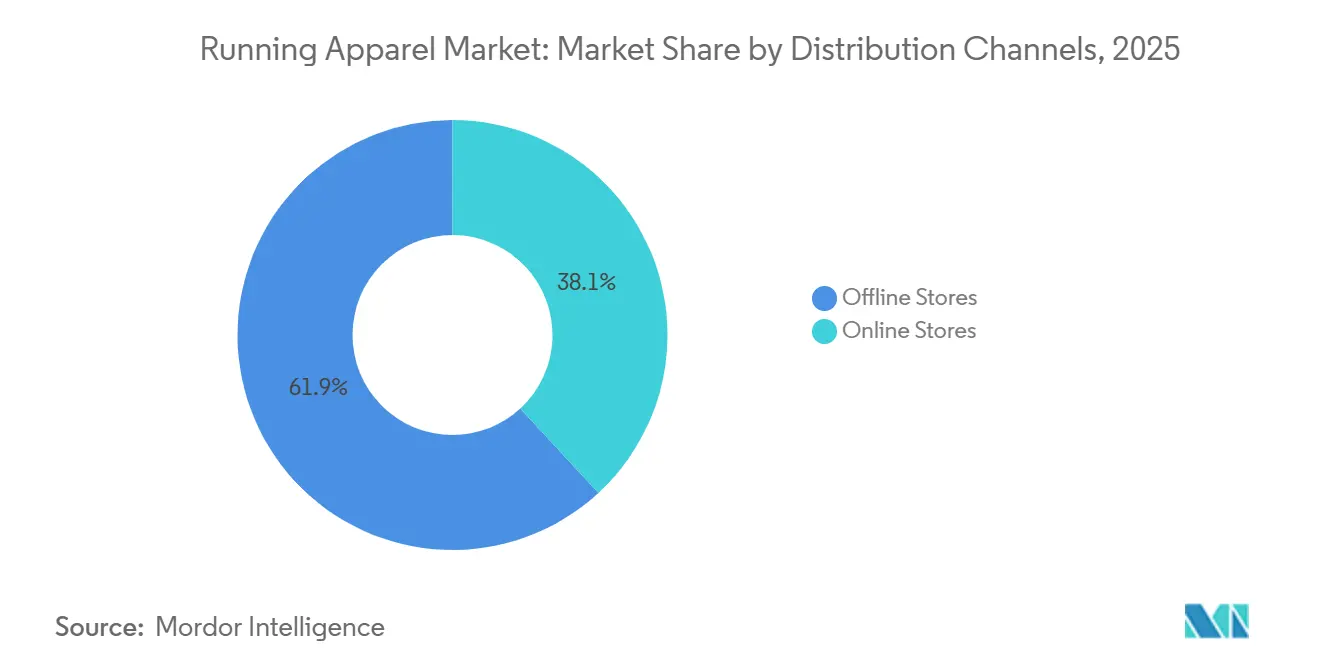

- By distribution channel, offline stores captured 61.87% share in 2025, but online store sales are predicted to rise at a 9.80% CAGR.

- By geography, North America led with 42.22% share in 2025, yet Asia-Pacific is expected to post the fastest 7.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Running Apparel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global participation in recreational events | +1.2% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Rise of marathons and running events | +1.0% | North America, Europe, China, India, Australia | Medium term (2-4 years) |

| Influence of social media platforms and celebrity endorsements | +0.8% | Global, particularly North America, Europe, and digitally connected Asia-Pacific markets | Short term (≤ 2 years) |

| Significant growth in women sports participation rate | +1.1% | Global, with accelerated gains in North America, Europe, and emerging Asia-Pacific | Long term (≥ 4 years) |

| Athleisure-driven integration of fashion and everyday wear | +1.3% | North America, Europe, urban centers in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Advances in moisture-wicking and stretch fabric technologies | +0.9% | Global, with research and development hubs in North America, Europe, and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising global participation in recreational events

Government health initiatives and corporate wellness programs are driving significant growth in the demand for running apparel across both developed and emerging markets. In the United States, participation in running and jogging increased from 48.31 million in 2023 to 51.05 million in 2024, according to the Sports and Fitness Industry Association [1]Source: Sports and Fitness Industry Association,"2025 Sports, Fitness, and Leisure Activities Topline Participation Report", sfia.org. This growth encompasses not only recreational activities but also structured programs, reflecting a record high in sports participation. The increasing popularity of running events, such as marathons and charity runs, has further contributed to this trend, encouraging individuals to invest in high-quality running apparel. Similarly, in England, 6,544,700 individuals engaged in running activities in 2024, as reported by Sport England [2]Source: Sport England, "Active Lives Adult Survey November 2023-24", sportengland.org. This rise is supported by initiatives like community running clubs and government campaigns promoting physical activity. The combination of institutional support and grassroots participation is fueling consistent demand for performance-oriented running apparel that caters to both structured training and casual fitness needs. Additionally, corporate wellness programs are increasingly emphasizing measurable fitness outcomes, driving demand for technical apparel that facilitates performance tracking while maintaining a professional appearance. These programs often include incentives for employees to participate in fitness activities, further boosting the adoption of specialized running apparel.

Rise of marathons and running events

Marathons, charity runs, trail races, and other organized running events attract millions of participants each year. Many participants purchase specialized running apparel, such as moisture-wicking tops, lightweight outerwear, and accessories, to prepare for these events. Driven by the desire to enhance performance and prevent injuries, there is a growing demand for technologically advanced, comfortable, and high-utility apparel, particularly as training often spans several months. In 2024, marathon participation reached unprecedented levels, with the world record for the largest marathon being broken twice, first in Berlin and later in New York City. The TCS New York City Marathon, held in November, recorded over 56,000 finishers, reclaiming its title as the world's largest marathon and becoming the largest race of any distance in the United States, according to Running USA [3]Source: Running USA, "2024 Top Races Report", runningusa.org. This trend is not limited to elite events, as mass participation organizers increasingly emphasize lifestyle-oriented running events. This shift is generating commercial opportunities for apparel partnerships and event-specific merchandise that extend beyond traditional performance-focused categories.

Influence of social media platforms and celebrity endorsements

Social media platforms have transformed the marketing strategies for running apparel, shifting the emphasis from product-focused messaging to fostering lifestyle-oriented communities. Platforms such as Instagram, TikTok, and YouTube play a significant role in rapidly amplifying trends, turning specific products or styles into widespread phenomena. Collaborations with celebrities, elite athletes, and micro-influencers enhance the aspirational appeal of brands, encouraging followers to adopt their lifestyle and product choices. Endorsements now extend beyond traditional athlete sponsorships to include lifestyle influencers and entertainment personalities. For example, in February 2025, Nike collaborated with SKIMS, leveraging Kim Kardashian's cultural influence to introduce NikeSKIMS. Generation Z demonstrates distinct style preferences, such as favoring crew socks over no-show options, while coordinated outfits remain popular across all age groups. Blue is expected to emerge as the dominant color for 2025. To address this demographic segmentation, brands need to build genuine connections with diverse influencer networks and ensure their product offerings align with rapidly changing style trends.

Athleisure‑driven integration of fashion and everyday wear

The global running apparel market is witnessing notable growth, primarily driven by the rising popularity of athleisure fashion. This trend merges sportswear with everyday clothing, broadening the consumer base and contributing to increased market volume and value. Athleisure wear combines athletic performance with casual style, making running apparel, such as tops, bottoms, outerwear, and accessories, suitable for activities beyond exercise, including work, errands, and social events. By focusing on both comfort and style, athleisure appeals not only to athletes but also to older consumers and those prioritizing leisure, thereby expanding the market beyond traditional runners. Both established and niche brands are differentiating their running apparel lines by incorporating bold designs, vibrant colors, and flattering fits alongside performance-oriented features, turning technical running gear into fashionable items. Brands such as Lululemon, Nike, Adidas, and On are leveraging this combination of style and functionality. Furthermore, athleisure promotes repeat purchases as consumers seek fresh styles for diverse occasions, moving beyond the sole need for athletic replacements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of counterfeit products | -0.6% | Global, with concentration in Asia-Pacific, Middle East, and e-commerce platforms | Short term (≤ 2 years) |

| Regulatory pressure on synthetic fabrics | -0.4% | Europe (REACH), North America (CPSIA), emerging Asia-Pacific standards | Long term (≥ 4 years) |

| Seasonal demand fluctuations | -0.3% | North America, Europe, temperate regions with distinct seasons | Short term (≤ 2 years) |

| Volatile raw-material costs for advanced fabrics | -0.5% | Global, with supply chain dependencies in Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prevalence of counterfeit products

Counterfeit running apparel continues to pose a significant challenge to market growth, with enforcement actions highlighting the extent of illicit trade that undermines brand value and endangers consumer safety. In 2025, U.S. Immigration and Customs Enforcement seized counterfeit sports merchandise valued at USD 39.5 million through Operation Team Player[4]Source: U.S. Immigration and Customs Enforcement, "Intellectual Property Rights and Commercial Fraud", ice.gov. This initiative is part of a greater effort that has resulted in the confiscation of over USD 455 million in counterfeit sports merchandise, as reported by the agency in 2025. Counterfeit products not only present safety risks due to substandard materials and manufacturing processes but also diminish consumer trust and brand equity, making it increasingly difficult for legitimate brands to maintain their market position. The growth of e-commerce platforms and the widespread use of small-package international shipping have further complicated enforcement measures, as counterfeiters exploit these channels to distribute fake products globally. Over 90% of counterfeit seizures occur through mail and express channels, driving brands to invest in advanced authentication technologies, implement stricter monitoring systems, and enhance supply chain transparency to combat this persistent issue.

Regulatory pressure on synthetic fabrics

Regulatory frameworks aimed at reducing microplastic emissions from synthetic textiles are increasing compliance costs and imposing material limitations, thereby affecting product development and pricing strategies. The European Union's Ecodesign for Sustainable Products Regulation, effective from July 18, 2024, mandates eco-design requirements for textiles, emphasizing durability, recyclability, and environmental impact. France has announced a requirement for microfiber filters in washing machines starting in 2025. Furthermore, restrictions on PFAS are expanding globally: France plans to ban PFAS in textiles by 2026, while California will enforce similar restrictions with a threshold of 100 parts per million beginning in 2025. These regulations necessitate significant changes to water-repellent and stain-resistant treatments in performance running apparel, potentially increasing production costs and requiring alternative technologies that may impact functionality. Compliance frameworks, such as OEKO-TEX standards, are adapting to align with these restrictions, adding certification requirements that complicate supply chains and extend the time-to-market for new products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Types: Tops Drive Volume, Accessories Accelerate Growth

Tops accounted for 42.58% of the market share in 2025, driven by their high replacement frequency. Runners typically own 5-8 technical shirts compared to 2-3 pairs of shorts, and tops offer versatility across various training intensities and weather conditions. Socks and accessories are projected to grow at a CAGR of 7.89% through 2031, supported by advancements in compression technology, moisture management, and specialized features such as blister-prevention yarns and arch support bands. Bottoms and outerwear hold mid-tier positions in the market. Bottoms benefit from the athleisure trend, which has normalized the use of running tights or joggers in non-athletic settings. However, outerwear growth is limited by higher price points and longer replacement cycles.

Outerwear is shifting toward modular designs, such as detachable sleeves and convertible hoods, which enhance usability across varying temperature ranges and address consumer concerns about single-use garments. The top segment also gains from collaborations with fashion designers, such as Adidas' partnership with Stella McCartney. These collaborations elevate running shirts from functional items to fashion-forward products, enabling premium pricing. Meanwhile, bottoms face increasing competition from yoga and training pants, which offer similar comfort and stretch but cater to broader use cases. To remain competitive, running-specific brands are focusing on features like secure phone pockets and reflective detailing to differentiate their products from general activewear.

By Fabric and Material: Synthetics Dominate, Sustainability Drives Innovation

Synthetic fabrics, such as polyester, nylon, and spandex, accounted for 66.51% of the market share in 2025, attributed to their superior moisture-wicking properties, durability, and cost efficiency compared to natural fibers. Recycled and bio-based synthetic fabrics are growing at a CAGR of 9.86%, driven by regulatory mandates, such as the EU's Circular Economy Action Plan, which targets 30% recycled content in textiles by 2030, and evolving consumer preferences. In 2025, 62% of surveyed runners expressed a willingness to pay a 10-15% premium for sustainable materials. Natural and blended fabrics, including merino wool and cotton blends, maintain a niche appeal, particularly among ultra-distance runners who prioritize odor resistance and thermal regulation over quick-drying capabilities.

The increasing adoption of recycled synthetics is transforming supply chains, with brands investing in chemical recycling technologies that convert post-consumer polyester into virgin-quality feedstock, avoiding the quality degradation associated with mechanical recycling. Blended fabrics aim to balance performance and sustainability by combining the softness of cotton with the durability of polyester. However, they often face challenges in differentiating themselves in a market increasingly divided between high-performance synthetics and eco-conscious recycled alternatives.

By End User: Men Lead, Women Accelerate

Men contributed 49.78% of end-user revenue in 2025, driven by historically higher participation rates and larger average transaction sizes, attributed to greater spending on premium footwear and accessories. Women's running apparel is growing at a CAGR of 7.98%, surpassing the overall market growth as brands focus on gender-specific innovations, such as sports bras with adjustable compression, shorts with phone pockets, and reflective detailing for safety during early-morning or evening runs. Growth in the women's segment is particularly strong in the Asia-Pacific region, where cultural shifts, including increased female workforce participation and urbanization, are encouraging fitness activities that were previously male-dominated.

The men's segment is experiencing saturation in developed markets, where penetration rates exceed 40% among active runners, leading brands to focus on replacement cycles rather than acquiring new customers. Kids' apparel faces challenges such as rapid size changes that shorten product lifecycles and parental price sensitivity, which limits premium positioning. However, brands view this segment as a long-term opportunity to build lifelong brand loyalty.

By Price Range: Mass Dominates, Premium Outpaces

The mass segment accounted for 80.18% of the market share in 2025, driven by price-conscious consumers in emerging markets and value-focused shoppers in developed economies who prioritize durability over technical features. Premium products are growing at a CAGR of 9.61%, indicating a market bifurcation where affluent consumers are willing to pay for marginal performance improvements, such as seamless construction, anti-odor treatments, proprietary fabrics, and brand prestige. On Running, a Swiss brand, reported a 31% revenue increase in 2024 by positioning its CloudTec cushioning technology as a premium alternative to Nike and Adidas. The brand successfully captured market share among runners willing to spend USD 150-180 on shoes and USD 80-120 on apparel.

The growth in the premium segment is primarily concentrated in North America and Europe, where higher disposable incomes support discretionary spending on specialized gear. In contrast, the Asia-Pacific region shows mixed trends, urban centers like Shanghai and Singapore reflect Western-style premium adoption, while rural and lower-tier cities remain more price-sensitive. Mass-market brands are addressing this disparity by introducing tiered product lines with "good-better-best" options under a single brand umbrella, enabling consumers to trade up as their commitment to running increases.

By Distribution Channels: Offline Leads, Online Surges

In 2025, offline stores accounted for 61.87% of the market share, highlighting consumers' preference for tactile evaluation, such as testing fabric texture and verifying fit, particularly for higher-priced items like running shoes and jackets. Meanwhile, online stores are growing at a CAGR of 9.80%, supported by direct-to-consumer models that bypass retailer margins. This approach allows brands to offer competitive pricing while achieving higher gross margins. Omnichannel strategies are increasingly bridging the gap between offline and online channels. For example, brands like Lululemon offer "buy online, pick up in store" options, combining the convenience of e-commerce with immediate product access and reduced shipping costs.

Physical retail is shifting toward experiential formats, incorporating features like treadmill testing stations, gait analysis services, and community running clubs, transforming stores into hubs for brand engagement rather than solely transaction points. The channel mix varies by region: in China, e-commerce penetration for sportswear exceeds 50%, driven by platforms such as Tmall and JD.com. In contrast, Europe and North America maintain a stronger offline presence due to established specialty running stores and a preference for in-person service.

Geography Analysis

North America is projected to account for a significant 42.22%% share of revenue in 2025, supported by a well-established jogging culture, high disposable incomes, and a dense network of specialty stores. The region benefits from a mature sports infrastructure, extensive retail networks, and widespread e-commerce penetration, ensuring consumers have easy access to products and a seamless shopping experience. Regional players focus on performance differentiation and employ premium storytelling strategies to maintain their market share against competition from global entrants. The presence of major global brands such as Nike, Adidas, Under Armour, and New Balance, which are either headquartered in or maintain a strong operational presence in North America, further enhances the market's scale and competitiveness. Additionally, government initiatives, such as grants for community fitness trails, play a crucial role in expanding the participatory base and driving consistent upgrades in footwear and apparel.

Asia-Pacific, while currently smaller in market size, is expected to grow at the fastest rate among all regions, with a robust CAGR of 7.71%% through 2031. This growth is driven by rising middle-class incomes, urban development projects like bike lanes, and the incorporation of kinesiology-friendly curricula in schools, which collectively unlock new demand segments. Increasing health awareness and the growing popularity of organized running events and marathons significantly contribute to the market's expansion. The region experiences intense competition between local sportswear manufacturers and international brands, both of which focus on offering affordable and diverse product ranges to appeal to a price-sensitive yet aspirational consumer base. Domestic e-commerce platforms play a critical role in providing cost-effective distribution channels for international brands, although the risk of counterfeit products remains a challenge in the region.

Europe continues to experience steady growth, driven by a strong consumer preference for sustainability. Over 60% of European consumers consider eco-credentials a key factor influencing their purchasing decisions. The rapid adoption of recycled synthetic materials and the implementation of stringent regulations on micro-plastics are expected to shape both fabric innovation and marketing strategies in the region. In South America, the market benefits from a young and growing population as well as increasing urbanization. However, the region remains highly price-sensitive due to macroeconomic volatility, which poses challenges to sustained growth.

Regulatory Landscape

Sustainability and chemical-safety requirements are tightening for performance textiles, affecting running apparel materials, finishes, and end-of-life obligations. In the European Union, the Ecodesign for Sustainable Products Regulation (ESPR) is being implemented through product rules for textiles. The European Commission has also announced measures to stop the destruction of unsold clothes and shoes, with the destruction ban applying to large companies from 19 July 2026. In parallel, Member States are moving toward producer-funded waste management, following the EU Waste Framework Directive revision entering into force in October 2025, which requires mandatory Extended Producer Responsibility (EPR) schemes for textiles and footwear within 30 months.

In the United States, compliance risk spans both product and trade controls. California enacted the Responsible Textile Recovery Act of 2024 (AB 1170), establishing a statewide EPR framework for apparel and textile articles, with implementing regulations scheduled no earlier than July 2028. Separately, the Office of the United States Trade Representative (USTR) in June 2026 initiated Section 301 investigations covering forced-labor enforcement failures across multiple economies, with proposed additional duties in the 10% to 12.5% range on imports including apparel and textiles. This increases the focus on traceability, supplier compliance documentation, and sourcing diversification.

Competitive Landscape

The running apparel market demonstrates moderate consolidation, with increasing competition as established athletic brands contend with specialized running companies and direct-to-consumer entrants. Traditional market leaders leverage their extensive global distribution networks and strong marketing capabilities to sustain their market positions. At the same time, challenger brands are gradually capturing market share by emphasizing innovative product offerings and building authentic connections with their target communities.

Key players in the market, such as Nike Inc., Adidas AG, Under Armour, Puma SE, and Asics Corporation, are actively diversifying their product portfolios, intensifying competition within the market. These companies are adopting strategies to strengthen their global presence, including establishing new operational bases, expanding production facilities, and investing significantly in research and development. Their robust distribution networks and manufacturing expertise provide a competitive edge, enabling them to effectively broaden their product offerings across various regions.

Strategic consolidation is gaining momentum through partnerships and acquisitions, allowing companies to combine complementary strengths and enhance market access. For example, Nike's February 2025 partnership with SKIMS illustrates how established brands are leveraging cultural relevance and design expertise to target new demographic segments, particularly within the growing women's market. Furthermore, the adoption of advanced technologies, such as smart textiles, is driving competitive differentiation. Growth opportunities are emerging in areas like sustainable materials, personalized fit technologies, and regional market expansion. The Asia-Pacific region, in particular, offers significant growth potential, as health club penetration in major economies such as China and India remains below 1%, indicating a largely untapped market.

Running Apparel Industry Leaders

-

Nike, Inc.

-

Adidas AG

-

Under Armour, Inc.

-

ASICS Corporation

-

Puma SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory and standards changes around chemicals and circularity are creating room for running apparel assortments built around compliant water-repellent alternatives, safer chemistry, and more traceable recycled inputs. The June 1, 2026 effective update to OEKO-TEX Standards 2026 tightens limit values that affect dyeing, finishing, and materials selection, strengthening the commercial value of certified and documentation-ready supply chains for global brands and private labels. In Europe, the ESPR-linked move to prevent the destruction of unsold apparel (applying to large companies from 19 July 2026) and the post-October 2025 shift toward mandatory textile EPR schemes support demand for product design choices that improve durability, repairability, and recyclability, consistent with recycled and bio-based synthetics gaining traction.

Technology and manufacturing approaches are also creating clearer differentiation and margin headroom. On Running scaled automated LightSpray production with a second facility near Busan, South Korea (announced February 2026), adding 32 robots and reporting a 30-fold increase in LightSpray capacity, which points to a more automation-led approach to reducing lead times and supply risk for performance products. On also published its first global materials policy in April 2026, indicating tighter supplier and farm-level traceability requirements that can carry into apparel material sourcing. In product innovation, 2026 research on integrated, breathable textile systems with multiplex biosensing signals an R&D direction for smart training apparel beyond moisture management, while partnerships such as Nuyarn Technologies with Unknown Runner (July 2026) support continued opportunities for premium trail-running layers using lightweight merino blends.

Recent Industry Developments

- July 2026: Nike launched the Keely Hodgkinson Collection, combining running apparel with footwear models including the Vomero Plus and Vaporfly 4. The athlete-led capsule reinforces performance storytelling in womens running while supporting full-look merchandising across apparel and footwear.

- February 2025: Nike and SKIMS launched NikeSKIMS, a collaborative brand focused on womens activewear with designs tailored to the female silhouette. The partnership broadens access to fashion-led fit and comfort propositions that translate into running-adjacent apparel purchasing and community-driven demand.

- August 2024: Sealskinz released a new Run collection for men and women, spanning jackets, tees, shorts, and accessories engineered for varied weather conditions. The launch highlights continued category expansion in technical outerwear and accessories, where functional differentiation can support premium pricing.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers clothing and related items that are primarily designed and marketed for running, and it is sized in value terms at the point of sale across major regions. It includes performance-oriented apparel used by recreational and professional runners through offline and online channels.

Scope exclusions: We exclude general sportswear that is not positioned for running use, along with second-hand sales and counterfeit products.

Segmentation Overview

-

By Product Type

- Tops

- Bottoms

- Outerwear

- Socks and Accessories

-

By Fabric and Material

- Synthetic (Polyester, Nylon, Spandex)

- Recycled and Bio-based Synthetics

- Natural and Blended (Merino, Cotton Blends)

-

By End User

- Men

- Women

- Kids

-

By Price Range

- Mass

- Premium

-

By Distribution Channels

- Offline Stores

- Online Stores

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Sweden

- Belgium

- Poland

- Netherlands

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Thailand

- Singapore

- Indonesia

- South Korea

- Australia

- New Zealand

- Rest of Asia-Pacific

-

Middle East and Africa

- United Arab Emirates

- South Africa

- Saudi Arabia

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base on participation and consumer demand signals for running. We typically use public sources such as the US Census Bureau retail and trade statistics, US International Trade Commission trade data, Eurostat, UN Comtrade, and World Bank macro series to anchor currency, inflation, and regional demand context.

We also review company annual reports and investor presentations, press releases, and sports and outdoor association websites to understand product positioning and channel mix shifts. Where needed, we reference paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export data to sanity-check scale and pricing direction. This list is not exhaustive, and many other public and paid sources were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test assumptions that are hard to confirm from public data, especially for the share of running-specific apparel inside broader activewear baskets. We spoke with brand and channel executives, product and sourcing leaders, and retail managers across major regions so our sizing logic reflects real pricing, mix, and sell-through behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 16% | APAC: 46% |

| Mid tier: 57% | Functional/Unit leaders: 39% | EMEA: 31% |

| Smaller Players: 16% | Managers: 45% | Americas: 23% |

Market-Sizing & Forecasting

Our sizing model starts with a top-down demand pool build that links running participation and apparel purchasing intensity to an addressable spend base by region. To keep the totals realistic, the output is then corroborated with selective bottom-up checks such as sampled average selling price (ASP) by category multiplied by implied volumes, along with channel checks on online versus offline mix.

Key inputs used in the model include running participation levels and event activity, apparel price bands and promotion intensity, share shift toward online retail, material and product mix (for example, synthetic performance fabrics versus blends), and regional income and inflation trends that influence discretionary spend. When one input series is missing for a country, gaps are handled through proxy indicators from similar markets and then corrected through interview feedback.

For forecasting, we rely on scenario analysis supported by expert views on participation momentum, pricing power, and channel expansion, and we stress-test outcomes against expected macro conditions. Assumptions are kept traceable so updates can be made quickly when new public data or channel signals appear.

Data Validation & Update Cycle

Checks are run at multiple points so the numbers do not drift away from real-world signals. We compare model outputs with independent indicators such as apparel retail trends, trade flows for relevant categories, and stated business performance comments from key brands and retailers, and then investigate large variances before sign-off.

A second analyst review is completed for logic, unit consistency, and currency conversion timing, and follow-up questions are triggered when interview feedback conflicts with desk findings. Reports are refreshed annually, and interim updates are made when material events occur, such as demand shocks or major pricing resets. Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Running Apparel Market Size Compared With Other Published Estimates

Published numbers for running apparel do not always match because researchers draw the scope line differently, and they also use different price and channel assumptions. Differences also show up when base years shift, when currencies are converted using different timing, and when the estimate is not rechecked against participation and retail signals.

Some estimates treat running apparel as a narrow technical subset and exclude broader running-oriented apparel sold through mass retail channels, and Mordor Intelligence counts running-focused clothing value across offline and online sales and then rechecks totals against participation trends and pricing moves.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 112.55 B (2026) | |

| Trade Journal A | USD 16.81 B (2025) | Uses a narrower basket that appears closer to technical running wear and accessories, and it likely applies tighter inclusion rules for products and channels, which can reduce the captured value versus broader retail apparel spending signals. |

| Global Consultancy B | USD 47.00 B (2024) | Starts from an earlier base year and appears to apply a smaller definition that does not fully capture cross-over demand from athleisure purchases labeled for running, which can lower the starting value even before forecasting assumptions are applied. |

The spread in the table mostly comes from what is counted as running apparel and how consistently the value is followed through retail channels. Once the scope, base year, and pricing logic are aligned and then validated with independent demand signals, the market number becomes easier to replicate with the same steps over time.

Key Questions Answered in the Report

What is the forecast value of the running apparel market by 2031?

It is projected to reach USD 161.77 billion by 2031 at a 7.53% CAGR from 2026 to 2031.

Which product category currently leads global sales?

Tops lead with 42.58% revenue share in 2025.

Which region will grow the fastest through 2031?

Asia-Pacific is set to post the quickest 7.71% CAGR, driven by China and India.

How significant are recycled fabrics in future growth?

Recycled and bio-based synthetics are expanding at 9.86% CAGR and are expected to exceed 20% share by 2031.

Page last updated on: