Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 14.58 Billion |

| Market Size (2026) | USD 15.21 Billion |

| Market Size (2031) | USD 18.75 Billion |

| Growth Rate (2026 - 2031) | 4.28% CAGR |

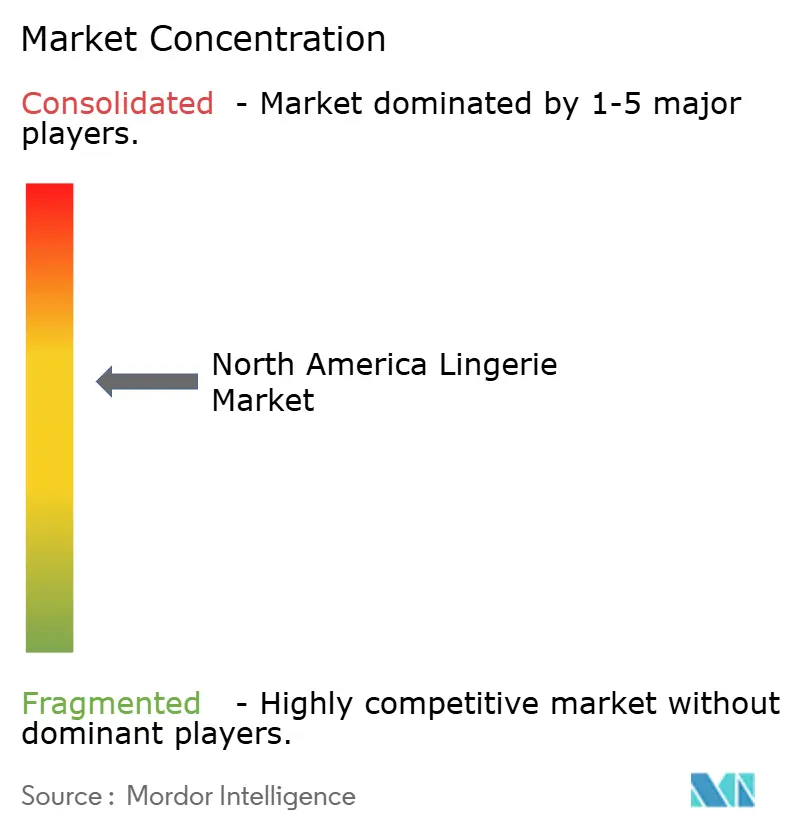

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Lingerie Market Analysis by Mordor Intelligence

The North America Lingerie Market size in 2026 is estimated at USD 15.21 billion, growing from 2025 value of USD 14.58 billion with 2031 projections showing USD 18.75 billion, growing at 4.28% CAGR over 2026-2031. This growth trajectory reflects a market undergoing fundamental transformation, driven by evolving consumer expectations around body positivity, technological innovation in fabrics, and the accelerating shift toward direct-to-consumer channels. The market's moderate but steady expansion masks significant underlying disruptions, particularly the decline of traditional wholesale models and the rise of digitally native brands that prioritize inclusive sizing and personalized fit solutions. Digitally native labels are eroding the primacy of wholesale distribution as personalized fit algorithms, virtual try-ons, and narrative-rich social media campaigns lift conversion and loyalty. Meanwhile, sustainability imperatives are accelerating fiber substitution, and the pace of mergers, acquisitions, and retail partnerships underscores a market that rewards agility. Competitive intensity is moderated yet meaningful; a market concentration score of 6 indicates ample room for incumbents and disruptors alike to gain share through differentiated positioning.

Key Report Takeaways

- By product category, brassieres held 52.05% of North American lingerie market share in 2025, while briefs are projected to grow at a 4.96% CAGR through 2031.

- By price range, the mass segment commanded 70.18% of the North American lingerie market size in 2025; premium products are advancing at a 6.05% CAGR to 2031.

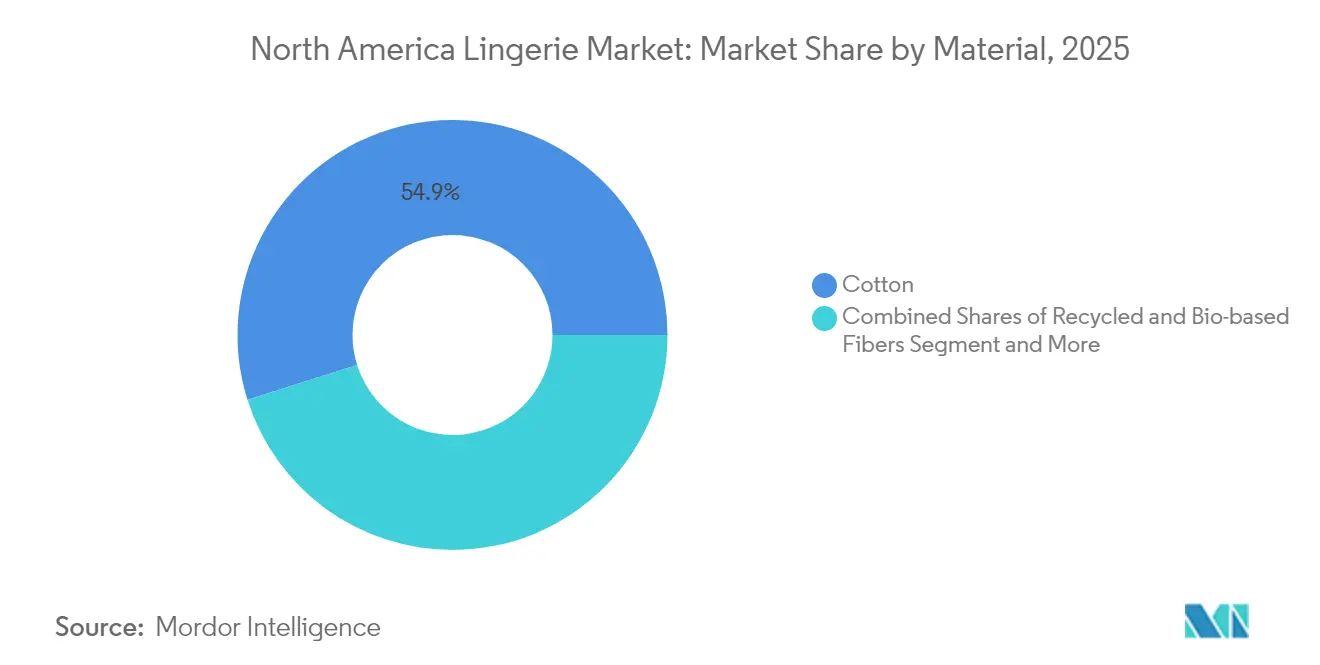

- By material, cotton accounted for 54.86% share of the North American lingerie market size in 2025, whereas recycled and bio-based fibers are expanding at a 5.58% CAGR.

- By distribution channel, specialty stores led with 40.27% revenue share in 2025, yet online retail stores are forecast to post a 6.53% CAGR through 2031.

- By geography, the United States captured 83.62% of North American lingerie market share in 2025, while Canada is expected to register a 6.42% CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Lingerie Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for Comfortable and Stylish Lingerie | +1.2% | North America, with strongest adoption in urban centers | Medium term (2-4 years) |

| Growth of Body Positivity and Size Inclusivity | +0.8% | United States and Canada, expanding to Mexico | Long term (≥ 4 years) |

| Impact of Social Media and Influencer Marketing | +0.6% | North America, particularly among Gen Z and Millennial demographics | Short term (≤ 2 years) |

| Rising Focus on Sustainability and Eco-friendly Materials | +0.5% | United States and Canada, with regulatory influence from GOTS and OEKO-TEX standards | Long term (≥ 4 years) |

| Innovations in Fabric and Design Technology | +0.4% | North America, with technology adoption led by premium brands | Medium term (2-4 years) |

| Expansion of E-Commerce and Online Sales | +0.9% | North America, accelerated by post-pandemic digital adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Demand for Comfortable and Stylish Lingerie

The convergence of comfort and style represents a fundamental shift in consumer priorities, moving beyond traditional aesthetic-focused purchasing decisions toward functionality-driven choices. This trend gained significant momentum during the pandemic as remote work normalized comfort-first apparel, with consumers increasingly refusing to compromise between appearance and wearability. The LYCRA Company's ADAPTIV fiber technology exemplifies this evolution, delivering dynamic compression that adapts to movement while maintaining shaping properties, addressing the core tension between support and comfort. American Eagle's Aerie brand capitalized on this shift, achieving record quarterly revenue of USD 539.7 million in Q4 2024 through collections emphasizing soft fabrics and wireless designs that prioritize comfort without sacrificing style. This driver particularly impacts the premium segment, where consumers demonstrate willingness to pay higher prices for innovative materials and construction techniques that deliver superior comfort. The trend extends beyond product features to encompass brand messaging, with successful companies positioning comfort as a form of self-care rather than compromise.

Growth of Body Positivity and Size Inclusivity

The body positivity movement has evolved from social activism into a core business imperative, fundamentally reshaping product development, marketing strategies, and brand positioning across the industry. This transformation extends beyond expanded size ranges to encompass inclusive design principles, diverse representation in marketing campaigns, and the rejection of traditional beauty standards that historically dominated lingerie advertising. American Eagle's Aerie brand demonstrates the commercial viability of this approach, achieving 21 consecutive quarters of double-digit comparable sales growth through 2024 by embracing unretouched photography and size inclusivity. The movement's impact transcends marketing aesthetics, driving substantive changes in product development processes, with brands investing in fit studies across diverse body types and expanding size ranges to accommodate previously underserved segments. Research indicates that over one-third of women fall between standard cup sizes, creating significant market opportunities for brands offering half-cup sizing and personalized fit solutions. This driver particularly benefits direct-to-consumer brands that can rapidly iterate product offerings based on customer feedback and data analytics.

Impact of Social Media and Influencer Marketing

Social media platforms have transformed lingerie marketing from traditional advertising to community-driven brand building, enabling direct consumer engagement and authentic product endorsement through influencer partnerships. This shift proves particularly powerful in intimate apparel, where traditional advertising often felt disconnected from real consumer experiences and body diversity. Platforms like Instagram and TikTok allow brands to showcase products on diverse body types, demonstrate fit and comfort through user-generated content, and build communities around shared values rather than aspirational imagery alone. The effectiveness of this approach is evidenced by digitally native brands achieving significant market penetration despite limited traditional advertising budgets, leveraging organic social content and micro-influencer partnerships to drive awareness and conversion. Victoria's Secret's strategic pivot illustrates the urgency of this transformation, launching campaigns featuring diverse talent and authentic storytelling to reconnect with consumers who had migrated to more inclusive brands. The channel's impact extends beyond marketing to product development, with social media feedback directly informing design decisions and size range expansions.

Innovations in Fabric and Design Technology

Technological advancement in textile engineering has unlocked new performance capabilities that address longstanding consumer pain points while enabling entirely new product categories and market segments. Smart textiles incorporating phase-change materials, moisture-wicking properties, and temperature regulation represent the convergence of fashion and function, creating competitive advantages for brands that successfully integrate these innovations. Outlast Technologies' temperature regulation technology, utilizing microencapsulated phase-change wax, demonstrates how advanced materials can deliver measurable comfort benefits, claiming up to 48% reduction in sweat production. These innovations particularly impact the sports bra and activewear segments, where performance requirements drive premium pricing and brand differentiation. Nike's development of wearable pump-compatible sports bras for mothers illustrates how technology can address specific consumer needs while creating new market categories. The driver's medium-term impact reflects the time required for technology adoption and consumer education, but early movers gain significant competitive advantages through patent protection and brand association with innovation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from Fast Fashion and Private Labels | -0.7% | North America, with particular pressure in Mexico from Chinese platforms | Short term (≤ 2 years) |

| Proliferation of Counterfeit and Low-Quality Products | -0.4% | United States and Canada, with enforcement challenges in cross-border e-commerce | Medium term (2-4 years) |

| Fit-related Concerns in Online Purchases | -0.5% | North America, affecting all demographics but particularly older consumers | Medium term (2-4 years) |

| Rapidly Changing Fashion Trends | -0.3% | North America, with fastest impact on younger consumer segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of Counterfeit and Low-Quality Products

Counterfeit intimate apparel poses multifaceted challenges encompassing consumer safety, brand integrity, and market share erosion, with enforcement complexity amplified by cross-border e-commerce and sophisticated distribution networks. U.S. Customs and Border Protection seized counterfeit goods worth nearly USD 1.3 billion in fiscal 2020, with wearing apparel and accessories representing 26.2% of seizure lines by count, indicating the scale of illicit trade affecting legitimate market participants [1]Source: U.S. Customs and Border Protection, "The Truth Behind Counterfeits", cbp.gov. The largest-ever counterfeit goods seizure in U.S. history occurred in 2023, involving approximately 219,000 items with an estimated manufacturer's suggested retail price of about USD 1.03 billion, demonstrating the sophisticated operations undermining authentic brands [2]Source: U.S. Attorney's Office, Southern District of New York, "Largest-Ever Counterfeit Goods Seizures Result In Trafficking Charges Against Two Individuals", justice.gov. E-commerce platforms facilitate counterfeit distribution, with over 90% of intellectual property rights seizures occurring in international mail and express shipments, complicating enforcement efforts and consumer protection. The restraint particularly impacts premium brands whose higher price points create attractive targets for counterfeiters, while consumer safety concerns arise from substandard materials that may not meet flammability standards required under the Consumer Product Safety Commission's Flammable Fabrics Act [3]Source: U.S. Consumer Product Safety Commission, "Flammable Fabrics Act (FFA)", cpsc.gov.

Rapidly Changing Fashion Trends

Accelerated trend cycles driven by social media and fast fashion have compressed product development timelines while increasing inventory risk, forcing brands to balance trend responsiveness with sustainable business practices and quality standards. This dynamic particularly challenges intimate apparel brands that traditionally operated on seasonal collections and longer product lifecycles, now facing pressure to introduce new styles and colorways at unprecedented frequency. The tension between trend-driven demand and the intimate nature of lingerie purchases creates complex consumer behavior patterns, where some segments prioritize fashion-forward designs while others seek timeless, high-quality pieces that transcend seasonal trends. Social media platforms amplify trend velocity by enabling rapid style dissemination and creating viral moments that can drive sudden demand spikes for specific products or aesthetics, requiring sophisticated demand forecasting and agile supply chain capabilities. Brands must navigate this environment while maintaining brand identity and quality standards, as the intimate nature of the category means that poor-quality trend pieces can damage long-term customer relationships more severely than in other fashion categories. The restraint's short-term impact reflects the immediate pressure on inventory management and product development cycles, while the long-term implications include potential brand dilution and increased operational complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Brassieres Dominate Despite Brief Innovation

Brassieres command 52.05% market share in 2025, reflecting their fundamental role in women's wardrobes and the category's continued innovation in comfort, support, and style integration. However, briefs emerge as the fastest-growing segment with 4.96% CAGR through 2031, driven by technological advances in moisture-wicking fabrics, seamless construction, and body-positive sizing approaches that address previously underserved market segments. The brassiere segment's dominance stems from higher average selling prices and frequent replacement cycles, with consumers increasingly willing to invest in premium options that deliver superior fit and comfort. Victoria's Secret's Dream Collection launch in 2024, featuring ForeverStretch Lace and Marshmallow Memory Foam padding across sizes 32-40 bands and A-G cups, illustrates how established players are innovating within traditional categories to maintain market leadership.

Other product types, including shapewear, loungewear, and specialty items, represent emerging opportunities as consumer preferences expand beyond traditional intimate apparel categories. The convergence of activewear and intimate apparel has created hybrid products that serve multiple functions, appealing to consumers seeking versatility and value in their purchases. Nike's development of pump-compatible sports bras demonstrates how major brands are expanding into specialized segments that address specific consumer needs while commanding premium pricing. Regulatory compliance factors, particularly Consumer Product Safety Commission flammability standards under 16 CFR Part 1610, influence product development across all segments, requiring manufacturers to ensure materials meet safety requirements while maintaining aesthetic and functional properties.

By Price Range: Premium Growth Outpaces Mass Market

The mass market segment maintains 70.18% share in 2025, reflecting the broad consumer base seeking accessible pricing for essential intimate apparel, yet premium offerings surge ahead with 6.05% CAGR, indicating significant opportunities for brands that successfully differentiate through quality, innovation, and brand positioning. This divergence reflects a bifurcating market where value-conscious consumers gravitate toward functional, affordable options while a growing segment prioritizes premium features, sustainable materials, and personalized experiences worth higher price points. American Eagle's Aerie brand exemplifies successful premium positioning within accessible luxury, achieving record revenues through inclusive sizing, body-positive messaging, and quality construction that justifies price premiums over fast fashion alternatives.

Victoria's Secret's collaboration with designer Joseph Altuzarra, launching limited-edition pieces priced between USD 95-500, demonstrates how established brands are exploring ultra-premium segments to capture consumers willing to pay luxury prices for exclusive designs and superior craftsmanship. The premium segment's growth trajectory benefits from technological innovations like LYCRA ADAPTIV fiber, which enables brands to deliver measurable performance improvements that justify higher pricing through enhanced comfort and durability. Direct-to-consumer brands particularly benefit from this trend, as they can capture the full margin structure while investing in premium materials, innovative construction techniques, and personalized customer experiences that traditional wholesale models cannot economically support.

By Material: Cotton Leads While Sustainable Fibers Gain Momentum

Cotton maintains 54.86% market share in 2025 due to its natural breathability, comfort properties, and consumer familiarity, yet recycled and bio-based fibers represent the fastest-growing segment at 5.58% CAGR, reflecting accelerating sustainability demands and regulatory pressures for circular economy adoption. This growth trajectory indicates a fundamental shift in consumer values, particularly among younger demographics who prioritize environmental responsibility and are willing to pay premium prices for verified sustainable materials. OEKO-TEX and Global Organic Textile Standard (GOTS) certifications have become critical differentiators, providing third-party verification of environmental and social responsibility claims that increasingly influence purchasing decisions.

Silk and satin segments serve niche luxury markets where aesthetic appeal and premium positioning justify higher price points, while synthetic materials continue evolving through technological advancement in moisture management, durability, and comfort properties. The synthetic segment benefits from innovations like Outlast Technologies' temperature regulation fibers, which deliver measurable performance improvements that natural materials cannot match. Between the Sheets' use of FSC-certified modal fibers and domestic manufacturing illustrates how premium brands are building entire value propositions around sustainable material sourcing and transparent supply chains. Regulatory compliance factors, including OEKO-TEX Standard 100 testing for harmful substances, increasingly influence material selection as brands seek to minimize consumer safety risks while meeting environmental standards that appeal to conscious consumers.

By Distribution Channel: Digital Transformation Accelerates

Specialty stores command 40.27% market share in 2025, leveraging personalized fitting services, expert consultation, and curated product selections that address the intimate nature of lingerie purchasing, yet online retail stores project 6.53% CAGR growth, representing the fastest-expanding channel as digital natives mature and virtual fitting technologies improve. This channel evolution reflects broader retail transformation accelerated by pandemic-driven behavioral changes, with consumers who initially embraced online purchasing out of necessity now permanently integrating digital channels into their shopping behaviors. ThirdLove's expansion from pure direct-to-consumer into wholesale partnerships with Neiman Marcus and Amazon marketplace presence illustrates how digitally native brands are adopting omnichannel strategies to capture broader market opportunities.

Supermarkets and hypermarkets serve the convenience and value segments, offering basic intimate apparel alongside other household essentials, while other distribution channels include department stores, outlet centers, and emerging subscription services that provide personalized curation and automatic replenishment. The online channel's growth trajectory benefits from technological solutions addressing traditional fit concerns, with virtual sizing tools and comprehensive return policies reducing purchase barriers that historically limited digital adoption. Fit Analytics' size recommendation engine, powered by machine learning and billions of purchase records, demonstrates how technology can address the fundamental challenge of online intimate apparel shopping. The channel transformation particularly impacts inventory management and customer acquisition costs, as brands must balance the efficiency of digital fulfillment with the higher marketing investments required to drive online discovery and conversion.

Geography Analysis

The United States anchors the North American lingerie market with 83.62% share in 2025, driven by a mature consumer base, sophisticated retail infrastructure, and cultural leadership in intimate apparel trends that influence global market directions. American consumers demonstrate increasing sophistication in their purchasing decisions, prioritizing fit, comfort, and brand values over traditional price-focused considerations, creating opportunities for premium positioning and innovative product development. Victoria's Secret's strategic repositioning through designer collaborations and inclusive sizing, combined with Aerie's continued market share gains through body-positive messaging, illustrates the competitive dynamics reshaping the U.S. market. The market benefits from strong e-commerce infrastructure and consumer comfort with online intimate apparel purchasing, supported by comprehensive return policies and emerging virtual fitting technologies that address traditional sizing concerns.

Canada emerges as the fastest-growing geography with 6.42% CAGR through 2031, reflecting expanding disposable income, increasing awareness of premium intimate apparel options, and growing adoption of direct-to-consumer brands that offer expanded sizing and inclusive messaging. Canadian consumers demonstrate particular interest in sustainable and ethically produced intimate apparel, creating opportunities for brands that can credibly communicate environmental and social responsibility throughout their supply chains. Statistics Canada's classification systems for women's lingerie, sleepwear, and underwear provide structured frameworks for market analysis, while retail sales data indicates resilient demand despite economic volatility Statistics. ThirdLove's expansion into Canadian shipping with localized pricing and customer service demonstrates how successful brands are adapting their direct-to-consumer models for cross-border growth.

Mexico represents an emerging opportunity within the North American market, though growth faces headwinds from economic challenges, currency fluctuations, and intense competition from low-cost imports that pressure both domestic manufacturing and retail pricing structures. The Mexican textile industry has lost approximately 80,000 jobs from peak employment levels as Chinese fast fashion platforms like Shein and Temu capture market share through ultra-low pricing enabled by favorable import regulations. Government responses include a 35% tariff on textile imports from countries without free trade agreements and enhanced traceability requirements for e-commerce orders, but enforcement challenges persist in digital channels. Mexican consumer spending data shows modest growth, with private consumption increasing 0.2% month-over-month in August 2024, indicating cautious but positive demand trends that could support premium intimate apparel positioning. The market's long-term potential depends on economic stability, middle-class expansion, and successful differentiation from low-cost alternatives through quality, fit, and brand positioning strategies.

Competitive Landscape

The North American lingerie market exhibits moderate concentration, indicating significant opportunities for both consolidation by established players and market entry by innovative newcomers who can differentiate through technology, sustainability, or inclusive positioning. Legacy incumbents like Victoria's Secret are executing strategic repositioning initiatives, including designer collaborations and expanded size ranges, while simultaneously facing market share erosion to digitally native brands that better align with evolving consumer values around body positivity and authentic brand messaging.

American Eagle's Aerie brand exemplifies successful disruption within established retail frameworks, achieving 21 consecutive quarters of double-digit growth by embracing unretouched photography, inclusive sizing, and comfort-focused product development that resonates with younger demographics. The competitive landscape increasingly rewards brands that can successfully integrate omnichannel distribution strategies, with pure-play e-commerce companies like ThirdLove expanding into wholesale partnerships while traditional retailers enhance their digital capabilities and direct-to-consumer offerings. Regulatory compliance factors, particularly Consumer Product Safety Commission flammability standards and OEKO-TEX certifications, create barriers to entry that favor established players with sophisticated supply chain management capabilities while simultaneously providing differentiation opportunities for brands that exceed minimum requirements.

Technology adoption has become a critical competitive differentiator, with successful brands leveraging virtual fitting solutions, AI-powered size recommendations, and advanced fabric innovations to address longstanding consumer pain points around fit and comfort. PVH Corp's divestiture of its Heritage Brands women's intimate’s business in November 2023 illustrates how major apparel conglomerates are focusing resources on core brands like Calvin Klein while exiting lower-margin intimate apparel operations. Opportunities exist in sustainable luxury positioning, adaptive intimate apparel for specific consumer needs, and technology-enabled personalization that goes beyond traditional sizing to encompass individual preferences for support, coverage, and aesthetic appeal.

North America Lingerie Industry Leaders

-

PVH Corp.

-

Nike Inc.

-

Victoria's Secret & Co.

-

HANESBRANDS INC.

-

AEO Management Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Victoria's Secret announced the launch of its addition to the Body by Victoria collection, which featured the Body by Victoria FlexFactor Lightly Lined Plunge Demi Bra. Body by Victoria was the brand's premier collection, debuting its newest silhouette that was designed with precise bra technology to create a barely there, wireless feel for everyday movement and absolute support. The one Body by Victoria collection enhanced its selection of seamless styles, featuring the FlexFactor Bra with unmatched support that felt better than being braless.

- July 2025: Wacoal America announced the launch of the Ever-Flexing Underwire Bra, a first-of-its-kind innovation engineered to flex across six traditional sizes, redefining how women experienced support, comfort, and fit. Designed in response to the realities of women's ever-changing bodies, the Ever-Flexing bra met the moment for those experiencing everything from hormonal shifts and pregnancy to menopause and the effects of weight-loss medications.

- July 2025: Shapermint, one of the world's fastest-growing and leading intimate apparel brands, officially launched in Canada. Known for defining the category of comfortable shaping essentials--intimates and apparel that shaped while being comfortable for everyday use--Shapermint offered a wide range of comfortable shaping essentials, from shaping shorts and wireless bras to leggings and camis, engineered for comfort, support, and value.

- March 2025: The Understance boutique opened its doors in Burnaby at Unit #2150, 4700 Kingsway St. Building on the success of its Calgary and Toronto store openings late last year, the brand expanded its reach and worked toward its vision of making solution-based lingerie more accessible across Canada.

North America Lingerie Market Report Scope

Lingerie is a niche category of women's clothing comprising undergarments, primarily bras and panties, loungewear, and lightweight robes commonly made using silk or satin materials.

The North American lingerie market is segmented by product type, distribution channel, and geography. By product type, the market is segmented into brassiere, briefs, and other product types. The market is segmented by distribution channel into supermarkets/hypermarkets, specialty stores, online retail stores, and other distribution channels. The report analyzes emerging and established economies across the region, comprising the United States, Canada, Mexico, and the Rest of North America. The market sizing and forecasts have been done for each segment based on value (USD).

By Product Type

| Brassiere |

| Briefs |

| Other Product Types |

By Price Range

| Mass |

| Premium |

By Material

| Cotton |

| Silk and Satin |

| Synthetic |

| Recycled and Bio-based Fibers |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Brassiere |

| Briefs | |

| Other Product Types | |

| By Price Range | Mass |

| Premium | |

| By Material | Cotton |

| Silk and Satin | |

| Synthetic | |

| Recycled and Bio-based Fibers | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

What is the current value of the North American lingerie market?

The market was valued at USD 15.21 billion in 2026 and is projected to reach USD 18.75 billion by 2031.

Which product category leads sales?

Brassieres hold the largest share at 52.05% of 2025 revenue.

Which channel is growing fastest for lingerie sales in North America?

Online retail stores are forecast to expand at a 6.53% CAGR through 2031.

Which geography shows the highest growth outlook through 2031?

Canada is expected to post a 6.42% CAGR, outpacing the regional average.

Page last updated on: