Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

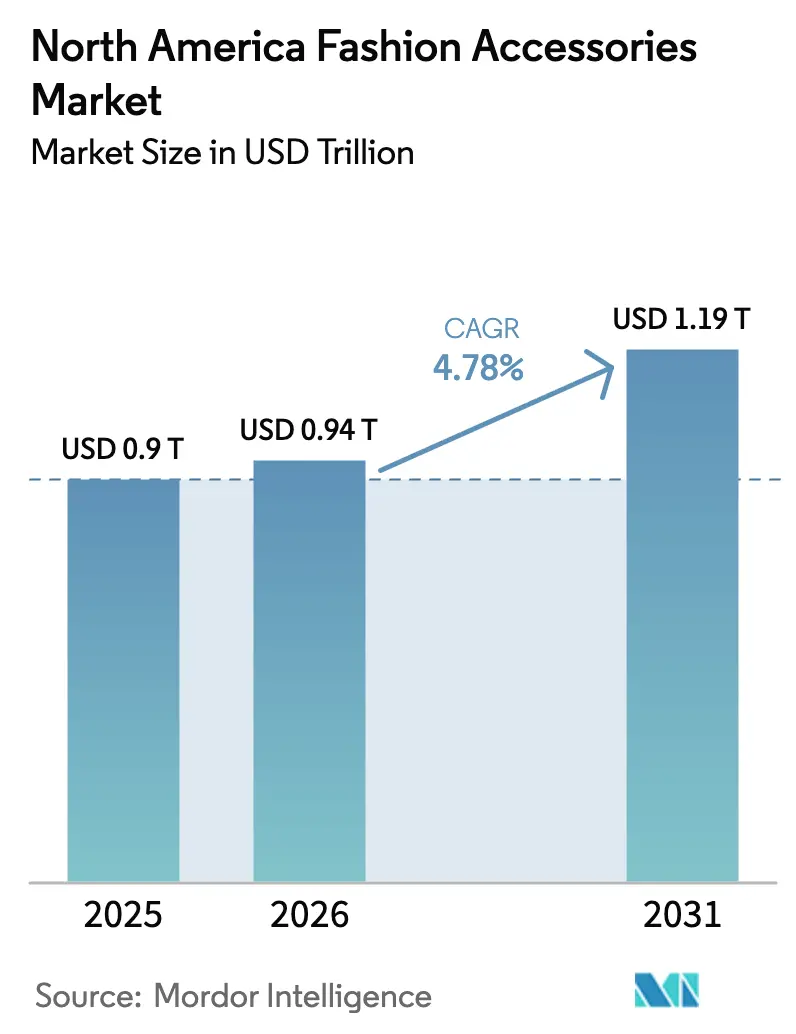

| Base Year Market Size (2025) | USD 0.90 Trillion |

| Market Size (2026) | USD 0.94 Trillion |

| Market Size (2031) | USD 1.19 Trillion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

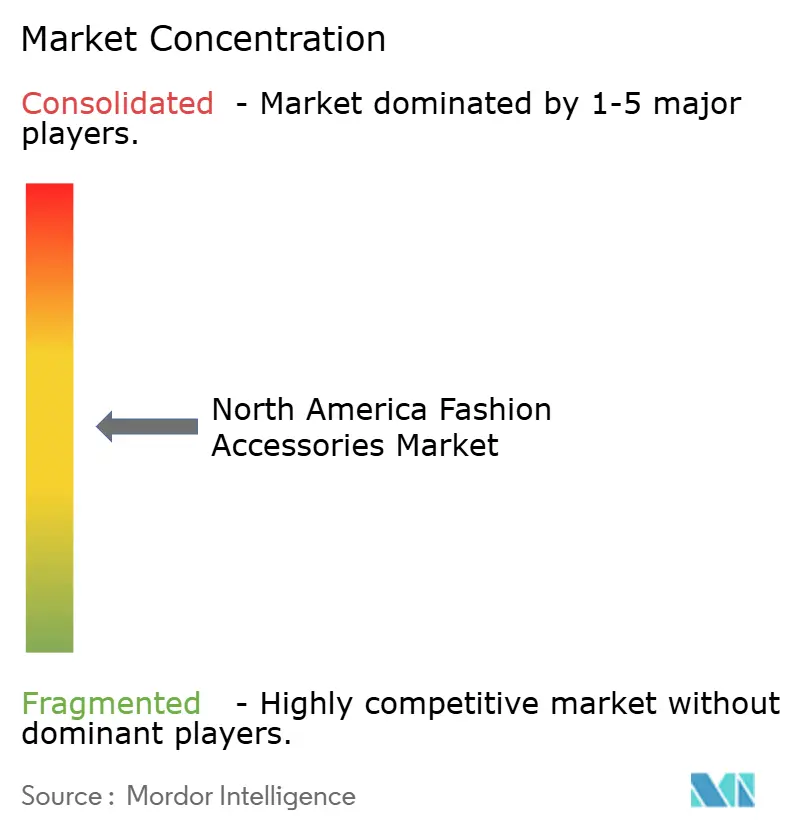

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Fashion Accessories Market Analysis by Mordor Intelligence

North American fashion accessories market size in 2026 is estimated at USD 0.94 trillion, growing from 2025 value of USD 0.90 trillion with 2031 projections showing USD 1.19 trillion, growing at 4.78% CAGR over 2026-2031. The current expansion is powered by digital-first retail formats, rising eco-awareness, and social-media-led trend cycles that reward brands able to blend functionality with prestige. Consumers have tightened discretionary budgets, yet they still trade up for accessories that communicate status or add meaningful utility, illustrating the market’s ability to absorb macro volatility. Apparel add-ons such as belts, scarves, and hats remain wardrobe staples, whereas watches are enjoying a renaissance owing to luxury horology and smart-wearable convergence. Additionally, Mexico’s urban middle class is lifting regional growth momentum, while the United States continues to anchor volumes and brand innovation. A steady pivot toward omnichannel experiences and traceable supply chains keeps reshaping competitive strategy across the North American fashion accessories market

Key Report Takeaways

- By product category, apparel accessories led with 57.10% revenue share in 2025; watches are projected to expand at a 5.05% CAGR through 2031.

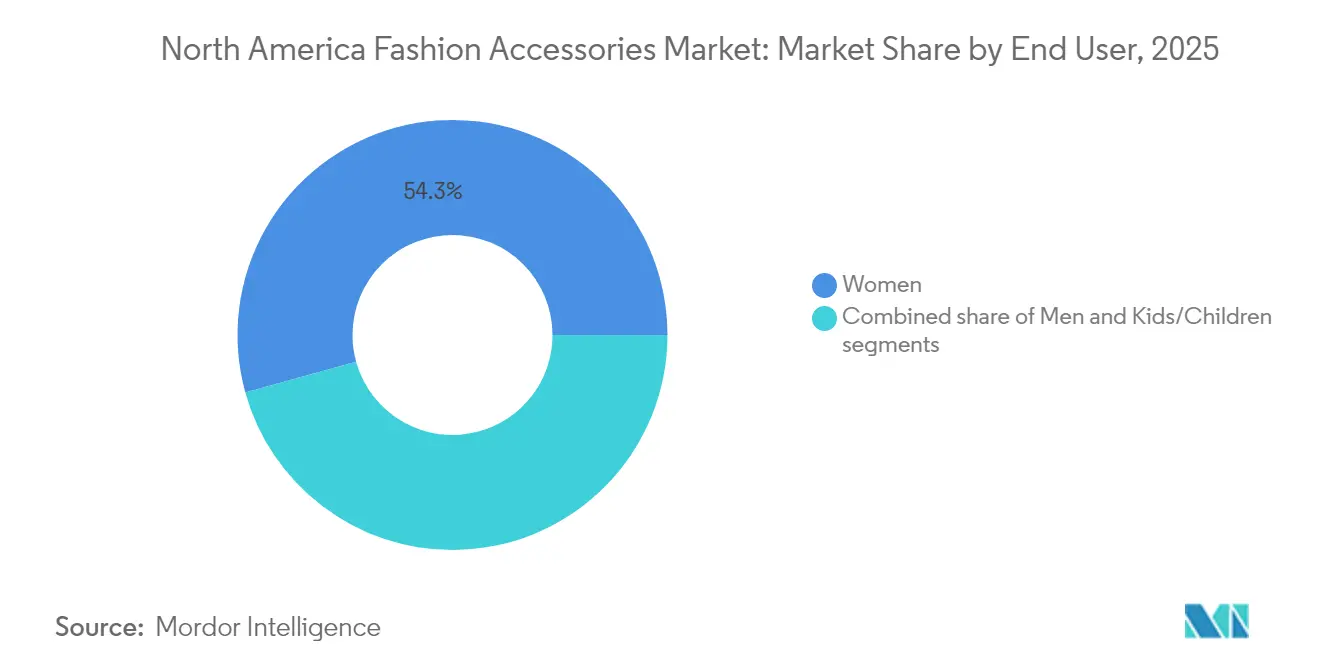

- By end user, women captured 54.30% of the North American fashion accessories market share in 2025, while the children’s segment records the fastest 5.31% CAGR.

- By category, the mass tier captured 65.00% share of the North American fashion accessories market size in 2025, while the premium tier is forecast to grow 5.73% annually to 2031.

- By distribution channel, offline retail controlled 68.10% share in 2025; online sales are rising at a 6.02% CAGR and are set to reshape customer acquisition economics.

- By geography, the United States commanded 81.10% of 2025 revenue, whereas Mexico is advancing at a 6.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Fashion Accessories Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumers' inclination towards luxury and status symbols | +1.2% | United States and Canada, with spillover to Mexico urban centers | Medium term (2-4 years) |

| Technological advancements in terms of design and raw material | +0.8% | North America, with early adoption in regional tech hubs | Long term (≥ 4 years) |

| Influence of social media and celebrity endorsements | +1.1% | North America core, particularly among Gen Z and Millennial demographics | Short term (≤ 2 years) |

| Sustainability and eco-conscious consumer demand | +0.7% | United States and Canada primarily, emerging in Mexico | Medium term (2-4 years) |

| Rising demand for sportswear from fitness-conscious consumers | +0.9% | North America, with strongest growth in United States | Short term (≤ 2 years) |

| Seasonal spikes and the influence of gift-giving culture | +0.6% | North America, with peak impact during Q4 holiday seasons | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumers' Inclination Towards Luxury and Status Symbols

Consumer appetite for luxury fashion accessories remains robust in the region. This trend is fueled by rising disposable incomes, urbanization, and the growing influence of social media platforms that promote luxury lifestyles. The U.S. Census Bureau highlights that the median household income in the United States reached approximately USD 80,610 in 2023, indicating a robust consumer base for luxury goods [1]Source: United States Census Bureau, "Income in the United States: 2023", census.gov . Furthermore, the growing millennial and Gen Z population, who are more inclined toward branded and high-end products, is significantly contributing to this trend. This demographic shift creates opportunities for brands that authentically connect with diverse consumer identities while maintaining luxury positioning. The polarization between high-net-worth individuals and middle-income consumers drives market segmentation, with ultra-high net worth individuals stabilizing premium segments while mass market consumers seek value-driven luxury alternatives.

Technological Advancements in Terms of Design and Raw Material

Fashion accessory innovation is increasingly focusing on smart functionality and sustainable materials, leading to the emergence of new product categories that merge traditional craftsmanship with modern technology. Notable advancements include the introduction of photochromic fiber displays, which allow for interactive and customizable light effects in textiles, marking a significant leap in wearable technology. Beyond mere aesthetics, material innovations are tackling sustainability challenges head-on. Brands are now turning to lab-grown leather alternatives and recycled precious metals, aligning with consumer demands for environmental responsibility. Furthermore, the infusion of artificial intelligence into design processes is paving the way for mass customization. This shift empowers brands to deliver personalized accessories on a larger scale without compromising on cost efficiency. Such technological strides not only offer a competitive edge to early adopters but also reshape consumer expectations, emphasizing functionality and environmental stewardship.

Influence of Social Media and Celebrity Endorsements

Social media platforms and celebrity endorsements significantly drive the market. The increasing penetration of social media has transformed how consumers discover and engage with fashion trends. Platforms like Instagram, TikTok, and Pinterest have become key channels for brands to showcase their products, leveraging influencers and celebrities to amplify their reach. According to StatCounter, Facebook dominated the social media landscape in May 2025, accounting for 57.91% of usage share, while Pinterest captured 16.54% and Instagram held 8.35%, highlighting the vast audience available for targeted marketing campaigns [2]Source: Statcounter Global Stats, “Social Media Stats Canada”, gs.statcounter.com . Celebrity endorsements further enhance brand visibility and credibility, influencing consumer purchasing decisions. The combination of social media influence and celebrity endorsements continues to shape consumer preferences, making it a critical driver for the fashion accessories market in North America.

Sustainability and Eco-conscious Consumer Demand

The growing emphasis on sustainability is significantly driving the North American fashion accessories market. Consumers in the region are increasingly prioritizing eco-friendly and sustainable products, reflecting a shift in purchasing behavior. This trend is fueled by heightened awareness of environmental issues, the adverse effects of fast fashion, and the desire to reduce carbon footprints. Fashion accessory manufacturers are responding by adopting sustainable practices, including the use of recycled and biodegradable materials, reducing production waste, and ensuring the ethical sourcing of raw materials. Furthermore, companies are investing in innovative technologies to create sustainable alternatives that do not compromise on quality or design. Brands are also leveraging eco-conscious marketing strategies, including transparent communication about their sustainability initiatives, to appeal to this growing segment of environmentally aware consumers. The rise of second-hand and upcycled fashion accessories is another notable trend, as consumers increasingly seek products that align with their values.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit products | -0.9% | North America, with highest impact in United States border regions | Short term (≤ 2 years) |

| Supply chain disruptions | -0.7% | North America, with particular vulnerability in Mexico-United States trade corridor | Medium term (2-4 years) |

| Fluctuating raw material prices | -0.5% | North America, with regional variations based on sourcing patterns | Short term (≤ 2 years) |

| Rising trade barriers and tariffs | -0.8% | United States primarily, with spillover effects to Canada and Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Counterfeit Products

The proliferation of counterfeit products poses a significant restraint on the North American fashion accessories market. Counterfeit goods, often sold at lower prices, undermine the revenue of legitimate brands and erode consumer trust. These fake products not only impact brand reputation but also lead to financial losses for manufacturers and retailers. The availability of counterfeit fashion accessories, facilitated by online platforms and unregulated markets, has further exacerbated the issue. Additionally, consumers purchasing counterfeit items may face quality and safety concerns, which can tarnish the overall perception of the fashion accessories market. The increasing sophistication of counterfeiters, who replicate designs and branding with high accuracy, makes it challenging for companies to combat this issue effectively. As a result, brands are compelled to invest heavily in anti-counterfeiting measures, such as advanced labeling technologies and legal actions, which increase operational costs.

Rising Trade Barriers and Tariffs

Rising trade barriers and tariffs are major challenges for the North American fashion accessories market. Higher tariffs on imported goods, especially from countries like China, have made raw materials and finished products more expensive. This has disrupted supply chains and forced businesses to either bear the extra costs or increase prices for consumers. For example, the Office of the United States Trade Representative (USTR) reports that the United States currently has a trade-weighted average import tariff rate of 2.0% on industrial goods and could increase [3]Source: Office of the United States Trade Representative, "Industrial Tariffs", ustr.gov. The United States-Mexico-Canada Agreement (USMCA) has also introduced new trade rules. While these rules aim to boost regional trade, they have made compliance more complicated for businesses. Small and medium-sized businesses in the fashion accessories market are particularly affected, as they often lack the resources to handle these challenges. Additionally, Canada has imposed retaliatory tariffs on U.S. goods due to trade disputes, making cross-border trade even harder. These trade policies are reducing profits and slowing down growth in the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Apparel Dominance Faces Watch Innovation

Apparel add-ons dominated the revenue landscape in 2025, accounting for a substantial 57.10%. This highlights their widespread adoption in daily wear, driven by their versatility across varying climates and cultural contexts. These add-ons, which include items such as scarves, belts, hats, and gloves, have become essential components of consumers' wardrobes. Their ability to seamlessly blend functionality with style has made them a preferred choice for individuals looking to enhance their outfits. Additionally, the growing influence of social media and fashion influencers has further propelled the demand for these accessories, as consumers increasingly seek to emulate trending styles and personalize their looks.

Watches, while representing a smaller segment within the market, are experiencing notable growth. With a projected CAGR of 5.05% through 2031, this category is gaining traction due to increasing consumer interest in both traditional and smart timepieces. Traditional watches continue to hold their appeal as timeless fashion statements, while smartwatches are driving innovation with features such as fitness tracking, health monitoring, and connectivity. The rising adoption of wearable technology, coupled with the growing preference for multifunctional accessories, is fueling this growth. Furthermore, the premium and luxury watch segment is also witnessing steady demand, supported by brand-conscious consumers and the perception of watches as status symbols. These factors collectively contribute to the expanding role of watches in the North American Fashion Accessories Market.

By Category: Premium Growth Outpaces Mass Market

Mass-market fashion accessories dominated the revenue landscape in 2025, accounting for a substantial 65.00%. This highlights their widespread adoption in daily wear, driven by affordability, accessibility, and versatility across varying climates and cultural contexts. Mass-market accessories, such as scarves, belts, hats, and costume jewelry, cater to a broad consumer base seeking stylish yet budget-friendly options. The rise of fast fashion and the growing influence of e-commerce platforms have further propelled the demand for these products, as consumers increasingly prioritize convenience and variety. Additionally, the introduction of sustainable and eco-friendly materials in mass-market accessories is gaining traction, aligning with the preferences of environmentally conscious buyers and enhancing the appeal of this segment.

Premium fashion accessories, while representing a smaller segment, are experiencing notable growth and are growing at a CAGR of 5.73% annually due to their association with quality, exclusivity, and brand value. Items such as luxury handbags, high-end watches, and fine jewelry are highly sought after by consumers who view them as status symbols and long-term investments. The premium segment is driven by affluent consumers and the rising trend of aspirational purchasing, where individuals seek to own luxury items as a mark of success. Furthermore, the increasing focus on craftsmanship, innovative designs, and the use of premium materials has elevated the appeal of these products. The growing presence of premium brands on digital platforms and their targeted marketing strategies have also contributed to the expanding role of premium accessories in the market.

By End User: Women Lead While Children Accelerate

Women’s accessories dominated the revenue landscape in 2025, accounting for a substantial 54.30%. In North America, consumer demand for women's fashion accessories continues to expand, driven by increased disposable income levels, customization requirements, and individual expression preferences. The handbags and purses segment demonstrates the highest growth rate, while jewelry maintains revenue leadership, indicating sustained consumer investment in both premium and essential accessories. Digital retail channels and social media marketing, specifically through Instagram and TikTok platforms, accelerate market trends and increase demand for multi-functional products, including belt bags, statement jewelry, decorative headbands, and hair accessories. For instance, Pop & Suki's millennial-pink camera bag illustrates this market transformation, delivering customizable products that meet North American female consumer preferences.

The children's fashion accessories segment demonstrates a CAGR of 5.31%, attributed to increased consumer demand for products combining aesthetic appeal and practical utility. Items such as hats, gloves, backpacks, and hair accessories are witnessing steady demand, driven by the growing trend of mini-me fashion, where parents dress their children in styles that mirror adult fashion. The rising popularity of character-themed accessories, inspired by movies, cartoons, and popular franchises, is also fueling growth in this segment. Furthermore, the emphasis on safety and comfort in children’s products has led to the introduction of accessories made from hypoallergenic and durable materials.

By Distribution Channel: Digital Transformation Accelerates

Offline stores continue to dominate the market, accounting for a 68.10% share of the revenue in 2025. These stores remain a preferred shopping channel for consumers who value the tactile experience of trying on accessories such as handbags, watches, and jewelry before making a purchase. Brick-and-mortar stores, including department stores, specialty stores, and brand-exclusive outlets, benefit from their ability to offer personalized customer service and immediate product availability. Additionally, the strategic placement of offline stores in high-traffic areas, such as malls and shopping districts, enhances their accessibility and visibility. Seasonal promotions, in-store events, and exclusive collections further attract foot traffic, solidifying the role of offline stores in driving sales within the fashion accessories market.

Online stores, on the other hand, are witnessing rapid growth and are projected to grow at a CAGR of 6.02%. The convenience of shopping from home, coupled with the availability of a wide range of products, has made e-commerce platforms increasingly popular among consumers. Online stores offer competitive pricing, frequent discounts, and easy comparison of products, which appeal to price-sensitive buyers. The integration of advanced technologies, such as augmented reality (AR) for virtual try-ons and artificial intelligence (AI) for personalized recommendations, has further enhanced the online shopping experience. Additionally, the rise of social commerce, where consumers purchase directly through social media platforms, is driving the growth of online sales. With the increasing penetration of smartphones and improved internet connectivity, online stores are expected to play a pivotal role in shaping the future of the market.

Geography Analysis

In 2025, the United States commands a dominant 81.10% share of the North American fashion accessories market. This stronghold is bolstered by the nation's robust consumer spending power, its cultural sway over global fashion trends, and a sophisticated retail infrastructure that caters to a wide array of consumer preferences. For instance, the popularity of smartwatches and fitness trackers among tech-savvy consumers highlights the integration of technology into fashion accessories. Additionally, traditional luxury brands like Tiffany & Co. and Coach continue to thrive, appealing to high-net-worth individuals who regard these accessories as investment pieces rather than mere fashion items.

Canada stands out as a stable secondary market, marked by distinct seasonal purchasing patterns and a penchant for cross-border shopping. These behaviors introduce unique competitive dynamics. For example, Canadian consumers often shop for winter accessories such as scarves and gloves during colder months, while cross-border shopping with the United States influences purchasing decisions. Canadian shoppers increasingly favor sustainable and ethically sourced accessories. This trend presents a golden opportunity for brands that prioritize environmental responsibility and social impact, such as Matt & Nat, a Canadian brand known for its vegan and eco-friendly products. However, the market grapples with challenges related to counterfeit enforcement.

Mexico is on the rise, boasting the title of the fastest-growing market with a projected 6.32% CAGR through 2031. This growth is fueled by an expanding middle class, rising disposable incomes, and a heightened fashion consciousness among urban dwellers. For example, the increasing popularity of affordable yet stylish accessories from local brands and international players like Zara and H&M reflects the growing demand for fashion-forward products in urban areas. Additionally, the influence of social media and e-commerce platforms has significantly shaped consumer behavior in Mexico, with younger demographics driving demand for trendy and affordable accessories.

Competitive Landscape

The North American fashion accessories market demonstrates moderate fragmentation among industry participants. This score highlights a competitive landscape where established luxury conglomerates, such as LVMH and Kering, coexist with emerging direct-to-consumer brands like Mejuri and MVMT, as well as regional specialists catering to localized preferences. Major players are increasingly turning to vertical integration, aiming to tighten their grip on supply chains and elevate customer experiences. For instance, luxury brands are acquiring raw material suppliers and investing in in-house manufacturing to ensure quality control and faster time-to-market.

Meanwhile, challenger brands are carving out their niche, capturing market share through targeted positioning and genuine brand stories that resonate deeply with select consumer segments. Brands like Allbirds and Rothy’s, for example, have gained traction by emphasizing sustainability and eco-friendly practices, appealing to environmentally conscious consumers. These companies leverage their unique value propositions to differentiate themselves in a crowded market, often using social media and influencer marketing to amplify their reach.

Technology is a pivotal differentiator in this arena, with companies channeling investments into innovative solutions to stay ahead. Artificial intelligence is being utilized for personalized recommendations, enabling brands to offer tailored product suggestions based on consumer preferences and behavior. Augmented reality tools, such as virtual try-ons offered by brands like Warby Parker, enhance the online shopping experience by allowing customers to visualize products before purchase. Additionally, blockchain technology is being adopted to improve supply chain transparency, addressing growing consumer demands for authenticity and sustainability.

North America Fashion Accessories Industry Leaders

-

Tapestry, Inc.

-

LVMH Moët Hennessy Louis Vuitton SE

-

Fossil Group, Inc

-

Kering S.A.

-

Nike Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Kering Eyewear released two Gucci sunglasses designed specifically for travel retail in its spring/summer collection. The women's model incorporated a cat-eye shape with an interlocking G pattern on the temples. The sunglasses were available in black, Havana, burgundy, and white colors, with a gold-plated logo accent.

- February 2025: Nike introduced its signature shoe and apparel collection, "The Nike A'One," at the commencement of the 2025 WNBA season. The collection integrated performance features with style elements, demonstrating Nike's investment in women's basketball. The products were available at USD 110 for adult sizes and USD 90 for youth sizes.

- February 2025: Nike established a partnership with Kim Kardashian's Skims to introduce NikeSkims, a women's fitness brand that offered apparel, footwear, and accessories. The collection focused on body-fitting activewear to address the athleisure market segment.

- November 2024: Adidas released the Supernova Rise 2 collection, which incorporated a breathable upper design and improved heel construction with a foam collar to enhance comfort and stability for everyday runners.

North America Fashion Accessories Market Report Scope

A fashion accessory is a decorative item that supplements one's outfit. Items such as jewelry, handbags, belts, watches, and sunglasses, among others have been covered in our study scope. A fashion accessory 'contributes' or is 'part of an outfit. The North American fashion accessories market (henceforth referred to as the market studied) is segmented by product type, end-user, distribution channel, and geography. By product type, the market is segmented into apparel, footwear, handbags, wallet, watches, and other product types. By end user, the market is segmented into men, women, children, and unisex. Based on the distribution channel, the market studied is segmented into online retail stores and offline retail stores.

It provides an analysis of leading North American markets like the United States, Canada, Mexico, and the Rest of North America. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Footwear |

| Apparel |

| Wallets |

| Handbags |

| Watches |

| Sunglasses |

| Jewelery |

By End User

| Men |

| Women |

| Kids/Children |

By Category

| Mass |

| Premium |

By Distribution Channel

| Offline Stores |

| Online Stores |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Footwear |

| Apparel | |

| Wallets | |

| Handbags | |

| Watches | |

| Sunglasses | |

| Jewelery | |

| By End User | Men |

| Women | |

| Kids/Children | |

| By Category | Mass |

| Premium | |

| By Distribution Channel | Offline Stores |

| Online Stores | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

What is the current value of the North American fashion accessories market?

The marketplace generated USD 0.94 trillion in 2026 and is forecast to rise to USD 1.19 trillion by 2031.

Which product segment is expanding the fastest?

Watches are leading with a 5.05% CAGR, fueled by luxury collectors and smart-wearable features.

Why is Mexico viewed as a growth hotspot?

Urban middle-class expansion, digital-commerce penetration, and fashion-conscious youth underpin Mexico’s 6.32% CAGR through 2031.

Which distribution channel is gaining ground the quickest?

Online stores are growing at a 6.02% CAGR, outpacing physical retail as consumers embrace omnichannel shopping journeys.

Page last updated on: