Luxury Footwear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 50.55 Billion |

| Market Size (2031) | USD 62.54 Billion |

| Growth Rate (2026 - 2031) | 4.35% CAGR |

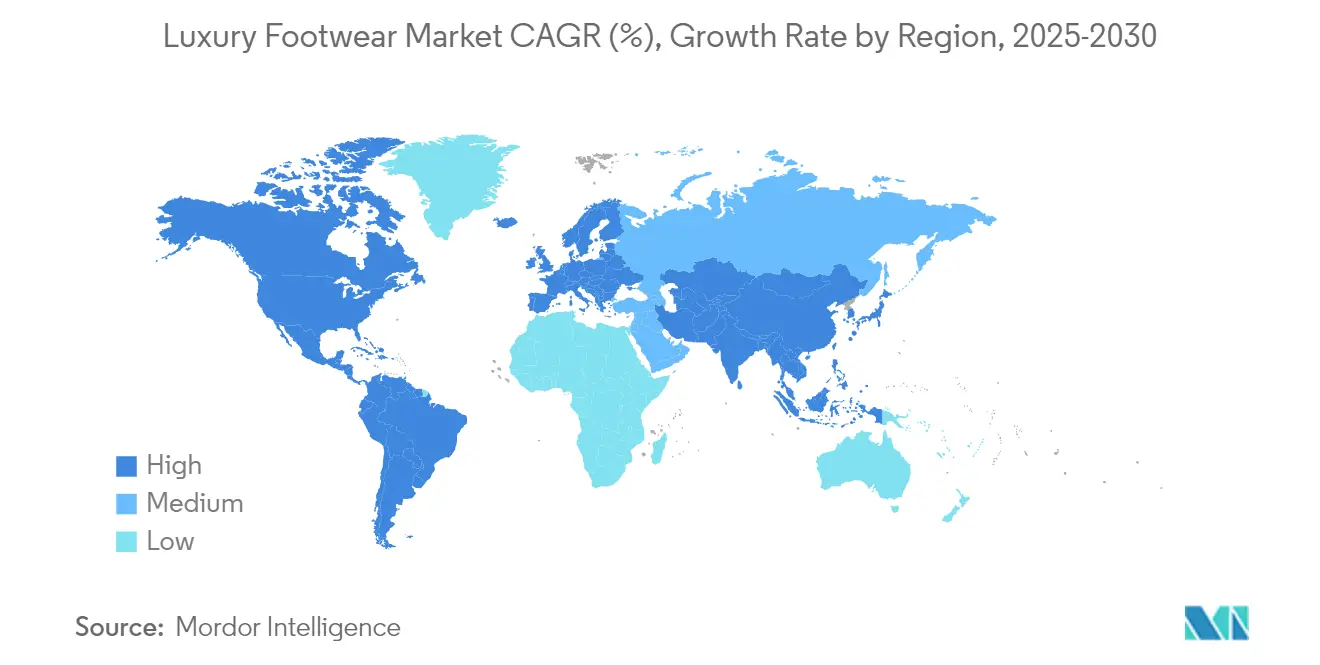

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

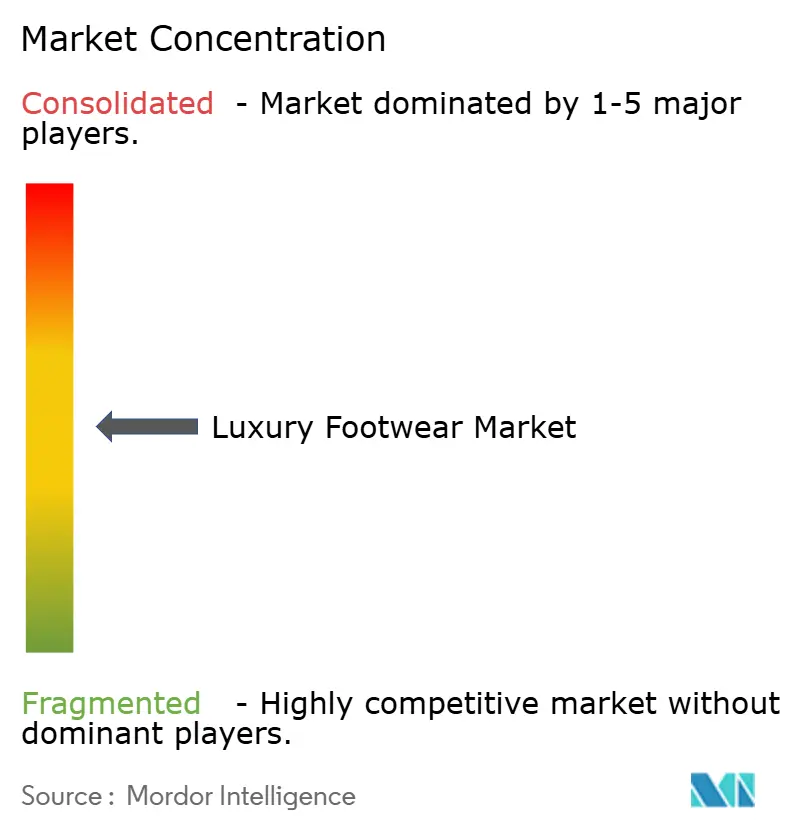

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Luxury Footwear Market Analysis by Mordor Intelligence

The luxury footwear market size is expected to grow from USD 49.08 billion in 2025 to USD 50.55 billion in 2026 and is forecast to reach USD 62.54 billion by 2031 at 4.35% CAGR over 2026-2031. This steady growth highlights the market's ability to maintain strong pricing, the dual appeal of footwear as both a practical necessity and a symbol of status, and the increasing use of digital sales channels. Key factors driving this growth include high demand in the Asia-Pacific region, consistent replacement cycles in North America, and a growing preference among consumers for premium and environmentally friendly products. Challenges such as supply chain disruptions and rising costs due to tariffs have pushed brands to adopt strategies like improving vertical integration, diversifying their sourcing options, and investing in automated manufacturing processes. The rising influence of sneaker culture, increasing wealth in emerging markets, and the popularity of limited-edition collaborations are further supporting the long-term growth of the luxury footwear market. The competitive landscape is moderately intense, with a mix of global corporations and smaller, specialized brands. Companies like LVMH, Kering, and Richemont benefit from their extensive portfolios, shared resources, and brand development capabilities, which give them significant advantages in scale and market presence.

Key Report Takeaways

- By category, non-athletic footwear led with 58.05% of the luxury footwear market share in 2025, while the athletic segment is forecast to record a 4.67% CAGR through 2031.

- By end-user, female consumers held 48.20% of the luxury footwear market share in 2025; the kids/children segment is expected to grow at a 4.92% CAGR over the same period.

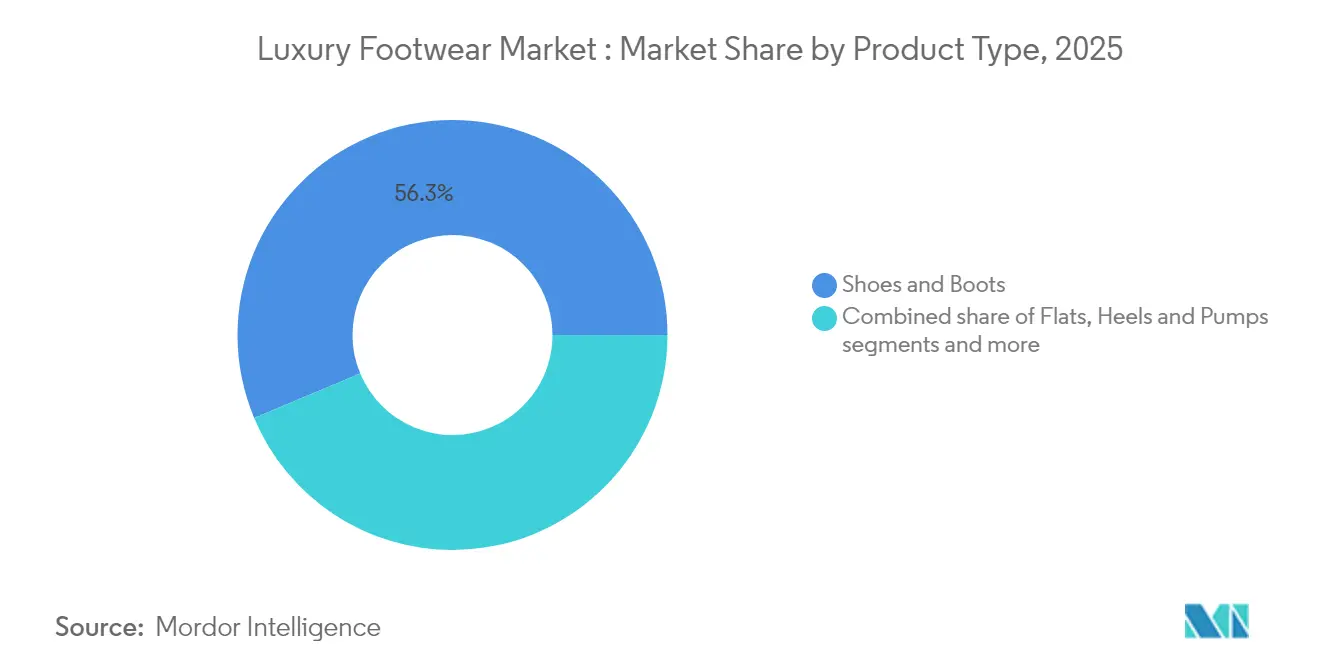

- By product type, shoes and boots accounted for the largest 56.30% slice of the luxury footwear market size in 2025, whereas flats are advancing at a 4.66% CAGR to 2031.

- By distribution channel, specialty stores commanded 38.15% of the luxury footwear market size in 2025, while online retail is projected to expand at a 5.62% CAGR.

- By geography, North America retained 29.40% of the luxury footwear market share in 2025, but Asia-Pacific is on track for the fastest 5.28% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Luxury Footwear Market Trends and Insights

Drivers Impact Table*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Consumer shift toward sustainable and eco-certified luxury products | +0.8% | Global, with Europe leading regulatory compliance | Medium term (2-4 years) |

| Celebrity endorsements and influencer culture | +0.6% | Global, with North America and Asia-Pacific core markets | Short term (≤ 2 years) |

| Product innovation in terms of raw material and design | +0.5% | Global, with early adoption in North America and Europe | Long term (≥ 4 years) |

| Increasing sports participation rate | +0.4% | Asia-Pacific core, spill-over to global markets | Medium term (2-4 years) |

| Consumers inclination towards limited edition products | +0.7% | Global, with premium positioning in developed markets | Short term (≤ 2 years) |

| Growth of experience-based luxury and personalization services | +0.9% | Asia-Pacific, Latin America, and Middle East focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consumer shift toward sustainable and eco-certified luxury products

The increasing demand for sustainable and eco-friendly luxury products is playing a major role in driving the growth of the luxury footwear market. Consumers are becoming more environmentally conscious, and this is influencing their purchasing decisions. In 2024, the European Union implemented the Corporate Sustainability Reporting Directive (CSRD) and is preparing to introduce Digital Product Passport regulations [1]Source: European Union, "EU's Digital Product Passport: Advancing transparency and sustainability," europa.eu. These measures are pushing luxury brands to be more transparent about their sourcing and the materials they use. As a result, many brands are now adopting materials that are traceable and have a lower environmental impact, such as vegetable-tanned leather, recycled rubber soles, and bio-based fabrics. For instance, Tod’s has announced the use of traceable leather certified by the Italian Leather Certification Institute (ICEC) as part of its sustainability strategy, which aligns with EU regulations. In the United States, organizations like the Environmental Protection Agency (EPA) and the Department of Agriculture (USDA) are offering grants and recognition to companies that use bio-preferred materials. This is encouraging luxury footwear brands to innovate and incorporate certified sustainable materials into their products.

Increasing sports participation rate

The growing interest in sports and fitness is playing a key role in driving the luxury footwear market, as more people look for high-performance shoes that also showcase their style and brand preferences. In 2024, participation in recreational and amateur sports, such as running, tennis, and gym workouts, has significantly increased, creating a larger demand for footwear that combines functionality with luxury. For example, the SFIA’s Topline Participation Report highlights that 247.1 million Americans were actively involved in sports and fitness activities in 2024 [2]Source: Sports and Fitness Industry Association, "SFIA’s Topline Participation Report Shows 247.1 Million Americans Were Active in 2024," sfia.org. This trend is especially popular among urban millennials and Gen Z consumers, who see fitness not just as a health activity but as a lifestyle choice. The rise of boutique fitness studios, marathon events, and social media influencers promoting active lifestyles has further encouraged the use of athletic footwear in everyday fashion. Luxury brands are responding to this demand by designing shoes that merge technical performance with premium designs. Products like Louis Vuitton’s LV Trainer, Balenciaga’s 3XL sneaker, and Dior’s B30 are marketed as both stylish fashion pieces and functional athletic gear.

Celebrity endorsements and influencer culture

Collaborations with celebrities and influencers are playing a major role in shaping the image of luxury footwear brands, combining cultural relevance with exclusivity. For example, in 2024, Christian Louboutin partnered with fashion designer Coco Brandolini d’Adda to release a limited-edition collection of women’s shoes, inspired by their friendship and shared love for art. Similarly, Gucci’s collaboration with Harry Styles has brought a fresh, gender-fluid appeal to its footwear, such as loafers and retro sneakers, making them popular worldwide. Balenciaga has also worked with celebrities like Kim Kardashian, which has helped its chunky sneakers and sculptural boots gain immense popularity. These partnerships not only boost brand visibility but also create a sense of aspiration among consumers. Social media further amplifies this effect, increasing emotional connections with the brand and encouraging repeat purchases. This trend is particularly impactful where celebrity endorsements strongly influence consumer choices and drive luxury footwear sales.

Consumers inclination towards limited edition products

Limited-edition releases and collaborations with well-known designers or celebrities have become a key strategy for luxury footwear brands, helping them create exclusivity and boost their appeal. These partnerships not only drive immediate sales but also keep the brands culturally relevant. For example, in March 2024, Gucci teamed up with British designer Martine Rose to launch a special collection of hybrid loafers and sneakers during Paris Fashion Week. The collection sold out within hours and gained massive attention on social media. Similarly, Balmain collaborated with Puma earlier in 2024 to release a unique sneaker line that combined elements of sportswear and high fashion. These limited-edition launches are often timed with major cultural or fashion events, creating a sense of urgency among buyers and enhancing the brand's exclusivity. By offering products that are both rare and tied to significant moments, luxury footwear brands not only increase sales but also strengthen their emotional connection with consumers, especially in global fashion markets.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Strong presence of counterfeit products | -1.2% | Global, with Asia-Pacific and Europe most affected | Short term (≤ 2 years) |

| Lesser demand from price sensitive markets | -0.8% | Emerging markets and lower-income segments globally | Medium term (2-4 years) |

| High import duties and complex trade regulations | -0.6% | Global trade corridors, particularly United States, Europe-China | Short term (≤ 2 years) |

| Volatile raw material prices | -0.4% | Global supply chains, with Italy and Asia production centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong presence of counterfeit products erodes brand value

The ongoing issue of counterfeit products remains a significant challenge for the luxury footwear market, impacting both brand reputation and revenue. Counterfeit goods undermine the exclusivity that luxury brands are built upon, as they flood the market with fake versions of high-end products. According to the OECD, on average, counterfeit goods make up over 2% of global trade, highlighting the scale of the problem. For example, in June 2025, authorities in Western Sydney charged three individuals for allegedly earning USD 9.75 million by selling counterfeit luxury items, including shoes and watches, through an online criminal network. Counterfeiters have become more sophisticated, replicating not only logos but also packaging, authentication cards, and even QR tags, making it harder to distinguish fake products from genuine ones. To combat this, luxury brands such as Gucci, Balenciaga, and Christian Louboutin are adopting advanced technologies like NFC-enabled tags, blockchain-based tracking systems, and AI-driven authentication tools. These measures aim to protect their products and reassure customers about the authenticity of their purchases.

High import duties and complex trade regulations increase cost structures

Luxury footwear brands are facing increasing challenges due to high import duties and complicated trade regulations, which are making it harder to maintain competitive pricing in important markets. For example, in 2024, the U.S. continues to impose significant tariffs on imported footwear, with rates as high as 20% for shoes made in the European Union and 31% for those from Switzerland, according to USTR schedules. These high tariffs often lead to increased retail prices, which can discourage potential buyers, especially those aspiring to own luxury products. Some specific footwear categories face even steeper duties, reaching up to 145%, which further complicates pricing strategies and puts pressure on profit margins. Since nearly 99% of footwear sold in the U.S. is imported, for instance, 2.147 billion pairs of shoes were imported into the U.S. in 2024 [3]Source: FDRA.ORG, "Sourcing and Compliance," fdra.org. Brands like Santoni and Church’s are particularly affected by these costs. To address these challenges, many luxury footwear companies are shifting their production to countries in Southeast Asia with lower tariffs or adopting near-shoring strategies in regions like Eastern Europe and North Africa.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Athletic Luxury Gains Ground

Athletic styles are expected to grow at a 4.67% CAGR, surpassing the growth of the overall luxury footwear market and steadily competing with non-athletic styles, which held a 58.05% market share in 2025. This growth is driven by increasing government initiatives promoting sports participation, the rising popularity of wellness-focused lifestyles, and the merging of streetwear with high fashion. Advanced technologies, such as high-temperature fused midsoles and carbon-fiber plates, are being incorporated into athletic footwear, enhancing both performance and luxury appeal, which justifies their premium pricing.

The trend of limited-edition athletic collaborations, such as the Dior x Air Jordan partnership, highlights the blending of sneaker culture with high-end design. These exclusive releases often use raffle systems to create digital queues, increasing the perception of scarcity and exclusivity. This approach resonates particularly well with millennial consumers in the Asia-Pacific region, who are familiar with flash sales and queue culture, leading to higher purchase rates. Additionally, luxury brands are leveraging their archives to reintroduce classic running or court shoe designs in premium materials, combining nostalgia with modern craftsmanship. These strategies are helping the luxury footwear market attract a broader audience beyond traditional formal shoe buyers.

By End-User: Kids Drive Future Growth

Children’s footwear is expected to grow at a strong CAGR of 4.92%, making it the fastest-growing segment in the luxury footwear market. This growth is driven by increasing disposable income among affluent parents and a growing trend of prioritizing premium products for children. Parents are now more inclined to purchase high-quality, stylish footwear for their kids, often as part of gifting or special occasions. Limited-edition mini sneakers that replicate adult designs are particularly popular, creating additional demand. Social media also plays a significant role, as influencer parents frequently showcase matching outfits and footwear with their children, inspiring similar purchases among their followers.

In 2025, female consumers accounted for 48.20% of the luxury footwear market share, driven by their strong interest in seasonal trends, curated wardrobe collections, and purchases for specific events. Brands are focusing on building loyalty among women by offering exclusive membership programs, early access to new collections, and personalized fitting services. Meanwhile, men’s footwear remains a significant segment, though its growth is more stable. The demand in this category is closely tied to the resurgence of corporate wear and the popularity of limited-edition sneaker releases associated with sports celebrities. Across all demographics, brands are increasingly adopting size-inclusive ranges and virtual try-on technologies.

By Product Type: Flats Challenge Traditional Hierarchies

Flats are expected to grow at a 4.66% CAGR, gradually becoming more popular in a market traditionally dominated by shoes and boots, which still account for 56.30% of the luxury footwear market share. The rise of remote and hybrid work models has reduced the need for high heels, as consumers now prefer footwear that offers both comfort and style. This shift has driven demand for premium options like ballet flats, loafers, and driving shoes. Luxury brands, especially Italian ones, are responding by introducing features such as memory foam insoles and stretchable leathers, ensuring these products provide both comfort and high-quality craftsmanship. These innovations are helping flats gain a stronger foothold in the market.

Shoes and boots continue to perform well, supported by their association with traditional craftsmanship, limited production runs, and seasonal collections. For instance, lug-sole boots inspired by alpine designs, crafted from responsibly sourced suede, are becoming increasingly popular among winter travelers. Similarly, pumps are staying relevant by incorporating features like jeweled embellishments and adjustable heel-height systems, offering consumers a mix of elegance and practicality. Sandals and mules are also maintaining steady demand, particularly as part of resort collections. These products often use lightweight, eco-friendly materials, which align with the growing emphasis on sustainability in the luxury footwear market.

By Distribution Channel: Digital Transformation Accelerates

E-commerce is projected to grow at a 5.62% CAGR, making it the fastest-expanding channel in the luxury footwear market. Online platforms have significantly widened their reach, especially in areas beyond major cities, by offering convenience and accessibility. Virtual flagship stores are now designed to replicate the personalized experience of boutique shopping. Advanced technologies, such as dynamic fit assistants, holographic try-ons, and concierge-style chat services, are making online shopping more user-friendly and efficient. These innovations help customers find the right fit and style with ease, driving a notable increase in online sales. As a result, the e-commerce channel has nearly doubled its market presence, becoming a key driver of growth in the luxury footwear market.

Specialty stores, which still account for 38.15% of the luxury footwear market in 2025, are focusing on enhancing in-store experiences to retain customer interest. These stores are introducing unique features like artisan workshops, exclusive by-appointment lounges, and personalization studios where customers can customize their footwear. Such initiatives are helping specialty stores maintain foot traffic and build customer loyalty. At the same time, omnichannel strategies are gaining importance, with features like click-and-collect services, endless-aisle tablets, and unified loyalty programs ensuring a seamless shopping experience across both online and physical stores. Direct-to-consumer websites are also becoming more popular, as they offer brands higher profit margins and the ability to use customer data for personalized product offerings.

Geography Analysis

North America retained a 29.40% stake in the luxury footwear market in 2025, underpinned by deep-rooted sneaker culture, diversified income streams, and an advanced omnichannel retail infrastructure. Tariff-driven average price hikes of 5% and an overall 0.8% footwear inflation in 2024 have dented volume growth, especially for entry-luxury consumers. Nevertheless, affluent shoppers continue to trade up to collections offering exclusivity, artisanal provenance, or technological novelty. Retailers are experimenting with resale corners inside flagships to cater to sustainability-minded buyers and to keep wardrobe cycles short.

Asia-Pacific is expected to log the fastest 5.28% CAGR through 2031 thanks to demographic tailwinds and rapid urbanization. China’s deceleration highlights macro volatility, yet domestic labels and cross-border duty-free stores remain vibrant. Japan’s luxury renaissance, fueled by yen softness and tourism rebound, has revived Ginza footfall and undergirded full-price sell-through. India stands out with a projected 100 million affluent consumers by 2027, according to Goldman Sachs, opening a vast runway for premium brands . Localization collaborations with Bollywood stylists, festival capsules, and region-specific sizing will be essential for brands to capture long-term brand equity.

Europe, South America, and the Middle East and Africa together form a diversified opportunity mix. In Europe, heightened sustainability regulation pressures supply chains but also elevates premium products certified as low-impact. Italy’s leather sector output fell in 2024, prompting capacity shifts to Portugal and Spain. South American consumers, buoyed by luxury-tax relaxations in select markets, gravitate toward European heritage names, while local tanneries increasingly integrate traceability. Gulf Cooperation Council countries leverage tourism mega-projects to draw high spenders, with Dubai’s high-service malls serving as regional showcases. African growth remains nascent yet promising as mobile commerce accelerates and middle-class purchasing power strengthens.

Competitive Landscape

The competition in the luxury footwear market is moderate, with a mix of large global companies and smaller, specialized brands. Leading players like LVMH, Kering, and Richemont have a strong advantage due to their extensive product portfolios, shared resources, and ability to develop new brands. For example, LVMH’s Fashion and Leather Goods division reported EUR 41,060 million in organic growth in 2024, driven by the popularity of Louis Vuitton and Dior footwear collections. These companies use their scale to invest in high-quality craftsmanship and advanced customer engagement strategies, ensuring they stay ahead in the market. Their focus on artisan-led manufacturing and data-driven approaches helps them maintain a competitive edge while meeting consumer expectations for premium products.

Strategic mergers and acquisitions are shaping the market dynamics by helping brands expand their reach and strengthen their offerings. For instance, Steve Madden’s acquisition of Kurt Geiger for GBP 289 million has boosted its presence in Europe and added luxury price points to its portfolio. Similarly, in 2024, OTB’s majority purchase of Italian footwear maker Calzaturificio Stephen ensures a steady supply for Maison Margiela’s iconic Tabi boots while improving control over production processes. These moves allow brands to better manage raw material price fluctuations, maintain consistent quality, and enhance operational efficiency. Vertical integration strategies like these are becoming essential for brands to safeguard their supply chains and protect their margins in a competitive market.

Technology and sustainability are emerging as key factors that set innovative brands apart in the luxury footwear market. Companies like Zellerfeld are using 3-D printing technology to create footwear with minimal inventory and fully circular designs, challenging traditional manufacturing methods. Established brands are responding by exploring robotics in production and experimenting with plant-based leather alternatives to align with sustainability trends. Additionally, collaborations between luxury brands and tech startups, artists, and sports organizations are creating unique and engaging narratives. These partnerships help brands connect with diverse audiences across regions and age groups, ensuring they remain relevant and innovative in a rapidly evolving market.

Luxury Footwear Industry Leaders

-

LVMH Moët Hennessy Louis Vuitton SE

-

Kering SA

-

Compagnie Financière Richemont SA

-

Prada SpA

-

Capri Holdings Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The luxury footwear brand Moreschi has been acquired by Glam Srl, an Italian company known for its Superglamourous shoe brand, along with a British investment fund. This acquisition marks a significant step for Glam Srl as it expands its portfolio by adding Moreschi.

- February 2025: Steve Madden agreed to acquire UK-based Kurt Geiger for GBP 289 million, adding the Kurt Geiger London, KG Kurt Geiger, and Carvela labels to its portfolio.

- October 2024: Christian Louboutin and fashion designer Coco Brandolini d’Adda teamed up to launch a limited-edition capsule collection of women’s shoes, celebrating their friendship and shared passion for art.

- March 2024: The Italy-based group, OTB, owner of fashion brands such as Margiela, Jil Sander, Marni, Viktor&Rolf, and Diesel, acquired a majority stake in luxury footwear manufacturer Calzaturificio Stephen.

Global Luxury Footwear Market Report Scope

Luxury footwear is manufactured using premium quality materials and provides greater durability, uniqueness, and comfort. Luxury products are controlled by limited availability. They are not mass-produced. This means that designer shoes are by nature unique, exclusive, feature sophisticated designs, and are uncommon in the market. They are exceptionally crafted to make a visual impression.

The scope of the global luxury footwear market includes category, end user, product type, distribution channel, and geography. By category, the market is segmented into athletic footwear and non-athletic footwear. By end user, the market is segmented into men, women and kids/children. By product type, the market is divided into shoes and boots, heels and pumps, flats and other product types. By distribution channel, the market is segmented into speciatly stores, online retail and other distribution channels. By geography, the market is segmented by North America, Europe, Asia Pacific, South America, the Middle East & Africa.

For each segment, market sizing and forecasts have been done based on the value in USD million.

| Athletic Footwear |

| Non-Athletic Footwear |

| Men |

| Women |

| Kids/Children |

| Shoes and Boots |

| Heels and Pumps |

| Flats |

| Other Product Types |

| Specialty Stores |

| Online Retail Stores |

| Others Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Category | Athletic Footwear | |

| Non-Athletic Footwear | ||

| By End-User | Men | |

| Women | ||

| Kids/Children | ||

| By Product Type | Shoes and Boots | |

| Heels and Pumps | ||

| Flats | ||

| Other Product Types | ||

| By Distribution Channel | Specialty Stores | |

| Online Retail Stores | ||

| Others Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the luxury footwear market?

The luxury footwear market stands at USD 50.55 Billion in 2026 and is forecast to grow to USD 62.54 Billion by 2031.

Which region is growing the fastest for luxury footwear?

Asia-Pacific leads with a projected 5.28% CAGR through 2031, driven by rising affluence and robust sneaker culture.

Which product category commands the highest luxury footwear market share?

Non-athletic styles, primarily formal and casual dress shoes and boots, held 58.05% of global share in 2025.

How significant is online retail in the luxury footwear market?

Online retail is the fastest-growing channel at a 5.62% CAGR, supported by virtual try-on tools and direct-to-consumer strategies.

Page last updated on: