Outdoor Apparel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

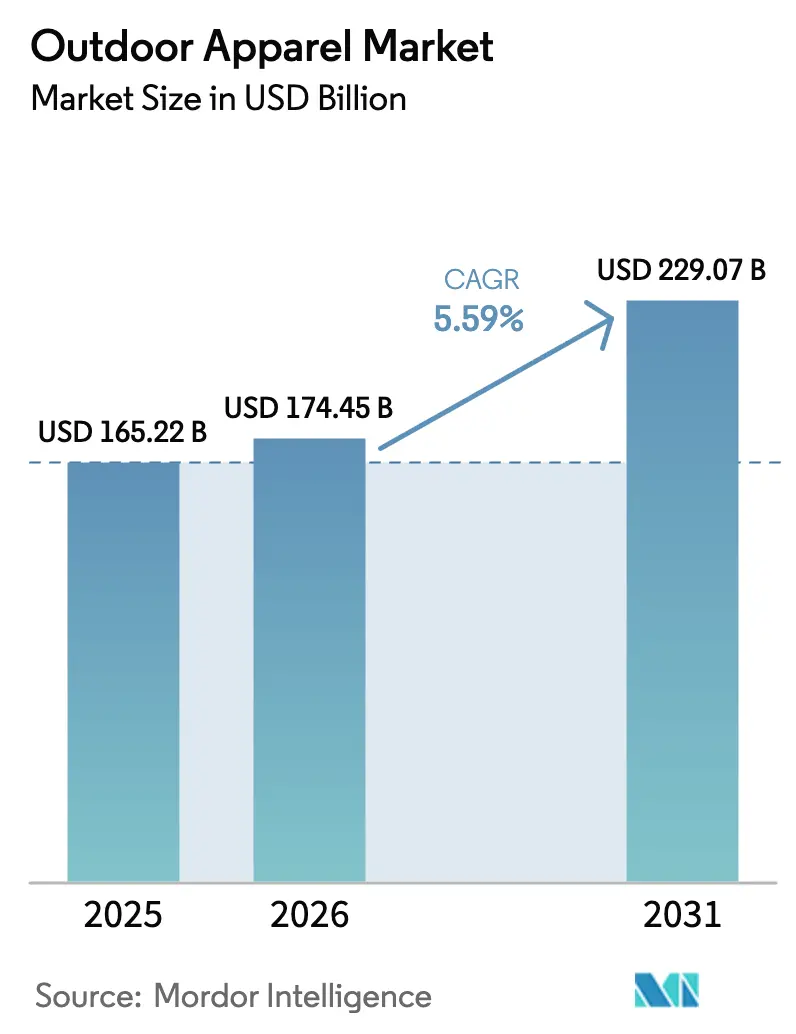

| Market Size (2026) | USD 174.45 Billion |

| Market Size (2031) | USD 229.07 Billion |

| Growth Rate (2026 - 2031) | 5.59% CAGR |

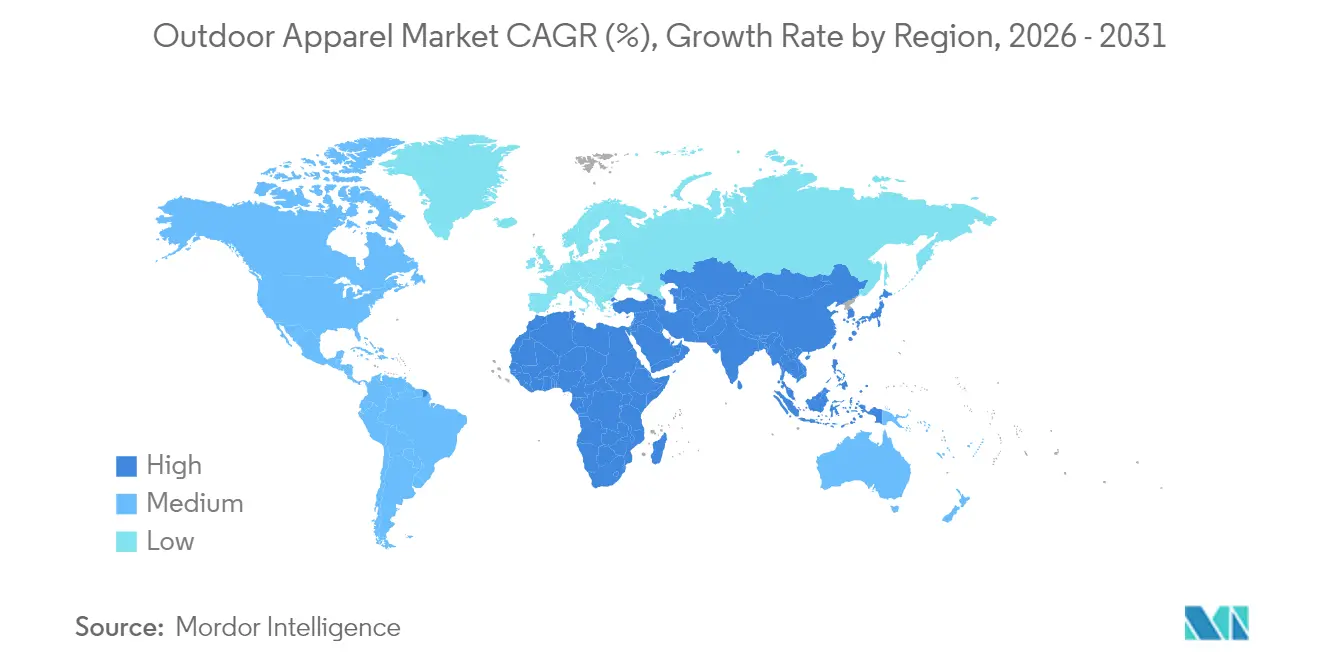

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

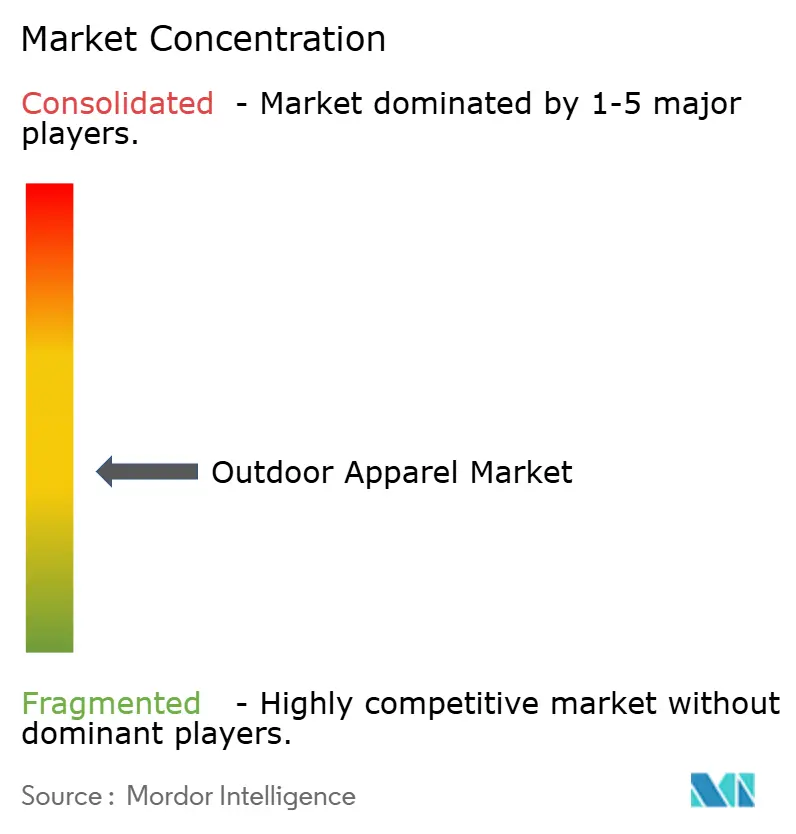

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Outdoor Apparel Market Analysis by Mordor Intelligence

The outdoor apparel market size was valued at USD 165.22 billion in 2025 and estimated to grow from USD 174.45 billion in 2026 to reach USD 229.07 billion by 2031, at a CAGR of 5.59% during the forecast period (2026-2031). The market growth is supported by changing consumer preferences, including increased demand for versatile and durable outdoor clothing, as well as technological advancements in moisture-wicking fabrics, thermal regulation, and weather resistance. The Outdoor Industry Association reported that outdoor recreation participation increased for the ninth consecutive year, growing by 4.1% in 2023 to reach 175.8 million participants in the United States, with significant increases in hiking, camping, and trail running activities[1]Source: Outdoor Industry Association, "Outdoor Participation Hits Record Levels for Ninth Consecutive Year," outdoorindustry.org. The sector contributed USD 639.5 billion to the US economy in 2023, accounting for 2.3% of GDP and supporting 5.0 million jobs across manufacturing, retail, and distribution channels[2]Source: U.S. Bureau of Economic Analysis, "Outdoor Recreation Statistics for 2023," apps.bea.gov. Regulatory changes regarding PFAS chemicals, particularly in California and New York with bans effective January 1, 2025, are driving the adoption of sustainable materials, including recycled polyester, organic cotton, and bio-based alternatives[3]Source: New York State Department of Environmental Conservation, "PFAS In Apparel Law," dec.ny.gov. Manufacturers are investing in research and development to create eco-friendly water-repellent treatments and innovative fabric technologies that comply with these regulations while maintaining performance standards.

Key Report Takeaways

- By product type, top wear dominated the outdoor apparel market with a 42.14% share in 2025, while accessories segment is expected to grow at a 6.43% CAGR during 2026-2031.

- By fabric type, polyester dominated the fabric segment with a 38.31% market share in 2025, while the smart/heated fabrics segment is projected to grow at a 7.05% CAGR through 2031.

- By end user, the men's segment held a 53.62% market share in 2025, while the women's wear segment is expected to grow at a 6.55% CAGR during the forecast period.

- By distribution channel, specialty stores led with a 61.88% market share in 2025, while online retail stores are expected to grow at a 7.12% CAGR through 2031.

- By geography, North America dominated the market with a 35.54% revenue share in 2025, while Asia-Pacific is expected to grow at the highest CAGR of 6.88% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Outdoor Apparel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in outdoor recreational participation | +1.2% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Rising health and wellness consciousness | +0.8% | Global, particularly developed markets | Long term (≥ 4 years) |

| Expansion of e-commerce and DTC channels | +1.0% | Global, with Asia-Pacific leading adoption | Short term (≤ 2 years) |

| Technological innovation in fabrics | +0.9% | North America and Europe for development, Asia-Pacific for manufacturing | Medium term (2-4 years) |

| Athleisure and everyday versatility | +0.7% | Global, with urban centers driving adoption | Medium term (2-4 years) |

| Sustainability and eco-conscious consumerism | +0.6% | Europe and North America leading, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in outdoor recreational participation

Outdoor recreation participation has expanded across demographics, with senior participation increasing by 7.4% and youth participation growing by 5.6%, creating a diverse, multigenerational outdoor community[4]Source: Outdoor Industry Association, "2025 Outdoor Participation Trends Report Executive Summary," outdoorindustry.org. This broader participant base drives sustained demand for technical apparel across age groups, with specialized clothing, footwear, and gear sales representing a substantial portion of total outdoor spending. The rise in participation reflects fundamental lifestyle shifts toward active recreation and wellness activities, supported by federal and state government initiatives, park development programs, and infrastructure investments that improve outdoor accessibility.

Rising health and wellness consciousness

Health consciousness integration with outdoor activities creates sustained demand for performance-oriented apparel that supports active lifestyles beyond traditional sports contexts. The connection between outdoor recreation and wellness drives consumers toward technical fabrics that enhance comfort and performance during extended outdoor exposure. Post-pandemic recovery patterns show outdoor activities maintaining elevated participation levels. This wellness-driven consumption pattern favors brands that communicate health benefits and performance enhancement through their product offerings. The trend extends beyond core outdoor enthusiasts to include urban consumers seeking active lifestyle integration, expanding the addressable market for technical outdoor apparel.

Expansion of e-commerce and DTC channels

E-commerce transformation accelerates as brands prioritize direct-to-consumer (DTC) strategies to capture higher margins and deeper customer relationships. Amer Sports, parent company of Arc'teryx, reported a strategic shift toward DTC channels, with strong growth in the technical Apparel segment increasing 33% in Q4 2024. Social media platforms, particularly TikTok, emerge as significant product discovery channels, requiring brands to create engaging, authentic content that resonates with younger demographics. The digital transformation enables personalized customer experiences and data-driven inventory management, reducing traditional retail dependencies.

Technological innovation in fabrics

Smart fabric integration represents a paradigm shift from passive to active outdoor apparel, with innovations ranging from temperature regulation to health monitoring capabilities. MIT researchers developed fiber computers that can be embedded in clothing, enabling real-time health monitoring and activity tracking, with the U.S. Army testing these garments during Arctic operations. University of Waterloo scientists created smart fabrics that generate heat using sunlight, reaching temperatures up to 30°C and featuring color-changing capabilities for temperature indication. These technological advances create new market categories and premium positioning opportunities, though they require significant R&D investments and manufacturing process adaptations. The integration of textiles and electronics enables the development of clothing that responds to environmental conditions and the wearer's physiological state.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of technical fabrics and premium pricing | -0.8% | Global, with stronger impact in price-sensitive markets | Medium term (2-4 years) |

| Seasonal demand cyclicality and inventory risk | -0.6% | Northern hemisphere markets primarily | Short term (≤ 2 years) |

| Increasing availability of counterfeit products | -0.5% | Global, with Asia-Pacific and emerging markets most affected | Medium term (2-4 years) |

| Rapidly changing consumer preferences | -0.4% | Global, with developed markets showing higher volatility | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High cost of technical fabrics and premium pricing

Technical fabric costs create pricing pressures that limit market accessibility, particularly as sustainable and smart materials command premium pricing. PFAS-free alternatives typically cost 15-20% more than conventional treatments, while smart fabrics with integrated electronics can increase production costs by 50-100%. Raw material inflation, particularly for specialized synthetic fibers, compounds these challenges as brands balance performance requirements with price sensitivity. The premium positioning of technical outdoor apparel creates barriers for mass market adoption, limiting growth potential in price-sensitive segments. Manufacturing complexity for advanced materials requires specialized facilities and skilled labor, further increasing production costs.

Seasonal demand cyclicality and inventory risk

Seasonal demand patterns create inventory management challenges that impact cash flow and profitability, particularly for brands with concentrated product lines. The outdoor industry's heavy weighting toward third and fourth quarters creates working capital pressures and forces aggressive inventory planning decisions. Weather variability increasingly affects seasonal patterns, with climate change creating unpredictable demand shifts that complicate forecasting accuracy. VF Corporation's inventory reduction of 24% in Q1 FY25 demonstrates the ongoing challenge of balancing stock levels with demand uncertainty. The seasonal nature of outdoor activities requires brands to maintain diverse product portfolios and flexible manufacturing arrangements to manage demand fluctuations effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Technical Innovation Drives Accessories Growth

The accessories segment is growing at a 6.43% CAGR through 2031, while top wear holds a 42.14% market share in 2025. This shift indicates the market's transition toward integrated outdoor systems rather than individual garments. The integration of technology in accessories, including heated gloves and temperature-regulating headwear, provides higher profit margins alongside traditional apparel. Bottom Wear continues to show consistent demand through improvements in mobility and durability. Footwear growth is driven by advancements in materials and construction methods. The increasing accessories market share demonstrates consumer preference for specialized equipment, including GPS watches and solar charging devices, that enhance outdoor activities.

Top wear holds the largest market share due to its versatility in both outdoor activities and daily use. Companies like The North Face have integrated technologies such as FlashDry™, which combines moisture management with UV protection. Bottom wear development focuses on improving mobility and weather resistance, while footwear innovations emphasize reduced weight and enhanced traction systems. This product segmentation aligns with outdoor enthusiasts' preference for layered clothing systems that adapt to different weather conditions and activity intensities.

By Fabric Type: Smart Materials Revolutionize Performance

The smart/heated fabrics market is growing at a CAGR of 7.05%, with synthetic fabric maintaining a dominant 38.31% market share in 2025. This growth reflects the industry's shift toward temperature-responsive materials that enhance user comfort and performance. Research breakthroughs include the University of Waterloo's development of fabrics that generate heat from sunlight and MIT's fiber computers that monitor physiological data in real-time. Natural fibers like Cotton and Wool maintain relevance through organic and sustainable positioning, while Blends offer performance-cost optimization for mainstream consumers. Recycled/Eco-friendly materials gain traction through regulatory mandates and consumer preferences, with brands increasingly adopting circular economy principles.

Polyester dominance reflects its versatility, durability, and cost-effectiveness across diverse outdoor applications, from base layers to outer shells. Nylon provides superior strength-to-weight ratios for technical applications, while smart fabrics create entirely new product categories that command premium pricing. The fabric evolution demonstrates how material science advances drive market differentiation and enable brands to create proprietary technologies that enhance competitive positioning.

By End-User: Women's Segment Drives Market Evolution

The women's segment is projected to grow at a 6.55% CAGR through 2031, while the men's segment maintains a dominant 53.62% market share in 2025. This shift indicates the outdoor industry's evolution from its traditionally male-focused market. The growth in women's outdoor participation is driven by product development that specifically addresses fit, functionality, and design preferences. Manufacturers are introducing women-specific outdoor gear, including backpacks with adjusted shoulder straps and hip belts, clothing with tailored cuts, and footwear designed for women's foot anatomy. The expansion of women's outdoor participation is further supported by targeted marketing campaigns, women-focused outdoor communities, and specialized retail experiences. Retailers are creating dedicated spaces and training staff to better serve female customers, while brands are developing ambassador programs featuring women athletes and outdoor enthusiasts.

The kids segment continues to expand due to increased family outdoor activities and growing parental focus on children's active lifestyles. This growth is supported by the development of durable, adjustable equipment that accommodates children's rapid growth, as well as educational programs and family-oriented outdoor events that encourage youth participation in outdoor activities. The outdoor recreation industry is experiencing a shift in gender dynamics as more women participate in technical outdoor activities requiring specialized apparel. In response, outdoor brands are developing dedicated women's product lines, implementing female-focused marketing initiatives, and expanding size ranges to accommodate diverse body types. This demographic change presents opportunities for companies to develop specialized products and expand their market presence.

By Distribution Channel: Digital Transformation Accelerates

Online retail stores expand at 7.12% CAGR through 2031 while specialty stores maintain 61.88% market share in 2025, illustrating the industry's omnichannel evolution that combines digital convenience with experiential retail expertise. REI's plans to open 10 new stores in 2024 and additional locations in 2025 showcase the integration of physical and digital channels to meet customer needs. Supermarkets and Hypermarkets provide accessibility for mainstream outdoor products, while the other category includes emerging channels like rental services and subscription models that align with sustainability trends.

Specialty stores maintain their market leadership through product expertise, personalized fitting services, and post-purchase support - elements essential for outdoor apparel purchases. These retailers effectively combine online presence with in-store knowledge to deliver comprehensive shopping experiences. The e-commerce channel grows through detailed product specifications, user reviews, and flexible return policies that address customer concerns about technical apparel purchases.

Geography Analysis

North America holds 35.54% market share in 2025, driven by established outdoor culture, high disposable income, and extensive recreational infrastructure that supports sustained outdoor participation. The region's market leadership reflects deep-rooted outdoor traditions, government support for public lands access, and consumer willingness to invest in premium outdoor gear. Manufacturing reshoring initiatives, exemplified by Walmart's plan to produce clothing domestically and various textile companies' nearshoring strategies, aim to reduce supply chain dependencies while supporting local economies. The region benefits from technological innovation centers and venture capital availability that fund outdoor apparel startups and established brand R&D initiatives.

Asia-Pacific emerges as the fastest-growing region with 6.88% CAGR through 2031, propelled by rising disposable incomes, urbanization, and growing outdoor recreation adoption across diverse markets from China to Australia. Amer Sports reported that sales share from Asia-Pacific and Greater China increased from 29% in 1H23 to 38% in 1H24, demonstrating the region's accelerating importance. Manufacturing capabilities in countries like Vietnam and Bangladesh provide cost advantages and production flexibility that support global supply chains. The region's young demographics and increasing health consciousness create favorable conditions for outdoor apparel adoption.

The European market emphasizes sustainability and regulatory developments through initiatives like the EU's Circular Economy Action Plan, which mandates recyclable textiles from recycled fibers by 2030. Regional outdoor brands, including Haglöfs and Mammut, integrate technical advancements with environmental practices to meet consumer demand for sustainable outdoor products. European consumers consistently show a higher willingness to pay more for environmentally responsible products.

Competitive Landscape

The outdoor apparel market shows moderate fragmentation, with a concentration index of 4 out of 10. This market structure enables established multinational brands and emerging specialists to compete through differentiation strategies instead of relying solely on economies of scale. Strategic consolidation activities reshape competitive dynamics, with Anta Sports' USD 290 million acquisition of Jack Wolfskin demonstrating how companies pursue geographic expansion and portfolio diversification.

Technology integration becomes a key differentiator, exemplified by Arc'teryx's collaboration with Skip to develop powered hiking pants that create entirely new product categories. Direct-to-consumer strategies gain prominence as brands seek higher margins and deeper customer relationships, with companies like Amer Sports reporting strategic shifts toward DTC channels. White-space opportunities emerge in smart textiles, sustainable materials, and inclusive sizing as traditional boundaries between outdoor and lifestyle apparel blur.

Emerging disruptors leverage e-commerce platforms and social media marketing to challenge established players, particularly in niche segments like ultralight gear and urban outdoor wear. The competitive landscape increasingly rewards brands that combine technical innovation with sustainability credentials, as regulatory pressures and consumer preferences drive demand for environmentally responsible products. Patent filings in smart textiles and sustainable materials indicate intensifying R&D competition, with companies investing heavily in proprietary technologies that create competitive moats.

Outdoor Apparel Industry Leaders

-

Adidas AG

-

Nike Inc.

-

VF Corporation

-

Columbia Sportswear Company

-

Amer Sports

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Anta Sports finalized its USD 290 million acquisition of German outdoor brand Jack Wolfskin from Topgolf Callaway Brands, expanding its international presence and outdoor product portfolio. The acquisition provides Anta access to Jack Wolfskin's materials technologies and European market expertise.

- August 2024: Arc'teryx launched the world's first powered hiking pants (MO/GO) in collaboration with Skip and featuring exoskeleton technology that provides 40% more power for climbing while reducing joint impact.

- July 2024: WNDR Alpine, based in Salt Lake City, introduced all-season outdoor gear that demonstrates its focus on sustainable innovation. The company integrates biotechnology into its high-performance products, utilizing microalgae oil-derived materials as a renewable and traceable alternative to petroleum. WNDR has expanded its Phase Series technical apparel line to include the UPF 50+ Diurnal Tech Hoodie and the Stasis Longsleeve, available in men's and women's styles. The garments incorporate miDori bioWick, a petroleum-free wicking technology developed with Beyond Surface Technologies. This technology features 100% biobased content and reduces the carbon footprint by 80% compared to conventional wicking treatments.

Global Outdoor Apparel Market Report Scope

| Top Wear | Jackets |

| T-Shirts | |

| Hoodies and Fleeces | |

| Others | |

| Bottom Wear | Trousers and Pants |

| Shorts | |

| Others | |

| Footwear | |

| Accessories | Gloves |

| Headwear | |

| Socks | |

| Others |

| Synthetic | Polyester |

| Nylon | |

| Natural | Cotton |

| Wool | |

| Blends | |

| Recycled/Eco-friendly | |

| Smart/Heated Fabrics |

| Men |

| Women |

| Kids |

| Specialty Stores |

| Supermarkets and Hypermarkets |

| Online Retail Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| New Zealand | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Top Wear | Jackets |

| T-Shirts | ||

| Hoodies and Fleeces | ||

| Others | ||

| Bottom Wear | Trousers and Pants | |

| Shorts | ||

| Others | ||

| Footwear | ||

| Accessories | Gloves | |

| Headwear | ||

| Socks | ||

| Others | ||

| By Fabric Type | Synthetic | Polyester |

| Nylon | ||

| Natural | Cotton | |

| Wool | ||

| Blends | ||

| Recycled/Eco-friendly | ||

| Smart/Heated Fabrics | ||

| By End-User | Men | |

| Women | ||

| Kids | ||

| By Distribution Channel | Specialty Stores | |

| Supermarkets and Hypermarkets | ||

| Online Retail Stores | ||

| Others | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| New Zealand | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the outdoor apparel market?

The outdoor apparel market is valued at USD 174.45 billion in 2026 and is forecast to reach USD 229.07 billion by 2031.

How fast is the outdoor apparel market growing?

The market is set to expand at a 5.59% CAGR between 2026 and 2031, supported by record participation and material innovation.

Which region shows the fastest growth?

Asia-Pacific is projected to record a 6.88% CAGR through 2031 as rising incomes and government sports initiatives fuel demand.

Which product segment is expanding the quickest?

Accessories are expected to grow at a 6.43% CAGR over 2026-2031.

Page last updated on: