Luxury Apparel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

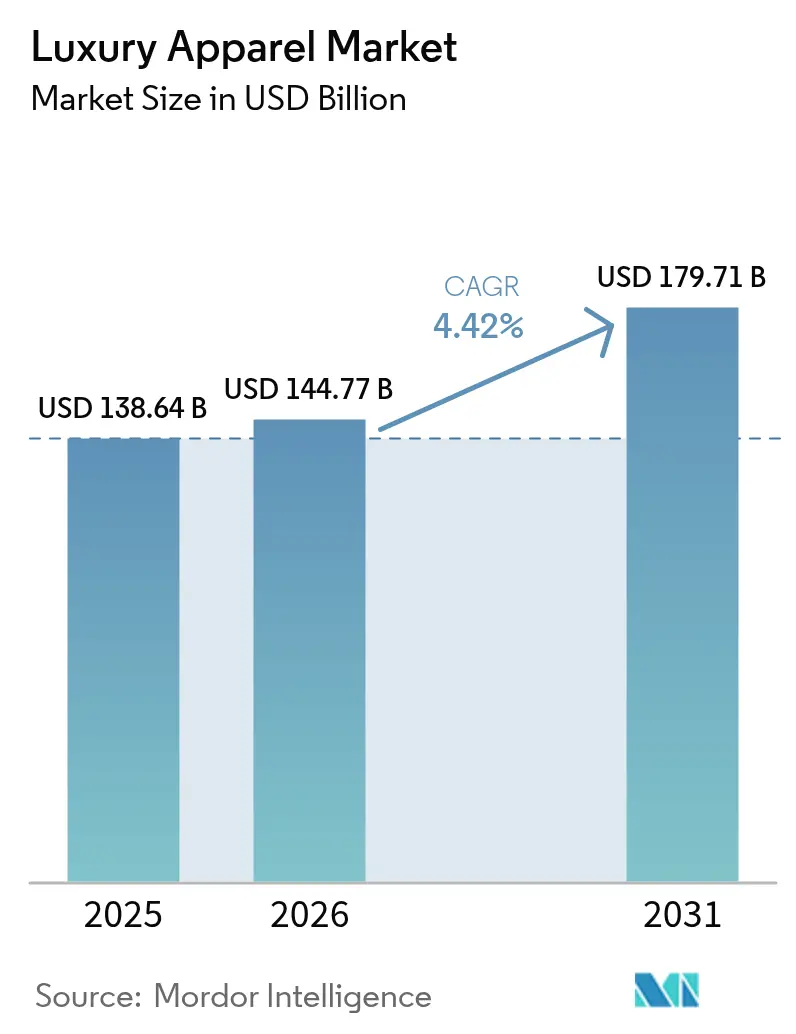

| Market Size (2026) | USD 144.77 Billion |

| Market Size (2031) | USD 179.71 Billion |

| Growth Rate (2026 - 2031) | 4.42% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Luxury Apparel Market Analysis by Mordor Intelligence

The luxury apparel market size is expected to grow from USD 138.64 billion in 2025 to USD 144.77 billion in 2026 and is forecast to reach USD 179.71 billion by 2031 at 4.42% CAGR over 2026-2031. This resilience is driven by consumers' readiness to invest in premium craftsmanship, transparent supply chains, and immersive shopping experiences. Factors like the rise of blockchain-enabled Digital Product Passports, a resurgence in travel retail, and the blending of streetwear with traditional designs are expanding the market's reach. Concurrently, tightening sustainability regulations elevates operational standards, bolstering the pricing power of brands already committed to traceable, low-volume production. Competitive dynamics are evolving, influenced by technology integration, strategic consolidations, and omnichannel retailing. Luxury conglomerates are harnessing AI forecasting tools to optimize inventory and are incorporating NFC tags to ensure authenticity verification at the point of sale.

Key Report Takeaways

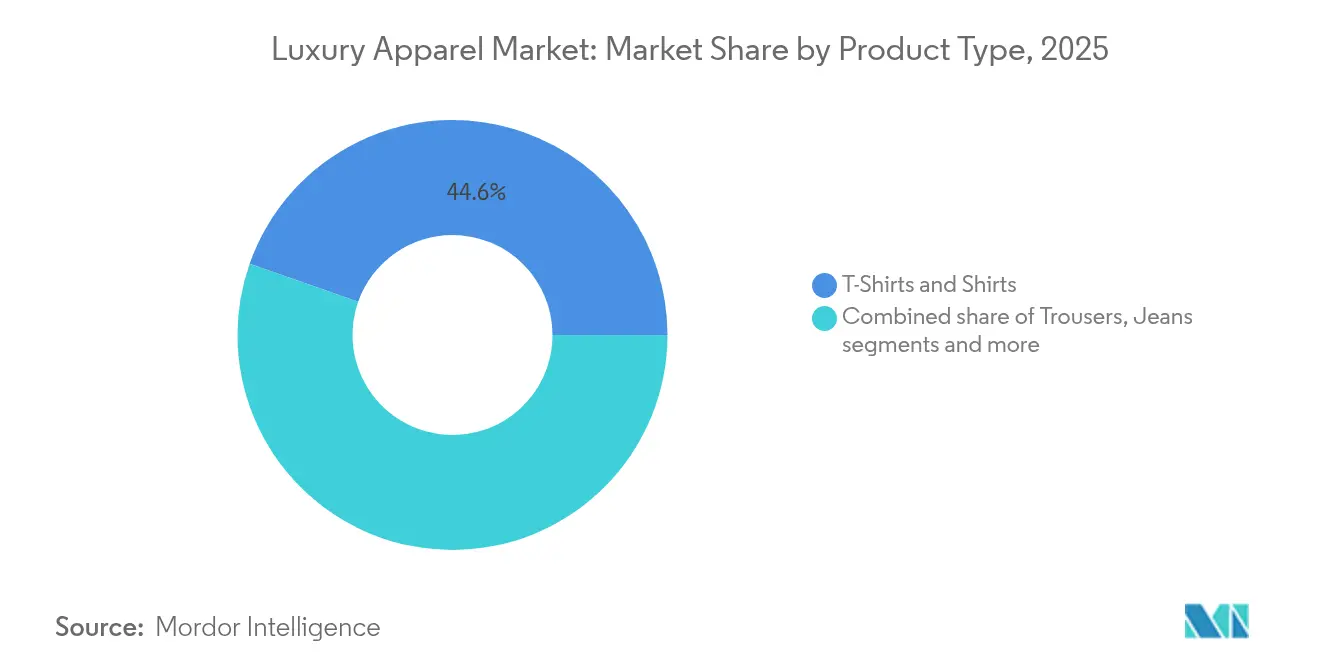

- By product type, t-shirts and shirts led with 44.62% of the luxury apparel market share in 2025, whereas jackets, sweatshirts, and hoodies are set to grow the fastest at a 4.72% CAGR to 2031.

- By end purpose, fashion and casual captured 65.05% of the luxury apparel market in 2025; athleisure registers the highest projected CAGR of 5.05% for 2026-2031.

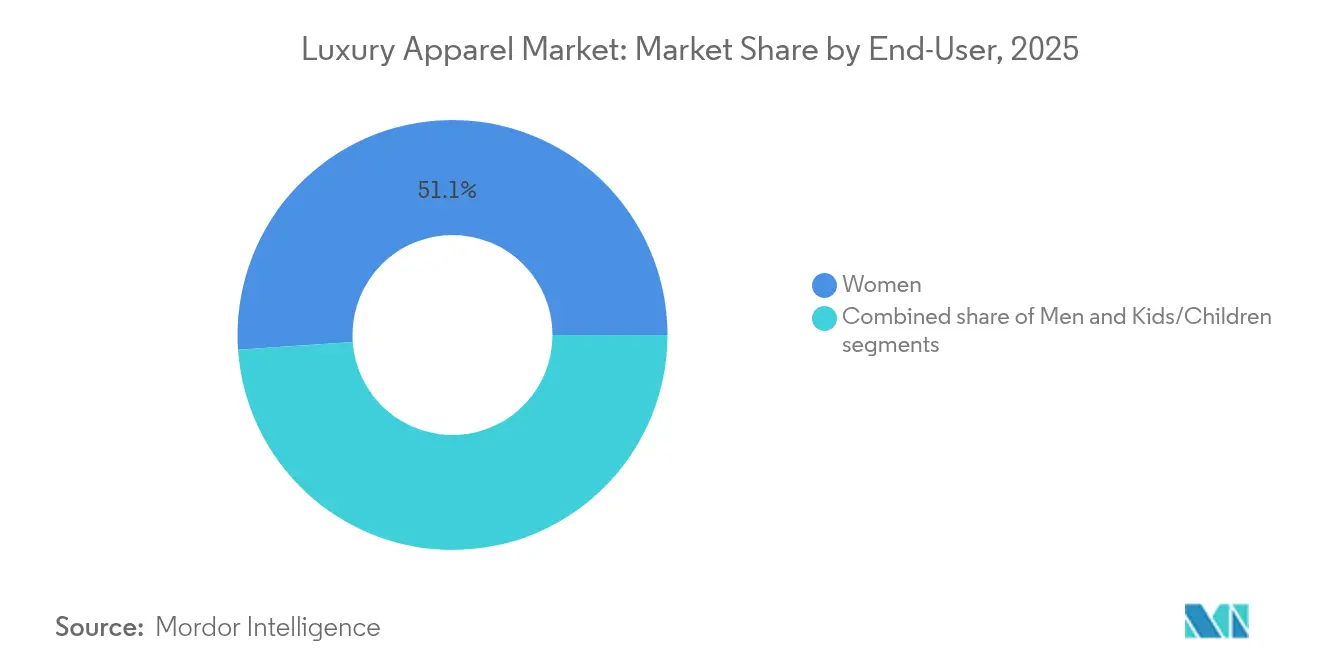

- By end user, women dominated at 51.10% market share in 2025, while the kids/children segment exhibits a 5.58% CAGR through 2031.

- By distribution channel, specialty stores claimed 36.72% share in 2025, and online retail stores expanded the quickest at 6.02% CAGR over the forecast period.

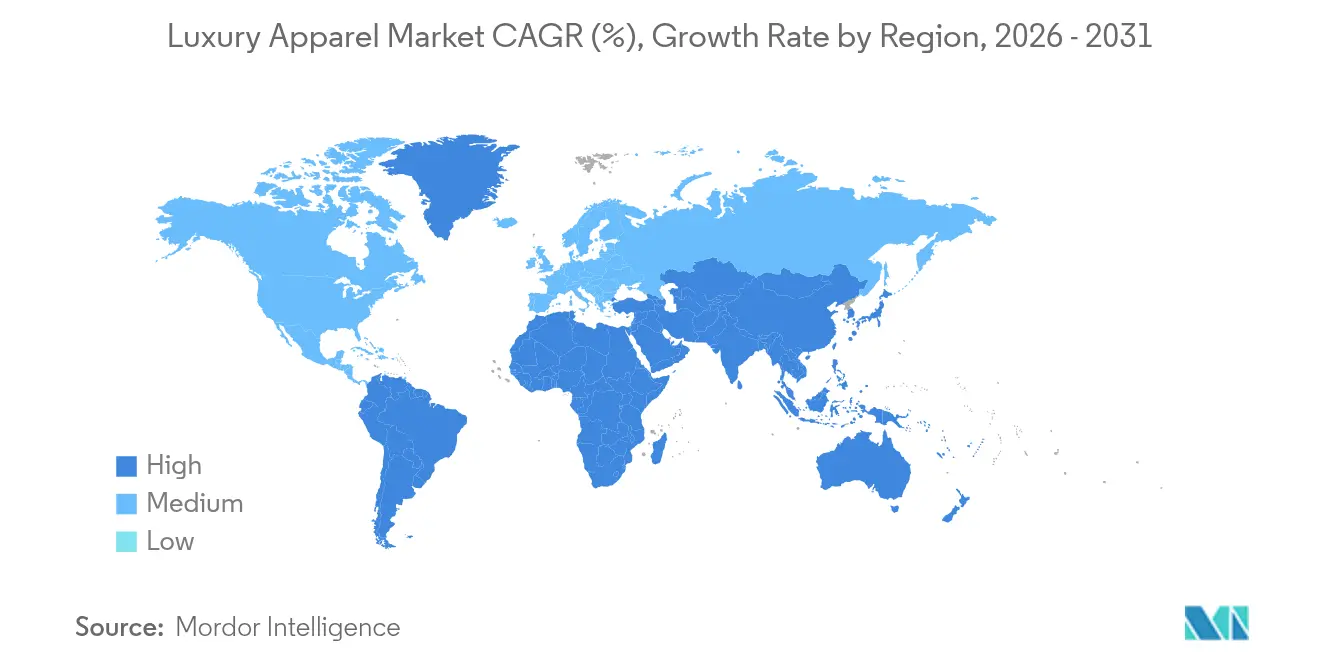

- By geography, North America accounted for a 27.62% share in 2025, but Asia-Pacific posts the strongest regional CAGR of 6.48% up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Luxury Apparel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Sustainable High-End Materials | +0.8% | Global, with EU leading regulatory enforcement | Medium term (2-4 years) |

| Influence of Social Media and Celebrity Endorsement | +1.2% | Global, with strongest impact in North America and Asia-Pacific | Short term (≤ 2 years) |

| Technological Advancements in Fabric and Design | +0.6% | Global, with innovation centers in Europe and North America | Long term (≥ 4 years) |

| Globalisation of Fashion Trends | +0.7% | Global, with emerging market acceleration | Medium term (2-4 years) |

| Expansion of Luxury Streetwear and Athleisure | +0.9% | North America and Asia-Pacific core, spillover to Europe | Medium term (2-4 years) |

| Increased Travel and Tourism | +0.5% | Global, with recovery patterns varying by region | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Sustainable High-End Materials

Regulatory mandates are reshaping the economics of luxury apparel production. The European Union's Digital Product Passport requirements introduce new compliance costs, inadvertently bolstering the competitive advantages of market leaders. Under the California Responsible Textile Recovery Act of 2024, producers with revenues over USD 1 billion must join Producer Responsibility Organizations by July 2026. This move effectively erects a regulatory barrier, favoring established luxury players and consolidating their market share. France's proposed taxation framework for fast fashion, akin to cigarette taxes, inadvertently benefits luxury brands. Their premium pricing and limited production volumes resonate with sustainability goals. The EU's Corporate Sustainability Due Diligence Directive, set for implementation by 2027, favors luxury brands boasting supply chain transparency [1]Source: European Commission, "Corporate sustainability due diligence", commission.europa.eu. In contrast, smaller players grapple with steeper compliance costs. In response to this evolving regulatory landscape, luxury brands are increasingly turning to blockchain-based authentication systems.

Influence of Social Media and Celebrity Endorsement

Luxury brands are shifting their strategies, moving from mere endorsements to a deeper integration within brand ecosystems. This evolution sees luxury houses fiercely vying for exclusive talent partnerships, amplifying their marketing efforts. A prime example of this shift is Chanel's 2025 signing of Kendrick Lamar as its brand ambassador. This move underscores a strategic pivot, emphasizing cultural influence over mere demographic outreach, aiming squarely at younger consumers. In another instance, the collaboration between Nike and Kim Kardashian's NikeSkims highlights a convergence of luxury and adjacent brands. Here, the clout of celebrity endorsements is birthing new product categories, challenging the confines of traditional luxury. Furthermore, global social media influencers are increasingly endorsing luxury apparel brands, showcasing their benefits and quality through reels and videos. This trend is particularly resonating with Gen Z and Millennials, driven by their heightened engagement with social media. Supporting this, data from StatCounter Global Stats in 2025 revealed that 66.08% of individuals in the UK were on Facebook, while 10.73% used Instagram [2]Source: StatCounter Global Stats, "Social Media Usage in the United Kingdom", gs.statcounter.com.

Technological Advancements in Fabric and Design

Luxury brands are harnessing AI-driven demand forecasting to cut down on inventory waste, all while preserving their exclusivity. Generative AI is paving the way for mass customization, ensuring that artisanal quality standards remain intact. The rise of smart textiles, coupled with the integration of wearable technology, is birthing new product categories in luxury athleisure, seamlessly blending technical performance with aesthetic appeal. LVMH's blockchain initiatives showcase the power of digital twin technology, crafting virtual representations of products that not only boost customer engagement but also ensure traceability in the supply chain. This fusion of age-old craftsmanship with cutting-edge digital innovation empowers luxury brands to uphold their heritage authenticity, all while catering to today's consumers who prioritize technological advancement and environmental stewardship.

Globalisation of Fashion Trends

Online runway streams and social platforms are shortening the time between a trend's inception and its commercial debut. Designers are adopting a "glocal" approach, blending global brand elements with local motifs to connect with markets in high-growth regions like Southeast Asia. In 2024, Milan's Via Monte Napoleone surpassed New York's Fifth Avenue, becoming the priciest retail street globally, highlighting the allure of major fashion capitals for tourists, as reported by theguardian.com. Due to Brexit-related logistics challenges, many UK designers relocated their flagship shows to Milan, showcasing how geopolitical events can shift creative centers. The swift dissemination of information enables niche trends to gain global traction almost instantly, necessitating responsive supply chains and data-informed product assortments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Counterfeit Products | -0.6% | Global, with highest impact in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Lesser Demand from Price Sensitive Consumers | -0.8% | Global, with pronounced effects in Europe and price-sensitive regions | Medium term (2-4 years) |

| Slow Adoption in Price-Sensitive Regions | -0.5% | Emerging markets and developing economies | Long term (≥ 4 years) |

| Challenges of Balancing Exclusivity with Accessibility | -0.4% | Global, with strategic implications for brand positioning | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Counterfeit Products

Counterfeits undermine the luxury apparel market by compromising price integrity and diminishing brand prestige. Today's sophisticated replicas closely mimic original fabrics, hangtags, and even digital IDs. This has compelled legitimate players to invest in legal protections, customs training, and forensic authentication. Major groups, spearheading blockchain consortia, are introducing serialized tags that consumers can read via apps. However, this adoption remains uneven and capital-intensive, as highlighted by whitecase.com. In developing markets, especially in parts of Asia-Pacific, entrenched production clusters pose challenges for enforcement. Over time, while the counterfeit threat depletes resources, it simultaneously nudges the sector towards advanced security technologies and fosters tighter collaboration with customs authorities.

Lesser Demand from Price Sensitive Consumers

Between 2020 and 2024, mid-tier luxury buyers felt the pinch of sharp price hikes, a move aimed at countering raw-material and logistics inflation. Younger consumers are increasingly turning to pre-owned channels and rental services, seeking brand prestige without the hefty price tag. The viral "under-consumptioncore" movement on social media advocates for purchasing fewer, yet higher-quality items, nudging aspirational shoppers towards vintage collections. While ultra-high-net-worth households continue their spending spree, brands dependent on occasional buyers grapple with volume pressures. Some brands are responding by broadening entry lines or enhancing experiential services, yet they find themselves on a tightrope, balancing the delicate line between accessibility and exclusivity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Casualization Drives Market Evolution

In 2025, t-shirts and shirts captured 44.62% of sales, underscoring a consumer pivot towards elevated everyday pieces that seamlessly blend comfort with couture nuances. This dominance not only solidifies the luxury apparel market's focus on basics but also justifies the premium pricing of fine cotton, silk blends, and artisanal touches. Jackets, sweatshirts, and hoodies are poised for the swiftest revenue ascent, projected at a 4.72% CAGR. This surge is attributed to the expanding versatility of technical fabrics, including breathable membranes and water-repellent cashmere. Meanwhile, luxury streetwear capsules, frequently unveiled via online raffles, are supercharging both sell-through rates and social buzz.

Dresses and gowns cater to ceremonial needs, while jeans offer a gateway, enticing younger demographics into brand ecosystems ripe for future cross-selling of higher-margin items. Looking ahead, the luxury apparel market is set to witness a surge in investments towards premium innerwear. Brands are keen to capitalize on the narrative of “next-to-skin” comfort. Meanwhile, shorts and skirts are reaping the rewards from affluent consumers' rotation towards resort wear, a trend further buoyed by the rise in leisure travel. Across the board, attributes like longevity, repair services, and recyclable materials are becoming pivotal purchase drivers, overshadowing traditional aesthetic considerations.

By End Purpose: Athleisure Reshapes Luxury Boundaries

In 2025, fashion and casual wear took a commanding 65.05% revenue share, cementing its status as a lifestyle choice rather than merely occasion-specific attire. Athleisure, however, is poised to expand at a vigorous 5.05% CAGR, outpacing all other categories and highlighting the luxury apparel market's pivot towards performance-driven elegance. With sports participation on the rise, market players are debuting luxury athleisure lines to meet this burgeoning demand. Data from Sports England in 2024 revealed that 6,695.5 thousand individuals engaged in fitness classes, while 2,222.5 thousand participated in football across the United Kingdom . Luxury elements are now seamlessly woven into wellness-centric wardrobes, from technical leggings made of recycled polyamide to odor-resistant merino polos and moisture-wicking cashmere hoodies. This evolution underscores a growing consumer appetite for apparel that marries functionality with upscale aesthetics, propelling advancements in fabric technology and design.

As health consciousness rises, office dress codes relax, and hybrid work models gain traction, the demand for versatile attire surges. Luxury brands, leveraging proprietary knit technologies and biomechanical designs, are setting premium price tags on garments that transition smoothly from gym sessions to fine dining. With the boundaries between sport and fashion increasingly blurred, there's a ripe opportunity for cross-merchandising with travel gear, footwear, and accessories, resulting in heightened customer spending. Moreover, this fusion of sport and style is catalyzing partnerships between luxury brands and activewear firms, amplifying the market's growth trajectory.

By End User: Generational Shifts Drive Growth

In 2025, women accounted for 51.10% of spending, highlighting their pivotal role in design cycles and marketing budgets. This significant contribution underscores the importance of tailoring strategies to meet the preferences and demands of this demographic. Meanwhile, the kids/children's line experienced the fastest growth at a 5.58% CAGR, transforming iconic pieces into lucrative miniatures. This growth is driven by the increasing trend of parents investing in premium clothing for their children, viewing it as a reflection of their lifestyle and status. Early exposure to brands fosters lifelong loyalty, enabling parents to showcase family status through coordinated outfits.

While the luxury children's apparel market lags behind its adult counterpart, emerging economies with rapidly rising disposable incomes present opportunities for double-digit growth. The growing middle class in these regions is increasingly prioritizing high-quality and branded clothing for children, further fueling market expansion. Men's fashion is evolving, with heightened interest in bespoke street-tailoring blends and luxury outerwear tailored for tech-savvy city dwellers. This shift reflects a broader trend of men seeking versatile and functional clothing that aligns with their urban lifestyles. Additionally, gender-fluid collections not only broaden the assortment but also mitigate inventory risks by catering to a wider range of body types from a singular SKU pool. These collections address the growing demand for inclusivity and adaptability in fashion, appealing to a diverse consumer base.

By Distribution Channel: Digital Transformation Accelerates

In 2025, specialty stores commanded a significant 36.72% of turnover, underscoring the importance of curated spaces. These spaces, manned by expert advisors, not only offer styling across categories but also provide essential after-sales services. Meanwhile, online retail stores are witnessing the fastest growth among channels, boasting a 6.02% CAGR. Brands are enhancing the online shopping experience by integrating immersive 3-D showroom tools, live-chat styling assistance, and even same-day courier deliveries. The luxury apparel market is increasingly leaning on omnichannel strategies, with nearly every purchase journey now bridging both digital platforms and physical stores.

Time-sensitive exclusivity is the name of the game. Pop-up installations, resort boutiques, and flagship stores at airports are not just complements to mainline stores; they're strategically capturing tourists with high spending potential. Retailers are becoming more data-driven, utilizing first-party e-commerce insights to tailor product assortments, adjust inventories in real time, and customize in-store experiences. Even after a purchase, digital platforms play a pivotal role, fostering community engagement through alerts on limited-edition items and loyalty rewards, effectively transforming one-time buyers into loyal patrons.

Geography Analysis

In 2025, North America accounted for 27.62% of global luxury revenue, bolstered by its rich luxury heritage, a high concentration of ultra-high-net-worth individuals, and robust tourism spending. Printemps’ inauguration of a 55,000-square-foot flagship in New York underscores the ongoing investment in prestigious real estate, even amidst the rise of e-commerce. While local sustainability laws, such as California’s textile take-back mandate, complicate operations, they also reward established players capable of managing compliance costs.

Asia-Pacific leads the luxury apparel market with a 6.48% CAGR through 2031. This growth is fueled by rising incomes in the middle class, a shift towards digital purchasing, and the resurgence of cross-border travel. Japan, with its weakened yen, draws in bargain-hunting tourists, leading to record sales in department stores as visitor numbers bounce back. Concurrently, Hongkong Land’s USD 1 billion investment to enhance its LANDMARK complex, featuring 10 multi-story Maison concepts, signals a bullish outlook on Greater China's luxury fashion appetite.

Europe navigates a landscape of established demand and rigorous regulations. The EU's impending Corporate Sustainability Due Diligence rules elevate documentation standards, yet top maisons turn this challenge into an opportunity, using transparency as a unique selling point. Via Monte Napoleone in Milan, now fetching an annual rent of USD 23,583 per m², stands as a testament to the resilience of premier shopping districts, driven by tourist interest. Meanwhile, Brexit reshapes the movement of creative talent, introducing new challenges for sourcing and logistics in pan-European businesses. While South America and the Middle East and Africa present long-term growth potential, currency fluctuations and infrastructural challenges pose hurdles for immediate expansion.

Competitive Landscape

Regional and global players, particularly heritage houses, dominate the moderately fragmented luxury apparel market, leveraging brand equity and established distribution networks. This concentration erects formidable entry barriers, making it challenging for new luxury brands to navigate capital demands, brand development hurdles, and restricted access to distribution channels. The industry is witnessing a strategic pivot from price-centric competition to a focus on operational efficiency. Notably, brands like Chanel and Prada are acquiring suppliers, bolstering their supply chain control and agility.

Such vertical integration not only hastens market responsiveness but also elevates quality control, which is crucial in a domain where craftsmanship sets brands apart. There's a burgeoning market where technology intersects with traditional luxury, especially in realms like sustainability and digital engagement. Brands are turning to Enterprise Asset Management (EAM) systems, streamlining manufacturing and retail processes, and enhancing both compliance and customer experience. These advancements are reshaping how luxury brands operate in an increasingly competitive environment.

The competitive landscape is shifting, welcoming newcomers like digital-first luxury brands that bypass conventional distribution channels and sustainable luxury firms that are reshaping premium market perceptions. Highlighting the industry's focus on brand development and tech innovation, Kering's 2024 annual report reveals a hefty USD 1,058.31 million marketing spend and a notable USD 290.96 million investment in innovation. These investments underscore the importance of maintaining market position through technological advancements and strategic brand development.

Luxury Apparel Industry Leaders

-

LVMH Moët Hennessy Louis Vuitton

-

Prada Holding S.P.A.

-

Kering SA

-

Capri Holdings Limited

-

Hermès International S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Loewe has opened its new CASA Loewe Shanghai flagship store in the Jing'an district, at the intersection of Nanjing West and Changde Road. The 695 m² space, the largest Loewe flagship store in Asia, offers a comprehensive range of products, including men's and women's ready-to-wear and store-exclusive items.

- January 2025: Prada launched its Fall/Winter 2025 Menswear collection at Milan Fashion Week. The collection, designed by Miuccia Prada and Raf Simons, examines fundamental aspects of human nature and their influence on creative expression.

- November 2024: Gucci announced its comeback to co-ed fashion shows, showcasing collections for both men and women simultaneously. The Italian luxury brand, under the ownership of the Kering group, revealed its intention to implement this format during Milan's womenswear weeks in February 2025, aligning with the Fall/Winter 2025-26 season. Furthermore, the brand is set to unveil its Spring/Summer 2026 collection in September 2025. On top of that, a co-ed cruise collection for 2026 is slated to make its debut on May 15th in Florence.

- November 2024: Dolce & Gabbana has collaborated with SKIMS to launch an exclusive collection that merges Italian luxury with modern comfort. This limited-edition line features a range of ready-to-wear and lingerie pieces, showcasing the iconic Dolce & Gabbana leopard print alongside SKIMS' signature body-positive designs.

Global Luxury Apparel Market Report Scope

Luxury clothes are usually fashionable, trendy, or high-class, and expensive. Brands not only focus on providing the latest looks but also cater to cultural trends and street culture to attract different kinds of consumers.

The luxury apparel market is segmented by product type, end purpose, end user, distribution channel, and geography. By product type, the market is segmented into trousers, jeans, T-shirts & shirts, shorts & skirts, jackets, sweatshirts & hoodies, innerwear, dresses & gowns, and other product types. The market is segmented by end purpose into athleisure and fashion & casual. By end user, the market is segmented into men, women, and children. By distribution channels, the market is segmented into specialty stores, online retail stores, and other distribution channels. The market is segmented by geography into North America, Europe, Asia, South America, and the Middle East and Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

| Trousers |

| Jeans |

| T-Shirts and Shirts |

| Shorts and Skirts |

| Jackets, Sweatshirts and Hoodies |

| Innerwear |

| Dresses and Gowns |

| Other Product Types |

| Athleisure |

| Fashion and Casual |

| Men |

| Women |

| Kids/Children |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Nigeria | |

| Saudi Arabia | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Trousers | |

| Jeans | ||

| T-Shirts and Shirts | ||

| Shorts and Skirts | ||

| Jackets, Sweatshirts and Hoodies | ||

| Innerwear | ||

| Dresses and Gowns | ||

| Other Product Types | ||

| By End-Purpose | Athleisure | |

| Fashion and Casual | ||

| By End User | Men | |

| Women | ||

| Kids/Children | ||

| By Distribution Channel | Specialty Stores | |

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Nigeria | ||

| Saudi Arabia | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the luxury apparel market?

The luxury apparel market is valued at USD 144.77 billion in 2026.

How fast is the luxury apparel market expected to grow?

It is projected to register a 4.42% CAGR, reaching USD 179.71 billion by 2031.

Which product category leads the luxury apparel market?

T-Shirts and Shirts hold the largest 2025 share at 44.62%, reflecting the shift toward elevated everyday wear.

Which region shows the strongest growth outlook?

Asia-Pacific is forecast to expand at a 6.48% CAGR through 2031, driven by rising middle-class spending and digital shopping adoption.

Page last updated on: