Alpaca Apparel and Accessories Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

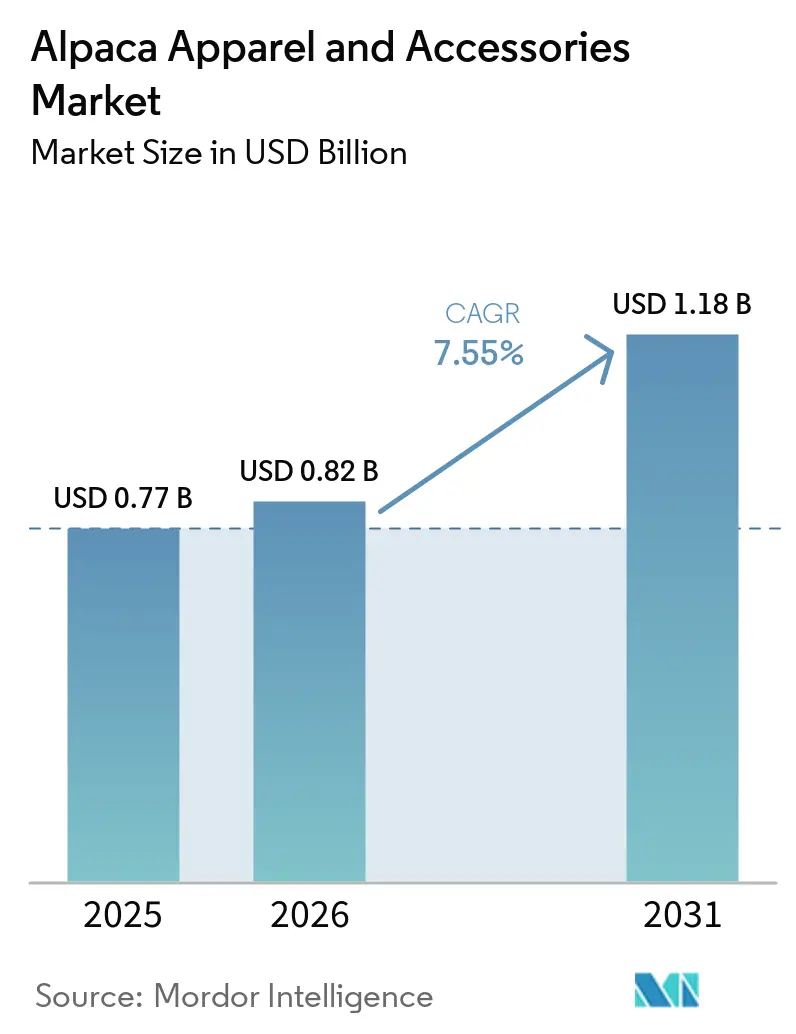

| Market Size (2026) | USD 0.82 Billion |

| Market Size (2031) | USD 1.18 Billion |

| Growth Rate (2026 - 2031) | 7.55% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Alpaca Apparel and Accessories Market Analysis by Mordor Intelligence

The alpaca apparel and accessories market is projected to grow significantly, with its size anticipated to rise from USD 0.77 billion in 2025 to USD 0.82 billion in 2026, eventually reaching USD 1.18 billion by 2031, reflecting a robust CAGR of 7.55% during the forecast period of 2026-2031. This growth is primarily driven by increasing consumer preference for sustainable luxury products, with factors such as fiber origin, product authenticity, and natural performance playing pivotal roles in purchasing decisions alongside aesthetic appeal. The rising demand for natural thermal textiles is bolstering the market, as consumers increasingly prioritize materials that provide warmth, comfort, and reduced dependence on synthetic inputs. Competitive dynamics in the market are increasingly shaped by companies' ability to ensure traceable sourcing, maintain certified fiber quality, and establish a strong premium narrative that justifies higher pricing. However, challenges such as the risks of counterfeit products and the concentration of supply chains remain critical constraints that market players must address to sustain growth and competitiveness.

Key Report Takeaways

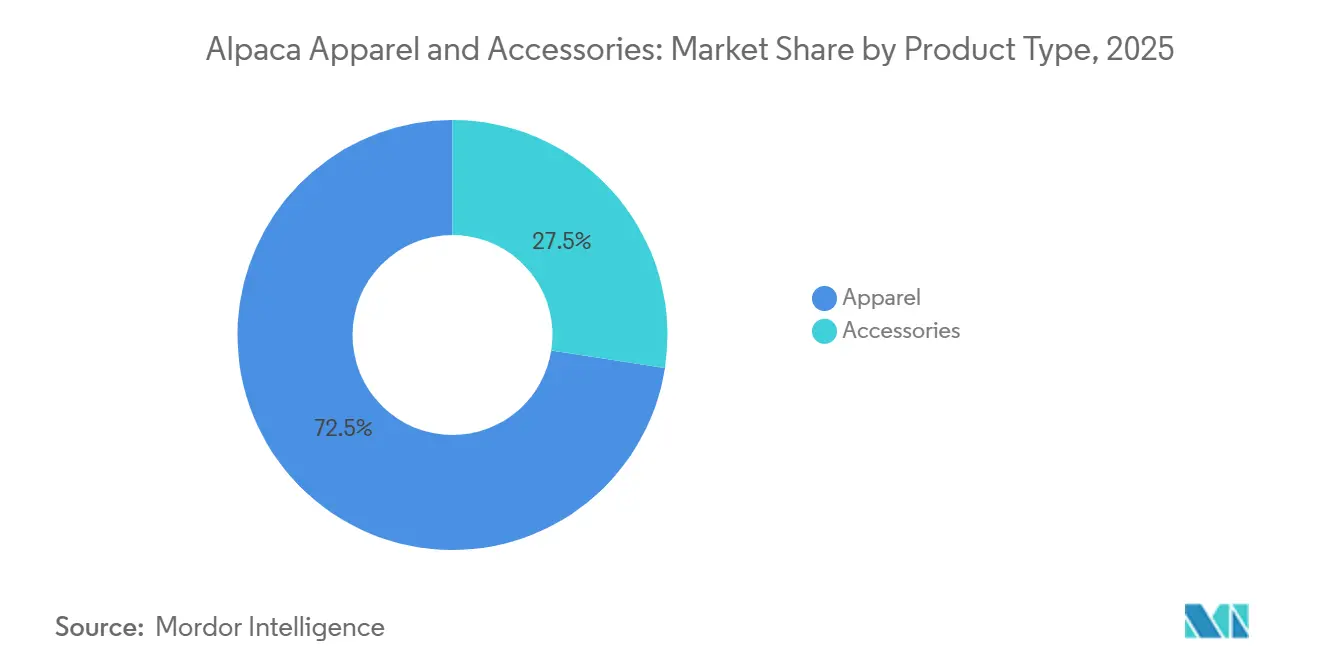

- By product type, apparel held 72.54% of the alpaca apparel and accessories market share in 2025, while accessories are forecast to expand at an 8.47% CAGR through 2031.

- By end user, women accounted for 58.17% of the alpaca apparel and accessories market share in 2025, while men recorded the highest projected CAGR at 8.52% through 2031.

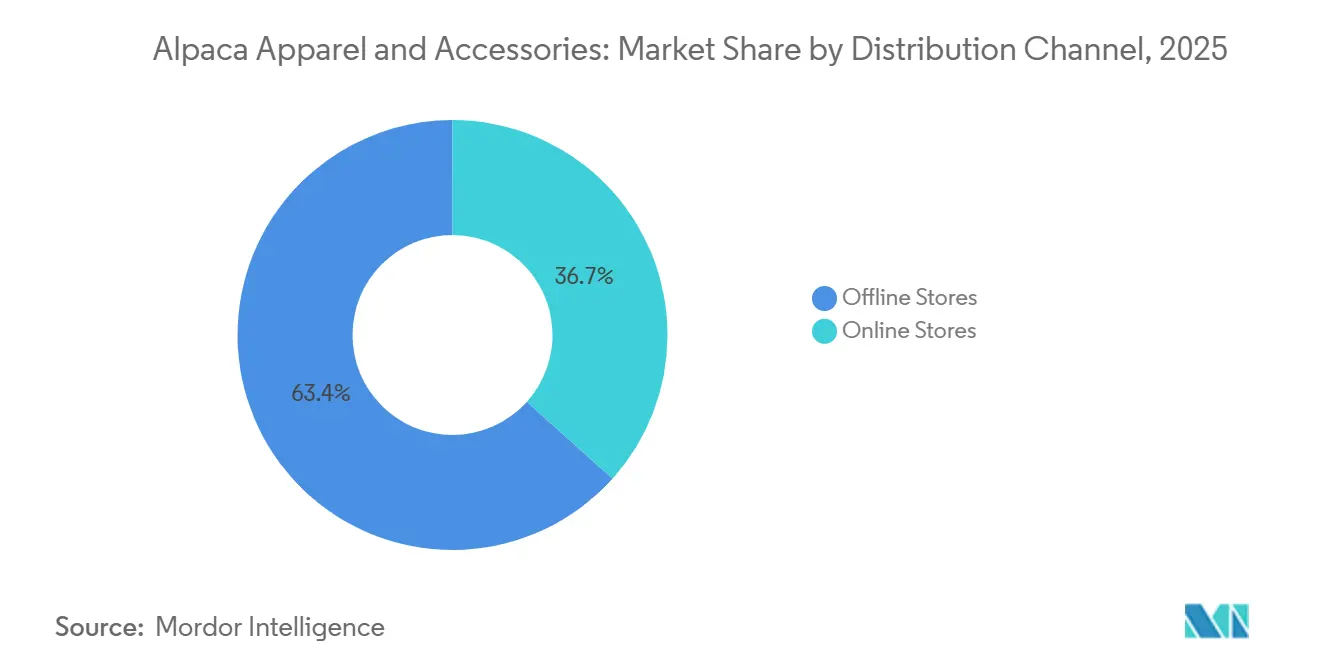

- By distribution channel, offline retail accounted for 63.35% of the global alpaca apparel and accessories market in 2025, while online stores are advancing at a 8.33% CAGR through 2031.

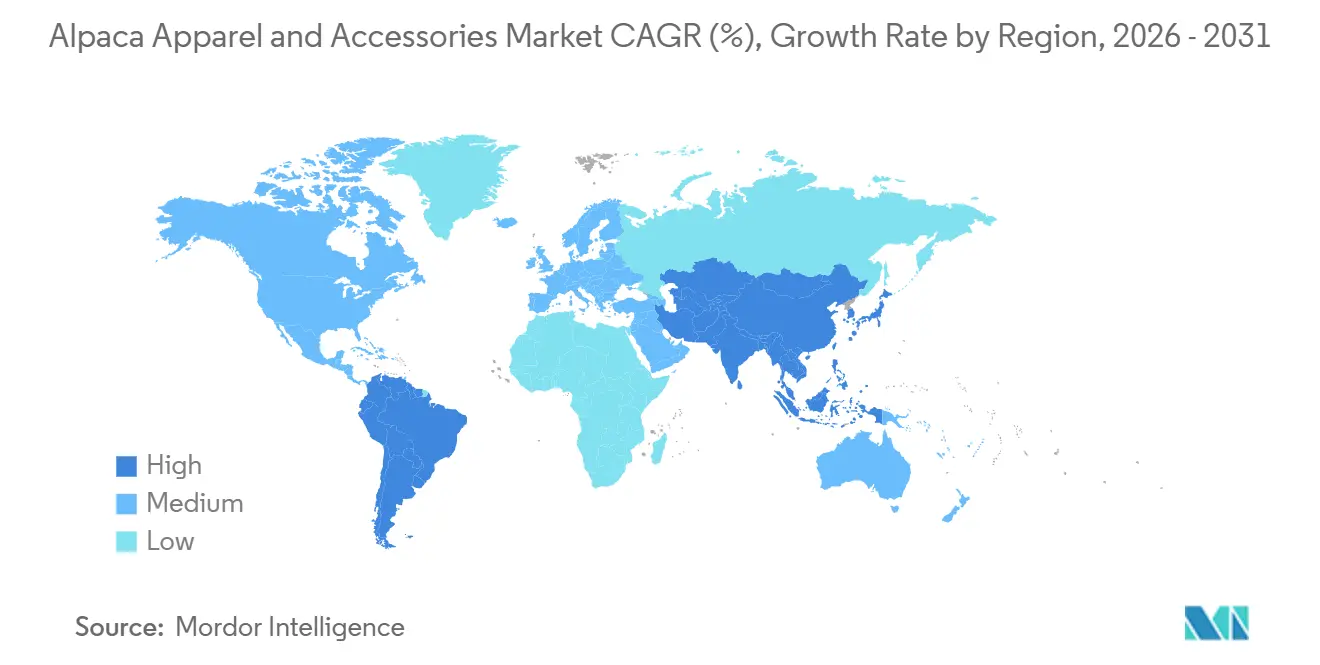

- By geography, North America held 32.68% of the alpaca apparel and accessories market share in 2025, while Asia-Pacific is forecast to expand at an 8.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Alpaca Apparel and Accessories Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for thermally efficient natural-fiber apparel and accessories | +1.8% | Global, with intensity in North America, Northern Europe, and Northeast Asia | Short term (≤ 2 years) |

| Growing penetration of alpaca fiber in designer and luxury fashion collections | +1.5% | Europe (Italy, France, United Kingdom) and North America (United States) as primary markets | Medium term (2-4 years) |

| Expanding adoption of ethical and traceable fashion products | +1.2% | Global; early gains concentrated in North America and Europe | Medium term (2-4 years) |

| Awareness of hypoallergenic and skin-friendly textile products | +0.9% | Global, with notable demand in North America, Europe, and Asia-Pacific core | Short term (≤ 2 years) |

| Tourism demand for authentic alpaca-based fashion and souvenir products | +0.7% | South America (Peru, Bolivia), with spill-over to Asia-Pacific travel retail | Short term (≤ 2 years) |

| Product innovation in contemporary alpaca apparel and accessory designs | +0.9% | Global; most impactful in North America and Asia-Pacific emerging luxury | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing demand for thermally efficient natural-fiber apparel and accessories

The alpaca apparel and accessories market is witnessing significant growth, driven by rising consumer demand for sustainable, natural-fiber clothing that offers superior thermal efficiency and comfort. Alpaca fiber, known for its softness, warmth, and lightweight properties, is increasingly being preferred over traditional wool and synthetic materials. Sustainability has emerged as a critical factor influencing purchasing decisions, with a June 2024 report by Program for the Endorsement of Forest Certification (PEFC) International indicating that over 60% of European consumers consider sustainability labels when buying clothing[1]Source: Program for the Endorsement of Forest Certification (PEFC) International, "Consumer Survey: Fashion From Sustainable Forests", cdn.pefc.org. In response to this trend, companies like PAKA have taken proactive steps to enhance transparency and traceability in their supply chains. For instance, in November 2024, PAKA expanded its Traceable Alpaca Program across its entire product range, allowing customers to scan QR codes and trace the origin of the alpaca fiber used in each garment.

Growing penetration of alpaca fiber in designer and luxury fashion collections

The growing use of alpaca fiber in designer and luxury fashion collections is driving significant growth in the global alpaca apparel and accessories market. Luxury fashion brands are increasingly integrating this premium natural fiber into their product lines to meet rising consumer demand for high-quality, sustainable, and ethically sourced materials. This trend was prominently showcased at Perú Moda Deco & Alpaca Fiesta 2024, where renowned fashion houses such as Christian Dior, Balmain, Prada, and MM LaFleur actively collaborated with Peruvian alpaca suppliers. These collaborations aimed to strengthen sourcing partnerships and explore innovative product opportunities, further solidifying alpaca fiber's position in the luxury segment. The involvement of these high-end brands not only enhances the global visibility of alpaca fiber but also elevates its perceived value, driving its adoption across various premium apparel and accessory categories.

Awareness of hypoallergenic and skin-friendly textile products

Increasing awareness of hypoallergenic and skin-friendly textile products is significantly driving the growth of the global alpaca apparel and accessories market. Modern consumers are placing greater emphasis on comfort, softness, and skin compatibility when selecting premium apparel and accessories, particularly as irritation and allergic reactions associated with conventional wool products become more prominent concerns. Alpaca fiber, known for its smooth texture and hypoallergenic nature, is emerging as a preferred alternative to traditional wool. According to Alpaca Apparel UK, as of January 2025, alpaca fiber lacks lanolin, a common allergen found in sheep's wool, making it an ideal choice for individuals with sensitive skin or wool allergies[2]Source: Alpaca Apparel UK, "The Future of Fashion: Why Hypoallergenic Alpaca Knitwear is a Great Choice", alpacaapparel.co.uk. This unique property is fueling demand for alpaca-based products such as apparel, scarves, wraps, and socks, especially among consumers seeking high-quality, skin-friendly options.

Tourism demand for authentic alpaca-based fashion and souvenir products

The increasing demand for authentic alpaca-based fashion and souvenir products among tourists is driving significant growth in the global alpaca apparel and accessories market. Travelers are progressively seeking unique, locally crafted, and sustainable items that reflect the cultural heritage of the destinations they visit. This shift in consumer preferences aligns with the broader growth of the global tourism industry, which, according to the World Travel & Tourism Council (WTTC), contributed USD 11.6 trillion to global GDP in 2025[3]Source: World Travel & Tourism Council, "Travel & Tourism Economic Impact Research (EIR)", wttc.org. Destinations renowned for alpaca production, such as Peru, are experiencing heightened demand for alpaca-based products, including sweaters, scarves, ponchos, shawls, and other handcrafted accessories that highlight traditional Andean craftsmanship. The rise of cultural and experiential tourism is further amplifying the appeal of alpaca products, as tourists increasingly value meaningful and authentic experiences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High product prices compared to conventional wool and synthetic alternatives | -1.0% | Global; most pronounced in price-sensitive emerging markets within Asia-Pacific and Middle East and Africa | Long term (≥ 4 years) |

| Competition from established luxury fibers such as cashmere and merino wool | -0.8% | Europe & North America (core luxury markets); Asia-Pacific premium segment | Medium term (2-4 years) |

| Counterfeit and misleading fiber labeling practices | -0.5% | Global; acute in South America tourism corridors and Asian e-commerce platforms | Short term (≤ 2 years) |

| Supply chain dependence on specific geographic regions | -0.6% | Global supply chain; upstream risk concentrated in Peruvian Andean highlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from established luxury fibers such as cashmere and merino wool

Competition from well-established luxury fibers such as cashmere and Merino wool continues to pose a significant challenge for the alpaca apparel and accessories market. These fibers have built strong consumer trust over decades, supported by their widespread availability, consistent quality, and reputation for offering superior comfort and luxury. Cashmere, in particular, dominates the premium apparel segment, while Merino wool has carved a niche in performance and outdoor wear due to its recognized functional benefits, such as moisture-wicking and breathability. Despite alpaca fiber's unique advantages, including its sustainability, exceptional softness, lightweight nature, and superior thermal insulation, its adoption remains gradual. This slow uptake is partly due to limited consumer awareness and the need for alpaca brands to compete against the entrenched market presence of cashmere and Merino wool. To overcome these challenges, alpaca manufacturers must invest significantly in marketing, consumer education, and brand positioning to highlight the distinctive qualities of alpaca fiber.

High product prices compared to conventional wool and synthetic alternatives

High product prices, compared with conventional wool and synthetic alternatives, continue to be a significant barrier to the growth of the global alpaca apparel and accessories market. The premium pricing of alpaca products stems from several factors, including the limited supply of alpaca fiber, labor-intensive farming and shearing processes, specialized manufacturing techniques, and elevated production costs. Consequently, these products primarily cater to affluent consumers and high-end fashion markets, making them less accessible to price-sensitive demographics. In many developing and emerging economies, alpaca apparel is often perceived as a luxury purchase, suitable for gifting or occasional use, rather than a practical, everyday clothing option. To address this challenge, manufacturers are increasingly exploring strategies such as introducing blended-fiber products and more affordable entry-level accessories to attract a broader customer base.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Apparel Anchors Volume, Accessories Expand the Category

In 2025, apparel accounted for 72.54% of the alpaca apparel and accessories market. This significant share is driven by high demand for alpaca-based garments, such as sweaters, cardigans, coats, and ponchos, valued for their softness, warmth, and durability. The increasing consumer preference for natural and sustainable fibers has further propelled the adoption of alpaca apparel, particularly in premium and luxury fashion segments. The rise of eco-conscious fashion trends and the growing influence of online retail platforms have bolstered global sales. Manufacturers are also focusing on introducing innovative designs and collections to meet consumers' evolving tastes, ensuring sustained growth in this segment.

The accessories segment is projected to grow the fastest, with a CAGR of 8.47% through 2031. This growth is fueled by rising demand for high-quality alpaca accessories, including scarves, gloves, hats, shawls, and socks. Consumers are increasingly drawn to lightweight, comfortable, and environmentally friendly fashion products, enhancing the appeal of alpaca accessories. The segment also benefits from the growing trend of gifting and increased spending on luxury fashion items. Furthermore, the diversification of product offerings and the widespread availability of alpaca accessories through e-commerce platforms are expected to drive consistent growth in the coming years.

By End User: Women Lead, Men’s Premium Demand Builds Momentum

Women continue to dominate the alpaca apparel and accessories market, contributing 58.17% of the total market value in 2025. This leadership is attributed to the high demand for alpaca-based products such as sweaters, scarves, shawls, and ponchos, which are both stylish and functional. The growing inclination toward sustainable, premium clothing has further fueled the adoption of alpaca apparel among female consumers. Increased spending on luxury fashion and the availability of diverse, innovative designs have reinforced the segment's prominence. To cater to evolving fashion trends, brands are increasingly launching women-centric alpaca collections, enhancing their appeal in this segment.

The men's segment, on the other hand, is expected to grow the fastest, with a projected CAGR of 8.52% through 2031. This growth is driven by rising awareness of alpaca fiber's unique properties, including durability, thermal insulation, and moisture-wicking, which make it ideal for a range of apparel categories. The increasing demand for premium casualwear, outdoor clothing, and sustainable fashion has opened new avenues for this segment. Manufacturers are expanding their product offerings by introducing alpaca-based jackets, sweaters, socks, and accessories tailored to male preferences. Furthermore, higher disposable incomes and a shift toward high-quality, natural-fiber products are anticipated to sustain the segment's rapid expansion.

By Distribution Channel: Offline Retail Leads, Online Reach Expands

Offline retail dominated the alpaca apparel and accessories market in 2025, contributing 63.35% of the total market value. This channel remains popular as consumers prefer to physically assess the quality, texture, and comfort of alpaca products before making a purchase. Specialty stores, luxury boutiques, department stores, and brand-owned outlets play a significant role by offering personalized shopping experiences and hands-on product demonstrations. The immediate availability of products and strong brand visibility in physical stores have reinforced the dominance of offline retail. The premium nature of alpaca products further aligns with the exclusivity offered by brick-and-mortar outlets, driving consistent demand through this channel.

In contrast, online retail is projected to be the fastest-growing distribution channel, with a CAGR of 8.33% through 2031. The growth of this segment is fueled by increasing internet penetration, the expansion of e-commerce platforms, and the rising preference for convenient shopping experiences. Online channels provide consumers with access to a broader range of products, competitive pricing, and direct-to-consumer options, making them increasingly attractive. Alpaca apparel brands are leveraging digital marketing strategies and social media promotions to enhance their online presence and boost sales. Furthermore, advancements in logistics and the growth of cross-border e-commerce are expected to sustain the rapid expansion of online retail during the forecast period.

Geography Analysis

North America dominated the alpaca apparel and accessories market in 2025, accounting for 32.68% of total market revenue. The region's growth is driven by a strong preference for premium and sustainable natural-fiber products, particularly in the United States. The increasing popularity of luxury apparel, coupled with a growing inclination toward eco-friendly fashion, has significantly boosted demand. Additionally, the expansion of direct-to-consumer sales channels has further fueled market growth. For instance, in March 2025, PAKA partnered with major United States retailers to enhance the availability of its alpaca-fiber apparel, making sustainable clothing more accessible to consumers. The rising adoption of alpaca-based products among both men and women continues to strengthen the region's market position.

Asia-Pacific is anticipated to be the fastest-growing region in the alpaca apparel and accessories market, with a projected CAGR of 8.52% through 2031. The region's growth is supported by increasing disposable incomes, heightened awareness of sustainable fashion, and a rising demand for premium apparel. Countries such as China, Japan, South Korea, and Australia are witnessing a surge in interest in luxury natural-fiber products, creating lucrative opportunities for market players. Furthermore, the influence of global fashion trends and the rapid expansion of e-commerce platforms are driving market penetration. As consumers increasingly prioritize high-quality and eco-friendly textiles, Asia-Pacific is expected to emerge as a critical growth hub for the market.

Europe remains a significant market for alpaca apparel and accessories, driven by strong demand for sustainably sourced and high-quality textile products. Consumers in key European countries value premium natural fibers for their comfort, durability, and environmental advantages. The region's well-established luxury fashion industry and robust textile manufacturing infrastructure play a pivotal role in sustaining demand for alpaca-based products. The growing focus on sustainability, traceability, and ethical sourcing practices is encouraging the adoption of alpaca apparel. Meanwhile, South America continues to serve as a vital production hub for alpaca fiber, while the Middle East and Africa are gradually emerging as promising markets due to expanding premium fashion retail networks and increasing consumer awareness.

Competitive Landscape

The alpaca apparel and accessories market is characterized by moderate fragmentation, with key players including Alpaca Direct, LLC, Peru Unlimited, KUNA, Alpaca Collections, and Shupaca. The absence of a dominant market leader creates opportunities for both vertically integrated manufacturers and niche premium brands to thrive. Competition in this market is driven by factors such as fiber quality, transparency in sourcing, product innovation, craftsmanship, and brand reputation, rather than sheer scale. This dynamic enables established companies and emerging direct-to-consumer brands to cater to diverse consumer preferences. As demand for sustainable, high-quality natural-fiber products continues to rise, differentiation remains a critical factor for success.

Prominent companies like Michell Group and Incalpaca TPX leverage their vertically integrated operations to maintain control over fiber sourcing, processing, product quality, and distribution. These capabilities ensure consistent product standards and foster long-term partnerships with international fashion and retail brands. Additionally, collaborations between alpaca suppliers and global luxury fashion brands are emphasizing the importance of quality assurance, traceability, and ethical sourcing practices. For example, in June 2024, KUNA launched its Alpaca Lovers Fall-Winter 2024 Collection through a fashion show in Peru, highlighting premium alpaca garments and reinforcing its commitment to sustainable fashion and luxury craftsmanship. Such initiatives enhance consumer engagement and strengthen the competitive positioning of premium brands in the market.

Digital-first and sustainability-focused brands are playing a transformative role in shaping the competitive landscape of the alpaca apparel and accessories market. Companies like PAKA are utilizing product traceability technologies, transparent sourcing methods, and sustainability-focused messaging to attract environmentally conscious consumers. The growing demand for ethical production standards and verifiable supply chains is prompting brands to invest in transparency initiatives and certification programs. Meanwhile, smaller brands are differentiating themselves through artisanal craftsmanship, community-based sourcing practices, and exclusive product offerings. Moving forward, competition is expected to center around sourcing integrity, sustainability credentials, compelling brand narratives, and premium product positioning.

Alpaca Apparel and Accessories Industry Leaders

-

Alpaca Direct, LLC

-

Peru Unlimited

-

KUNA

-

Alpaca Collections

-

Shupaca

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: PAKA unveiled the Women’s Original Crew Sweater in honor of International Women’s Month, aiming to celebrate and empower women. This launch further strengthened its women-centric alpaca apparel collection, showcasing the brand’s dedication to providing high-quality, sustainable, and stylish options for female consumers.

- February 2026: Alpaca Apparel launched a premium line of alpaca-fiber garments tailored for outdoor and lifestyle consumers. The company emphasized the natural performance advantages of alpaca wool, such as warmth, breathability, moisture management, and durability.

- May 2025: PAKA expanded its product portfolio by introducing the Coolplus Collection, an ultralight alpaca apparel line tailored for warm-weather conditions.

- November 2024: AKA introduced the Mountain Crew Line, broadening its selection of alpaca-based performance apparel tailored for outdoor enthusiasts. This collection was crafted to deliver superior comfort, warmth, and durability, utilizing sustainably sourced alpaca fiber.

Global Alpaca Apparel and Accessories Market Report Scope

Alpaca apparel and accessories encompass clothing, footwear, and fashion items crafted from alpaca fiber, renowned for its softness, warmth, durability, and lightweight characteristics. The global alpaca apparel and accessories market comprises product type, end user, distribution channel, and geography. Based on product type, the market is classified into apparel and accessories. Based on end user, the market is classified into men, women, and children. Based on the distribution channel, the market is classified into online stores and offline stores. Based on geography, the market is classified into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market forecasts are provided in terms of value (USD).

| Apparel | Sweaters and Cardigans |

| Jackets and Coats | |

| T-Shirts and Tops | |

| Socks | |

| Scarves and Shawls | |

| Ponchos and Capes | |

| Others | |

| Accessories | Hats |

| Bags/Handbags | |

| Gloves/Mittens | |

| Belts | |

| Others |

| Men |

| Women |

| Children |

| Online Stores | |

| Offline Stores | Single-Brand Stores |

| Multi-Brand Stores | |

| Other Offline Channels (Artisan Stores, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Apparel | Sweaters and Cardigans |

| Jackets and Coats | ||

| T-Shirts and Tops | ||

| Socks | ||

| Scarves and Shawls | ||

| Ponchos and Capes | ||

| Others | ||

| Accessories | Hats | |

| Bags/Handbags | ||

| Gloves/Mittens | ||

| Belts | ||

| Others | ||

| By End User | Men | |

| Women | ||

| Children | ||

| By Distribution Channel | Online Stores | |

| Offline Stores | Single-Brand Stores | |

| Multi-Brand Stores | ||

| Other Offline Channels (Artisan Stores, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the global alpaca apparel and accessories market by 2031?

The global alpaca apparel and accessories market is projected to reach USD 1.18 billion by 2031, rising from USD 0.82 billion in 2026, projected to grow at a CAGR of 7.55% over 2026-2031.

Which product category leads sales in alpaca apparel and accessories?

Apparel led the category with 72.54% of market value in 2025, supported by demand for sweaters, cardigans, jackets, coats, scarves, and shawls.

Which segment is growing fastest by product type?

Accessories are the fastest growing product category, with an expected CAGR of 8.47% through 2031, helped by lower entry prices and strong gifting demand.

Who is the main buyer group for alpaca products today?

Women remained the leading end user segment in 2025 with 58.17% of market value, although men are forecast to grow faster at 8.52% CAGR through 2031.

Page last updated on: