North America Hospital Gowns Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

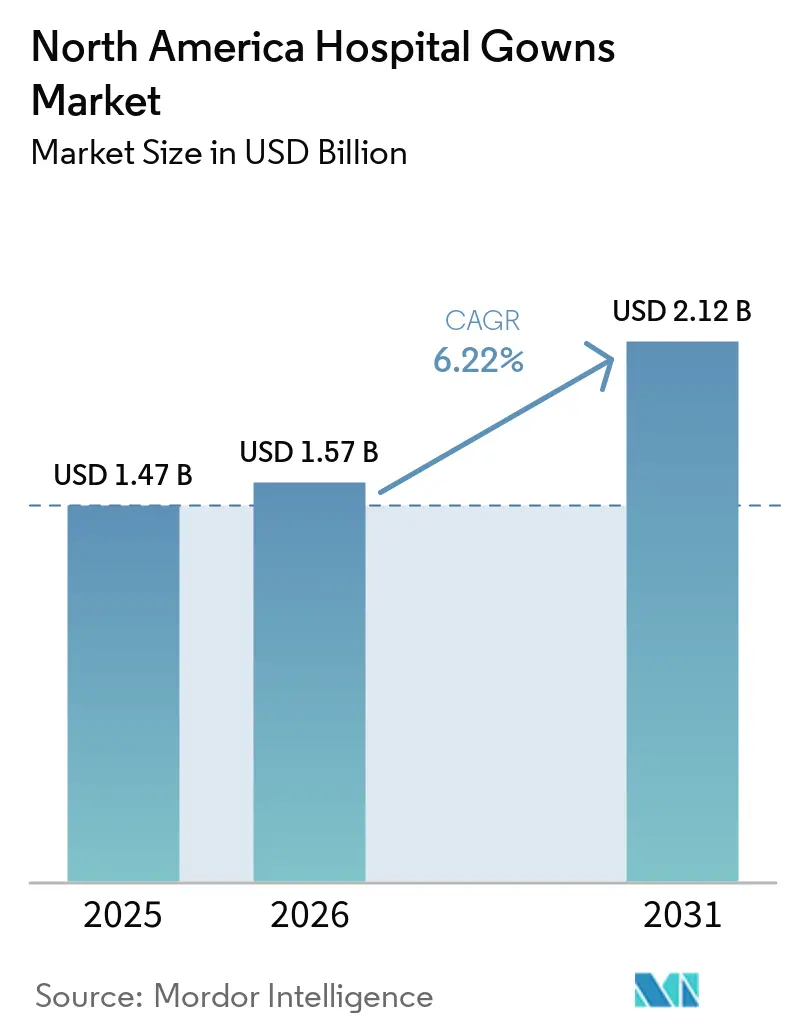

| Base Year Market Size (2025) | USD 1.47 Billion |

| Market Size (2026) | USD 1.57 Billion |

| Market Size (2031) | USD 2.12 Billion |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

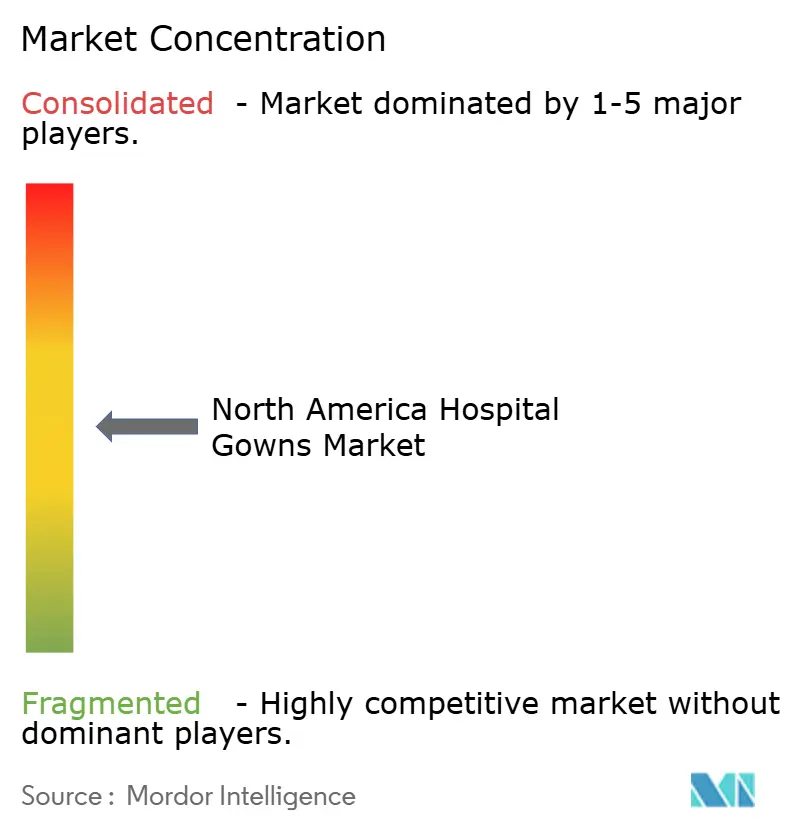

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Hospital Gowns Market Analysis by Mordor Intelligence

The North America Hospital Gowns Market size is expected to increase from USD 1.47 billion in 2025 to USD 1.57 billion in 2026 and reach USD 2.12 billion by 2031, growing at a CAGR of 6.22% over 2026-2031.

Demand in the North America hospital gowns market remains supported by healthcare facility expansion, stricter infection prevention practice, and a steady flow of elective and high-acuity procedures across the region. A structural shift toward ambulatory surgery is changing where gowns are bought, stocked, and used, which is widening the channel mix inside the North America hospital gowns market and raising the importance of flexible fulfillment. Procurement teams are also moving beyond unit price and are weighing reuse economics, laundry validation, product traceability, and waste reduction more directly in contract decisions across large health systems and multisite care networks. This is keeping competition balanced between large disposable suppliers and service-led reusable gown providers, especially in systems that want stronger continuity of supply, better compliance documentation, and clearer visibility into total textile use. Cost pressure, raw material exposure, and barrier-performance compliance remain real limits, yet vendors that can manage documentation, service reliability, and product mix are still finding room to expand in the North America hospital gowns market.

Key Report Takeaways

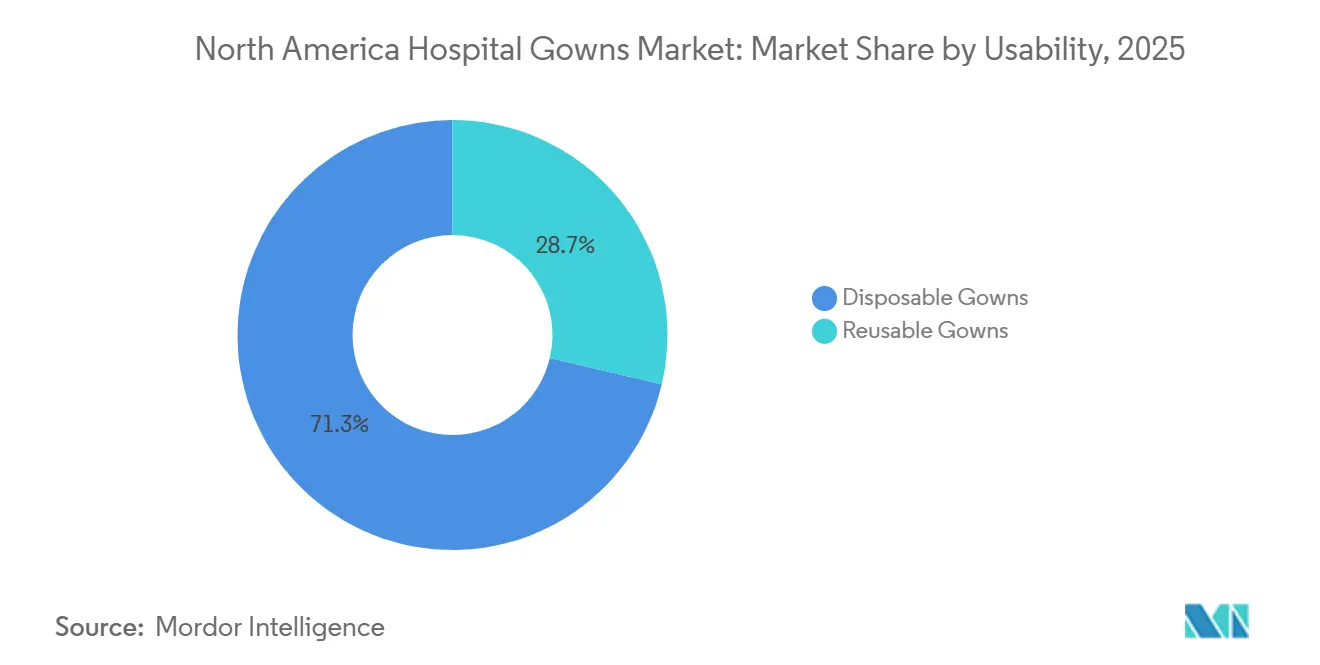

- By usability, disposable gowns held 71.31% of North America hospital gowns market share in 2025, while reusable gowns are forecast to expand at 8.38% CAGR through 2031.

- By type, surgical gowns accounted for 55.24% share of the North America hospital gowns market size in 2025, while patient gowns are projected to grow at 9.52% CAGR through 2031.

- By risk type, high-risk gowns held 34.52% revenue share in 2025 and are expected to project a 8.25% CAGR through 2031.

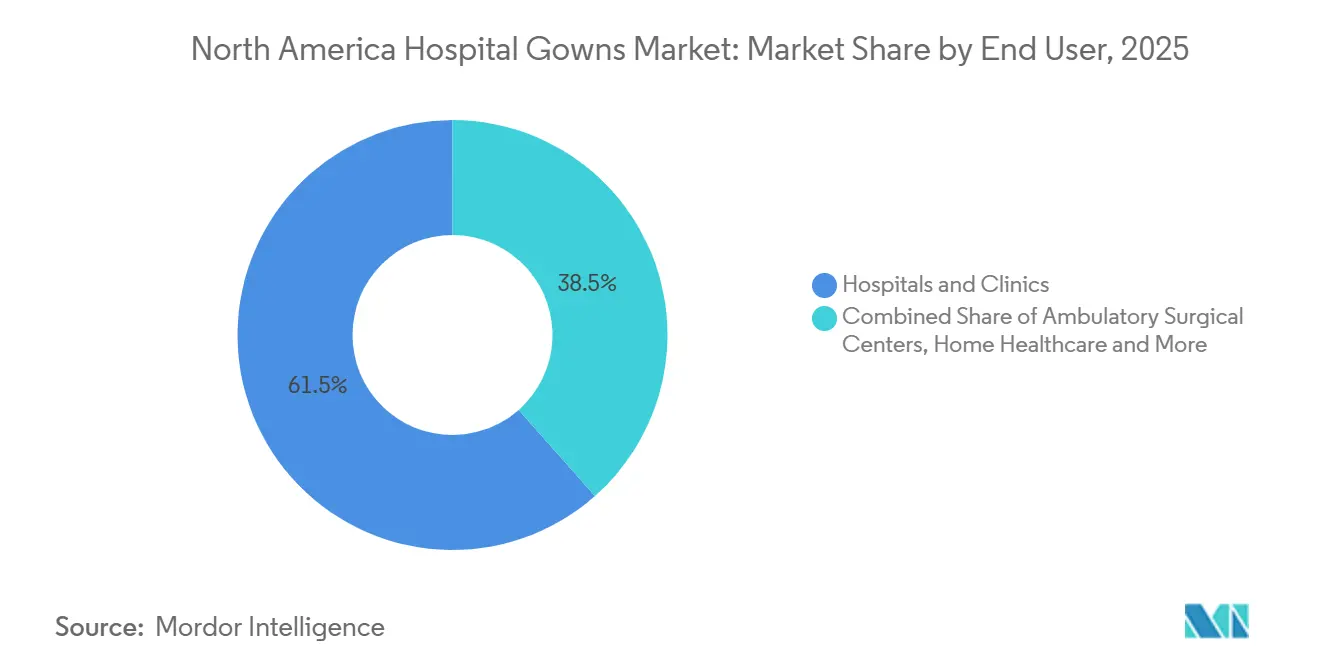

- By end user, Hospitals and Clinics accounted for 61.52% share of the North America hospital gowns market size in 2025, while ambulatory surgical centers are forecast to advance at 8.65% CAGR through 2031.

- By country, the United States held 84.22% of North America hospital gowns market share in 2025, while Mexico is projected to record the highest CAGR at 9.15% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Hospital Gowns Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infection Control Mandates and Hospital-Acquired Infection Prevention | +1.2% | Global, dominant in US and Canada | Short term (≤ 2 years) |

| Surgical Volume Growth and Procedural Throughput Requirements | +1.0% | North America-wide, led by US ASC expansion | Medium term (2-4 years) |

| Rising Preference for Disposable Gowns in High-Turnover Care Settings | +1.1% | US and Canada, spill-over to Mexico | Short term (≤ 2 years) |

| Sustainability-Led Reusable Gown Procurement in Mature Health Systems | +0.8% | US, Canada (particularly Ontario, BC) | Medium term (2-4 years) |

| Reusable Gown Laundering Validation and Closed-Loop Service Models | +0.6% | US, Canada, emerging in Mexico | Medium term (2-4 years) |

| Gown Performance Verification, Traceability, and Procurement Digitization | +0.5% | US-led, with early adoption in Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infection Control Mandates and Hospital-Acquired Infection Prevention

Infection control rules continue to set the base demand pattern for the North America hospital gowns market, because facilities still need compliant protective apparel across acute care, post-acute settings, and long-term care environments. CDC reporting cited by CIDRAP showed that 1 in 31 hospitalized patients had at least 1 healthcare-associated infection on any given day in 2024, which keeps prevention spending tied to routine care practice rather than temporary outbreak response. Lower rates for CLABSI, CAUTI, and hospital-onset C. difficile did not reduce the need for gowns, because those gains depended on consistent infection-control behavior and continued PPE discipline at the point of care[1]CIDRAP, “CDC Data Show Decline in Hospital-Related Infections in 2024,” University of Minnesota, cidrap.umn.edu. CDC Enhanced Barrier Precautions also extended gown-and-glove use for high-contact activities in nursing homes, which widened the use case beyond acute care hospitals and made utilization more routine in skilled nursing settings. That broader care footprint matters because gowns are no longer tied only to operating rooms or isolation episodes, they are also tied to everyday resident handling and direct-contact care tasks in facilities with vulnerable patients. The result is a demand floor that stays firm even when individual infection indicators improve, because the health systems that perform better are usually the ones that keep protective routines in place rather than easing them.

Surgical Volume Growth and Procedural Throughput Requirements

Surgical throughput remains a direct growth engine for the North America hospital gowns market, especially as more procedures move into ambulatory settings that need dependable supply and rapid replenishment. MedPAC reported that ambulatory surgical center volume per 1,000 Medicare fee-for-service beneficiaries rose 3.4% in 2024, which confirms that outpatient procedural demand kept moving higher and continued to shift case volume beyond the hospital setting[2]Medicare Payment Advisory Commission, “Ambulatory Surgical Center Services: Status Report,” Medicare Payment Advisory Commission, medpac.gov. This matters for gown demand because ASCs usually run tighter inventories and faster room turnover, which raises the value of ready-to-use stock, simple SKU planning, and dependable delivery cadence. It also changes channel economics, since many outpatient sites operate outside the large centralized procurement structures that define purchasing in major hospital systems. Vendors that can support premium barrier protection, responsive restocking, and a smaller-site service model are better positioned as procedural mix keeps changing across the region. What looks like a volume shift is also a distribution shift, and that gives suppliers with flexible fulfillment a clearer timing advantage in the North America hospital gowns market.

Rising Preference for Disposable Gowns in High-Turnover Care Settings

Disposable products still hold the strongest operational position in the North America hospital gowns market, especially where turnaround time, cross-contamination risk, and staffing limits shape daily workflow. FDA classifies surgical gowns as Class 2 medical devices, and the recognized ANSI/AAMI PB70 framework keeps liquid barrier performance at the center of procurement decisions in regulated care environments. In emergency departments, operating rooms, and high-volume outpatient centers, single-use gowns remove the reprocessing burden and reduce the operational friction that comes with collection, sorting, validation, and return cycles. Medline received FDA 510(k) clearance in February 2025 for its Level 4 Surgical Gown with Breathable Sleeves, which shows that suppliers are still trying to improve comfort and protection together in a category that often faces user acceptance tradeoffs. That product direction matters because clinician comfort can affect compliance in longer procedures, particularly when higher-barrier products are required for fluid-heavy cases. Facilities facing staffing shortages also stay more dependent on disposables, because reusable programs require tighter textile management and validation discipline than many sites can reliably support today.

Sustainability-Led Reusable Gown Procurement in Mature Health Systems

Sustainability goals are pushing a second growth lane inside the North America hospital gowns market, even though reusable gowns still trail disposables in current volume and remain more dependent on operational readiness. Island Health launched a reusable Level 2 isolation gown program in 2025, which showed that validated laundering and infection control can be aligned within an active health system rather than treated as a pilot concept. This matters because procurement teams are paying closer attention to total cost of ownership, waste reduction, and service reliability instead of relying only on first-cost comparisons for every textile decision. The shift is strongest in mature systems that can validate laundering performance, track garment cycles, and coordinate return logistics without disrupting patient care operations. Reusable adoption is also moving first into routine care, isolation corridors, and longer-stay environments where repeated daily use makes lifecycle economics easier to justify. As this model becomes more familiar, the North America hospital gowns market is likely to see more separation between facilities that can operationalize reuse at scale and facilities that still depend on disposable convenience.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium Product Cost Pressure in Budget-Constrained Facilities | -0.6% | US rural/safety-net hospitals, Canada public health system, Mexico public sector | Short term (≤ 2 years) |

| Regulatory and Barrier-Performance Compliance Complexity | -0.4% | US (FDA 510(k), AAMI PB70), Canada (Health Canada), Mexico (COFEPRIS) | Medium term (2-4 years) |

| Supply Chain Dependence on Nonwoven and Meltblown Inputs | -0.5% | North America-wide, with acute exposure in US import-dependent segment | Short term (≤ 2 years) |

| Operational Readiness Gaps for Reusable Gown Adoption | -0.4% | US mid-size and rural hospitals, Mexico public hospitals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premium Product Cost Pressure in Budget-Constrained Facilities

Cost pressure still limits how far the North America hospital gowns market can move into premium products across every care setting, especially where infection-control needs must be balanced against fixed operating budgets. Safety-net hospitals, critical access sites, and public facilities with constrained supply spending are more likely to favor lower-cost tiers when higher-barrier gowns carry a visible price premium over standard alternatives. That pressure becomes stronger under bundled and value-based payment models, because administrators are pushed to manage supply cost per encounter without disrupting clinical throughput or compliance. Hybrid purchasing is therefore becoming more common, with reusable products used for routine care and disposable products reserved for surgery or higher-risk isolation use. This approach protects clinical standards, but it can reduce unit demand for premium single-use gowns in facilities that are actively reviewing every line item in their textile budgets. The result is a slower upgrade cycle in budget-sensitive accounts, even when clinicians recognize the operational benefits of better barrier protection and more specialized gown formats.

Supply Chain Dependence on Nonwoven and Meltblown Inputs

Supply chain dependence on nonwoven and meltblown inputs remains a practical restraint for the North America hospital gowns market, because higher-barrier products rely on material layers that are not easily substituted without affecting performance. Disposable gowns depend on SMS and SMMS fabrics, and tighter availability in key barrier layers can quickly affect lead times, purchase planning, and manufacturer pricing. Post-pandemic supply normalization reduced emergency scarcity, but it did not remove sourcing risk tied to logistics conditions, resin cost movement, or import dependence across parts of the regional supply base. Because meltblown material is essential for higher-barrier products, disruptions tend to affect Level 3 and Level 4 gowns more directly than basic protective items with lower performance requirements. This creates a concentrated vulnerability in the premium end of the portfolio, where hospitals also expect tighter compliance documentation and dependable fill rates. Suppliers with multi-region sourcing, strong raw material qualification processes, and disciplined inventory planning are therefore better placed to protect service levels when material markets tighten.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Usability: Disposable Volume Dominates, Reusable Economics Gain Ground

Disposable gowns held 71.31% of North America hospital gowns market share in 2025, which reflected their entrenched role in surgical, isolation, and fast-turnover care environments where immediate availability remains a clinical expectation. Their lead was structural rather than temporary, because many infection-prevention protocols and day-to-day hospital workflows still favor single-use assurance when contact intensity is high and turnaround windows are short. This position is reinforced in emergency care, operating rooms, and outpatient sites that do not want added complexity from collection, sorting, or reprocessing steps between encounters. It is also reinforced by the regulatory culture around barrier validation, where facilities often prefer products with straightforward deployment and consistent unit-level performance. As a result, disposable volume remains deeply rooted across the North America hospital gowns industry even as procurement teams put more pressure on waste reduction and lifecycle cost.

Reusable gowns are forecast to expand at 8.38% CAGR through 2031, which makes them the faster-moving usability segment in the North America hospital gowns market as sustainability and cost-per-use logic gain wider acceptance. The growth case is strongest where health systems can support laundry validation, return logistics, and garment tracking without increasing operational burden for frontline staff. Island Health’s 2025 reusable gown program showed that these requirements can be managed inside a working care network while maintaining infection-control standards and consistent textile handling practices. Adoption is not moving fastest in complex surgical settings, because those environments carry more fluid-management demands and stricter barrier-performance expectations over prolonged procedures. It is moving faster in routine patient care, isolation corridors, and long-term care environments where gowns are changed often and the cumulative waste from disposables is easier to measure. This is why reusable programs are increasingly framed as operational systems rather than textile substitutions, because their economics depend on service design as much as garment specification.

By Type: Surgical Gowns Lead, Patient Gowns Accelerate on Outpatient Volume

Surgical gowns accounted for 55.24% share of the North America hospital gowns market size in 2025, which kept this category in the leading position across type segments and reflected its mandatory use in every operating room encounter. Their position remains supported by the broad range of invasive procedures that still require reliable barrier protection, standardized classification, and dependable SKU availability across hospital and outpatient settings. Revenue concentration stays strongest in surgical gowns because these products carry higher performance requirements and often command more value per unit than basic non-surgical alternatives. At the same time, the expansion of outpatient case flow is extending operating-room-equivalent gown demand into a wider set of facilities that do not purchase in exactly the same way as large hospitals. This keeps surgical gowns at the center of competitive strategy in the North America hospital gowns market, particularly for suppliers with premium barrier portfolios and strong delivery performance.

Patient gowns are projected to grow at 9.52% CAGR through 2031, which makes them the fastest-moving type segment as outpatient admissions, longer patient stays in selected settings, and comfort-related procurement priorities gain weight. Non-surgical gowns still serve a broad daily care base across nursing, examination, and post-procedure use, but their lower unit values keep the category more exposed to budget tradeoffs. Medline’s July 2025 launch of the ComfortTemp Patient Warming System showed how patient gown development is moving beyond basic coverage toward added clinical utility in perioperative care. That direction matters because providers are looking more closely at patient comfort, fit, and compliance when textile decisions affect both care experience and workflow efficiency. It also matters because premium patient gown formats can support broader care objectives without requiring the same barrier premium that defines surgical products. The patient gown opportunity is therefore expanding on both volume and design relevance, which gives suppliers space to differentiate in a category once treated as a simple commodity.

By Risk Type: High-Risk Protection Anchors Market, Demand Skewed by Procedural Mix

High risk gowns held 34.52% of the by-risk-type segment in 2025, which reflected the concentration of procurement value around AAMI Level 3 and Level 4 protection in surgery, trauma, emergency, and higher-exposure care settings. That share is disproportionate to patient census, because not every encounter is high exposure, yet the settings that do require stronger protection consume these gowns frequently and cannot compromise on validated performance. Operating rooms, trauma bays, isolation wards, and emergency departments therefore exert an outsized pull on the revenue mix even when lower-risk encounters remain more numerous in daily clinical activity. This segment also benefits from the fact that higher-barrier products are more tightly linked to formal compliance review and product qualification in regulated healthcare settings. FDA recognition of the ANSI/AAMI PB70 classification framework keeps purchasing anchored to validated barrier thresholds rather than informal substitution. That compliance discipline helps preserve demand for high-risk gowns even when facilities are scrutinizing supply budgets very closely.

High risk gowns remained the largest segment at 34.52% in 2025, while moderate risk gowns continued to occupy the middle of procurement portfolios for isolation, wound care, and situations where Level 2 protection meets clinical need without the full premium of reinforced designs. Minimal and low risk gowns cover the broadest range of routine tasks, including standard nursing activity, administrative clinical contact, and basic outpatient examination. Their wide use does not translate into equivalent value capture, because the price point is lower and facilities can be more willing to trade down in these categories when budgets tighten. Moderate risk products are receiving closer attention from procurement teams that want to reduce over-specification and simplify SKU counts without weakening compliance. This keeps the middle of the portfolio strategically important, especially for suppliers that can guide facilities on when higher-barrier protection is necessary and when it is not. The overall risk mix therefore reflects both clinical exposure and purchasing discipline, which is why segment performance is shaped as much by procedural setting as by simple encounter volume.

By End User: Hospitals and Clinics Anchor Volume, ASCs Drive Premium Segment Growth

Hospitals and Clinics held 61.52% share of the North America hospital gowns market size in 2025, which kept them as the largest end-user group because of scale, breadth of care activity, and established purchasing frameworks. Their purchasing power is anchored in multiyear contracting, large order volumes, and the need to serve everything from routine exams to surgery, emergency care, and isolation episodes within the same network. This makes continuity of supply a core requirement, often ahead of product novelty, because service disruptions can affect multiple departments at once. It also means gown decisions are often tied to standardization, compliance documentation, and the ability to support diverse clinical settings with a manageable number of approved SKUs. For this reason, the hospital and clinic segment still defines the baseline volume structure of the North America hospital gowns market even as other channels grow faster.

Ambulatory surgical centers are forecast to expand at 8.65% CAGR through 2031, which makes them the fastest-growing end-user segment as more procedures shift into outpatient care environments. MedPAC’s latest reporting supports this direction by showing continued growth in ASC utilization, which confirms that these sites are absorbing a larger procedural role within the care system. The commercial impact is important because ASCs often maintain leaner inventory, faster restocking needs, and a greater preference for ready-to-use products that fit high-turnover schedules. Long-term care also represents a meaningful demand pocket, since CDC Enhanced Barrier Precautions require gown-and-glove use for certain high-contact resident care activities and expand routine use outside hospital walls. Home healthcare remains the smallest end-user segment, but it is gaining relevance as more post-acute care moves into residential settings for wound care, oncology, and immunocompromised patients. Medline’s March 2026 Prime Vendor agreement with CarDon & Associates also showed that large suppliers are actively building scale in the long-term care channel, where structured infection-prevention purchasing is becoming more important.

Geography Analysis

The United States held 84.22% of North America hospital gowns market share in 2025, which made it the clear anchor for regional demand across both hospital and outpatient channels. Its lead reflects high surgical volume, a dense network of hospitals and ambulatory care sites, and a procurement environment that operates under formal device standards and accreditation expectations. That structure supports stable demand for compliant protective apparel across a wide mix of operating rooms, emergency departments, patient care floors, and long-term care units. Outpatient procedure growth is also strengthening premium gown demand beyond traditional hospital walls, and MedPAC’s 2024 utilization data points to continued expansion in the ASC setting. At the same time, the country does not behave as a single uniform market, because rural hospitals, safety-net facilities, academic systems, and multisite outpatient platforms all buy under different budget and service conditions.

Canada remained the second-largest country market in 2025, and its position was shaped by centralized procurement patterns across provincial health systems and coordinated buying structures. That setup can shift sizable volume through a limited number of contract decisions, which favors suppliers that can combine compliance support with dependable service execution. Island Health’s reusable gown initiative in 2025 showed that sustainability-led textile programs are moving from policy discussion into practical deployment inside Canadian care delivery. Cross-border sourcing links with the United States also keep supply resilience, validated laundering standards, and distribution dependability high on the agenda for Canadian buyers.

Mexico is projected to grow at 9.15% CAGR through 2031, which makes it the fastest-growing country in the regional footprint of the North America hospital gowns market. The country presents a different purchasing mix, with public procurement priorities and private hospital demand operating side by side rather than through a single dominant model. That split creates room for both value-oriented supply strategies and premium certified product offerings, depending on the facility type and patient mix being served. Mexico therefore stands out as the regional growth market where channel strategy, product positioning, and service flexibility may matter more than simple scale alone. Its role in the North America hospital gowns market is likely to keep rising as vendors look for expansion beyond the mature buying patterns seen in the United States and Canada.

Competitive Landscape

The North America hospital gowns market remains moderately consolidated at the top, with Medline Industries, Cardinal Health, and Owens & Minor/Halyard forming the core leadership tier in disposable surgical and isolation gowns. Their position is supported by broad healthcare relationships, large distribution capabilities, and the ability to serve high-volume accounts that require continuity across multiple care settings. The reusable portion of the market is shaped by a different competitive group, including Standard Textile, Encompass Group, and textile service operators whose strength depends more on laundering systems and logistics than on barrier-material scale alone. This dual structure leaves space for both product-led competition and service-led competition, which is why no single model defines the whole North America hospital gowns market.

Competition is also shifting toward service depth, digital visibility, and category extension rather than unit price alone inside the North America hospital gowns market. Medline’s 2025 rollout of its Mpower AI digital control tower, which was piloted with Northwestern Medicine and Providence, showed how leading suppliers are trying to link inventory visibility and operational analytics more tightly to hospital supply relationships. Medline’s July 2025 ComfortTemp launch also showed that patient gown design is moving toward added clinical functionality, not just fabric supply, which helps defend value in a category often treated as basic apparel[3]Medline, “Medline Launches New ComfortTemp Patient Warming System with Blankets and Gowns,” Medline Newsroom, newsroom.medline.com. Cardinal Health has also pursued product differentiation through clinically informed gown design, which indicates that innovation is still a live lever even in mature hospital textile categories. These moves suggest that larger suppliers are trying to build stickier customer relationships through workflow support, product specialization, and broader portfolio relevance rather than relying only on scale.

Reusable program operators are differentiating themselves through laundry validation, route density, and item-level traceability inside the North America hospital gowns market. United Hospital Services processes 20,000 RFID-tagged reusable gowns per day with Positek’s Textile Track solution, which shows that lifecycle monitoring is becoming operational rather than experimental in reusable gown programs. That capability matters because health systems want proof of wash cycles, barrier integrity, and available inventory across large multisite networks before they commit more volume to closed-loop textile models. The result is a competitive field where switching costs rise when a supplier can connect product availability, service verification, and utilization data in one program, which is steadily changing how value is defined in the North America hospital gowns market.

North America Hospital Gowns Industry Leaders

Medline Industries, LP

Cardinal Health, Inc.

Owens and Minor, Inc.

Molnlycke Health Care AB

Standard Textile Co., Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Medline signed a Prime Vendor deal with CarDon & Associates, a 20-community long-term care provider in Indiana. The agreement gives CarDon access to Medline's full medical-surgical portfolio, including textiles. This reflects a strategic move by distributors into post-acute care, driven by CDC infection prevention protocols shaping gown procurement.

- January 2026: Mexico's ISSSTE announced its Plan de Obras 2026, covering 241 hospital projects for construction, expansion, and renovation. This includes 7 second-level hospitals and new facilities in Tampico, Cancún, and Lázaro Cárdenas. The plan boosts hospital space and surgical capacity, creating demand for gowns in new facilities.

North America Hospital Gowns Market Report Scope

As per the scope of the report, hospital gowns are loose-fitting garments worn by patients during medical examinations, procedures, or hospital stays. They are designed to provide easy access for healthcare providers while maintaining patient comfort and modesty.

The segmentation for the North America hospital gowns market is categorized by usability, type, risk type, end user, and country. By usability, the market is divided into disposable gowns and reusable gowns. By type, it includes surgical gowns, non-surgical gowns, and patient gowns. By risk type, the segmentation covers minimal risk gowns, low risk gowns, moderate risk gowns, and high risk gowns. By end user, the market is segmented into hospitals and clinics, long-term care facilities, ambulatory surgical centers, and home healthcare. By country, the market is analyzed across the United States, Canada, and Mexico. For each segment, the market size and forecast are provided in terms of value (USD).

| Disposable Gowns |

| Reusable Gowns |

| Surgical Gowns |

| Non-Surgical Gowns |

| Patient Gowns |

| Minimal Risk Gowns |

| Low Risk Gowns |

| Moderate Risk Gowns |

| High Risk Gowns |

| Hospitals and Clinics |

| Long-Term Care Facilities |

| Ambulatory Surgical Centers |

| Home Healthcare |

| United States |

| Canada |

| Mexico |

| By Usability | Disposable Gowns |

| Reusable Gowns | |

| By Type | Surgical Gowns |

| Non-Surgical Gowns | |

| Patient Gowns | |

| By Risk Type | Minimal Risk Gowns |

| Low Risk Gowns | |

| Moderate Risk Gowns | |

| High Risk Gowns | |

| By End User | Hospitals and Clinics |

| Long-Term Care Facilities | |

| Ambulatory Surgical Centers | |

| Home Healthcare | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the 2026 value of the North America hospital gowns sector and where is it heading by 2031?

The sector is valued at USD 1.57 billion in 2026 and is projected to reach USD 2.12 billion by 2031, growing at a 6.22% CAGR over 2026 to 2031.

Which country leads regional demand for hospital gowns in North America?

The United States led the region with 84.22% share in 2025, supported by high surgical volume, dense healthcare infrastructure, and formal procurement standards.

Which product format is growing faster, disposable or reusable gowns?

Disposable gowns led with 71.31% share in 2025, but reusable gowns are growing faster at an 8.38% CAGR through 2031 as health systems focus more on lifecycle cost and sustainability.

Why are ambulatory surgical centers becoming more important for gown suppliers?

Ambulatory surgical centers are forecast to grow at 8.65% CAGR through 2031, and they often need faster replenishment, leaner inventory planning, and ready-to-use premium products.

Which gown type shows the strongest growth outlook through 2031?

Patient gowns are projected to grow at 9.52% CAGR through 2031, while surgical gowns remained the largest type segment with 55.24% share in 2025.

What is the main competitive pattern in this healthcare apparel space?

The top of the market is led by large disposable-gown suppliers, while reusable gown competition is shaped by textile service providers that differentiate through laundering validation, logistics, and traceability.

Page last updated on: