Hospital Gowns Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

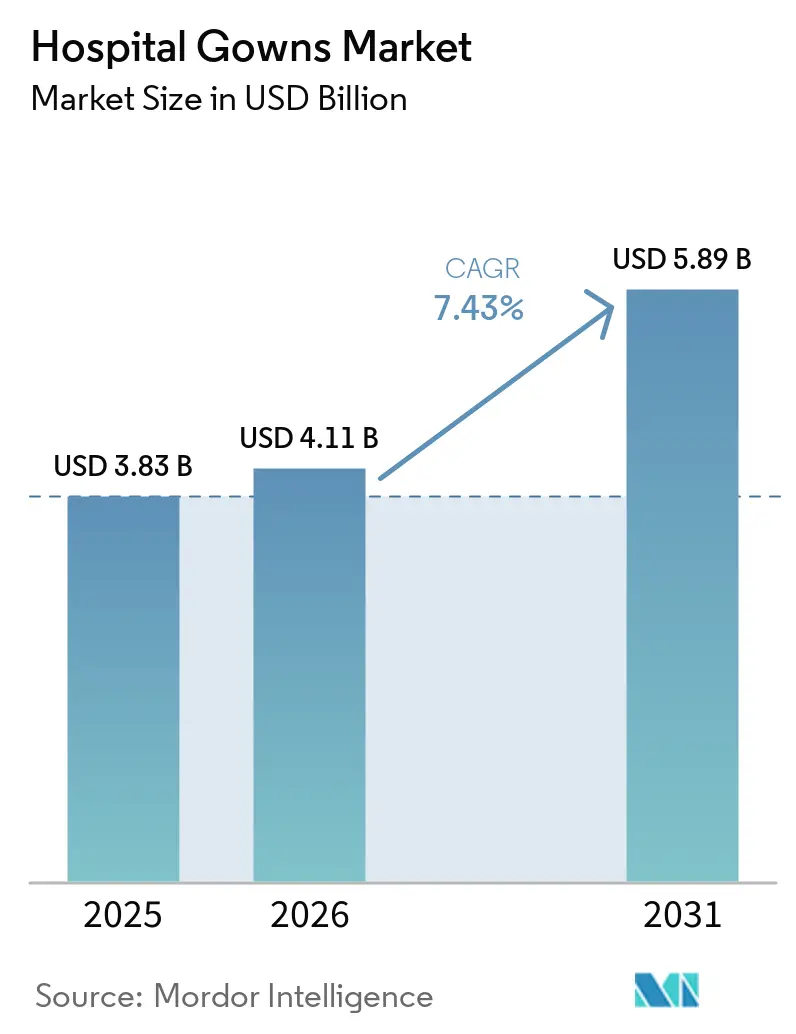

| Market Size (2026) | USD 4.11 Billion |

| Market Size (2031) | USD 5.89 Billion |

| Growth Rate (2026 - 2031) | 7.43% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hospital Gowns Market Analysis by Mordor Intelligence

The Hospital Gowns Market size is expected to grow from USD 3.83 billion in 2025 to USD 4.11 billion in 2026 and is forecast to reach USD 5.89 billion by 2031 at 7.43% CAGR over 2026-2031.

Demand remains firm because infection prevention rules, higher procedure volumes, and stricter control of healthcare associated infections keep gown use embedded across hospitals, long term care, and ambulatory care settings. Surgical recovery and the continuing shift of procedures into efficient outpatient settings are raising gown consumption per case, especially where quick room turnover and standardized protection protocols are essential. North America continues to lead the hospital gowns market, while Asia-Pacific is set to expand the fastest as hospital capacity, procedural demand, and infection prevention investment rise across large healthcare systems. Europe is becoming a distinct procurement arena in the hospital gowns market because sustainability targets are pushing more health systems to evaluate reusable operating room textiles and closed loop service models. Competition in the hospital gowns market remains moderately fragmented, but raw material concentration in polypropylene based nonwovens and tighter enforcement of barrier performance claims are increasing execution risk for suppliers that compete on both price and compliance.

Key Report Takeaways

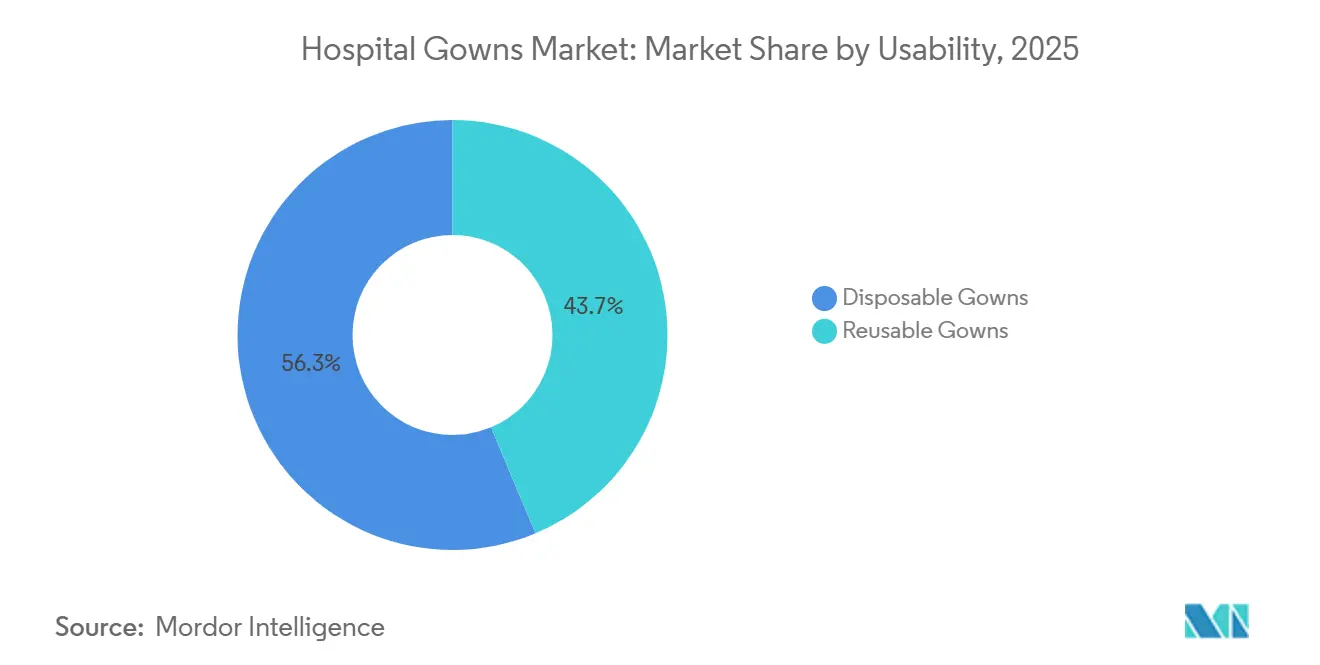

- By usability, Disposable Gowns commanded 56.31% of hospital gowns market share in 2025, while Reusable Gowns are projected to expand at a 10.38% CAGR through 2031.

- By type, Surgical Gowns accounted for 45.24% share of the hospital gowns market size in 2025, while Patient Gowns are forecast to grow at a 10.52% CAGR through 2031.

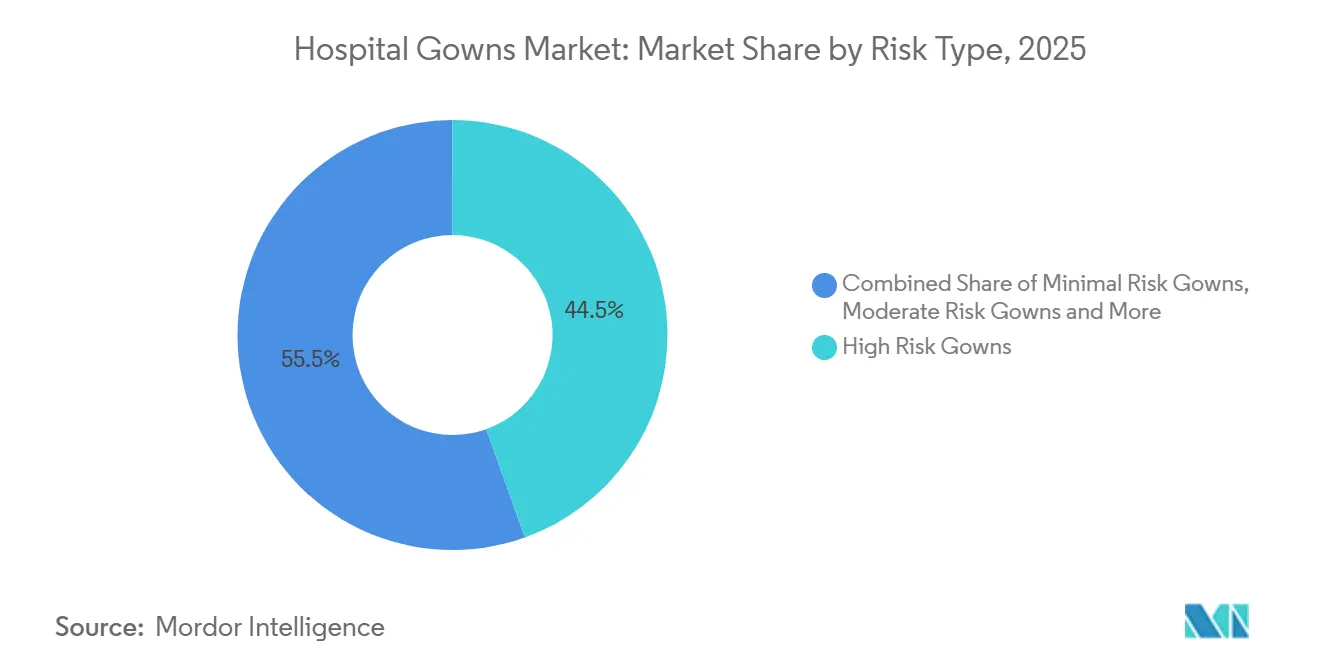

- By risk classification, High Risk Gowns held 44.52% revenue share in 2025, while Minimal Risk Gowns are expected to advance at an 11.25% CAGR through 2031.

- By end user, Hospitals and Clinics represented 56.24% share in 2025, while Ambulatory Surgical Centers are expected to record a 9.52% CAGR through 2031.

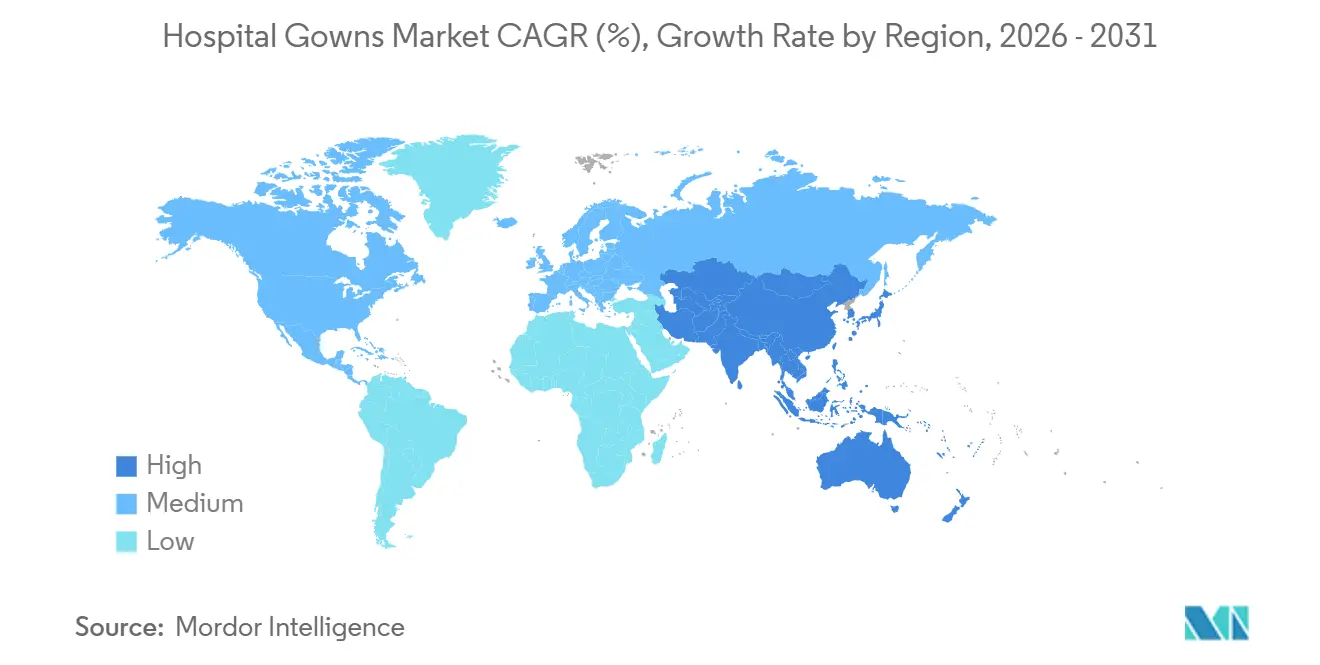

- By geography, North America held 38.52% share of the hospital gowns market size in 2025, while Asia-Pacific is projected to expand at a 9.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hospital Gowns Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infection Control Mandates and HAI Prevention | +1.8% | Global, highest in APAC, MEA, and LMICs with elevated HAI burdens | Short term (≤ 2 years) |

| Surgical Volume Growth and Procedural Throughput Requirements | +1.5% | Global, with North America and APAC leading recovery | Short term (≤ 2 years), Medium term (2-4 years) |

| Rising Preference for Disposable Gowns in High-Turnover Care Settings | +1.2% | North America, APAC emerging markets, Middle East | Short term (≤ 2 years) |

| Sustainability-Led Reusable Gown Procurement in Mature Health Systems | +0.9% | Europe, Canada, and the United States | Medium term (2-4 years) |

| Reusable Gown Laundering Validation and Closed-Loop Service Models | +0.6% | Western Europe, ANZ, and select North America IDNs | Medium term (2-4 years), Long term (≥ 4 years) |

| Gown Performance Verification, Traceability, and Procurement Digitization | +0.5% | North America, Northern Europe, with spillover to GCC and APAC core markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infection Control Mandates And HAI Prevention

Healthcare associated infections continue to create a firm demand floor for the hospital gowns market because prevention protocols require regular gown use in acute care, long term care, and other patient contact settings. WHO reported that healthcare associated infections add 25 million extra hospital days each year in Europe and impose EUR 13-24 billion (USD 15.1 to 27.9 billion) in annual costs, which keeps infection prevention spending difficult to defer. OECD also found that infection prevention and control measures, including appropriate gown use, can reduce infections by up to 70% and return USD 24.6 for every USD 1 invested across OECD and EU and EEA countries[1]Organisation for Economic Co-operation and Development, “Health at a Glance, Europe 2024,” OECD, oecd.org. The burden is even higher in lower income settings, where WHO noted much greater infection incidence, and that pushes large public systems to formalize procurement of protective apparel rather than treat it as a variable line item. In the United States, CDC guidance on Enhanced Barrier Precautions is extending routine gown use into nursing home activities that involve close contact, which broadens the addressable base for the hospital gowns market beyond hospitals alone.

Surgical Volume Growth And Procedural Throughput Requirements

Procedure growth continues to support the hospital gowns market because surgical case recovery has moved beyond backlog clearing and into a broader expansion of outpatient and minimally invasive care pathways. The Lancet projected global surgical volumes at no less than 160 million operations annually, which implies durable consumption of surgical gowns across hospital and ambulatory settings. CMS added 289 procedures to the ASC Covered Procedures List for 2026, which keeps moving more cases into ambulatory settings where throughput matters and disposable configurations remain common. That site of care shift matters because high acuity procedures done in ASCs often use tightly standardized packs and lean room turnover protocols, which increases the operational value of dependable gown supply. As a result, procedure growth is not only lifting unit demand in the hospital gowns market, it is also changing the mix toward products that can support faster turnover, predictable compliance, and easier inventory control.

Rising Preference For Disposable Gowns In High-Turnover Care Settings

Disposable gowns continue to hold a large position in the hospital gowns market because emergency departments, ASCs, and procedural suites value products that remove the need for collection, washing, validation, and redistribution. The preference is strongest where room turnover is fast and where staff want each case to begin with a fresh item that is already qualified for its barrier level. The migration of orthopaedic, cardiovascular, and spine procedures into ambulatory settings strengthens this pattern because those centers often prioritize standardization and speed over textile reprocessing logistics. Regulatory structure also supports this segment because the FDA requires 510(k) clearance for medical gowns that make moderate or high fluid barrier claims, including AAMI Level 4, which raises the value of compliant disposable product lines. This leaves the hospital gowns market in a position where disposables remain the practical choice in high velocity settings, even while reusables gain traction in selected operating room programs.

Sustainability-Led Reusable Gown Procurement In Mature Health Systems

Sustainability goals are creating a second major demand path in the hospital gowns market, especially in mature health systems that now link procurement decisions to waste reduction and emissions targets. Health Innovation North West Coast reported that reusable gown systems can reduce solid waste by up to 93% and greenhouse gas emissions by 66% compared with single use alternatives, which has made the environmental case much easier for procurement teams to defend. In February 2025, Barts Health NHS Trust awarded a 3 year contract covering reusable theatre gowns across 6 sites, with expected annual volume of 400,000 gowns and a projected reduction of 90 tonnes of clinical waste[2]Government Commercial Authority, “Greener Gowns for Barts Health NHS Trust Surgical Staff,” Government Commercial Authority, gca.gov.uk. Policy support is also becoming more visible, with Italy prioritizing reusable operating room textiles and other European systems evaluating how to move from simple product purchasing to service based textile models. This means the hospital gowns market is no longer shaped only by infection control rules, because environmental performance now influences contract design, vendor selection, and long term replacement cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium Product Cost Pressure in Budget-Constrained Facilities | -0.8% | Global, with highest impact in LMIC public hospitals, South America, and MEA | Short term (≤ 2 years), Medium term (2-4 years) |

| Regulatory and Barrier-Performance Compliance Complexity | -0.6% | North America and Europe, with heavier burden on emerging market manufacturers | Medium term (2-4 years) |

| Supply Chain Dependence on Nonwoven and Meltblown Inputs | -0.5% | Global, with APAC manufacturers most exposed to polypropylene price volatility | Short term (≤ 2 years) |

| Operational Readiness Gaps for Reusable Gown Adoption | -0.4% | LMIC hospital systems and mid tier acute care facilities lacking validated laundry capacity | Medium term (2-4 years), Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Product Cost Pressure In Budget-Constrained Facilities

Cost pressure remains a real brake on the hospital gowns market because higher barrier garments raise procurement costs for facilities that already face tight operating budgets. The 2025 international study covering 5,230 perioperative professionals across 134 countries found that financial constraints were the most frequently cited barrier to improving gown quality, identified by 19.9% of respondents. The same study showed that infrastructure limits and cost pressures often appear together, which means facilities do not move through adoption stages in a simple sequence. Smaller ASCs, long term care centers, and public hospitals also lack the purchasing leverage available to large integrated networks, so per unit costs can stay structurally higher for them. This keeps part of the hospital gowns market anchored to basic product tiers, even where clinical teams would prefer better comfort, breathability, or barrier performance.

Regulatory And Barrier-Performance Compliance Complexity

Compliance complexity slows parts of the hospital gowns market because suppliers often need to manage overlapping requirements across AAMI, European, and evolving international standards. The FDA framework adds further burden because gowns with moderate or high fluid barrier claims require premarket review, and even a product line change can trigger added testing and submission work. The PMC study on disposable isolation gowns also showed that claimed classifications do not always match real performance, which increases pressure on regulators and hospitals to verify data more closely. The Kimberly-Clark case raised the stakes by showing how compliance failures can become legal action when barrier claims are not backed by consistent testing controls. Larger incumbents can usually absorb these burdens more effectively than newer entrants, so the hospital gowns market still carries a meaningful scale advantage for established suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Usability: Disposable Volume Persists as Reusable Models Scale

Disposable Gowns held 56.31% of the hospital gowns market share in 2025, which reflected their deep use in acute care hospitals, ASCs, and emergency settings where single patient use remains central to workflow discipline. Their position in the hospital gowns market is supported by fast turnover, simple logistics, and a lower need for internal textile management. Facilities that face unpredictable caseloads or limited reprocessing infrastructure still rely on disposables because they remove the risk of laundry bottlenecks and reduce coordination across departments. This makes disposable volume resilient even as the broader hospital gowns market shifts toward more selective product and service combinations.

Reusable Gowns are forecast to grow at a 10.38% CAGR during 2026-2031, making them the faster moving usability segment as sustainability goals and life cycle cost reviews gain more weight in procurement. The 2025 global perioperative study found that sterilization related limits remain a core barrier, so reusable adoption depends less on clinical acceptance and more on service readiness. In practice, the hospital gowns industry is moving toward coexistence rather than replacement, with reusable programs strongest in planned surgical environments and disposable demand staying firm in emergency, trauma, and outpatient channels. Hybrid procurement models fit this reality well because they let systems use reusable textiles for scheduled operating room volume and keep disposable stock for surge periods and high turnover care. Suppliers that can serve both models should be better placed in the hospital gowns market because buyers increasingly want flexibility instead of a single format commitment.

By Type: Surgical Gowns Lead as Patient Gowns Gain from Ambulatory Expansion

Surgical Gowns accounted for 45.24% share of the hospital gowns market size in 2025, which reflected their mandatory role in operative care and their higher average value under stricter barrier requirements. Their lead in the hospital gowns market is tied to every procedure that demands controlled sterile conditions, including cardiothoracic, orthopedic, laparoscopic, and other fluid exposure settings. Non surgical gowns remain an important institutional category because they support isolation, contact precautions, chemotherapy handling, and other procedural needs shaped by infection control guidance. This keeps type level demand broad based, with surgical, non surgical, and patient use categories responding to different care pathways rather than one common demand pattern.

Patient Gowns are projected to grow at a 10.52% CAGR during 2026-2031, which is a faster pace than the overall hospital gowns market because outpatient care and home based services are expanding. More ambulatory centers and independent clinics are now buying directly instead of drawing from hospital led channels, which is widening the purchasing base for this category. Design upgrades are also giving patient gowns more strategic value, especially where comfort, dignity, and better handling support patient experience goals. In procedural settings, some patient facing garments are also moving closer to standardized fluid protection expectations when exposure risk is present. The result is that patient gowns no longer sit only at the low end of the hospital gowns market, because service model changes are making them a more active source of recurring volume.

By Risk Type: High-Risk Segment Anchors Revenue as Minimal-Risk Category Grows

High Risk Gowns represented 44.52% of hospital gowns market size in 2025, and that value lead came from mandatory use in surgical settings where strong fluid and pathogen resistance are essential. Their pricing power in the hospital gowns market is reinforced by the FDA requirement that products making AAMI Level 4 claims go through 510(k) review, which narrows the pool of credible suppliers. Moderate Risk Gowns remain widely used in general surgery, infusion therapy, and high exposure diagnostics, while Low Risk Gowns continue to serve routine blood draw, IV, and minor procedure environments. This creates a wide demand ladder in the hospital gowns market, where revenue concentration sits higher in the risk spectrum even when unit volumes are spread across several levels.

Minimal Risk Gowns are forecast to grow at an 11.25% CAGR during 2026-2031, making them the fastest growing risk segment as long term care, home health, and ambulatory settings formalize apparel purchasing. CDC guidance on Enhanced Barrier Precautions is directly expanding gown use in nursing homes during high contact resident care activities, which increases demand in settings that often lacked formal gown budgets in the past. ANSI and AAMI PB70:2022 continues to provide the recognized performance framework across all 4 levels, which helps hospital systems align claims, purchasing specifications, and audit requirements. As lower acuity channels become more structured, the hospital gowns market is expanding from the bottom of the risk ladder as well as from the premium surgical tier. That broadens the supplier opportunity set, but it also makes clear product positioning and compliance language more important across the full portfolio.

By End User: Hospital Dominance Persists as ASCs Capture Share

Hospitals and Clinics generated 56.24% of revenue in 2025, which kept them as the core demand center of the hospital gowns market because they concentrate high acuity surgery, isolation demand, and broad procedural activity. Their buying patterns shape product mix across the hospital gowns market because they purchase across all risk levels and both disposable and reusable formats. Long term care facilities are becoming a more formal end user group as infection prevention protocols extend gown use beyond acute care and into resident contact workflows. Home healthcare remains a smaller channel, but it is beginning to generate more structured demand as skilled nursing, wound care, and therapy related visits expand outside hospital walls.

Ambulatory Surgical Centers are forecast to grow at a 9.52% CAGR during 2026-2031, making them the fastest expanding end user group in the hospital gowns market. CMS support for more ASC eligible procedures is a major reason, because it keeps directing cardiovascular, spine, vascular, and orthopedic cases into outpatient surgical settings. This channel leans heavily toward disposables because the care model values quick room turnover, standardized packs, and simpler inventory control over internal laundry operations. As a result, ASC growth does more than add volume, it also influences the future mix of the hospital gowns market toward products that fit speed, compliance, and workflow simplicity. Hospitals will still remain the anchor buyer group, but ASCs are taking a larger role in how suppliers think about design, packaging, and distribution strategy.

Geography Analysis

North America accounted for 38.52% of the hospital gowns market share in 2025, which made it the largest regional contributor on the back of a dense accredited provider base, clear AAMI alignment, and strong purchasing scale. The United States remains the central revenue engine in the hospital gowns market because its hospitals, ASCs, and group purchasing organizations favor suppliers with dependable logistics and strong compliance records. Canada adds a different layer, with centralized procurement and growing interest in reusable gown programs that fit broader health system sustainability goals. Mexico continues to develop as a growth market as public and private providers expand structured procurement for surgical and infection prevention products. Regulatory scrutiny also intensified after the August 2025 DOJ settlement involving adulterated MicroCool surgical gowns, which raised the importance of testing credibility and supplier documentation across North American sourcing decisions.

Europe remains a strategically distinct region in the hospital gowns market because sustainability targets are changing how buyers compare single use and reusable options. Western European systems are moving faster on reusable operating room textiles, and Barts Health NHS Trust provided a visible example in 2025 with a large reusable gown contract tied to waste reduction goals. The regional backdrop is still shaped by a high infection burden, with OECD reporting around 4.3 million healthcare associated infection episodes each year in EU acute care hospitals, which sustains the baseline need for gowns across member states. This leaves Europe with a dual demand structure in the hospital gowns market, where infection control keeps volumes steady while sustainability policy changes the preferred textile model.

Asia-Pacific is forecast to expand at a 9.55% CAGR during 2026-2031, making it the fastest growing regional block in the hospital gowns market. China held the largest regional share in 2025 as hospital expansion, procurement rationalization, and export capability strengthened the role of validated gown categories. India is also adding scale through government backed hospital expansion and a growing private system that demands higher performance products. The Middle East and Africa shows a split pattern, with GCC systems moving toward international standards and local production initiatives such as Mölnlycke's Saudi joint venture, while much of sub Saharan Africa remains limited by budget and infrastructure constraints[3]Mölnlycke Health Care, “Tamer Mölnlycke Care Celebrates a New Chapter in Healthcare in the Kingdom of Saudi Arabia,” Mölnlycke, molnlycke.com. South America is being supported by structured public and private procurement in Brazil and a gradual normalization of institutional purchasing in Argentina.

Competitive Landscape

The hospital gowns market is moderately fragmented, with Medline Industries, Cardinal Health, Mölnlycke Health Care, and other companies forming the visible top tier in premium acute care channels, while a long tail of regional suppliers remains active in lower-priced disposable categories. Medline strengthened its position in 2025 through prime vendor wins, including the Veterans Administration contract outcome and large provider agreements such as The Ohio State University Wexner Medical Center, which reinforce the value of scale, reliability, and distribution depth. Its network of 45 U.S. distribution centers and MedTrans fleet makes service reliability a competitive tool rather than just an operating feature. Cardinal Health is also working to deepen its presence in high acuity gowns through product differentiation and a broader compliant portfolio. That means the hospital gowns market is not only about price competition, because logistics, compliance depth, and account coverage are becoming equally important.

Mölnlycke is using manufacturing and regional expansion to improve supply resilience in the hospital gowns market, supported by its Malaysia production base and renewable electricity strategy. Its Tamer Mölnlycke Care joint venture began producing drapes and gowns in Saudi Arabia in 2025, which gives the company closer access to GCC and wider MENA demand. Ansell reshaped its protection portfolio through the USD 635.1 million acquisition of Kimberly-Clark's Personal Protective Equipment business and then expanded brand integration across North America, Europe, and Asia-Pacific during 2025. These moves show that adjacent protection players still see room to build share in the hospital gowns market by combining brand equity, channel access, and product range.

Lohmann and Rauscher is pursuing a nearshoring and capability strategy, highlighted by its 49% stake in Portugal's ADA Group in July 2025 to strengthen European supply resilience. The company's Sentinex Solo surgical gown also points to workflow focused innovation, because it addresses staffing efficiency in busy operating room environments. At the same time, newer Asian manufacturers are moving into premium tiers as they secure clearer regulatory standing and seek access to North American institutional channels. The next layer of competition in the hospital gowns market is likely to center on traceability, laundering validation, sustainability reporting, and inventory visibility, because large health systems increasingly want evidence based procurement rather than simple unit cost comparisons.

Hospital Gowns Industry Leaders

Medline Industries, LP

Cardinal Health, Inc.

Solventum Corporation

Standard Textile Co., Inc.

Mölnlycke Health Care AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Cardinal Health received FDA 510(k) clearance (K253243) for its Poly Reinforced Surgical Gown. This milestone expands the company’s product offerings in the high-acuity surgical segment and strengthens its role as a trusted supplier of AAMI-classified gowns in North America.

- December 2025: Medline strengthened its presence in the long-term care gown market by partnering with Signature HealthCARE through a Prime Vendor agreement. This collaboration connects Medline with a network of 67 facilities spread across five U.S. states.

Global Hospital Gowns Market Report Scope

As per the scope of the report, hospital gowns are garments worn by patients during medical examinations, procedures, or hospital stays. They are typically loose-fitting, lightweight, and designed for easy access to the body for medical assessment and treatment.

The hospital gowns market is segmented by usability into disposable gowns and reusable gowns. By type, the market is categorized into surgical gowns, non-surgical gowns, and patient gowns. Based on risk type, the segmentation includes minimal risk gowns, low risk gowns, moderate risk gowns, and high risk gowns. By end user, the market is divided into hospitals and clinics, long-term care facilities, ambulatory surgical centers, and home healthcare. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Disposable Gowns |

| Reusable Gowns |

| Surgical Gowns |

| Non-Surgical Gowns |

| Patient Gowns |

| Minimal Risk Gowns |

| Low Risk Gowns |

| Moderate Risk Gowns |

| High Risk Gowns |

| Hospitals and Clinics |

| Long-Term Care Facilities |

| Ambulatory Surgical Centers |

| Home Healthcare |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Usability | Disposable Gowns | |

| Reusable Gowns | ||

| By Type | Surgical Gowns | |

| Non-Surgical Gowns | ||

| Patient Gowns | ||

| By Risk Type | Minimal Risk Gowns | |

| Low Risk Gowns | ||

| Moderate Risk Gowns | ||

| High Risk Gowns | ||

| By End User | Hospitals and Clinics | |

| Long-Term Care Facilities | ||

| Ambulatory Surgical Centers | ||

| Home Healthcare | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected size of the hospital gowns space by 2031?

The hospital gowns market is projected to reach USD 5.89 billion by 2031 from USD 4.11 billion in 2026, with growth supported by infection prevention rules and higher procedure volumes.

What is driving demand for hospital gowns in 2026?

Demand is being supported by healthcare associated infection prevention, rising surgical throughput, and broader gown use in nursing homes and ambulatory settings.

Which region is leading revenue and which one is growing the fastest?

North America led with 38.52% share in 2025, while Asia-Pacific is forecast to grow the fastest at a 9.55% CAGR through 2031.

Are disposable or reusable gowns growing faster?

Disposable gowns remain the largest usability segment at 56.31% share in 2025, but reusable gowns are growing faster at a 10.38% CAGR through 2031 as health systems weigh sustainability and service based textile models.

Why are ambulatory surgical centers becoming more important?

Ambulatory Surgical Centers are projected to grow at a 9.52% CAGR through 2031 because CMS continues to widen the list of procedures eligible for outpatient settings, which lifts demand for fast turnover gown supply.

What are the main risks suppliers face in this category?

The main risks are raw material concentration in nonwoven inputs, cost pressure in budget constrained facilities, and tighter enforcement of barrier performance claims after the August 2025 DOJ action.

Page last updated on: