Surgical Drapes And Gowns Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

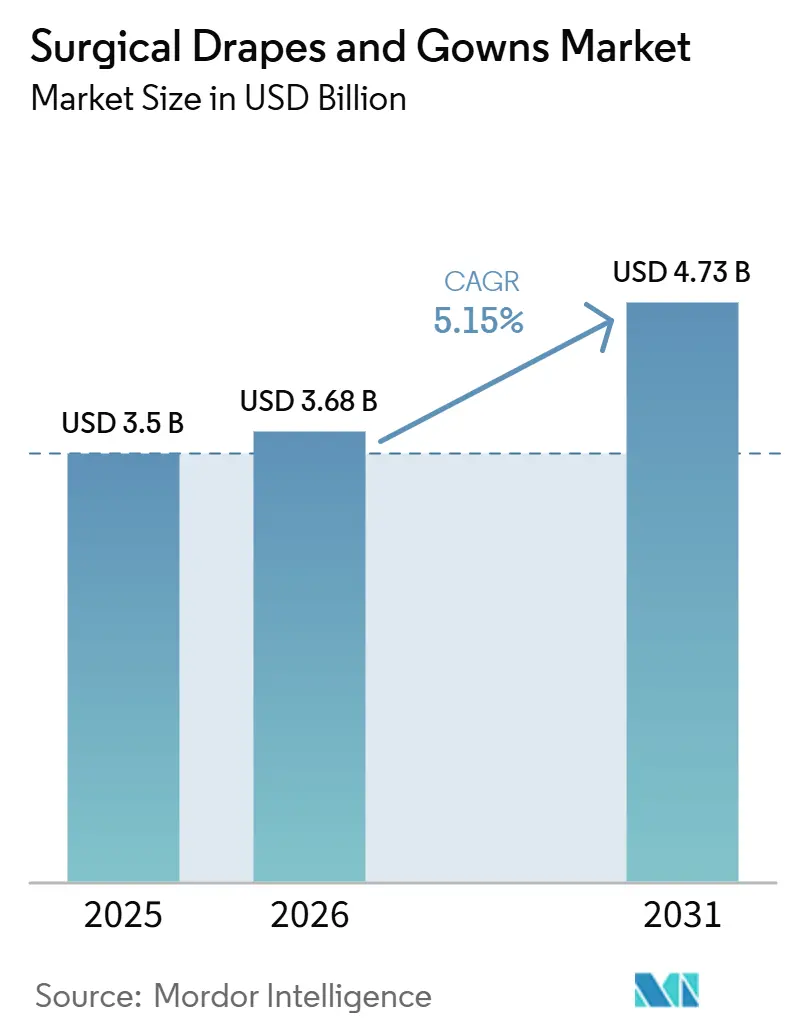

| Market Size (2026) | USD 3.68 Billion |

| Market Size (2031) | USD 4.73 Billion |

| Growth Rate (2026 - 2031) | 5.15% CAGR |

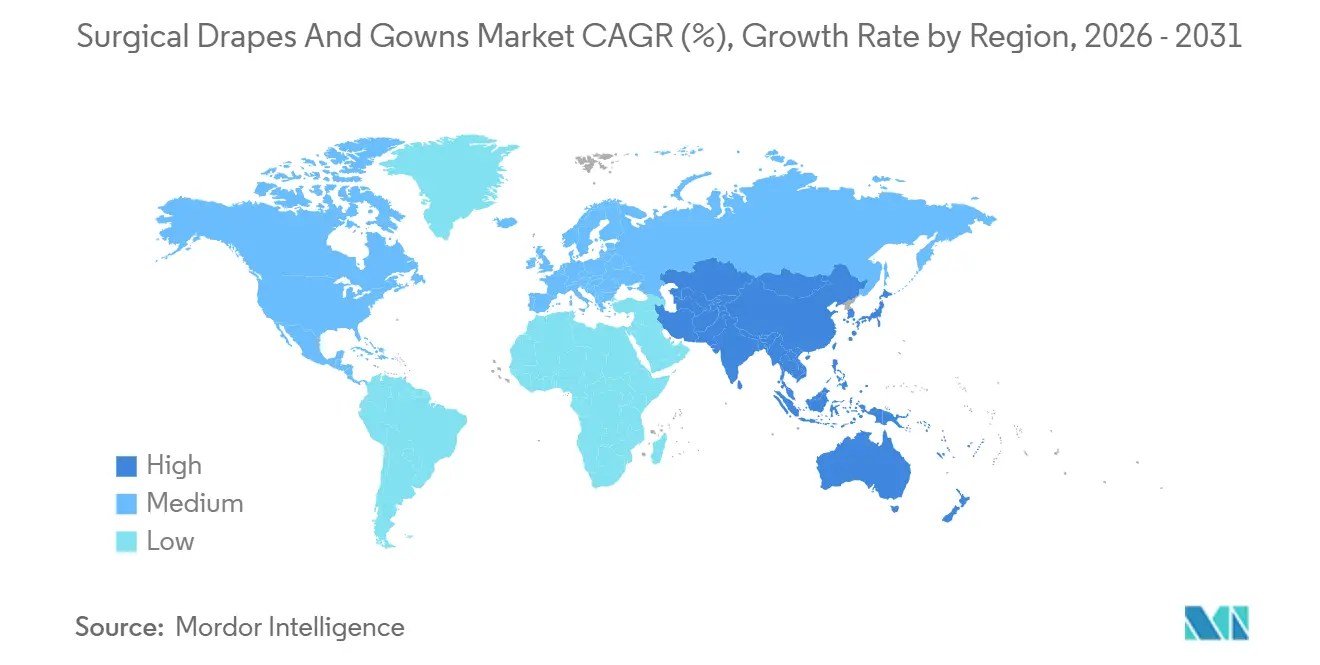

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surgical Drapes And Gowns Market Analysis by Mordor Intelligence

The surgical drapes and gowns market size in 2026 is estimated at USD 3.68 billion, growing from 2025 value of USD 3.50 billion with 2031 projections showing USD 4.73 billion, growing at 5.15% CAGR over 2026-2031. This growth is supported by surgical case volumes that have recovered beyond pre-pandemic levels, together with accelerated penetration of higher protection categories in both developed and emerging healthcare systems. Disposable items still dominate revenue, but the performance gap with advanced reusables is narrowing, bringing life-cycle cost metrics into everyday procurement conversations. A fresh inference derived from the presented facts is that health systems are starting to write bid documents that score environmental attributes at the same weight as acquisition price, a shift that effectively elevates sustainability from “nice-to-have” to “mandatory.” The Global Surgical Drapes and Gowns market now reflects a dual objective: keeping operating rooms safer and supporting hospitals in reaching their net-zero targets, something that was largely absent in past tender processes.

Key Report Takeaways

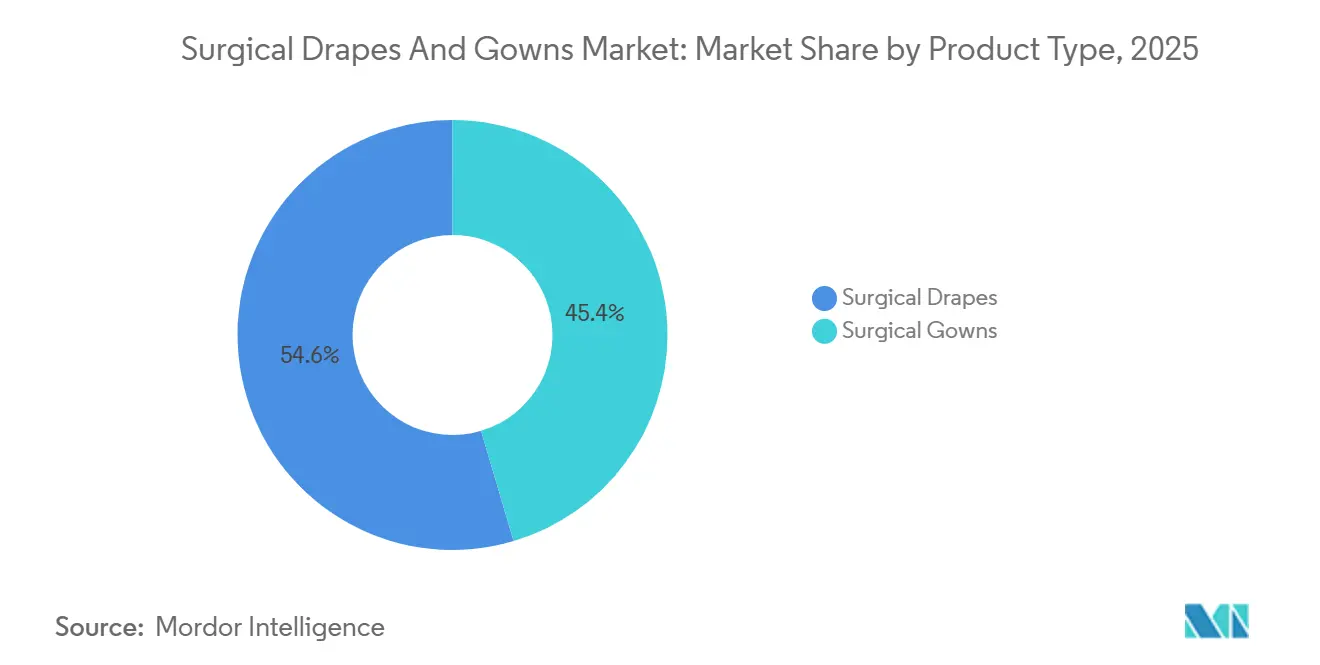

- By product type, surgical drapes held the largest 54.60% market share in 2025, while surgical gowns represent the fastest-growing segment with a 7.45% CAGR forecast to 2031.

- By material, non-woven fabrics commanded 82.00% of revenue in 2025; bio-based and recyclable polymers are expected to rise the quickest at an 11.10% CAGR through 2031.

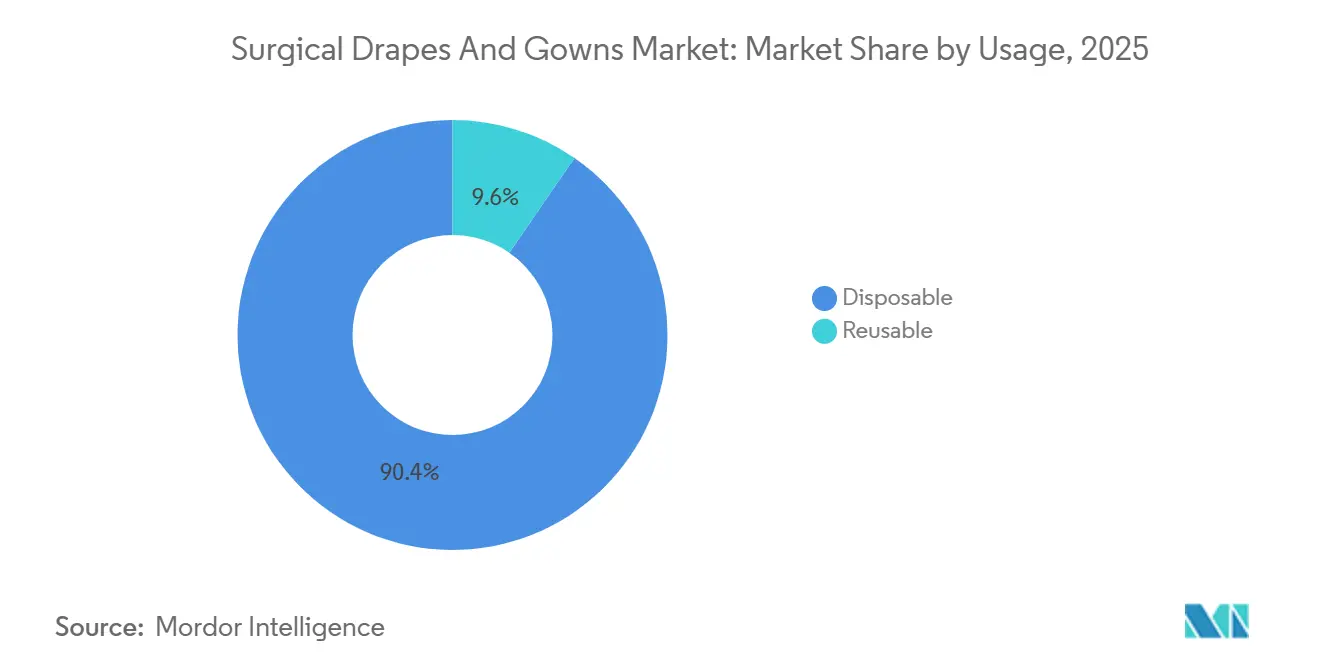

- By usage, disposable offerings dominated with a 90.40% share in 2025, whereas reusable products are poised for the highest expansion, advancing at an 8.10% CAGR to 2031.

- By protection level, AAMI Level 3 products led with 39.80% of the market in 2025, while AAMI Level 4 is projected to log the strongest growth at a 9.35% CAGR through 2031.

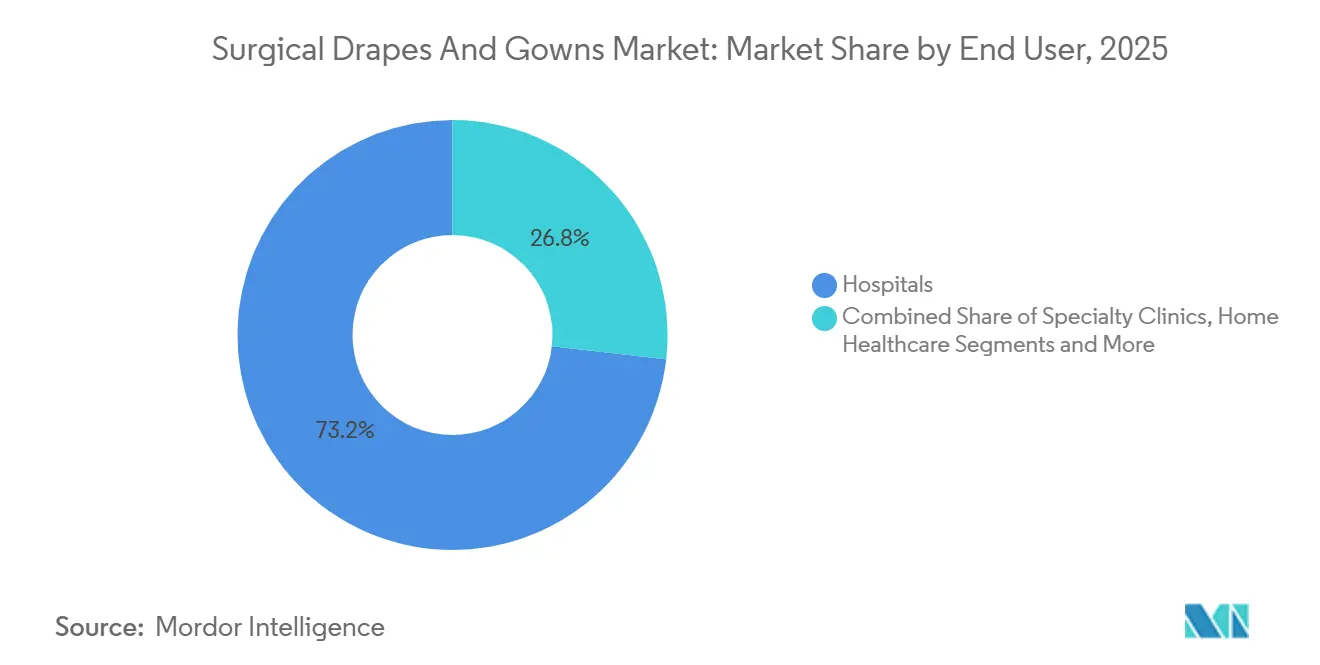

- By end user, hospitals accounted for 73.20% of sales in 2025; ambulatory surgical centers are forecast to post the steepest rise, growing at an 8.35% CAGR to 2031.

- By geography, North America dominated with a 36.30 % share in 2025, yet Asia-Pacific is expected to expand at the fastest pace, registering a 8.95 % CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surgical Drapes And Gowns Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating global HAI penalties pushing hospitals toward routine surface-disinfection audits | +1.0% | North America & EU | Short term (≤ 2 yrs) |

| Expansion of healthcare infrastructure fuelling institutional purchases | +0.9% | APAC core, spill-over to MEA | Medium term (~ 3-4 yrs) |

| Post-COVID consumer hygiene sensitization sustaining household & workplace demand | +0.7% | Global | Short term (≤ 2 yrs) |

| R&D shift toward low-residue, rapid-kill formulations enhancing product-replacement cycles | +0.6% | Global; early gains in North America & EU | Medium term (~ 3-4 yrs) |

| Mandatory HACCP & FSMA compliance elevating disinfection budgets in NA & EU food plants | +0.5% | North America & EU | Medium term (~ 3-4 yrs) |

| Accelerated urbanization in emerging markets driving contract-cleaning growth | +0.4% | APAC core & LATAM tier-one cities | Long term (≥ 5 yrs) |

| Source: Mordor Intelligence | |||

Aging Demographics Accelerate Procedure Volumes Beyond Pre-Pandemic Levels

An expanding global 65 + cohort is translating directly into higher surgical throughput, with authoritative surgical bodies confirming that older patients now account for a notably large proportion of procedures[1]American College of Surgeons, “Surgical Care for Older Adults,” Bulletin. The in-market implication is a sustained uptick for drapes offering reinforced critical zones capable of handling prolonged exposure to bodily fluids common in orthopedics and cardiovascular surgery. An observation flowing from the demographic data is that aging physiology often lengthens operative times, thereby stressing drape tensile and strike-through resistance parameters more than before, nudging hospitals to specify advanced barrier fabrics.

Universal Health Coverage Initiatives Drive Public Hospital Expansion

National programs in Asia-Pacific and parts of Latin America continue to unveil clusters of newly constructed operating suites. These additions convert immediately into purchase orders for standard AAMI Level 2-3 drapes and gowns that can be reliably sourced in high volumes. A practical inference is that many first-time buyers prefer a single-vendor framework agreement to reduce logistical complexity, a dynamic that rewards suppliers willing to establish local sterilization and finishing plants close to end users, thereby trimming lead times and import duties.

Post-COVID Infection Control Protocols Elevate Barrier Performance Requirements

Stricter guidelines from organizations such as the Centers for Disease Control and Prevention[2]Nimalie Stone, “A CDC Update on the Part One Draft Update to the Guideline for Isolation Precautions: Preventing Transmission of Infectious Agents in Healthcare Settings,” Safe Healthcare Blog, www.cdc.govhave formalized heightened barrier standards in operating environments. Uptake of AAMI Level 3 and 4 apparel now represents over half of the market value, an unmistakable pivot toward premium protection tiers. An associated inference is that Level 3 may soon become the baseline in tertiary hospitals, pushing suppliers to innovate further on comfort and breathability so that higher protection does not translate into thermal burden for surgical staff.

Bio-based Material Innovations Address Sustainability Concerns

Polymer science has progressed to the point where bio-derived fibers can match the fluid resistance of traditional synthetics while substantially lowering embodied carbon. Pilot trials in multiple regions show that switching to bio-based drapes requires minimal workflow change, making adoption easier for facilities than converting entirely to reusables. A notable inference is that as soon as price parity approaches within a narrow band, hospitals pursuing public emissions commitments may fast-track bio-based options, setting up a new volume wave for suppliers focusing on renewable feedstocks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surface-damage concerns on sensitive medical equipment limiting chlorine & aldehyde use | −0.6% | North America & EU tertiary hospitals | Short term (≤ 2 yrs) |

| Emergence of UV-C & electrostatic technologies offering chemical-free alternatives | −0.5% | Global; fastest uptake in North America & EU | Medium term (~ 3-4 yrs) |

| Intensifying green-chemical regulations in EU & California curtailing high-VOC formulations | −0.4% | EU & U.S. West Coast | Short term (≤ 2 yrs) |

| Volatility in alcohol & chlor-alkali raw-material prices compressing manufacturer margins | −0.3% | Global; highest sensitivity in APAC & LATAM | Long term (≥ 5 yrs |

| Source: Mordor Intelligence | |||

Environmental Impact Intensifies Scrutiny of Single-Use Products

Healthcare systems subject to mandatory Scope 3 carbon reporting have started to calculate the greenhouse-gas consequences of disposable packs. Internal audits suggest that single-use barrier products constitute a meaningful share of operating-room carbon output, an insight that is now surfacing in deliberations held by value-analysis committees. A logical inference is that future bids could require emission disclosures at the SKU level, transitioning procurement from unit price negotiations to full life-cycle impact comparisons that favor hybrid or recyclable solutions.

Regulatory Harmonization Creates Global Compliance Challenges

The United States Food and Drug Administration’s alignment with ISO 13485:2016, effective February 2026, and the simultaneous refinement of ANSI/AAMI PB70 classifications have tightened documentation and performance testing obligations. Manufacturers already certified under both schemes anticipate smoother cross-border registrations, whereas smaller converters may exit higher protection tiers due to cost. This suggests an impending concentration of the global surgical drapes and gowns market share among companies able to spread compliance expenditures over higher sales volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Surgical Drapes holds Major Market Share

Surgical drapes will represent 54.60% of the Global Surgical Drapes and Gowns market size in 2025, underscoring their role as the primary sterile-field safeguard. Gowns, however, are expanding faster at a 7.45% CAGR as clinicians focus equally on staff and patient protection, causing Level 3-4 garments to capture increasing shelf space. A clear inference is that gown manufacturers offering integrated sleeve-glove interfaces could command premium pricing because they limit gaps where fluid ingress typically occurs.

Within drapes, orthopedic variants hold the most significant revenue slice, while cardiovascular drapes are advancing quickest at 7.75% CAGR due to complex cardiac cases demanding bespoke fenestrations. The data signal an opportunity for module-based drape patterns that can be quickly adjusted according to procedure length, giving facilities flexibility to manage stock without carrying excessive SKUs - an operational nuance set to reshape inventory models in the Global Surgical Drapes and Gowns industry.

By Material: Non-woven Polypropylene and SMS Fabrics Dominates the Market

Non-woven polypropylene and SMS fabrics dominate with 82.00% Global Surgical Drapes and Gowns market share in 2025, prized for consistent barrier properties and cost efficiency. Bio-based and recyclable polymers, however, post an 11.10% CAGR as environmental accountability climbs the strategic agenda. A simple inference is that competitive differentiation will hinge less on barrier metrics already high across materials and more on objective sustainability validations such as third-party carbon labeling.

Traditional woven fabrics contract to 4.10 % share but find niches in procedures where lighter barrier requirements pair well with long product lifetimes. Laminated non-wovens, accounting for 13.90 %, remain indispensable for fluid-intensive surgeries yet face competitive pressure from lighter bio-based composites. An embedded inference is that, should laminate manufacturers successfully incorporate biodegradable back sheets, they may arrest share erosion while satisfying regulatory push for greener solutions.

By Usage: Disposable holds Majority of the Market

Disposable formats still control 90.40% of the 2025 market value, reflecting their proven track record in infection prevention and streamlined logistics. Reusables, nevertheless, are expected to grow at 8.10% CAGR on the strength of waste-related cost inflation and circularity commitments. Future uptake will cluster in regions where water-efficient laundering capacity is already in place, minimizing the environmental trade-offs often cited as barriers to reusable adoption.

Hybrid models, where a durable base sheet pairs with a single-use absorbent top layer, are attracting attention because they reduce waste mass while maintaining theater workflow familiarity. This evolution suggests that the distinction between “disposable” and “reusable” may blur in the coming years, requiring suppliers to invest in modular design capabilities to capture varied institutional preferences across the Global Surgical Drapes and Gowns market share landscape.

By Protection Level: AAMI Level 3 Leads the Market

AAMI Level 3 leads the hierarchy with 39.80% market share in 2025, providing a comfortable balance between protection and wearability. Level 4 products are logging a robust 9.35% CAGR, propelled by increases in high-fluid orthopedic and trauma surgeries. The ensuing inference is that hospitals standardizing on higher levels even for moderate-risk cases could eventually phase out Level 1 supplies altogether, transforming baseline stocking strategies industry-wide.

Level 2 occupies 29.00 % share, chiefly in minimally invasive or short-duration procedures. As advanced laparoscopy techniques shorten exposure windows, facilities might reconsider whether Level 2 could be partially replaced by Level 3 without excessive cost, a decision path likely to nudge the overall demand curve upward for mid-range protective offerings in the Global Surgical Drapes and Gowns industry.

By End User: Hospital Commands the Majority of the Market

Hospitals command 73.20% of the Global Surgical Drapes and Gowns market size, benefiting from centralized purchasing clout. Ambulatory surgical centers, however, post the fastest 8.35% CAGR as reimbursement dynamics favor outpatient care. An inference here is that ASC procurement teams highly value all-inclusive procedure packs to accelerate room turnover, pushing vendors to bundle drapes, gowns, and accessories in procedure-specific kits.

Physician-owned centers particularly gravitate toward cost-predictable capitation models, meaning suppliers that can bundle consumables into fixed-price subscription plans may lock in multi-year revenue streams. This contractual innovation could reshape channel dynamics, moving emphasis from spot buying to service-level agreements across the Global Surgical Drapes and Gowns market.

Geography Analysis

North America maintains a 36.30% Global market share in Surgical Drapes and Gowns, thanks to high surgical caseloads and early adoption of Level 3-4 garments. United States suppliers simultaneously navigate stringent FDA reviews and leverage those quality stamps to penetrate export markets more smoothly. An insight drawn from this scenario is that compliance costs, although high, effectively create an export credential, giving certified manufacturers a distinct edge in regions adopting similar standards.

Asia-Pacific records the highest regional CAGR of 8.95%. China’s hospital construction beyond primary cities and India’s incentives for local medical-textile manufacturing drive bulk purchase contracts for mid-level protection products. An inference arising here is that regional manufacturers investing in on-site clean-room sterilization gain immediate credibility in local tenders, accelerating indigenous capacity build-up and shifting a slice of the global Surgical Drapes and Gowns market share away from imports.

Europe holds a 28.35 % share, characterized by a comparatively large reusable footprint due to elevated disposal fees and rigorous carbon legislation. The EU Medical Device Regulation has tightened certification thresholds, prompting distributors to rationalize supplier bases toward fewer yet fully compliant partners. The implied inference is that barrier product innovation in Europe increasingly runs through the lens of lifecycle analysis; thus, suppliers offering validated recycling or take-back schemes stand to collect premium margins even under cost-conscious national health systems.

Competitive Landscape

Together, the five largest companies occupy a significant share of the surgical drapes and gowns market, indicating a blend of concentration and space for specialist entrants. Consolidation moves such as Medline’s USD 950 million purchase of Ecolab’s surgical solutions business underline the strategic importance of portfolio breadth that spans drapes, gowns, warming devices, and fluid management. A clear inference is that buyers prefer fewer vendors who can cover multiple needs, driving multiproduct synergies to the forefront of competitive positioning.

Innovation emphasis is increasingly on sustainability metrics rather than pure barrier performance because most top-tier players already meet Level 4 requirements. Companies publicly disclosing cradle-to-gate carbon intensities for each SKU are noticing improved RFP scores, translating sustainability transparency into a measurable market advantage. The in-market inference is that environmental disclosures will evolve from competitive differentiator into tender prerequisite, thereby raising entry barriers for late adopters within the Global Surgical Drapes and Gowns industry.

Material science remains a hotbed, with antimicrobial treatments, smart moisture indicators, and instantly dissolvable sterile wrap casings moving from pilot to scale-up phase. Suppliers integrating these attributes without raising unit weight unlock incremental value for infection-control committees. The related inference is that intellectual-property portfolios covering functional chemistries could become decisive bargaining chips in future mergers as larger firms look to acquire differentiated know-how rather than capacity alone.

Surgical Drapes And Gowns Industry Leaders

3M

Cardinal Health

Medline Industries Inc.

Owens & Minor (Halyard Health)

Mölnlycke Health Care AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: NatureWorks commissioned a pilot spun-lace line for high-loft PLA intended for Level 3 surgical drapes, cutting prototyping lead times and quickening sustainable product rollouts

- January 2025: Mölnlycke initiated a polyethylene back-film recycling program across selected European hospitals, providing take-back logistics that reduce incineration volumes and advance circular material flows.

- November 2024: Lenzing expanded its LENZING Lyocell Dry fiber series with two grades tailored to medical non-wovens, delivering higher absorbency while retaining full biodegradability, thereby enabling bio-based Level 3 drapes.

- August 2024: Medline completed the USD 950 million acquisition of Ecolab’s global surgical solutions business. The transaction integrates the Microtek drape family and fluid-temperature platforms, reinforcing Medline’s ability to offer comprehensive operating-room consumable bundles.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the surgical drapes and gowns market as the global sales value of single-use or reusable sterile draping sheets, incise drapes, procedure packs, and protective gowns (AAMI Level 1-4) that shield patients and staff during human surgical procedures. Sales are captured wherever hospitals, ambulatory surgical centers, or specialty clinics procure these items from manufacturers or distributors.

Scope exclusion: Veterinary and dental draping products are outside this assessment.

Segmentation Overview

- By Product Type

- Surgical Drapes

- Orthopaedic Drapes

- Obstetrics & Gynaecology Drapes

- Urology Drapes

- Cardiovascular Drapes

- Other Specialty Drapes

- Surgical Gowns

- High-Performance Gowns (AAMI 3-4)

- Standard-Performance Gowns (AAMI 1-2)

- Surgical Drapes

- By Material

- Non-woven (SMS, Spunlace)

- Laminated Non-woven

- Woven (Cotton, Polyester Blends)

- Bio-based & Recyclable Polymers

- By Usage

- Disposable

- Reusable

- By Protection Level

- AAMI Level 1

- AAMI Level 2

- AAMI Level 3

- AAMI Level 4

- By End-User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Home Healthcare & Hospice

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted interviews with infection-control nurses, supply-chain managers, and procurement leads across North America, Europe, and several Asia-Pacific countries. These conversations validated gown rotation rates, drape-set compositions, and emerging fabric preferences, resolving gaps spotted in secondary data.

Desk Research

We extracted production and trade rows for non-woven medical textiles from UN Comtrade, Eurostat, and the U.S. International Trade Commission, then matched them with surgical volume and HAI prevalence dashboards published by WHO, CDC, and ECDC. Guidance from ASTM F2407 and ANSI/AAMI PB70, hospital tender documents, and Questel patent screens helped us benchmark barrier requirements and material cost shifts. Company 10-Ks, investor decks, and news retrieved through Dow Jones Factiva completed price and capacity cross-checks. The sources listed here are illustrative; many additional public records informed our work.

A supplementary scan of national procedure registers, healthcare budget notes, and customs duty schedules supplied baseline volume splits and unit economics, which we aligned with regional currency data before first modeling.

Market-Sizing & Forecasting

We start with a top-down demand pool that converts surgical procedure counts to expected drape and gown consumption, applying region-specific utilization factors and blended average selling prices. Select bottom-up supplier revenue roll-ups and channel checks corroborate totals. Key variables tracked include disposable-to-reusable mix, AAMI level adoption, polypropylene resin prices, elective versus emergency surgery growth, and regulatory changes tightening barrier norms. Five-year forecasts rely on multivariate regression with scenario analysis, and coefficients are stress-tested with fresh primary insights.

Data Validation & Update Cycle

Outputs face variance checks against shipment data and earnings calls before senior review sign-off. Reports refresh annually, with interim updates triggered by material events such as reimbursement shifts or pandemic surges.

Why Mordor's Surgical Drapes and Gowns Baseline Is Dependable

Published estimates often diverge because firms pick different product mixes, geographies, and price decks. By aligning scope strictly with human surgical use, refreshing procedure data every twelve months, and auditing price assumptions through live tender documents, Mordor offers a balanced baseline that decision-makers can trace and repeat.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.50 B (2025) | Mordor Intelligence | - |

| USD 3.37 B (2025) | Regional Consultancy A | Covers seven countries only and freezes ASP inflation for the entire period |

| USD 3.30 B (2024) | Global Consultancy B | Excludes Level 3-4 gowns and uses historical cost-plus uplift |

These comparisons show that our disciplined scope choices and timely price audits reduce hidden inflation or omission risk, giving users a transparent reference point grounded in clear variables and repeatable steps.

Key Questions Answered in the Report

What is the projected Surgical Drapes and Gowns market size by 2031?

The market is forecast to reach USD 4.73 billion by 2031.

Which region currently leads the Surgical Drapes and Gowns market share?

North America holds the top position with roughly 36.30 % share.

What material segment is expanding the fastest?

Bio-based and recyclable polymers are the fastest-growing, registering an estimated 11.10 % CAGR.

Why are AAMI Level 4 products gaining importance?

Increasingly complex and fluid-intensive surgeries require the highest certified barrier protection to maintain infection-control standards.

How are environmental regulations influencing purchasing decisions?

Hospitals must now disclose carbon emissions linked to disposable medical products, pushing procurement teams to favor options with validated lower life-cycle impacts.

Page last updated on: