Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

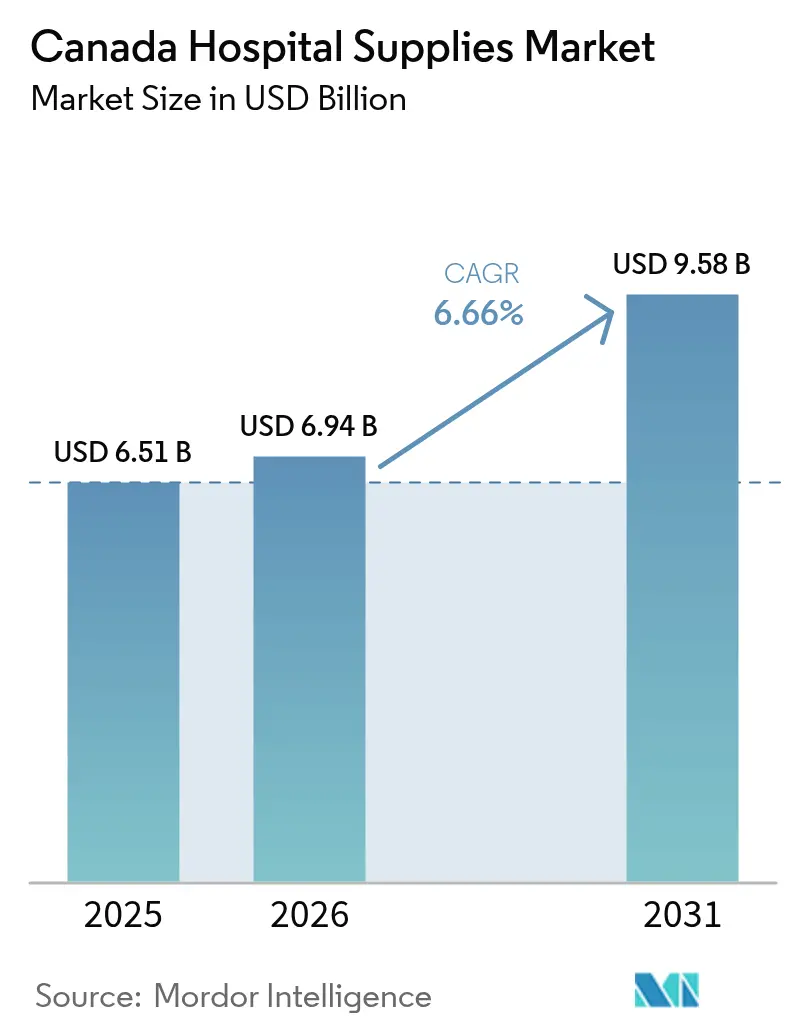

| Base Year Market Size (2025) | USD 6.51 Billion |

| Market Size (2026) | USD 6.94 Billion |

| Market Size (2031) | USD 9.58 Billion |

| Growth Rate (2026 - 2031) | 6.66% CAGR |

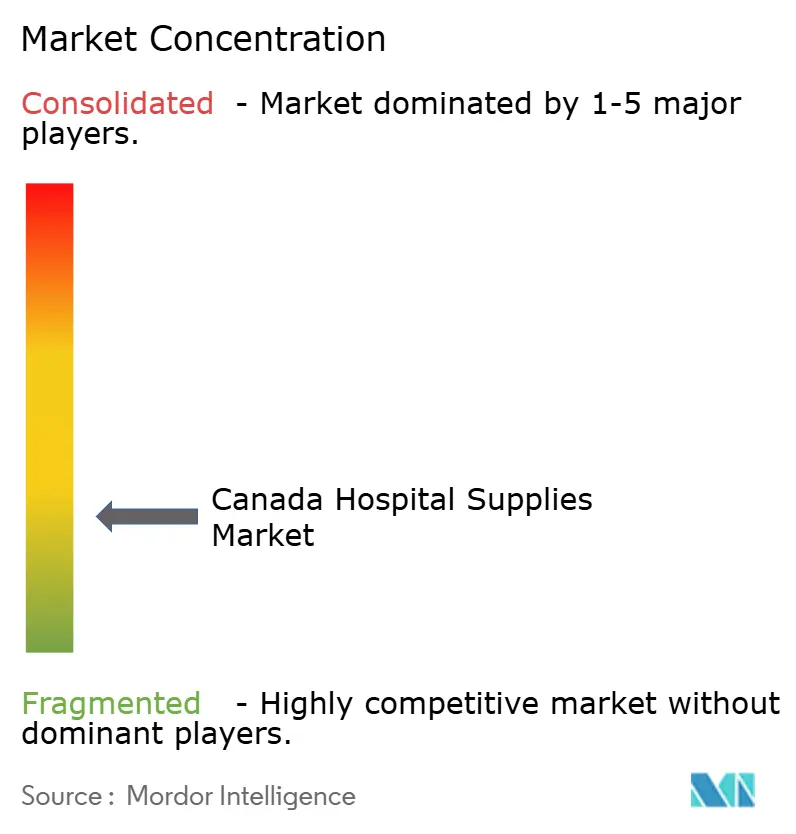

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Hospital Supplies Market Analysis by Mordor Intelligence

The Canada Hospital Supplies market size is expected to grow from USD 6.51 billion in 2025 to USD 6.94 billion in 2026 and is forecast to reach USD 9.58 billion by 2031 at 6.66% CAGR over 2026-2031.

The market size expansion is outpacing overall healthcare spending growth and is underpinned by strong government capital programs, rapid technological adoption, and rising surgical volumes. Provincial infrastructure projects worth more than CAD 80 (USD 58.3) billion are unlocking procurement opportunities, while demographic aging is reshaping product demand toward mobility aids, chronic-care disposables, and advanced patient monitoring. Technological breakthroughs—from low-temperature sterilization to connected operating-room equipment—are widening product ranges and lifting average selling prices. Meanwhile, multinational suppliers are deepening local partnerships to secure long-term contracts as hospitals sharpen sustainability goals and compliance requirements.

Key Report Takeaways

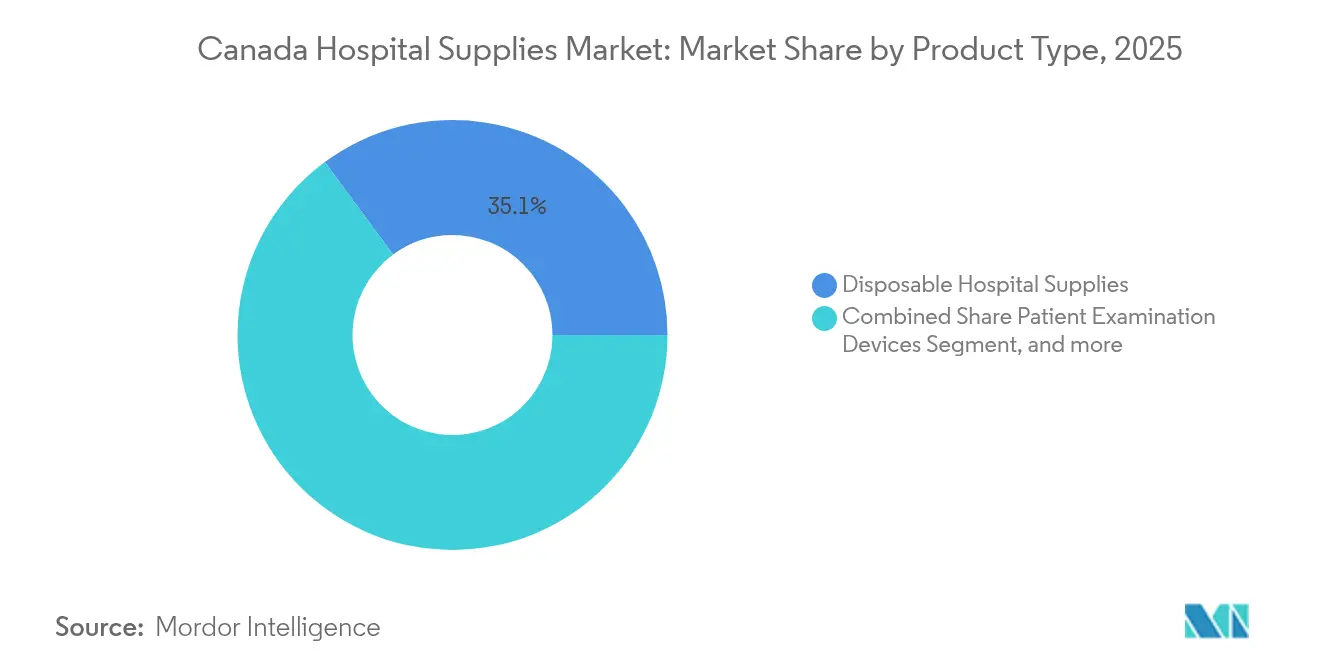

- By product type, disposable supplies led with 35.12% revenue share in 2025; sterilization equipment is projected to advance at an 8.5% CAGR through 2031.

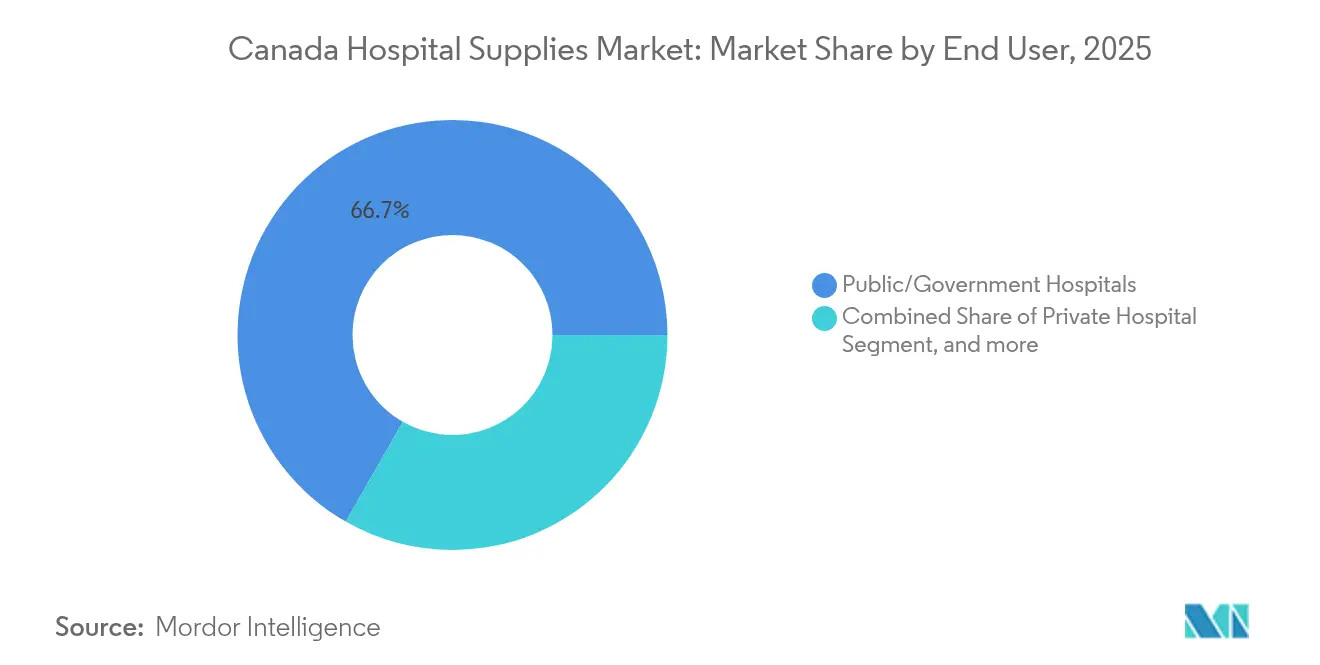

- By end user, public hospitals commanded 66.73% of the Canada hospital supplies market share in 2025, while specialty and ambulatory surgical centers are forecast to grow at 7.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Hospital Supplies Market Trends and Insights

Drivers Impact Analysis*

| Market Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of hospital infrastructure pipeline | +1.8% | Ontario, Quebec, British Columbia, Saskatchewan | Medium term (2–4 years) |

| Increase in geriatric population and in-patient admissions | +1.5% | National urban centers | Long term (≥ 4 years) |

| Technological advancements in hospital supplies | +2.0% | National, early adoption in major urban hospitals | Medium term (2–4 years) |

| Rising surgical volume in region | +1.5% | Provinces with surgical backlogs | Short term (≤ 2 years) |

| Government healthcare spending & universal coverage | +0.9% | National | Short term (≤2 years) |

| Focus on infection control & sustainability | +1.0% | National, strong in tertiary hospitals | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Hospital Infrastructure Pipeline

More than CAD 80 (USD 58.3) billion in provincial capital programs are either underway or approved, with Ontario allocating CAD 56 (USD 40.8) billion for new hospitals and 3,000 additional beds. British Columbia’s New St. Paul’s Hospital alone will add 548 beds by 2027. These builds lift baseline procurement for everything from surgical instruments to diagnostic imaging consoles as new departments come online. The project schedules are staggered, creating a rolling demand curve that suppliers can target for recurring contracts. Green-building mandates are also boosting sales of energy-efficient sterilizers and low-waste disposables as facilities pursue LEED standards and lower operating costs.[1]Ontario Ministry of Finance, “Building a Strong Ontario,” Ontario Budget 2025, ontario.ca

Increase in Geriatric Population and In-patient Admissions in Hospitals

Seniors will rise 68% between 2017 and 2037, increasing from 6.2 million to 10.4 million people. Older Canadians already drive disproportionate utilization: 482.63 hospital admissions per 1,000 assisted-living residents compared with far lower rates among younger adults. Hospitals are therefore buying more fall-prevention mobility aids, pressure-relief mattresses, and chronic-wound dressings. Integrated patient-monitoring systems with larger screen displays and remote-alert features are also gaining traction as clinicians manage complex multimorbid cases.[2]Statistics Canada, “Health Care Utilization of Older Canadians, 2019/2020,” statcan.gc.ca

Technological Advancements in Hospital Supplies

The Canada hospital supplies market is rapidly absorbing AI-ready imaging carts, connected infusion pumps, and low-temperature hydrogen-peroxide sterilizers. STERIS’s AMSCO 600 system occupies 40% less floor space and delivers up to five times the throughput of prior steam units, a major draw for urban hospitals facing space constraints. Toronto General’s adoption of the da Vinci robotic platform has expanded ancillary demand for 3D visualization drapes, articulating laparoscopic instruments, and single-port access kits. These premium categories carry unit prices 2-3 times higher than conventional equivalents, magnifying revenue growth.[3]STERIS Corporation, “AMSCO 600 Series Steam Sterilizer,” steris.com

Rising Surgical Volume in Region

Surgical throughput rebounded to 2.33 million procedures in 2023-2024, a 4.9% year-over-year jump as pandemic backlogs eased. Orthopedic interventions are forecast to climb 17.7% between 2020 and 2027, while ophthalmic cases may surge 27.7% in the same window. The volume resurgence is increasing consumption of single-use trocars, precision sutures, and antimicrobial drapes, and is accelerating turnover of high-wear items such as endoscopic blades and stapling cartridges.

Restraints Impact Analysis*

| Market Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Emergence of home care services | -0.8% | Urban areas with robust home-care networks | Medium term (2–4 years) |

| Stringent regulatory framework | -0.2% | National | Long term (≥ 4 years) |

| Price sensitivity & budget constraints | -0.5% | National, pronounced in smaller hospitals | Short term (≤ 2 years) |

| Supply chain vulnerabilities | -0.4% | National, heightened in remote regions | Short to medium term (≤ 3 years) |

| Source: Mordor Intelligence | |||

Emergence of Home Care Services

The federal Aging with Dignity program is channeling CAD 5.4 (USD 3.9) billion into home-care capacity, giving chronic-disease patients viable alternatives to extended hospital stays. Remote patient monitoring kits, negative-pressure wound-therapy pumps, and portable oxygen concentrators are now stocked by home-health distributors. This shift siphons demand away from inpatient-only formats such as large-volume suction canisters and fixed-site telemetry stations. Suppliers that lack consumer-grade product lines risk losing share as purchasing decision-making decentralizes from hospital procurement offices to community agencies.

Stringent Regulatory Framework

Manufacturers must navigate Class I-IV clearances under Medical Devices Regulations (SOR/98-282) plus new recall-reporting rules effective January 2025. AI-enabled devices face additional ambiguity because Canada lacks an assessment framework comparable to the UK DTAC. Extended review cycles elevate working-capital requirements and can delay commercial launches by six to nine months. Smaller innovators may defer entry or partner with established license holders, slowing competitive churn and constraining supply diversity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Disposables Dominate as Sterilization Devices Accelerate

Disposable consumables delivered 35.12% of 2025 revenue, reflecting infection-control priorities that gained urgency during the pandemic. The Canada hospital supplies market size for disposables equaled USD 2.29 billion in 2025 and is tracking a 6.21% CAGR through 2031. Tightened provincial infection-control standards and the drive to cut reprocessing labor are steering buyers toward single-use procedure kits, cannulae, and barrier gowns. The federal award of CAD 42 (USD 30.6) million to build a new nitrile-glove plant in Ontario underscores policy support for domestic manufacturing capacity, which mitigates import-risk premiums during supply disruptions.

Sterilization and disinfectant equipment is the standout growth pocket, forecast to race ahead at 8.5% annually. Hospitals are retiring legacy steam units in favor of low-temperature plasma and vaporized-hydrogen-peroxide systems that safeguard heat-sensitive endoscopes and ophthalmic instruments. Capital budgets are also earmarked for autoclaves with IoT modules that integrate with electronic health records to automate cycle validation. As a result, the Canada hospital supplies market share for sterilization devices is expected to climb from 12.65% in 2025 to nearly 14.85% by 2031. Mid-tier product categories—patient-examination devices, operating-room tables, and mobility aids—continue respectable mid-single-digit growth, buoyed by rising outpatient volumes and geriatric demand.

By End User: Public Hospitals Lead, Specialty Centers Scale Fastest

Public institutions consumed 66.73% of sector revenue in 2025, translating into a Canada hospital supplies market size of USD 4.35 billion. Universal coverage and global budgets concentrate purchasing power within provincial supply-chain alliances, enabling bulk-buy contracts that prioritize quality certifications and vendor sustainability scores. High nursing overtime and agency staffing costs have nudged administrators to adopt single-patient-use items to reduce cross-contamination risk and shorten cleaning cycles.

Specialty and ambulatory surgical centers, though representing under 10% of 2025 outlays, are projected to post a 7.82% CAGR through 2031. Same-day orthopedic and ophthalmic centers contract directly with suppliers for bundled instrument packs and robotic-compatible disposables, often at higher margins than public tenders. Private hospitals remain a small but growing customer set with demand tied to employer-funded insurance for services outside the universal basket. Long-term-care and rehabilitation facilities secure stable procurement volumes in mobility and pressure-injury prevention products as the over-65 cohort expands.

Geography Analysis

Ontario anchors the Canada hospital supplies market with its dense population and a CAD 56 (USD 40.8) billion health-infrastructure pipeline. The Trillium Health Partners redevelopment alone will add 2,400 medical-surgical beds by 2029, lifting annual demand for monitors, IV sets, and wound-closure materials. Ontario’s integrated procurement network leans on multi-year vendor-of-record agreements, providing volume guarantees that attract global manufacturers.

British Columbia showcases the fastest CAGR, supported by USD 6.4 billion in new facilities slated for construction in 2025-2026. Projects such as the New St. Paul’s Hospital will feature smart-building HVAC systems that integrate sterile-processing and energy-management functions, driving procurement of sensor-embedded devices and eco-certified disposables.

The Prairie provinces collectively add momentum through rural-hospital upgrades. Atlantic Canada’s infrastructure surge highlighted by the USD 5.1 billion expansion of Halifax’s Queen Elizabeth II Health Sciences Centre broadens market coverage into historically underserved regions. Device requirements focus on tele-ICU carts and climate-resilient supply packaging suitable for coastal logistics.

Competitive Landscape

Global diversified players dominate the upper tier of the Canada hospital supplies market, with Johnson & Johnson, Medtronic, and Stryker leveraging broad catalogs to win system-wide contracts. Boston Scientific recorded 16.9% sales growth in Canada and Latin America in 2024, reflecting successful integration of its single-use endoscopy line and drug-eluting technologies into provincial formularies. Vertical integration insulates these suppliers from component shortages and gives hospitals confidence in lifecycle support.

Sustainability has emerged as a core differentiator. Zimmer Biomet, Boston Scientific, and Stryker have publicly committed to net-zero scopes 1 and 2 emissions by 2030, influencing purchasing committees that must meet provincial green-procurement mandates. Product take-back schemes for surgical-tool recycling are a notable competitive lever as hospitals pursue waste-diversion targets.

Strategic M&A remains active. DAS Health’s 2024 entry via acquisition of a Canadian health-IT integrator highlights cross-border interest in bundled device-and-software offerings. Supplier alliances with construction consortia on design-build projects, such as the Peter Gilgan Mississauga Hospital, further cement early equipment procurement commitments.

Canada Hospital Supplies Industry Leaders

Boston Scientific Corporation

McKesson Corporation

Baxter Canada

3M Canada

GE Healthcare Canada

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: An international consortium has been awarded a USD 5.1 billion contract to lead the expansion of the Queen Elizabeth II Health Sciences Centre in Halifax, Nova Scotia. This major infrastructure project marks one of the most significant hospital expansions in Canadian history and underscores the growing role of global partnerships in delivering complex healthcare infrastructure. The project will significantly enhance healthcare capacity in the Atlantic region, supporting advanced medical services and improved patient care for years to come.

- February 2025: British Columbia will see more than USD 6.4 billion in new hospital construction beginning in 2025, with additional projects extending into 2026. This initiative is part of the provincial NDP government’s commitment to enhance healthcare access and capacity by building or upgrading 30 hospital and health facility projects, 11 long-term care centres, and four cancer centres across five health regions. The large-scale effort aims to modernize the province’s healthcare system, reduce patient wait times, and prepare for future population growth and healthcare demands.

- July 2024: ED+PCL Healthcare Partners, a joint venture between EllisDon (Mississauga, ON) and PCL Construction (Edmonton, AB), has initiated site preparation for what is being billed as Canada’s largest hospital—the Peter Gilgan Mississauga Hospital in Ontario. This transformative project will include Ontario’s first dedicated women’s and children’s health center, significantly expanding specialized care capacity in the region. This development signals a substantial future demand for hospital infrastructure, medical equipment, and clinical supplies, and is expected to positively impact the Canadian hospital supplies market through increased procurement opportunities and long-term operational needs.

Canada Hospital Supplies Market Report Scope

As per the scope of the report, hospital supplies include every medical utility product that serves both the patient and medical professional with hospital infrastructure and enhances the network and transportation between hospitals. These include hospital equipment, patient aid, mobility equipment, and sterilization disposable hospital supplies. The Canada Hospital Supplies Market is segmented by Type of Product (Patient Examination Devices, Operating Room Equipment, Mobility Aids and Transportation Equipment, Sterilization and Disinfectant Equipment, Disposable Hospital Supplies, and Syringes and Needles). The report offers the value (in USD million) for the above segments.

By Product Type

| Patient Examination Devices |

| Operating Room Equipment |

| Mobility Aids & Transportation Equipment |

| Sterilization & Disinfectant Equipment |

| Disposable Hospital Supplies |

| Syringes & Needles |

| Other Product Types |

By End User

| Public/Government Hospitals |

| Private Hospitals |

| Specialty & Ambulatory Surgical Centers |

| Long-Term Care & Rehabilitation Hospitals |

| By Product Type | Patient Examination Devices |

| Operating Room Equipment | |

| Mobility Aids & Transportation Equipment | |

| Sterilization & Disinfectant Equipment | |

| Disposable Hospital Supplies | |

| Syringes & Needles | |

| Other Product Types | |

| By End User | Public/Government Hospitals |

| Private Hospitals | |

| Specialty & Ambulatory Surgical Centers | |

| Long-Term Care & Rehabilitation Hospitals |

Key Questions Answered in the Report

What is the current size of the Canada hospital supplies market?

The market is valued at USD 6.94 billion in 2026 and is projected to reach USD 9.58 billion by 2031.

Which product category is growing the fastest?

Sterilization and disinfectant equipment is forecast to grow at an 8.5% CAGR, outperforming all other categories.

Why do public hospitals dominate purchasing?

Canada’s universal coverage model channels 66.73% of spending through publicly funded hospitals, concentrating procurement power in provincial supply alliances.

How is demographic aging influencing demand?

A 68% rise in the senior population by 2037 is increasing purchases of mobility aids, wound-care dressings, and geriatric-focused monitoring systems.

What regulatory changes should suppliers monitor?

January 2025 amendments to the Medical Devices Regulations broaden recall definitions and add reporting duties, raising compliance complexity for manufacturers.

Page last updated on: