Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 159.44 Billion |

| Market Size (2031) | USD 193.94 Billion |

| Growth Rate (2026 - 2031) | 3.99% CAGR |

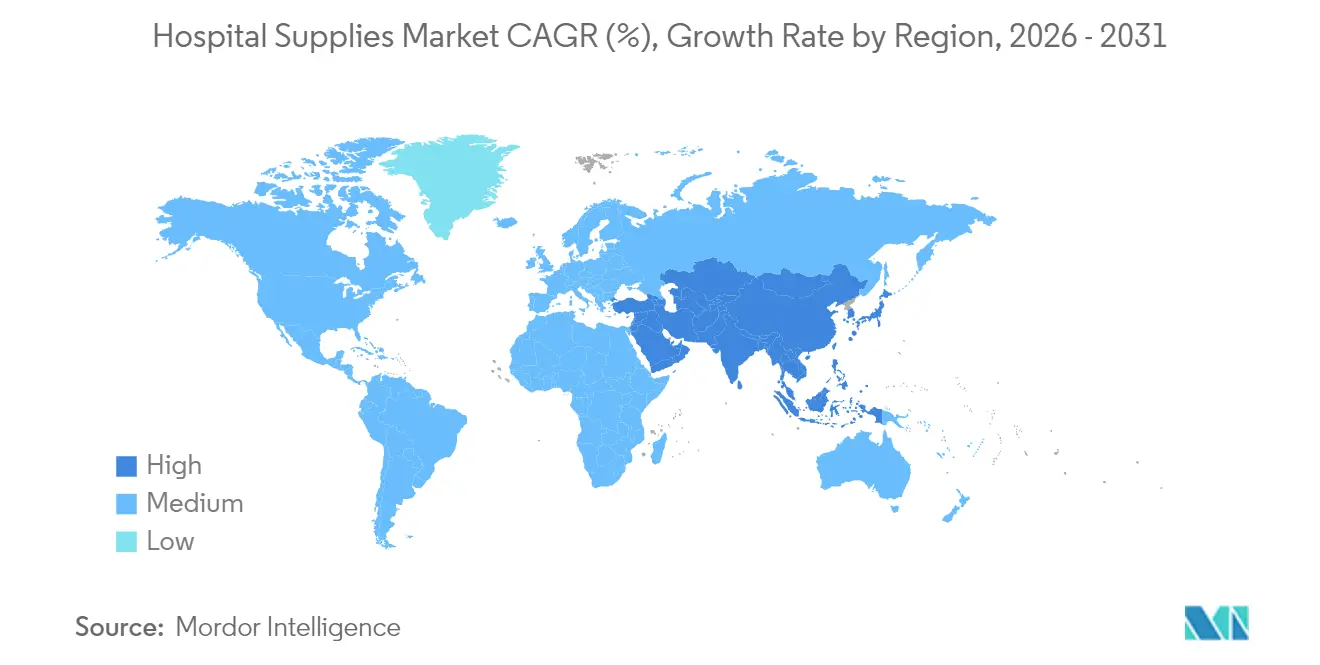

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

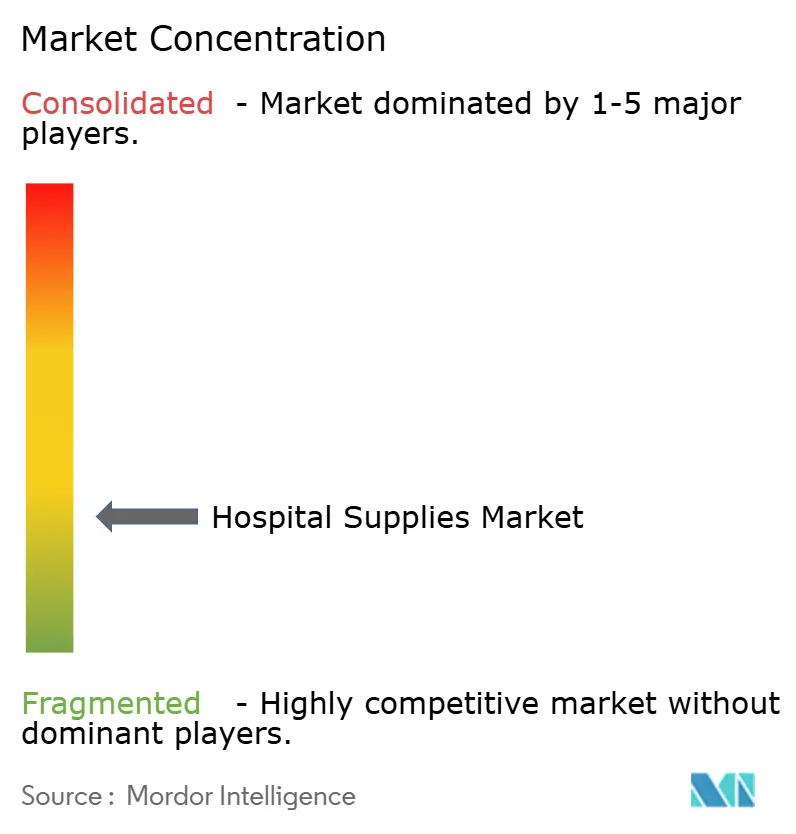

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hospital Supplies Market Analysis by Mordor Intelligence

The Hospital Supplies Market size is expected to grow from USD 153.33 billion in 2025 to USD 159.44 billion in 2026 and is forecast to reach USD 193.94 billion by 2031 at 3.99% CAGR over 2026-2031.

This trajectory is supported by infection-control investments, technology-enabled inventory systems, and accelerating demand from developing regions. Disposable products, sterile processing equipment, and digital supply-chain solutions remain central to procurement decisions, while sustainability mandates are beginning to influence product selection. Asia-Pacific’s rapid infrastructure build-out, coupled with post-pandemic surgery backlogs in developed nations, is reshaping global competitive dynamics. Suppliers that combine physical goods with analytics-driven efficiency tools are capturing share as hospitals seek to align clinical performance, cost control, and regulatory compliance within tighter budget cycles.

Key Report Takeaways

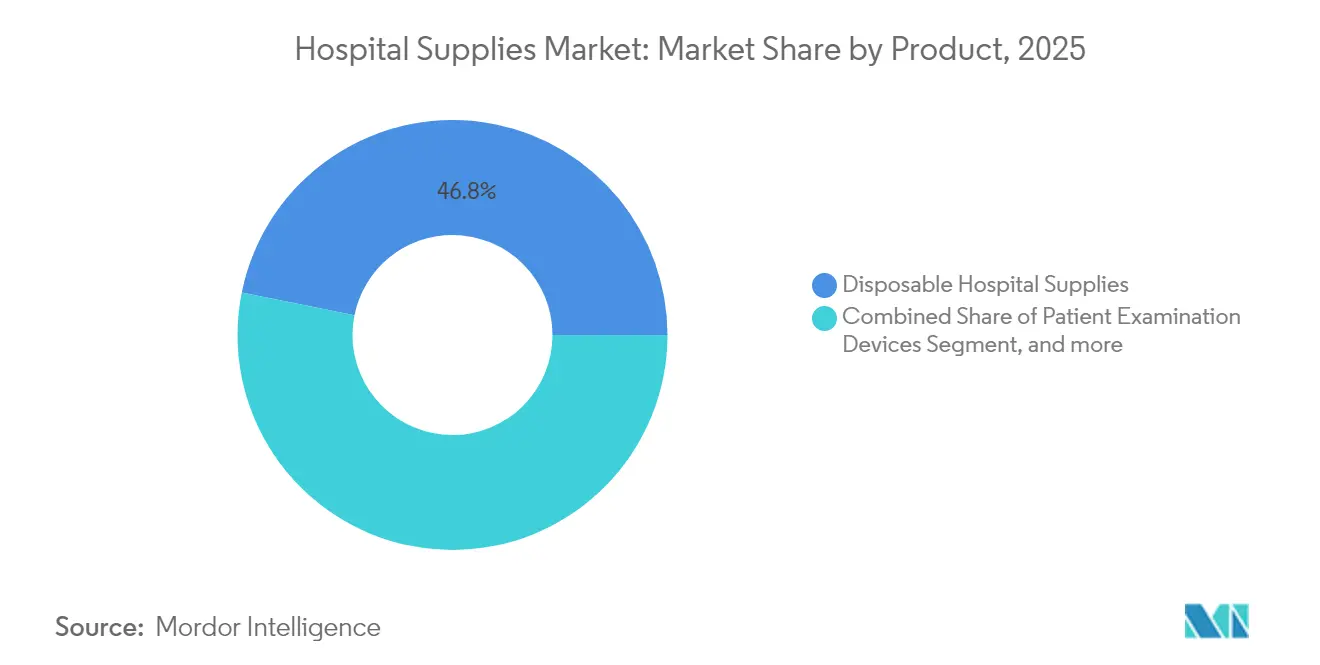

- By product category, disposable hospital supplies led with 46.83% hospital supplies market share in 2025; sterilization and disinfectant equipment is projected to advance at a 10.42% CAGR through 2031.

- By end-user, hospitals accounted for 67.88% of the hospital supplies market size in 2025, while ambulatory surgical centers are forecast to grow at 6.45% CAGR between 2026-2031.

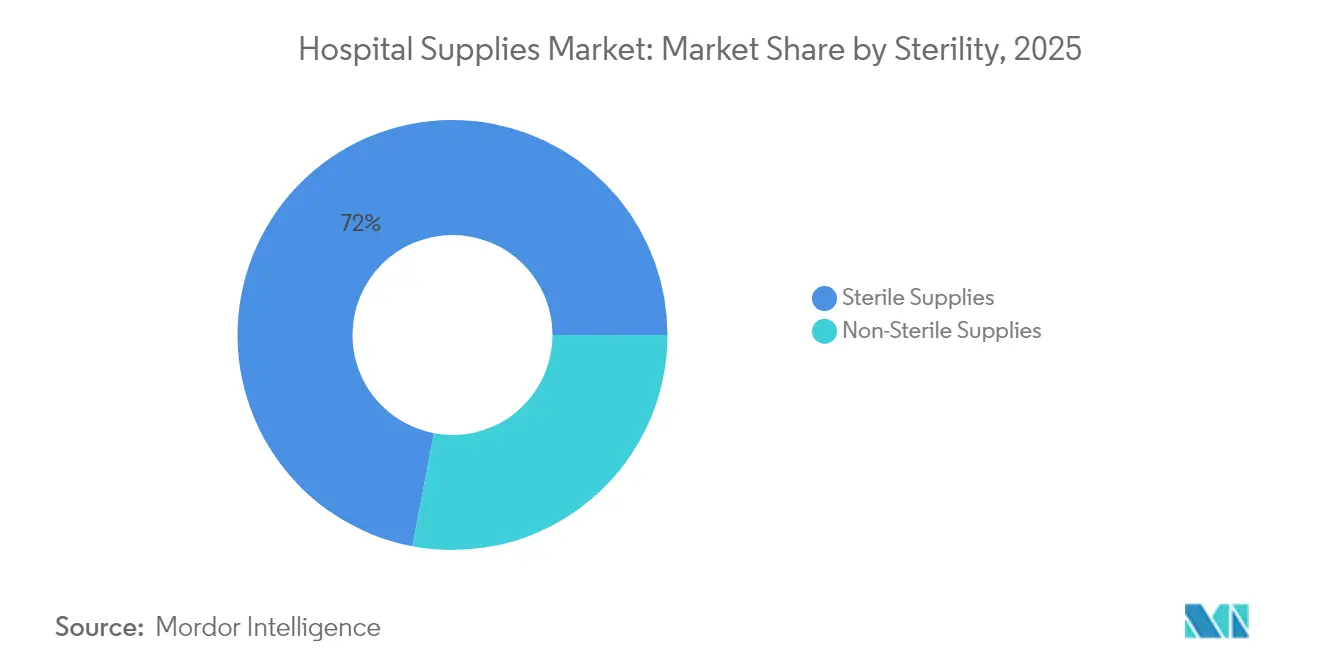

- By sterility, sterile supplies commanded 72.02% share of the hospital supplies market size in 2025 and are expanding at a 6.19% CAGR through 2031.

- By geography, North America retained 33.92% share in 2025; Asia-Pacific is the fastest-growing region at an 8.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hospital Supplies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing incidences of communicable and chronic diseases | +1.2% | Global – higher impact in Asia-Pacific | Medium term (2-4 years) |

| Growing public awareness about hospital-acquired infections | +0.8% | North America, Europe | Medium term (2-4 years) |

| High demand for hospital supplies in developing countries | +1.5% | Asia-Pacific, Middle East & Africa | Long term (≥ 4 years) |

| Hospital-acquired infection penalties catalyzing investment in sterilization equipment | +0.9% | North America, Europe | Short term (≤ 2 years) |

| Surge in surgical volume post-pandemic in developed countries | +0.6% | North America, Europe | Short term (≤ 2 years) |

| Government initiatives and healthcare spending | +0.5% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Incidences of Communicable and Chronic Diseases

Rising diabetes, cardiovascular, and respiratory case loads are forcing hospitals to re-think inventory plans to assure continuous availability of wound-care dressings, monitoring kits, and ventilation circuits. Diabetes alone affects 537 million adults and is projected to reach 783 million by 2045, pushing up specialized dressing use by 30% since 2024.[1]Centers for Disease Control and Prevention, “Chronic Disease in America,” cdc.gov Health systems now pair electronic health-record data with predictive stocking algorithms, enabling tighter alignment between anticipated caseloads and replenishment cycles. This patient-centric approach is steering capital allocations toward versatile sterile supplies, driving the hospital supplies market forward in both mature and emerging economies.

Growing Public Awareness about Hospital-Acquired Infections

Consumers increasingly select facilities based on perceived infection-control performance. Each HAI adds USD 28,400–33,800 in treatment costs, prompting administrators to adopt antimicrobial materials for high-touch surfaces and to publicize compliance metrics. The Centers for Disease Control and Prevention notes that 1 in 31 hospitalized patients contracts an HAI on any given day, spurring hospital supplies market investment into single-use drapes, barrier gowns, and self-disinfecting device casings.[2]Centers for Disease Control and Prevention, “Healthcare-Associated Infections Data,” cdc.gov Suppliers offering verifiable sterility assurance and product traceability gain a competitive advantage.

High Demand for Hospital Supplies in Developing Countries

Asia-Pacific’s expanding middle class is accelerating healthcare construction and driving bulk purchases of beds, surgical packs, and diagnostic disposables. Innovative financing programs such as the International Finance Corporation’s USD 300 million Africa Medical Equipment Facility allow small providers to bypass legacy constraints and adopt modern inventory platforms from day one. Manufacturers that localize production and embed RFID-ready labels are well positioned as regional governments push for resilient supply chains and clinical self-sufficiency.

Hospital-Acquired Infection Penalties Catalyzing Investment in Sterilization Equipment

The Hospital-Acquired Condition Reduction Program cut Medicare payments by up to 1% for the lowest-performing quartile of U.S. hospitals. By 2025, 98.1% of penalized facilities improved scores, triggering a 35% rise in capital outlays for low-temperature sterilizers and track-and-trace autoclaves.[3]JAMA Network, “Teaching and Safety-Net Hospitals Face HACRP Penalties,” jamanetwork.com Administrators increasingly deploy automated re-processing lines that capture cycle parameters and push data back into quality dashboards, aligning regulatory reporting with lean workflow principles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory framework | −0.7% | Global – higher impact in North America & Europe | Medium term (2-4 years) |

| Emergence of home care services | −0.5% | North America, Europe, developed Asia-Pacific | Long term (≥ 4 years) |

| High costs of advanced equipment | −0.4% | Europe, developed Asia-Pacific | Long term (≥ 4 years) |

| Supply chain disruptions | −0.2% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Framework

Efforts to curb ethylene-oxide emissions threaten the sterility pathways for roughly 20 billion medical devices annually. The FDA warned that abrupt closures of sterilization plants could disrupt care continuity, illustrating how environmental policy can ripple through hospital supplies market logistics. Firms now investigate alternative sterilants and invest in redundant capacity, adding cost and complexity to already tight production schedules.

Emergence of Home Care Services

Shifting chronic-care delivery into the home reduces inpatient bed-days and alters purchasing channels. Medicare reimburses approved home-hospital models, prompting manufacturers like 3M Healthcare, Medtronic, and Medline to develop compact infusion pumps, sensor patches, and mail-ready packaging. The distributed nature of home care raises last-mile fulfillment costs and requires consumer-grade user interfaces, tempering traditional volume growth within centralized hospital accounts while opening new but fragmented revenue streams across the wider hospital supplies industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Infection Control Technologies Accelerate Upgrade Cycles

Disposable supplies retained a 46.83% hospital supplies market share in 2025, underscoring their role in combating cross-contamination. Bundled procedure packs and single-use gowns streamline operating-room turnover and reduce labor spent on laundering. However, sustainability policies have sparked pilot projects in selective re-processing and recyclable polymers, pressuring vendors to declare lifecycle emissions. Sterilization and disinfectant equipment, while only a mid-sized segment, is growing fastest at a 10.42% CAGR to 2031. The hospital supplies market size for sterilization equipment is forecast to climb in tandem with digital record-keeping mandates that tie device release to documented microbial kill parameters. Suppliers that bundle cloud-based validation software with low-temperature sterilizers see traction in tier-1 hospital systems.

Patient examination devices and operating-room equipment are integrating sensor arrays and IoT gateways. Smart stethoscopes, computer-assisted navigation, and AI-driven intraoperative imaging drive premium pricing tiers, with procurement decisions increasingly influenced by interoperability scores. Mobility aids and transportation equipment ride demographic trends as aging populations demand pressure-reducing mattresses, electric hoists, and bariatric wheelchairs. Sustainability credentials, spare-parts availability, and cloud-ready diagnostics are now weighted alongside upfront price when frameworks evaluate bids.

By End User: Ambulatory Centers Challenge Hospital Dominance

Hospitals still represent 67.88% of 2025 demand and wield scale economies that translate into bulk-purchase rebates and customized consignment stocks. Their steady case mix supports multi-year sourcing contracts covering gowns, drapes, suction canisters, and composite furniture. However, ASCs are on track to register a 6.45% CAGR through 2031, absorbing an expanding share of elective orthopedics, ophthalmology, and cardiology cases. The hospital supplies market size for ASC-specific product kits is forecast to widen as procedure migration continues. Manufacturers now offer compact autoclaves, low-profile instrument tables, and pre-configured mayo stands optimized for rapid room turnover in small-footprint facilities.

Trauma centers and specialty clinics create niche demand for advanced airway management consumables and tissue adhesives. Private chains deploy enterprise-wide RFID cabinets that feed real-time depletion alerts into central dashboards. Such analytics enhance compliance with FIFO rotation policies and reduce expiration-driven write-offs, translating into lower total-supply costs even when unit prices are higher. Vendors supplement physical goods with data subscriptions, driving sticky, recurring revenue beyond the one-time sale.

By Sterility: Premium on Assured Cleanliness

Sterile supplies captured 72.02% of 2025 revenue. This dominance is tied to infection-penalty programs that penalize facilities with preventable contamination incidents. The hospital supplies market size advantage for sterile products is amplified by 6.19% CAGR growth to 2031. Mobile sterile processing units allow hospitals to refurbish central re-processing departments without interrupting surgical schedules, expanding demand for rental solutions and single-use container systems. Innovations range from vaporized-hydrogen-peroxide cabinets to plasma-based sterilizers, each accompanied by traceability software.

Non-sterile supplies retain essential roles in low-risk procedures and primary care. A 2024 MDPI study found comparable infection outcomes for certain minor dermatological interventions conducted with non-sterile gloves, encouraging formulary committees to re-assess over-specification that may inflate costs. Yet, even in these categories, antimicrobial surface treatments and sustainable packaging improvements differentiate offerings and maintain relevance within broader hospital supplies market purchasing frameworks.

Geography Analysis

North America’s advanced infrastructure and strict infection-control mandates secured 33.92% share of global revenue in 2025. Large-scale adoption of RFID-enabled smart cabinets and AI-assisted demand-planning systems underpins supplier opportunities for analytics-rich value propositions. Tariff uncertainties threatened price stability, prompting distributors like Cardinal Health to consider pass-through mechanisms that could influence hospital supplies market elasticity in 2026.

Asia-Pacific delivers the strongest growth at an 8.18% CAGR, driven by healthcare capacity expansion in China, India, and Southeast Asia. Rapid investment in tertiary hospitals, coupled with government incentives for local manufacturing, shifts component sourcing closer to end-markets. The hospital supplies market size for sterilization consumables is rising briskly as accreditation bodies adopt Western infection-control benchmarks. Medical tourism growth in Thailand and Malaysia further widens procurement pipelines for high-quality but cost-competitive disposables.

Europe maintains a technology-oriented stance, with sustainability mandates encouraging suppliers to validate carbon footprints and integrate recycled polymers. Germany leads by volume, while Switzerland’s high-tech niche manufactures propel segment innovation. Regulatory clarity around the Medical Device Regulation (MDR) encourages early-adopter hospitals to pilot smart labeling and tamper-evident packaging, sustaining premium price points in a mature hospital supplies market.

The Middle East and Africa witness marked divergence. Gulf Cooperation Council nations invest in flagship hospitals that demand state-of-the-art sterilization suites and automated inventory systems. Meanwhile, the International Finance Corporation’s Africa Medical Equipment Facility funds small providers, creating distributed demand for essential devices across East and West Africa. Suppliers that bundle training, maintenance, and micro-leasing schemes gain traction in these price-sensitive yet volume-rich niches.

Competitive Landscape

The hospital supplies market is fragmented, with leading players leveraging integration, innovation, and regional manufacturing to preserve margins amid pricing pressure. Johnson & Johnson and Medtronic expand digital ecosystems by embedding sensors in disposables and harvesting utilization data through cloud portals. Becton, Dickinson and Company’s 2025 decision to spin off its Biosciences and Diagnostic Solutions unit illustrates a sharpened focus on core medical-surgical lines that align tightly with infection-prevention spending priorities.

Sumitomo Corporation deepened its presence in the U.S. home-care channel by acquiring ActivStyle and raising its stake in Vast Medical Holdings, demonstrating how conglomerates deploy diversified capital to capture chronic-disease therapy spend. Henry Schein’s late-2024 acquisition of Acentus underscores the strategic logic of integrating direct-to-patient logistics with sensor-enabled glucose monitoring portfolios. Smaller firms carve out defensible positions in antimicrobial coatings, low-temperature plasma sterilizers, and AI-assisted asset-tracking, frequently partnering with large distributors to extend global reach.

Strategic alliances between device manufacturers and software vendors generate bundled value propositions that streamline clinician workflows. For example, RFID cabinet deployments often come packaged with predictive analytics dashboards co-developed by start-ups specializing in supply-chain AI. The resulting data feeds enable just-in-time restocking, slashing stock-outs and expiration losses. Meanwhile, private-label opportunities proliferate as health systems seek to reduce brand premiums while maintaining stringent quality benchmarks. Suppliers mindful of regulatory shifts, raw-material cost inflation, and sustainability metrics will continue to out-perform within the evolving hospital supplies market.

Hospital Supplies Industry Leaders

Boston Scientific Corporation

Cardinal Health Inc.

B Braun Melsugen AG

3M

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sumitomo Corporation Group (through its U.S. subsidiary, Sumitomo Corporation of Americas) acquired ActivStyle, LLC, a prominent U.S.-based provider of home medical supplies for patients with chronic conditions. This acquisition follows Sumitomo’s move in April 2025 to increase its equity stake in Vast Medical Holdings, the parent company of Quest, a leading supplier of home medical equipment, supplies, and services for individuals managing diabetes.

- December 2024: Gilgal Medical Supplies, a prominent medical supply provider with multiple locations across Florida, has announced a significant shift in its business model. Effective immediately, the company will no longer accept insurance for medical supplies. This strategic change is driven by ongoing challenges and systemic inefficiencies in the insurance reimbursement process, which have increasingly impacted operational sustainability.

- November 2024: Henry Schein, Inc. has announced its agreement to acquire Acentus, a specialized provider of glucose sensors and other medical supplies delivered directly to patients’ homes. This acquisition underscores Henry Schein’s ongoing strategic focus on expanding its homecare medical supplies business, aligning with growing demand for chronic disease management and home-based care solutions.

Global Hospital Supplies Market Report Scope

As per the scope of the report, hospital supplies include every medical utility product that serves both the patient and medical professional with hospital infrastructure and enhances the network and transportation between hospitals. These include hospital equipment, patient aids, mobility equipment, and sterilization disposable hospital supplies. The hospital supplies market is segmented by Product (Patient Examination Devices, Operating Room Equipment, Mobility Aids and Transportation Equipment, Sterilization and Disinfectant Equipment, Disposable Hospital Supplies, Syringes and Needles, and Other Types) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

By Product

| Patient Examination Devices |

| Operating Room Equipment |

| Mobility Aids & Transportation Equipment |

| Sterilization & Disinfectant Equipment |

| Disposable Hospital Supplies |

| Syringes & Needles |

| Smart RFID-Enabled Consumables |

| Other Products |

By End User

| Public Hospitals |

| Private & Chain Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics & Trauma Centers |

By Sterility

| Sterile Supplies |

| Non-Sterile Supplies |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Patient Examination Devices | |

| Operating Room Equipment | ||

| Mobility Aids & Transportation Equipment | ||

| Sterilization & Disinfectant Equipment | ||

| Disposable Hospital Supplies | ||

| Syringes & Needles | ||

| Smart RFID-Enabled Consumables | ||

| Other Products | ||

| By End User | Public Hospitals | |

| Private & Chain Hospitals | ||

| Ambulatory Surgical Centers | ||

| Specialty Clinics & Trauma Centers | ||

| By Sterility | Sterile Supplies | |

| Non-Sterile Supplies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the hospital supplies market?

The hospital supplies market size is USD 159.44 billion in 2026 and is projected to reach USD 193.94 billion by 2031.

Which product segment is growing fastest?

Sterilization and disinfectant equipment is expanding at a 10.42% CAGR due to intensified infection-control investments.

Why are ambulatory surgical centers important for suppliers?

ASCs are forecast to grow at 6.45% CAGR, creating demand for compact, high-throughput kits that differ from traditional hospital preferences.

How are sustainability concerns influencing procurement?

Hospitals increasingly evaluate disposables based on recyclability and carbon footprint, opening opportunities for eco-designed products with validated lifecycle metrics.

What role does technology play in modern hospital supplies?

RFID-enabled cabinets and AI-powered analytics integrate with electronic health records to optimize stock levels, reduce waste, and strengthen compliance reporting, giving tech-savvy suppliers a competitive edge.

Page last updated on: