Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

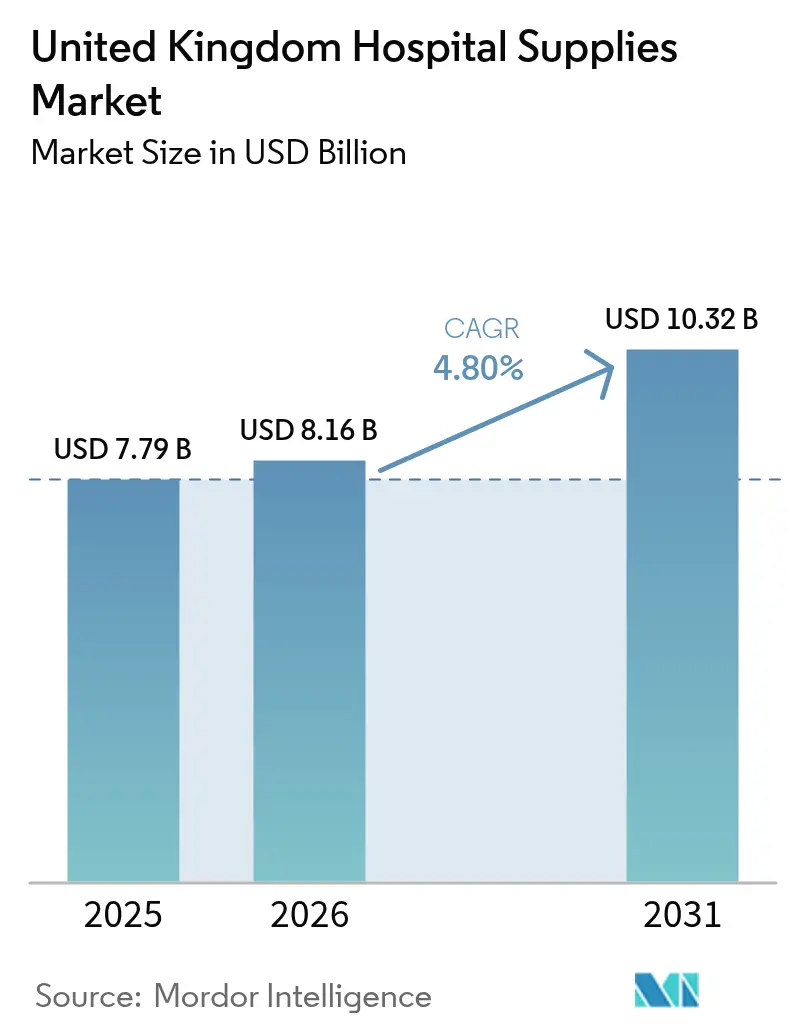

| Base Year Market Size (2025) | USD 7.79 Billion |

| Market Size (2026) | USD 8.16 Billion |

| Market Size (2031) | USD 10.32 Billion |

| Growth Rate (2026 - 2031) | 4.80% CAGR |

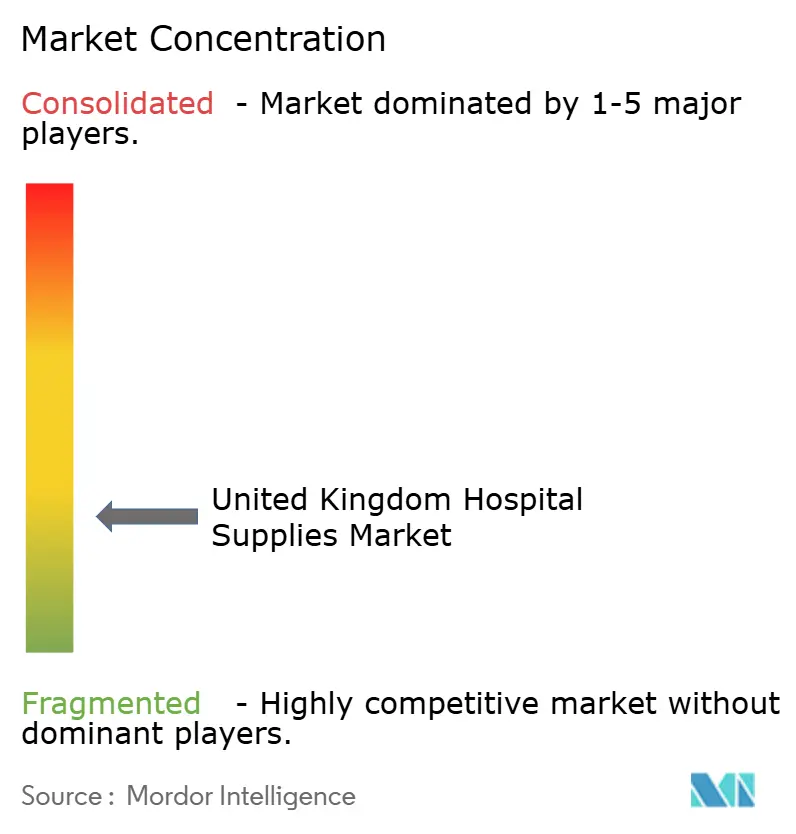

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Hospital Supplies Market Analysis by Mordor Intelligence

The United Kingdom Hospital Supplies Market size in 2026 is estimated at USD 8.16 billion, growing from 2025 value of USD 7.79 billion with 2031 projections showing USD 10.32 billion, growing at 4.80% CAGR over 2026-2031.

The upward trajectory reflects resilient demand despite cost-containment efforts and changing procurement rules. Disposable products remain pivotal as strict infection-control policies drive high turnover of single-use items. At the same time, NHS capital spending and digital-ward initiatives are stimulating replacement purchases of connected equipment. Compliance with the new UKCA labelling regime is reshaping product design and documentation requirements, prompting manufacturers to streamline quality-management systems. Suppliers that couple sustainability credentials with proven clinical performance are gaining preferred-supplier status across regional purchasing groups.

Key Report Takeaways

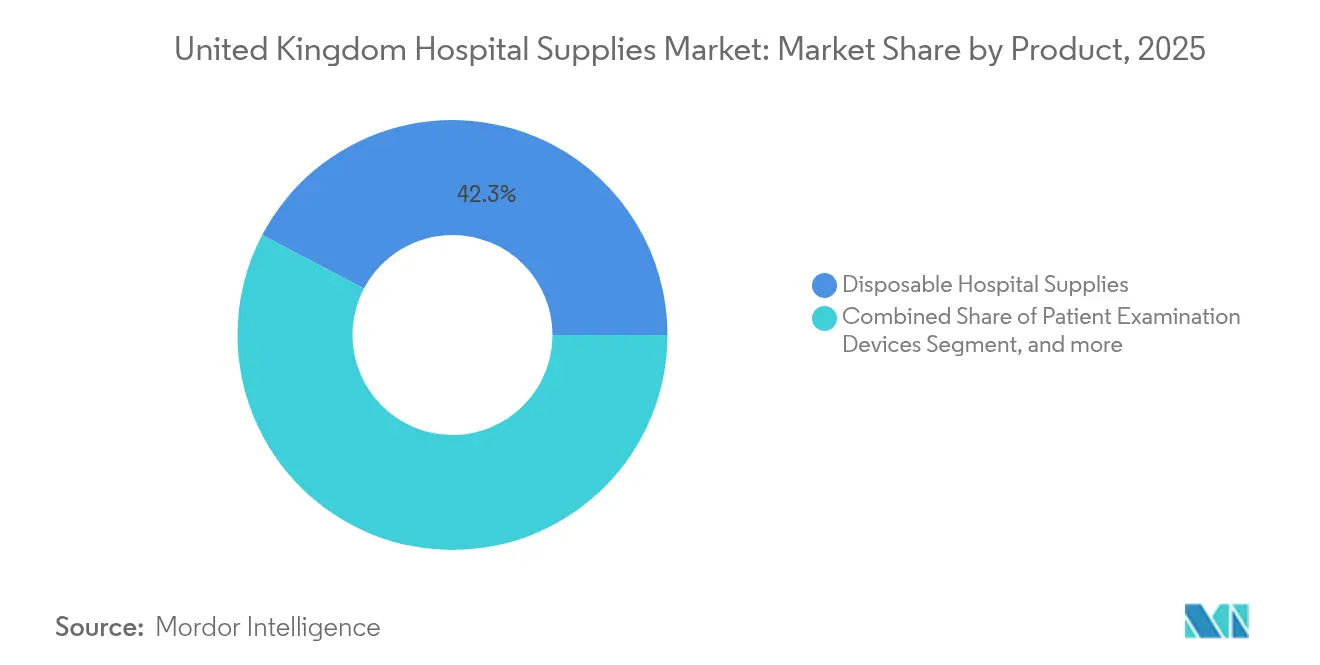

- By product category, disposable hospital supplies led with a 42.31% revenue share in 2025, while sterilization and disinfectant equipment is projected to advance at a 7.31% CAGR through 2031.

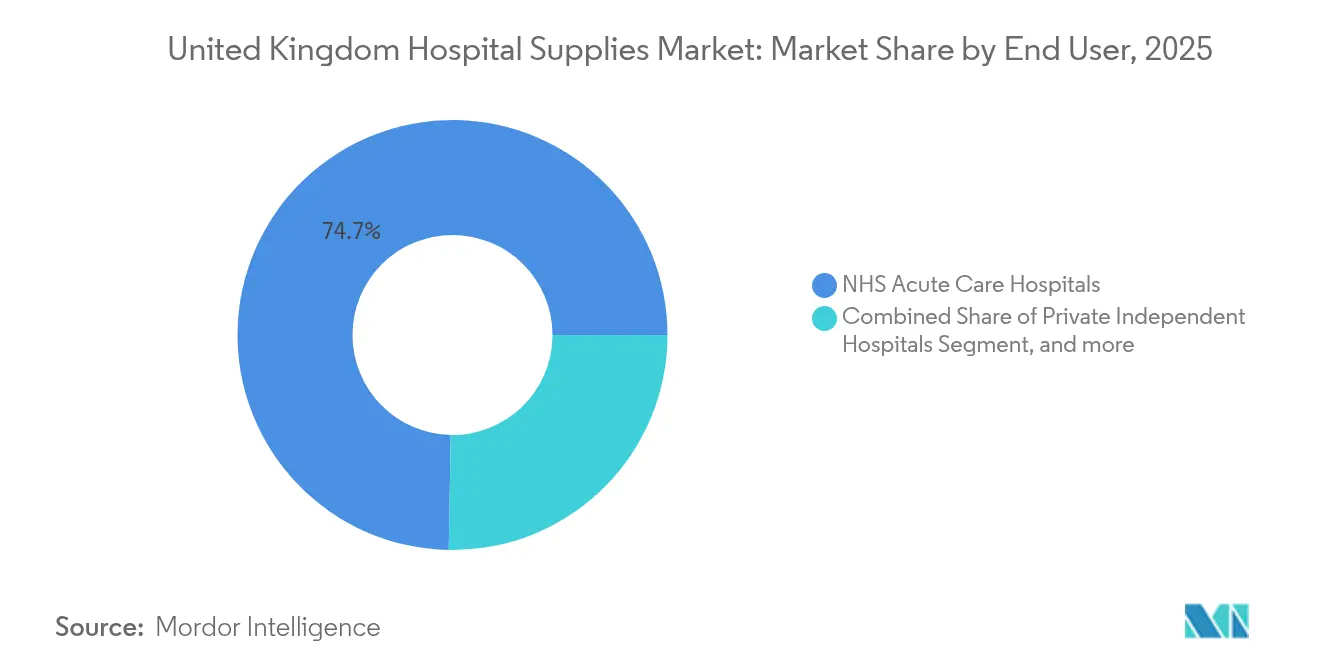

- By end user, NHS acute-care hospitals accounted for 74.72% of the United Kingdom hospital supplies market share in 2025, and private independent hospitals are set to register the fastest 6.14% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Hospital Supplies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population and chronic-disease burden | +1.2% | National, higher in coastal and rural regions with older demographics | Long term (≥ 4 years) |

| Stringent infection-control and antimicrobial-resistance policies | +0.9% | National, emphasis in major urban centers | Medium term (2-4 years) |

| NHS capital investment and digital-ward programmes | +0.7% | National, early adoption in teaching hospitals | Medium term (2-4 years) |

| Growing public awareness about hospital-acquired infections | +0.5% | National, highest in metropolitan areas | Short term (≤ 2 years) |

| Growth in surgical procedures and emergency care | +0.4% | National | Short term (≤ 2 years) |

| Medical tourism and international patient influx | +0.2% | London, Manchester, Birmingham | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population & Chronic Disease Burden

The share of United Kingdom residents aged 65 and over continues to climb, accelerating demand for mobility aids, wound-care items, and multi-parameter monitors. The Royal Society projects the 85-plus cohort will double to 5.1 million by 2066, reinforcing the need for equipment that supports complex comorbidities.[1]The Royal Society, “Ageing Population Statistics,” royalsociety.org Acute-care wards are prioritizing bariatric beds, lifting devices, and low-profile mattresses that cut fall risk while easing manual handling strains on staff. Suppliers that validate ergonomics and patient-comfort benefits are being listed on national procurement frameworks. Rehabilitation units are also expanding orders for multifunction wheelchairs and walking aids tailored to arthritic and neurological patients.

Stringent Infection-Control & AMR Policies

The 2024–2029 UK antimicrobial-resistance action plan mandates proactive surveillance and robust sterilization practices. Hospitals are upgrading autoclaves and UV-C disinfection units that achieve faster cycle times and verifiable log-reduction levels. Single-use drapes, gowns, and minimally-invasive procedure kits are preferred for isolation rooms. Demand is especially high in London teaching hospitals where antimicrobial stewardship committees audit usage rates. Manufacturers that certify products under the Microbiological Cleanliness Gold Standard are improving tender success rates across integrated-care systems.

NHS Capital Investment & Digital-Ward Initiatives

The New Hospital Programme and allied digitization funds allocate GBP 15 billion from 2030 for estate renewal and smart-ward rollouts.[2]UK Government, “Antimicrobial Resistance Action Plan 2024-2029,” gov.uk Priority purchases include connected infusion pumps, smart vital-sign monitors, and asset-tracking tags that feed real-time data to electronic patient-record platforms. Framework agreements now include interoperability scoring, incentivizing suppliers to embed open-architecture protocols. Earlier pilots at University College London Hospital show a 17% reduction in bed-turnaround time after adopting location-tracking trolleys, encouraging wider replication across acute trusts.

Growing Public Awareness about Hospital-Acquired Infections

Post-pandemic patient surveys indicate perceived cleanliness is a leading factor in hospital choice. Trusts have responded by installing touch-free sanitizer stations, antimicrobial copper fixtures, and visible air filtration kiosks in reception areas.[3]UK Health Security Agency, “Business Plan 2024-2025,” gov.uk These highly-visible interventions are fostering a parallel market for aesthetic-grade infection-control products that demonstrate efficacy without institutional appearance. Suppliers offering colour-coded packaging and public-facing educational material are securing premium positioning in facility-wide contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory framework | -0.8% | National, larger effect on small and medium suppliers | Medium term (2-4 years) |

| Hospital-at-home model lowering inpatient supply usage | -0.6% | Early adoption in urban centers | Long term (≥ 4 years) |

| Budget constraints and NHS cost pressures | -0.5% | National | Short term (≤ 2 years) |

| Supply-chain vulnerabilities | -0.4% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Framework

The transition from CE to UKCA marking raises documentation workload and prolongs certification lead times. The Medicines & Healthcare products Regulatory Agency now requires an expanded technical-file structure and enhanced post-market surveillance. Smaller manufacturers risk missed tender windows as recertification stretches to 2028 for high-risk devices. Combined with upcoming environmental-impact disclosures, the heavier compliance burden can deter niche innovators from UK launches.

Hospital-at-Home Model Lowering Inpatient Supply Usage

Virtual wards are targeting 40–50 beds per 100,000 residents by 2025. Each remote bed averts one acute admission, reducing usage of standard ward consumables such as disposable linens, emesis bags, and bulk cleaning solutions. Suppliers must redesign inventory forecasts and develop dual-use devices with clinic-to-home adaptability. Portable oxygen concentrators and Bluetooth-enabled blood-pressure cuffs are gaining traction as trusts reallocate budgets toward community-based monitoring kits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Disposable Dominance Faces Sustainability Shift

Disposable supplies generated the largest revenue in 2025 with a 42.31% share of the United Kingdom hospital supplies market. Hospital infection-control committees favour single-use masks, gowns, and procedure packs that eliminate reprocessing risks and speed operating-room turnover. That dominance is being challenged by the Design for Life roadmap, which urges an 84% cut in waste through reusable textiles and instrument trays. The roadmap is steering procurement teams toward life-cycle costing models. In this context, the United Kingdom hospital supplies market size for sterilization and disinfectant equipment is expected to expand 7.31% CAGR to 2031 as facilities invest in low-temperature plasma units and traceability software.

The sustainability imperative is also prompting suppliers to introduce hybrid kits that combine reusable trays with single-use inserts. Pilot studies at South-Tees Hospitals show a 66% reduction in carbon emissions when laparoscopic-instrument handles are reprocessed and paired with disposable tips. Larger trusts are issuing multiphase tenders that split volumes between disposable and reusable lines, creating opportunities for specialized SMEs that can validate washing-cycle durability and comparable clinical outcomes.

By End User: Private Hospitals Accelerate Procurement Cycles

NHS acute-care hospitals accounted for 74.72% of the United Kingdom hospital supplies market in 2025, driven by centrally funded purchases and bulk-buy agreements. Framework contracts for core consumables such as IV sets and wound dressings often span four years, locking in high volumes. The United Kingdom hospital supplies market share attributable to NHS orders remains high but incremental growth is shifting to the independent sector. Private hospitals are projected to post a 6.14% CAGR through 2031 as NHS outsourcing and self-pay patient demand rise.

Private operators typically operate shorter procurement cycles and favour premium devices that differentiate their service offer. For example, Spire Healthcare is retrofitting theatres with robotic surgical arms and ordering single-port instrument kits that command higher average selling prices. Suppliers that offer flexible consignment stock and rapid restocking windows are securing multi-site agreements. Teaching hospitals remain niche but influential buyers because they trial prototype devices and generate clinical-evidence dossiers that influence national adoption pathways.

Geography Analysis

London and the Southeast produced the highest spending within the United Kingdom hospital supplies market in 2024, reflecting higher population density, top-tier research hospitals, and substantial private-healthcare penetration. The presence of major cardiac and oncology centres drives demand for advanced surgeries and related consumables. Teaching hospitals in the capital are early adopters of AI-enabled endoscopy towers and smart beds that update electronic records in near real time.

Northern England and Scotland are earmarked for accelerated capital replacement through targeted levelling-up funds. NHS Ayrshire & Arran will channel GBP 24.34 (USD 32.59) million into equipment renewal during FY 2025-26, prioritizing imaging suites and digital asset-tracking systems. The United Kingdom hospital supplies market size across Scotland is expected to grow faster than the national average as health boards modernize estates and expand virtual-ward capacity.

Wales and Northern Ireland contribute smaller but rising shares. Welsh initiatives that target sustainable procurement are opening tenders for reusable surgical textiles, while Northern Ireland’s integrated-care strategy is increasing orders for home-monitoring kits. The Innovative Devices Access Pathway is operating across all devolved nations and offers regulatory support for breakthrough devices. Suppliers winning IDAP acceptance can secure pilot deployments in several regional health boards simultaneously, shortening time to scaled adoption.

Regulatory Landscape

Hospital supplies sold into Great Britain are regulated as medical devices under the Medicines and Healthcare products Regulatory Agency (MHRA). The ongoing transition from CE to UKCA is reshaping labeling, technical documentation, and post-market surveillance requirements. CE-marked devices continue to be accepted on the GB market under published transition timelines, with acceptance running to 30 June 2028 or 30 June 2030 depending on device type and certification status, which helps limit near-term supply disruption while manufacturers rework compliance files and labeling.

Regulatory reform activity accelerated with the Medical Devices (Amendment) (Great Britain) Regulations 2025, which came into force on 24 May 2025 to extend application of specific assimilated EU law elements (including technical specifications and electronic instructions). On 8 May 2026, MHRA published the draft Medical Devices (Amendment) Regulations 2026 via the WTO notification process, setting out proposals such as international reliance routes, mandatory Unique Device Identification (UDI), and updated IVD classifications. These changes increase the importance of traceability data and structured regulatory evidence for suppliers serving NHS and private hospital procurement.

Value Chain Analysis

The UK hospital supplies value chain starts with raw-material and component providers (polymers and nonwovens for disposables, metals and electronics for devices), then moves to manufacturers and contract packers. Importers and UK distributors manage UKCA/CE documentation, labeling, and batch traceability before products enter hospital procurement channels. NHS Supply Chain acts as a central procurement and logistics node for many consumables and devices, with frameworks supported by national warehousing, while suppliers also pursue direct sales to large trusts and independent hospital groups for higher-acuity equipment and service-led categories.

On the demand side, Integrated Care Systems (ICS) and Integrated Care Boards (ICB) provide a regional coordination layer for tendering and inventory aggregation, which can drive greater standardization across trusts and increase the scale of multi-site awards. Procurement governance has shifted with the Procurement Act 2023 for non-clinical goods and services effective 24 February 2025. At the same time, evolving MHRA requirements, including movement toward UDI in the draft 2026 amendments, raise the operational importance of master data management across NHS Supply Chain catalogs, hospital ERP systems, and supplier QA systems.

Competitive Landscape

The United Kingdom hospital supplies market features a fragmentation. Multinational suppliers protect share through extensive catalogues that cover critical-care disposables, implantables, and capital equipment. 3M expanded its antimicrobials portfolio in 2025 with a zinc-oxide transparent barrier film that shortens dressing changes by 21%. B. Braun rolled out a modular drug-compounding robot to English oncology centres, integrating it with existing closed-system transfer devices.

Acquisitions are streamlining supply chains and broadening product depth. Lohmann & Rauscher Group acquired Unisurge International in April 2025 to secure domestic sterile-kit manufacturing and lower post-Brexit border friction. The deal adds high-volume procedure packs and surgical gowns to Lohmann’s wound-care and compression-therapy lines. Sustainability is becoming a procurement differentiator. Smith & Nephew reports that its wound-care plant in Hull now operates on 100% renewable electricity, meeting new NHS carbon-footprint thresholds ahead of peer targets. Mölnlycke publishes supplier-audit data that tracks water and energy intensity per finished-square-metre across its gown facilities, supporting hospitals that assess embedded emissions within tender scoring.

Digital capabilities are another pivot. Baxter’s infusion pumps now export infusion-time data to electronic patient-record platforms used across eight acute trusts. Medtronic has partnered with NHS England to co-develop AI algorithms that predict surgical-kit usage and reduce unused-tray costs. Start-ups focusing on remote patient monitoring are also attracting procurement attention as virtual beds expand.

United Kingdom Hospital Supplies Industry Leaders

B. Braun Melsungen AG

3M

Baxter International Inc.

Medtronic

Cardinal Health Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Procurement is moving toward structured value demonstration, creating whitespace for suppliers that can quantify pathway and whole-life benefits across high-usage hospital supplies. In June 2026, the UK Government rolled out Value Based Procurement (VBP) national standard guidance for medical technology, requiring buyers to weight value domains (minimum 60%) against whole-life cost (maximum 40%). This shifts the emphasis toward clinical and health-economic evidence for products such as infection-control consumables, smart ward equipment, and traceability-enabled sterilization systems.

Capital and commercial programmes also create buying windows for suppliers positioned around estate renewal and technology-enabled productivity. In July 2026, the Government published the 10 Year Capital Plan for Health and Social Care, including GBP 6.75 billion over nine years for hospital repairs and a capital budget for health rising to GBP 15 billion in 2029/30, alongside NHS England capital guidance for 2026/27 to 2029/30 and national program funding covering the New Hospital Programme and technology/productivity initiatives. The publication of a MedTech Commercial Strategy 2026 (developed by NHS England, DHSC, and NHS Supply Chain) supports a more unified commercial lifecycle, increasing the need for suppliers to align catalog readiness, data standards, and service models with NHS Supply Chain and ICS-led procurement routes.

Recent Industry Developments

- May 2026: NHS Supply Chain issued a product update on the phased branding, packaging, and labeling transition from 3M to Solventum for multiple healthcare products, with the changeover running through to the end of 2027. The update required hospitals and distributors to manage SKU and label continuity in ordering, receiving, and clinical areas. It also raises the importance of traceability and catalog master data across NHS supply channels during the transition period.

- April 2026: The distribution partnership between B. Braun and Joint Operations Ltd for its spine portfolio across the United Kingdom strengthens local coverage and clinical support for specialist surgical supplies, improving access for hospital customers relying on distributor-led service and inventory models. It also illustrates continued channel optimization among multinational suppliers to protect share in procedure-driven categories.

- April 2025: Lohmann & Rauscher Group acquired Unisurge International Ltd., adding UK-based sterile kit manufacturing and expanding its portfolio of procedure packs and surgical gowns. The combination improves domestic supply capability for high-turnover sterile products and reduces exposure to post-Brexit border friction for time-sensitive hospital consumables. The acquisition also supports broader framework participation by pairing Unisurge kits with Lohmann & Rauscher wound care and compression offerings.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of supplies and equipment routinely used inside UK hospitals to examine, treat, and care for patients, including operating room, sterilization, mobility, and disposable supply needs, measured at selling price levels.

Scope exclusions: This sizing does not include medicines and vaccines, hospital construction, or non-medical facility services such as catering and general housekeeping.

Segmentation Overview

- By Product

- Patient Examination Devices

- Operating Room Equipment

- Mobility Aids & Transportation Equipment

- Sterilisation & Disinfectant Equipment

- Disposable Hospital Supplies

- Syringes & Needles

- Other Products

- By End User

- NHS Acute Care Hospitals

- Private Independent Hospitals

- Specialty & Teaching Hospitals

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with a plain mapping of what hospitals buy and how that shows up in public data. We pulled UK health spending and activity indicators from sources such as NHS England publications, the UK Office for National Statistics, and HMRC trade and customs statistics to understand demand direction and import exposure for key categories.

To ground assumptions, we also referenced sources such as MHRA safety notices and device registration guidance, peer reviewed clinical and procurement papers, and relevant association websites that discuss procurement frameworks and usage practices. Company annual reports, investor presentations, and reputable press were used to cross-check category mix and price movement signals, and a paid subscription for company financials and a patent database were used selectively to validate supplier scale and innovation intensity. These sources are illustrative only, and many additional public documents were reviewed to collect, validate, and clarify the final inputs.

Primary Interviews and Surveys

Primary discussions were used to pressure test what is counted as hospital supplies in real purchasing cycles, and to align pricing and volume assumptions with on-the-ground procurement behavior. We spoke with participants across manufacturers, distributors, group purchasing functions, hospital procurement teams, and clinical users, and coverage was balanced across the UK to reflect differences in trust level buying patterns and private hospital demand.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 12% | |

| Mid tier: 53% | Functional/Unit leaders: 39% | |

| Smaller Players: 17% | Managers: 49% |

Market-Sizing & Forecasting

Sizing was first built using a top-down demand reconstruction, where UK hospital activity levels and procurement intensity were translated into category spend using publicly observable signals and interview-backed ratios. Once the total was formed, it was corroborated with selective bottom-up checks, like sample supplier revenue allocation to the UK, channel discussions on category throughput, and simple ASP times volume approximations for high-run-rate consumables.

Inputs that matter in this market include elective procedure recovery pace, inpatient and outpatient volumes, infection prevention intensity (which changes disposable use), sterilization throughput needs, mobility and transport equipment replacement cycles, and imported product share that affects pricing through currency timing. Forecasts leaned on scenario analysis with a base case agreed through expert inputs, and it was then stress-tested using short series trend tools such as exponential smoothing for categories that track hospital activity closely. When supplier level data was incomplete, gaps were handled through category mix benchmarks and procurement share ranges validated again in follow-up calls.

Data Validation & Update Cycle

Model outputs were checked against independent signals like NHS spending direction, procedure and admission volumes, and import patterns for relevant supply groups, and the largest variances were reviewed line by line. Outliers were questioned, assumptions were re-tested with respondents, and then the draft was reviewed in multiple analyst passes before sign-off.

The report is refreshed annually, and interim updates are made when material events shift demand, pricing, or procurement behavior. Before delivery, a final refresh pass is done so clients receive the most current view that can be traced back to clear inputs and checks.

Mordor Intelligence's UK Hospital Supplies Market Estimate Compared With Other Published Estimates

Published market values for UK hospital supplies can look different because each publisher draws the scope line in its own way, and then applies its own price and activity assumptions to build the total. Differences also come from the year used for pricing, how imports are converted into value, and how often the model is refreshed.

Some external totals appear to bundle broader healthcare equipment and supply spend across settings beyond hospitals or add adjacent non-hospital channels, and then carry that wider spend into the UK number. In Mordor Intelligence sizing, only products purchased for hospital use are counted, and adjacent categories like pharmaceuticals and non-medical facility services are kept out to prevent inflating the spend base.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.79 B (2025) | |

| Global Consultancy A | USD 8.60 B (2026) | Uses a longer forecast window and a starting-year value that can reflect more aggressive price progression for disposables and broader inclusion of hospital equipment spend, which lifts the first forecast-year total versus a strict base-year spend view. |

| Trade Publisher B | USD 14.16 B (2035) | Reports a far-out forecast year and may compound growth across wider healthcare supply categories, which makes the end-year number look much larger and less tied to near-term hospital activity and replacement cycles. |

The spread in figures mostly comes from scope width and the choice of starting and ending years, which can magnify growth when compounded over a longer horizon. By keeping the spend definition linked to hospital-use products and checking assumptions against activity and procurement signals, our estimate stays easier to replicate and audit across years.

Key Questions Answered in the Report

What is the current value of the United Kingdom hospital supplies market?

The market is valued at USD 8.16 billion in 2026 and is projected to reach USD 10.32 billion by 2031.

Which product category generates the highest demand?

Disposable hospital supplies lead with a 42.31% revenue share in 2025, driven by infection-control priorities.

How fast will sterilization and disinfectant equipment grow?

This segment is expected to post a 7.31% CAGR between 2026 and 2031 as hospitals strengthen antimicrobial-resistance defenses.

Why are private independent hospitals gaining momentum?

NHS outsourcing and rising self-pay demand are steering more procedures to private facilities, underpinning a 6.14% CAGR for their supplies spending.

How is the regulatory shift to UKCA marking affecting suppliers?

Manufacturers must invest in new conformity assessments and post-market surveillance, raising compliance costs and extending product-launch timelines.

What role does sustainability play in purchasing decisions?

NHS procurement frameworks now award points for carbon-footprint reductions, favouring suppliers that offer reusable products and transparent environmental data.

Page last updated on: