U.S. Specialty Medical Chairs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.74 Billion |

| Market Size (2026) | USD 1.86 Billion |

| Market Size (2031) | USD 2.64 Billion |

| Growth Rate (2026 - 2031) | 7.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Specialty Medical Chairs Market Analysis by Mordor Intelligence

The U.S. Specialty Medical Chairs Market size is projected to be USD 1.74 billion in 2025, USD 1.86 billion in 2026, and reach USD 2.64 billion by 2031, growing at a CAGR of 7.20% from 2026 to 2031.

Healthcare delivery in the United States is shifting significantly, with more procedures transitioning from inpatient hospitals to ambulatory and outpatient settings. This change is driving demand for flexible clinical seating to support a broader range of procedures. CMS has added 560 procedures to the Ambulatory Surgical Center Covered Procedures List for CY 2026 and initiated a 3-year phase-out of the Inpatient-Only list, influencing equipment planning across facilities. The aging population in the United States, with over 59 million adults aged 65 and older representing 17.7% of the total population in 2023, is sustaining demand for height-adjustable, bariatric-capable, and accessible chairs across various care settings.

Key Report Takeaways

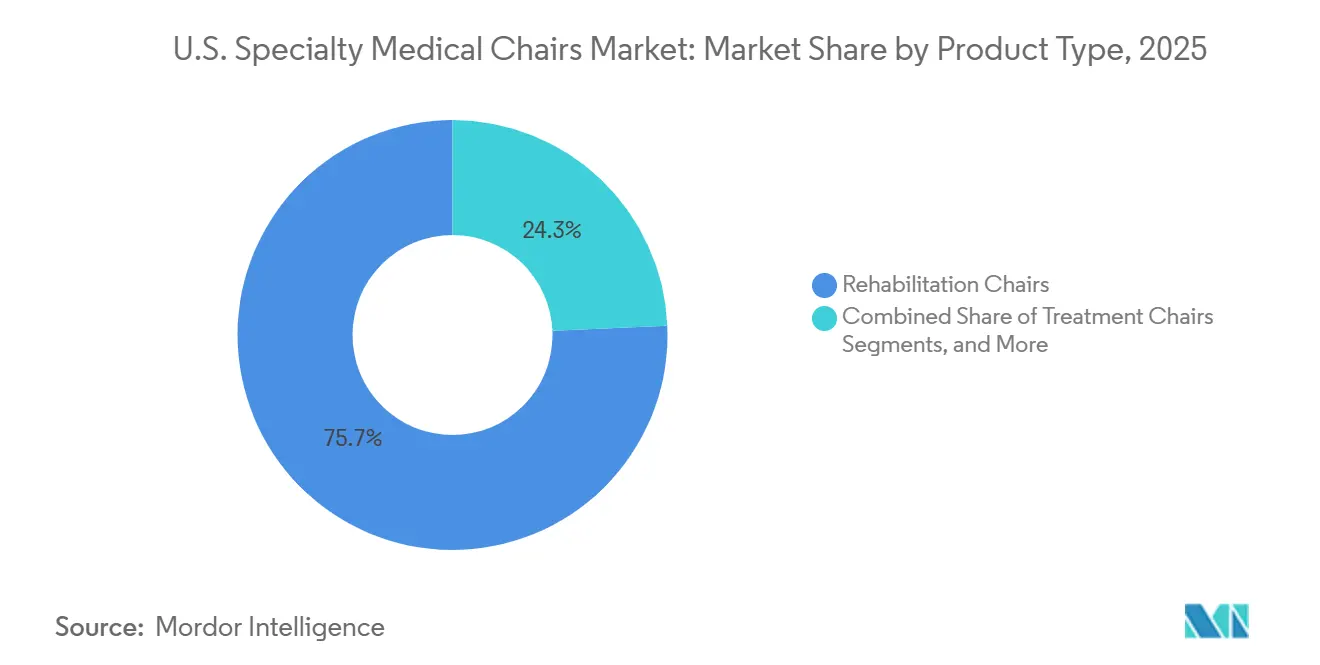

- By product type, rehabilitation chairs led with a 75.69% share in 2025, while treatment chairs are projected to expand at an 8.20% CAGR through 2031.

- By technology/actuation, fully electric chairs held 65.55% share in 2025, while hydraulic and semi-electric chairs are forecasted to grow at a 7.99% CAGR through 2031.

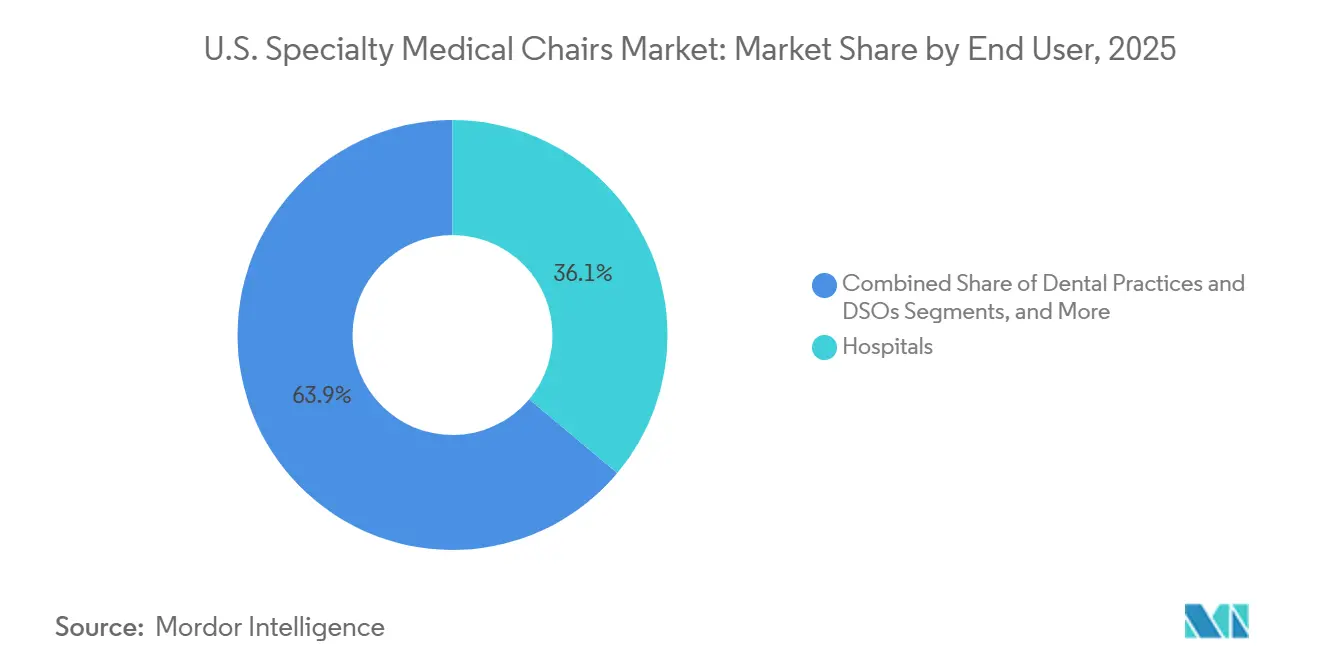

- By end user, hospitals accounted for 36.10% share in 2025, while dental practices and DSOs are expected to record the fastest growth at an 8.34% CAGR through 2031.

- By clinical application, dental held 32.56% share in 2025, while OB/GYN is projected to grow at an 8.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Specialty Medical Chairs Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Outpatient procedure migration from inpatient and hospital settings | +2.3% | National, concentrated in urban markets with dense ASC networks | Short term (≤ 2 years) |

| Aging and mobility-limited patient base generating higher clinical encounter volumes | +1.8% | National, amplified in Florida, Arizona, Texas, and Sun Belt states | Long term (≥ 4 years) |

| Dental chair replacement and DSO fleet standardization | +1.2% | National, concentrated in metropolitan DSO clusters | Medium term (2-4 years) |

| Chronic kidney disease and infusion-treatment demand at dedicated outpatient centers | +1.0% | National, especially Southeast, Midwest, and urban-dense Northeast | Medium term (2-4 years) |

| Accessible exam-chair compliance mandates following the MDE rule | +0.8% | National, priority in states with large public healthcare provider networks | Short term (≤ 2 years) |

| Pressure-injury prevention seating protocols in acute and post-acute care settings | +0.5% | National, highest uptake in hospital-dense Northeastern and Midwestern states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Outpatient Procedure Migration Restructuring Chair Demand in Real Time

CMS has removed 285 musculoskeletal procedures from its Inpatient-Only list for CY 2026 and added 560 procedures to the ASC Covered Procedures List, accelerating the shift of treatment volumes to ambulatory settings. Medicare facility payments to ASCs are projected to reach USD 9.2 billion in 2026, with ASC surgical procedures per fee-for-service Medicare beneficiary increasing by 3.4% in 2024.[1]Centers for Medicare & Medicaid Services, “Calendar Year 2026 Hospital Outpatient Prospective Payment System (OPPS) and Ambulatory Surgical Center Final Rule (CMS-1834-FC),” Fact Sheets, cms.gov This shift is driving demand in the United States specialty medical chairs market for versatile, programmable electric platforms that support multi-procedure workflows and optimize outpatient room layouts.

Aging Demographics Driving Multi-Comorbidity Seating Requirements

The aging population in the United States, projected to reach 88.8 million by 2060, is increasing the need for medical chairs designed for mobility challenges, transfer difficulties, and fall prevention.[2]United Health Foundation, “2025 Senior Report,” America’s Health Rankings, americashealthrankings.org With 53% of Medicare beneficiaries aged 65-74 managing three or more chronic conditions, facilities are replacing older fixed-height chairs with models offering safer transfers and longer treatment support, broadening demand geographically and extending replacement cycles.

DSO Standardization Creating Fleet-Level Chair Procurement

DSO-supported practices accounted for 51% of dental visits in 2024, up from 40% two years earlier, with Heartland Dental expanding to over 1,900 practices by 2025.[3]Thomas N., Kingsbury S., Lansing J., and Houtenville A., “Section 1, Population and Prevalence, Compendium (2026),” Center for Research on Disability, researchondisability.org This scale is reshaping procurement in the United States specialty medical chairs market, as large dental groups prioritize fleet-level contracts, ergonomic consistency, and planned maintenance, accelerating the replacement of older hydraulic chairs with advanced electric platforms.

CKD and Infusion-Treatment Demand Sustained by Evolving Treatment Modalities

In 2024, 59,000 Medicare beneficiaries began dialysis, while over 7,600 outpatient dialysis facilities operated nationwide. DaVita served approximately 295,000 patients across 2,657 centers by 2025. Increasing chemotherapy infusion volumes and the rollout of Fresenius Medical Care’s 5008X CAREsystem in 2026 are further driving demand for durable therapy chairs in the United States specialty medical chairs market, with renal and oncology treatments fueling growth through 2031.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High upfront acquisition cost of fully electric and connected specialty chairs | -1.5% | National, most acute in rural and underserved markets | Short term (≤ 2 years) |

| Budget pressure and capital constraints in small clinics and independent private practices | -0.8% | National, concentrated in nonmetropolitan and lower-income regions | Medium term (2-4 years) |

| Actuator and upholstery service availability bottlenecks | -0.4% | National, worsened in regions with thin service-technician networks | Medium term (2-4 years) |

| Room retrofit and electrical-load infrastructure requirements for powered chair installation | -0.3% | National, concentrated in older clinic stock in rural and suburban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Chair Costs Creating Capital Access Disparities

Fully electric specialty exam chairs in ophthalmic applications are priced between USD 5,850 and USD 11,650, while dental chairs range from USD 6,300 to USD 11,650. Fixed phlebotomy seating is more affordable, priced between USD 400 and USD 1,300. Redesigning products to meet the 17-inch low transfer height standard could increase manufacturer costs by 20% to 30%, creating a financial gap between large health systems and smaller clinics with limited budgets. Compliance pressures remain high, as federally funded providers must meet accessibility standards by July 8, 2026. Demand in the United States specialty medical chairs market is steady at the compliance threshold, but broader upgrades are constrained by budget limitations.

Budget Pressure in Small and Independent Practices Dampening Replacement Cycles

A 2026 review of over 8,500 dental practices found that approximately 1,050 practices averaged 44 chairs, generating only USD 56,000 in annual revenue per chair. Underutilization of existing equipment makes capital investments challenging for independent practices, which often extend replacement cycles beyond the typical 10-15 years due to financial pressures. Subscription models ease upfront costs but are primarily adopted by larger DSO affiliates, leaving smaller practices behind. As a result, the United States specialty medical chairs market relies on hospitals, DSOs, and dialysis chains for near-term growth, while older independent chair fleets remain a slower-moving segment for replacement demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Treatment Chairs Outpacing Legacy Examination Formats

Treatment chairs are projected to grow at an 8.20% CAGR through 2031, driven by the shift of chemotherapy, infusion, and hemodialysis activities to outpatient centers. These chairs are valued for comfort during long sessions, stable positioning, safe transfers, and durability for high utilization, making them a key growth driver in the United States specialty medical chairs market. Models balancing recline range, transfer access, and durability are gaining preference.

Rehabilitation chairs held a 75.69% market share in 2025, reflecting their demand in skilled nursing, post-acute recovery, and long-term care settings. Extended daily use emphasizes pressure redistribution, bariatric capacity, and caregiver safety.

By Technology/Actuation: Connectivity Now Defining Competitive Differentiation

Fully electric chairs accounted for 65.55% of the United States specialty medical chairs market in 2025, driven by programmable positioning, enhanced ergonomics, and accessibility compliance. These systems reduce caregiver strain and support multiple workflows, maintaining their strong position across hospitals, DSOs, and outpatient sites.

Hydraulic and semi-electric chairs, with a projected 7.99% CAGR through 2031, cater to cost-sensitive settings requiring height adjustability without premium connectivity. Manual chairs remain relevant in home care and home dialysis but are expected to see reduced facility-based applications. Maintenance visibility and service simplicity are becoming critical purchase factors.

By End User: DSO Consolidation Reshaping the Upper Tier of Demand

Hospitals held 36.10% of the United States specialty medical chairs market in 2025, driven by their diverse clinical applications and higher revenue per installed chair. Hospitals remain central to premium chair adoption due to complex clinical and ergonomic requirements.

Dental practices and DSOs, with an 8.34% CAGR forecast through 2031, represent a strong procurement channel. Centralized buying power is rising, supported by DSO expansions. Dialysis centers, ambulatory surgery centers, physician offices, and rehabilitation facilities exhibit varied buying patterns, while home care and dialysis are growing as therapy shifts to home settings.

By Clinical Application: OB/GYN Compliance Wave Reshaping a Historically Under-Invested Segment

Dental applications accounted for 32.56% of the United States specialty medical chairs market in 2025, supported by high visit volumes and standardized procurement across multi-site practices. Replacement demand is driven by prolonged use and the need for ergonomic upgrades.

OB/GYN applications are projected to grow at an 8.25% CAGR through 2031, driven by compliance requirements for accessible exam chairs. Public healthcare entities face deadlines for accessibility targets, spurring replacement activity. Infusion, oncology, dialysis, and other specialties benefit from the broader trend of shifting procedures to outpatient settings.

Geography Analysis

The Northeast holds the largest regional share in the United States specialty medical chairs market, driven by dense hospital networks, academic medical centers, and mature dialysis facility coverage. This concentration ensures stable replacement demand across various clinical applications, reducing reliance on a single procedure category. Florida remains a key aging-driven demand center, with adults aged 65 and older comprising 21.7% of its population in 2023. States like Texas, Arizona, Tennessee, and Georgia are also experiencing growth in retirement-age residents, increasing demand for accessible seating in ambulatory and post-acute settings. Procedure-specific demand aligns with facility density, as illustrated by ASC activity, where ASC density varies significantly across states.

The Midwest plays a dual role in the United States specialty medical chairs market by combining domestic chair manufacturing with a substantial treatment base. Companies such as Ohio-based Midmark and Florida-based Champion Healthcare Solutions highlight the connection between production and provider networks. Midwestern hospital systems serve broad rural areas with higher chronic disease burdens, ensuring steady demand for rehabilitation and treatment chairs. This balance benefits the region through both replacement needs and ongoing demand from mobility-limited patients, favoring vendors with extensive service coverage.

The West remains a significant region in the United States specialty medical chairs market, with California leading due to high ASC utilization and strong outpatient procedure activity. Nationwide, a majority of simple cataract removals with intraocular lens insertion are now performed in ASCs rather than hospital outpatient departments, benefiting states with dense ASC networks. Rural and nonmetropolitan areas face longer chair replacement cycles due to factors such as limited service-technician networks, extended travel times, tighter financing conditions, and older clinic infrastructures requiring retrofits for powered chair installations.

Competitive Landscape

The United States specialty medical chairs market is moderately fragmented, with competition driven by clinical specialization rather than a unified equipment category. Dental chair vendors such as A-dec, Midmark, DENTALEZ, Planmeca, Dentsply Sirona, J. Morita, and Takara Belmont focus on ergonomics, DSO fleet compatibility, and software integration. Rehabilitation and treatment chair suppliers like Champion Healthcare Solutions, ActiveAid, Hill Laboratories, and Winco emphasize pressure redistribution, bariatric load support, transport usability, and caregiver handling. Buyers typically compare vendors within specific care settings, leading to varied market leadership based on end use.

The dialysis segment is a key concentration point in the United States specialty medical chairs market, with DaVita and Fresenius Medical Care controlling approximately 75% of freestanding dialysis facilities in 2024. Fresenius benefits from its therapy chair portfolio, developed with Likamed, which is deployed across its clinic network, limiting third-party access. In February 2026, Midmark expanded its platform by launching next-generation connected dental operatory solutions, including a redesigned dental chair with Smart View connectivity. Additionally, Midmark partnered with Bien-Air Dental to integrate electric micromotors and contra-angle handpieces into its Procenter and Elevance systems, reflecting a shift toward integrated clinical environments.

Dentsply Sirona announced an annual allocation of USD 120 million in 2026 to enhance connected dentistry and clinical education. Smaller companies like MTI and S4OPTIK leverage the exam chair replacement cycle by offering compliant designs at competitive prices, increasing pressure on mid-tier brands. Procurement trends favor vendors that ensure uptime, service responsiveness, fleet consistency, and compliance across hospitals, DSOs, dialysis chains, and outpatient centers. Competitive advantage now hinges on supporting the lifecycle of chair fleets across distributed sites rather than individual ergonomic features.

U.S. Specialty Medical Chairs Industry Leaders

Midmark Corporation

A-dec, Inc.

Dentsply Sirona Inc.

Fresenius Medical Care AG

Planmeca Oy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Midmark Corporation launched next-generation connected dental operatory solutions, positioning itself as a platform provider with integrated real-time monitoring to minimize downtime and support DSO multi-site management.

- February 2026: Midmark and Bien-Air Dental SA partnered to integrate Bien-Air's precision instruments into Midmark's delivery systems, enhancing ergonomics and reducing cross-contamination risks.

- February 2026: DENTALEZ, Darby Dental Supply, and UptimeHealth introduced TotalOp, an operatory subscription model offering standardized setups, predictive maintenance, and automated service scheduling for DSOs.

- February 2026: DENTALEZ launched the Forest 5400 Chair Package, a cost-effective, US-assembled dental chair targeting DSOs and independent practices with high lift capacity and reliable performance.

- June 2025: Fresenius Medical Care received FDA clearance for its 5008X CAREsystem and began U.S. commercialization, driving demand for compatible therapy chairs across hemodialysis installations.

U.S. Specialty Medical Chairs Market Report Scope

As per the scope of the report, specialty medical chairs are purpose-built, ergonomic medical devices designed for specific clinical treatments, examinations, or patient rehabilitation. Engineered to prioritize patient comfort and clinician accessibility, they feature automated positioning, antimicrobial surfaces, and heavy-duty weight capacities.

The U.S. specialty medical chairs market is segmented by product type, technology/actuation, end-user, and clinical application. By product type, the market includes examination chairs, treatment chairs, and rehabilitation chairs. By technology/actuation, the market is segmented into manual, hydraulic/semi-electric, fully electric, and connected/programmable electric. By end-user, the market is categorized into hospitals, physician offices and specialty clinics, dental practices and DSOs, ambulatory surgery centers, dialysis centers, blood collection centers, rehabilitation centers (skilled nursing facilities and long-term care settings), home care and home dialysis settings, and others. By clinical application, the market is segmented into dental, ophthalmic, ENT, dialysis, infusion and oncology, OB/GYN, dermatology and aesthetics, podiatry, rehabilitation and physiotherapy, and others. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Examination Chairs |

| Treatment Chairs |

| Rehabilitation Chairs |

| Manual |

| Hydraulic / Semi-electric |

| Fully Electric |

| Connected / Programmable Electric |

| Hospitals |

| Physician Offices and Specialty Clinics |

| Dental Practices and DSOs |

| Ambulatory Surgery Centers |

| Dialysis Centers |

| Blood Collection Centers |

| Rehabilitation Centers, Skilled Nursing Facilities, and Long-term Care Settings |

| Home Care and Home Dialysis Settings |

| Others |

| Dental |

| Ophthalmic |

| ENT |

| Dialysis |

| Infusion and Oncology |

| OB/GYN |

| Dermatology and Aesthetics |

| Podiatry |

| Rehabilitation and Physiotherapy |

| Others |

| By Product Type | Examination Chairs |

| Treatment Chairs | |

| Rehabilitation Chairs | |

| By Technology / Actuation | Manual |

| Hydraulic / Semi-electric | |

| Fully Electric | |

| Connected / Programmable Electric | |

| By End User | Hospitals |

| Physician Offices and Specialty Clinics | |

| Dental Practices and DSOs | |

| Ambulatory Surgery Centers | |

| Dialysis Centers | |

| Blood Collection Centers | |

| Rehabilitation Centers, Skilled Nursing Facilities, and Long-term Care Settings | |

| Home Care and Home Dialysis Settings | |

| Others | |

| By Clinical Application | Dental |

| Ophthalmic | |

| ENT | |

| Dialysis | |

| Infusion and Oncology | |

| OB/GYN | |

| Dermatology and Aesthetics | |

| Podiatry | |

| Rehabilitation and Physiotherapy | |

| Others |

Key Questions Answered in the Report

What is the forecast value of the US specialty medical chairs market by 2031?

The US specialty medical chairs market is forecast to reach USD 2.64 billion by 2031 from USD 1.86 billion in 2026, with a CAGR of 7.20% over 2026-2031.

Which product segment leads demand in 2025?

Rehabilitation chairs held the largest share in 2025 at 75.69%, supported by strong use across skilled nursing, post-acute, and long-term care settings.

Which segment is growing the fastest through 2031?

Treatment chairs are projected to expand at an 8.20% CAGR through 2031 because more dialysis, infusion, and chemotherapy activity is moving into outpatient centers.

Why are dental practices and DSOs becoming more important buyers?

Dental practices and DSOs are projected to grow at an 8.34% CAGR, and DSO-supported practices already accounted for 51% of U.S. dental visits in 2024, which supports larger fleet-style procurement.

What is driving growth in OB/GYN chair demand?

OB/GYN is forecast to grow at an 8.25% CAGR through 2031, largely because accessible exam chair compliance rules are forcing replacement in a category that historically had low compliance with transfer-height standards.

What is the main barrier to faster adoption of fully electric specialty chairs?

The biggest restraint is upfront cost, because fully electric specialty chairs can cost several times more than fixed seating, while many smaller clinics still face tight capital budgets and longer replacement cycles.

Page last updated on: