South America AI-powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

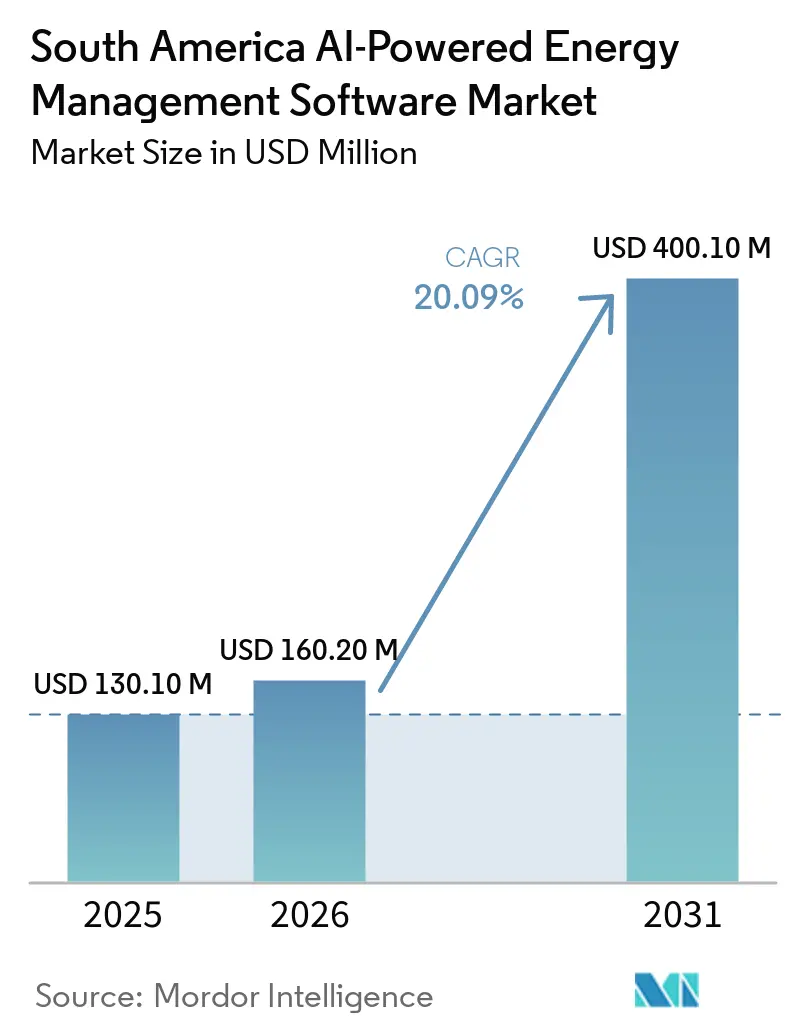

| Base Year Market Size (2025) | USD 130.10 Million |

| Market Size (2026) | USD 160.20 Million |

| Market Size (2031) | USD 400.10 Million |

| Growth Rate (2026 - 2031) | 20.09% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America AI-powered Energy Management Software Market Analysis by Mordor Intelligence

The South America AI-powered Energy Management Software Market was valued at USD 130.1 million in 2025 and estimated to grow from USD 160.2 million in 2026 to reach USD 400.1 million by 2031, at a CAGR of 20.09% during the forecast period 2026-2031. Mandatory carbon reporting rules, smart meter programs, and broader grid digitalization are driving buyers to adopt platforms that continuously monitor energy use and turn operational data into actionable insights. A grid mix led by hydropower, with rising solar and wind additions, is making forecasting and flexible load management more valuable than legacy monitoring tools alone. Industrial users are no longer treating AI-enabled energy platforms as stand-alone sustainability projects, as these systems now support compliance reporting, production planning, and cost control. Competition is also moving toward bundled software, services, and integration support because aging OT and IT environments still slow deployment at many facilities. This leaves the strongest opportunities in recurring analytics, faster reporting, and site-level optimization across large, distributed operations in the South America AI-powered Energy Management Software Market.

Key Report Takeaways

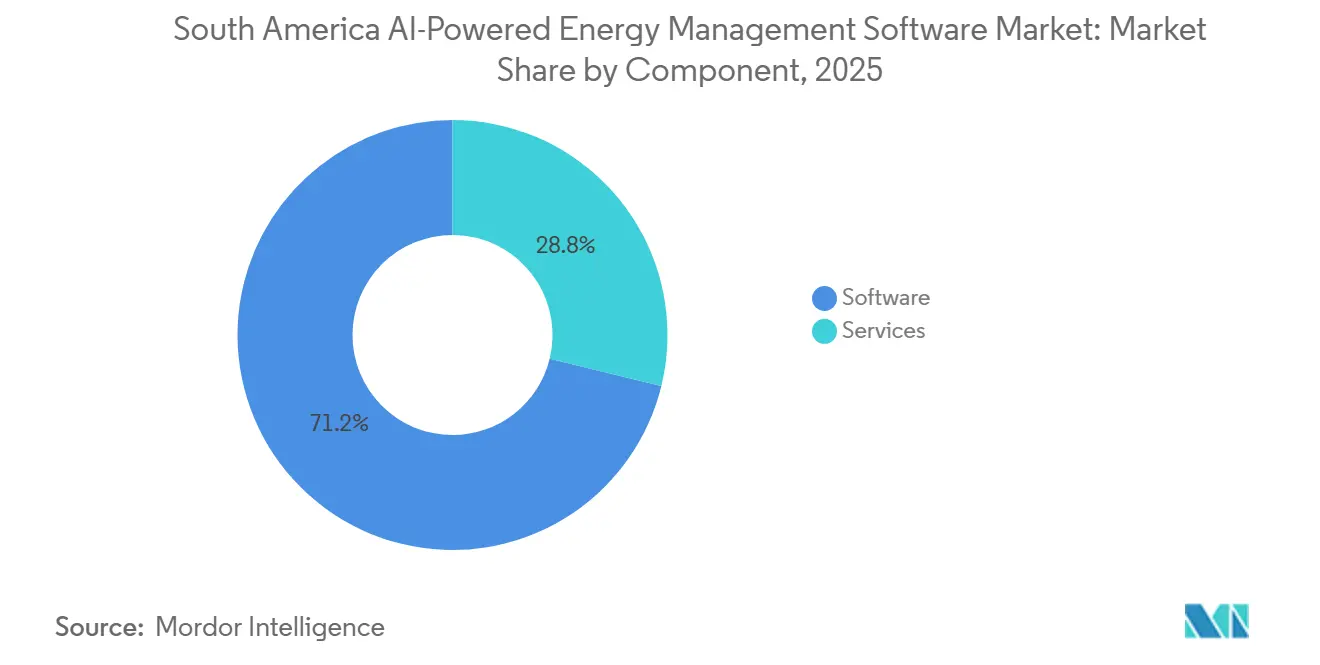

- By component, software accounted for 71.19% of the South America AI-powered Energy Management Software Market in 2025, while services are projected to expand at a 20.23% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 59.14% of the market in 2025, while hybrid deployment is projected to grow at a 20.34% CAGR through 2031.

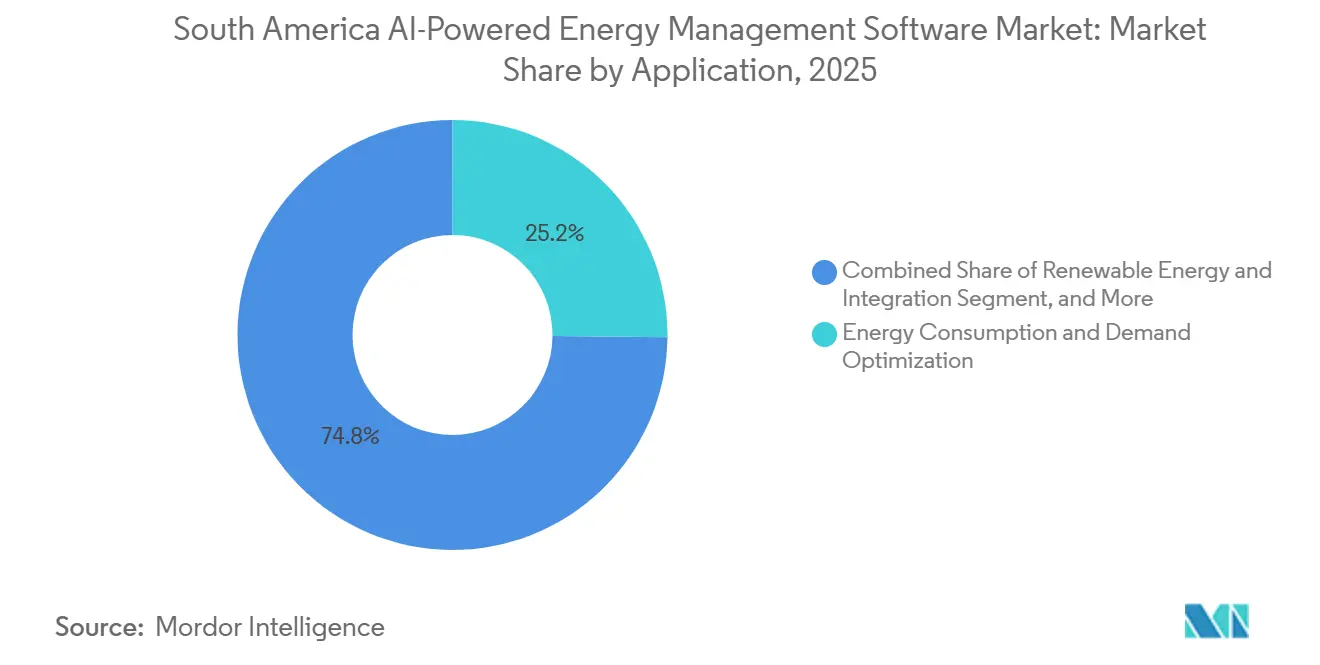

- By application, energy consumption and demand optimization captured 25.16% of the market share in 2025, while renewable energy forecasting and integration are projected to expand at a 20.47% CAGR through 2031.

- By end user, utilities held 31.12% share in 2025, while industrial facilities are projected to advance at a 20.58% CAGR through 2031.

- By geography, Brazil held 39.11% of the South America AI-powered Energy Management Software Market share in 2025, while Chile is projected to record the highest CAGR at 20.67% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America AI-powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Industrial Demand for AI-Based Load Optimization | +4.5% | Brazil, Chile, Colombia | Medium term (2-4 years) |

| Regulatory Push for Energy Efficiency and Carbon Reporting | +3.8% | Brazil, Chile, Colombia | Short term (≤ 2 years) |

| Utility AMI and Smart Meter Rollouts | +3.2% | Brazil, Chile | Short term (≤ 2 years) |

| Cloud and Edge Deployment for Distributed Sites | +2.8% | Brazil, Chile, Colombia, Argentina | Medium term (2-4 years) |

| ESG-Linked Procurement in Export-Oriented Industries | +2.5% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| Retrofit Demand in Mining, Manufacturing, and Commercial Real Estate | +2.2% | Brazil, Chile, Colombia, Argentina | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Industrial Demand for AI-Based Load Optimization

South America’s energy-intensive industrial base is generating clear returns from AI-based load optimization, especially in mining, cement, pulp, paper, and metals. Vale inaugurated its first AI-powered ore processing plant in Minas Gerais in June 2026, and the site delivered a 25% productivity gain while optimizing more than 400 variables in real time, demonstrating how energy choices are being integrated into core production control rather than handled separately. ABB added generative AI to the ABB Ability Energy Management System in April 2026, which lowered the skill barrier for plant teams by enabling natural-language queries on energy use, emissions, and equipment performance. In Chile, rising power tariffs are making AI load shifting and time-of-use management a direct margin tool for mining companies, which broadens the role of the South America AI-powered Energy Management Software Market beyond compliance work alone. Samarco’s COI Maestro rollout in April 2026 also showed that buyers increasingly want one operating layer that combines production monitoring, quality control, supply chain coordination, and energy tracking.

Regulatory Push for Energy Efficiency and Carbon Reporting

The South America AI-powered Energy Management Software Market is also benefiting from regulations that now link energy monitoring to carbon disclosure and formal management systems. Brazil’s Law 15.042/2024 created annual greenhouse gas inventory obligations for companies that emit more than 10,000 tons of CO₂ equivalent per year, which pushed energy data collection closer to the asset level from 2026 onward.[1]B4 Capital, “Brazilian Law 15.042/2024: Regulatory Framework and Practical Guidelines for Companies With Carbon Inventory Obligations,” B4 Capital, b4.capital Chile’s Energy Efficiency Law, expanded in 2026, added 522 companies to mandatory consumption reporting, with operational energy management systems required by August 2026. Colombia’s Senate approved Law 143/2024 in December 2025, which widened the policy base for energy efficiency standards and emissions reduction. This regulatory mix is giving the South America AI-powered Energy Management Software Market a steadier demand base, although vendors still need to separate buyers moving for compliance from those moving for performance gains.

Utility AMI and Smart Meter Rollouts

Smart meter and advanced metering infrastructure programs are expanding the data foundation that AI energy platforms need to operate at scale in the South America AI-powered Energy Management Software Market. South America is projected to see USD 6.8 billion in smart meter investments between 2026 and 2033, with Brazil holding the dominant share and requiring at least 60 million devices over 8–10 years at BRL 25 billion to BRL 35 billion, or USD 5 billion to USD 7 billion.[2]BNamericas, “Latin America Smart Meter Investments Seen Totalling US$6.8bn By 2033,” BNamericas, bnamericas.com Brazil’s Ministry of Mines and Energy set a March 2026 target for distributors to install smart meters in at least 2% of consumer units each year, equal to 3.6 million meters in the initial phase. Ordinance 111/2025 also required open consumer data APIs and aligned distribution network digitalization with LGPD cybersecurity and interoperability needs. The Siemens and CPFL Energia partnership announced in March 2025 for 1.6 million meters in São Paulo by 2029 showed why recurring analytics and data management services are becoming more valuable than the hardware sale itself.[3]Siemens AG and CPFL Energia, “Siemens Partners With CPFL Energia To Digitalize Brazil’s Electricity Sector,” Plant Automation Technology, plantautomation-technology.com

Cloud and Edge Deployment for Distributed Sites

Distributed energy assets and remote industrial sites are pushing the South America AI-powered Energy Management Software Market toward mixed cloud and edge architectures. Brazil’s market liberalization under Law 15.269/2025 increased the need for cloud-native platforms that can coordinate trading, demand response, and peer-to-peer transactions while linking with national power institutions. The National Grid Operator used the AVEVA PI System across 12 processes and 4 centers to automate real-time dispatch, which showed how centralized data layers support grid-scale optimization. At the same time, mining sites, remote hydropower assets, and offshore facilities still need sub-second edge control for operational loops and safety functions, which is why hybrid deployment is rising quickly in the South America AI-powered Energy Management Software Market. Procurement standards such as OpenADR and DLMS/COSEM are gaining weight in this environment because buyers want systems that can connect across utilities, meters, and distributed energy resources.[4]Brasilienergie, “Energy Cloud Brazil: Why Cloud-Native Platforms Will Make Liberalization Work,” Brasilienergie, brasilienergie.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity With Legacy OT and IT Systems | -3.5% | Brazil, Argentina | Medium term (2-4 years) |

| Upfront Retrofit CAPEX and Long Payback Cycles | -2.8% | Argentina, Colombia | Short term (≤ 2 years) |

| Data Quality and Interoperability Gaps Across Multi-Site Operations | -2.0% | Rest of South America | Medium term (2-4 years) |

| Cybersecurity and Data Sovereignty Concerns for Critical Energy Assets | -1.5% | Brazil, Chile | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity With Legacy OT and IT Systems

The main barrier in the South America AI-powered Energy Management Software Market remains the difficulty of connecting older operational systems with newer AI and cloud layers. Energisa’s centralized ADMS rollout spans 4 years and requires training for 7,000 staff, underscoring the scale of the operational change burden even for well-resourced utilities. Petrobras also needed a broader redesign of OT and IT boundaries because older network segmentation tools were insufficient for a distributed asset base that combined legacy systems with cloud infrastructure. Academic work on AI manufacturing adoption in Latin America found that Brazil and Colombia had policy support for Industry 4.0 but limited, binding implementation mechanisms for SMEs, leaving many firms to absorb integration risks on their own. This complexity favors incumbents that already own connectors, protocol libraries, and site relationships, which raises switching costs for newer software specialists in the South America AI-powered Energy Management Software Market.

Upfront Retrofit CAPEX and Long Payback Cycles

High upfront spending and longer payback cycles still slow some projects in the South America AI-powered Energy Management Software Market, especially where financing costs remain elevated. Heavy-industry energy-optimization retrofits can have payback periods of 4–7 years, making many digital projects harder to approve when bundled with broader plant upgrades. In Colombia, AI energy platforms reported typical payback periods of 18–36 months for mid-sized commercial and industrial users, which showed that adoption becomes easier when the consumption base is clear and measurable. Development bank and green credit programs in Brazil and Colombia can shorten effective payback periods by 10–12 months, but many borrowers still lack the technical teams needed to deploy systems quickly. This is why service contracts that shift spending from capital budgets to operating budgets are becoming more relevant across the South America AI-powered Energy Management Software Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Anchors Revenue as Services Shift Toward Recurring Models

Software held 71.19% of the South America AI-powered Energy Management Software Market share in 2025, reflecting the shift from isolated instruments toward platforms that combine forecasting, reporting, anomaly detection, and benchmarking. Brazil’s carbon inventory rules and Chile’s SGE reporting requirements are both pushing buyers toward platforms that can validate data and automate recurring submissions. That regulatory structure gives software a structural advantage because it can be updated continuously as obligations change across countries. In this setting, software serves as the control layer that links operational data with business reporting in the South America AI-powered Energy Management Software Market.

Services are projected to expand at a 20.23% CAGR through 2031, because many users still need outside support for integration, model tuning, compliance workflows, and ongoing monitoring. The Siemens and CPFL Energia metering program showed that the long-term value increasingly lies in data management, fraud detection, and analytics subscriptions rather than in device shipments alone. ABB’s April 2026 update to the ABB Ability Energy Management System also supports this shift by making the platform easier for plant teams to use, thereby deepening recurring service relationships even when internal analyst resources are limited. The relevance of ISO 50001 in large industrial settings further supports demand for managed services, as certification and reporting routines require steady oversight across the South America AI-powered Energy Management Software Market.

By Deployment Mode: Cloud Anchors Scale as Hybrid Closes the Gap

Cloud-based deployment held 59.14% of the South America AI-powered Energy Management Software Market share in 2025, supported by utilities and large operators that need centralized visibility across wide asset networks. The Eletrobras and C3 AI expansion in August 2025 showed that cloud-native architecture can detect and mitigate transmission faults in under 10 seconds across a national network. Cloud environments also align with Brazil’s growing free energy market, where settlement, metering, trading, and benchmarking require shared data layers. This has kept cloud deployment in the lead across the South America AI-powered Energy Management Software Market, especially where operating footprints span several regions.

Hybrid deployment is projected to grow at a 20.34% CAGR through 2031, because remote mines, hydropower sites, and offshore assets need edge control at the site and enterprise analytics in the cloud. Antofagasta’s operating model in Chile illustrated this need by linking remote operations with planning and optimization across a power-intensive mining base. The ONS use of the AVEVA PI System also provided a practical model for balancing centralized visibility with local infrastructure control inside Brazil’s grid environment. On-premises demand remains smaller but durable, as data residency and critical infrastructure rules limit external hosting, keeping deployment choices varied across the South America AI-powered Energy Management Software Market.

By Application: Demand Optimization Leads as Renewables Integration Accelerates

Energy consumption and demand optimization accounted for 25.16% of the South America AI-powered Energy Management Software Market size in 2025, making it the largest application in the regional mix. Its lead reflects the direct savings available from tariff management, demand response, and benchmarking across distributed sites, especially where time-of-use pricing and demand charges affect margins. Asset performance and predictive maintenance also held strong positions because unplanned outages incur both production losses and energy penalties in process industries. Smart grid and distributed energy resource management are gaining support as distributed generation expands under grid rules that require closer coordination between prosumers and system operators.

Renewable energy forecasting and integration is projected to advance at a 20.47% CAGR through 2031, making it the fastest-moving application in the South America AI-powered Energy Management Software Market. Brazil’s renewable-heavy power mix and rising solar and wind additions are making dispatch forecasting more urgent than in systems that still rely mainly on fossil fuels. Stem’s PowerTrack deployment at Chile’s 135 MW Granja Solar project, with a 420 MWh battery retrofit, demonstrated how a single platform can integrate generation forecasting, storage dispatch, and grid-interactive control. Chile’s Nexor software launch in 2026 also pointed to stronger interest in tools that connect weather, operations, and pricing data for renewable dispatch and trading decisions.

By End User: Utilities Anchor the Base as Industrial Facilities Set the Pace

Utilities held 31.12% of the South America AI-powered Energy Management Software Market share in 2025, supported by the scale of transmission and distribution networks that need continuous monitoring. This user group remains foundational because utilities generate steady demand for fault prediction, dispatch support, meter data management, and software for renewable integration. Commercial buildings followed as a meaningful user base, especially where HVAC optimization and demand response can deliver visible savings across office, retail, and mixed-use sites. Residential buildings stayed small because average loads are lower, and smart-home infrastructure is still limited across much of the region.

Industrial facilities are projected to record a 20.58% CAGR through 2031, the fastest pace among end users in the South America AI-powered Energy Management Software Market. Vale, Samarco, and ABB each showed in 2026 that mining and process industries are moving from pilots to production-scale deployments that tie energy management more closely to operations. Export-facing sectors such as steel and cement also face growing pressure to document energy performance and emissions for international buyers, which strengthens the business case for continuous monitoring tools. This mix of cost control, compliance pressure, and production integration is driving industrial adoption faster than the base utility segment across the South America AI-powered Energy Management Software Market.

Geography Analysis

Brazil held 39.11% of the South America AI-powered Energy Management Software Market share in 2025, making it the largest country market in the region. Its lead came from the region’s biggest utility network, the broadest industrial AI rollout base, and a regulatory agenda that now covers carbon reporting, smart meters, and network digitalization. The Ministry of Mines and Energy set a target in March 2026 for distributors to install smart meters in at least 2% of consumer units each year, which started a structured path toward large-scale data availability. Ordinance 111/2025 strengthened that path by requiring open APIs and LGPD-aligned digitalization rules for low-voltage distribution networks. This combination keeps Brazil at the center of the South America AI-powered Energy Management Software Market because utilities and industrial firms both need higher-quality data pipelines.

Argentina and Colombia each held meaningful positions in 2025, although their demand patterns differed. Argentina’s oil and gas base supported demand for asset performance and predictive maintenance tools, with AVEVA-linked deployments reported across major operators. Currency volatility and high funding costs still limit longer-payback digital programs in Argentina, hindering faster expansion. Colombia moved with a more supportive policy backdrop after the December 2025 approval of Law 143/2024, and local platforms such as NOVA+Ema added a domestic innovation layer to the South America AI-powered Energy Management Software Market.

Chile is projected to grow at a 20.67% CAGR through 2031, the fastest rate among regional countries and a clear driver of growth in the South America AI-powered Energy Management Software Market. Its momentum comes from mandatory reporting under the Energy Efficiency Law, strong renewable energy penetration, and a mining sector already comfortable with digital operations. ABB’s 2026 regional strategy also positioned Chile as a digital hub for energy transition projects, which supported the country’s role as a launch market for software and edge solutions. The rest of South America remains earlier in adoption, but smart meter plans and grid modernization work in smaller markets still widen the long-run addressable base.

Competitive Landscape

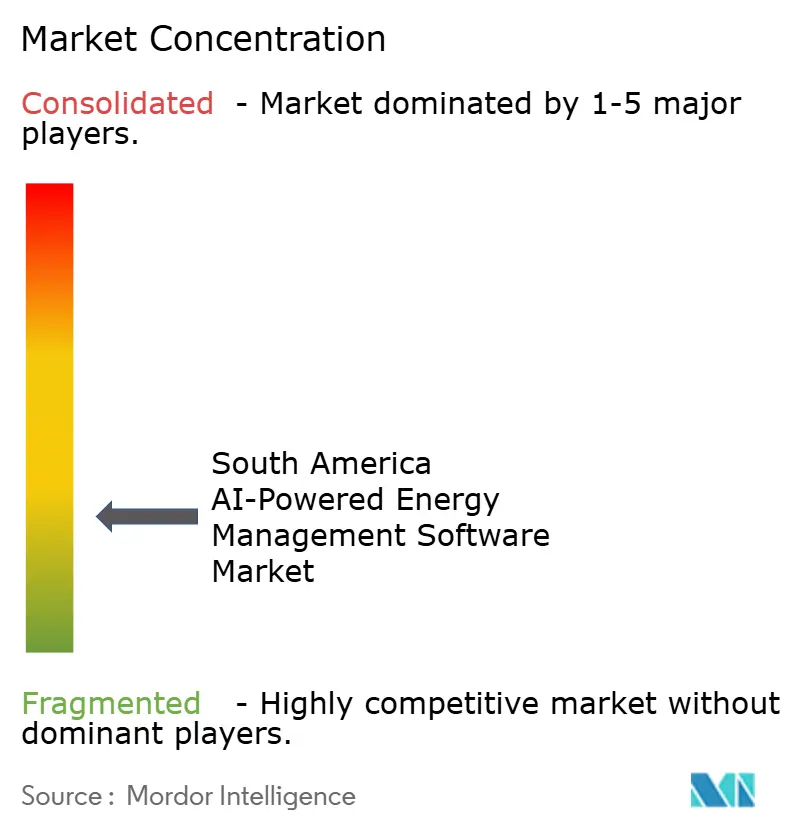

The South America AI-powered Energy Management Software Market remained fragmented in 2025, with ABB Ltd., Schneider Electric SE, and Siemens AG together holding a dominating share of revenue. Their strength comes from installed OT bases, utility relationships, and the ability to bundle software, services, and hardware, along with long contract terms, into a single offer. Schneider Electric strengthened its distributed energy and grid management position through the acquisition of AutoGrid Systems, which expanded the scope of its end-to-end platform in the region. Siemens used its CPFL Energia partnership to deepen its meter data management presence in Brazil, while ABB continued to build industrial stickiness through product updates and local manufacturing support. This structure gives incumbents an edge when buyers want a single supplier to handle integration, cybersecurity, reporting, and ongoing optimization.

The competitive landscape is not closed, as AI-focused specialists are still finding openings at the application layer in the South America AI-powered Energy Management Software Market. C3 AI expanded across Eletrobras’ transmission assets after its pilot phase, which showed that a focused software vendor can win where the customer already has scale and technical capacity. Stem entered its first South America utility-scale PowerTrack EMS project in Chile, which showed that renewable and storage projects can support challenger entry points. Bidgely’s acquisition of Grid4C also signaled wider global competition in utility-side analytics, fault detection, load forecasting, and distributed energy resource forecasting.

White space is strongest in the mid-market industrial base, where many manufacturers, agribusiness processors, and commercial property operators still fall short of the engagement size targeted by large incumbents. A second opening sits in energy trading and market intelligence software, especially in Chile, Colombia, and Brazil, where market liberalization is increasing the need for tools that connect weather, operating, and settlement data. Vendors that arrive with stronger local integrations with grid operator systems can move faster than those that offer only generic analytics. The South America AI-powered Energy Management Software Market, therefore, supports a stable incumbent core, but it still leaves room for specialists who solve a narrow operational problem better than a bundled platform.

South America AI-powered Energy Management Software Industry Leaders

Schneider Electric SE

Siemens AG

ABB Ltd.

Honeywell International Inc.

Johnson Controls International plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Vale inaugurated its first AI-powered ore processing plant at the Conceição 2 unit in Itabira, Minas Gerais, integrating AI to optimize more than 400 production variables and achieving a 25% productivity gain against the 2024 baseline. With a processing capacity of 11.2 million tons per year, the facility serves as a replication template for Vale’s other South American operations, directly raising the ROI benchmark for industrial AI energy management deployments across the region.

- May 2026: Stem Inc. deployed its PowerTrack Energy Management System at the Granja Solar project in Chile, the company’s first South American utility-scale EMS installation. PowerTrack serves as the master control system for the 135 MW PV plant undergoing a 420 MWh battery storage retrofit, with Copec Flux providing local EPC and O and M support. The companies indicated plans to extend the delivery model to additional projects in Chile and Colombia.

- May 2026: Brazil’s National Electric System Operator deployed the AVEVA PI System to automate real-time energy dispatch, integrating it with proprietary operational tools GERIN and SINapse. The platform monitors 12 processes across 4 operational centers in Brasília, Recife, Rio de Janeiro, and Florianópolis, reducing energy waste and improving renewable source utilization in the national grid.

- April 2026: ABB Ltd. integrated Generative AI capabilities into the ABB Ability Energy Management System via the ABB Ability Industrial Knowledge Vault, enabling natural-language queries on energy consumption, emissions, and equipment performance. The product targets mining, pulp and paper, metals, and cement industries across South America, accelerating operational insight without additional analyst headcount.

South America AI-powered Energy Management Software Market Report Scope

The South America AI-powered Energy Management Software Market refers to platforms and services that leverage artificial intelligence to optimize energy consumption, enhance asset performance, and enable smarter grid and distributed energy resource (DER) management across the region. These solutions provide advanced capabilities, including predictive maintenance, renewable energy forecasting, demand-side optimization, and market intelligence for energy trading and pricing.

The South America AI-powered Energy Management Software Market report is segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings), and Geography (Brazil, Argentina, Chile, Colombia, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Rest of South America |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings | |

| By Geography | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America |

Key Questions Answered in the Report

What is the size of the South America AI-powered Energy Management Software Market?

The South America AI-powered Energy Management Software Market was valued at USD 130.1 million in 2025 and estimated to grow from USD 160.2 million in 2026 to reach USD 400.1 million by 2031, at a CAGR of 20.09% during the forecast period 2026-2031

Which component leads regional revenue?

Software led with 71.19% share in 2025 because buyers need integrated forecasting, reporting, anomaly detection, and regulatory support in one platform.

Which deployment model is growing the fastest in South America?

Hybrid deployment is projected to grow at a 20.34% CAGR through 2031 as remote sites need edge control and enterprise users still want cloud analytics.

What is the largest application area for AI-powered energy management software in South America?

Energy consumption and demand optimization held the largest share at 25.16% in 2025, supported by tariff management, demand response, and benchmarking use cases.

Which end-user group is expanding the quickest?

Industrial facilities are projected to grow at a 20.58% CAGR through 2031 as mining, manufacturing, cement, and metals users tie energy management more closely to operations and compliance.

Which country is leading adoption and which one is growing the fastest?

Brazil led with 39.11% share in 2025 because of its utility scale and regulatory push, while Chile is projected to grow the fastest at a 20.67% CAGR through 2031.

Page last updated on: