ASEAN AI-powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

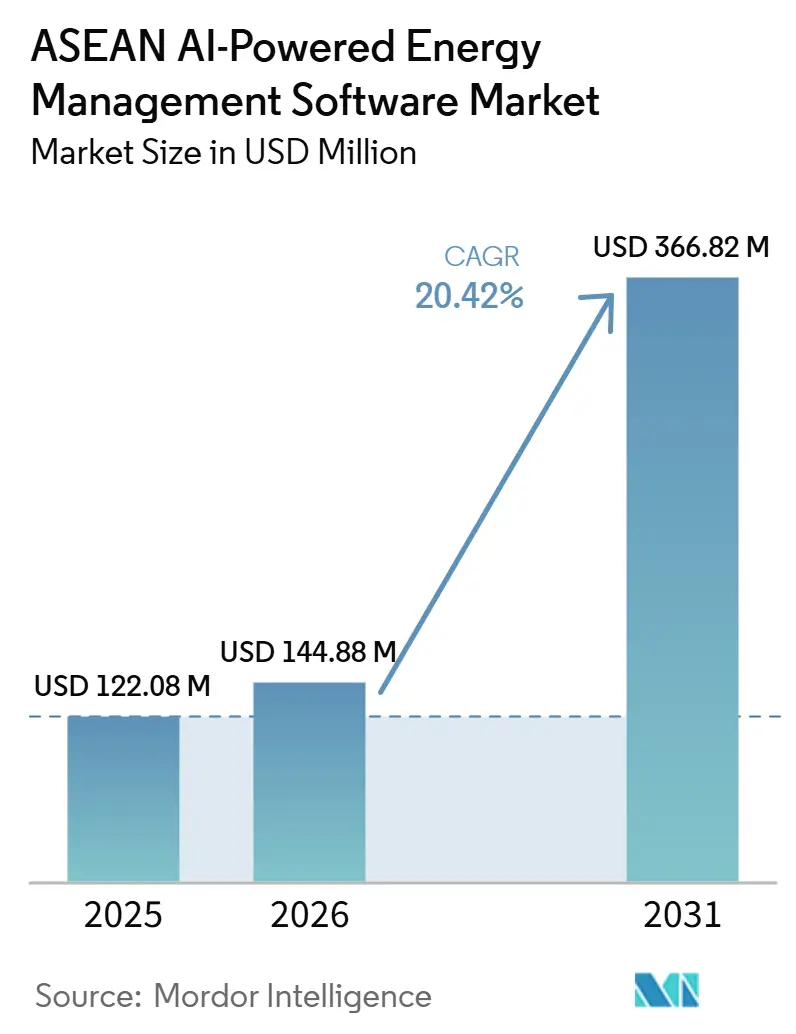

| Base Year Market Size (2025) | USD 122.08 Million |

| Market Size (2026) | USD 144.88 Million |

| Market Size (2031) | USD 366.82 Million |

| Growth Rate (2026 - 2031) | 20.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN AI-powered Energy Management Software Market Analysis by Mordor Intelligence

The ASEAN AI-powered Energy Management Software Market size is expected to grow from USD 122.08 million in 2025 to USD 144.88 million in 2026 and is forecast to reach USD 366.82 million by 2031 at 20.42% CAGR over 2026-2031. Electricity demand is rising faster than many existing systems were built to handle, pushing energy control software into core operating budgets rather than optional efficiency spending. Fast data center expansion is adding another layer of pressure, as operators need tighter control over cooling loads, power quality, and site-level energy use. Regional policy is also giving buyers greater confidence to move forward, as energy-intensity reduction goals and national efficiency programs are becoming harder to ignore. At the same time, software adoption still depends on how well vendors can work with older building and grid control systems, which keeps implementation capability as important as analytics quality. The ASEAN AI-powered Energy Management Software Market is therefore growing on the back of energy cost pressure, grid stress, stricter compliance needs, and vendor strategies that focus on integration support and measurable payback.

Key Report Takeaways

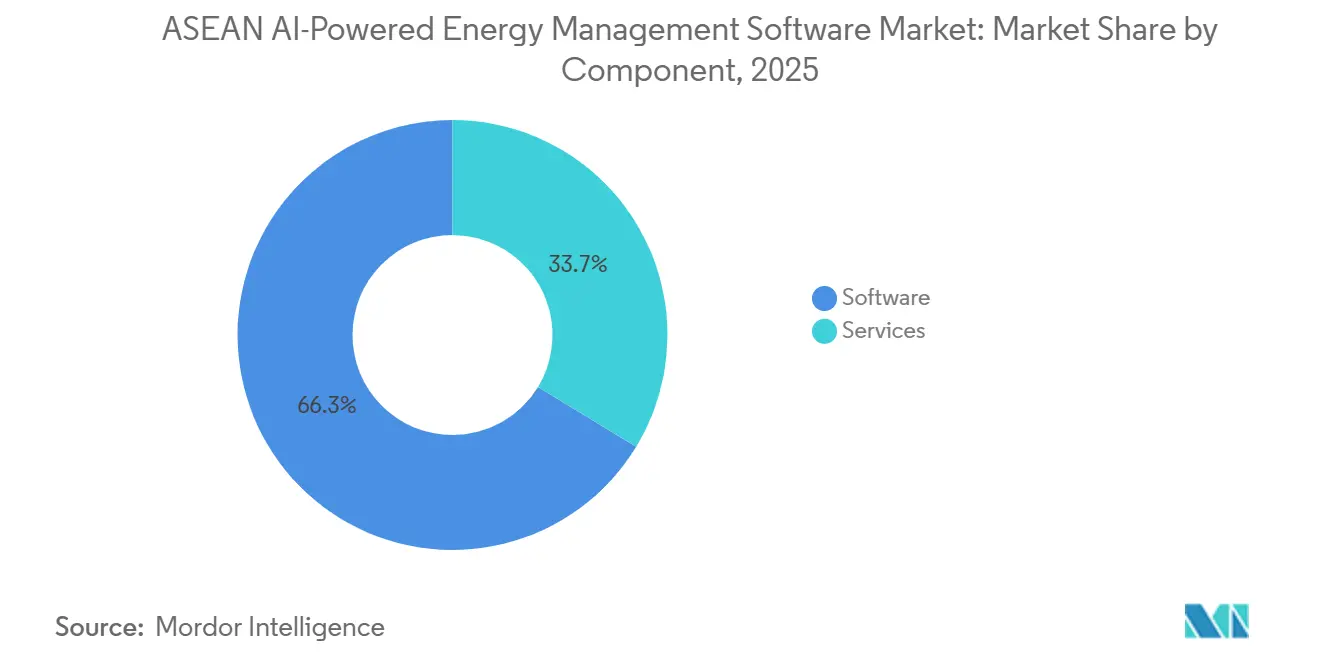

- By component, software accounted for 66.31% of the ASEAN AI-powered Energy Management Software Market in 2025, while services are projected to expand at a 23.81% CAGR through 2031.

- By deployment mode, cloud-based solutions held 61.45% of the ASEAN Artificial Intelligence Powered Energy Management Software (EMS) Market in 2025, while hybrid deployment is projected to grow at a 23.48% CAGR through 2031.

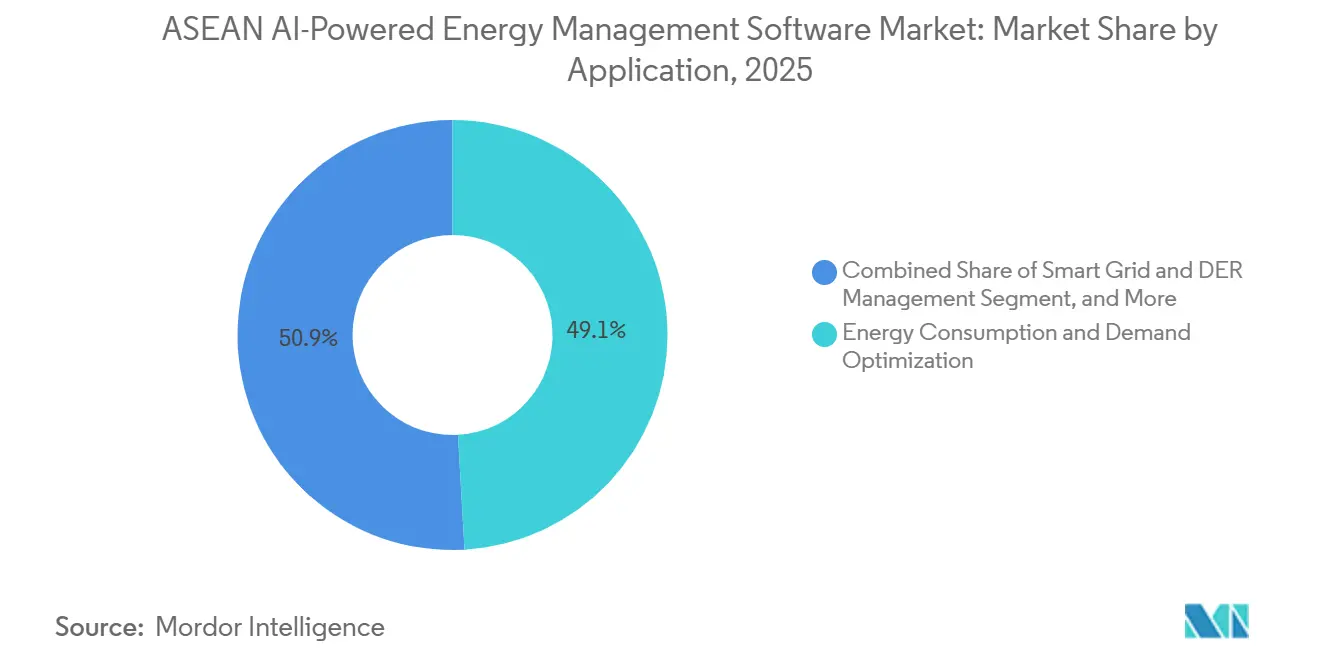

- By application, energy consumption and demand optimization accounted for 49.12% of the ASEAN Artificial Intelligence Powered EMS Market in 2025, while renewable energy forecasting and integration are projected to advance at a 22.67% CAGR through 2031.

- By end user, commercial buildings represented 56.47% of the ASEAN Artificial Intelligence Powered Energy Management Software Market in 2025, while utilities are projected to expand at a 23.05% CAGR through 2031.

- By geography, Indonesia held 31.29% of the ASEAN AI-powered Energy Management Software Market share in 2025, while Vietnam is projected to expand at a 22.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

ASEAN AI-powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Energy Costs and Peak Load Volatility | +3.5% | Global, highest in Singapore, Thailand, Philippines | Short term (≤ 2 years) |

| Accelerated Smart Building Retrofits in ASEAN Urban Clusters | +3.0% | Singapore, Indonesia, Malaysia, Thailand, Vietnam | Medium term (2-4 years) |

| Government Incentives for Energy Efficiency and Digitalization | +2.8% | Malaysia, Thailand, Vietnam, Indonesia | Medium term (2-4 years) |

| AI-Enabled Load Optimization Across Multi-Site Portfolios | +2.5% | Singapore, Malaysia, Indonesia | Medium term (2-4 years) |

| Growth of Distributed Energy Resources and Battery Integration | +2.0% | Philippines, Vietnam, Indonesia, Thailand | Long term (≥ 4 years) |

| Demand for Continuous Compliance Reporting and ESG Traceability | +1.8% | Singapore, Malaysia, Indonesia, Vietnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Energy Costs and Peak Load Volatility

Power price volatility has pushed energy software to the forefront of day-to-day cost control across the ASEAN AI-powered Energy Management Software Market. The International Energy Agency said Southeast Asia’s electricity demand is projected to rise by 4% annually to 2035, which keeps pressure on utilities and large users to manage load more precisely. When demand rises this quickly, buyers pay more attention to tariff exposure, peak demand charges, and sub-hourly scheduling than they did a few years ago. That changes procurement behavior because software is now expected to reduce billing volatility, not just trim annual consumption. APAEC 2026-2030 also set a target to reduce ASEAN energy intensity by 40% by 2030 relative to 2005 levels, which adds policy weight to tighter energy controls. In the ASEAN Artificial Intelligence Powered Energy Management Software Market, vendors with strong load management and reporting tools are therefore finding a more direct path into budget approval.

Accelerated Smart Building Retrofits in ASEAN Urban Clusters

Retrofit activity in commercial properties remains one of the clearest demand channels for the ASEAN AI-powered Energy Management Software Market. Siemens launched Building X for ASEAN in March 2025 and used True Digital Park in Bangkok as an early reference site for cloud-based building optimization. Siemens said the deployment enabled real-time monitoring and AI-driven optimization of temperature, humidity, and energy parameters, with a typical return on investment of under 1 year for participating buildings. This matters because many property owners want staged upgrades that improve performance without forcing a full replacement of older site controls. The ASEAN Center for Energy said ESCO models can bundle audits, financing, installation, and measurement, thereby reducing the burden on owners who lack internal implementation capacity. That combination of retrofit demand and delivery support keeps existing buildings at the center of near-term software adoption.

Government Incentives for Energy Efficiency and Digitalization

Regulation is becoming a steadier demand driver across the ASEAN AI-powered Energy Management Software Market. The ASEAN Centre for Energy reported that Malaysia’s Energy Efficiency and Conservation Act and Thailand’s Energy Efficiency Plan 2024 strengthened the case for energy management systems and digital tools in large facilities. The same source noted that Thailand combines mandatory standards with ENCON Fund support and Board of Investment tax incentives for IoT, big data, and AI-based efficiency solutions. In Vietnam, the National Assembly reviewed revisions to the law on economical and efficient use of energy in June 2026 and called for stronger digital transformation in energy auditing and monitoring. APAEC 2026-2030 ties these national efforts into a common regional direction through its energy intensity target. This policy mix gives vendors a more dependable demand floor than voluntary efficiency messaging alone.

AI-Enabled Load Optimization Across Multi-Site Portfolios

Large organizations are moving beyond single-site pilots, and that is changing buying behavior across the ASEAN AI-powered Energy Management Software Market. Siemens reinforced this shift in June 2026, signing MoUs in Indonesia with PT Accenture Indonesia, PT PLN Enjiniring, and Telkomsel during Tech Summit 2026. Johnson Controls showed the same direction in Jakarta, where OpenBlue and Metasys at Thamrin Nine delivered up to 30% energy savings and cut cooling and lighting costs by 20%. These examples matter because portfolio owners want a single platform that can learn across multiple sites and support repeatable workflows. They also favor vendors that can combine analytics, control integration, and field support under a single commercial relationship. As a result, the ASEAN AI-powered Energy Management Software Market is rewarding suppliers that can scale software performance and local delivery simultaneously.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity with Legacy BMS and SCADA | -3.2% | Indonesia, Thailand, Philippines | Short term (≤ 2 years) |

| Limited Availability of Skilled Energy Data and AI Specialists | -2.5% | Vietnam, Philippines, Indonesia | Medium term (2-4 years) |

| Data Sovereignty and Cybersecurity Concerns for Cloud Deployment | -1.8% | Indonesia, Vietnam, Malaysia | Medium term (2-4 years) |

| Uneven Digitization Across ASEAN Commercial and Industrial Assets | -1.2% | Philippines, Vietnam tier-2 cities, Rest of ASEAN | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity With Legacy BMS and SCADA

Integration with older building and grid control systems remains the most immediate barrier in the ASEAN AI-powered Energy Management Software Market. Many brownfield assets still operate with separate systems for HVAC, lighting, metering, and plant controls, and those systems were not built to cleanly exchange data. That weak data flow reduces the quality of AI recommendations and extends testing, commissioning, and troubleshooting time. The ASEAN Centre for Energy said ESCO-led retrofits can combine audits, financing, installation, and verification, but older assets still require careful site-level design before software can perform consistently. Buyers, therefore, look for short payback, proven interoperability, and clear implementation support before expanding beyond initial sites. This slows adoption most in mid-tier commercial properties where energy use is meaningful but technical budgets remain limited.

Limited Availability of Skilled Energy Data and AI Specialists

The shortage of workers who understand both energy systems and AI is also slowing delivery in the ASEAN AI-powered Energy Management Software Market. The Singapore Economic Development Board said Southeast Asia still faces shortages in mid-level and senior AI roles, especially for complex initiatives that need strong technical judgment.[1]Singapore Economic Development Board, “Unlocking Southeast Asia’s AI Potential, Opportunities for Growth and Innovation,” Singapore Economic Development Board, edb.gov.sg The same report said that fragmented infrastructure and legacy systems make scalable AI deployment harder, underscoring the importance of experienced teams. When customers lack internal expertise, deployments depend more heavily on vendor service teams and require longer operator training. That raises suppliers' delivery costs and delays the point at which customers can see measurable savings. Vendors that package software with managed support are, therefore, better placed to convert interest into steady use.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Anchors Deployment, Services Fuel Expansion

Software accounted for 66.31% of the ASEAN AI-powered Energy Management Software Market in 2025, making it the primary focus for customers seeking visibility across multiple sites. Buyers usually started with analytics, dashboards, and reporting because those tools created a usable data layer before deeper automation work began. This ordering mattered because the first platform choice often shaped later integration, workflow, and renewal decisions. In the ASEAN AI-powered Energy Management Software Market, software also benefited from cloud delivery models that enabled vendors to update functionality without rebuilding site infrastructure. The segment led in 2025 because it delivered direct operational value and also acted as the gateway to broader digital energy programs.

Services are projected to expand at a 23.81% CAGR through 2031, the fastest pace within this segmentation. That growth reflects the significant support many customers still need for integration, commissioning, training, and change management. The ASEAN Center for Energy said ESCO providers in ASEAN can combine audits, financing, installation, and measurement and verification, thereby reducing the execution burden for building owners.[2]ASEAN Centre for Energy, “Enabling Energy Service Company ESCO Market for ASEAN’s Low-Carbon Buildings Transition,” ASEAN Centre for Energy, aseanenergy.org This service layer matters because AI tools only perform well when meters, controls, and operating schedules are reliably connected. Services are therefore set to grow faster than software, even though software will remain the larger revenue pool across the forecast period.

By Deployment Mode: Cloud Leads, Hybrid Reshapes the Architecture

Cloud-based solutions held 61.45% of the ASEAN AI-powered Energy Management Software Market share in 2025, which showed that scalability and lower upfront infrastructure costs remained the strongest buying priorities. Cloud deployment lets organizations activate monitoring, reporting, and software updates across dispersed portfolios without building separate local server environments at each site. Siemens gave the region a visible example when it launched Building X for ASEAN in March 2025. That launch mattered because commercial operators wanted faster rollout, lighter upkeep, and clearer paths to remote optimization. Cloud, therefore, remained the default choice for new multi-site building portfolios in 2025.

Hybrid deployment is projected to grow at a 23.48% CAGR through 2031, the fastest rate in this grouping. Utilities and industrial operators often keep time-sensitive control functions on site while shifting wider analytics and reporting to cloud environments. This structure suits facilities that need to balance uptime, internal approval rules, and operational risk. It also gives vendors a practical route into markets where data handling expectations remain strict or unsettled. As the ASEAN AI-powered Energy Management Software Market matures, hybrid design is likely to gain more ground in industrial and grid-facing use cases.

By Application: Demand Optimization Leads While Renewable Integration Accelerates

Energy consumption and demand optimization accounted for 49.12% share of the ASEAN AI-powered Energy Management Software Market size in 2025, making it the first use case most customers adopted. The reason was straightforward: buyers could see direct value when peak demand, equipment schedules, and energy waste were better managed. This application also created the baseline data that later supported predictive maintenance, DER control, and compliance workflows. In the ASEAN AI-powered Energy Management Software Market, demand optimization remained the easiest entry point for commercial portfolios, factories, and power-dense sites. Its lead in 2025 reflected both immediate savings and broad relevance across end users.

Renewable energy forecasting and integration is projected to advance at a 22.67% CAGR through 2031, the fastest rate among applications. The International Energy Agency said the ASEAN Power Grid initiative requires USD 27 billion in cross-border interconnection investment through 2040, underscoring the scale of the grid modernization still underway. As more variable generation and distributed resources enter local systems, utilities and large operators need stronger forecasting and balancing tools. This creates room for AI software that can improve planning before storage deployment and network reinforcement fully catch up. The result is a faster growth path for renewable integration applications within the ASEAN AI-powered Energy Management Software Market.

By End User: Commercial Buildings Dominate, Utilities Lead Growth

Commercial buildings accounted for 56.47% of end-user demand in 2025, keeping them at the center of the ASEAN AI-powered Energy Management Software Market. Office towers, hotels, retail centers, and mixed-use properties offer clear savings cases because occupancy levels and cooling loads change throughout the day. Vendors also favor this segment because one successful project can often be repeated across a larger property portfolio. Johnson Controls demonstrated this in Jakarta, where OpenBlue and Metasys at Thamrin Nine delivered up to 30% energy savings and cut cooling and lighting costs by 20%. That kind of reference project supports continued adoption among owners who want proof before expanding site by site.

Utilities are projected to expand at a 23.05% CAGR through 2031, making them the fastest-growing end user group. The International Energy Agency said Southeast Asia’s electricity demand is projected to rise by 4% annually to 2035, underscoring the need for stronger forecasting, dispatch support, and system-balancing tools. APAEC 2026-2030 also formalized a regional target to reduce energy intensity by 40% by 2030, which adds pressure on power systems to manage supply and demand more intelligently. Utility contracts are often larger and longer than building-level software deals, so even a smaller installed base can create strong revenue growth. This is why utilities are set to generate the fastest incremental expansion within the ASEAN AI-powered Energy Management Software Market.

Geography Analysis

Indonesia held 31.29% of the ASEAN AI-powered Energy Management Software Market in 2025, the largest country share in the region. Its lead came from a large commercial property base, rising digital energy management needs, and growing attention from global vendors. Siemens treated Indonesia as a core execution market in June 2026 when it signed MoUs with PT Accenture Indonesia, PT PLN Enjiniring, and Telkomsel during Tech Summit 2026.[3]Siemens, “Siemens Tech Summit 2026 Accelerates Indonesia Digital and Green Transformation,” Siemens, news.siemens.com Johnson Controls also used Jakarta’s Thamrin Nine as a reference site, where AI-led control delivered up to 30% energy savings and cut cooling and lighting costs by 20%. These moves show that major suppliers now view Indonesia as a scaling market for commercial building and wider digital-energy programs.

Vietnam is projected to expand at a 22.14% CAGR through 2031, the fastest rate among ASEAN countries, and it is taking a larger role in the ASEAN AI-powered Energy Management Software Market. The country’s legislative review in June 2026 called for stronger digital transformation in energy auditing and monitoring, which supports a more formal adoption path for software tools. Industrial zone growth is also expanding the customer base, as more factories need structured monitoring and load control as power use rises. The Philippines remains important for the next wave of renewable and distributed resource management, even though its installed base is smaller than Indonesia’s. Together, Vietnam and the Philippines form a strong growth corridor for forecasting, load balancing, and digital compliance applications.

Singapore remains the region’s technology validation hub, and Johnson Controls said data centers there consume 7% of national electricity and could reach 12% by 2030, which strengthens the case for advanced optimization tools. Malaysia offers a supportive setting for the ASEAN AI-powered Energy Management Software Market, while Thailand continues to back digital efficiency adoption through the Energy Efficiency Plan 2024, ENCON Fund support, and Board of Investment tax incentives. Thailand also gained an early commercial reference case when Siemens launched Building X at True Digital Park in Bangkok in March 2025. The rest of ASEAN remains earlier in adoption, but regional coordination under APAEC 2026-2030 still creates a common direction for future software demand.

Competitive Landscape

The ASEAN AI-powered Energy Management Software Market remains moderately concentrated, with several global incumbents benefiting from installed control systems, service reach, and long enterprise relationships. Schneider Electric, Siemens, Honeywell, and Johnson Controls entered many accounts through building automation, controls, and energy management stacks already embedded on customer sites. This gave them a practical edge because software selection often followed the vendor that already understood the building or plant environment. At the same time, local and regional specialists competed by offering lighter integration layers, managed services, and faster customization for ASEAN operating conditions. The main contest, therefore, centered on interoperability, execution speed, and proof of savings rather than on analytics features alone.

Siemens used 2 moves to strengthen its position: launching Building X for ASEAN in March 2025, followed by signing multi-party MoUs in Indonesia in June 2026 to deepen digital-energy execution. Johnson Controls followed a similar path by expanding its Singapore Innovation Centre with a USD 60 million five-year commitment and by turning Thamrin Nine into a live ASEAN reference site for OpenBlue and Metasys.[4]Johnson Controls, “Johnson Controls Helps Cut Energy Use at Jakarta’s Thamrin Nine,” Johnson Controls, johnsoncontrols.com These actions mattered because buyers in the ASEAN AI-powered Energy Management Software Market usually wanted both reg could keep paceional support depth and local proof before committing to broader rollouts. Vendor strategy also continued to shift toward outcome-based service models, which could ease buyer concerns about integration work and staffing constraints. That approach was especially relevant in commercial real estate and data center projects where performance guarantees carried more weight than software license labels.

White space remained strongest in mid-market buildings, renewable forecasting, DER orchestration, and automated compliance reporting, where buyer needs were growing faster than legacy delivery models. Emerging ASEAN platforms such as Esave.ai, AIOTKU, EcoXplore, ENX Systems, and Tanand Technology used local deployment support and regulatory familiarity to compete for these openings. The AJEEP Sustainable ASEAN Energy Management Certification Scheme could also shape procurement criteria once finalized, as standardized energy management requirements often favor vendors that can map software outputs to formal reporting requirements. The competitive balance in the ASEAN Artificial Intelligence Powered Energy Management Software Market is therefore likely to remain open, even as global incumbents maintain the strongest installed base.

ASEAN AI-powered Energy Management Software Industry Leaders

Schneider Electric SE

Siemens AG

Honeywell International Inc.

IBM Corporation

Cisco Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Siemens officially launched the Siemens Tech Summit 2026 (STS26) in Jakarta, signing strategic memorandums of understanding (MoUs) with PT Accenture Indonesia, PT PLN Enjiniring, and PT Telekomunikasi Selular (Telkomsel) to accelerate Indonesia's industrial digitalization and energy transition through integrated OT/IT, AI-driven platforms, IoT integration, and power engineering capacity-building initiatives spanning the utility and commercial building sectors.

- May 2026: Johnson Controls deployed its OpenBlue AI-powered ecosystem and Metasys Building Management System at Jakarta's Thamrin Nine complex, achieving up to 30% energy savings and approximately 20% reduction in cooling and lighting costs, the company's first chiller plant optimization deployment in Indonesia, through real-time predictive control that analyzes occupancy, weather, and demand patterns.

- May 2026: Schneider Electric announced plans to open a Southeast Asian training center in Malaysia, dedicated to developing technical skills among partners and end users for energy management systems spanning medium-voltage applications and data center solutions, in response to growing AI infrastructure investments across the region that are intensifying energy management requirements.

- January 2026: Johnson Controls committed USD 60 million over five years to expand its Innovation Centre in Singapore, adding 90-100 engineering roles focused on next-generation thermal management, advanced cooling strategies, and AI-powered data center energy solutions, supported by the Singapore Economic Development Board.

ASEAN AI-powered Energy Management Software Market Report Scope

The ASEAN AI-powered Energy Management Software Market encompasses intelligent software platforms that Southeast Asian nations are increasingly turning to to optimize energy consumption. These intelligent solutions not only forecast demand and assess asset performance but also seamlessly integrate renewable energy systems, all within the backdrop of rapidly industrializing and urbanizing landscapes. The market's expansion is spurred by rising energy demand, rapid industrialization, and proactive government initiatives that champion both sustainability and digital transformation. With AI at the helm, organizations are not just slashing operational costs and boosting efficiency but are also ensuring compliance with stringent environmental regulations. As smart infrastructure expands and cloud adoption surges, the region's embrace of energy management technologies becomes ever more pronounced across diverse industries.

The ASEAN AI‑Powered Energy Management Software Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud‑Based, On‑Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings), and Geography (Singapore, Indonesia, Malaysia, Philippines, Thailand, Vietnam, and Rest of ASEAN). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| Singapore |

| Indonesia |

| Malaysia |

| Philippines |

| Thailand |

| Vietnam |

| Rest of ASEAN |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings | |

| By Geography | Singapore |

| Indonesia | |

| Malaysia | |

| Philippines | |

| Thailand | |

| Vietnam | |

| Rest of ASEAN |

Key Questions Answered in the Report

What is the size outlook for ASEAN AI-Powered Energy Management Software?

The ASEAN AI-powered Energy Management Software Market was valued at USD 122.08 million in 2025, stood at USD 144.88 million in 2026, and is forecast to reach USD 366.82 million by 2031 at a 20.42% CAGR.

Which country leads software adoption across Southeast Asia?

Indonesia held the largest country share at 31.29% in 2025, supported by a large commercial building base and visible deployments from major global vendors.

Which end-user group is creating the strongest near-term revenue base?

Commercial buildings led demand with 56.47% share in 2025 because office, retail, hospitality, and mixed-use sites offer clear and repeatable savings cases.

Where is the fastest growth likely to come from through 2031?

Vietnam is projected to record the fastest country growth at 22.14% CAGR, while utilities are projected to be the fastest-growing end-user group at 23.05% CAGR.

Why are cloud and hybrid deployments both gaining traction?

Cloud led with 61.45% share in 2025 because it scales quickly and lowers upfront infrastructure needs, while hybrid is growing faster at 23.48% CAGR because industrial and utility users still need local control for critical operations.

What is the main barrier slowing wider rollout across ASEAN?

The biggest challenge remains integration with legacy BMS and SCADA systems, followed by a shortage of professionals who can combine energy domain knowledge with AI deployment skills.

Page last updated on: