Singapore AI-powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

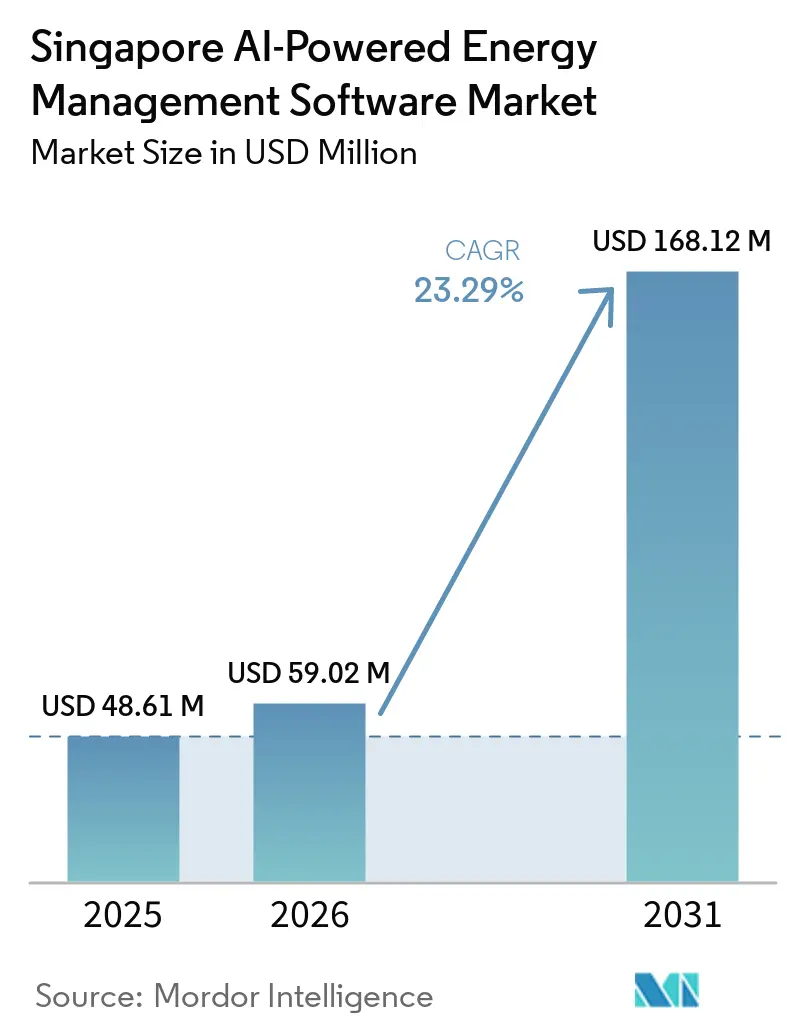

| Base Year Market Size (2025) | USD 48.61 Million |

| Market Size (2026) | USD 59.02 Million |

| Market Size (2031) | USD 168.12 Million |

| Growth Rate (2026 - 2031) | 23.29% CAGR |

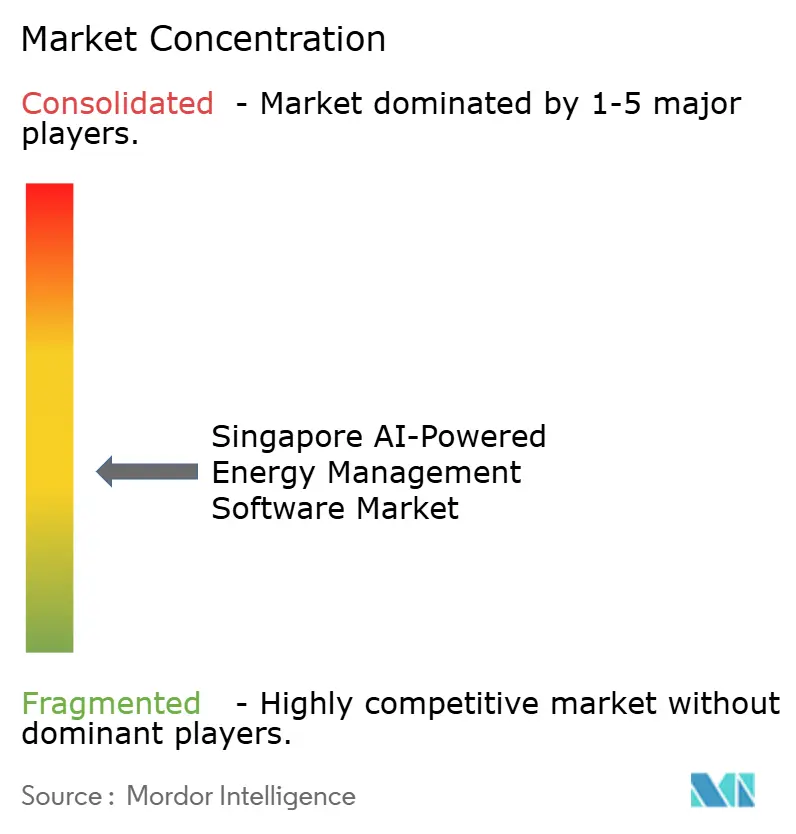

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore AI-powered Energy Management Software Market Analysis by Mordor Intelligence

The Singapore AI-powered Energy Management Software Market size was valued at USD 48.61 million in 2025 and is estimated to grow from USD 59.02 million in 2026 to reach USD 168.12 million by 2031, at a CAGR of 23.29% during the forecast period (2026-2031). The carbon tax increase to SGD 45/tCO₂e in 2026 is making it easier to justify energy optimization software by shortening the payback period for continuous monitoring and control. The Green Building Masterplan and the Mandatory Energy Improvement regime have also moved this software closer to a compliance requirement for many commercial and institutional building owners. Demand is no longer coming only from facilities teams, as finance, sustainability, and real estate functions now need a single system that supports reporting, optimization, and audit readiness. The competitive focus is also changing, with vendors under pressure to unify mixed-vendor building systems and convert operating data into audit-ready ESG outputs. A further opening is developing around virtual power plant participation, where buyers who choose platforms with distributed energy resource orchestration can position buildings as revenue-generating grid assets rather than treating energy management solely as a cost-control function.

Key Report Takeaways

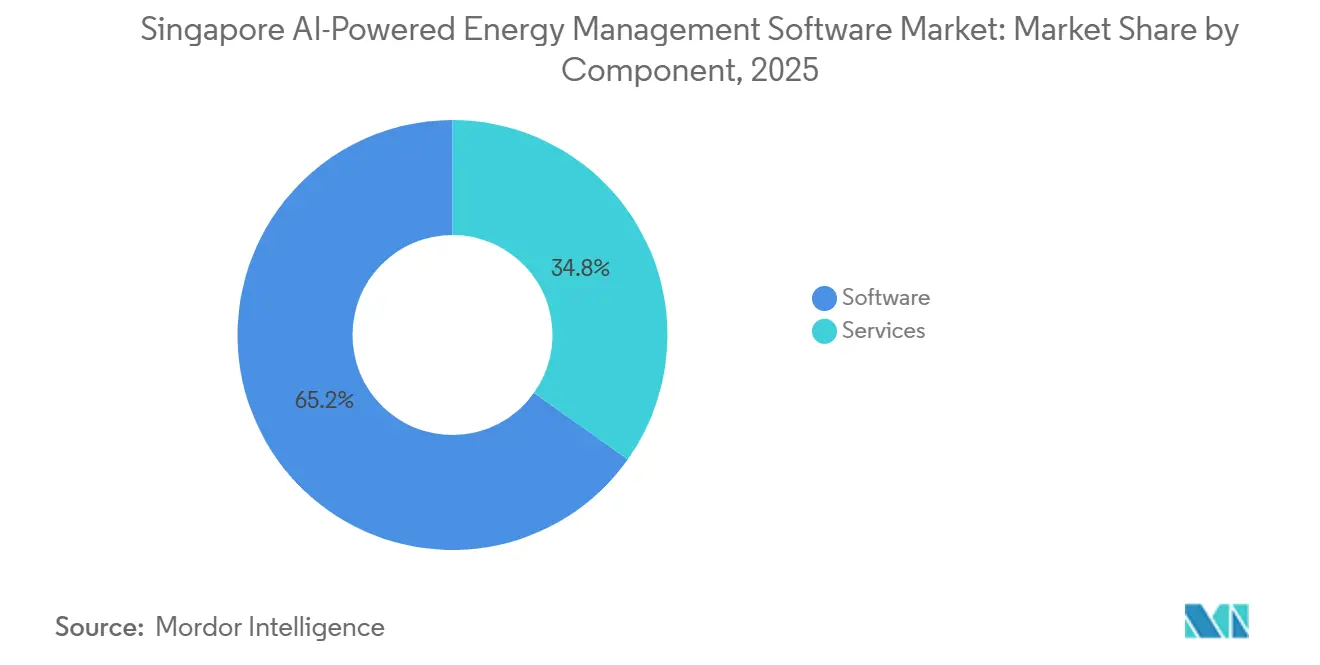

- By component, software held 65.18% of revenue in 2025, while services are projected to expand at a 24.31% CAGR through 2031 in the Singapore AI-powered Energy Management Software Market.

- By deployment mode, cloud-based solutions accounted for 55.14% of the market share in 2025, while hybrid deployment is expected to record the fastest CAGR of 24.42% through 2031.

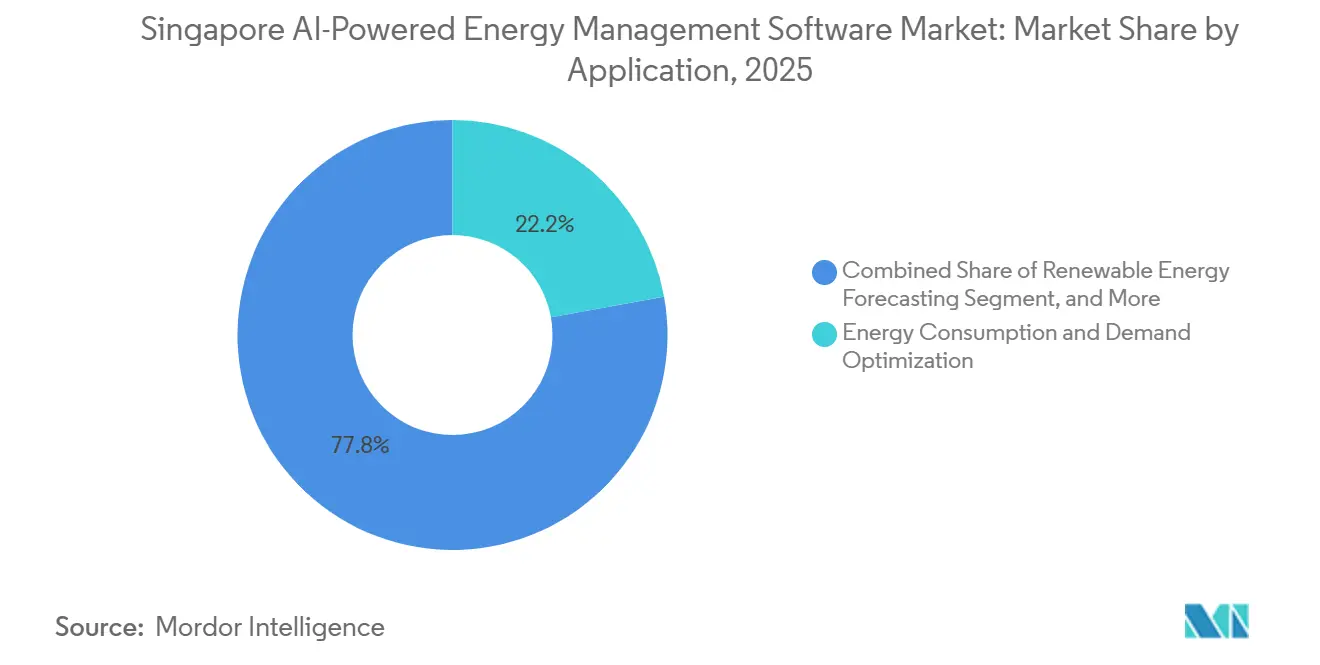

- By application, Energy Consumption and Demand Optimization accounted for 22.16% of the market in 2025, while Renewable Energy Forecasting and Integration is projected to expand at a 24.53% CAGR through 2031.

- By end user, utilities held 36.11% share of the Singapore AI-powered Energy Management Software Market in 2025, while industrial facilities are expected to grow at the fastest CAGR of 24.64% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore AI-powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Smart Building Retrofits in Singapore Commercial Real Estate | +5.2% | Singapore-wide, concentrated in CBD, Marina Bay, Orchard Road, and Jurong Lake District | Short term (≤ 2 years) |

| Tightening Corporate Energy Reporting and ESG Disclosure Requirements | +4.8% | Singapore-wide, most immediate among STI constituent listed companies and large non-listed companies | Short term (≤ 2 years) |

| Accelerating Utility Tariff Optimization and Demand Charge Management | +4.1% | Singapore-wide, with high intensity in data center clusters in Jurong and Woodlands, and industrial zones in Tuas | Medium term (2-4 years) |

| AI-Enabled Fault Detection, Diagnostics, and Predictive Control Adoption | +3.7% | Singapore-wide, concentrated in commercial buildings, healthcare facilities, and data centers | Medium term (2-4 years) |

| Edge-Connected IoT Metering and Building Management System Integration | +2.9% | Singapore-wide, strongest uptake in Punggol Digital District and newly commissioned commercial developments | Medium term (2-4 years) |

| Growing Enterprise Preference for Continuous Commissioning and Autonomous Optimization | +2.4% | Singapore-wide, accelerating in healthcare, education, and hospitality verticals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Smart Building Retrofits in Singapore Commercial Real Estate

The Green Mark Incentive Scheme for Existing Buildings 2.0, a SGD 63 million (USD 46 million) program, lowered the financial barrier to retrofitting in privately owned buildings with a gross floor area above 5,000 m².[1]Building and Construction Authority, “Green Mark Incentive Scheme for Existing Buildings 2.0,” Building and Construction Authority, bca.gov.sg That directly widened the deployment base for the Singapore AI-powered Energy Management Software Market because more older buildings are now being fitted with the controls and metering needed for AI optimization. The Mandatory Energy Improvement regime also began to require action when energy-intensive buildings exceeded Energy Use Intensity thresholds for three consecutive years, pushing owners toward structured upgrade programs. These retrofit programs often require granular submetering, and that data layer lowers integration costs later when AI software is added on top. The effect is especially visible in hospitality and healthcare, where owners are trying to meet compliance, Green Mark recertification, and investor reporting needs within the same capital cycle.

Tightening Corporate Energy Reporting and ESG Disclosure Requirements

Mandatory climate reporting is moving energy data from a facilities issue into a finance and governance issue in Singapore.[2]Accounting and Corporate Regulatory Authority, “Sustainability Reporting and Assurance Requirements Timeline,” Accounting and Corporate Regulatory Authority, acra.gov.sg SGX-listed companies must report Scope 1 and Scope 2 emissions from the financial year 2025, and STI constituents must also report Scope 3 emissions from FY2026. That shift is driving demand for continuous, audit-ready energy data because periodic manual readings do not provide the consistency reporting teams now need. The carbon tax increase from SGD 25/tCO₂e in 2024-2025 to SGD 45/tCO₂e in 2026 is also making the business case more direct for finance teams that are deciding where to allocate spending. In the Singapore AI-powered Energy Management Software Market, this policy stack is aligning facilities, finance, and sustainability functions around a single software decision.

Accelerating Utility Tariff Optimization and Demand Charge Management

Singapore’s power system is handling more rooftop solar PV, battery storage, and EV charging, making building load profiles more volatile and increasing the value of real-time optimization.[3]Energy Market Authority, “Demand-Side Flexibility Roadmap,” Energy Market Authority, ema.gov.sg AI energy management platforms are well placed to convert tariff signals into dispatch schedules for on-site assets, helping users reduce peak import costs and manage demand charges more actively. EMA’s Demand-Side Flexibility Roadmap also identified automated demand response as a priority capability, supporting deeper adoption of AI and IoT-based control systems. The opportunity extends beyond cost control because buildings with the right orchestration layer can also prepare for future participation in virtual power plant and grid services models. Data center operators are helping validate these tools under high-load conditions, which lowers perceived software risk for mainstream commercial buyers in the Singapore AI-powered Energy Management Software Market.

AI-Enabled Fault Detection, Diagnostics, and Predictive Control Adoption

AI-enabled fault detection and diagnostics are gaining adoption because it is producing visible savings in cooling-intensive Singapore facilities. Work with GlaxoSmithKline at the Tuas South manufacturing facility was projected to deliver up to 615 MWh of annual electricity savings, reduce CO₂ emissions by 246 tonnes, and lower energy costs by up to USD 130,000.[4]ABB Ltd., “Net-Zero in Action, ABB Powers GSK’s Sustainability Leap in Singapore,” ABB, abb.com The value is stronger in Singapore than in many temperate markets because HVAC systems operate under persistent high cooling loads, and performance declines show up quickly in energy bills. The Asia-Pacific Energy Transition Readiness Index 2025 found that 78% of Singapore respondents identified AI and automation as key enablers of the energy transition, which suggests that many buyers have moved beyond pilot evaluation. Honeywell’s 2025 decision to establish a Center of Excellence in Singapore also showed that vendors now see the city-state as a proving ground for wider regional deployment of AI-led building technologies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Fragmentation Across Legacy Building Systems | -2.1% | Singapore-wide, most acute in pre-2010 commercial buildings and smaller institutional assets | Medium term (2-4 years) |

| Cybersecurity and Data Residency Concerns in Cloud-Hosted Energy Platforms | -1.8% | Singapore-wide, intensified in government-linked, healthcare, and financial-sector building portfolios | Short term (≤ 2 years) |

| High Integration Complexity with Mixed Vendor Building Estates | -1.3% | Singapore-wide, most acute in multi-tenanted commercial towers with sequential BMS upgrades | Medium term (2-4 years) |

| Limited Energy Baseline Visibility in Older Small and Medium Buildings | -0.9% | Singapore-wide, concentrated in older commercial blocks and SME-occupied industrial properties | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Fragmentation across Legacy Building Systems

Data fragmentation across older building estates remains one of the clearest barriers in the Singapore AI-powered Energy Management Software Market. Many commercial properties built before 2005 still operate with proprietary building management environments and uneven protocol implementation across BACnet, Modbus, and LonWorks systems. Retrofit layers added over time by different contractors have left gaps between meters, HVAC controls, lighting platforms, and access systems, which slows unified data ingestion. Those gaps degrade baseline quality, weakening forecast accuracy and making audit-ready reporting harder to defend. Vendors with strong edge-layer protocol translation are better placed to win retrofit-heavy projects because they can normalize data without forcing a full BMS replacement.

Cybersecurity And Data Residency Concerns in Cloud-Hosted Energy Platforms

Cybersecurity and data residency concerns continue to slow cloud adoption among a portion of the buyer base in the Singapore AI-powered Energy Management Software Market. Building-level energy data can reveal production patterns, occupancy density, and maintenance cycles, so risk and legal teams often review cloud deployment more closely than facilities teams first expect. This has created a split market in which government-linked, healthcare, financial-sector, and large-enterprise portfolios seek tighter local hosting and control arrangements, while smaller operators remain more price-sensitive. The result is a clear advantage for vendors that can offer stronger security credentials, Singapore-based support, and deployment models that keep sensitive telemetry under closer local control. The restraint does not stop adoption, but it does stretch procurement timelines and strengthen the appeal of hybrid architecture.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Strength Remains Clear While Services Gain Speed

Software held 65.18% of the Singapore AI-powered Energy Management Software Market share in 2025, which reflected the depth of platform adoption across utilities, commercial real estate portfolios, and industrial facilities. Buyers have already embedded energy analytics, real-time dashboards, and carbon reporting into day-to-day operating workflows, which gives the software layer a central role in building operations. That position is reinforced by switching costs: once building management system data, historical baselines, and reporting workflows are housed on a single platform, vendor migration becomes disruptive for owners and operators. This helps incumbent software providers maintain stronger renewal rates than many adjacent enterprise software categories.

Services are projected to expand at a 24.31% CAGR from 2026 to 2031, making them the fastest-growing component of the Singapore AI-powered Energy Management Software Market. Mid-size commercial and industrial operators are driving much of this momentum because many lack in-house energy engineering teams and prefer managed outcomes over software administration. A multi-year AI-native ecosystem initiative from Singapore directly addressed this shift by linking energy monitoring and ESG reporting into a more continuous managed workflow. Outcome-based energy performance contracts are also becoming more attractive because they shift part of the execution risk to vendors and convert upfront investment into recurring operating expense.

By Deployment Mode: Cloud Leads While Hybrid Solves Control And Scalability Needs

Cloud-based deployment accounted for 55.14% of the Singapore AI-powered Energy Management Software Market in 2025, supported by subscription economics, continuous model updates, and easier benchmarking across multi-site portfolios. It also reduced the need for regular on-site hardware refresh cycles, which many property owners and operators prefer to avoid. Even so, hybrid deployment is projected to grow at a 24.42% CAGR from 2026 to 2031 and is becoming the preferred architecture for more regulated and complex environments. Enterprises are using hybrid setups to keep sensitive telemetry local while still sending normalized performance indicators into cloud analytics layers.

This balance fits the Singapore AI-powered Energy Management Software Market well because it gives buyers a way to combine AI scalability with tighter data control. It is particularly relevant in hospitals, data centers, and government-linked sites where air-gapping, local hosting, or stricter review processes still shape procurement. On-premises deployment, therefore, retains a role, especially where full cloud connectivity is operationally difficult or not preferred. Purpose-built edge inference hardware, including the Univers EnOS™ AI Box introduced at CES 2026, also shows how the gap between on-premises and hybrid architecture is narrowing for high-frequency control applications.

By Application: Demand Optimization Anchors Revenue While Renewable Forecasting Advances Fastest

Energy Consumption and Demand Optimization held the largest application share at 22.16% in 2025 because it addresses the most common energy management need across building types. Real-time load profiling, demand charge avoidance, and automated setpoint control can be deployed over a broader base of installed meters and controls than more specialized applications. That wide compatibility helps the segment hold its revenue lead even as other use cases expand. Asset Performance and Predictive Maintenance is also gaining ground because downtime costs in data centers and industrial facilities can quickly exceed the cost of software.

Renewable Energy Forecasting and Integration is projected to expand at a 24.53% CAGR from 2026 to 2031, which makes it the fastest-growing application in the Singapore AI-powered Energy Management Software Market. The need is rising as rooftop solar, battery storage systems, and electricity import planning create a stronger requirement for yield prediction and dispatch optimization. Smart Grid and Distributed Energy Resource Management is moving ahead in parallel after the VPP Regulatory Sandbox launched in October 2025 with SP Group, Blue Whale Energy, and Nanyang Technological University aggregating up to 15 MW of distributed assets. Energy Trading, Pricing, and Market Intelligence remains smaller today, but it is becoming strategically important as buildings with AI-connected distributed assets move closer to automated participation in Singapore’s electricity market framework.

By End User: Utilities Hold The Base While Industrial Facilities Expand Fastest

Utilities held 36.11% of the market in 2025, making them the largest end-user group in the Singapore AI-powered Energy Management Software Market. Their lead reflects large investments in grid digital twins, distributed energy resource management, and AI-based demand forecasting that require software operating at the network level rather than only at the individual building level. This demand profile gives utility-linked projects a wider system scope and a stronger need for integration across energy assets. The Punggol Digital District smart grid provides a visible example of that utility-led architecture in practice.

Industrial Facilities are projected to grow at a 24.64% CAGR from 2026 to 2031, which makes them the fastest-expanding end-user segment. The increase in Singapore’s carbon tax to SGD 45/tCO₂e in 2026 provides large taxable facilities with a direct incentive to optimize equipment-level performance, where efficiency gains can exceed software costs by a wide margin. Commercial buildings continue to scale adoption as Green Mark recertification and investor-ready ESG reporting converge in day-to-day property management. Residential buildings remain a smaller revenue pool because most consumer interaction still runs through utility and public housing channels rather than through licensed enterprise platforms, although the Energy Efficiency Grant is helping improve the equipment base that feeds future AI deployments.

Geography Analysis

Singapore is a compact island market, so adoption patterns in the Singapore AI-powered Energy Management Software Market are shaped more by building type and energy intensity than by regional policy differences. The central business district, including Marina Bay, Raffles Place, and Shenton Way, is home to a large share of Grade A commercial buildings, where landlords are increasingly specifying AI energy management platforms to support Green Mark targets and tenant disclosure requirements. Data center clusters in Jurong, Woodlands, and Tampines constitute another major demand pocket, as data centers account for 7% of Singapore’s total electricity demand. The October 2025 allocation of a 20-hectare Jurong Island site for a 700 MW data center park showed that this load center will remain central to future software demand. Jurong Island and the wider western industrial corridor also matter because carbon-taxed petrochemical, pharmaceutical, and precision engineering sites there have a direct financial reason to optimize energy use.

The Punggol Digital District is set to open in 2026 as a 50-hectare smart business park and will serve as a live testbed for district-level AI energy management in Singapore. JTC and Univers designed its smart grid to integrate rooftop solar PV, battery storage, and EV charging under a unified AI controller, aiming for more than a 50% improvement in district-level energy efficiency. That model matters beyond one district because it provides planners and operators with a clear template for future mixed-use precincts seeking centralized energy orchestration. Tengah Town added a residential example when Keppel received a 20-year contract in April 2026 to connect all central cooling systems to an AI-powered operations nerve center for remote monitoring, predictive maintenance, anomaly detection, and performance optimization. Together, these projects show that both commercial and residential deployments are moving toward more centralized AI-operated infrastructure.

Singapore also matters as a regional base because Schneider Electric, Siemens, Honeywell, ABB, and Johnson Controls run significant Asia-Pacific activities from the city-state. Respondents in Singapore showed the highest confidence in AI and automation among the 12 surveyed markets. Procurement choices made in Singapore often serve as reference architectures for wider Southeast Asian portfolios, giving the Singapore AI-powered Energy Management Software Market influence beyond its physical size. Smart Nation 2030 priorities keep smart buildings and intelligent energy systems high on the public agenda, which helps maintain a stable institutional demand floor through the forecast period.

Competitive Landscape

The Singapore AI-powered Energy Management Software Market is moderately fragmented around a core group of global building automation and industrial software vendors. Schneider Electric, Siemens, Johnson Controls, Honeywell, and ABB benefit from long-standing building management system integration contracts that give them access to installed data streams, customer relationships, and renewal cycles. That installed base still matters because customers are less willing to change vendors after ESG reporting baselines and operating workflows have already been built inside a platform. Johnson Controls strengthened this position in January 2026, committing up to SGD 60 million (USD 44 million) over 5 years to expand its Singapore Innovation Center for thermal management and intelligent automation in AI-ready data centers. ABB also widened its platform offering in 2026 with ABB Ability BuildingPro Suites, an open cybersecure platform that unifies building automation, HVAC, energy, IT, and IoT systems.

Schneider Electric took a similar strategic step in May 2025, launching a multi-year AI-native ecosystem initiative from Singapore to connect energy monitoring, automation, and ISSB-aligned ESG reporting. These moves show that rivalry is shifting away from hardware-led metering and toward software layers that can unify mixed-vendor estates and convert operating data into decision-ready outputs. White space remains strongest in buildings between 5,000 m² and 30,000 m², especially owner-occupied commercial properties, smaller industrial sites, and hospitality assets. Many of these customers are still underserved by enterprise platforms that were priced and scoped for very large portfolios. That gap is giving faster-moving local and AI-native suppliers more room to compete on deployment speed, local regulatory knowledge, and outcome-based pricing.

Univers is one of the clearer examples because it has already worked with SP Group and JTC on live virtual power plant and smart grid projects under Singapore’s regulatory framework. Competitive pressure is also rising in data centers following the introduction of SS 715:2025 for IT energy efficiency, which has created a new compliance-driven procurement cycle for operators and their software vendors. The result is a market where incumbents are investing to close AI capability gaps, while newer entrants are pushing into mid-market and project-led opportunities. This structure supports steady rivalry, selective partnerships, and a plausible path to acquisition-led consolidation without making the market highly fragmented.

Singapore AI-powered Energy Management Software Industry Leaders

Schneider Electric SE

Siemens AG

Johnson Controls International plc

Honeywell International Inc.

ABB Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Schneider Electric and Hon Hai Technology Group (Foxconn) announced a strategic collaboration to define and scale next-generation AI data centers, combining Schneider Electric's power systems, cooling, and energy management capabilities with Foxconn's compute platform expertise, with production expected to begin in the second half of 2026. The partnership directly addresses the energy management requirements of hyperscale AI data center infrastructure expanding across Singapore and the Asia-Pacific region.

- April 2026: Midea Building Technologies and Keppel Ltd. (Infrastructure Division) signed a strategic cooperation agreement to jointly develop AI-driven, energy-efficient modular cooling solutions for Asian markets, building on their existing collaboration in the HDB Tengah Town Phase 2 District Cooling System project. The agreement establishes a commercially replicable AI-integrated district cooling model with direct relevance to Singapore's ongoing and planned public residential developments.

- April 2026: Keppel was awarded a 20-year contract for the Tengah Town pre-built public housing central cooling system, covering all 12 pre-built project cooling systems to be connected to Keppel's operations nerve center using AI for real-time remote monitoring, predictive maintenance, anomaly detection, and performance optimization.

- January 2026: Johnson Controls announced an investment of up to SGD 60 million (USD 44 million) over 5 years to expand its Singapore Innovation Centre, with focus on next-generation thermal management, intelligent automation for AI-ready data centers, and expanding the engineering workforce to 90-100 roles. The investment was supported by the Singapore Economic Development Board.

Singapore AI-powered Energy Management Software Market Report Scope

The Singapore AI-powered Energy Management Software Market refers to platforms and services that leverage artificial intelligence to optimize energy consumption, enhance asset performance, and enable smarter grid and distributed energy resource (DER) management. These solutions provide advanced capabilities, including predictive maintenance, renewable energy forecasting, demand-side optimization, and market intelligence for energy trading and pricing.

The Singapore AI-powered Energy Management Software Market report is segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), and End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings |

Key Questions Answered in the Report

What is the current size and forecast for Singapore AI-powered energy management software?

The Singapore AI-powered Energy Management Software Market was valued at USD 48.61 million in 2025, is estimated at USD 59.02 million in 2026, and is expected to reach USD 168.12 million by 2031 at a 23.29% CAGR.

What is driving adoption in Singapore right now?

The strongest drivers are the higher carbon tax, mandatory climate reporting, building retrofit activity, and the push for better tariff optimization and fault detection across commercial and industrial assets.

Which deployment model is most widely used?

Cloud-based deployment led with 55.14% share in 2025 because it supports subscription pricing, continuous updates, and multi-site benchmarking, while hybrid is growing faster at 24.42% CAGR.

Which application is expanding the fastest?

Renewable Energy Forecasting and Integration is the fastest-growing application, projected to expand at a 24.53% CAGR through 2031 as solar, storage, and grid coordination needs become more important.

Which customer group is creating the most near-term revenue?

Utilities held the largest end-user share at 36.11% in 2025 because grid-level demand forecasting, distributed energy resource management, and digital twin programs require broader software deployment.

How is competition changing among vendors in Singapore?

Competition is shifting toward vendor-agnostic software layers that can unify mixed building systems, support ESG reporting, and work across cloud, hybrid, and edge environments, with incumbents and local AI-native firms both pushing into this space.

Page last updated on: