Belgium Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

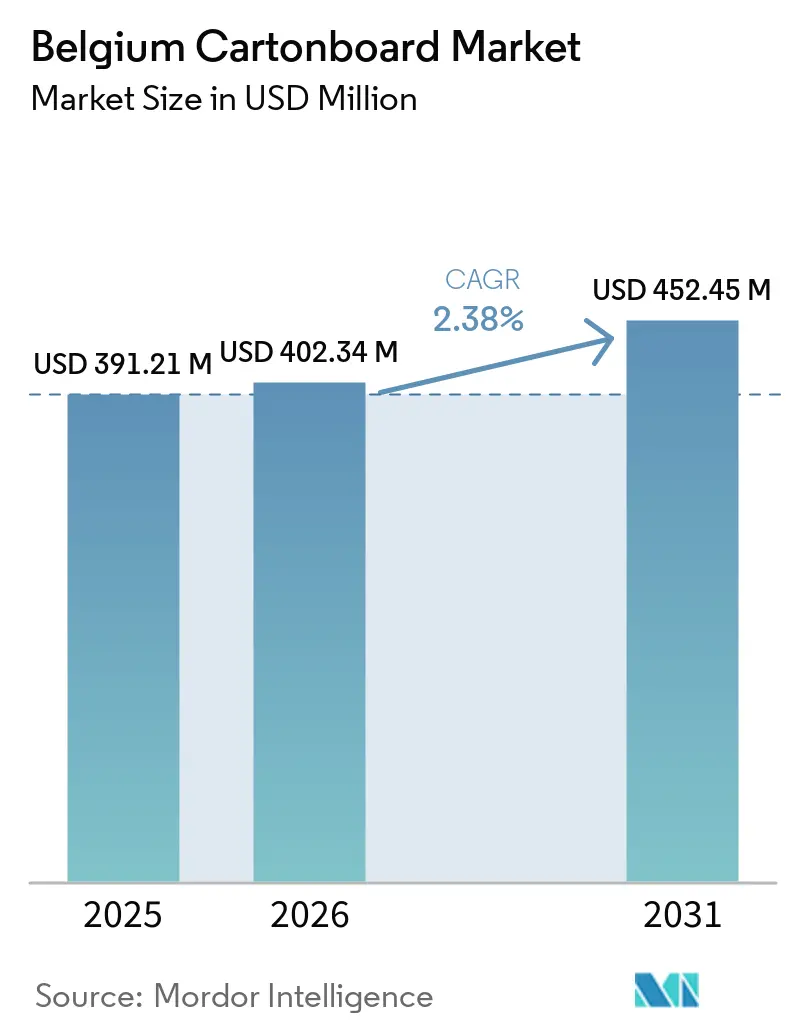

| Base Year Market Size (2025) | USD 391.21 Million |

| Market Size (2026) | USD 402.34 Million |

| Market Size (2031) | USD 452.45 Million |

| Growth Rate (2026 - 2031) | 2.38% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Belgium Cartonboard Market Analysis by Mordor Intelligence

The Belgium Cartonboard Market size is expected to increase from USD 391.21 million in 2025 to USD 402.34 million in 2026 and reach USD 452.45 million by 2031, growing at a CAGR of 2.38% over 2026-2031.

The Belgium cartonboard market is expanding at a measured pace because demand is tied more to specification upgrades than to broad volume growth. The biggest shift is coming from the EU Packaging and Packaging Waste Regulation, which is moving Belgian buyers toward recyclable and PFAS-free grades and is changing procurement standards across food and consumer packaging. The country’s strong pharmaceutical base also gives the Belgium cartonboard market a distinctive quality profile because medicine packaging requires serialized, compliant, and highly consistent secondary cartons. At the same time, energy costs, fiber costs, and new European board capacity are keeping pricing conditions difficult for producers and converters. That combination leaves the Belgium cartonboard market with steady growth, tighter qualification standards, and better opportunities for suppliers that can deliver compliance, barrier performance, and reliable supply.

Key Report Takeaways

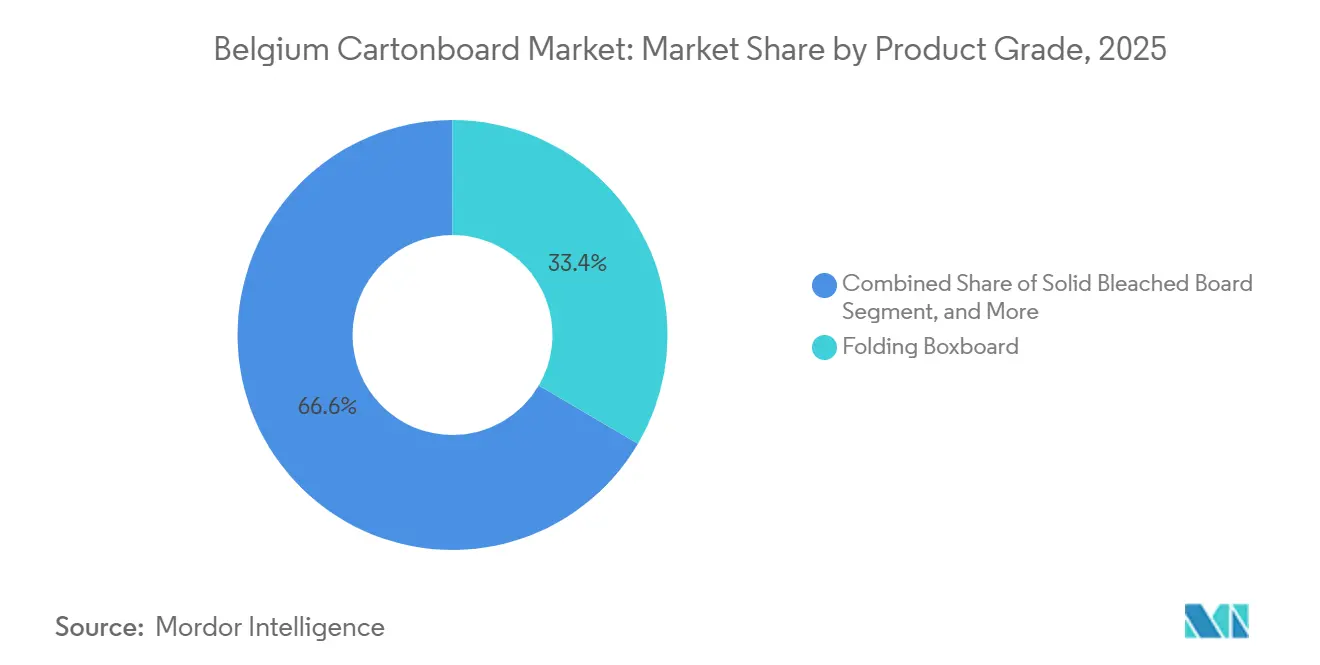

- By product grade, folding boxboard held 33.43% of the Belgium cartonboard market share in 2025, while food service board is forecast to expand at a 5.91% CAGR through 2031.

- By packaging format, folding cartons accounted for 69.67% of the Belgium cartonboard market size in 2025, while other packaging formats are projected to grow at a 6.32% CAGR through 2031.

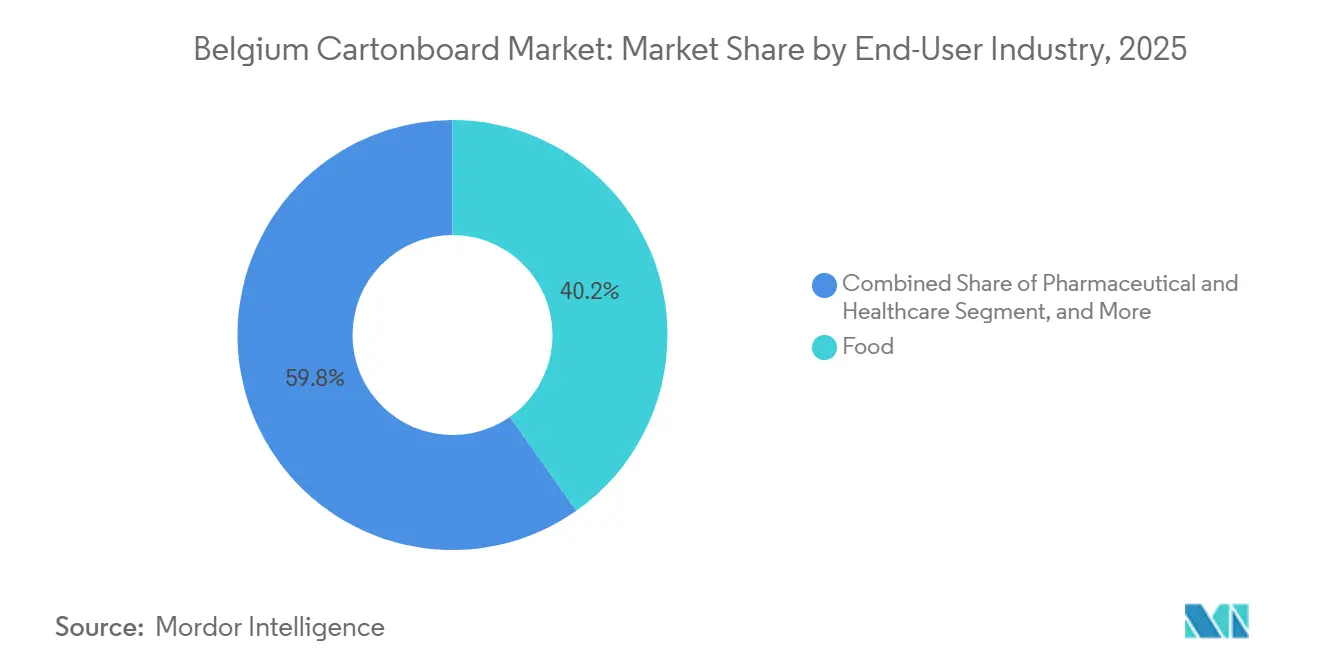

- By end-user industry, food held a 40.23% share in 2025, while pharmaceutical and healthcare packaging is expected to advance at a 6.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Belgium Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic-To-Fiber Shift Under PPWR And Retail Sustainability Targets | +0.7% | EU-wide, Belgium as PPWR early-compliance market | Short term (≤ 2 years) |

| Stable Food And Beverage Carton Demand | +0.5% | National, concentrated in Flanders and Brussels-Capital Region food processing clusters | Medium term (2-4 years) |

| Pharmaceutical Serialization And Export Packaging Intensity | +0.4% | National, spill-over to export-oriented pharma packaging plants in Antwerp, Ghent, and Liège | Medium term (2-4 years) |

| High Paper And Cardboard Collection And Recycling Readiness | +0.3% | National, with framework influence across Benelux | Long term (≥ 4 years) |

| PFAS-Free Barrier Redesign In Foodservice And Chilled Packs | +0.2% | EU-wide, Belgium foodservice and chilled logistics channels | Short term (≤ 2 years) |

| Beverage Multipack Conversion From Shrink Film To Paperboard | +0.1% | National, concentrated in Belgian brewery and beverages sector | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Plastic-To-Fiber Shift Under PPWR And Retail Sustainability Targets

The Belgium cartonboard market is being reshaped by PPWR because the regulation applies across EU member states from August 12, 2026 and changes what packaging formats remain acceptable in food retail and foodservice channels.[1]European Commission, “Packaging Waste,” European Commission, environment.ec.europa.eu Article 5 also sets strict PFAS limits for food-contact packaging, which directly challenges legacy grease-barrier systems used in paperboard formats across Europe. Belgian packaging buyers are therefore moving away from plastic-heavy formats and toward cartonboard structures that can pass recyclability and chemical-compliance reviews with less redesign risk. This shift matters in sandwich packs, bakery sleeves, produce trays, and chilled food formats, where cartonboard is no longer competing only on cost but on regulatory fit.[2]European Union, “Regulation (EU) 2025/40 of the European Parliament and of the Council of 19 December 2024 on Packaging and Packaging Waste,” EUR-Lex, eur-lex.europa.eu Industry guidance also indicates that most paper and board packaging already sits within the PPWR PFAS limits, which gives Belgian converters a usable compliance base for many applications. The remaining work is concentrated in premium coated and direct-contact applications, where reformulation and testing will continue to shape the Belgium cartonboard market through 2027.

Stable Food And Beverage Carton Demand

The Belgium cartonboard market continues to benefit from a stable food and beverage base because the country combines local consumption with a dense export-oriented processing network. Belgian food and drinks producers also value local and near-market packaging supply because lead times and pack changeovers matter in retail programs with frequent design updates. The commercial case for cartonboard is visible in brewery packaging, where technically demanding multipack formats are now being redesigned to remove plastic without sacrificing pack strength. The Leffe beer multipack developed with Graphic Packaging International shows that folding boxboard can carry heavy glass-bottle loads while also meeting brand and sustainability goals. That matters for the Belgium cartonboard market because food demand is not driven only by tonnage, it is also supported by better graphics, stronger shelf impact, and upgraded board specifications. As a result, higher-caliper and better-finished grades continue to hold value even when consumer spending is not especially strong.

Pharmaceutical Serialization And Export Packaging Intensity

The Belgium cartonboard market has an unusual demand floor in pharmaceutical packaging because medicine exports and compliance rules keep secondary carton needs high even when other packaging categories slow. Belgium’s medicines verification deferral ended on February 9, 2025, which brought prescription medicine packaging into full safety-feature implementation under the Falsified Medicines Directive framework. That means each carton must support serialized coding, lot identification, expiry data, tamper evidence, and printing consistency that can be verified in high-speed operations. Belgium also ranked third in EU pharmaceutical exports in 2025 with EUR 38.5 billion, or USD 45.1 billion, which shows why packaging intensity is high relative to the size of the domestic economy. This is not a one-time compliance step because readability standards and traceability requirements create a recurring need for board, print, and converting compatibility. That keeps the Belgium cartonboard market closely tied to premium carton grades and raises the entry barrier for suppliers that lack pharmaceutical validation capability.

High Paper And Cardboard Collection And Recycling Readiness

The Belgium cartonboard market benefits from one of Europe’s stronger paper and packaging recovery systems, which supports the economics of recycled-fiber grades in a practical way. Commercial paper-cardboard packaging reached a 107.7% recycling rate in 2024, while household paper-cardboard reached 152%, with the reporting gap reflecting collection volumes that exceed formally declared packaging volumes. Belgian citizens also sorted 24.7 kg of paper and cardboard per person in 2024, and 99% of single-use packaging on the market was recyclable by year-end. That infrastructure supports white-lined chipboard and recycled-content grades because converters can point to credible local collection and recycling pathways when customers ask for evidence. It also reduces some of the cost premium that can otherwise hold back recycled-fiber board in consumer-facing applications. The Belgium cartonboard market therefore has a circularity advantage that supports long-term adoption of recycled-content solutions under tighter EU packaging rules.

Res*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy And Fiber Cost Volatility In Europe | -0.5% | EU-wide, Belgium as an energy-import-dependent manufacturing hub | Short term (≤ 2 years) |

| Recyclability Penalties For Complex Coated Structures | -0.2% | EU-wide, concentrated in Belgian food and pharmaceutical packaging segments | Medium term (2-4 years) |

| Compliance And Documentation Burden Under PPWR And Food-Contact Rules | -0.1% | National, with cross-border supply chain implications | Short term (≤ 2 years) |

| Reuse Models In Selected Foodservice Channels | -0.1% | National, concentrated in Brussels-Capital foodservice and quick-service restaurant chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy And Fiber Cost Volatility In Europe | -0.5% | EU-wide, Belgium as an energy-import-dependent manufacturing hub | Short term (≤ 2 years) |

| Recyclability Penalties For Complex Coated Structures | -0.2% | EU-wide, concentrated in Belgian food and pharmaceutical packaging segments | Medium term (2-4 years) |

| Compliance And Documentation Burden Under PPWR And Food-Contact Rules | -0.1% | National, with cross-border supply chain implications | Short term (≤ 2 years) |

| Reuse Models In Selected Foodservice Channels | -0.1% | National, concentrated in Brussels-Capital foodservice and quick-service restaurant chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy And Fiber Cost Volatility In Europe

The Belgium cartonboard market is exposed to European energy and fiber cost swings because many Belgian converters rely on purchased board from regional mills rather than fully integrated local production. European packaging paper prices rose by up to EUR 100 per tonne in April 2026 as natural gas costs, OCC prices, and logistics pressures moved upward together. Recycled-fiber grades are especially sensitive because coated recycled board has a much higher gas dependency than folding boxboard in normal operating conditions. Fastmarkets noted that a EUR 10 per MWh increase in gas prices can add up to EUR 20 per tonne to white-lined chipboard production costs, versus EUR 5 per tonne for folding boxboard. Mayr-Melnhof described the 2026 market backdrop as persistently challenging, with structural overcapacity and intense competition, which helps explain why pass-through has remained difficult. The result is recurring margin pressure in the Belgium cartonboard market, especially for converters serving long-term contracts where price resets are slower than input-cost changes.

Recyclability Penalties For Complex Coated Structures

The Belgium cartonboard market also faces a technical restraint because not every coated or laminated board structure will remain equally acceptable under future recyclability rules. PPWR requires packaging placed on the EU market to be recyclable in an economically viable way by 2030, which raises the compliance bar for multi-layer formats that use polymer coatings, foil, or complex barrier stacks. That creates direct pressure in pharmaceutical and food-contact uses where barrier and seal performance often depend on specialized coatings. Belgian converters may therefore need to spend on reformulation, qualification, and customer testing over a short period, while still protecting product performance and pack integrity. The transition is not entirely negative because PFAS-free and bio-based barrier systems are expanding, but the change still raises execution risk in the near term. For the Belgium cartonboard market, the main challenge is timing, because customers want compliant structures quickly while converters still need dependable quality and competitive cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Folding Boxboard Leads While Food Service Board Expands Fast

Folding boxboard held 33.43% of the Belgium cartonboard market share in 2025, which kept it ahead of every other product grade in the country. FBB remains the core grade in the Belgium cartonboard market because it combines print quality, stiffness, and converting efficiency in a way that works across food, pharmaceutical, and cosmetics packs. The grade is especially well suited to pharmaceutical cartons, where consistent creasing, clean print surfaces, and dimensional stability support serialized packaging requirements. Solid bleached board continues to serve hygiene-sensitive applications, especially where direct-contact quality expectations and premium appearance are both important. Solid unbleached board remains relevant in the Belgium cartonboard industry for applications where kraft aesthetics and stronger natural-fiber positioning have commercial value.

White-lined chipboard serves more volume-sensitive food and consumer goods uses, and its position is strengthened by Belgium’s well-developed paper and cardboard recovery system. Food service board is forecast to grow at a 5.91% CAGR through 2031, making it the fastest-moving grade within the Belgium cartonboard market. That growth is tied to the PFAS-free redesign cycle in foodservice and chilled packs, where board structures now have to meet tougher compliance needs without giving up grease resistance or machinability. Metsä Board’s Muoto molded-fiber and folding-board concept, shown at Interpack 2026, illustrates the kind of recyclable format innovation now shaping this part of the Belgium cartonboard industry. Liquid packaging board also keeps a place in dairy and beverage uses, where Tetra Pak and SIG are moving toward paper-based barrier structures that reduce dependence on conventional material combinations.

By Packaging Format: Folding Cartons Stay Dominant While Alternative Formats Accelerate

Folding cartons accounted for 69.67% of the Belgium cartonboard market size in 2025, which reflects the depth of the country’s pharmaceutical and food converting base. Folding cartons remain central to the Belgium cartonboard market because both industries require format consistency, strong graphics, and dependable high-speed filling performance. Pharmaceutical converting adds extra stability because serialization and tamper-evidence rules keep the carton format indispensable for many prescription products. Belgium also has a concentrated cluster of pharmaceutical packaging operations, which reinforces local demand for high-specification carton formats with validated print and traceability performance. That makes the leading format in the Belgium cartonboard market stable by structure, not simply dominant by legacy use.

Other packaging formats are forecast to grow at a 6.32% CAGR through 2031, which makes them the fastest-growing format group. This growth comes from cups, foodservice containers, and related formats that are gaining from the move away from plastic-coated single-use packaging. Liquid packaging remains another important format because suppliers are redesigning aseptic cartons with higher paper content and lighter barrier structures. Tetra Pak and Sterilgarda Alimenti launched the first 1-litre aseptic carton with a paper-based barrier in April 2026, which shows how quickly commercial formats are moving in this direction. Sleeve and tray formats also matter in beverage multipacks and retail-ready packaging, where the replacement of shrink film with paperboard is gaining traction in Belgium’s brewery channels.

By End-User Industry: Food Holds The Base While Pharma Packaging Adds Momentum

Food accounted for 40.23% of demand in 2025, which made it the largest end-user base in the Belgium cartonboard market. Food demand stays broad because Belgian producers operate across bakery, confectionery, chilled dairy, frozen meals, and shelf-stable products, each with distinct board and barrier needs. The country’s role as a logistics and processing hub also supports a steady packaging requirement that is spread across many product categories rather than concentrated in one narrow niche. Within the Belgium cartonboard industry, retail pressure for stronger shelf appearance is also pushing more food packs toward better print surfaces and improved structural design. Beverage remains the second-largest end-user group, and brewery packaging is an active area for paperboard conversion because heavy multipacks are now being redesigned around plastic reduction.

Pharmaceutical and healthcare packaging is projected to grow at a 6.09% CAGR through 2031, making it the fastest-growing end-user segment in the Belgium cartonboard market. This pace reflects Belgium’s export-led pharmaceutical base, its serialization rules, and the high packaging intensity required for regulated medicine supply. The Falsified Medicines Directive framework, implemented locally through FAMHP and GS1-based coding standards, requires every secondary carton to carry machine-readable data and verified safety features. That creates a non-discretionary consumption base for high-specification cartons, which gives this end-user segment more resilience than most consumer-facing categories. Tobacco, cosmetics and toiletries, and other end-user groups such as toys, apparel, and household goods complete the demand base and reduce the risk of overdependence on a single sector. This spread of end uses helps the Belgium cartonboard market absorb shocks even when one packaging category softens.

Geography Analysis

The Belgium cartonboard market is shaped first by the country’s location between Germany, France, the Netherlands, and the United Kingdom, which makes it a heavily served packaging node despite its modest absolute size. Belgium’s position supports short lead times, active cross-border trade, and efficient supply into Western Europe’s largest consumer and industrial corridors. The Port of Antwerp plays a central role because it handles inbound pulp, recovered fiber, and finished board rolls while also supporting exports of converted cartons into nearby markets. Flanders remains the main industrial center for the Belgium cartonboard market because it hosts much of the country’s food processing, pharmaceutical production, and FMCG converting activity. Turnhout is especially important in this geography because it is home to Van Genechten Packaging Group and remains a known hub for high-end folding carton manufacturing.[3]European Carton Makers Association, “Van Genechten Packaging Group Voted Flemish Company of the Year 2025,” ECMA, ecma.org

Brussels-Capital Region adds a different kind of weight to the Belgium cartonboard market because regulatory coordination and pharmaceutical decision-making are concentrated there. That matters because packaging compliance decisions for medicines are often made close to regulatory and corporate headquarters rather than only at plant level. Belgium’s full activation of the national medicines verification system from February 2025 keeps pharmaceutical carton demand structurally embedded and removes the uncertainty that existed under the earlier deferral period. Autajon Packaging Belgium operates 2 dedicated folding carton facilities in Arlon and Brussels with a pharmaceutical focus, which shows how this regulatory geography translates into converter clustering. The Belgium cartonboard market therefore has a concentration of pharma-converting capability that is larger than the country’s population size would suggest.

Wallonia contributes through food and industrial manufacturing, although its pharmaceutical base is not as dense as that of Flanders. Benelux trade also remains important because Belgium imports cartonboard rolls from Dutch, German, and Scandinavian mills and exports higher-value converted cartons after printing and finishing. Import prices in the Benelux folding boxboard trade averaged USD 1,225 per tonne for Belgium, while export prices for converted output averaged USD 1,471 per tonne, which shows the value captured by local conversion. Belgium’s 80% packaging waste recycling rate, among Europe’s highest levels as of 2022, gives the Belgium cartonboard market a circular-material advantage that supports recycled-fiber use and documented compliance pathways.

Competitive Landscape

The Belgium cartonboard market is moderately concentrated at the board-supply level because a small set of pan-European producers supplies much of the material used by Belgian converters. Mayr-Melnhof Karton AG, Stora Enso Oyj, Metsä Board Corporation, Billerud Aktiebolag, and Mondi plc are the main board-side names in the competitive frame, with Belgian demand served from mills across Finland, Austria, Sweden, and Germany. At the converting level, the Belgium cartonboard market includes one leading domestic independent, Van Genechten Packaging Group, alongside a smaller group of international carton specialists. Van Genechten Packaging Group is a Belgian-headquartered carton specialist with a broad European footprint, and the company reported approximately EUR 500 million, or USD 550 million, in annual revenue. Liquid packaging remains a separate lane because SIG Group and Tetra Pak compete through integrated carton-and-filling-system propositions rather than through open-market board supply alone.

Strategic competition in 2026 is centered on sustainability credentials, multi-mill supply resilience, and compliance capability for pharmaceutical packaging. Tetra Pak strengthened its position by launching the first 1-litre aseptic carton with a paper-based barrier in April 2026, which pushed paper content and renewable-content performance further into mainstream commercial formats. SIG also gained ground in this innovation race because its alu-layer-free full-barrier cartons recorded 24% year-on-year sales growth in 2025. Stora Enso added a major supply-side move when it inaugurated the Oulu consumer board line in August 2025 with 750,000 tonnes of annual capacity, which has helped keep European supply conditions loose. That capacity backdrop matters in the Belgium cartonboard market because it supports customer choice but also keeps pricing pressure high for converters that cannot easily pass costs through.

Mayr-Melnhof’s Fit-For-Future program targets an earnings uplift of more than EUR 250 million, or USD 275 million, in 2027 versus 2024, which shows that cost resilience remains a major strategic priority.[4]Mayr-Melnhof Karton AG, “MM Trading Statement Q1 2026,” Mayr-Melnhof Group, mm.group Metsä Board’s Lead the Pack strategy for 2026-2030 targets more than 4% annual CAGR in consumer packaging revenue, which confirms that premium consumer-board demand is still an area of active investment. WEIG Group’s May 2026 study also supported the commercial case for recycled cartonboard by showing higher brand perception and purchase intent than virgin-fiber alternatives in direct testing across 6 European markets. Overall, the Belgium cartonboard market favors suppliers that can combine documentation strength, regulatory readiness, and product consistency rather than competing only on base price.

Belgium Cartonboard Industry Leaders

Van Genechten Packaging Group NV

Mayr-Melnhof Karton AG

Smurfit Westrock plc

Stora Enso Oyj

Graphic Packaging International, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Tetra Pak, in partnership with Sterilgarda Alimenti, launched the first 1-litre aseptic carton with a paper-based barrier, the Tetra Brik Aseptic 1000 Edge, achieving 90% renewable content and reducing package carbon footprint by up to 50% versus conventional foil-barrier cartons, as verified by Carbon Trust. The launch extends the paper-based barrier technology from portion-pack formats to the most commercially significant aseptic carton size globally, directly expanding the addressable market for premium liquid packaging board.

- March 2026: Van Genechten Packaging Group officially inaugurated its expanded production facility at VG Kvadra Pak JSC in Riga, Latvia, completing a EUR 10 million (USD 10.8 million) investment on schedule. The facility, operational from March 1, 2026, strengthens VGP's production capacity for premium confectionery and beauty-and-cosmetics folding cartons across Baltic and Nordic markets, extending the Belgian group's nine-country converting network.

- February 2026: Tetra Pak announced a EUR 60 million (USD 66 million) investment in a new paper-based barrier pilot plant in Lund, Sweden, as part of its commitment to invest EUR 100 million annually through 2030 in sustainable packaging innovation. The pilot plant will provide customers with end-to-end manufacturing insight from barrier creation to filled-package production, accelerating the commercial scaling of paper-based barrier liquid cartons.

Belgium Cartonboard Market Report Scope

The Belgium Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The Belgium Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, Other Packaging Formats), End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, Other End-User Industries). The Market Forecasts are in Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

Key Questions Answered in the Report

How large is the Belgium cartonboard market in 2026 and where is it heading by 2031?

The Belgium cartonboard market is valued at USD 402.34 million in 2026 and is projected to reach USD 452.45 million by 2031, growing at a 2.38% CAGR.

Which product grade leads demand in Belgium?

Folding boxboard led demand with a 33.43% share in 2025 because it fits food, pharmaceutical, and cosmetics packaging with strong printability and converting performance.

Which packaging format is growing the fastest?

Other packaging formats, including cups and foodservice containers, are projected to grow the fastest at a 6.32% CAGR through 2031 as plastic substitution expands.

Why is pharmaceutical packaging so important in Belgium?

Pharmaceutical and healthcare packaging is forecast to grow at a 6.09% CAGR because serialization, export intensity, and compliance rules keep demand for high-specification cartons elevated.

What is the biggest regulatory factor affecting cartonboard demand?

PPWR is the main regulatory driver because it pushes recyclable and PFAS-free packaging design, which is changing material choices across food retail and foodservice.

What is holding back faster growth?

The main constraints are European energy and fiber cost volatility, plus the reformulation burden facing complex coated structures under future recyclability requirements.

Page last updated on: