Nordic Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

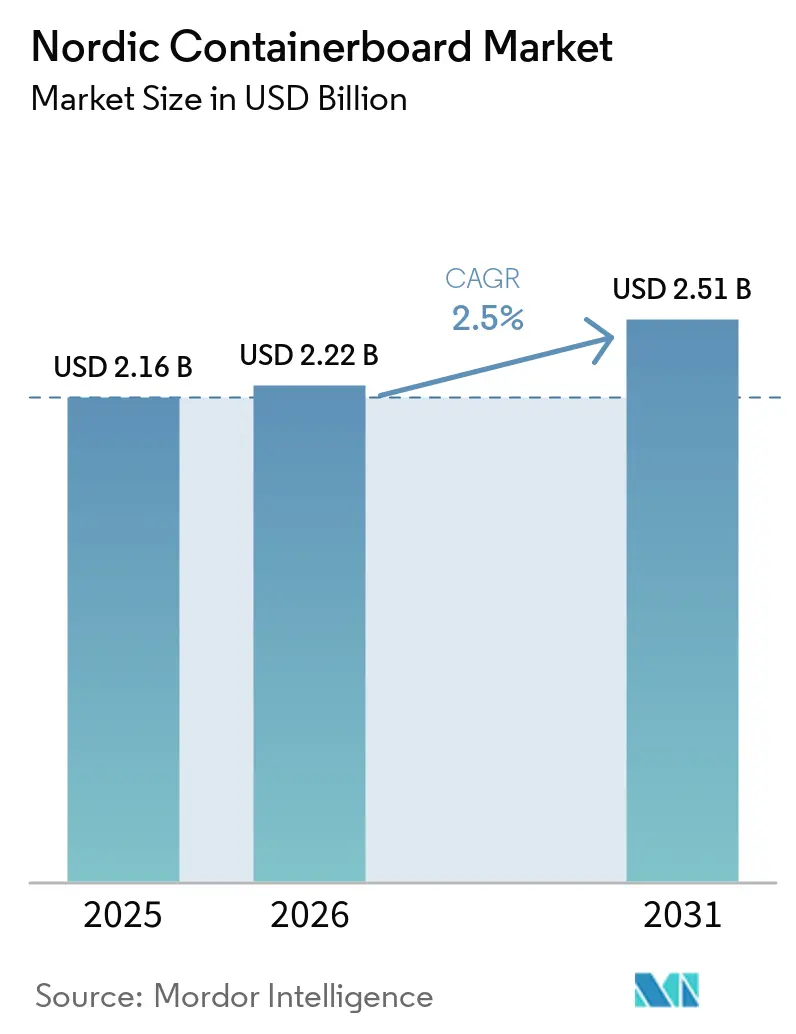

| Base Year Market Size (2025) | USD 2.16 Billion |

| Market Size (2026) | USD 2.22 Billion |

| Market Size (2031) | USD 2.51 Billion |

| Growth Rate (2026 - 2031) | 2.50% CAGR |

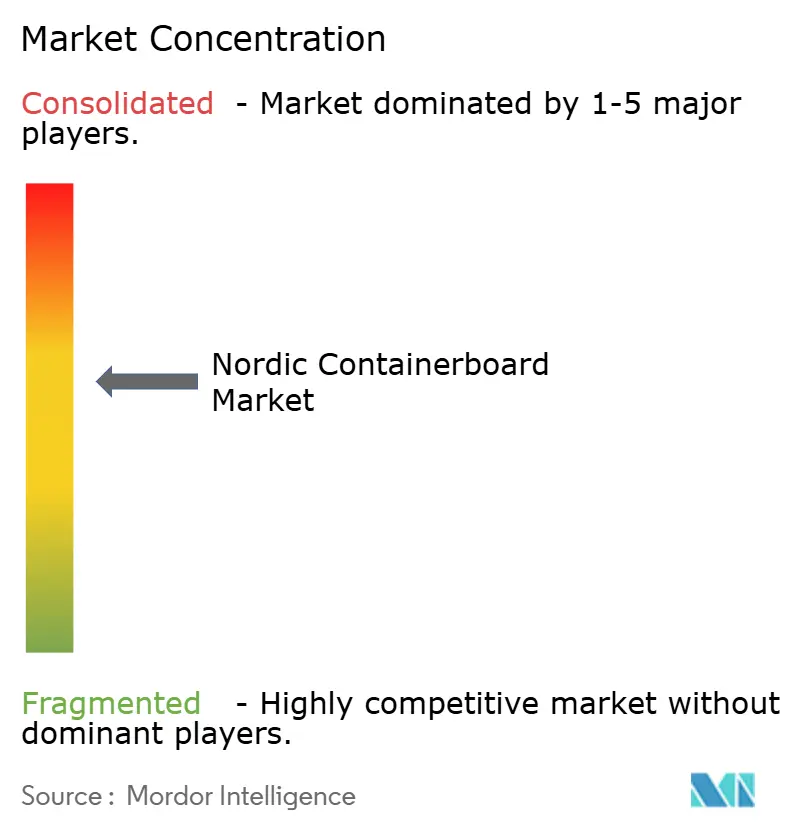

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nordic Containerboard Market Analysis by Mordor Intelligence

The Nordic containerboard market size is projected to expand from USD 2.16 billion in 2025 and USD 2.22 billion in 2026 to USD 2.51 billion by 2031, registering a CAGR of 2.50% between 2026 to 2031. The Nordic containerboard market is supported by the region's strong position in sustainably certified softwood fiber, which enables local producers to serve demanding export packaging needs for food, seafood, and industrial shipments. Growth is also tied to rules favoring recyclable packaging, rising online shopping volumes, and the wider use of recycled-content specifications by buyers across Europe. At the same time, the Nordic containerboard market continues to face pressure from structural oversupply in wider European board markets, limiting near-term pricing power. Demand conditions remain more durable in applications where performance, moisture resistance, and food-contact suitability matter more than lowest-cost sourcing alone. This leaves the Nordic containerboard market in a position where long-term demand support is clear, but near-term gains still depend on better regional supply discipline and firmer industrial demand.

Key Report Takeaways

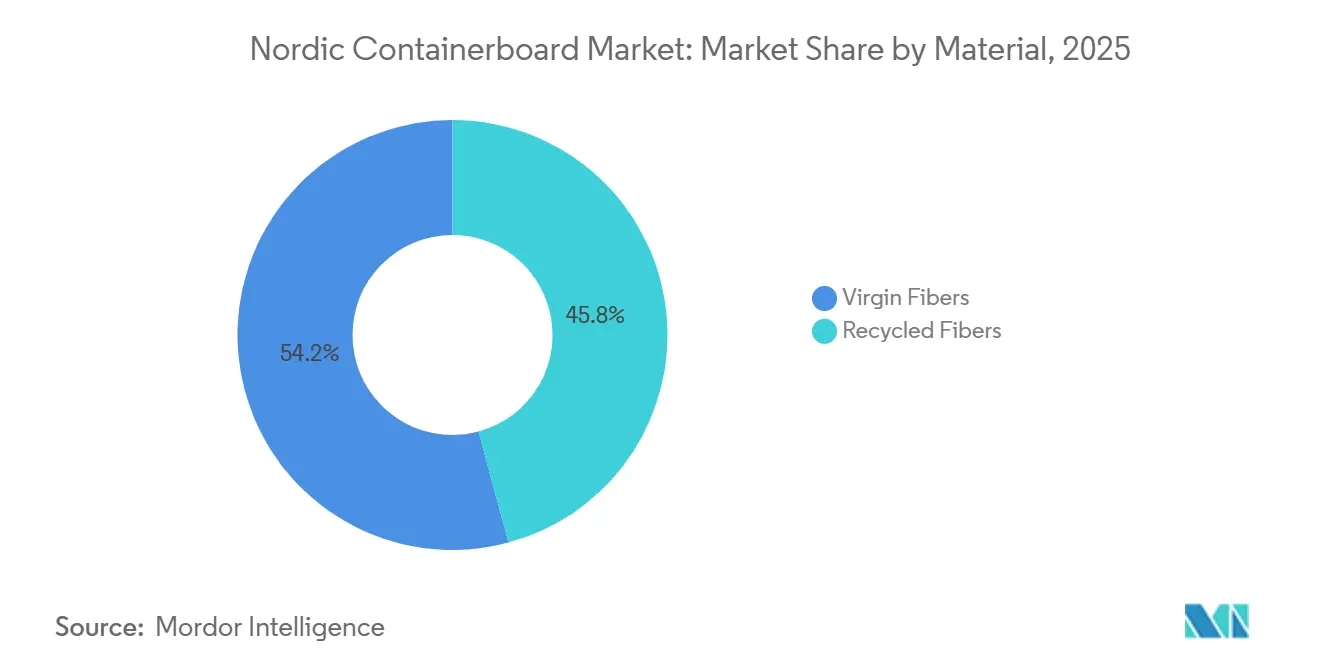

- By material, virgin fibers captured 54.19% of the Nordic containerboard market share in 2025.

- By product type, the Nordic containerboard market for testliners is forecast to grow at a 3.19% CAGR through 2031.

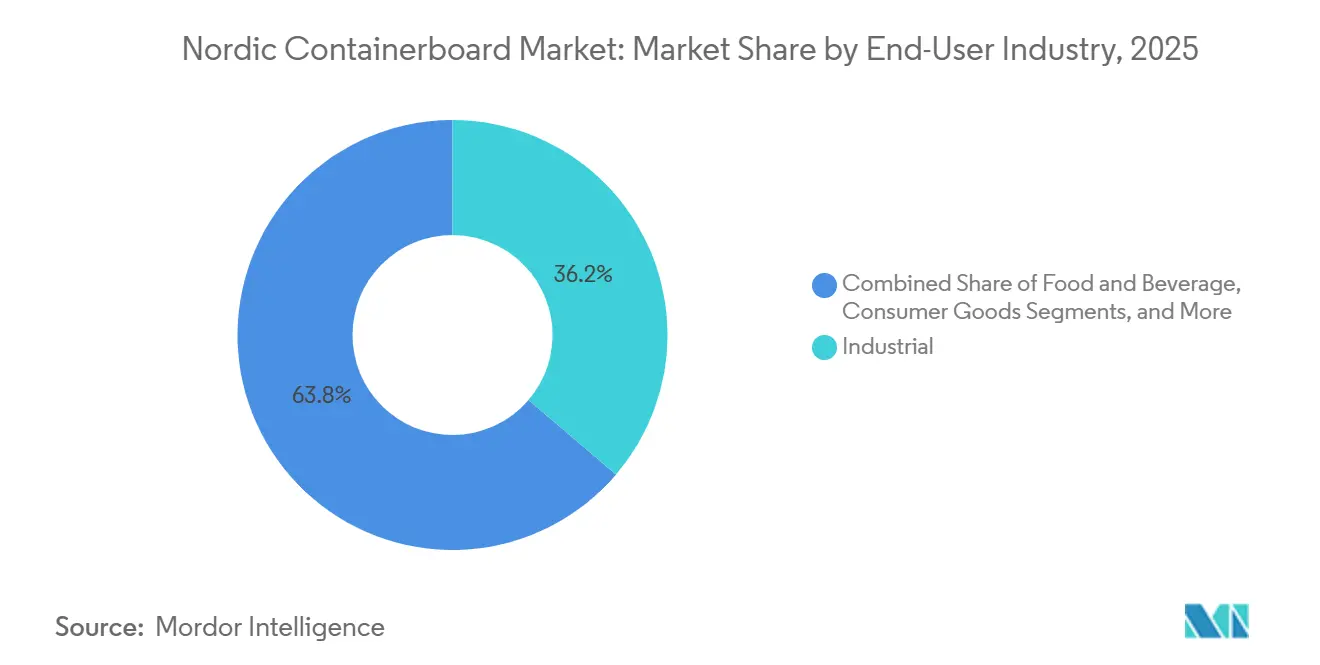

- By end-user industry, industrial captured 36.24% of the Nordic containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Nordic Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift From Plastic to Recyclable Fiber Packaging | +0.5% | EU-wide, with highest adoption velocity in Nordic and Central European markets | Short term (≤ 2 years) |

| Growth in Food and Beverage Packaging Demand | +0.4% | Nordic core markets, spill-over to export-oriented food processors in Sweden and Finland | Medium term (2-4 years) |

| E-Commerce and Parcel-Shipment Growth | +0.3% | Sweden, Denmark, Norway, Finland | Short term (≤ 2 years) |

| Demand for Recycled-Content Packaging in Europe | +0.3% | EU-wide, with procurement pressure concentrated in Sweden, Denmark, and the Netherlands | Medium term (2-4 years) |

| Nordic Seafood Export Packaging Needs for Wet-Strength and Moisture-Stable Grades | +0.2% | Norway and Iceland as origin markets, Asia-Pacific and North America as export destinations | Medium term (2-4 years) |

| Lightweighting Economics From High-Strength Nordic Virgin Fiber Grades | +0.1% | Global, with Nordic mills as primary technology and supply origin | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift From Plastic to Recyclable Fiber Packaging

The shift from plastic to recyclable fiber formats is one of the clearest supports for the Nordic containerboard market. Regulation EU 2025/40 entered into force on February 11, 2025, and its main provisions began applying from August 12, 2026, which has already changed how packaging buyers plan future material choices.[1]European Parliament and Council, “Regulation (EU) 2025/40 on Packaging and Packaging Waste,” Official Journal of the European Union, europen-packaging.eu Annex V of the regulation bans several single-use plastic packaging formats from January 1, 2030, including packaging for fresh produce under 1.5 kg, HORECA food service disposables, and grouped collation films, which opens more space for corrugated fiber-based substitutes. Cost-effectiveness is also important because Articles 6 and 44 tie future fee modulation to recyclability performance, creating a disadvantage for complex plastic formats that corrugated packaging does not face to the same degree. FEFCO reported in March 2026 that corrugated cardboard recycling in Europe exceeded 90%, which gives paper-based formats a strong compliance position as recyclability becomes a market-access condition.[2]FEFCO, “Recycling Performance of Corrugated Cardboard in Europe,” FEFCO, fefco.org Stora Enso has also stated that customer requests for plastic-to-fiber switching are increasingly linked to PPWR recyclability rules and related single-use plastics requirements, which shows that this change is already shaping procurement decisions rather than remaining a distant policy theme.

Growth in Food and Beverage Packaging Demand

Food and beverage packaging remains a durable volume base for the Nordic containerboard market because demand in this area is less exposed to swings in discretionary spending. SCA stated in its April 2026 investor presentation that fresh food and industrial applications together account for around 25% of global containerboard demand, which supports the importance of food-related packaging in the Nordic production mix.[3]SCA, “Investor Presentation,” SCA, sca.com The same presentation highlighted food-contact certified kraftliner grades at Obbola, including ISEGA-certified output, which helps preserve premium positioning in food processors' procurement. Metsä Board reported that the global packaging market grew by 3.9% annually, while paperboard was the fastest-growing material class at 4.2% over 2023 to 2028, supporting continued substitution toward fiber-based formats in packaged food applications. PPWR also bans PFAS-containing food-contact packaging from August 12, 2026, pushing buyers toward uncoated, intrinsically moisture-managed fiber substrates in categories where direct food-contact performance matters. Metsä Board further noted the weaker availability of high-quality de-inkable recycled fiber, which makes fresh fiber grades more attractive where contamination risk cannot be accepted.[4]Metsä Board Corporation, “Investor Presentation, Results for January-December 2025,” Metsä Board, metsagroup.com

E-Commerce and Parcel-Shipment Growth

E-commerce continues to support the Nordic containerboard market because parcel shipping raises corrugated box use more directly than many other retail channels. PostNord's Spring 2026 survey covered 4,000 consumers across Sweden, Denmark, Finland, and Norway and found that 86% had shopped online in the previous 30 days. The same survey showed that 71% had purchased from cross-border retailers in the previous 12 months, which is especially relevant because international deliveries often require stronger, more protective corrugated formats. PostNord also stated that 2025 marked a recovery year for Nordic household purchasing power as interest rates normalized and inflation stabilized, with Norway and Sweden showing the strongest retail momentum in the region. Stora Enso estimated a 3.3% CAGR for e-commerce packaging demand from 2024 to 2040, which is stronger than the broader packaging average and keeps transport packaging demand on a firmer path than several other end uses. This pattern particularly benefits testliner and fluting grades, which explains why the fastest product growth in the Nordic containerboard market sits in grades closely tied to standard shipper boxes.

Demand for Recycled-Content Packaging in Europe

Demand for recycled-content packaging is shaping the Nordic containerboard market through customer specifications rather than through a direct paper-specific legal quota. Many brand owners now include minimum recycled-fiber content in tenders for secondary packaging because retail customers and internal sustainability scorecards increasingly require it. PPWR sets recycled-content minimums for plastics rather than paper, but the practical outcome still benefits recycled paper grades, as buyers shifting away from plastic composites often prefer mono-material corrugated formats with visible post-consumer content claims. This is especially relevant in transport and secondary packaging, where performance demands are lower than in heavy export or direct food-contact uses, so recycled testliners and fluting grades can more easily meet specification requirements. FEFCO confirmed in March 2026 that corrugated cardboard remains Europe's most recycled packaging material and already exceeds the 85% paper and cardboard recycling target set for 2030 under PPWR. For exporters in the Nordic containerboard market, certified recyclability also works as a commercial argument in markets such as Germany and the Netherlands, where retail buyers expect clear environmental declarations from suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oversupply and Redirected Trade Flows in European Board Markets | -0.4% | EU-wide, concentrated in Nordic, Iberian, and Central European production regions | Short term (≤ 2 years) |

| Recovered Paper and Energy Cost Volatility | -0.4% | EU-wide, high exposure in Germany, France, Benelux, Nordics facing wood fiber cost variability | Medium term (2-4 years) |

| Packaging Minimization and Right-Sizing Under PPWR | -0.2% | EU-wide, directly affecting e-commerce and grouped packaging corrugated demand | Medium term (2-4 years) |

| EUDR Traceability Burden on Virgin-Fiber and Packaging Supply Chains | -0.2% | Nordic and Baltic virgin-fiber supply chains, affects all large and medium operators from December 30, 2026 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Oversupply and Redirected Trade Flows in European Board Markets

The biggest near-term constraint on the Nordic containerboard market is still structural oversupply across European board markets. Billerud described this imbalance in its Q3 2025 reporting as structural rather than cyclical, indicating the company viewed the issue as driven by industry capacity conditions rather than a short-lived demand dip. The company also linked pressure in Europe to redirected trade flows after tariffs changed export routes, pushing volumes that had been targeted for North America back into the European supply base. Billerud's containerboard net sales in Europe fell to SEK 4,982 million (USD 478 million) in 2025, from SEK 5,470 million (USD 525 million) in 2024, highlighting the oversupply's impact on both prices and volume realization. The Nordic containerboard market still has advantages in forest integration and higher-performance grades, but those strengths do not fully shield producers when too much board is chasing limited demand across Europe. Recovery is likely to depend on broader capacity discipline and a firmer industrial backdrop, which means pricing relief may come later than end-market demand stabilization.

Recovered Paper and Energy Cost Volatility

Recovered paper and energy cost volatility remain clear drags on the Nordic containerboard market, especially for producers with greater exposure to purchased inputs. The Bureau of International Recycling noted in 2025 that high energy costs in Germany, France, and the Benelux region were forcing shutdowns and lower production volumes, while the lack of a harmonized EU end-of-waste status for recovered paper continued to complicate cross-border trade. Nordic producers are somewhat better placed where own-forest integration lowers dependence on purchased recovered fiber, and Billerud reported that Nordic pulpwood prices fell by around 20% from the Q2 2025 peak by late 2025. Even so, Billerud's Q1 2026 report said that geopolitical tensions in the Middle East were increasing logistics and chemical costs, offsetting part of the pulpwood benefit. Metsä Board stated that it is around 90% energy self-sufficient, with 75% of energy coming from wood-based side streams and 18% from nuclear power, which underlines how important energy structure has become to competitive resilience. This leaves the Nordic containerboard market with a split cost profile, where integrated mills can manage shocks more effectively than players that remain exposed to external power and recycled-fiber price swings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Virgin Fiber Dominates, Recycled Grades Gain on Circularity Mandates

Virgin fiber held 54.19% of the Nordic containerboard market share in 2025, maintaining its leading position. That lead rests on the region's vertically integrated forest-to-board chains and on food-contact applications, where recycled grades still face more stringent acceptance tests. In seafood, fresh produce, and chilled food packaging, contamination concerns tied to mineral oils and printing ink residues continue to limit the extent to which recovered fiber can replace fresh fiber in direct-contact or moisture-sensitive applications. SCA's kraftliner deliveries increased by 6% to 948,000 tonnes in 2025, despite a difficult European market, demonstrating that premium virgin-fiber demand remained resilient where performance and certification mattered most. Metsä Board also stated that its white kraftliners serve a top-quality niche within the 12.5 million tonne global white linerboard category, with European deliveries up 4% in 2025.

Recycled fibers remain the fastest-moving material category, with the Nordic containerboard market for recycled fibers projected to expand at a 2.81% CAGR from 2026 to 2031. Growth is centered on secondary packaging and e-commerce outer packaging, where performance needs are lower, and buyers place greater value on circularity claims. This part of the Nordic containerboard industry is benefiting from procurement standards that increasingly ask for post-consumer fiber content in transport packaging sold into European retail and distribution chains. FEFCO's March 2026 assessment confirmed that corrugated cardboard recycling in Europe already exceeds 90%, providing recycled-grade suppliers with a strong, measurable circularity message in customer discussions. The result is a clear split in the Nordic containerboard market, with recycled grades gaining traction in secondary and transit formats, while virgin fiber remains the preferred choice for food-contact, export, and higher-risk packaging conditions.

By Product Type: Kraftliners Anchor Volume, Testliners Reflect Consumer Goods Acceleration

Kraftliners accounted for 40.25% share of the Nordic containerboard market size in 2025, making them the leading product type. Their lead reflects the region's long-established use of Nordic softwood pulp in high-strength linerboard production, and the premium role of food-contact-certified and wet-strength grades. SCA's Obbola mill reached its full 1,140,000 tonne annual capacity in 2026 and remains the largest individual kraftliner production site in Europe, which reinforces Sweden's importance in high-performance linerboard supply. SCA also introduced a 110 gsm grade of SCA Eurokraft white-top kraftliner, effective December 1, 2025, extending its offer into lighter-weight formats without sacrificing strength performance. In value terms, kraftliners remain especially important because premium grades support stronger margins than commoditized recycled linerboard in periods of weak market pricing.

Testliners are the fastest-growing product type, with the Nordic containerboard market size for testliners projected to rise at a 3.19% CAGR through 2031. Their growth follows the steady increase in e-commerce shipper boxes and consumer goods secondary packaging, where recycled-content corrugated formats are gaining share. As household purchasing power recovered and cross-border e-commerce stayed strong in the Nordics, lower-specification transit packaging became a more reliable source of incremental volume. Billerud is preparing for this trend by planning to install a new headbox on PM6 at Gruvön, with the next generation of Billerud Flute scheduled for commercial launch in H2 2026 to support stronger, more consistent fluting performance. That product work matters because flutings and testliners increasingly sit at the center of everyday parcel and shelf-ready packaging demand in the Nordic containerboard market.

By End-User Industry: Industrial Leads, Consumer Goods Builds Steady Momentum

Industrial accounted for 36.24% of the Nordic containerboard market share in 2025, making it the largest end-user segment. This leadership reflects the structure of Nordic export economies, where machinery, automotive components, process equipment, and energy-sector shipments need durable corrugated formats with high compression strength. Sweden, Finland, and Norway all ship goods over long distances and face demanding logistics cycles, which keep heavy-duty corrugated board relevant even when consumer demand softens. SCA has indicated that industrial and fresh food applications together account for around 65% of global kraftliner end use, which aligns with the weight of industrial packaging in regional board demand. The industrial segment also tends to favor virgin-fiber kraftliner and stronger wall constructions, which supports mills that focus on higher-performance rather than lowest-cost grades.

Consumer goods are projected to expand at a 3.05% CAGR from 2026 to 2031, making it the fastest-growing end-user category in the Nordic containerboard market. Growth comes from both e-commerce shipping and wider use of retail-ready corrugated packaging, where one format serves transport, shelf display, and replenishment needs. Stora Enso estimates that consumer products and e-commerce packaging will grow at 1.9% to 3.3% annually from 2024 to 2040, supporting continued growth in corrugated demand linked to packaged retail sales. Brands in processed foods, personal care, and home products are also moving away from plastic-heavy outer packaging as retailers tighten recyclable packaging expectations and PPWR raises compliance pressure on mixed-material packs. The Nordic containerboard market, therefore, benefits from a consumer goods shift that is less about one product launch cycle and more about how retail distribution and fulfillment are being redesigned around corrugated formats.

Geography Analysis

Sweden remains the main production anchor within the Nordic containerboard market because it hosts the region's largest and most advanced kraftliner assets. SCA's Obbola mill reached its full 1,140,000 tonne annual capacity in 2026, supported by direct access to long-fiber spruce and pine from more than 2.6 million hectares of owned forest land. Billerud also operates 5 containerboard and packaging board mills in Sweden, namely Gruvön, Gävle, Frövi-Rockhammar, Skärblacka, and Karlsborg, with a combined European production capacity of around 3.1 million tonnes per year. Swedish producers faced a difficult 2025 as pulpwood prices stayed elevated through Q2 before falling by around 20% by year-end, underscoring how exposed even strong integrated systems remain to raw-material cycles. Billerud responded with an annualized SEK 800 million (USD 81.5 million) cost-saving program, with SEK 500 million (USD 48.0 million) expected as 2026 savings, which shows how the Swedish base is adjusting to structurally lower board pricing.

Finland is the leading investment growth center in the Nordic containerboard market. Stora Enso completed its EUR 1.1 billion (USD 1.19 billion) Oulu investment in August 2025, creating Europe's largest and most modern consumer packaging board production line with an annual capacity of 750,000 tonnes. The company has said the line uses FiberLight Tec technology, cuts fossil CO2 emissions by 90%, and is expected to generate EUR 800 million (USD 864 million) in annual sales at full capacity by 2027. Metsä Board also renewed its Simpele mill in 2025 and has emphasized that its system is around 90% energy self-sufficient, with 18% from nuclear power and 75% from wood-based side streams, which gives Finnish producers a steadier cost base than many continental peers. This makes Finland important not only for capacity expansion, but also for a lower-carbon, more energy-stable board supply to Baltic and Central European demand centers.

Norway and Denmark represent two very different demand profiles within the Nordic containerboard market. Norway supports a specialized niche in wet-strength, moisture-stable linerboard because seafood exports require corrugated packaging that withstands icing, condensation, cold-chain handling, and long-distance air freight. VPK Packaging AS documented that its PetaFresh seafood packaging transports fish products to North American and Asian markets on routes above 4,000 km, which illustrates the commercial depth of this niche. Denmark, by contrast, is the most e-commerce-intensive Nordic market, with 82% of consumers making at least 1 international online purchase in 2025. That pattern keeps Danish demand closely tied to testliner and fluting consumption in fulfillment and parcel distribution, while Norway leans more heavily toward higher-performance packaging grades.

Competitive Landscape

The Nordic containerboard market has a moderately concentrated production base, with SCA, Stora Enso, Metsä Board, and Billerud forming the core group that shapes capacity, product quality, and cost positioning. SCA holds the leading position as Europe's independent kraftliner producer, with 1,140,000 tonnes per year of capacity at Obbola, giving it significant scale in premium virgin-fiber linerboard. Stora Enso has stated that it ranks No. 3 globally in virgin fiber containerboard and No. 2 in recycled containerboard, underscoring how closely the Nordic supply base is tied to large multinational players rather than small regional mills. Multinational competitors such as International Paper, after completing the acquisition of DS Smith in 2024, and other pan-European corrugated groups still matter because they can serve Nordic customers through converting and distribution networks beyond the region's own mills. This means the Nordic containerboard market is concentrated at the production level, but competition remains active at the customer interface because broad European packaging groups also shape commercial access.

Competition in the Nordic containerboard market is increasingly built around cost control, energy performance, and product differentiation rather than simple volume growth. Metsä Board's Lead the Pack 2026-2030 strategy targets EUR 200 million (USD 216 million) in annual EBITDA improvement by the end of 2027 through procurement, productivity, and commercial measures. Billerud's annualized SEK 800 million (USD 81.5 million) savings program shows a similar focus on lowering the cost base, ensuring operations remain viable amid structurally weaker European pricing. Stora Enso has invested heavily to strengthen its competitive position, first through the Oulu consumer board line and then through the EUR 30 million (USD 33.8 million) bioenergy conversion at Heinola, which reduced fossil CO2 emissions by more than 90% at that mill. These moves show that leading suppliers are trying to defend margins through technology, carbon performance, and manufacturing scale rather than relying on a quick pricing rebound.

A second layer of competition sits in specialized grades where non-Nordic producers have a harder time matching the same mix of fiber quality, geography, and certification. Seafood export packaging is a good example because wet-strength and moisture-stable linerboard works best when mills can draw on high-strength virgin fiber and stay close to Nordic fish processing and export routes. Low-carbon positioning is also becoming more visible in buyer decisions, and both Stora Enso and Metsä Board are pushing near-fossil-free or strongly reduced-emission production as a commercial advantage. Billerud's net-zero target by 2050 received formal approval from the Science Based Targets initiative in November 2025, further strengthening the region's sustainability positioning in customer discussions. As a result, the Nordic containerboard market remains competitive, but leadership is increasingly tied to integrated fiber access, energy resilience, and the ability to translate sustainability performance into customer preference.

Nordic Containerboard Industry Leaders

Stora Enso Oyj

Svenska Cellulosa Aktiebolaget SCA

Smurfit Westrock plc

Metsa Board Corporation

Billerud Aktiebolag

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Metsä Board showcased its Muoto molded fiber packaging solution at Interpack 2026 in Düsseldorf, Germany, highlighting the company's expansion into formed fiber tray applications for food service and consumer goods categories beyond its core kraftliner product range.

- April 2026: Metsa Board announced the acquisition of the Winschoten sheeting and distribution center in the Netherlands, strengthening supply chain flexibility and supporting utilization at the Husum white kraftliner mill in Sweden. The company simultaneously announced its "Lead the Pack" 2026-2030 strategy, targeting an annual EBITDA run-rate improvement of EUR 200 million (USD 216 million) by the end of 2027.

- April 2026: Fiberdom, a Finnish wood fiber innovation company, completed industrial pilot trials of its Duranova plastic-free material using a continuous reel-to-reel pilot line with Vits Technology GmbH in Germany, demonstrating industrial scalability for PPWR-aligned fiber-based packaging applications.

- March 2026: Metsä Board launched its "Lead the Pack" 2026-2030 corporate strategy at a capital markets event, outlining a two-phase program focused first on EUR 200 million (USD 225.7 million) in EBITDA recovery and then on expansion in brand-enhancing consumer packaging segments.

Nordic Containerboard Market Report Scope

The Nordic Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Nordic Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size and forecast for the Nordic containerboard market?

The Nordic containerboard market was valued at USD 2.16 billion in 2025, is projected at USD 2.22 billion in 2026, and is expected to reach USD 2.51 billion by 2031 at a CAGR of 2.50%.

Which material type leads demand in Nordic containerboard?

Virgin fiber led with 54.19% share in 2025 because food-contact safety, wet-strength performance, and export packaging needs still favor fresh fiber grades in many applications.

Which product category is growing fastest across the Nordics?

Testliners are the fastest-growing product type, with a projected CAGR of 3.19% from 2026 to 2031, supported by e-commerce shipping and consumer goods secondary packaging demand.

Why is food and beverage packaging important for regional board producers?

Food and beverage packaging provides a stable demand base because it is less exposed to cyclical consumer spending and increasingly favors certified, recyclable, and PFAS-free fiber solutions.

How is e-commerce affecting boxboard and corrugated demand in the Nordics?

Online shopping remains a major demand driver. In Spring 2026, 86% of consumers in the 4 core Nordic markets had shopped online in the previous 30 days, and 71% had bought cross-border in the prior year.

Which end-user segment is largest, and which is expanding fastest?

Industrial was the largest end-user segment with 36.24% share in 2025, while consumer goods is the fastest-growing segment with a projected 3.05% CAGR through 2031.

What is the biggest near-term challenge for producers in the region?

Structural oversupply in European board markets remains the main near-term challenge because it weakens pricing power even for Nordic mills with strong fiber integration and premium product positioning.

Page last updated on: