Poland Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

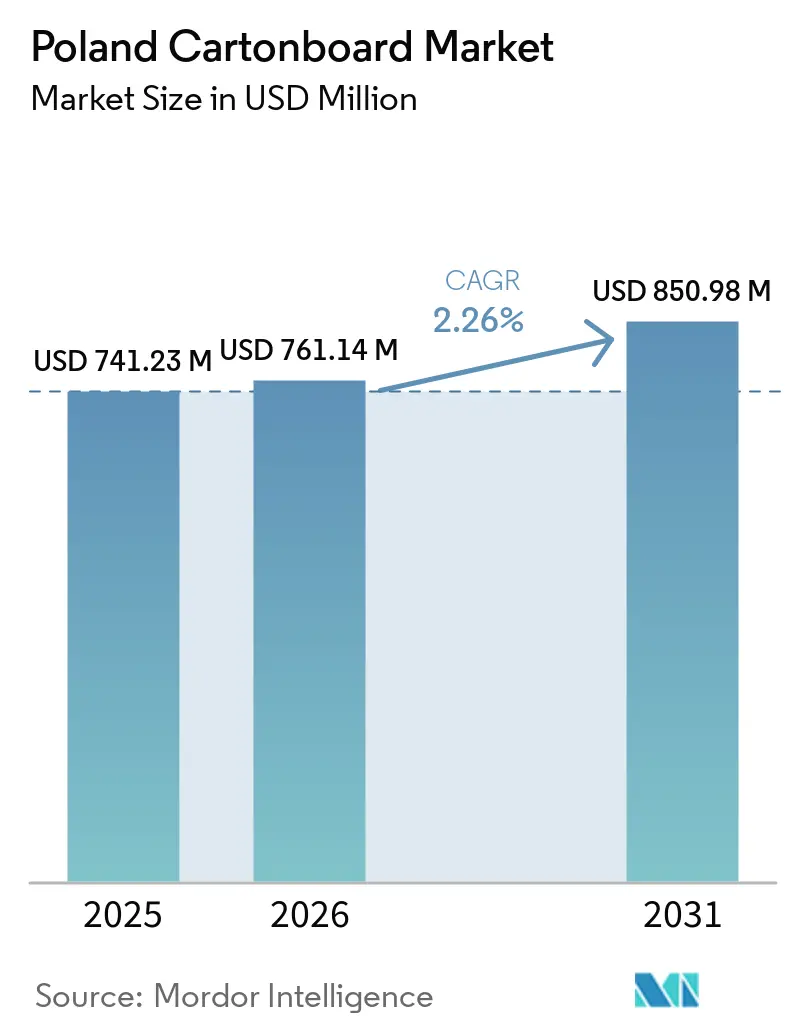

| Base Year Market Size (2025) | USD 741.23 Million |

| Market Size (2026) | USD 761.14 Million |

| Market Size (2031) | USD 850.98 Million |

| Growth Rate (2026 - 2031) | 2.26% CAGR |

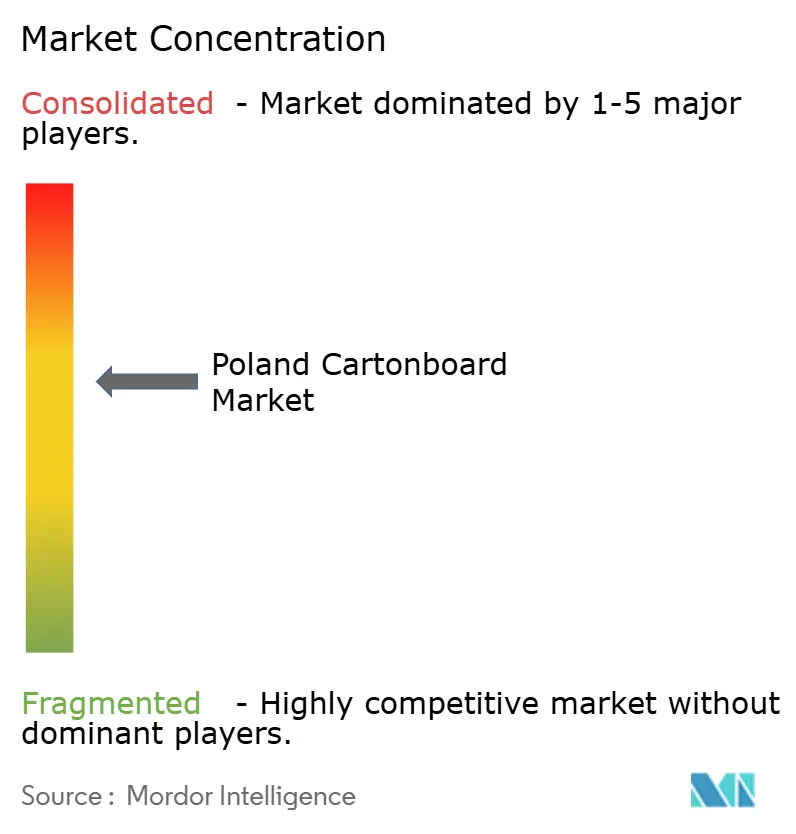

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Cartonboard Market Analysis by Mordor Intelligence

The Poland Cartonboard Market size is expected to increase from USD 741.23 million in 2025 to USD 761.14 million in 2026 and reach USD 850.98 million by 2031, growing at a CAGR of 2.26% over 2026-2031.

The Poland cartonboard market is being supported by two linked forces, the shift from plastic to paper under the EU Packaging and Packaging Waste Regulation and Poland’s stronger role as a Central European production and export base. This policy setting is turning sustainability from a brand preference into a compliance requirement, which supports demand for cartonboard in food, pharmaceutical, and consumer goods packaging. Poland’s expected GDP growth in 2025 and 2026 also provides a stable demand base for converters, even while fiber, energy, and logistics costs continue to pressure margins. Competition in the Poland cartonboard market is moving away from basic grade availability and toward technical service, short-run digital print capability, and documentation that supports extended producer responsibility compliance. The clearest opportunities remain in pharmaceutical cartons, liquid packaging formats, and export-oriented food packs that need traceable, recyclable, and high-specification cartonboard solutions.

Key Report Takeaways

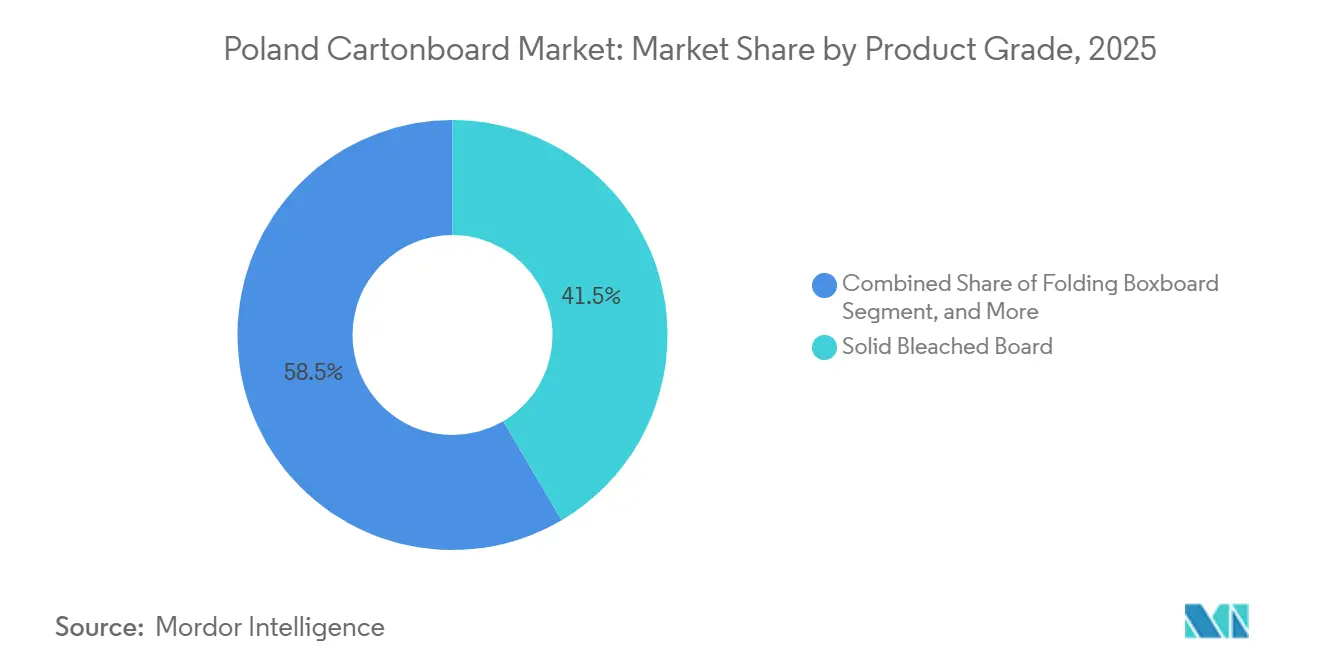

- By product grade, Solid Bleached Board (SUB) held 41.52% share of the Poland cartonboard market in 2025, while Solid Unbleached Board (SUB) is forecast to expand at a 6.65% CAGR through 2031.

- By packaging format, folding cartons accounted for 54.34% of the Poland cartonboard market size in 2025, while liquid packaging is projected to grow at a 6.12% CAGR through 2031.

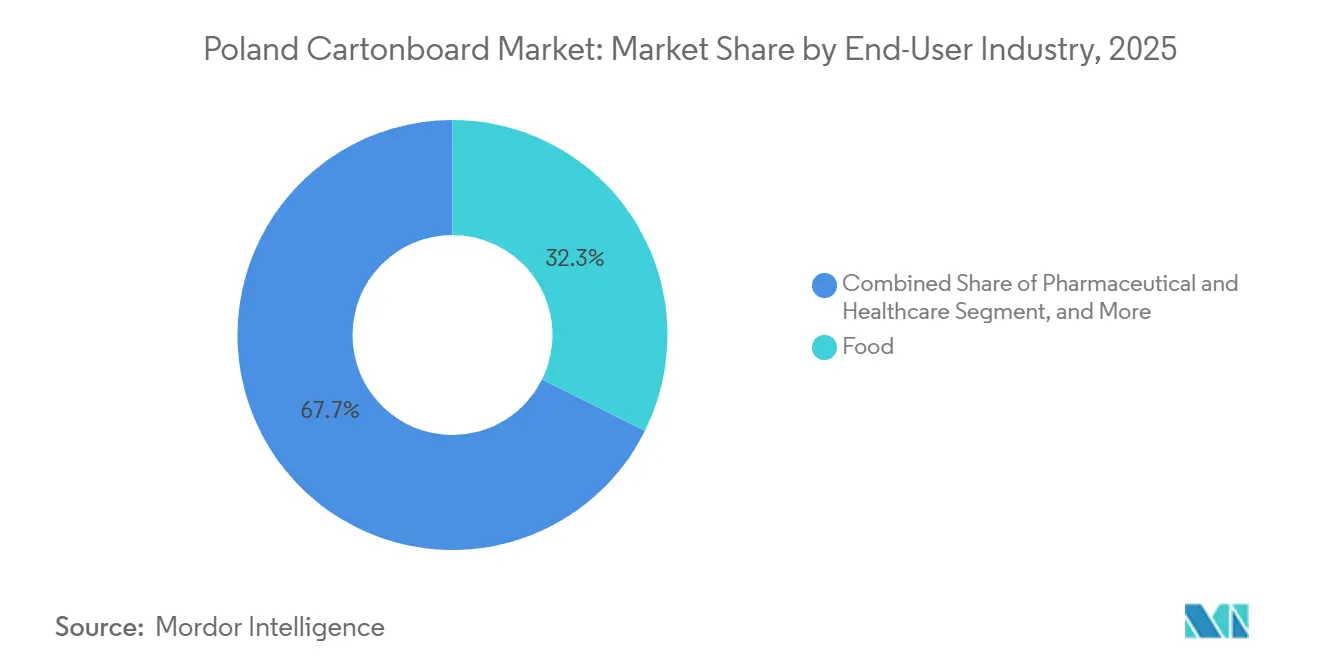

- By end-user industry, food held 32.34% of the Poland cartonboard market share in 2025, while healthcare and pharmaceuticals recorded the highest projected CAGR at 6.82% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Poland Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic-To-Paper Substitution Under PPWR And SUP Rules | +0.8% | EU-wide mandate with near-term concentration in food and foodservice categories across Mazovia and Silesia industrial zones | Short term (≤ 2 years) |

| Expanding Food Export And Domestic Food Pack Demand | +0.5% | National, with strongest flows from Mazovia, Greater Poland, and Pomerania agri-processing hubs | Medium term (2-4 years) |

| E-Commerce And E-Grocery Growth Supporting Folding Cartons | +0.4% | Concentrated in Warsaw, Kraków, Wrocław, and Gdańsk urban centers, spill-over to central Polish logistics corridors | Short term (≤ 2 years) |

| Pharmaceutical Capacity Expansion Supporting Compliance-Grade Cartons | +0.3% | Concentrated in Gdańsk, Poznań, and Łódź pharmaceutical manufacturing corridors | Medium term (2-4 years) |

| Ostrołęka Recycling Hub De-Risking Liquid Packaging Board Adoption | +0.2% | National, with spill-over capacity absorption from Czech Republic, Hungary, and Slovakia | Medium term (2-4 years) |

| Poland's Export Manufacturing Role Attracting Nearshored Packaging Demand | +0.2% | Cross-border, with primary flows to Germany, Netherlands, and France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plastic-To-Paper Substitution Under PPWR And SUP Rules

The Poland cartonboard market is receiving direct support from the PPWR because the rule set starts applying broadly from August 12, 2026 and places packaging choices under formal compliance review. The regulation requires recyclability assessment, a Declaration of Conformity, and document retention for multiple years, which makes established fiber-based formats easier to deploy than materials that still need fresh qualification work.[1]KH Law, “The New EU Packaging and Packaging Waste Regulation - Highlights and Challenges Ahead,” KH Law, khlaw.com The Single-Use Plastics Directive also narrows the practical design space for plastic packs in takeaway and foodservice uses, where folding boxboard and food service board already fit common converting lines. In the Poland cartonboard market, that matters because converters can now position recyclability as a compliance feature instead of a marketing claim. The EN 18120 standards published in May 2026 provide the technical framework used for PPWR recyclability assessments, which lowers requalification friction for cartonboard grades that already have certified pathways.[2]Pulp and Paper News, “PPWR Gains Technical Framework Through New EN 18120 Standards,” Pulp and Paper News, pulpapernews.com This timing gives incumbent suppliers in the Poland cartonboard market a clear near-term advantage when brand owners need pack redesigns completed before the wider PPWR compliance window takes hold.

Expanding Food Export And Domestic Food Pack Demand

The Poland cartonboard market is closely tied to food exports because rising shipment volumes directly lift demand for branded, protective, and shelf-ready packaging. In the first 10 months of 2025, Polish agri-food exports reached EUR 48.5 billion, USD 52.9 billion, and grew 8% year on year, with poultry, dairy, and confectionery among the leading categories. Export mix is also becoming more valuable for cartonboard because higher shipments to Germany, France, and the Netherlands favor packs that need stronger print quality and more formal retail presentation. That supports SBS and folding boxboard demand in the Poland cartonboard market more than low-cost recycled grades used in simpler transport packs. Domestic retail modernization adds another layer of demand because discount and convenience chains continue to expand unit-based packaging across impulse and ready-to-eat categories. The January 2026 extension of Poland’s deposit return framework to milk and dairy beverage containers also supports liquid packaging board adoption inside the food packaging chain.

E-Commerce And E-Grocery Growth Supporting Folding Cartons

The Poland cartonboard market is also gaining from e-commerce because online retail keeps taking share from physical channels in several packaged goods categories. Allegro reported 11.6% year-on-year gross merchandise value growth in Q1 2026 and had 15.5 million active buyers in Poland, which shows continued scale growth in the local online channel. That shift raises carton demand because direct-to-consumer shipments often need packs that work as both sales packaging and transit packaging. In the Poland cartonboard market, this tends to raise caliper, raise print requirements, and create more redesign work for converters. Allegro’s full-year 2025 GMV in Poland approached PLN 70 billion, USD 17.5 billion, and the platform is expanding into adjacent categories including healthcare and travel. PPWR right-sizing requirements for e-commerce packaging from August 2026 should further support cartonboard-based pack development that reduces void space while keeping packs recyclable.

Pharmaceutical Capacity Expansion Supporting Compliance-Grade Cartons

The Poland cartonboard market is seeing stronger pharmaceutical demand because new domestic drug production requires compliant secondary packaging with print accuracy and traceability. Polpharma launched a PLN 238.7 million, USD 62 million, RNA-based medicines manufacturing platform in Starogard Gdańsk in May 2026, creating a full API-to-finished-goods chain that raises local demand for folding cartons. Public support is also strengthening the broader production base, with the Warsaw CeTeAPI project and EU-backed strategic autonomy programs improving Poland’s position in reshored pharmaceutical manufacturing. These projects support the Poland cartonboard market because regulated medicines need serialization, braille, tamper-evidence, and stable print reproduction. Compliance under the EU Falsified Medicines Directive and ISO 15378 packaging quality systems favors converters with documented operating controls and validated processes. That makes pharma cartons one of the clearest higher-value pockets in the Poland cartonboard market over the forecast period.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy And Fiber Cost Volatility Pressuring Converter Margins | -0.3% | EU-wide, with Central European mills, including Poland, among the most exposed due to high natural gas dependency in recycled-grade production | Short term (≤ 2 years) |

| Board Price Swings And Supply Tightness In European Sourcing | -0.2% | Global, with concentrated impact on Polish converters sourcing virgin-fiber grades from Nordic and Austrian suppliers | Medium term (2-4 years) |

| EPR Fee Uncertainty During The 2026-2027 Transition | -0.1% | National, Poland, with spill-over implications for cross-border converters supplying the Polish market | Short term (≤ 2 years) |

| PFAS And Barrier-Coating Reformulation Costs For Foodservice Packs | -0.1% | EU-wide, with near-term cost burden concentrated on foodservice and quick-service restaurant pack formats using fluorinated barrier coatings | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Energy And Fiber Cost Volatility Pressuring Converter Margins

The Poland cartonboard market continues to face cost pressure from energy, fiber, and logistics inputs that do not move in a stable way. Euro Area producer prices in pulp and paper manufacturing stood at 110.40 index points in March 2026, showing that the broader input environment remains elevated for downstream buyers. When board costs rise faster than contract resets, converters in the Poland cartonboard market struggle to defend margins, especially in food and consumer goods supply agreements. This is more visible for independent converters because they do not have the same fiber integration or energy assets as large board producers. Mayr-Melnhof is continuing work on the Kwidzyn continuous pulp digester and expects the project to reduce carbon dioxide emissions by around one-third by the end of 2026, which underlines the structural advantage of integrated capacity in a high-cost cycle. If input volatility persists, the Poland cartonboard market is likely to see more share shift toward producers that can absorb cost swings through scale, integration, or long-term energy planning.

Board Price Swings And Supply Tightness In European Sourcing

The Poland cartonboard market is exposed to European supply tightness because a large share of virgin-fiber and specialty grades is sourced from outside Poland. Reno de Medici announced a EUR 50 per tonne increase for coated board grades effective January 2025, which shows that board pricing had already been moving upward before the current 2026 cost cycle. Smurfit Westrock stated in its Q1 2026 results that containerboard prices increased in March and April 2026, linking price firming to energy costs and demand conditions in the region. For the Poland cartonboard market, the main issue is timing because board procurement, production runs, and customer price negotiations often move on different schedules. That creates a lag between when converters face higher input bills and when they can recover those costs from customers. In practice, this sourcing pattern favors larger converters in the Poland cartonboard market that can negotiate supply agreements, carry more working capital, or diversify purchases across several mills.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Solid Bleached Board Holds Premium Packaging While CUK Gains Momentum

Solid Bleached Board (SBB) accounted for 41.52% of the Poland cartonboard market size in 2025, which made it the leading product grade by value. The grade remained strong because pharmaceutical packs, premium food cartons, and cosmetics packaging still require high brightness, strong print quality, and stable barrier performance. In the Poland cartonboard market, SBB is also favored where serialization, braille, and precise regulatory text must be printed without loss of clarity in production runs linked to medicines and health products. Folding boxboard remained the main volume grade for a broad set of food and retail uses because it balances stiffness, weight, and pack economics well. WLC kept its role in secondary packs and shelf-display formats, but converters stayed exposed to cost pressure when recycled-grade production economics tightened across Europe.

Solid Unbleached Board (SUB) is forecast to expand at a 6.65% CAGR through 2031, making it the fastest-growing product grade in the Poland cartonboard market. Its strength-to-weight profile and recyclability fit well with eco-design scoring under the PPWR, especially in chilled food and beverage packs where plastic substitution is now a practical design goal. This is one area where the Poland cartonboard industry is moving toward performance grades that can meet both logistics needs and recyclability checks. Food service board and liquid packaging board remain smaller segments, but both are receiving more attention as converters prepare for PPWR and food-contact material changes. The Poland cartonboard industry is also seeing more interest in fiber-based alternatives that can replace plastic-heavy pack structures without forcing brand owners into a full redesign of their filling or retail systems.

By Packaging Format: Folding Cartons Lead While Liquid Packaging Expands Faster

Folding cartons held 54.34% of the Poland cartonboard market size in 2025, which kept this format at the center of demand across food, pharmaceuticals, cosmetics, and e-commerce. The format has remained resilient because it serves many end users at once and allows converters to spread risk across consumer, health, and export-linked categories. In the Poland cartonboard market, folding cartons are also benefiting from redesign work as brands adjust pack dimensions, material declarations, and recyclability claims under the PPWR. Sleeve and tray formats kept meaningful volume in fresh and frozen food because they fit retailer-ready display needs and cross-border food shipments. Strong food exports also supported these formats because Western European retailers continue to favor shelf-ready packs with consistent presentation standards.

Liquid packaging is projected to grow at a 6.12% CAGR through 2031, making it the fastest-growing format in the Poland cartonboard market. Poland’s deposit return system for beverage containers has been in operation since October 2025 and its January 2026 extension to milk and dairy containers strengthens the collection logic that supports liquid board adoption. The Ostrołęka recycling hub reduces end-of-life uncertainty for beverage cartons, which matters when producers need defensible recycling pathways in their compliance files. Other formats, including cups and foodservice containers, face near-term reformulation work because PFAS-related restrictions are forcing a move toward alternative barrier systems. Even with that cost burden, the Poland cartonboard market should continue to see format innovation where fiber-based packs can replace hard-to-recycle plastic items.

By End-User Industry: Food Leads Demand While Pharmaceuticals Grow Faster

Food held 32.34% of the Poland cartonboard market share in 2025 and remained the largest end-user segment by value. That position reflected Poland’s role as a major EU agri-food exporter and its large domestic food processing base. In the Poland cartonboard market, food demand is wide rather than narrow because it spans confectionery, dairy, poultry, chilled products, frozen products, and convenience items sold through both retail and export channels. As exporters push more branded and shelf-ready products into Germany, France, and the Netherlands, specification needs are moving upward toward SBS and FBB rather than basic low-cost formats. Beverage packaging also remains important because deposit return collection systems are giving liquid packaging board a stronger circularity case in the food value chain.

Healthcare and pharmaceuticals are forecast to grow at a 6.82% CAGR through 2031, which makes them the fastest-growing end-user group in the Poland cartonboard market. Demand is rising because new local drug manufacturing capacity increases output of regulated products that need compliant cartons with traceability features. The Poland cartonboard industry benefits here because entry barriers are higher than in standard food packaging, especially when customers require audited quality systems and repeatable print control. Tobacco packaging still contributes value because premium print and barrier specifications remain important, even though cigarette consumption presents a long-term volume headwind. Cosmetics and toiletries form another stable mid-tier segment where premium appearance and ingredient transparency continue to favor folding cartons over flexible formats. Other end users, including toys, apparel, household products, electrical items, foodservice, and automotive components, add a steady base of demand as e-commerce and export packaging needs widen across the Poland cartonboard market.

Geography Analysis

Poland accounted for 10.4% of total EU packaging export volumes in 2025, which shows how strongly the Poland cartonboard market is tied to regional trade flows rather than only domestic consumption. The main consumption corridors remain Greater Poland, Mazovia, Lower Silesia, and Pomerania, where food processing, pharmaceuticals, logistics, and export manufacturing are concentrated.[3]Fachpack, “Dynamics and Future Prospects for the Polish Packaging Market,” Nuremberg Messe, fachpack.de This makes the Poland cartonboard market more sensitive to German, Dutch, and French demand cycles than a purely domestic packaging market would be. Poland’s broader economic setting is still supportive, with the European Commission projecting GDP growth of 3.2% in 2025 and 3.5% in 2026. Even so, converters remain exposed to exchange-rate and transport costs because imported SBS and FBB are often invoiced in EUR while a significant share of local revenues stays in PLN.

Pomerania and the wider Gdańsk corridor are becoming more important to the Poland cartonboard market because pharmaceutical manufacturing and biologics investment are deepening in the north. Polpharma’s new RNA platform in Starogard Gdańsk strengthens this corridor and adds demand for secondary pharmaceutical cartons with high print control. Mazovia remains the main e-commerce and fulfillment zone, which keeps folding carton demand high around Warsaw and along central logistics routes. Ostrołęka adds another regional feature because its recycling and board-related infrastructure supports liquid packaging circularity and improves domestic recovery economics for fiber-based packs.

Poland’s location next to Germany supports the Poland cartonboard market by making the country a practical nearshore converting base for Western European brand owners. Germany alone imported EUR 12.3 billion, USD 13.4 billion, of Polish food products in the first 10 months of 2025, which keeps packaging demand closely linked to export order flow.[4]Polish Investment and Trade Agency, “Poland's Food Exports on the Rise,” Polish Investment and Trade Agency, trade.gov.pl As PPWR compliance work intensifies, Poland offers a verifiable manufacturing environment inside the EU, which supports its role in regulated packaging supply chains. Smaller regions such as Lublin and Subcarpathia also contribute incremental demand through food processing and pharmaceutical activity, but their density remains lower than the main western and central industrial corridors.

Competitive Landscape

The Poland cartonboard market has a split structure in which large European board producers supply virgin-fiber and recycled grades while a fragmented group of Polish and regional converters competes for customer contracts. The main large suppliers active in the Poland cartonboard market include Mayr-Melnhof Karton AG, Stora Enso Oyj, Metsä Board Corporation, Holmen AB, and Reno de Medici S.p.A. Mayr-Melnhof’s Kwidzyn mill remains the most important domestic board asset because it links pulp production, cartonboard output, and newer fiber-based packaging capabilities in one location. In 2025, capital expenditure across MM Board and Paper reached EUR 123.1 million, USD 134.2 million, and the Kwidzyn continuous pulp digester is expected to complete by the end of 2026. That level of integration gives large producers a stronger cost position in the Poland cartonboard market when independent converters face board shortages or energy-driven price pressure.

Competitive strategy in the Poland cartonboard market is increasingly centered on compliance support, digital printing flexibility, and access to stable board supply. Mayr-Melnhof is also building out plastic-substitution capability through molded pulp at Kwidzyn, which broadens its offer to customers looking for fiber-based pack redesigns. Reno de Medici launched Vincicoat Plus in March 2026, a coated recycled board grade designed to cut packaging weight by up to 20%, which increases pressure on virgin-fiber grades in several retail and food applications. Smurfit Westrock is also adapting its European system after the 2024 combination and is targeting growth through innovation, sustainability, and service in e-commerce and industrial packaging.

Stora Enso is reviewing parts of its Central European setup while ramping its large Oulu consumer board line, and that change will continue to affect available folding boxboard supply across Europe. In the Poland cartonboard market, this means supply dynamics are shaped not only by local demand, but also by strategic decisions made at the European producer level. Smaller converters such as DOT2DOT S.A., Akomex Sp. z o.o., and KARTON-PAK CIESZYN Sp. z o.o. remain relevant because they compete on speed, customer proximity, and specialist execution rather than scale. The strongest open spaces remain pharmaceutical compliance cartons and recyclable liquid packaging formats, where customer qualification work is more demanding and price competition is less purely transactional.

Poland Cartonboard Industry Leaders

Mayr-Melnhof Karton AG

Stora Enso Oyj

Graphic Packaging International, LLC

Metsä Board Corporation

Holmen AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Polpharma launched its PLN 238.7 million (USD 62 million) RNA-based medicines manufacturing platform in Starogard Gdańsk, creating an integrated API-to-finished-goods pharmaceutical production chain and materially expanding demand for GMP-compliant folding cartons with serialization and tamper-evidence features in northern Poland.

- May 2026: Allegro reported Q1 2026 GMV growth of 11.6% year-on-year in Poland, more than twice the pace of overall nominal retail sales, sustaining folding carton demand in e-commerce fulfillment and e-grocery channels across the Warsaw, Kraków, and Wrocław logistics corridors

- March 2026: Mayr-Melnhof accelerated its Fit-For-Future transformation program, targeting a EUR 250 million (USD 282.5 million) earnings uplift by 2027 relative to 2024, and the group planned EUR 250 million (USD 282.5 million) in capital expenditure for 2026, with continued progress on the Kwidzyn continuous pulp digester expected to complete by end-2026.

- January 2026: Poland's deposit return system extended to milk and dairy beverage containers, broadening certified recycling infrastructure to dairy liquid packaging board and expanding the addressable market for compliant liquid packaging board grades across the food sector.

Poland Cartonboard Market Report Scope

The Poland Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The Poland Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, Other Packaging Formats), End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, Other End-User Industries). The Market Forecasts are in Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

Key Questions Answered in the Report

What is the current and forecast value of the Poland cartonboard market?

The Poland cartonboard market was valued at USD 741.23 million in 2025 and is projected to reach USD 850.98 million by 2031, growing at a 2.26% CAGR over 2026-2031.

Which product grade leads demand in Poland?

Solid Bleached Board (SBB) led by value with a 41.52% share in 2025 because it fits pharmaceutical, premium food, and cosmetics packs that need strong print quality and barrier performance.

Which packaging format is growing the fastest in Poland?

Liquid packaging is the fastest-growing format, with a projected 6.12% CAGR through 2031, supported by Poland’s deposit return system and stronger recycling infrastructure.

Why is pharmaceutical demand important for cartonboard suppliers in Poland?

Pharmaceutical packaging is forecast to grow at a 6.82% CAGR through 2031 because new domestic drug production needs cartons with serialization, braille, tamper-evidence, and documented quality systems.

How is the PPWR changing cartonboard demand in Poland?

The PPWR is turning recyclability into a formal compliance requirement, which favors cartonboard in food, pharmaceutical, and consumer goods packaging where documentation and Declaration of Conformity requirements matter.

What is the biggest challenge facing cartonboard converters in Poland?

Input cost volatility remains the main challenge because energy, fiber, and imported board price swings compress converter margins and make contract pricing harder to manage.

Page last updated on: