Netherlands Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

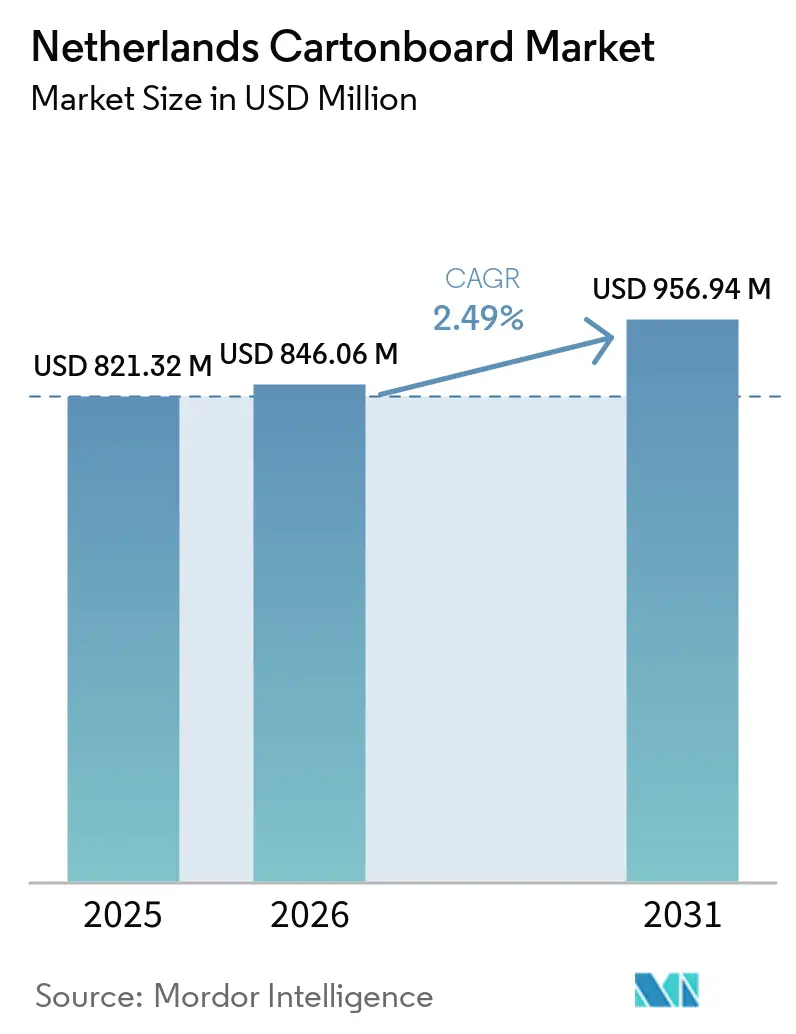

| Base Year Market Size (2025) | USD 821.32 Million |

| Market Size (2026) | USD 846.06 Million |

| Market Size (2031) | USD 956.94 Million |

| Growth Rate (2026 - 2031) | 2.49% CAGR |

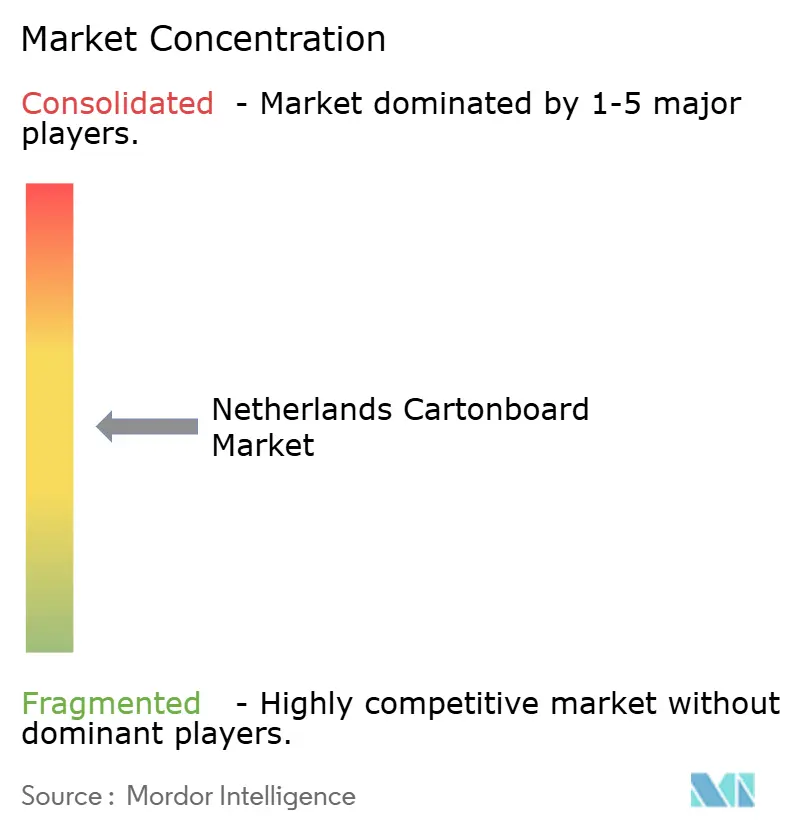

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Cartonboard Market Analysis by Mordor Intelligence

The Netherlands cartonboard market size is projected to expand from USD 821.32 million in 2025 and USD 846.06 million in 2026 to USD 956.94 million by 2031, registering a CAGR of 2.49% between 2026 to 2031. The Netherlands cartonboard market is moving through a compliance-led transition, where packaging design rules, recyclability requirements, and fee structures are now influencing procurement decisions as much as volume demand. Regulation (EU) 2025/40, with full implementation from August 2026, is pushing converters and brand owners toward recyclable fiber-based formats, especially as multi-material designs now face a weaker compliance outlook. The Dutch packaging fee system adds to that shift because paper and cardboard carry a much lower producer levy than rigid plastic, which makes fiber-based designs more attractive in day-to-day pack specification work. At the same time, recycling infrastructure for beverage cartons is improving, which reduces one of the historical barriers that had held back wider adoption in liquid packaging applications. Cost pressure remains the main near-term constraint, as board, energy, and logistics costs continue to weigh on converter margins and reward suppliers that can combine compliant structures with reliable local service.

Key Report Takeaways

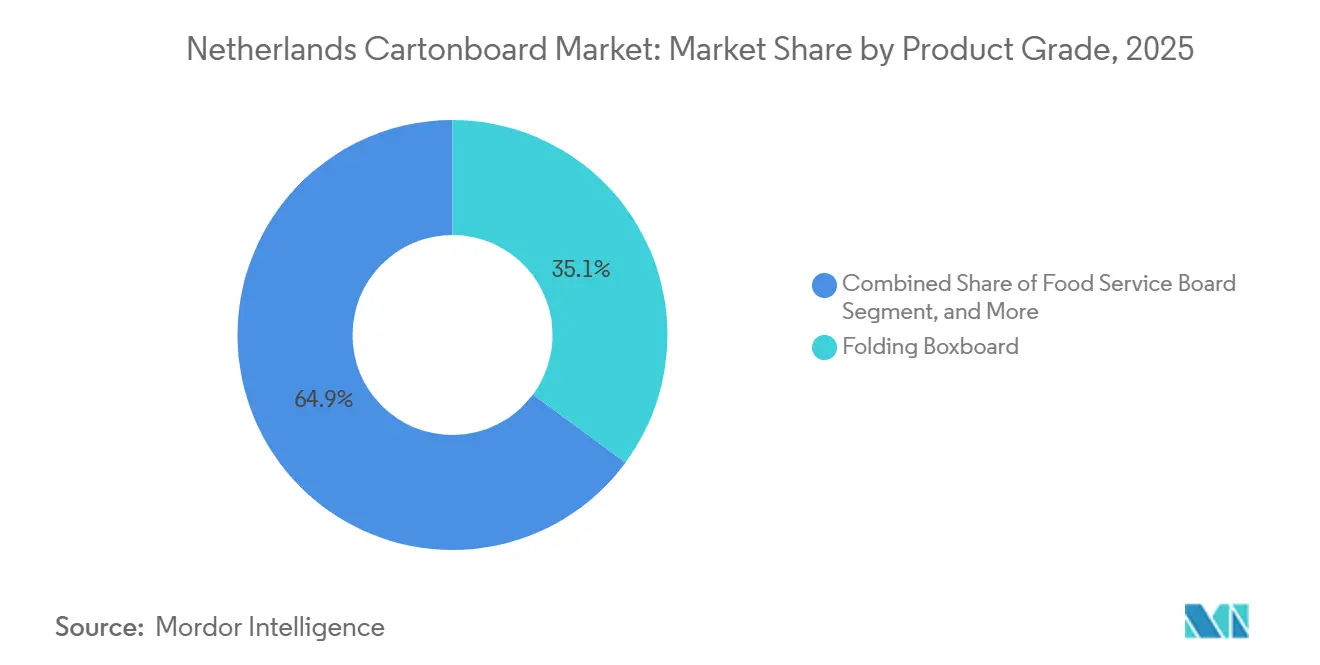

- By product grade, folding boxboard captured 35.12% of the Netherlands cartonboard market share in 2025.

- By packaging format, the Netherlands cartonboard market size for the liquid packaging segment is forecast to advance at a 3.61% CAGR through 2031.

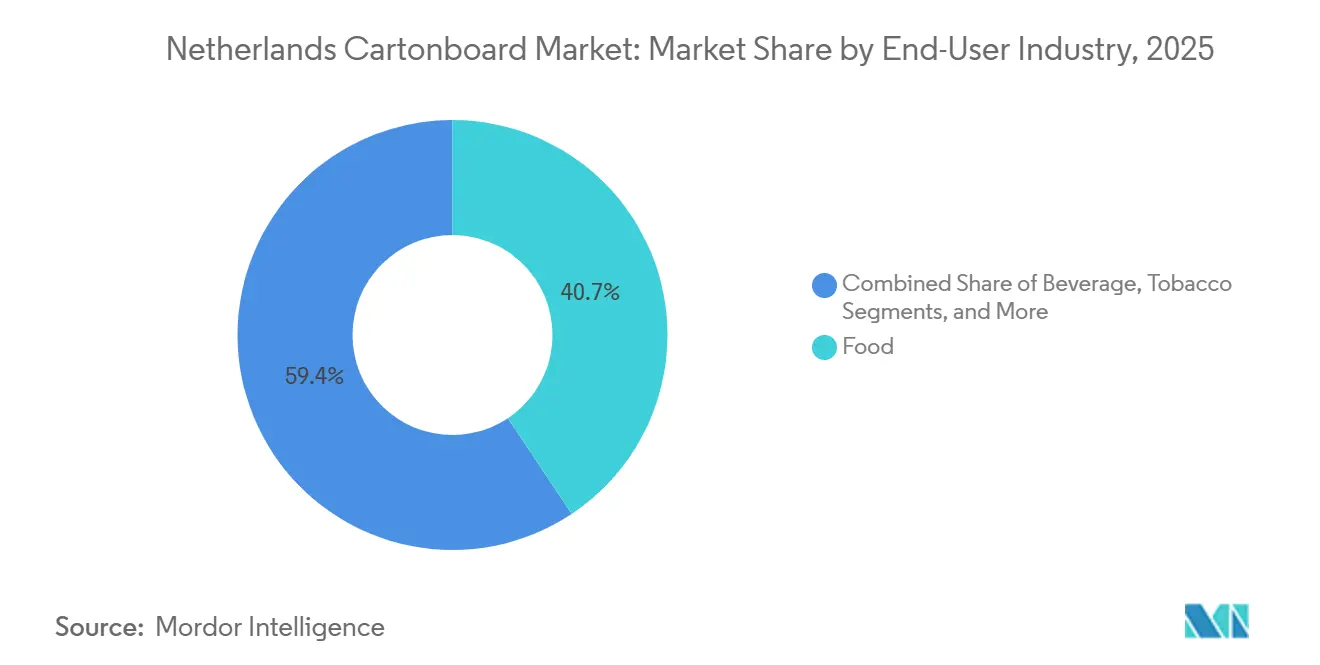

- By end-user industry, food captured 40.65% of the Netherlands cartonboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Netherlands Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Packaging Rules-Driven Shift To Recyclable Fiber Packs | +0.7% | National, with compliance intensity concentrated in Randstad-based consumer goods manufacturers | Medium term (2-4 years) |

| Plastic-To-Fiber Switching In Foodservice And Takeaway Formats | +0.5% | National, with highest demand generation in Amsterdam, Rotterdam, The Hague, and Utrecht hospitality clusters | Short term (≤ 2 years) |

| Food And Beverage Demand Base Anchoring Cartonboard Consumption | +0.4% | National, with core demand from North Brabant, Gelderland, and South Holland food-processing zones | Long term (≥ 4 years) |

| Premium Print And Compliance Needs In Pharmaceutical And Healthcare Packs | +0.3% | National, spill-over to export corridors into Germany and Belgium | Medium term (2-4 years) |

| Dutch Eco-Fee Penalties Favor Pure-Fiber Carton Design | +0.2% | National, under the Verpact EPR scheme | Short term (≤ 2 years) |

| Beverage Carton Recycling Capacity Expansion Improves Liquid Packaging Adoption | +0.2% | National, with infrastructure concentrated in Ittervoort and Roosendaal | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Packaging Rules-Driven Shift To Recyclable Fiber Packs

Regulation (EU) 2025/40 entered into force on February 11, 2025, and applies in full from August 12, 2026, which makes packaging compliance a near-term commercial issue rather than a distant policy theme in the Netherlands cartonboard market.[1]European Commission, “Packaging And Packaging Waste Regulation (EU) 2025/40,” European Commission, environment.ec.europa.eu The regulation pushes all packaging placed on the EU market toward economic recyclability and restricts PFAS in food-contact packaging from August 2026, which raises the value of simpler fiber-based designs. The Dutch market was already operating with a strong recovery culture, since Rijksoverheid required 85% of paper and cardboard packaging to be recycled by 2025, so local players entered the PPWR period with a favorable base for fiber adoption.[2]Dutch Government, “Verpakkingen En Verpakkingsafval,” Rijksoverheid, rijksoverheid.nl In practice, this shifts redesign work toward removing problematic coatings, reducing mixed-material structures, and choosing board formats that can move through existing recovery systems with fewer objections from compliance teams. The Commission’s March 2026 guidance provided pack specifiers with a clearer framework for classification and design treatment, helping buyers finalize material choices faster rather than delaying them. That combination of legal certainty and rising compliance pressure gives the Netherlands cartonboard market a structural demand lift that goes beyond simple volume replacement and reaches packaging architecture itself.

Plastic-To-Fiber Switching In Foodservice And Takeaway Formats

The Dutch single-use plastics framework continued to shape buying behavior in 2026, as hospitality operators still face operational pressure from disposable plastic cups and food containers. ILT requires separate collection thresholds of 85% for on-site food packaging in 2026 and 90% in 2027, and those targets are difficult enough that many operators prefer to avoid plastic formats where possible. For procurement teams, fiber-based cups, clamshells, and food containers increasingly look like the safer default because they align more naturally with both Dutch enforcement and incoming PPWR recyclability rules. The regulatory debate around coated paper cups did not remove the broader commercial logic behind this shift, since brand owners and catering groups still need formats that remain acceptable across multiple compliance frameworks. As a result, the Netherlands cartonboard market is seeing steady support from takeaway, convenience food, and institutional catering applications, where pure-fiber formats reduce regulatory uncertainty for operators managing thousands of daily transactions.

Food And Beverage Demand Base Anchoring Cartonboard Consumption

Food remained the largest end-user in 2025, with a 40.65% share, giving the Netherlands cartonboard market a broad and stable demand base anchored in everyday consumer categories rather than in discretionary purchases. KIDV reported beverage carton consumption of 52-55 kilotonnes per year in recent years, which confirms that liquid food and beverage packaging already has a material footprint in the country. This matters because dairy, soups, sauces, and plant-based drinks generate repeat demand for cartonboard formats tied to essential retail flows and export-oriented food production. The Dutch policy framework also supports continued improvements in the collection and recycling of beverage cartons, keeping fiber-based packaging visible in sustainability planning and supplier negotiations.[3]Verpact, “Beverage Cartons, Recycling Targets And EPR Framework,” Verpact, verpact.nl Together, those factors give the Netherlands cartonboard market a demand floor that is stronger than in categories where purchases depend more on fashion cycles or promotional spending.

Premium Print And Compliance Needs In Pharmaceutical And Healthcare Packs

A compliance-heavy packaging environment supports the pharmaceutical and healthcare segment, and NMVO’s 2026 fee structure of EUR 8,200 (USD 9,255) per marketing authorization holder indicates that serialization remains an active operating requirement rather than a completed transition.[4]Nationaal Medicijnen Verificatie Organisatie, “Voor Fabrikanten En Registratiehouders, Fee Structure 2026,” NMVO, nmvo.nl These rules keep demand focused on cartonboard surfaces that can support GS1-compliant 2D DataMatrix codes, tamper evidence, and consistent print quality during verification workflows. In the Netherlands cartonboard market, that favors high-performance grades that hold dimensional stability and optical consistency across tightly controlled pharmaceutical production runs. PPWR adds another layer of pressure because recyclability expectations are becoming increasingly important across packaging categories, which is encouraging earlier redesign work in regulated applications as well. MM Group reported an encouraging margin increase in its Pharma and Healthcare Packaging division in 2025, which supports the view that regulated cartonboard applications can still command better pricing than more commoditized formats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pulp, Energy, And Imported Board Cost Volatility | -0.4% | National, with high exposure in energy-intensive mills across North Holland and South Holland | Short term (≤ 2 years) |

| Barrier-Coating Reformulation After PFAS Restrictions | -0.3% | National and EU-wide, under REACH Annex XVII and PPWR Article 21 | Short term (≤ 2 years) |

| Dependence On Imported Liquid Packaging Board And Folding Boxboard | -0.2% | National, with Rotterdam port as the critical import gateway for Scandinavian and Central European board grades | Medium term (2-4 years) |

| Labor And Automation Gaps At Independent Converters | -0.2% | National, concentrated among smaller converters in North Brabant and Overijssel | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pulp, Energy, And Imported Board Cost Volatility

Cost pressure remains the sharpest near-term restraint in the Netherlands cartonboard market because a large part of the converter base depends on purchased board, imported grades, and energy-sensitive supply chains. Fastmarkets noted that gas price increases have a much larger effect on white-lined chipboard production costs than on folding boxboard production costs in Europe, which matters in a market exposed to energy-linked packaging inputs. The same source also described firmer pulp conditions heading into 2026, suggesting converter relief from upstream costs will likely remain limited even as inventories improve. Independent converters feel this most clearly because customer contracts and pricing cycles often delay cost pass-through, while freight and working-capital needs rise at the same time. That margin squeeze does not remove demand from the Netherlands cartonboard market, but it does slow investment capacity and increases the advantage of larger or better-integrated suppliers.

Barrier-Coating Reformulation After Pfas Restrictions

PPWR Article 21 takes full effect on August 12, 2026, for PFAS in food-contact packaging, requiring converters to replace barrier systems that have long been used in grease-resistant and moisture-sensitive applications. KIVO explained that the shift affects functional needs in foodservice board, microwave-ready packaging, and other formats where grease, oil, or water resistance cannot be treated as optional. Replacement systems such as water-based dispersions or mineral-based barriers often require equipment tuning, supplier validation, and food-contact testing, and smaller converters may struggle to finish that work on tight timelines. The burden is uneven because dry-food, confectionery, and cosmetics cartons face less reformulation risk than foodservice and liquid packaging applications. In the Netherlands cartonboard market, this creates a short-term advantage for larger players that have already qualified PFAS-free solutions and can offer customers compliance-ready alternatives without delaying commercial launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Folding Boxboard Commands Share Amid Grade Divergence

Liquid packaging board is the fastest-growing product grade, and this segment of the Netherlands cartonboard market is projected to expand at a 3.32% CAGR through 2026-2031. That growth comes from dairy and plant-based beverage applications, where sterility, barrier protection, and filling-line compatibility remain difficult to match with simpler paper structures. Tetra Pak’s April 2026 launch of a 1-liter aseptic carton with a paper-based barrier, 90% renewable content, and a carbon footprint reduction of up to 50% compared to aluminum-barrier equivalents shows where product development is heading. Dutch beverage carton recycling targets of 43% in 2026 and 55% by 2030 also strengthen the commercial case for liquid packaging board by reducing concerns about end-of-life handling. As those targets move closer, beverage producers gain a clearer route to present carton-based packs as both functional and more aligned with future compliance expectations.

Folding boxboard held 35.12% of the Netherlands cartonboard market share in 2025 and remained the leading grade because it serves food, pharmaceutical, cosmetics, and consumer goods packaging with a strong balance of stiffness and print quality. Its position is reinforced by the fact that these end uses need broad-format convertibility, reliable finishing, and surfaces that can handle both brand graphics and regulatory information without compromising appearance. Metsä Board strengthened this part of the supply chain in 2026 through its new product and service concept linked to the Netherlands sheeting hub, which offers custom-cut deliveries in under 3 weeks across Europe and under 10 days in its ExpressTrack option. In the Netherlands cartonboard industry, solid bleached board retains a premium role in regulated and image-sensitive packs, while white-lined chipboard remains more exposed to cost pressure and energy sensitivity. The Netherlands cartonboard industry therefore shows a clear split, with premium virgin-fiber grades benefiting from compliance and presentation needs, while cost-led grades face a more difficult operating backdrop.

By Packaging Format: Liquid Packaging Growth Outpaces Folding Carton Incumbency

Folding cartons captured 58.16% of the Netherlands cartonboard market share in 2025, reflecting their broad use across food, pharmaceutical, cosmetics, and fast-moving consumer goods packaging. Their leading position comes from simple but durable advantages, including wide converter familiarity, efficient printing and die-cutting, and easy alignment with current recyclability expectations. In the Netherlands cartonboard market, folding cartons also benefit from their ability to carry branding, dosage instructions, ingredient panels, and legal information without requiring structural complexity that would weaken recovery performance. Sleeve and tray formats remain important in food retail, produce, and transit applications, but they do not match the all-purpose role of folding cartons across secondary packaging. That leaves folding cartons as the default choice for many Dutch converters, especially where high throughput, repeatability, and lower redesign risk matter most.

Liquid packaging is the fastest-growing format, and this segment of the Netherlands cartonboard market is projected to grow at a 3.61% CAGR through 2026-2031. Dutch beverage carton recycling targets, together with the second-half 2025 opening of the Ittervoort PolyAl recycling plant with 20,000 tonnes of annual capacity for Belgium and the Netherlands, are reducing one of the main historical objections to carton-based beverage packaging. This makes the format more attractive to dairy and plant-based beverage producers seeking a compliance-ready pack structure while maintaining shelf life and filling efficiency. Tetra Pak, SIG Group, and Elopak keep the format technologically demanding, since filling systems, barrier chemistry, and recycling claims all influence supplier choice in the Netherlands cartonboard market. Elopak’s 2025 annual report showed revenue of EUR 1.206 billion (USD 1.315 billion) and the launch of its first cartons made with recycled and renewable polymers, signaling that competitive pressure in liquid packaging is increasingly tied to materials innovation and scale.

By End-User Industry: Food Anchors Volume While Pharma Posts Strongest Growth

Pharmaceutical and healthcare packaging is forecast to grow at a 3.14% CAGR, making it the fastest-expanding segment of the Netherlands cartonboard market by end-user. The segment benefits from a regulated packaging environment in which verification, serialization, patient safety, and pack consistency place a premium on high-specification cartonboard. NMVO’s verification framework keeps pressure on marketing authorization holders and packaging suppliers to maintain code quality and reliable surface performance, which supports demand for premium grades. Once a healthcare packaging format is validated, switching becomes more difficult because regulatory, technical, and quality teams must all approve the change, which tends to protect incumbent board suppliers. Cosmetics and toiletries packaging also align with the same regulatory direction, as brands are replacing harder-to-recycle plastic formats with folding cartons that better align with PPWR-era expectations.

Food accounted for 40.65% of the Netherlands cartonboard market size in 2025, making it the broadest and most stable demand base in the market. The category covers cereals, confectionery, frozen food, chilled products, takeaway items, and liquid cartons for dairy and plant-based beverages, providing converters with balanced exposure across both everyday retail and export-oriented supply chains. This breadth matters because it spreads demand across many pack types and reduces dependence on any single product cycle inside the Netherlands cartonboard market. Beverage remains the second-largest end-user, while tobacco stays smaller but still requires print accuracy and specification discipline on secondary packaging surfaces. MM Group stated in April 2026 that its Pharma and Healthcare Packaging division outperformed the Board and Paper segment on margins, which supports the view that regulated end uses offer better pricing power than more standard food applications.

Geography Analysis

The Netherlands cartonboard market has a geographically concentrated demand base, shaped more by logistics, converter density, and recycling infrastructure than by domestic board mill scale. The Port of Rotterdam remains the main gateway for imported liquid packaging board and folding boxboard, connecting Dutch converters to Scandinavian and Central European supply chains and enabling fast replenishment of premium grades. This import-led structure creates some exposure to freight and currency movements, but it also gives local buyers early access to high-specification board that often sets the standard for recyclable packaging in Europe. The Rijksoverheid’s 2025 requirement that 85% of paper and cardboard packaging be recycled provides fiber-based formats with a strong policy backdrop and reinforces their role in procurement decisions across the country. Metsä Board strengthened in-country service in 2026 through its Netherlands sheeting hub and fast-delivery concept, which reduces lead times for converters that need custom-cut folding boxboard on shorter planning cycles.

The Randstad area, including Amsterdam, Rotterdam, The Hague, and Utrecht, holds a dense concentration of pharmaceutical, cosmetics, and consumer goods conversion activity in the Netherlands cartonboard market. That demand cluster favors solid bleached board and virgin-fiber folding boxboard because these applications depend on print precision, appearance, and consistent pack performance across repeat runs. North Brabant and Gelderland form another important demand zone, supported by food processing, dairy operations, and connected distribution flows into nearby European markets. These provinces matter especially for liquid packaging board and foodservice board, because they sit close to categories where throughput remains high and pack functionality is central to product protection. The compact national transport network ties these regions together efficiently, which lets converters serve domestic and export customers without carrying excess inventory and raises the value of responsive local service.

Germany, Belgium, and the United Kingdom remain the main export destinations for Dutch-converted cartonboard packaging, so external demand conditions feed quickly into Dutch order books. PPWR implementation in those neighboring markets matters because pack formats approved for export customers often become the working standard for runs produced in the Netherlands as well. Beverage carton recycling targets of 43% in 2026 and 55% by 2030, together with additional PolyAl processing capacity in the Belgium-Netherlands system, improve the recycling case for liquid cartons over time. That gives the Netherlands cartonboard market a geographic advantage in liquid packaging, since recyclability perceptions are improving within the same cross-border system that major beverage brand owners use for sourcing and compliance planning.

Competitive Landscape

The Netherlands cartonboard market operates with a concentrated upstream supply base and a more fragmented converting layer. Integrated board producers such as Metsä Board, Mayr-Melnhof Karton, and Stora Enso influence grade availability and specification standards through imported supply, while Dutch and multinational converters compete more directly on execution. The liquid packaging market is structurally tighter because filling systems, barrier know-how, and qualification requirements create higher entry barriers than standard folding carton work. By contrast, independent converters compete on print quality, pharmaceutical compliance credentials, lead times, and short-run flexibility rather than on raw material scale alone. PPWR is narrowing the range of acceptable packaging designs, which means converters that can offer validated recyclable and PFAS-free structures are gaining a clearer commercial edge in the Netherlands cartonboard market.

Several suppliers used 2025 and 2026 to strengthen that position through visible strategic moves. MM Group’s April 2026 investor presentation said its Fit-For-Future Program is targeting more than EUR 250 million (USD 282.5 million) in structural profit improvements by 2027, underscoring a strong focus on cost discipline and quality improvements at a time when margins remain under pressure. Metsä Board launched MetsäBoard Pro FBB Go in May 2026 and paired the product with under-3-week delivery from its Netherlands-based sheeting hub, which turns service speed into a competitive tool rather than a back-office function. Tetra Pak’s April 2026 paper-based barrier carton launch took a different route to advantage, aiming for higher renewable content and lower carbon impact without forcing dairy producers to invest heavily in new filling lines. In the Netherlands cartonboard market, these moves shift competition away from basic board availability and toward compliance readiness, material innovation, and speed of response.

Mondi also reinforced its position through scale and capability expansion. The company completed a EUR 1.2 billion (USD 1.356 billion) investment program in March 2026 and had already expanded its Western Europe packaging footprint through the Schumacher Packaging acquisition completed in April 2025, which strengthens its digital printing and solid board offer for shorter-run and premium work. Elopak reported revenue growth in 2025 and launched cartons made with recycled and renewable polymers, which supports its position with customers preparing for stricter recycled-content and design expectations. The result is a Netherlands cartonboard market where suppliers win more often by combining compliant materials, strong print performance, and reliable logistics than by competing solely on price. That keeps the market competitive, but it also gives companies that can invest in new substrates, validation work, and local service infrastructure an advantage.

Netherlands Cartonboard Industry Leaders

Tetra Pak International S.A.

SIG Group AG

Elopak ASA

Mayr-Melnhof Karton AG

Metsa Board Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Metsä Board launched MetsäBoard Pro FBB Go, a new folding boxboard for demanding food and pharmaceutical packaging, with custom-cut sheet delivery from its Netherlands-based sheeting hub. The FastTrack Service promises delivery in under 3 weeks across Europe, the ExpressTrack Service offers delivery in under 10 days, enabling converters and brand owners to reduce excess inventory and maintain supply-chain agility.

- April 2026: Tetra Pak, in partnership with Sterilgarda Alimenti, launched the world's first 1-liter aseptic carton featuring a paper-based barrier on April 22, 2026. The package achieves 90% renewable content, reduces the carbon footprint by up to 50% compared with aluminum-barrier equivalents, and is compatible with high-speed filling lines that produce up to 24,000 packages per hour, enabling large-scale deployment without significant capital investment from dairy producers.

- March 2026: Mondi completed a EUR 1.2 billion (USD 1.356 billion) investment program covering paper mills and packaging plants, with 5 major capacity-expansion projects now operational across its corrugated and flexible packaging operations. The program reinforces Mondi's scale in the European fiber-based packaging supply.

- November 2025: Mondi launched an extended food packaging portfolio incorporating solid board solutions and digital printing capabilities, following its April 2025 acquisition of Schumacher Packaging's Western Europe operations. The portfolio addresses EU regulations and provides FMCG and eCommerce customers with fiber-based, sustainable packaging at scale.

Netherlands Cartonboard Market Report Scope

The Netherlands Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The Netherlands Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and Other Packaging Formats), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics and Toiletries, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

Key Questions Answered in the Report

What is the size of the Netherlands cartonboard market?

The Netherlands cartonboard market reached USD 821.32 million in 2025, stands at USD 846.06 million in 2026, and is forecast to reach USD 956.94 million by 2031 at a 2.49% CAGR.

Which product grade leads demand in the Netherlands cartonboard space?

Folding boxboard led the product grade mix with 35.12% share in 2025 because it serves food, pharmaceutical, cosmetics, and consumer goods packaging.

Which packaging format is growing the fastest in the Netherlands?

Liquid packaging is the fastest-growing format, with a projected 3.61% CAGR through 2031, helped by stronger recycling infrastructure and rising demand for dairy and plant-based beverage cartons.

Why is regulation important for cartonboard demand in the Netherlands?

PPWR and Dutch single-use plastics rules are pushing converters and brand owners toward recyclable fiber-based designs, especially where plastic or multi-material packs face higher compliance risk.

Which end-user segment offers the best growth outlook?

Pharmaceutical and healthcare packaging shows the highest end-user growth outlook, with a projected 3.14% CAGR through 2031, supported by serialization and high print-quality requirements.

What is the main challenge for cartonboard suppliers and converters in the Netherlands?

The main challenge is cost pressure from energy-sensitive inputs, imported board exposure, and PFAS-related reformulation work, which hits smaller independent converters more heavily.

Page last updated on: