Spain Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

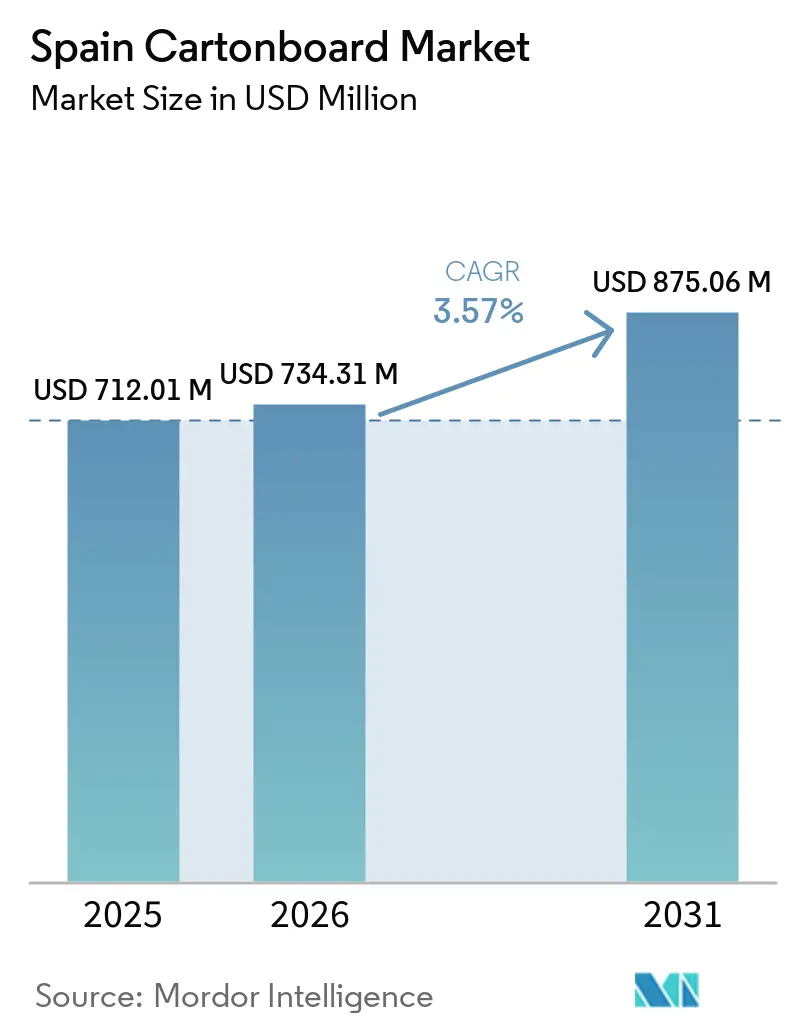

| Base Year Market Size (2025) | USD 712.01 Million |

| Market Size (2026) | USD 734.31 Million |

| Market Size (2031) | USD 875.06 Million |

| Growth Rate (2026 - 2031) | 3.57% CAGR |

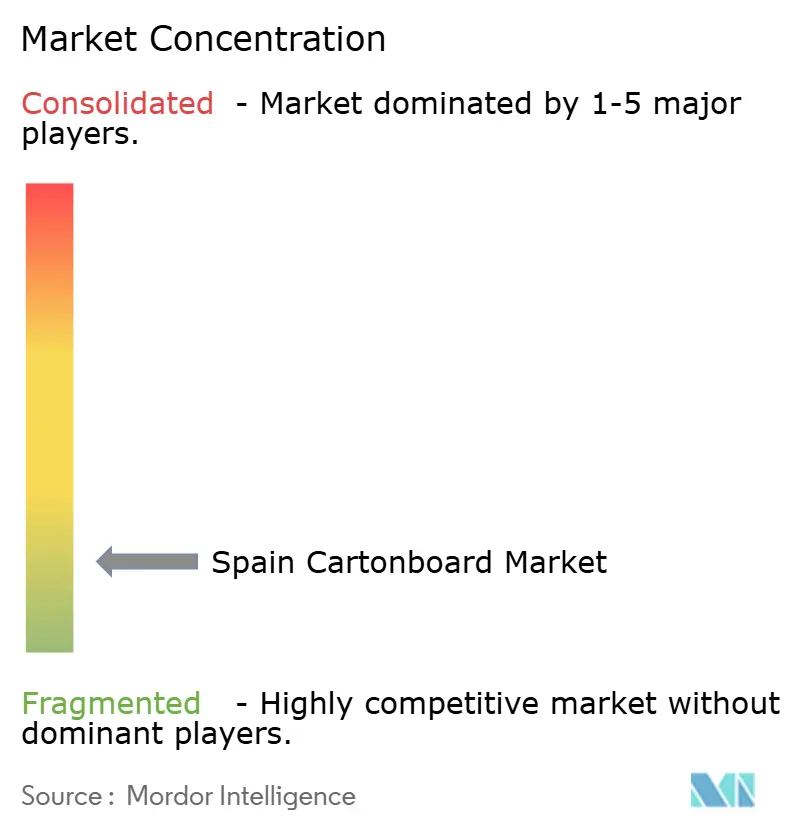

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Cartonboard Market Analysis by Mordor Intelligence

The Spain cartonboard market size was valued at USD 712.01 million in 2025 and estimated to grow from USD 734.31 million in 2026 to reach USD 875.06 million by 2031, at a CAGR of 3.57% during the forecast period (2026-2031). Spain’s folding carton industry produced 525,918 tonnes in 2025 and generated EUR 1.281 billion (USD 1.383 billion) in converter turnover, indicating that fiber-based secondary packaging maintained a stable role in national industrial output. The Spain cartonboard market is also being supported by a clear shift away from multi-layer plastic and aluminum-laminate packs toward mono-material cartonboard formats that fit retailer sustainability targets and updated labeling rules. Integrated converters with access to substrate production and digitized workflow systems are widening the cost and compliance gap over smaller operators that depend more on traded board. Strong agrifood exports, tighter packaging compliance, and growing requirements in regulated healthcare packs are keeping demand firm across the value chain. This leaves the Spain cartonboard market with room to grow through better recyclable formats, stronger documentation support, and higher-value printed packaging for food, health, and personal care applications.

Key Report Takeaways

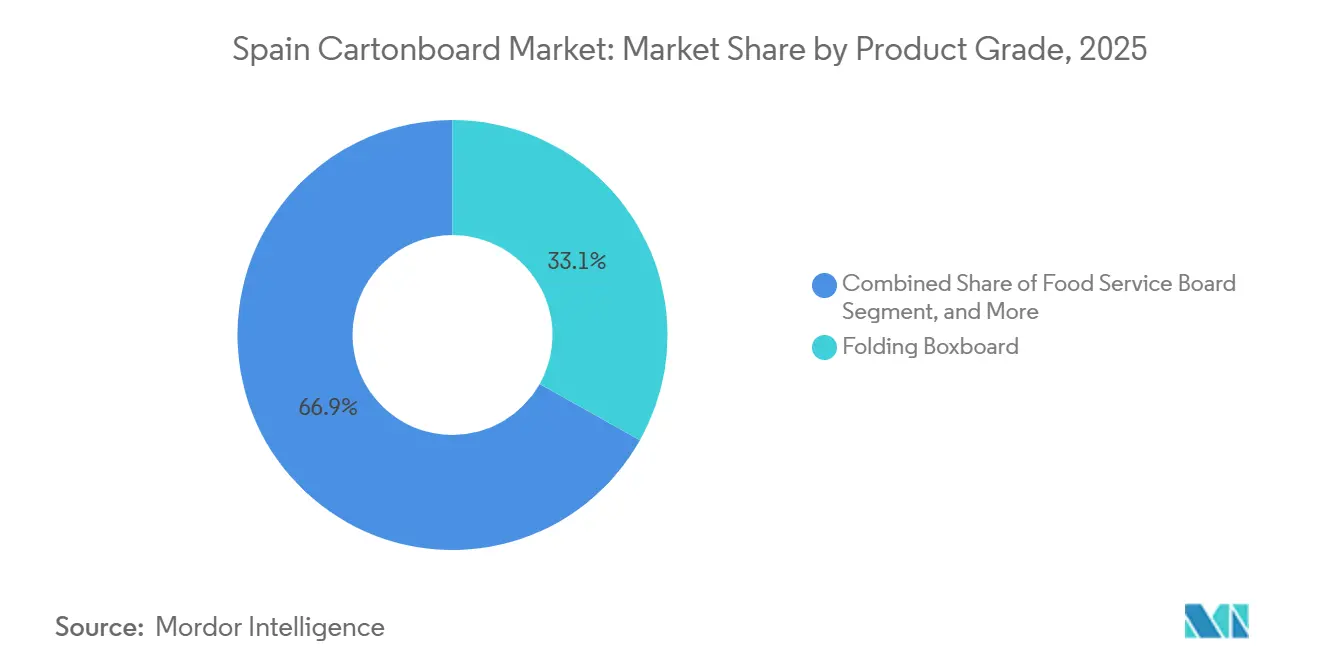

- By product grade, folding boxboard captured 33.14% of the Spain cartonboard market share in 2025.

- By packaging format, the Spain cartonboard market size for the liquid packaging segment is forecast to advance at a 4.31% CAGR through 2031.

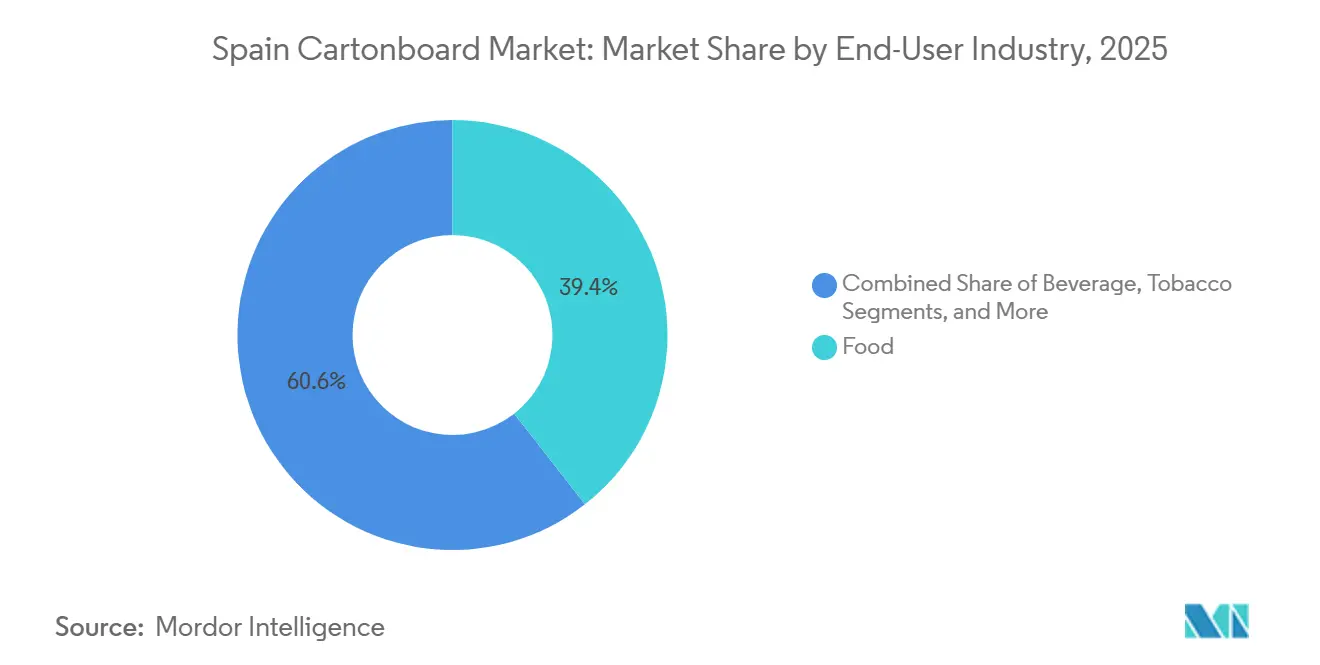

- By end-user industry, food captured 39.43% of the Spain cartonboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainable Packaging Substitution In Food And Beverage | +1.1% | Spain-wide, with intensity in Cataluña, Andalucía, and Comunidad Valenciana | Short term (≤ 2 years) |

| E-Commerce And Shelf-Ready Carton Demand | +0.9% | Madrid, Barcelona, Valencia logistics corridors | Short term (≤ 2 years) |

| Processed Food And Export Packaging Growth | +0.6% | Andalucía, Comunidad Valenciana, Cataluña, Murcia | Medium term (2-4 years) |

| Premium Secondary Packs For Pharma And Beauty | +0.5% | Madrid, Barcelona, Comunidad Valenciana | Medium term (2-4 years) |

| 2025 Printed Sorting-Label Compliance | +0.3% | Spain-wide, all household packaging placed on market | Short term (≤ 2 years) |

| Pharma Aggregation And Traceability Complexity | +0.2% | Spain-wide, with pharmaceutical manufacturing hubs in Cataluña and Madrid | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustainable Packaging Substitution In Food And Beverage

The Spain cartonboard market is gaining direct support from tighter plastic packaging rules and rising producer responsibility costs for non-fiber formats. Spain’s packaging framework increased pressure on brand owners to move toward recyclable packs with clearer end-of-life communication, making cartonboard a more practical commercial choice for food and beverage lines.[1]Spain Ministry of the Presidency, “Real Decreto 1055/2022, De 27 De Diciembre, De Envases Y Residuos De Envases,” Boletín Oficial del Estado, boe.es Fresh and frozen food represented 29% of folding carton converter turnover in Spain in 2025, while beverages accounted for 21%, so substitution in these categories carries clear volume potential for the Spain cartonboard market.[2]Asociación Española de Fabricantes de Envases, Embalajes y Transformados de Cartón, “El Sector Del Envase De Cartón Mantiene Su Crecimiento Y Mejora Su Rentabilidad En España,” Aspack, aspack.es The December 2024 launch of the PaperSeal Shape tray in Spain showed that converters were already replacing conventional plastic trays with paperboard structures before the August 2026 compliance deadline. As more food formats shift to mono-material fiber packs, demand is growing for both premium virgin-fiber boards and recyclable retail formats in the Spanish cartonboard market. That shift favors suppliers that can provide substrate access, conversion quality, and regulatory documentation in one offer.

E-Commerce And Shelf-Ready Carton Demand

The Spain cartonboard market is also benefiting from the spread of shelf-ready packaging in retail and online fulfillment. Retailers increasingly prefer formats that protect goods in transit and move directly onto store shelves without extra handling, giving cartonboard a more functional role in logistics. This use case supports Folding Boxboard and White-Lined Chipboard formats that sit between plain transport packaging and premium retail presentation. In the Spain cartonboard market, that requirement is broadening carton use from a branded secondary pack into a tool for labor reduction and faster replenishment. It is also pulling lighter grammage boards into categories that previously used heavier structures, changing the grade mix for converters with multi-grade portfolios. The result is a more stable demand base for cartons linked to omnichannel retail rather than to store traffic alone.

Processed Food And Export Packaging Growth

The Spain cartonboard market is closely tied to the country’s agrifood export base, which reached a record EUR 77.227 billion (USD 83.4 billion) in 2025, up 4% from 2024 and up more than 80% from 2018.[3]Instituto Español de Comercio Exterior and Plataforma Tierra, “Exportaciones Agroalimentarias Españolas 2025, Nuevo Récord De 77.227 Millones De Euros,” Plataforma Tierra, plataformatierra.es European Union partners accounted for 67% of total Spanish agrifood exports, indicating that packaging specifications in nearby export markets directly shape carton requirements in Spain. Fruit and vegetable exports exceeded EUR 18 billion (USD 19.4 billion) in 2025, and these flows depend heavily on secondary packaging that can protect goods during transport. Spain’s food and beverage manufacturing sector generated EUR 137.188 billion (USD 148.2 billion) in turnover in 2025, while exports accounted for EUR 52.564 billion (USD 56.8 billion), keeping packaging demand broad and geographically spread across the Spanish cartonboard market. This scale supports folding cartons and beverage carriers in Andalusia, Valencia, Catalonia, and Murcia, where many food production clusters are located. As export markets tighten packaging expectations, performance standards for cartonboard in Spain are becoming more closely linked to trade competitiveness.

Premium Secondary Packs For Pharma And Beauty

The Spain cartonboard market is seeing faster value growth in regulated healthcare and premium personal care applications. Spain’s pharmaceutical manufacturing base needs secondary packs with consistent print quality, tamper-evidence, and reliable code readability, which support higher-specification cartonboard. The AEMPS requirement that the first four EUDAMED modules become mandatory from May 28, 2026, added another layer of identification and documentation pressure to regulated packaging flows.[4]Agencia Española de Medicamentos y Productos Sanitarios, “La AEMPS Informa Sobre La Obligatoriedad De Los Cuatro Primeros Módulos De EUDAMED En 2026,” AEMPS, aemps.gob.es Beauty brands are adding a second demand stream by replacing plastic blister and shrink-wrap formats with cartonboard enclosures as secondary packs, which lifts board value per unit and supports more coated grades in the Spain cartonboard market. Metsä Board’s 2026 collaboration with HEIDELBERG demonstrated how board producers are moving upstream to address brand-owner packaging needs through combined materials and machinery offerings. This demand pattern favors converters that can balance regulatory precision with premium visual presentation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy And Recycled-Board Cost Volatility | -0.8% | Spain-wide, with highest exposure at board mills in Guipúzcoa, Navarra, and Cataluña | Medium term (2-4 years) |

| Barrier Performance Trade-Offs Versus Plastics | -0.5% | Spain-wide, particularly chilled and extended-shelf-life food categories | Long term (≥ 4 years) |

| Artwork Complexity From Printed Sorting Labels | -0.3% | Spain-wide, all household cartonboard packaging from January 2025 | Short term (≤ 2 years) |

| Recyclability Documentation Burden Before August 2026 | -0.2% | Spain-wide, with cross-border implications for Cataluña and Basque Country exporters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Energy And Recycled-Board Cost Volatility

The Spain cartonboard market remains exposed to energy cost swings because paper and board production runs on continuous industrial schedules with limited operating flexibility. When electricity and gas prices rise, mills cannot easily reduce output in short intervals, so pressure moves quickly into margins and working capital. The recycled-fiber cost side is also important because European OCC prices stayed near EUR 120 (USD 135) per tonne in late 2025 before stabilizing closer to EUR 105 (USD 118) per tonne. That level keeps a higher cost floor in recycled grades than the market faced before 2022, which leaves less room for weaker Spanish mills in the Spain cartonboard market. Reno de Medici’s closure agreement at Castellbisbal showed how prolonged cost pressure can translate into hard capacity decisions in Spain. The burden is most severe for operators without energy co-generation assets, renewable power contracts, or enough scale to pass cost moves through to customers.

Barrier Performance Trade-Offs Versus Plastics

The Spain cartonboard market still faces a technical limit in applications that need strong moisture, oxygen, or grease barriers. Matching multilayer plastic performance often requires extra coating layers or newer water-based dispersion systems, which can raise cost and complicate conversion. Billerud stated that competition in liquid packaging board intensified in the second half of 2025 as Asian producers redirected capacity into Europe when local demand weakened. That pricing pressure reduces the premium available to European mills and makes near-term returns on next-generation barrier investments harder to secure in the Spain cartonboard market. Converters serving chilled ready meals and ambient dairy packs are therefore taking longer to validate fiber-based barrier solutions under their own temperature and humidity conditions. Until that validation becomes easier at production scale, full substitution away from plastics will remain gradual in part of the Spain cartonboard market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Folding Boxboard Leads While Liquid Packaging Board Expands Faster

Folding Boxboard held 33.14% of the Spanish cartonboard market share in 2025, making it the leading grade by volume and value. Its lead in the Spanish cartonboard market stems from broad use across secondary packs that require stiffness, surface brightness, and reliable print quality. Solid Bleached Board remained relevant in premium cosmetics and confectionery packs where a white surface finish supports premium positioning. Solid Unbleached Board served food-service and retail-ready formats where strength mattered more than high whiteness. White-Lined Chipboard continued to serve cost-sensitive cereals and processed food packs where recycled content was commercially acceptable and often preferred.

Liquid Packaging Board is projected to grow at a 4.63% CAGR through 2031, making it the fastest-moving grade in the Spanish cartonboard market. Spain’s dairy, juice, and plant-based beverage base supports steady aseptic packaging demand, as these products require protection from light and oxygen. Royal Decree 1055/2022 also raised the importance of print quality from January 2025, which favored grades that can carry sorting information clearly and consistently. Food Service Board added another outlet through cups, trays, and carrier boards for out-of-home consumption, keeping the grade mix broader in the Spanish cartonboard industry. Stora Enso’s new consumer packaging board line at Oulu began ramp-up in early 2025 and will widen European supply from 2027, which may ease some board availability pressure for the Spanish cartonboard market and change converter buying patterns across the Spanish cartonboard industry.

By Packaging Format: Folding Cartons Dominate While Liquid Packaging Builds Momentum

Folding Cartons accounted for 56.36% of the Spain cartonboard market in 2025, keeping this format well ahead of all other pack types. Their lead in the Spain cartonboard market reflects broad use in pharmaceuticals, cosmetics, cereals, confectionery, and non-food consumer goods that need printed and branded secondary packaging. High-speed filling compatibility, easy handling on automated lines, and efficient shelf presentation kept folding cartons deeply embedded in large FMCG operations. Sleeve and Tray formats remained important for fresh produce, chilled food, and retail-ready applications, where display functionality and transport protection must work together. Other packaging formats, including fiber cups and food-service containers, also gained ground across the Spain foodservice market as paper-based alternatives replaced more single-use plastic items.

Liquid Packaging is projected to grow at a 4.31% CAGR through 2031, making it the fastest-growing format in the Spain cartonboard market. That pace shows that aseptic and chilled liquid carton solutions are outperforming the broader market as dairy-adjacent and plant-based beverage lines expand. It also suggests that part of this volume is being captured through imported system solutions rather than from a large domestic substrate base. Spain-based converters in the Spain cartonboard market therefore need stronger aseptic filling capability and barrier design expertise if they want to capture more of this growth. Elopak and SIG Group are well placed in these liquid carton systems, where performance certification and filling-line integration matter as much as the carton itself.

By End-User Industry: Food Anchors Volume While Pharmaceutical And Healthcare Grows Faster

Food accounted for 39.43% of the Spanish cartonboard market in 2025, making it the largest end-user by a clear margin. This leading position in the Spain cartonboard market reflects the scale and diversity of Spain’s food manufacturing base across fresh and frozen products, cereals, confectionery, and processed categories. Aspack stated that food accounted for 51% of total turnover for folding carton converters in Spain in 2025, including 29% from fresh and frozen products, 21% from beverages, 16% from cereals, and 16% from confectionery. Beverage applications also held structural relevance because wine, olive oil, and mineral water flows still rely on premium secondary packaging for protection and product presentation. Tobacco continued to lose weight, while cosmetics and toiletries kept moving toward brighter Folding Boxboard and Solid Bleached Board to support a premium shelf appearance.

Pharmaceutical and Healthcare is projected to grow at a 4.51% CAGR through 2031, making it the fastest-growing end-user segment in the Spain cartonboard market. Spain’s large pharmaceutical manufacturing base supports this trend because it requires precise labeling, tamper-evident seals, and clear print in secondary packs. The AEMPS decision that the first four EUDAMED modules became mandatory from May 28, 2026, added more identification and market surveillance requirements around regulated products. These requirements raise the value of smooth, bright substrates that can hold complex codes and mandatory pack content without print failure. Other end users, including toys, apparel, and household goods, still matter in the Spain cartonboard industry because they help stabilize converter utilization outside seasonal food peaks.

Geography Analysis

The Spain cartonboard market was valued at USD 712.01 million in 2025, and the country’s role in Europe rested more on conversion than on raw board output. Spain ranked among Europe’s larger corrugated and cartonboard converting economies because it had a broad installed base of printing, cutting, and folding capacity. The Spain cartonboard market depended on imported Folding Boxboard and Liquid Packaging Board from Scandinavian and Central European mills. That import reliance raised exposure when freight costs tightened or substrate availability shifted in Europe. At the same time, demand from agrifood, pharmaceuticals, and consumer goods provided the Spanish cartonboard market with a stable domestic base that supported long-term investment in conversion assets.

Northern Spain accounted for the main production cluster in the Spanish cartonboard market. Navarra hosted Lecta’s Leitza mill, where the Leitzaran line began operations on February 1, 2026, and added high-performance barrier paper capacity alongside the cartonboard converting base. Aragon and the Basque Country linked waste management, recovered fiber logistics, and industrial packaging operations through regional Saica assets. Catalonia lost domestic recycled board capacity after the closure agreement at Reno de Medici’s Castellbisbal mill, which removed 190,000 tonnes per year from local supply and increased the likelihood of extra sourcing from imports or northern Spanish alternatives.

Eastern and southern Spain served as the main demand centers in the Spanish cartonboard market because Andalusia, Murcia, and the Valencian Community lie within the agrifood export belt. Converters in these regions mainly served fresh produce, citrus, olive oil, and processed food applications, where printability, pack integrity, and export compliance are critical. Madrid is a hub for pharmaceutical, cosmetic, and consumer goods packaging procurement because many brand owners manage their Spanish supply chains from the capital. Barcelona added a second high-specification demand node for regulated and premium printed packaging. This split between higher food-volume demand in the south and east and higher-specification demand in Madrid and Barcelona favored converters with multi-site networks over single-plant operators in the Spanish cartonboard market.

Competitive Landscape

The Spain cartonboard market is split between a concentrated board supply layer and a fragmented converting layer. Global producers such as Mayr-Melnhof Karton, Graphic Packaging International, Stora Enso, Metsä Board, Holmen, and Billerud supply the main board grades that Spanish converters transform into finished cartons. At the downstream level, the Spain cartonboard market remained fragmented, with around 90 active converting companies and 7,000 workers. Mayr-Melnhof’s Fit-For-Future program delivered EUR 70 million (USD 75.6 million) in adjusted operating profit contribution by 2025, and management maintained a EUR 250 million (USD 270 million) uplift target for 2027 relative to the 2024 base. This set a hard benchmark for cost discipline that smaller converters in the Spain cartonboard market may struggle to match.

Consolidation pressures are increasing in the Spain cartonboard market because compliance, automation, and energy management now demand larger balance sheets. Apollo Capital Management’s clearance to acquire Lecta in March 2026 showed that fiber-adjacent specialty paper assets in Spain remained attractive even while parts of recycled board production faced financial strain. Graphic Packaging International also strengthened its competitive position through a virtual power purchase agreement tied to three solar plants in Spain, with a combined capacity of around 100 MW, with operations spanning 2025 and early 2026. These moves matter because buyers in the Spain cartonboard market are now judging vendors on cost stability and carbon positioning as much as on board quality.

White-space opportunities in the Spanish cartonboard market are concentrated in high-barrier fiber solutions for direct-food-contact applications and in small-format premium cartons for the pharmacy and beauty channels. Current Spanish converting capacity is still weighted toward standard pharmaceutical secondary packs and food-category folding cartons, so those niches remain underserved. Metsä Board’s collaboration with HEIDELBERG in 2026 showed a direct push toward combined board and machinery solutions for brand-owner packaging needs. Metsä Board’s 2026 transformation program and strategic goals also underlined the need to improve profitability while building a more value-added consumer packaging mix. In this setting, competitive advantage in the Spanish cartonboard market is shifting toward companies that can combine substrate access, automation, renewable energy positioning, and compliance support rather than just scale.

Spain Cartonboard Industry Leaders

Mayr-Melnhof Karton AG

Graphic Packaging Holding Company

Smurfit Westrock plc

Saica Group

Metsa Board Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Saica Group, headquartered in Zaragoza, Spain, announced the acquisition of Thimm Group, a corrugated packaging and display solutions provider with approximately EUR 539 million (USD 582 million) in 2024 revenues and around 2,500 employees. The transaction, subject to antitrust clearance, expands Saica's presence into Central European converting markets where the two companies had operated a strategic alliance and a Polish joint venture since the late 1990s.

- May 2026: Smurfit Westrock plc announced its intention to delist from the London Stock Exchange, consolidating its listing on the New York Stock Exchange. The board resolution followed a review of trading volumes and the regulatory and administrative costs of dual listing, with the last day of LSE trading expected on June 19, 2026.

- March 2026: The European Commission cleared Apollo Funds' acquisition of Lecta, a Spain-headquartered specialty paper manufacturer, under the simplified merger procedure (Case M.12333, March 11, 2026) without conditions. Apollo, which also sponsors Reno de Medici, now holds significant positions across both recycled cartonboard and specialty paper assets in Europe.

- March 2026: Graphic Packaging International announced the partial operationalization of its first European virtual power purchase agreement with Zelestra, covering three solar plants in Spain with a combined capacity of approximately 100 MW. The fully operational plants, José Cabrera (Guadalajara, 50.4 MW) and Socovos II (Albacete, 33 MW), came online in 2025, with Villamañán (León, 19 MW) operational in February 2026, and are designed to reduce the company’s EMEA Scope 1 and 2 GHG emissions by over 50%.

Spain Cartonboard Market Report Scope

The Spain Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include solid bleached board, solid unbleached board, folding boxboard, white-lined chipboard, liquid packaging board, and food service board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The Spain Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and Other Packaging Formats), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics and Toiletries, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

Key Questions Answered in the Report

What is the size of the Spain cartonboard market in 2026 and what is the 2031 outlook?

The Spain cartonboard market stands at USD 734.31 million in 2026 and is forecast to reach USD 875.06 million by 2031 at a CAGR of 3.57%.

Which product grade leads demand in Spain?

Folding Boxboard leads with a 33.14% share in 2025 because it is used widely in printed secondary packs across food, pharmaceuticals, and personal care.

Which packaging format is most widely used?

Folding Cartons dominate with a 56.36% share in 2025 due to strong fit with automated packing lines, branding needs, and shelf presentation.

Which end-user group is growing the fastest?

Pharmaceutical and Healthcare is the fastest-growing end-user, with a projected CAGR of 4.51% through 2031, supported by Spains regulated manufacturing base and tighter identification requirements.

Why is food still the main demand anchor?

Food holds 39.43% of 2025 demand because Spain has a large domestic and export-oriented food production base that needs reliable printed secondary packaging across many categories.

What are the main risks for cartonboard suppliers and converters in Spain?

The main risks are energy and recycled-board cost volatility, plus slower substitution in applications where cartonboard still trails plastics on barrier performance.

Page last updated on: