Italy AI-powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

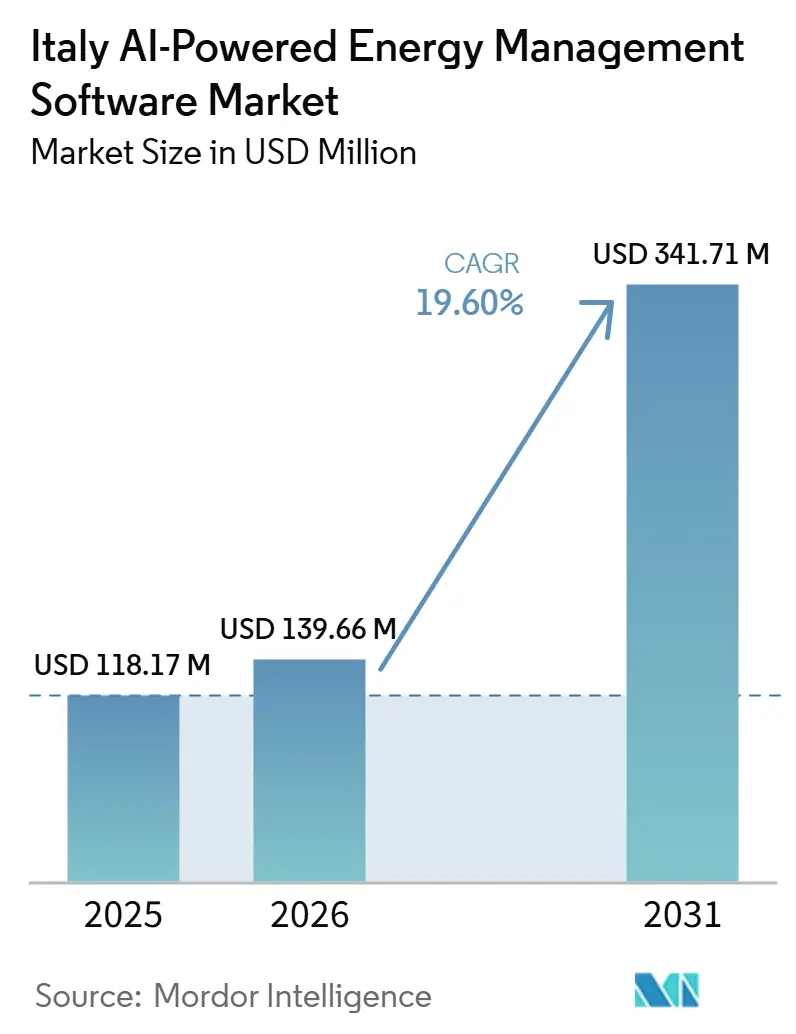

| Base Year Market Size (2025) | USD 118.17 Million |

| Market Size (2026) | USD 139.66 Million |

| Market Size (2031) | USD 341.71 Million |

| Growth Rate (2026 - 2031) | 19.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy AI-powered Energy Management Software Market Analysis by Mordor Intelligence

The Italy AI-powered Energy Management Software Market size is expected to increase from USD 118.17 million in 2025 to USD 139.66 million in 2026 and reach USD 341.71 million by 2031, growing at a CAGR of 19.60% over 2026-2031. The Italian AI-powered energy management software market is being shaped by high electricity costs, which keep energy savings at the center of software buying decisions. Regulatory deadlines are also pushing adoption, especially where energy audits, building automation, and measurable efficiency gains are now tied to compliance and incentives. Grid modernization and renewable integration are expanding use cases beyond buildings into utility operations, forecasting, balancing, and flexibility services. The competitive field remains broad, with global automation vendors, Italian energy operators, and AI-focused specialists all active in the same space. This leaves the Italian AI-powered energy management software market with its strongest near-term room for expansion in industrial facilities, utilities, and public-funded retrofit programs in Southern regions.

Key Report Takeaways

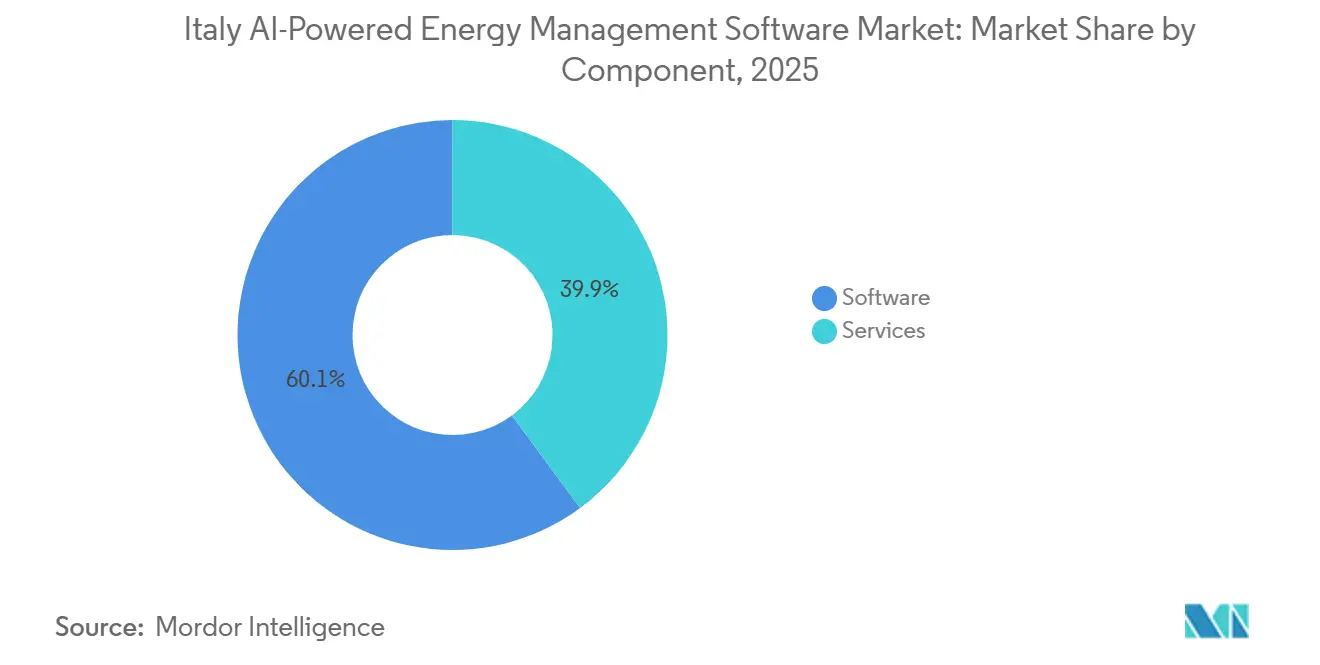

- By component, software led with a 60.13% share in 2025, while services are projected to expand at a 20.12% CAGR through 2031.

- By deployment mode, cloud-based deployment held a 66.21% share in 2025, while hybrid deployment is projected to grow at a 19.92% CAGR through 2031 in the Italy AI-powered Energy Management Software Market.

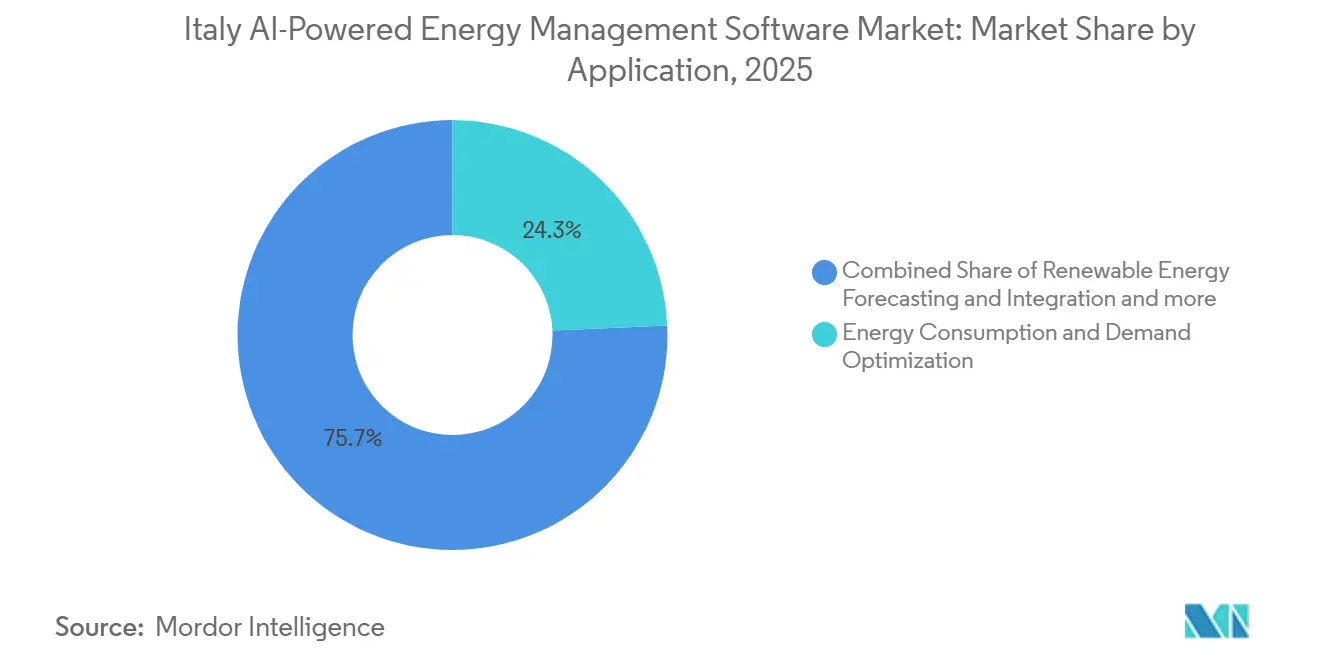

- By application, energy control and management accounted for a 24.30% share in 2025, while renewable energy management is projected to expand at a 21.34% CAGR through 2031.

- By end user, commercial buildings held a 36.62% share in 2025, while the same segment is projected to grow at a 19.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy AI-powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Energy Efficiency Regulations And Compliance Mandates | +4.2% | National, with early gains in Lombardy, Lazio, and Emilia-Romagna | Short term (≤ 2 years) |

| Rising Utility Costs And Energy Price Volatility | +3.8% | National, concentrated in Northern and Central industrial belts | Short term (≤ 2 years) |

| Growth Of AI And IoT Integration In Energy Infrastructure | +3.0% | National, with data center clusters in Milan metropolitan area | Medium term (2-4 years) |

| Expansion Of Renewable Energy And Smart Grid Investment | +2.5% | National, with high-voltage grid corridors and Southern Italy solar belt | Medium term (2-4 years) |

| Retrofit And Building Automation Upgrades Across Commercial And Industrial Sectors | +1.8% | National, with PNRR-funded momentum in Southern regions | Medium term (2-4 years) |

| Rising Need For Carbon Neutrality And Decarbonization Commitments | +1.3% | National, with industrial districts in Veneto, Piemonte, and Toscana | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Energy Efficiency Regulations And Compliance Mandates Drive AI Software Adoption

The Italy AI-powered Energy Management Software Market is receiving direct regulatory support, as compliance now depends on measurable energy performance and more consistent monitoring systems. The recast EPBD entered into force in 2024 and had to be transposed by EU member states, including Italy, by May 29, 2026, which increased the need for building automation and control systems in large non-residential assets. Italy's Legislative Decree 102/2014 also kept large enterprises on a recurring audit cycle, which raised the priority of structured energy data management and digital tracking within corporate operations. The Transition 5.0 Plan added a financial push because tax credits are linked to measurable reductions in energy consumption, which favors software that can record, analyze, and document those results. This made the Italian AI-powered energy management software market less dependent on voluntary sustainability spending and more closely tied to formal operational compliance.

Rising Utility Costs And Energy Price Volatility Accelerate Return Cases

The Italian AI-powered energy management software market is also being boosted by the direct cost pressures Italian businesses faced in 2025. Industrial electricity prices reached EUR 278/MWh (USD 302.9/MWh) in the first half of 2025, the highest level in the EU and a burden on competitiveness, according to Confindustria.[1]Confindustria, “Energy, the Gap That Weighs on Competitiveness in Italy, the Highest Bills in Europe,” Confindustria, confindustria.it At the same time, services sector electricity consumption rose 2.9% year over year in 2025, indicating that digitally managed commercial demand remained active even as energy bills remained elevated. In that setting, software that improves forecasting, load shifting, and real-time control became easier to justify because savings were more visible and payback periods shortened. This cost backdrop keeps the Italian AI-powered energy management software market anchored in practical operating economics rather than optional digital experimentation.

Growth Of AI And IoT Integration In Energy Infrastructure Creates Platform Demand

The Italy AI-powered Energy Management Software Market is entering a broader infrastructure phase as more grid assets, meters, sensors, and digital nodes generate usable operational data. Italy recorded strong private AI investment of nearly USD 860 million in 2024, which supported enterprise AI capability-building and a broader software deployment base in energy-related settings. ENEA launched the GEMINI project in November 2025 to develop AI-based predictive fault detection, advanced monitoring, and quantum-safe cybersecurity for medium-voltage grid nodes, which adds a public research layer to commercial software development.[2]ENEA, “GEMINI, Gestione Evoluta e Monitoraggio Intelligente dei Nodi di Rete con Intelligenza Artificiale,” ENEA, enea.it Terna also signed a strategic agreement with Microsoft to advance digitalization, innovation, and security across the national grid, thereby expanding the data environment available for analytics and asset performance tools.[3]Terna S.p.A., “Grid Development Plan 2025-2034,” Terna S.p.A., terna.it As a result, the Italian AI-powered energy management software market is shifting from isolated building tools toward connected platforms that can work across grid, facility, and distributed asset environments.

Expansion Of Renewable Energy And Smart Grid Investment Opens New Application Demand

The Italy AI-powered Energy Management Software Market is gaining greater utility and flexibility, as renewable integration now requires more forecasting and balancing than older control systems can provide. Terna's development plan sets out more than EUR 23 billion (USD 25.1 billion) of investment across 2025-2034 to integrate more than 65 GW of additional renewable capacity, alongside EUR 2.4 billion (USD 2.75 billion) dedicated to digital transformation. Acea's RomeFlex project was managing nearly 1,500 users and more than 37 MW of local flexibility by February 2026, which shows that AI-managed demand response had already moved beyond pilot scale in Italy. Siemens also began supporting AcegasApsAmga's deployment of Gridscale X in Trieste in June 2025, which linked digital twin development to congestion forecasting and grid modernization.[4]Siemens AG, “AcegasApsAmga Leverages Siemens' Gridscale X to Build Digital Twin of Trieste's Energy Grid,” Siemens AG, siemens.com This widened the addressable scope of the Italy AI-powered Energy Management Software Market from energy monitoring alone to renewable dispatch, local flexibility, and smart grid orchestration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity With Legacy Energy Systems | -2.3% | National, concentrated in older industrial sites in Veneto, Lombardy, and the South | Short term (≤ 2 years) |

| Cybersecurity And Data Privacy Risks In Connected Energy Infrastructure | -1.8% | National, across critical infrastructure nodes and DSO networks | Medium term (2-4 years) |

| Limited Access To Quality Data And AI Expertise | -1.1% | Southern Italy and SME-heavy districts in Central Italy | Medium term (2-4 years) |

| Unclear Return On Investment And Extended Payback Periods | -0.7% | National, most pronounced in residential and small commercial segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity With Legacy Energy Systems Delays Enterprise Deployments

The Italy AI-powered Energy Management Software Market still faces a significant slowdown in brownfield environments, as many industrial and utility sites run on older control architectures. Research from the Politecnico di Torino found that moving from traditional BACnet systems to BACnet Secure Connect introduced significant architectural and security complexity into building energy management environments. That problem is especially important for multi-site operators because legacy protocol support varies across software platforms, limiting vendor standardization across portfolios. This keeps the Italian AI-powered energy management software market slower in industrial rollouts than in commercial buildings, where digital systems are easier to connect and upgrade.

Cybersecurity And Data Privacy Risks In Connected Energy Infrastructure Constrain Adoption

The Italy AI-powered Energy Management Software Market is also constrained by the fact that connected energy systems create a larger attack surface inside critical infrastructure. CLUSIT reported a rise in cyberattacks targeting Italian energy and utility operators through Q1 2025, underscoring the growing risk posed by cloud-connected monitoring and control environments.[5]CLUSIT, “Rapporto Clusit Energy and Utilities 2025,” CLUSIT, clusit.it Terna Forward then invested EUR 4 million in Gyala S.r.l. in March 2026, which showed that grid-linked operators were treating cybersecurity as a strategic software priority rather than a narrow network issue. As more assets become connected, buyers are placing greater weight on governance, access control, anomaly detection, and auditability during procurement. This raises the threshold for new entrants and favors vendors in the Italian AI-powered energy management software market that can show stronger security design and compliance readiness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Holds The Revenue Base While Services Benefit From Integration Work

Software accounted for 60.13% of the Italy AI-powered Energy Management Software Market share in 2025, making it the leading component by revenue. This lead reflects a clear buying pattern in the Italian AI-powered energy management software market, where enterprises prefer licensed analytics, monitoring, and optimization platforms that can be deployed faster than full hardware overhauls. High electricity costs and tighter compliance timelines also favor software, as operators can begin measuring savings and reporting outcomes without waiting for major physical retrofits. That kept software at the center of commercial building and utility spending through 2025.

Services are projected to expand at a 20.12% CAGR through 2031, making them the fastest-growing component of the Italy AI-powered Energy Management Software Market. Growth in services is closely linked to the complexity of retrofitting brownfield industrial sites, utility assets, and mixed OT environments that cannot be connected with a simple software installation. System configuration, protocol mapping, cybersecurity hardening, and managed analytics support remain important where legacy infrastructure is still common. Over time, some of this work will move back into the product layer, but service demand should remain strong while large-scale Italian deployments continue to cross old and new system boundaries.

By Deployment Mode: Cloud Leads Early While Hybrid Gains Ground In Regulated Operations

Cloud-based deployment commanded a 66.21% share of the Italy AI-powered Energy Management Software Market in 2025, making it the dominant delivery model. The main reason was speed: commercial building managers and energy retailers could adopt cloud software without bearing the full burden of new on-site infrastructure. Italy's broader digital policy also reinforced that direction through cloud-first principles tied to national digital transformation programs. In the Italian AI-powered energy management software industry, this gave cloud vendors an early edge in settings where operational data was easier to centralize and manage.

Hybrid deployment is projected to grow at a 19.92% CAGR through 2031, which shows that the next wave of demand is moving into more regulated and technically complex environments. Utilities and industrial operators often need local processing for latency, data residency, and OT continuity, while still wanting cloud analytics and remote reporting. Gridspertise's ERALIS Suite reflected this direction in 2026 through a modular design that combined edge, on-premises, and cloud functions for grid digitalization. That makes hybrid capability an important differentiator in the Italian AI-powered energy management software market, especially where cybersecurity and operational resilience matter as much as analytics performance.

By Application: Energy Consumption and Demand Optimization Leads Today While Renewable Energy Management Expands Fastest

Energy Consumption and Demand Optimization held a 24.30% share in 2025, making it the largest application segment in the Italian AI-powered energy management software market. This position arose from the widespread adoption of load monitoring, demand management, meter analytics, and consumption optimization across commercial and industrial facilities. Because these use cases are already familiar to buyers, they provide a broad and steady revenue foundation for vendors operating in Italy. They also fit well with a market where the first software purchase often starts with visibility and control before expanding into more advanced forecasting.

Renewable Energy Forecasting and Integration is projected to expand at a 21.34% CAGR through 2031, which makes it the fastest-growing application. Terna's renewable integration plans and digital investment pipeline are raising the need for forecasting, balancing, and dispatch support that older grid tools were not built to provide. At the same time, projects such as RomeFlex and the Trieste digital twin are demonstrating that grid analytics, local flexibility, and renewable energy management are increasingly interconnected in real operating environments.[6]Siemens AG, “AcegasApsAmga Leverages Siemens' Gridscale X to Build Digital Twin of Trieste's Energy Grid,” Siemens AG, siemens.com This is why the Italy AI-powered Energy Management Software Market is gradually shifting from standalone monitoring applications toward multi-layer optimization across buildings, grids, and distributed energy assets.

By End User: Commercial Buildings Combine Scale, Compliance Pressure, And Growth

Commercial buildings accounted for a 36.62% share of the Italian AI-powered energy management software market in 2025 and are projected to expand at a 19.87% CAGR through 2031. That dual position came from a large installed base of offices, retail properties, and hospitality sites that faced both rising energy costs and tighter building performance expectations. The EPBD timetable and Transition 5.0 incentives made this user group especially responsive, as savings, compliance, and digital reporting could all be addressed through a single platform layer. The first large-scale Italian retail deployment of AI-EcO at a Brikò location in Vercelli, with energy savings above 10% and tax credit eligibility of up to 45%, demonstrated why this category continues to attract strong attention.[7]Eurast, “Smart Building AI-EcO, Per la Prima Volta in Italia in un Brikò,” Eurast, eurast.it

Utilities remained the second-largest end-user segment and accounted for some of the highest contract values, as grid software supports critical operations at scale. Industrial facilities still represent a major opportunity for the Italy AI-powered Energy Management Software Market, but conversion is slower due to more complex site integration and longer procurement cycles. Residential demand remained the smallest and slowest-moving part of the field because ownership is fragmented, and the willingness to pay for subscription software is weaker. Even so, renovation funding for more than 100,000 buildings and 36 million square meters is building the digital base that could support wider household and multi-dwelling software use later in the forecast period.

Geography Analysis

Northern Italy accounted for the largest concentration of deployments in the Italy AI-powered Energy Management Software Market in 2025. Lombardy, Piedmont, Veneto, and Emilia-Romagna combine energy-intensive manufacturing, large commercial real estate portfolios, and a strong share of the country's data infrastructure. Lombardy alone hosted nearly 37% of national data center capacity, which kept the Milan area important for real-time energy optimization and high-load management software. Terna also reported 0.1% electricity demand growth in Northern Italy in 2025, which suggests that electrification and digital operations continued to support consumption even as efficiency tools improved performance.

Central Italy represented the second-largest geography in the Italy AI-powered Energy Management Software Market, supported by utilities in Rome and public administration buildings, as well as retrofitted commercial assets. Terna reported a 0.4% decline in electricity demand in Central Italy in 2025, which aligned with stronger efficiency performance in public and commercial buildings. RomeFlex showed that local flexibility in the capital region was scaling quickly, with nearly 1,500 users and more than 37 MW under management by February 2026. VINCI Energies also demonstrated how multi-tenant office digitization could support ESG reporting, automation, and building performance control across complex portfolios that fit the Central Italian demand profile.

Southern Italy and the Islands are developing as the fastest-rising geography in the Italy AI-powered Energy Management Software Market. This shift is being driven less by existing industrial density and more by public capital allocation toward renovation, grid modernization, and renewable energy communities. The PNRR directed 80% of its energy renovation project budget to Southern regions, which created a strong base for digitally managed retrofits and automation-led efficiency gains. Terna reported a 0.7% decline in electricity demand across the South and Islands in 2025, which indicates that demand-side efficiency effects were already visible before much of the retrofit pipeline reached maturity. The SMARTER ISLAND project in Calabria added a practical example of this transition by embedding AI-based energy monitoring and control into renewable energy communities from 2026 onward.

Competitive Landscape

The Italian AI-powered energy management software market remained moderately fragmented in 2026. No single company held a dominant position across the component, deployment, application, and end-user categories simultaneously. Global automation players such as Schneider Electric, Siemens, Honeywell, and ABB remained strongest in markets with longer sales cycles and deeper system integration requirements. The Italian AI-powered energy management software market also included Italian energy-linked players such as Enel X S.r.l. and a growing set of AI-focused specialists that competed more aggressively in commercial buildings, grid flexibility, and cloud-led optimization.

Competition is tightening as vendors try to cover more of the workflow rather than sell only one point solution. In June 2026, EnergyCAP launched Watts Chat, which enabled access to generative AI on audited utility data and reduced the need for manual analyst support in large energy portfolios. In March 2026, GridBeyond closed a EUR 12 million funding round and paired it with a strategic collaboration with Samsung to expand AI-driven optimization and battery storage management capabilities. In April 2026, Johnson Controls acquired Nantum AI, demonstrating that building systems incumbents were still buying AI capabilities to improve their competitive position rather than relying solely on internal development.

The main white space remains in renewable energy communities, DSO predictive maintenance, and software that can connect national grid-level data with local network operations. Terna Forward's March 2026 investment in Gyala S.r.l. showed that cybersecurity and operational analytics are increasingly intertwined in utility software procurement. Uplight's May 2026 work with The Brattle Group also highlighted how integrated demand-side platforms can unlock more flexible capacity, which supports the strategic case for broader software stacks rather than isolated tools. This means the Italian AI-powered energy management software market is likely to see more partnerships, selective acquisitions, and platform bundling through 2031. Vendors that can combine optimization, reporting, cybersecurity readiness, and integration capabilities will be better positioned than those offering only narrow analytics.

Italy AI-powered Energy Management Software Industry Leaders

Schneider Electric SE

Siemens AG

Honeywell International Inc.

IBM Corporation

Johnson Controls International plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Creta Energie Speciali received approval for the SMARTER ISLAND project under Interreg NEXT MED, implementing AI-based energy monitoring and control across renewable energy communities in Calabria, Southern Italy, as part of Mediterranean decarbonization and digitalization initiatives.

- May 2026: Uplight and The Brattle Group published findings showing that an integrated demand-side resource stack could increase flexible capacity by 60% by 2030, growing from 146 MW to 235 MW for a representative utility, through combined demand response, energy efficiency, and time-of-use rate programs.

- April 2026: Johnson Controls acquired Nantum AI to integrate AI-driven HVAC optimization algorithms into its broader building management platform, strengthening its competitive position against cloud-native AI building energy management vendors in enterprise commercial accounts.

- March 2026: GridBeyond closed a EUR 12 million (USD 13.1 million) equity round led by Samsung Ventures alongside existing shareholders including ABB, Mirova, and Energy Impact Partners, with funds earmarked to expand AI-driven energy optimization and battery storage management across key strategic markets. The investment was accompanied by a strategic collaboration agreement with Samsung to jointly develop trading, asset optimization, and energy services capabilities.

Italy AI-powered Energy Management Software Market Report Scope

The Italy AI-powered Energy Management Software Market is Segmented by Component (Software and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Control, Asset Performance, Smart Grid Analytics, Renewable Energy Management, and Energy Trading), and End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings |

Key Questions Answered in the Report

What is the Italy AI-powered Energy Management Software Market size in 2026?

The Italy AI-powered Energy Management Software Market stood at USD 139.66 million in 2026 and is forecast to reach USD 341.71 million by 2031 at a 19.60% CAGR.

Which component leads revenue generation in Italy AI-powered energy management software?

Software led with a 60.13% share in 2025 because buyers favored analytics and optimization platforms that can be deployed faster than major hardware changes.

Which deployment model is expanding fastest in Italy?

Hybrid deployment is projected to grow at a 19.92% CAGR through 2031 as utilities and industrial users balance cloud analytics with local data control.

Which application is growing fastest across Italian deployments?

Renewable energy management is the fastest-growing application, with a 21.34% CAGR through 2031, supported by grid investment and renewable integration needs.

Why do commercial buildings hold the largest end-user position?

Commercial buildings held 36.62% share in 2025 and are also the fastest-growing end-user segment because compliance deadlines and energy costs are both pushing adoption.

Page last updated on: